Sample Category Title

Euro Cracked Down by Italian Populist Duo, Safe Haven Flow Caps Dollar Gains

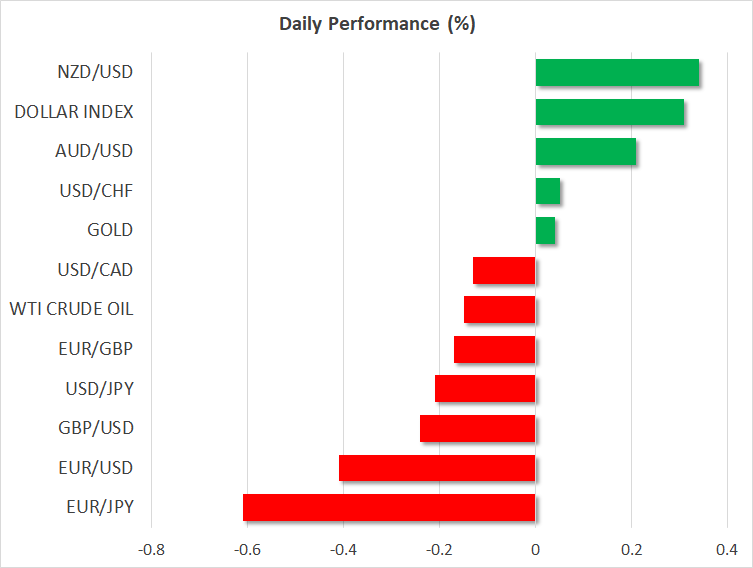

Politics are the main drivers in the forex markets today. Euro tumbles broadly on concern of the populist policies of the coalition government in Italy. EUR/USD finally took out 1.1822 support decisively But the more important development could be in EUR/CHF which dives through 1.8 handle. Dollar actually doesn't perform very well today as it's the third weakest one. Safe haven flows helped pushed treasury yields lower. 10 year yield hit seven year high at 3.094 yesterday but it's now back at around 3.06. The renewed uncertainties regarding North Korea, as well as Italy worries are the triggers.

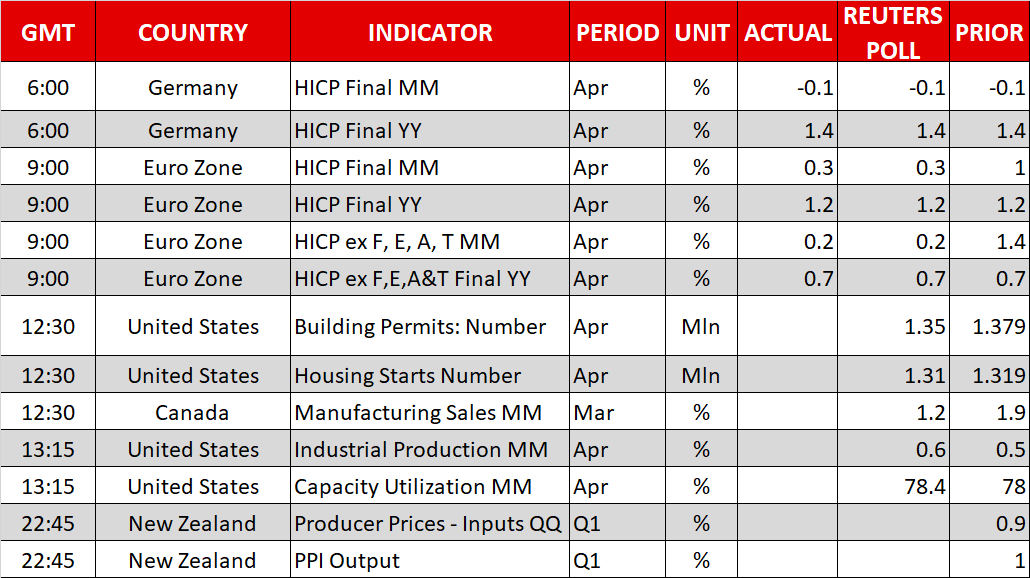

Released in North America session, US housing starts dropped -3.7% to 1.29m annualized rate in April, below expectation of 1.33m. Building permits dropped -1.8% to 1.35m, marched expectations. Canada manufacturing shipment rose 1.4% mom in March. above expectation of 1.0% mom.

Euro drops sharply as Italian populist duo could seek debt forgiveness

According to a 39-page draft obtained by Huffington Post Italia, the anti-establishment 5 Star Movement and far-right League are planning to ask ECB to forgive EUR 250B of Italian debt. Further than that, they would seek to renegotiate Italy's contribution to EU budget. And, the populist duo would also push for new Eurozone rule to allow member states to leave. It's generally expected that the final version of the policies will be watered down. But the sense of concerns is there in the markets, regarding the possibilities of chaos created by a government run by these two political outsiders.

Released from Eurozone, German CPI was finalized at 1.6% yoy in April. Eurozone CPI was finalized at 1.2% yoy, CPI core at 0.7% yoy. All were unrevised.

German Merkel: You can talk better if you remain in the Iran deal

German Chancellor Angela Merkel said in Bundestag that the Iran nuclear deal is the best way to address the concerns of Iran. She noted that "the question is whether you can talk better if you terminate an agreement or if you stay in it ... we say you can talk better if you remain in it."

Merkel admitted that the agreement "is everything other than ideal". But she acknowledged that "Iran is, according to all the knowledge of the international nuclear authorities, sticking to the commitments of the agreement."

Meanwhile, regarding the relationship with the US, Merkel said "despite all the difficulties that we have these days, the transatlantic relationship is and remains paramount." "But these transatlantic relationships also must be able to deal with differences of opinion."

China's ambassador to WTO: US requests clearly violent WTO rules

China's ambassador to WTO, Zhang Xiangchen said that "the US is blocking selection of new Appellate Body members, taking restrictive trade measures under Section 232 and threatening to impose tariff measures of US$50 billion of goods imports from China under Section 301 of US domestic law." And, he warned "any one of these, if left untreated, will fatally undermine the functioning of the WTO."

The US was reported to have requested China to cut its trade surplus with it by USD 200b by 2020. Zhang criticized that "such practices clearly violate the non-discrimination principle of the GATT, therefore have long been abandoned" by the WTO.

And he pointed out the contradiction in what the US is trying to do. He said "the US is blaming the Chinese Government for state intervention on the one hand, while pressing China, by way of issuing government orders, to increase imports, restrict exports, and reduce excess capacity on the other hand." Also, "governments can make efforts to promote trade, but cannot force companies to do business by pointing gun at their heads."

North Korea infuriated by Bolton, threatens to cancel Trump-Kim summit

North Korea threatened to cancel Trump-Kim summit after they're infuriated by comments from Trump's national security adviser John Bolton that North Korea could follow a Libyan model of nuclear disarmament. The meeting is scheduled to be on June 12.

North Korea's vice-foreign minister Kim Kye-gwan used strong words in a statement carried by the state news agency KCNA. He condemned that Bolton's suggestion was "not an expression of intention to address the issue through dialogue". And, "it is essentially a manifestation of awfully sinister move to impose on our dignified state the destiny of Libya or Iraq which had been collapsed due to yielding the whole of their countries to big powers."

Kim went further and warned that if the US "corners us and unilaterally demands we give up nuclear weapons we will no longer have an interest in talks and will have to reconsider whether we will accept the upcoming DPRK-US summit". And, "if President Trump follows in the footsteps of his predecessors, he will be recorded as more tragic and unsuccessful president than his predecessors, far from his initial ambition to make unprecedented success."

Japan GDP ended expansion streak... temporarily

Japan GDP contracted -0.2% qoq in Q1, worse than expectation of 0.0% qoq. On annualized basis,GDP contracted -0.6% versus expectation of -0.1%. The contraction marked the end of eight straight quarters of growth. And that was the longest streak since 1989. GDP deflator, however, rose 0.5% yoy, beating expectation of 0.3% yoy.

But it's generally believed that the contraction is temporary. In particular, a relatively weaker Yen at 100 against Dollar and global recovery, export led Japanese economy remains on solid footing for expansion.

Also from Japan, industrial production was revised up to 1.4% mom in March, from first estimate of 1.2% mom.

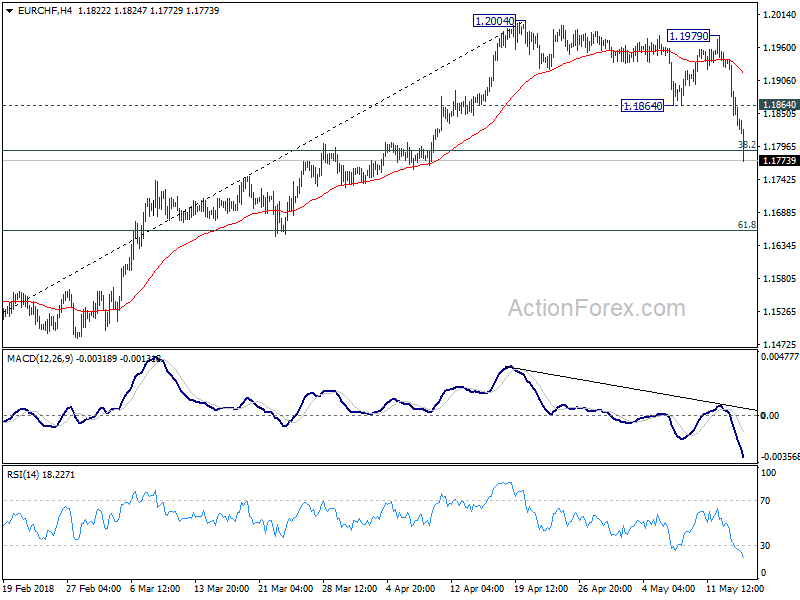

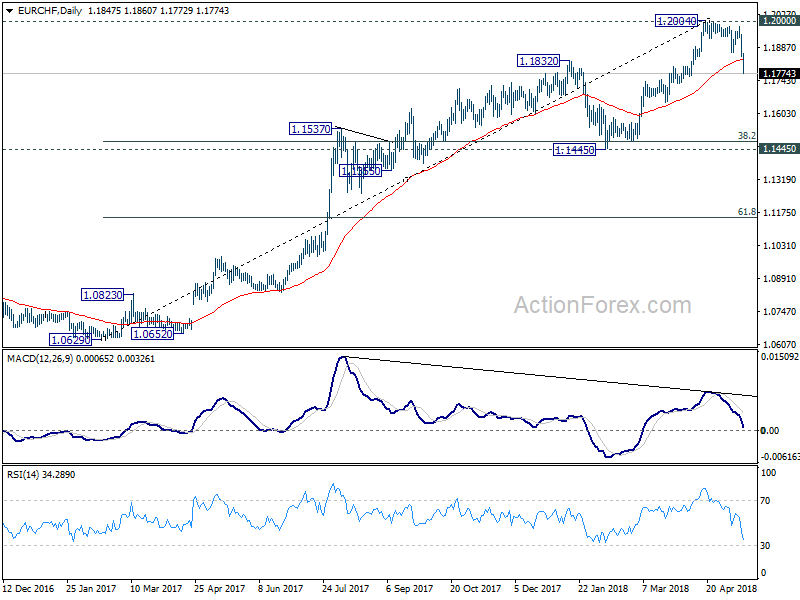

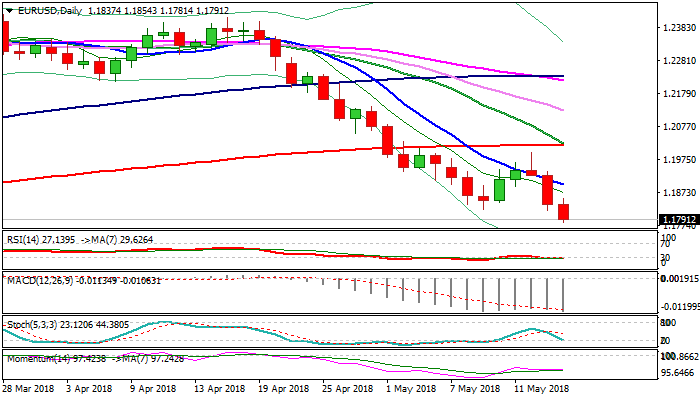

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1819; (P) 1.1883; (R1) 1.1917; More...

EUR/CHF drops sharply to as low as 1.1777 so far today and breaks 38.2% retracement of 1.1445 to 1.2004 at 1.1790. Based on current momentum, deeper decline would likely be seen. Intraday bias stays on the downside for 61.8% retracement at 1.1659 and below. On the upside, break of 1.1864 support turned resistance is needed to indicate short term bottoming. Otherwise, near term outlook will be mildly bearish even in case of recovery.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 could be a medium term top. And price action from 1.2004 is corrective the up trend from 1.0629. Hence, for now, deeper fall could be seen back to 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q1 P | -0.20% | 0.00% | 0.40% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | 0.50% | 0.30% | 0.10% | |

| 00:30 | AUD | Westpac Consumer Confidence May | -0.60% | -0.60% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.50% | 0.60% | 0.60% | |

| 04:30 | JPY | Industrial Production M/M Mar F | 1.40% | 1.20% | 1.20% | |

| 06:00 | EUR | German CPI M/M Apr F | 0.00% | 0.00% | 0.00% | |

| 06:00 | EUR | German CPI Y/Y Apr F | 1.60% | 1.60% | 1.60% | |

| 09:00 | EUR | Eurozone CPI M/M Apr | 0.30% | 0.30% | 1.00% | |

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 1.20% | 1.20% | 1.30% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr F | 0.70% | 0.70% | 0.70% | |

| 12:30 | CAD | Manufacturing Sales M/M Mar | 1.40% | 1.00% | 1.90% | 2.70% |

| 12:30 | USD | Housing Starts Apr | 1.29M | 1.33M | 1.32M | 1.34M |

| 12:30 | USD | Building Permits Apr | 1.35M | 1.35M | 1.35M | 1.38M |

| 13:15 | USD | Industrial Production M/M Apr | 0.60% | 0.50% | ||

| 13:15 | USD | Capacity Utilization Apr | 78.40% | 78.00% | ||

| 14:30 | USD | Crude Oil Inventories | -2.2M |

US housing starts at 1.29m, building permits at 1.35m in April

US housing starts dropped -3.7% to 1.29m annualized rate in April, below expectation of 1.33m. Building permits dropped -1.8% to 1.35m, marched expectations.

Canada manufacturing shipment rose 1.4% mom in March. above expectation of 1.0% mom.

Euro remains the weakest one today as weighed down by Italy concerns, followed by Sterling. Dollar is indeed the third weakest so far, as safe haven flows lifted US treasuries. 10 year yield is back below 3.06 at the time of writing, comparing to yesterday's high at 3.094. New Zealand Dollar is the strongest one, mainly as it digests recent losses.

Dollar Index Peaks At Fresh 5-Month Highs On Rising Treasury Yields

Here are the latest developments in global markets:

FOREX: The US dollar pared some of Tuesday’s gains that were posted after a rally in US treasury yields; 10-year Treasury yields hit as high as 3.095, the highest since 2011. Dollar/yen retreated by 0.18% after it marked a new 3-month high of 110.44 on yesterday’s US session. The US dollar index was moving higher on Wednesday by 0.25%, peaking at a fresh five-month high of 93.45. Eurozone’s inflation rate remained unchanged at 1.2% in April as expected but euro/dollar stretched lower to 1.1786 (-0.29%) on the back of a stronger dollar. Pound/dollar fell to 1.3474 (-0.21%), its lowest reading of 2018, as Brexit uncertainties continued to weigh in the background, with May’s conservatives remaining divided on the type of relationship the UK and the EU should have in the future. The UK government stated that it would publish a detailed withdrawal plan next month. The antipodean currencies were moving higher, both set to complete a bullish day. Aussie/dollar rose by 0.12% on the day, while kiwi/dollar climbed by 0.41%. Meanwhile, dollar/loonie traded slightly lower by 0.10% at 1.2862.The Turkish lira is one of the worst-performing currencies today and as well as of this year. The Turkish President Tagip Erdogan alarmed investors when he said that he plans to take greater control of the economy after the country’s elections. Dollar/lira surged by 1.14%, creating a new record high at 4.4990.

STOCKS: European stocks were moving mixed for the second day in a row at 1050 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.02% and 0.13% respectively. In Germany, the DAX rose by 0.25%, while the French CAC 40 fell by 0.05%. In Italy, the FTSE MIB 100 tumbled by 1.78% amid political worries, while the British FTSE 100 traded marginally higher by 0.09%. The Spanish IBEX 35 dived by 0.95%. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in negative territory, pointing to a lower open today after facing a sharp buying interest since early May. On Tuesday, US Stocks fell for the first time in eight straight sessions.

COMMODITIES: Oil prices dipped on Wednesday, after reaching a new high during yesterday’s session, as an increase in US crude inventories signaled that demand is easing despite the ongoing output cuts by OPEC. West Texas Intermediate (WTI) crude oil dropped by 0.18% to $71.18, while Brent moved lower by 0.68% to $77.90. In precious metals, gold recovered some lost ground today (+0.08%) after prices hit the lowest level this year of $1,288.31 on the back of surging US bond yields and a stronger dollar.

Day ahead: Geopolitical developments attract attention; US housing data & industrial production in focus

A potential escalation in tensions between the US and North Korea could keep investors in risk-off mode during the day following North Korea’s threat to scrap a historic summit between the US President Donald Trump and the North Korean leader Kim Jong-Un on June 12. The warning arose after a planned joint military exercise between Seoul and Washington, with the North Korea’s First Vice Minister of the Ministry of Foreign Affairs, Kim Kye-gwan, saying in KCNA news agency that if the US pushes “us into the corner and force only unilateral nuclear abandonment, we will no longer be interested in that kind of talks and (we) will have to reconsider whether we will accept the upcoming NK-US summit”. A tough response from the US side could enhance demand for safe-haven assets later in the day and at the same time weigh on the dollar.

A number of economic releases out of the US are also expected to affect the dollar today. At 1230 GMT, the number of building permits and housing starts for the month of April is expected to ease, with the former projected to slip by 290,000 to 1.350mn and the latter to decline by 9,000 to 1.310mn. A few minutes later at 1315 GMT, data on industrial production for the same month are forecast to show a monthly growth of 0.6% compared to an expansion of 0.5% in March.

In Canada, stats on manufacturing sales due at 1230 GMT will have the potential to move the loonie.

Elsewhere, political developments in Italy will attract traders’ attention as the two anti-establishment parties, Five-Star Movement and the right-wing League, will try to reach a coalition deal today. The parties are also said to propose a debt relief of 250 billion euros from the ECB.

In oil markets, the EIA weekly report on US oil inventories delivered at 1430 GMT is anticipated to keep traders busy. According to analysts, US crude oil inventories are said to have declined by around 0.8mn barrels in the week ending May 11, less than a decline of 2.2mn barrels in the preceding week. Yesterday, though, the API weekly report on US crude oil stocks didn’t meet projections for a decline, posting the highest buildup since early April.

In other data under consideration, New Zealand’s Q1 PPI figures and Japanese core machinery readings for the month of March due at 2245 and 2350 GMT respectively are anticipated to slow down. In Australia, the Australian Bureau of Statistics is scheduled to publish its employment report early on Thursday at 0130 GMT.

Meanwhile, in equity markets, CISCO will be delivering its quarterly earnings report before the US market open.

As of today’s public appearances, ECB policymakers, including President Mario Draghi (1200 GMT), and ECB Board members, Benoit Coeure (1230 GMT) and Peter Praet (1430 GMT) will be speaking at a conference in honor of departing ECB Vice President Vitor Constancio. In the US, Atlanta Fed President Raphael Bostic will be talking about the US economy at 1230 GMT, while in Canada, BoC Deputy Governor Lawrence Schembri will be making remarks at 1415 GMT.

DAX Steady As German CPI Matches Estimate

In the Tuesday session, the DAX is at 13,027, up 0.27% on the day. On the release front, German and eurozone CPI releases matched their estimates. ECB President Mario Draghi will speak at an ECB event in Frankfurt.

German Final CPI dropped to 0.0% in April, down from 0.4% a month earlier. Eurozone inflation indicators also pointed downwards. Final CPI edged lower to 1.2%, down from 1.3% a month earlier. Eurozone Final Core CPI followed a similar trend, dropping from 1.0% to 0.7%. If inflation levels continue to soften, the ECB will have to consider extending its stimulus scheme, which is scheduled to run until September. Germany will release additional inflation numbers on Friday.

Bank of France Governor Francois Villeroy de Galhau raised some eyebrows on Monday after making hawkish comments about ECB interest rates hikes. Villeroy said that the ECB could soon provide additional guidance on the timing of a rate hike. In its last rate statement, the ECB said that any rate hikes would occur ‘well past’ the wrap-up of the stimulus program, which is slated to end in September. Villeroy stated that ‘well past’ could be a matter of quarters, rather than years. Investors snapped up euros on Monday after Villeroy’s comment, but the euro failed to hold onto these gains and ended the Monday session with small losses.

Euro drops sharply as Italian populist duo could seek debt forgiveness

Euro drops sharply in European session with EUR/USD taking out 1.1822 support with conviction finally. EUR/JPY also dropped through 129.99 minor support and is heading back to 129.22 low. EUR/CHF's selloff accelerates and breaks 1.8 handle. Other currencies are relatively steady against each other.

The main trigger of the selloff is Italy. it's reported that the anti-establishment Five Star Movement and the anti-immigration League are discussing to seek EUR 250B write of in debt from ECB.

From trend following point of view, EUR/USD is a good candidate for short as it just went through a period of consolidation. Action Bias are back in downside red across time frame.

From trend reversal point of view, EUR/CHF could be a candidate for short. It just took out 1.1864 support with downside acceleration. Usually, we won't jump to call for short when weekly Action Bias is still in upside blue. But as EUR/CHF was just rejected by 1.2 key resistance, selling the cross can be considered.

EURUSD Probes Below 1.18 Handle As Weak EU Inflation Provided Additional Pressure

The Euro broke below psychological support at 1.1800 and hit new nearly five-month low as stronger dollar on rising US bond yields continues to drive the single currency lower and additional pressure came from slowdown in EU inflation. CPI in Eurozone slowed to 1.2% in April from 1.3% previous month, while core inflation which excludes volatile items such as food and energy, fell from 1.0% in March to 0.7% in April. Losing 1.1800 handle, the Euro became more vulnerable to further weakness, with key support at 1.1709 (Fibo 38.2% of 1.0340/1.2555 ascend came in focus). Larger bulls off 1.0340 (03 Jan 2017 low) are in corrective phase from new multi-year high at 1.2555 (2018 high), which should be ideally contained by 1.1709 support to keep broader bulls in play, however, recent strong weakness of the Euro doesn't show signs of fatigue and may break below 1.1709 pivot and risk deeper correction of 1.0340/1.2555 rally. Below 1.1709, next strong support lays at 1.1675 (top of thick weekly Ichimoku cloud).

Res: 1.1800, 1.1822, 1.1854, 1.1899

Sup: 1.1815, 1.1776, 1.1709, 1.1675

US and Oil Figures Eyed While Italy Nears Populist Coalition

- US Data in Focus After Encouraging Retail Sales Figures;

- Oil Inventories Could Trigger Some Profit Taking;

- Italian Yields Spike and FTSE MIB Slips as Draft Program is Leaked.

US Data in Focus After Encouraging Retail Sales Figures

US futures are flat ahead of the open on Wall Street on Wednesday, as we await a number of data points from the world’s largest economy and Italy closes in on a eurosceptic coalition government.

We got some interesting retail sales figures from the US on Tuesday which helped lift yields and saw a fourth rate hike this year being around 50% priced in. There’s plenty more data to come today which may further lift expectations including housing starts, building permits, capacity utilization and industrial production. The dollar is making gains again early in the session having pared gains late last week and has already set a new high for the year so far, ahead of the figures.

Oil Inventories Could Trigger Some Profit Taking

We’ll also get EIA crude inventories figures today, which comes shortly after OPEC published figures showing inventories in OECD countries had fallen to nine million barrels above the five year average from 340 million at the start of last year. Clearly the production cuts have been working but with the deal rolling on and Iranian sanctions potentially restricting them further, oil prices could rise further before they stabilise.

A drawdown of around three quarters of a million barrels is expected to be reported today although API reported their figures on Tuesday and they indicated that stockpiles actually rose by 4.854 million barrels. A similar reading from EIA today could relieve some of the upward pressure on prices and trigger some near-term profit taking.

Italian Yields Spike and FTSE MIB Slips as Draft Program is Leaked

In Europe, much of the focus has been on Italy where a leaked draft of the joint program of Five Star Movement and League has unsettled investors, leading to 1.5% losses in the FTSE MIB stock index and a spike in Italian yields with the 10-year rising back above 2%. Markets haven’t necessarily been complacent about the prospect of a eurosceptic coalition until now but investors have taken the developments very much in their stride and not got carried away.

The draft program though has fuelled investors’ fears about what a coalition of the two parties – both of which have openly opposed membership of the currency union in the past and most likely still do despite it not being a key feature of the election campaign – will mean for the country. The most concerning component was the desire to create economic and judicial procedures that allow member states to leave the monetary union, which makes clear their ultimate intentions.

While both parties have since claimed the draft was an old version and they had since decided against calling into question the single currency, it’s impossible to ignore and even if an exit isn’t pursued in the immediate future, it looks a case of when rather than if they do so, if the coalition is formed. There were other aspects of the draft that will also concern investors, not to mention the joint desire to no longer be constrained by the currency blocks fiscal rules.

It seems euro leaders were too quick to congratulate themselves on a job well done when defeating populists last year and may have a massive job on their hands that makes Brexit look more straight forward. I also wonder how much this could affect the European Union’s approach to Brexit as other leaders will be wary about giving the populists more reason to push for an exit of their own, citing the deal the UK got as an example of what can be achieved.

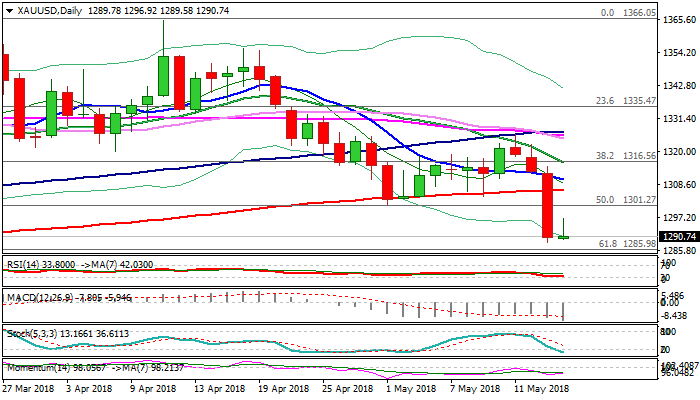

Gold Consolidates After Sharp Fall, Bears Need Break Below $1285 Fibo Support For Fresh Negative Signal

Gold price moved higher on Wednesday after falling sharply the previous day (gold fell nearly 1.7% on Tuesday), but recovery was so far limited and stayed below psychological $1300 barrier.

The yellow metal price was heavily sold as rallying dollar and US bond yields prompted investors out of gold positions.

Break and close below 2000SMA ($1306) previous low ($1301) was strong bearish signal and fresh extension lower dipped so far to $1288 (new 5 ½ month low).

Pivotal support at $1285 (Fibo 61.8% of $1236/$1366 ascend / weekly cloud top) is under pressure and break here would generate another negative signal.

Fresh bearish acceleration from $1325 (11 May lower top) marks the third wave of five-wave sequence from $1355, which could travel to its FE 100% at $1271.

Oversold slow stochastic suggests the price may hold in extended consolidation before final break through $1285 support, with broken 200SMA expected to cap extended upticks and maintain bearish bias.

Res: 1296, 1301, 1306, 1310

Sup: 1288, 1285, 1277, 1271

Euro Softer, German And Eurozone CPI Match Expectations

EUR/USD has posted losses in the Wednesday session, continuing the downward trend we saw on Tuesday. Currently, the pair is trading at 1.1803, down 0.31% on the day. On the release front, German and eurozone CPI releases matched their estimates. ECB President Mario Draghi will speak at an ECB event in Frankfurt. In the U.S, Housing Starts and Building Permits are expected to remain unchanged, at 1.32 million and 1.35 million, respectively. On Thursday, the U.S releases Philly Fed Manufacturing Index and unemployment claims.

German Final CPI continues to lose ground. The indicator dropped to 0.0%, marking a 3-month low. Eurozone Final CPI edged lower to 1.2%, down from 1.3% a month earlier. Eurozone Final Core CPI followed a similar trend, dropping from 1.0% to 0.7%. If inflation levels continue to soften, the ECB will have to consider extending its stimulus scheme, which is scheduled to run until September. Germany will release additional inflation numbers on Friday.

First-quarter eurozone and German GDP data were within expectations, but investors should not become too sanguine, as the numbers pointed to a slowdown in the eurozone economy. Both Germany and the eurozone posted gains of 0.6% in the fourth quarter of 2017. Will economic conditions improve in Q2? Institutional analysts don’t seem optimistic, according to the well-respected ZEW Economic Sentiment surveys. The German indicator posted a sharp drop of -8.2 for a second straight month – the first declines since July 2016. The eurozone release improved to 2.4, but low reading certainly doesn’t show much optimism. The markets are bracing for more soft numbers on Wednesday, as Germany and eurozone release CPI reports. If these indicators miss their estimates, the euro could lose ground.

GBPUSD Strongly Bearish Below 1.3500 Level

The British pound has started to retreat back below the key 1.3500 level against the US dollar, as the greenback continues to move higher across the board on Wednesday. The GBPUSD pair had made a strong technical bounce from the 1.3458 level on Tuesday, but soon found strong resistance from the 1.3525 level. Traders now look for continued sterling losses below the 1.3500 level, with further heavy declines likely below the 1.3458 level.

The GBPUSD pair is strongly bearish while trading below the 1.3500 level. Key support is now located at 1.3458 and 1.3425 levels.

If the GBPUSD pair starts to trade above the 1.3500 level, buyers may be encouraged to test towards the 1.3525 and 1.3553 levels.