Sample Category Title

Sterling Rebounds as UK May Stay in Customs Union after Brexit, Beyond 2021

US treasury yields rally continues with 10 year yield hitting as high as 3.109 in Asian session. But the lift to Dollar is rather non-existence this time. The greenback is trading generally lower against others today and is mixed for the week. Sterling, on the other hand, is the strongest one today as lifted by news that UK could stay in customs union after Brexit. Canadian Dollar is also firm with WTI crude oil is staying comfortable above 71.5 handle. Euro remains the weakest one for the weak as weighed down by Italian politics. But the common currency is paring some losses against Dollar and Yen.

Technically, Dollar failed to take out near term resistance of 1.3448 against Sterling and 1.0056 against Swiss Franc. It's actually kept quite well off 0.7566 against Aussie and 1.2998 against Canadian. That suggests the greenback's rally was one-sided (or two sided?) against Euro and Yen only. On the other hand, there is prospect of a reversal in GBP/USD. And 1.3607 minor resistance is a level to watch today.

Sterling rebounds as UK could stay in customs union beyond 2021

The Telegraph reported that UK is preparing to stay in the customs union after Brexit, and beyond 2021. The news came after Prime Minister Theresa May said she's aiming for a "future customs union" with the EU. And, her top ministers agreed this week on a last-resort plan to avoid a hard Irish border. Foreign Secretary Boris Johnson and Environment Secretary Michael Gove objected the plan but were "outgunned" by other during the meeting.

Australia jobs added 22.6k, participation rate made another record high

Australia employment market grew 22.6k in April (seasonally adjusted), slightly above expectation of 20.0k. Full time employment grew 32.7k while part time jobs dropped -10k. Unemployment rate rose 0.1% to 5.6%, above expectation of being unchanged at 5.5%. Participation rate rose to a further record high of 65.6%. ABS Chief Economist Bruce Hockman said "the labour force participation rate was the highest it has been since the series began in 1978, indicating increasing attachment to the labour force."

Also from Australia consumer inflation expectation rose to 3.7% in May.

New Zealand PPI input slowed to 0.6% qoq in Q1 but beat expectation of 0.3% qoq. PPI output slowed to 0.2% qoq, in line with consensus.

Japan ready for retaliation against US steel tariffs

The NHK reported that Japan is readying retaliation against US tariffs. And it's completing final arrangements to inform the WTO. It should be noted that Japan is one of the top 10 steel importers to the US who is not even granted a temporary exemption of the steel and aluminum tariffs. Meanwhile, South Korea was given permanent exemptions after updating the trade agreement.

Japan is said to be considering to impose tariffs on US imports that are worth USD 409m, equivalent of duties levied by the US through its tariffs. The list of goods was not publicized.

Release from Japan, machine orders dropped -3.9% mom in March versus expectation of -2.9% mom.

No news on NAFTA as May 17 deadline looms

There is so far no positive news out of NAFTA negotiation yet. House Speaker Paul Ryan said today (Thursday) is the last day the Congress has to receive a notification of a deal, if it is to pass it within this year. But it's believed that the fundamental differences regarding auto contents and sunset clause remain between the US and the other two countries, Mexico and Canada.

BoC Governing Council Member Schembri said yesterday that uncertainty on NAFTA is impacting firms' investment decisions. And, capacity is being "hindered" by firms' reluctance to take on investment in face of uncertainty. And some of which is related to NAFTA.

Looking ahead

The calendar is rather light today. Focus will be on US jobless claims and Philly Fed survey. US will release release leading indicator. Canada will release international securities transactions.

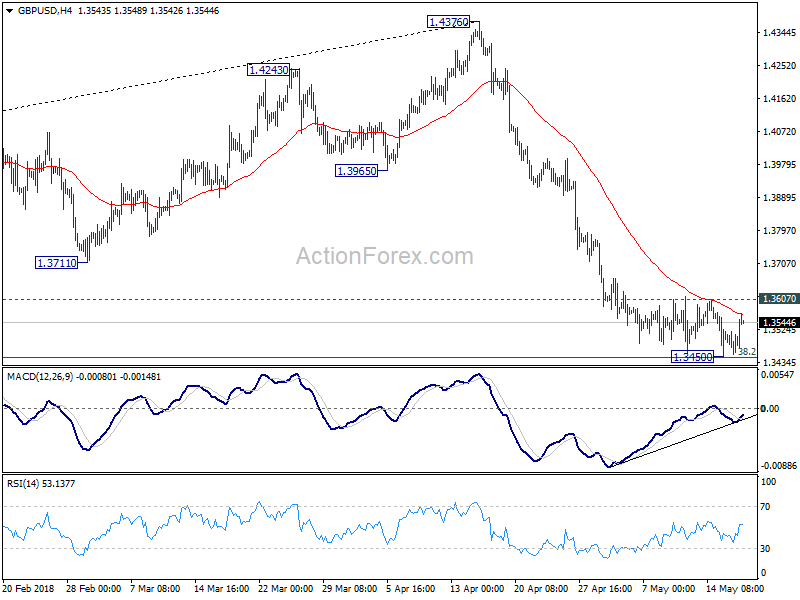

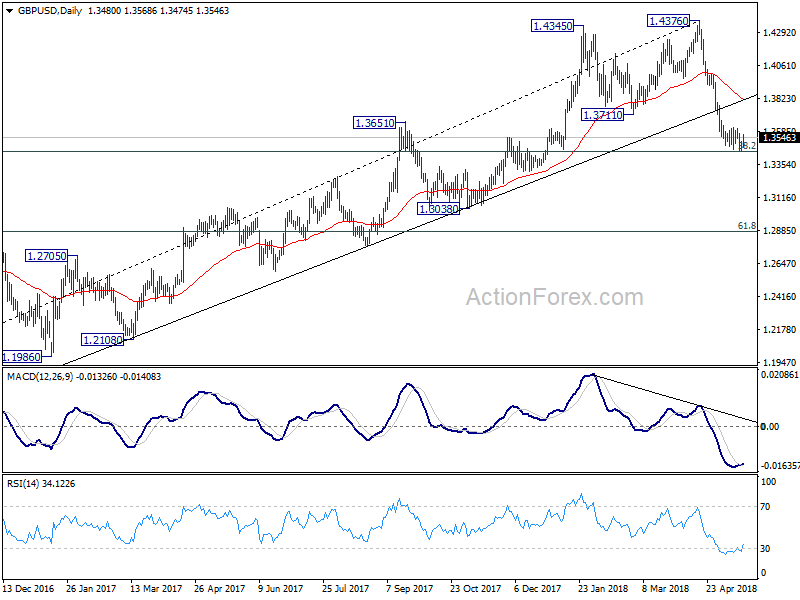

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3451; (P) 1.3495; (R1) 1.3535; More...

GBP/USD's strong recovery, with 4 hour MACD crossed above signal line, suggests temporary bottoming again at 1.3450, ahead of 1.3448 fibonacci level. Intraday bias is turned neutral again as fall from 1.4376 failed to resume. For now, near term outlook will remain bearish as long as 1.3607 minor resistance holds and deeper decline is expected. Firm break of 1.3448 will pave the way to next fibonacci level at 1.2874. However, break of 1.3607 will indicate near term bottoming, with bullish convergence condition in 4 hour MACD. Intraday bias will then be turned back to the upside for 55 day EMA (now at 1.3815).

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 was almost met. Break there will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3815) holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q1 | 0.60% | 0.30% | 0.90% | |

| 22:45 | NZD | PPI Output Q/Q Q1 | 0.20% | 0.20% | 1.00% | |

| 23:50 | JPY | Machine Orders M/M Mar | -3.90% | -2.80% | 2.10% | |

| 1:00 | AUD | Consumer Inflation Expectation May | 3.70% | 3.60% | ||

| 1:30 | AUD | Employment Change Apr | 22.5k | 20.0k | 4.9k | -0.7k |

| 1:30 | AUD | Unemployment Rate Apr | 5.60% | 5.50% | 5.50% | |

| 12:30 | CAD | International Securities Transactions (CAD) Mar | 3.96B | |||

| 12:30 | USD | Initial Jobless Claims (MAY 12) | 215K | 211K | ||

| 12:30 | USD | Philadelphia Fed Business Outlook May | 21.1 | 23.2 | ||

| 14:00 | USD | Leading Index Apr | 0.40% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 89B |

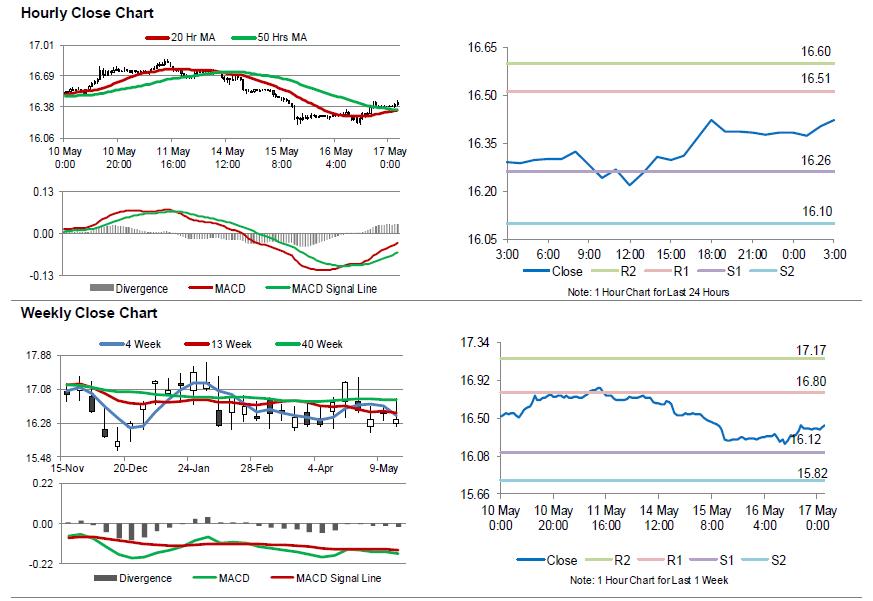

Silver: White Metal Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, Silver rose 0.61% against the USD and closed at USD16.39 per ounce, reversing its previous session losses.

In the Asian session, at GMT0300, the pair is trading at 16.43, with silver trading 0.24% higher against the USD from yesterday’s close.

The pair is expected to find support at 16.26, and a fall through could take it to the next support level of 16.10. The pair is expected to find its first resistance at 16.51, and a rise through could take it to the next resistance level of 16.60.

The white metal is trading above its 20 Hr and 50 Hr moving averages.

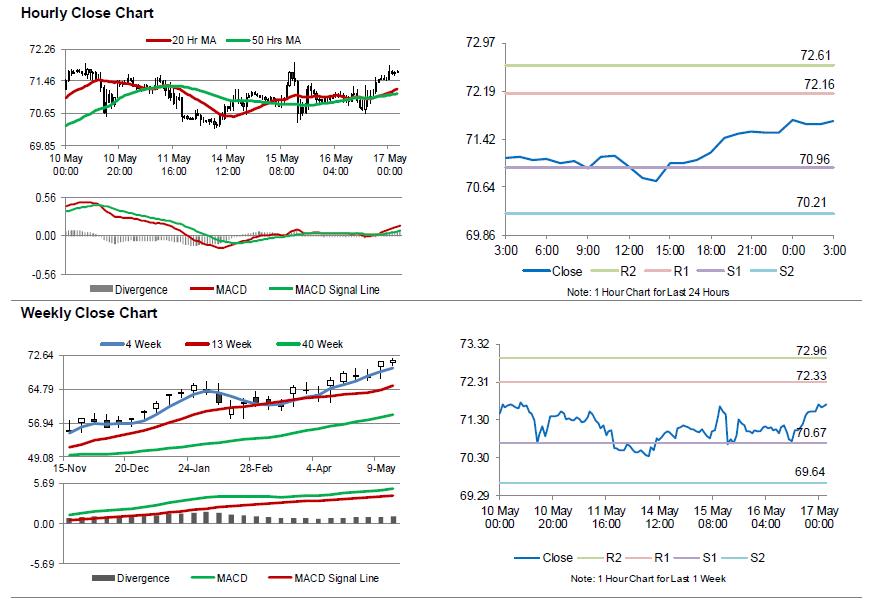

Crude Oil: Oil Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, Crude Oil rose 0.80% against the USD and closed at USD71.52 per barrel, after the Energy Information Administration (EIA) report indicated that US crude oil stockpiles fell 1.4 million barrels to 432.4 million barrels in the week ended 11 May.

In the Asian session, at GMT0300, the pair is trading at 71.71, with oil trading 0.27% higher against the USD from yesterday’s close.

The pair is expected to find support at 70.96, and a fall through could take it to the next support level of 70.21. The pair is expected to find its first resistance at 72.16, and a rise through could take it to the next resistance level of 72.61.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

Sterling rebounds as UK could stay in customs union beyond 2021

The Telegraph reported that UK is preparing to stay in the customs union after Brexit, and beyond 2021. The news came after Prime Minister Theresa May said she's aiming for a "future customs union" with the EU. And, her top ministers agreed this week on a last-resort plan to avoid a hard Irish border. Foreign Secretary Boris Johnson and Environment Secretary Michael Gove objected the plan but were "outgunned" by other during the meeting.

The news gave Sterling a strong lift as it's trading as the strongest one for today, and the second strongest next to Canadian Dollar.

Australia jobs +22.6k, participation rate made another record high

Australia employment market grew 22.6k in April (seasonally adjusted), slightly above expectation of 20.0k. Full time employment grew 32.7k while part time jobs dropped -10k. Unemployment rate rose 0.1% to 5.6%, above expectation of being unchanged at 5.5%. Participation rate rose to a further record high of 65.6%. ABS Chief Economist Bruce Hockman said "the labour force participation rate was the highest it has been since the series began in 1978, indicating increasing attachment to the labour force."

Also from Australia consumer inflation expectation rose to 3.7% in May.

New Zealand PPI input slowed to 0.6% qoq in Q1 but beat expectation of 0.3% qoq. PPI output slowed to 0.2% qoq, in line with consensus.

Crude Oil in Fresh 3.5-Year Highs on Inventory Draw and Geopolitical Tensions

Renewed geopolitical tensions and decline in US inventory have lifted oil prices, sending the front-month WTI and Brent crude oil contracts to highest levels since 4Q14. The Brent crude, pressing the US$ 80/bbl-level, is about to record its 6th consecutive weekly gain. The strength in oil prices, accompanied by greenback's failure to move decisively higher despite record-high yields, also helped the rebound of commodity currencies (AUD, NZD and CAD are under our coverage).

We see two geopolitical issues as the key driving forces in the near-term. First, the newly-formed Italian coalition government by 5 Star Movement and far-right League has already caused disturbance to European economy and politics. The government has planned to request the ECB to cancel 250B euro of Italian debt. Meanwhile, it would seek to renegotiate Italy’s contribution to EU budget and propose new Eurozone rules that allow member states to quit. Second, uncertainty has increased of whether the US-North Korea summit would be held, after Kim Jong-un cancelled high-level talks with South Korea on Wednesday. The pariah state blames the South for holding joint military exercises with the US. In a statement released on the same day, North Korea condemned that the US has made "reckless" remarks by requesting the North to have "complete, verifiable and irreversible denuclearization" first, calling these "extremely unjust behavior".

The report from the US Energy Information Administration (EIA) shows that total crude oil and petroleum products stocks fell -0.66 mmb to 1185.52 mmb in the week ended May 11. Crude oil inventory dropped -1.4 mmb (consensus: +0.76 mmb) to 432.35 mmb, amidst increases in 2 out of 5 PADDs. PADD 1 (East Coast) and PADD 3 (Gulf Coast) saw declines of -2.36 mmb and -1.5 mmb respectively. Cushing stock added +0.05 mmb to 37.22 mmb. Utilization rate increased +0.7% to 91.1%. Meanwhile, crude production increased +0.02M bpd to 10.72M bpd for the week.

For refined oil products, gasoline inventory plunged -3.79 mmb to 232.01 mmb although demand dropped -2.5% to 9.53M bpd. This was compared with consensus of a -1.42 mmb draw. Production rose +4.89% to 10.46M bpd while imports slumped -10.21% to 0.72M bpd during the week.

Distillate inventory slipped -0.09 mmb to 114.95 mmb although demand was down -1.97% to 4.22M bpd. The market had anticipated a --2.16 apmmb draw. Production added +0.76% to 5.03M bpd while imports plunged -39.84% to 0.77M bpd during the week.

Released after market close on Tuesday, the industry- sponsored API estimated that crude oil inventory gained +4.85 mmb during the week. For refined oil products, gasoline distillate dropped -3.37 mmb while distillate slid -0.77 mmb.

Market Morning Briefing: Euro Dipped To A Low Of 1.1763

STOCKS

Dow (24768.93, 0.25%) saw a low near 24629 yesterday after having come off from resistance on daily candles, and could continue dipping for few more sessions towards 24500-24250. Downside could be restricted till 21 DMA near 24380.

Dax (12996.33, 0.20%) saw an upmove yesterday after closing near 12916 on Tuesday. It could see a slight downmove over the next 1-2 sessions towards 12950-12900 (seen as support on daily candles), after which it should rise again. We repeat that the medium term outlook for Dax remains bullish.

Support for Nikkei (22817.88, 0.44%) on daily candles near 22700 held yesterday and it rose towards 22800. It could now rise further towards 23000+ in the coming sessions.

Shanghai (3159.88, -0.31%) is seeing a dip from resistance on daily and 3 day candles near 3180-3200 and looks bearish towards 3100 in the near to medium term.

Nifty (10741.10, -0.56%) after having seen a high near 10930 after the Karnataka election results has broken channel support on daily candles and saw a low of 10699 yesterday. If this break persists, we might see Nifty coming off towards 10600 in the near term.

COMMODITIES

Brent (79.39) and Nymex WTI (71.76) have both moved up and could test levels near 80 and 73 respectively over the next couple of sessions. 80 is seen as resistance for Brent on daily and 3 day candles while 73 is seen as resistance for WTI on 3 day candles. We don’t expect these resistances to be breached in the near term. Instead there might be a dip from those levels.

Gold (1292.73) is testing crucial support on 3 day candles and weekly candles near current levels and could rise in the near term towards 1320.

FOREX

Dollar index (93.12) had moved up sharply day before yesterday as the US 10 Year yield rose past 3% decisively. As we predicted, it is seeing a slight dip after testing levels near 93.6 yesterday. It could dip further towards support on daily candles near 93 before resuming its uptrend. It should target levels near 94-95 in this month.

Euro (1.1831) dipped to a low of 1.1763 yesterday and is very near to the 55 weeks moving average currently. It could be seeing some upward correction towards channel resistance on daily candles near 1.185. However, as the Dollar Index tests levels near 94-95, Euro could test levels near 1.17-1.16.

Dollar Yen (110.14) is currently trading in the 110.0-110.5 zone. There is decent likelihood of it going up further till 111 and then turning bearish after that for the medium term.

Euro Yen (130.30) saw a low near 129.5 yesterday as Euro dipped to 1.1763 and thereby tested support on 3 day candles. It might now range between 131-129.5 for some time as the Dollar Yen stays close to 110-111 and the Euro slowly moves down towards 1.17.

Pound (1.3563): Pound tested support on daily and 3 day candles near 1.345 yesterday and has risen from there. It could now range between 1.345 and 1.37 for few days before resuming its downtrend.

Dollar Rupee (67.7975): Good Support at 67.50. May see 68+ again next week.

INTEREST RATES

Repeating yesterday’s comment about US Retail Sales:

US Retail Sales grew 0.3% in April and the March growth figures were revised upward from 0.6% to 0.8%. Sentiment around US economic growth received a boost by these numbers, with the 2nd quarter of 2018 expected to see higher consumption as compared to the mild consumption figures in the 1st quarter. This data release (as we had anticipated), turned out to be the trigger which has made the US 10 Year yield breach the 3% level decisively (high near 3.11%). We can now expect US yields to move towards their medium term targets, which are as below:

3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.75% (2 Year)

As the expected rate hike in the June Fed meeting starts getting factored later this month, the rally in yields could continue till the above mentioned targets are reached. We also expect some more yield curve flattening in this month followed by steepening after that, as yields bounce from long term supports.

US 10 Yr Yield (3.10%), 30 Yr (3.22%), 5 Yr (2.94%), 2 Yr (2.58%): The 30 year yield and 5 year yield as per our expectation have moved past resistances near 3.2% and 2.9% on medium term charts and could now move further up towards their above mentioned medium term targets.

The German 10 Year – US 10 Year yield spread (-2.49) has broken below immediate support on medium term and long term charts as the US 10 year rose further to 3.1% while the German 10 year yield dipped towards 0.61%. If this break persists, we might revisit our prediction of a rise in the spread towards -2.3%. In that case, the spread might turn bearish towards long term channel support near -2.75%.

Japan ready for retaliation against US steel tariffs

The NHK reported that Japan is readying retaliation against US tariffs. And it's completing final arrangements to inform the WTO. It should be noted that Japan is one of the top 10 steel importers to the US who is not even granted a temporary exemption of the steel and aluminum tariffs. Meanwhile, South Korea was given permanent exemptions after updating the trade agreement.

Japan is said to be considering to impose tariffs on US imports that are worth USD 409m, equivalent of duties levied by the US through its tariffs. The list of goods was not publicized.

No news on NAFTA as May 17 deadline looms

There is so far no positive news out of NAFTA negotiation yet. House Speaker Paul Ryan said today (Thursday) is the last day the Congress has to receive a notification of a deal, if it is to pass it within this year. But it's believed that the fundamental differences regarding auto contents and sunset clause remain between the US and the other two countries, Mexico and Canada.

BoC Governing Council Member Schembri said yesterday that uncertainty on NAFTA is impacting firms' investment decisions. And, capacity is being "hindered" by firms' reluctance to take on investment in face of uncertainty. And some of which is related to NAFTA.

Euro At Risk Of More Declines Vs USD And GBP

Key Highlights

- The Euro declined heavily this week against most major currencies, including US Dollar and British Pound.

- A crucial bearish trend line with current resistance near 0.8790 protected gains on the daily chart of EUR/GBP.

- The Euro Area CPI in April 2018 increased 0.3% (MoM), similar to the forecast.

- The yearly change in the Euro Zone CPI was 1.2% in April 2018.

EURGBP Technical Analysis

The Euro faced a lot of selling interest recently against the US Dollar and British Pound. The EUR/USD pair declined below 1.1800 and EUR/GBP was rejected from a major resistance near 0.8800.

Looking at the daily chart of EUR/GBP, the pair started a decent upside move from the 0.8620 support in April 2018. It moved above the 38.2% Fib retracement level of the last decline from the 0.8967 high to 0.8620 low.

However, the upside move was capped by a crucial bearish trend line with current resistance near 0.8790. Moreover, the pair struggled to settle above the 0.8800 level and the 100-day simple moving average (red).

Lastly, the pair was rejected from the 61.8% Fib retracement level of the last decline from the 0.8967 high to 0.8620 low. The pair is currently declining and is trading well below 0.8780.

It may continue to decline towards the next support at 0.8720 and 0.8700. On the upside, a break above 0.8790 and 0.8800 is required for further gains in the near term.

Recently, the Euro Consumer Price Index for April 2018 was released by the Eurostat. The market was looking for a rise of 0.3% in the CPI compared with the previous month.

The actual result was similar, and the yearly change was also in line with the forecast of 1.2%. The report mentioned that:

The lowest annual rates were registered in Cyprus (-0.3%), Ireland (-0.1%) and Portugal (0.3%). The highest annual rates were recorded in Romania (4.3%), Slovakia (3.0%) and Estonia (2.9%). Compared with March 2018, annual inflation fell in twelve Member States, remained stable in one and rose in fourteen.

Overall, the Euro is in a bearish zone versus the US Dollar and British Pound. It may correct higher, but upsides are likely to remain capped in EUR/USD and EUR/GBP.

Economic Releases to Watch Today

- US Initial Jobless Claims – Forecast 215K, versus 211K previous.

- Canada’s ADP Employment Change April 2018 – Forecast 32.0K, versus 42.8K previous.