Sample Category Title

Euro Shakes Off Political Risk, Brent Near $80

The Euro strengthened slightly early Thursday to trade at 1.1837 after hitting a new five-month low of 1.1761 the previous day. It seems that the single currency has a new headache to deal with; this time, it’s Italy. A leaked draft of the coalition agreement betweenpopulist parties 5-Star Movement and the League revealed plans to defy E.U. rules and demand thecancelation of €250 billion of Italian bonds bought by the European Central Bank. However, leaders of the two parties said that debt cancellation was not in any official draft of a government program.

Although Italian stocks plunged and bond yields shot up by more than 15 basis points, the reaction was still relatively insignificant compared to the news itself. Italy's economy is around ten times the size of Greece’s; if investors took these plans seriously, we would have seen a sharp, broad selloff in European equities, and that has not been the case. Coalition talks tend to be toned down eventually, soinvestors shouldn’t be overtaken by political speech. It will be better to focus on the fundamentals, as there’s always going to be political noise in the background.

Brent testing a critical physiological level

Despite the rising U.S. yields and U.S. dollar, Brent crude continued its rally towards the $80 benchmark. The fall in U.S. inventories also added fuel to the rally, but whether prices are sustainable at current levels remains in significant doubt.

OPEC members themselves are not convinced ofthe move and see oil's rally towards current levels as a short-term spike driven by geopolitics. Higher oil prices along with a strong dollar area double whammy for emerging markets, that will feel the pain sooner rather than later. Further tightening in credit conditions will start pressuring emerging market economies and may eventually result in lower demand. I think OPEC members should be more flexible when they meet inJune, or they will contribute to the factors slowing the global economy.

China – U.S. trade talks

A new round of China-U.S. trade talks will be launched today in continued efforts to avert a trade war. Interestingly though, Peter Navarro won’t be the U.S. key negotiator;instead, Steven Mnuchin, Wilbur Ross, and Robert Lighthizer will take the lead. President Trump seems to have changed course with China, first inhis attempt to save ZTE, and now by sidelining Peter Navarro. It's still difficult to predict how the negotiations will end, but we’ll surely be in a better position compared toa few months ago.

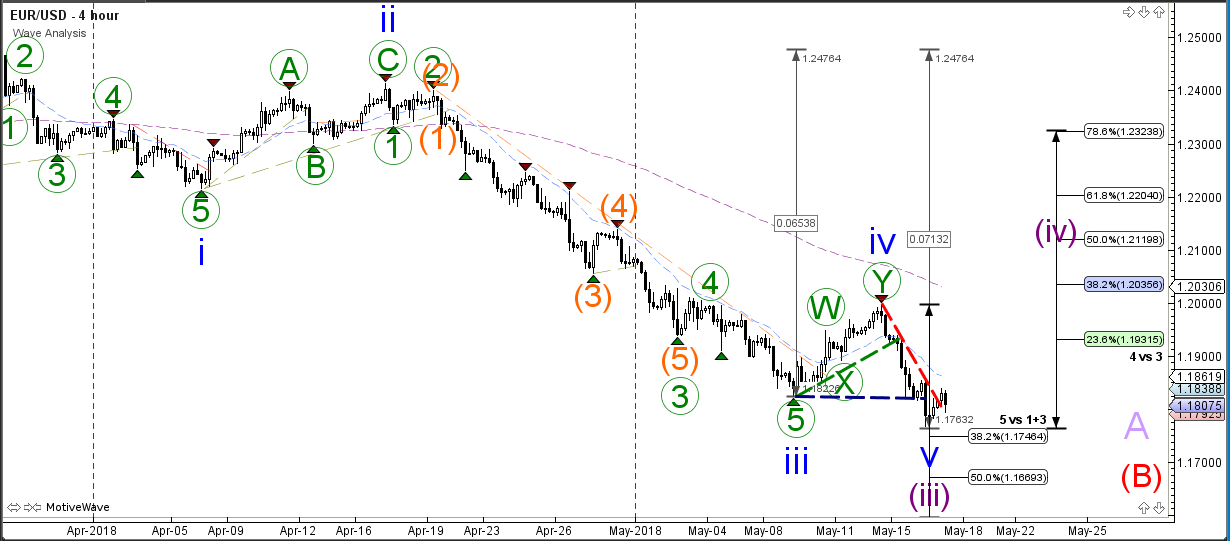

EUR/USD Reaches Bearish Wave 3 Target At 1.1750

The EUR/USD broke below the previous bottom (dotted blue line) and made a new lower low. The bearish breakout managed to reach the quarter level of 1.1750, which could be the main target for the wave 3 (purple). Price can sometimes extend further and hence it is possible that price could reach the next Fibonacci target as well but a break below 1.1750 support is needed. Otherwise it seems more likely that a wave 4 (purple) correction will take place

The EUR/USD seems to have completed a bearish wave 5 (green) and price could be building a bullish correction within wave 4 (purple) of the 4 hour chart. A bullish break above the resistance trend line (red) could indicate that larger retracement whereas a break below 1.1750 could see an extension of the bearish trend, although slower and more corrective.

Currencies: Euro Suffers From Uncertainty On Italy. More To Come?

Rates: US 10-yr yield breaks above 3.07%. Italian politics weighs on periphery

Italian political risk could keep peripheral bond markets under pressure at least until 5SM/Lega reach a coalition agreement and publish their official plans. The US Note future will probably underperform the Bund, especially if US eco data, even second tier, remain strong. The break above 3.07% (US 10-yr), if sustained, argues further in favour of Treasury selling.

Currencies: Euro suffers from uncertainty on Italy. More to come?

The focus for EUR/USD trading turned from the USD to the euro side of the story yesterday. EUR/USD dropped (temporary?) below 1.18 on headlines that the new Italian government program would contain some controversial measures on E(M)U politics. Sterling profits from press headlines that the UK government is considering to stay longer in the EU customs union

The Sunrise Headlines

- US stock markets ended 0.25% (Dow) to 0.63% (Nasdaq) higher yesterday. Asian risk equity indices are mixed overnight with Japan outperforming (+0.5%) and China underperforming (-0.3%).

- Britain will tell Brussels it is prepared to stay in the customs union beyond 2021 as ministers remain deadlocked over a future deal with the EU. (Telegraph)

- Brazil's central bank kept its policy rate unexpectedly unchanged at 6.5% following a strong of a dozen consecutive cuts. Policymakers cited the recent sell-off in emerging markets assets for the move. (FT)

- French energy giant Total joined other European companies in signalling they could exit Iran, casting doubt on whether European leaders meeting to try to salvage the Iran nuclear deal can safeguard trade with Tehran. (Reuters)

- A GOP-led Senate committee backed US intelligence agencies' finding that Moscow tried to boost Trump's campaign by hacking and spreading misinformation, a bipartisan conclusion that breaks with a House panel's position and the president's rejection that Russia wanted him to win. (WSJ)

- Australia's jobless rate rose to a nine-month high of 5.6% in April as more people looked for work, but the number of employed beat expectations as more full-time jobs were added (+32.7k). (Reuters)

- Today's eco calendar contains US weekly jobless claims and Philly Fed Business Outlook. Fed Kashkari, Fed Kaplan and ECB Constancio are scheduled to speak. Spain and France sell bonds

Currencies: Euro Suffers From Uncertainty On Italy. More To Come?

Italian politics weighs- on euro. More to come?

Earlier this week, EUR/USD resumed its downtrend. The move was mainly the result of USD strength and rising US yields. US yields rose further yesterday, but the focus for FX trading turned more to the euro. EUR/USD selling resumed on headlines that an Italian 5SM/Lega government would ask a write-down on debt held by the ECB. The parties who are negotiating a government program downplayed the issue, but couldn't restore confidence. Italian assets were sold. EUR/USD tumbled (temporary?) below 1.18, but closed at 1.1808. US eco data (production) remained good, but harly affected USD trading. USD/JPY ran into resistance, settling in the lower half of the 110 big figure.

Overnight, Asian equities hardly profit from a good close in the US. Japan outperforms. The US 10-yr yield reached 3.1%, but for now it doesn't trigger further USD gains. The trade-weighted USD (93.20) hovers just below the recent top as does USD/JPY (110.3). EUR/USD is changing hands near 1.1820. Australian April job growth was OK, but the 5.6% unemployment rate indicates that there is still spare capacity. AUD/USD (currently 0.7535) gained modest ground after the release.

Investors will keep a close eye on the negotiations to form a new Italian government today. Any controversial proposals to amend EU/EMU rules might weigh on the euro. In the US, the jobless claims and the Philly Fed business outlook will be released. US data recently confirmed a good momentum at the start of Q2 and we see no reason for this to change right now. However, will upcoming data be strong enough to support a further rise in the dollar after recent gains? The MT picture remains USD constructive, but yesterday's price action suggests that the dollar rally might be losing some momentum in a daily perspective. Some consolidation might be on the cards, especially for USD/JPY. Uncertainty on Italy might cap the topside in EUR/USD. EUR/USD 1.1718 remains the next reference.

Sterling held stable against the dollar and gained slightly against a soft euro yesterday. Overnight, sterling profits from a press article that the UK would be prepared to stay longer in the customs union (beyond 2021) if that would be necessary to implement a final solution. There are no important UK eco data. The hope on some kind of Brexit compromise might continue to support sterling in a daily perspective. EUR/GBP might drift lower in the 0.8850/0.8650 trading range.

EUR/USD touched new 2018 low on Italian political developments, but no follow-through price action yet

GBP Strengthens On Report UK Will Stay In Customs Union Beyond 2021

General Trend:

- Asian equities trade mixed

- Hang Seng pares 1% gain amid post earnings trade in Tencent and various ex-dividends

- USD trades generally weaker in Asia

- The pound (GBP) outperforms: Reportedly, the UK plans to tell EU it is prepared to stay in a customs union beyond 2021, says the London Telegraph

- Australia April unemployment rate hits 9-month high, as participation rate rises; Employment increase continued recent slowing of jobs growth (Australia Stats Agency)

- New Zealand sees higher budget surpluses in budget statement; raised bond issuance plans for FY18/19, FY19/20 and FY20/21; Kiwi gains, bond yields move higher

- US and China trade talks in focus

- Japan government downplays press report regarding possible retaliatory trade measures vs. US

- China said to set standards on implicit debt definition amid recent questions about implicit guarantees for local government debt

- Australia 3-month bank bill rate rises for the first time since mid-April

- Fitch: In China, the shift in credit cycle is coinciding with a peak in corporates’ domestic bond refinancing needs

- Singapore exports to China recover in April

- South Korea 3-year bond yields decline after cautious comments from BoK Chief

- South Korea plans to sell additional 50-year bonds following issuance in March

- Indonesia Central Bank is expected to raise rates by 25bps at meeting later today (would be first hike since late 2014)

- Japan April CPI data due for release on Friday

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.1%, closed -0.4%

- ASX 200 REIT index -1.1%, Financials -0.6%, Utilities -0.6% ; Resources +0.8%, Energy +0.2%

- (NZ) NEW ZEALAND Q1 PPI INPUT Q/Q: 0.6% V 0.9% PRIOR; PPI OUTPUT Q/Q: 0.2% V 1.0% PRIOR

- (AU) Australia 3-month bank bill fixed 1.9200% v 1.9000% prior (first rise since mid-April)

- (AU) Australia May Consumer Inflation Expectation: 3.7% v 3.6% prior

- (AU) AUSTRALIA APR EMPLOYMENT CHANGE: 22.6K V 20.0KE; UNEMPLOYMENT RATE: 5.6% V 5.5%E

- Treasury Wine Estates,[-8.6%], TWE.AU Said to be facing an over supply issue on some brands in China – AFR; Responds to press: comfortable with operating model in China, have some delays in shipments clearing China

- Kidman Resources [KDR.AU] announced lithium supply agreement with Tesla

- (NZ) NEW ZEALAND RELEASES ANNUAL BUDGET: Total budget for period NZ$11.4B, NZ$2.8B/yr on avg; total new capital investment in budget NZ$3.8B; raises bond issuance

- (NZ) Moody's: New Zealand budget shows commitment to strong public fiscal prudence

China/Hong Kong

- Shanghai Composite opened 0.0%, Hang Seng +1%

- Hang Seng Financials index -1.1%, Property/Construction -0.7%, Materials -0.3%; Info Tech +3.9% (Tencent +4.8%)

- (CN) China can ease credit on private companies to help with debt payments – Chinese Press

- (CN) China said to set standards on implicit debts definition - Chinese press; Reminder: China credit spreads had hit the widest level in about 2 years amid new regulations that raised questions about implicit guarantees on debt linked to local governments.

- (CN) Fitch: Bond refinancing risk is rising for corporates in China, notes tightened credit conditions and gov't efforts to contain leverage

- (CN) China PBoC sets yuan reference rate at 6.3679 v 6.3745 prior

- (CN) China PBoC Open Market Operation (OMO): Injects CNY50B in 7-day and 14-day reverse repos v CNY260B injected with 7-day and 14-day reverse repos prior; Net: CNY30B injection v CNY200B injection prior

- (CN) China Apr Foreign Direct Investment (FDI) YTD y/y: +0.1% v 0.5% prior

- Tencent, [+7%], 700.HK Reports Q1 (CNY) Net 23.3B v 17.4Be; Rev 73.5B v 70.8Be

- (HK) HKMA purchases to defend HK$ peg have reached HK$9.499B

- (CN) China said to plan to end purchase tax breaks for ~320 NEV models – US financial press

- (CN) China President Xi Top Economic Adviser Liu He meets with US lawmakers as part of trip to Washington D.C: Liu He says China and US should view trade issues 'objectivley'. - Xinhua

Japan

- Nikkei 225 opened +0.5%; closed +0.5%

- Topix Iron & Steel index +1.2%, Marine Transportation +0.6%

- Megabanks trade generally higher

- (JP) JAPAN MAR CORE MACHINE ORDERS M/M: -3.9% V -3.0%E; Y/Y: -2.4% V +0.3%E

- (JP) Japan Investors Net Buying of Foreign Bonds: +¥827.0B v -¥363.7B prior week; Foreign Net Buying of Japan Stocks: +¥126.3B v -¥0.3B prior week

- (JP) Japan said to inform WTO about retaliatory steps related to US tariffs - Japanese Media

- (JP) Follow Up: Japan said to be considering retaliatory tariffs against the US totaling $409M; Measures would be the equivalent value to duties imposed by US via its tariffs - NHK

- (JP) Japan MoF sells ¥2.0T v ¥2.0T indicated in 0.10% (prior 0.10%) 5-yr bonds; avg yield -0.1030% v -0.1200% prior; bid to cover 4.22x v 4.40x prior

Korea

- Kospi opened +0.4%

- (KR) South Korea Ministries said to have discussed measures to increase transparency related to FX policy

- (KR) South Korea Fin Min Kim: Employment market continues to be difficult

- (KR) South Korea: Not reviewing changing FX intervention disclosure period; disclosing FX intervention has little impact on market

- (KR) Bank of Korea Gov Kim: Difficult to be optimistic about the economy, sluggish employment is a concern domestically

Other Asia

- (MY) Malaysia Q1 GDP Q/Q: 1.4% v 0.9% prior; Y/Y: 5.4% v 5.6%e

- (MY) Malaysia Finance Ministry: To restore sales tax in near-term, to introduce sales and services tax [Reminder: Earlier this week, it was reported that the new Malaysia government might revise the goods and services tax (GST) from 6% to 0%]

- (MY) Moody's: Malaysia removal of GST is a credit negative if there are no offsets

- (SG) Singapore Apr Non-Oil Domestic Exports M/M: 6.5% v +0.8%e; Y/Y: 11.8% v +7.3%e; Electronic Exports Y/Y: -6.9% v -7.5% prior; Balance of Trade $6.0B v $5.5B prior

- Singapore Telecom, STEL.SG Reports Q4 (S$) underlying net 807M v 820Me; EBITDA 1.24B v 1.2Be; Rev 4.3B v 4.3B y/y

- (SL) Sri Lanka Central Bank: To curb unwarranted depreciation of Rupee currency (LKR)

North America

- US equities markets ended higher: Dow +0.3%, S&P500 +0.4%, Nasdaq +0.6%, Russell 2000 +1%

- S&P 500 Materials +1.2%

- (US) Fed Williams: not concerned about the yield curve yet or inflation; do not expect prices to jump

- (US) Fed’s Bullard (dove, non-voter): Additional rate hikes may depress inflation expectations; Fed action that inverts yield curve is a very negative sign

- (US) Fed's Bostic (voter, dove): Repeats 2-4 rates hikes this year is correct; Personally I am at 3 rate hikes this year due to the additional stimulus

- (US) US Trade Rep Lighthizer said to be not optimistic on an imminent agreement related to NAFTA - US Press

- (US) Trump Lawyer Giuliani said Special Counsel Mueller told Trump’s legal team he would follow DoJ guidance that a president cannot be indicted; Giuliani suggested that the DoJ can only write a report, as they cannot indict. – CNN

- (US) DOE CRUDE: -1.4M V -0.5ME

Europe

- (UK) Reportedly UK plans to tell EU it is prepared to stay in a customs union beyond 2021 – Telegraph

- (UK) UK trade body EEF: Customs plan backed by Johnson has major flaws - FT

- (UK) Former Reserve Bank of India (RBI) Gov Raghuram Rajan said he will not apply for BoE Governor position – FT

- Mothercare [MTC.UK]: With chairman Parker gone, former CEO Newton-Jones expected to be brought back on board as the company announces its results and a CVA that will see it close 50 doors in the next year - UK press

- Telecom Italia [TIT.IT]: Reports Q1 EBITDA €1.8B v €2Be, Rev €4.7B v €4.7Be

Levels as of 02:00ET

- Hang Seng -0.1%; Shanghai Composite -0.2%; Kospi -0.3%

- Equity Futures: S&P500 +0.0%; Nasdaq100 -0.1%, Dax +0.0%; FTSE100 -0.1%

- EUR 1.1805-1.1837 ; JPY 110.08-110.40 ; AUD 0.7509-0.7548 ;NZD 0.6895-0.6937

- Jun Gold -0.0% at $1,291/oz; Jun Crude Oil +0.3% at $71.69/brl; Jul Copper +0.1% at $3.08/lb

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5642; (P) 1.5760; (R1) 1.5831; More....

EUR/AUD's decline extends to as low as 1.5660 so far and intraday bias remains on the downside. Break of channel support indicates acceleration and raises the chance of medium term reversal. Focus will be on 1.5621 key support. On the upside, break of 1.5774 support turned resistance is needed to be first sign of short term bottoming. Otherwise, deeper will still be in favor in case of recovery.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. Current rally from 1.3624 could extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal. On the downside, sustained break of 1.5621 support should confirm reversal and turn outlook bearish for 1.5153 support and below.

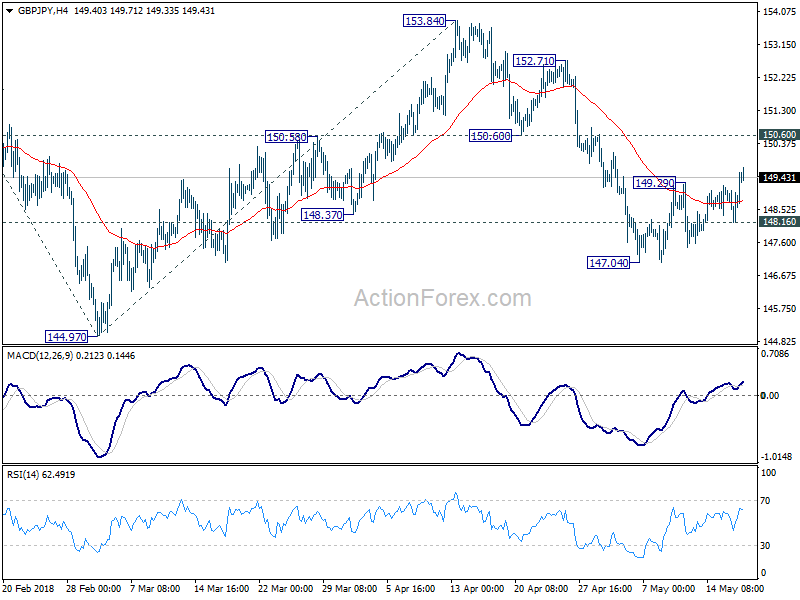

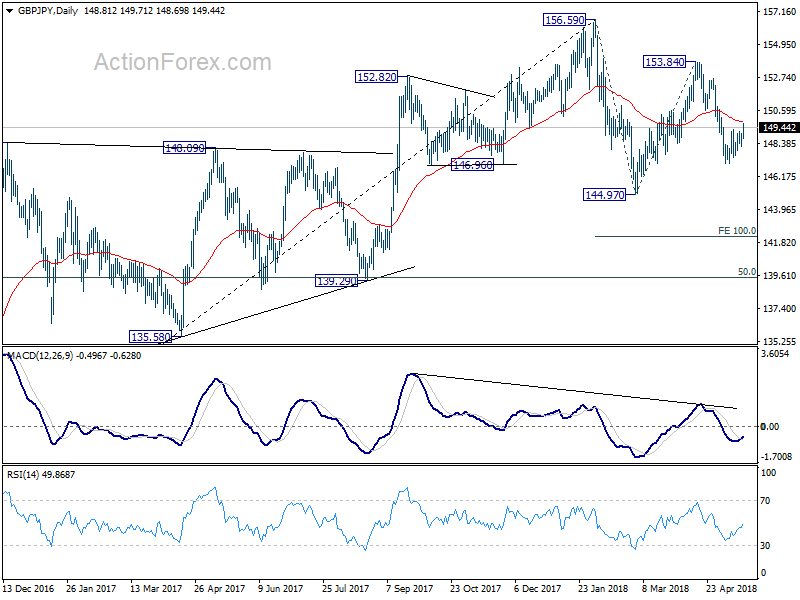

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.34; (P) 148.76; (R1) 149.34; More...

GBP/JPY's recovery from 147.03 resumed by taking out 149.29 minor resistance. Further rise could be seen. But still, such choppy rise is seen as a correction. Hence, upside should be limited below 150.60 support turned resistance to bring fall resumption eventually. On the downside, below 148.16 will likely resume the decline from 153.84 through 147.04 to 144.97 low. Break there will resume the fall from 156.59 and target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next.

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

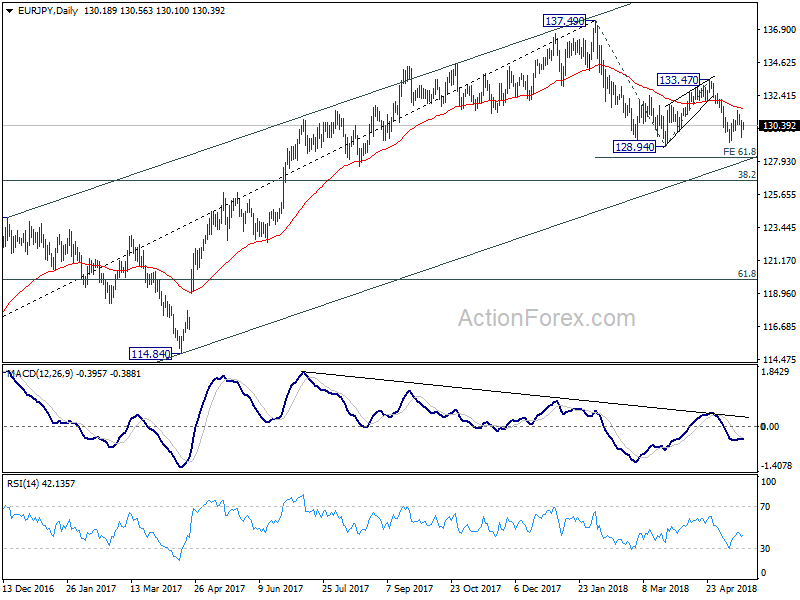

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.33; (P) 130.74; (R1) 131.05; More....

EUR/JPY rebounded strongly ahead of 129.22 support and intraday bias is turned neutral first. Near term outlook stays bearish with 131.36 resistance intact and deeper decline is expected. Below 129.22 will target 128.94 first. Break there will resume the corrective fall from 137.49 and target 61.8% projection of 137.49 to 128.94 from 133.47 at 128.18, and possibly further to 126.61 medium term fibonacci level.

In the bigger picture, for now, price actions from 137.49 are viewed as a corrective pattern only. Hence, while deeper decline would be seen, strong support is expected at 38.2% retracement of 109.03 to 137.49 at 126.61 to contain downside and bring rebound. Up trend from 109.03 (2016 low) is expected to resume afterwards. Though, sustained break of 126.61 will be an important sign of trend reversal and will turn focus to 124.08 resistance turned support.

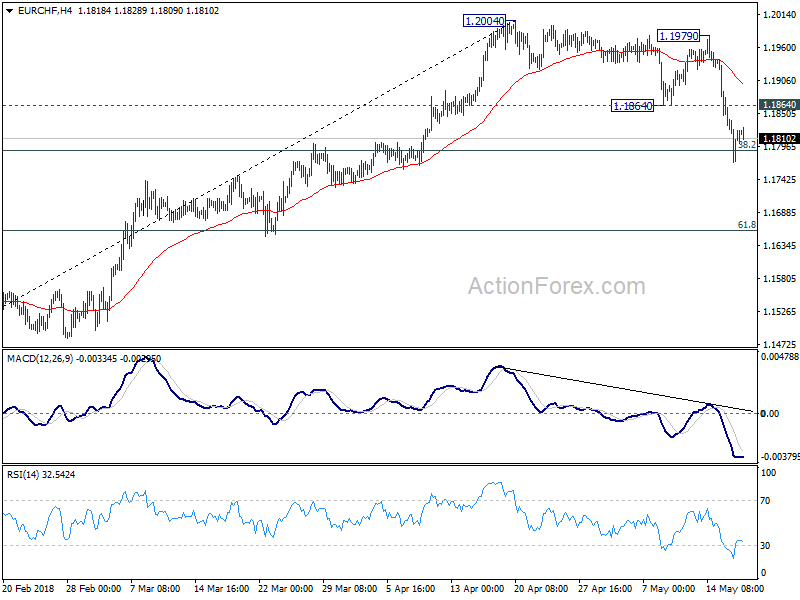

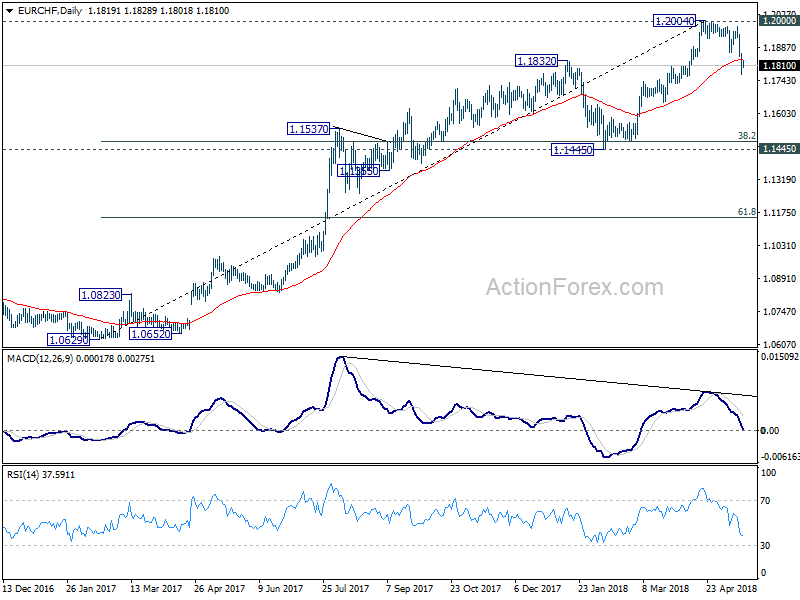

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1775; (P) 1.1818; (R1) 1.1866; More...

EUR/CHF recovers after hitting 38.2% retracement of 1.1445 to 1.2004 at 1.1790. But with 1.1864 support turned resistance intact, deeper fall is expected. Sustained trading below 1.1790 will pave the way to 61.8% retracement at 1.1659 and below. Nonetheless, break of 1.1864 will indicate short term bottoming and turn bias back to the upside for stronger rebound.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 could be a medium term top. And price action from 1.2004 is corrective the up trend from 1.0629. Hence, for now, deeper fall could be seen back to 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern.

Brexit Developments Take Centre Stage On Light Day For Economic Events

At 10:30 GMT, ECB Vice President Victor Constancio is due to deliver his closing remarks as he leaves his position with the Bank. EUR pairs may be influenced by this event if monetary policy is discussed.

At 12:30 GMT, US Continuing Jobless Claims (May 4) is expected to be 1.78M against 1.79M previously. Initial Jobless Claims (May 11) is expected to come in at 215K against 211K previously. This data is showing a continuing increase in the number of new claims, but continuing claims have stabilized somewhat. Philadelphia FED Manufacturing Survey (May) is expected to be 21.0 against 23.2 previously. This data is stable if slightly tilted downward, after reaching highs in early 2017. USD crosses could see an increase in volatility from this data release.

At 14:30 GMT, the Bank of Canada Review will be published, giving an insight into central banking and the Canadian economy. CAD pairs may be affected by this.

At 14:45 GMT, FOMC Member Kaskari is due to speak at a scheduled event. USD crosses could see spikes in volatility during this event.

At 16:00 GMT, UK MPC Member Haldane is due to deliver closing remarks at the Economic Statistics Centre of Excellence Conference on Economic Measurement, in London. GBP crosses may be affected by any comments made.

At 17:30 GMT, FOMC Member Kaplan is due to speak at a scheduled event. USD crosses may see spikes in volatility during this time.

Reports UK Is Prepared To Stay Within EU Customs Union Send GBP Higher

British Media has reported that the UK is to inform the EU that they are willing to stay in the EU Customs Union beyond 2021. The Government agreed on a new “backstop” earlier this week to avoid a hard border on the island of Ireland. This came after rejecting earlier EU proposals ahead of the looming June deadline. This was despite objections from Foreign Secretary Johnson and Environment Secretary Gove. GBP has rallied well and is the strongest currency as we approach the European open, up from 1.34554 to 1.35687 against the USD. EURGBP is down to 0.87206 from yesterday’s high of 0.87823. The USD has weakened somewhat, with EURUSD reaching a high of 1.18373 overnight.

Eurozone Consumer Price Index – Core (YoY) (Apr) came in as expected, unchanged at 0.7%. Consumer Price Index (MoM) (Apr) was also as expected at 0.3%, from 1.0% previously. Consumer Price Index (YoY) (Apr) was also as expected, unchanged at 1.2%. Consumer Price Index – Core (MoM) (Apr) was as expected at 0.2%, from 1.4% prior. CPI data is showing a decrease in the monthly figures, with yearly figures remaining in line with the previous reading. EURUSD fell from 1.18376 to a low of 1.17662 after this data release.

US Housing Starts (MoM) (Apr) were 1.287M against an expected 1.310M, from a previous number of 1.319M, which was revised up to 1.336M. Building Permits (MoM) (Apr) were 1.352M against an expected 1.350M, with the prior reading of 1.354M, which was revised up to 1.377M. This data shows a decrease in activity from previous readings. These data points have been recovering since hitting lows of 0.46M and 0.49M respectively after the financial crisis. GBPUSD halted its decent at 1.34668 when the data was released.

US Industrial Production (MoM) (Apr) was released, coming in at 0.7%. The consensus was for 0.6% from 0.5% previously, which was revised up to 0.7%. This measure rebounded strongly, to reach the highest reading since December 2014 in March, after slipping below the zero line previously. Capacity Utilization (Apr) was also released at this time, with a reading of 78.0% against the expectation of 78.4%, from 78.0% previously, which was revised down to 77.6%. The readings came in line with previous data, with capacity failing to create a new high and missing expectations. USDJPY rose from 110.056 to 110.341 after the release.

EURUSD is up 0.10% overnight, trading around 1.18185.

USDJPY is down -0.10% in early session trading at around 110.284.

GBPUSD is up 0.52% this morning, trading around 1.3560.

Gold is up 0.18% in early morning trading at around $1,292.98.

WTI is up 0.31% this morning, trading around $71.86.