Sample Category Title

The Trend Is Your Friend

Currency Markets

There was an intense focus on Italy Wednesday thanks to speculation that its new coalition government would request that the ECB write-off the bank’s QE-acquired debt of EUR250bn. Panic ensued with the EURUSD plunging to 1.1760 before recovering after the report was denied.

But the Italian political noise proved to be little more than a distraction from the markets complete focus on US 10-year yields as investors continue to challenge their conviction on both the USD and the trajectory of US bond yields. But, what’s new with this picture as the market has been second-guessing the emerging bullish dollar narrative since Mid-April and missing out on 550 pips EURUSD downside move

If the market continues to trade off US yields and diverging economic data between the US and EU, it’s hard to argue against the current direction in yields or the dollar. Forget the VIX the DXY is the new fear index if we consider the number of market cracks the dollar has exposed on its recent move.

On the US economic data front, the consumer remains the economy’s backbone, and if this robust trend in the retail space continues to build, factor in a bit of wage growth pressure and the US dollar will continue to move higher on the back of higher yields.

However, the Pound has firmed considerably on Brexit news breaking news from The Telegraph explains. “Britain will tell Brussels it is prepared to stay in the customs union beyond 2021 as ministers remain deadlocked over a future deal with the EU, the Telegraph has learned.” which has towed the EURUSD gingerly higher in early APAC trade

EUR: With the EURUSD back above 1.1800, we’re at a make or break point for judging near term trader sentiment. Over the next 48 hours will be telling, as the bulls and bears jostled for position but provided the EURUSD can finish the week below 1.1850, that would suggest the bullish USD story remains intact. But a close below 1.1775 would be even more convincing

JPY: Similarly, a weekly market close above 110 indicates the near term USD rally continues. The correlation between rates feels right, and the USDJPY could be the best bet to express the USD dollar bullish bias near-term

AUD: It remains to confuse by not trading in line with US fixed income. And even more frustrating for the Aussie bears is the copper continues to sell poorly. After yesterday miss on the wage price index, a lot of buying emerged. Far much more than usual, suggesting some real cash interest on the dip possible from resting orders. ( Exporters??)

Oil Markets

Oil prices resumed their climb Wednesday after shrugging off Tuesday’s API data as investors turned focuses on the key Energy Information Administration report which highlighted an unexpected draw of 1.4 million barrels for the week to May 11. Of course, more attention will fall on EIA given that the API is a voluntary metric and, at times entirely off the wall, whereas EIA reporting is a mandatory industry regulation and the preferred metric for short-term investors. None the less, divergence in the reports will leave some investors scratching their heads as this week’s API data provided traders with more questions than answers.

With the dual supply shortcomings from Iran and Venezuela providing substantial support and given we’re not even in peak July driving season, at least for the short term, it’s hard to imagine Oil prices giving up too much ground especially on bearish inference from one of highly unpredictable US Oil inventory reports. Dips continue to look attractive in this environment.

Gold Markets

Gold remains under pressure from the US dollar and utterly vulnerable to higher US bond yields which are showing signs of a significant topside breakout after the 10-year Treasury note yield hit 3.1 % overnight. The inflationary overtones from oil prices coupled with a substantial US retail sales print have increased Fed rate hike expectations. As the trickle-down effects from US fiscal stimulus continue to show in the data, bond yields will move higher, but ultimately the positive data prints will leave a larger than life footprint on Fed members interest rate views and challenge the current dot plot scenario.

Malaysia Markets

Not unexpected the political noise, stronger USD and higher US Treasury yields continue to dent sentiment in local markets. But given the higher US Bond Yields, I expect the USDMYR to grind higher over the short term in line with the broader USDASia basket.

Gold Steadies After Slipping Below $1300

Gold is trading sideways in the Wednesday session, after sharp losses on Tuesday. In North American trade, the spot price for one ounce of gold is $1290.61, down 0.03% on the day. On the release front, construction numbers were mixed. Building Permits remained steady at 1.35 million, matching the forecast. Housing Starts dropped to 1.29 million, short of the estimate of 1.32 million. On Thursday, the U.S releases Philly Fed Manufacturing Index and unemployment claims.

In the U.S, retail sales and core retail sales posted gains in April, although both indicators fell short of the estimates. Still, consumer spending is improving after a sluggish first quarter. Investors liked what they saw, and the US dollar was broadly higher on Tuesday. At the same time, a new concern is higher gas prices, which could put a dent in consumers' wallets and hurt spending. Oil prices have hit their highest levels in over 3 years, and with the US leaving the Iran nuclear deal and escalating tensions in the Middle East, gasoline prices could remain at high levels.

The U.S economy continues to perform well, but the Federal Reserve target of 2 percent remains elusive. CPI rebounded with a gain of 0.2%, but this fell short of the estimate of 0.3%. Core CPI edged lower to 0.1%, shy of the forecast of 0.2%. Inflation levels will be an important factor for the Fed in its monetary policy projection, which remains at two more hikes in 2018. The odds of a rate hike at the June hike stands close to 100%, and the US dollar could continue to make broad gains as we get closer to the June policy meeting.

Eco Data 5/17/18

[php_everywhere instance="1"]

Pound Edges Lower, US Posts Mixed Construction Data

The British pound has posted slight losses in the Wednesday session. In the North American session, GBP/USD is trading at 1.3477, down 0.21% on the day. On the release front, British CB Leading Index. In the US, construction numbers were mixed. Building Permits remained steady at 1.35 million, matching the forecast. Housing Starts dropped to 1.29 million, short of the estimate of 1.32 million. On Thursday, the U.S releases Philly Fed Manufacturing Index and unemployment claims.

British employment numbers were a mix on Tuesday. Unemployment claims and wage growth both missed their forecasts, but the unemployment rate remained steady, and the participation rate rose to 75.6%, the highest rate ever recorded. Policymakers at the Bank of England will have to digest the mixed job numbers, as the employment market and wage growth will be important factors in the bank’s thought process regarding rate future rate hikes. Weak economic numbers dissuaded the BoE from raising rates last week, but if second-quarter data is stronger, the bank could press the rate trigger at its August meeting.

In the U.S, retail sales and core retail sales posted gains in April, although both indicators fell short of the estimates. Still, consumer spending is improving after a sluggish first quarter. Investors liked what they saw, and the US dollar was broadly higher on Tuesday. At the same time, a new concern is higher gas prices, which could put a dent in consumers’ wallets and hurt spending. Oil prices have hit their highest levels in over 3 years, and with the US leaving the Iran nuclear deal and escalating tensions in the Middle East, gasoline prices could remain at high levels.

Japanese Yen Dips after GDP Contracts

The Japanese yen is trading sideways on Thursday, after losing ground on Wednesday. In the North American session, USD/JPY is trading at 110.27, down 0.08% on the day. On the release front, Japanese Preliminary GDP contracted 0.2%, missing the estimate of 0.0%. Japanese Industrial Production dropped to 1.4%, above the estimate of 1.2%. In the US, construction numbers were mixed. Building Permits remained steady at 1.35 million, matching the forecast. Housing Starts dropped to 1.29 million, short of the estimate of 1.32 million. Later in the day, Japan releases Japanese Core Machinery Orders, with the markets braced for a sharp decline of 2.9%. On Thursday, the U.S releases Philly Fed Manufacturing Index and unemployment claims. Japan will publish National Core CPI.

In the U.S, retail sales and core retail sales posted gains in April, although both indicators fell short of the estimates. Still, consumer spending is improving after a sluggish first quarter. Investors liked what they saw, and the US dollar was broadly higher on Tuesday. At the same time, a new concern is higher gas prices, which could put a dent in consumers’ wallets and hurt spending. Oil prices have hit their highest levels in over 3 years, and with the US leaving the Iran nuclear deal and escalating tensions in the Middle East, gasoline prices could remain at high levels.

The Bank of Japan, always a cautious player, will not be exiting from its exiting from its radical stimulus anytime soon. However, BoJ policymakers are looking to raise bond yields as part of normalizing policy. Any moves will be small and incremental in nature, in order not to rattle the markets or the yen exchange rate. The bank took one such step in April, when it removed a deadline for hitting its inflation target of around 2 percent. The stimulus program was introduced in 2013, when BoJ Governor Kuroda claimed that he would reach the inflation target within two years. Fast forward to 2018, and the inflation target remains elusive, despite trillions of yen in stimulus. A stronger Japanese economy will make it easier for the BoJ to depart its radical easing policy, but traders should be prepared for small, incremental steps towards this end.

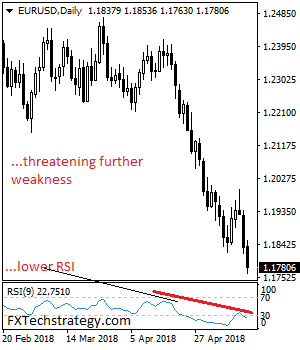

EURUSD: Weakens Further, Eyes The 1.1750 Zone

EURUSD: The pair faces further bear pressure as it continues to hold on to its bear pressure. On the upside, resistance comes in at 1.1850 level with a cut through here opening the door for more upside towards the 1.1900 level. Further up, resistance lies at the 1.1950 level where a break will expose the 1.2000 level. Conversely, support lies at the 1.1700 level where a violation will aim at the 1.1650 level. A break of here will aim at the 1.1600 level. Below here will open the door for more weakness towards the 1.1550. All in all, EURUSD faces further downside pressure.

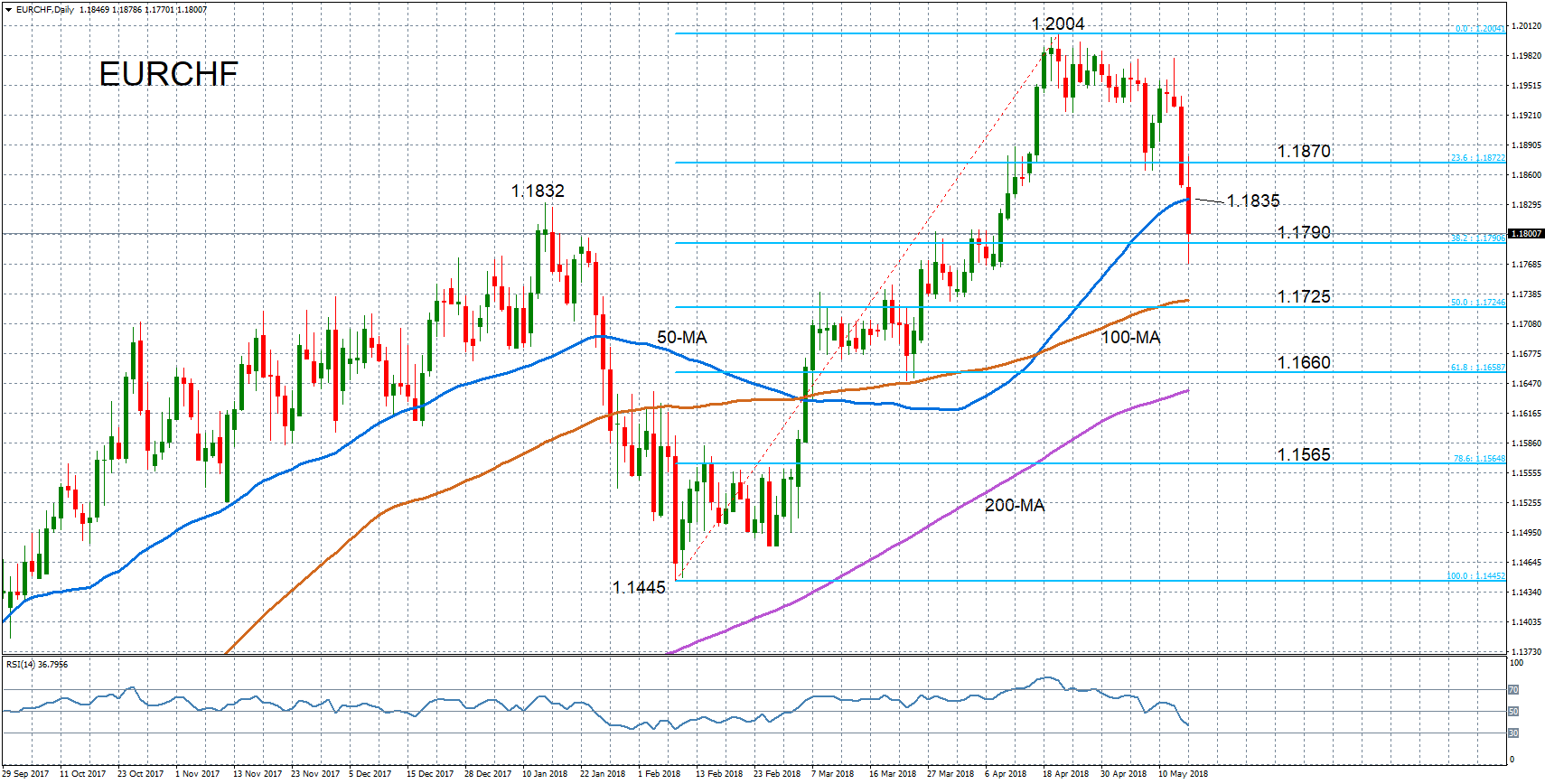

EURCHF turns bearish in short term after dramatic slump

EURCHF is on course for a fourth straight day of losses, which have taken the pair from above the 1.19 level to a one-month low of 1.1770 today. The sharp sell-off, especially in the past two sessions, has shifted the near-term bias from positive to negative. The momentum indicators are supportive of the bearish picture, with the RSI falling into negative territory below 50 and approaching the 30 oversold mark.

Immediate support is being provided by the 38.2% Fibonacci retracement of the upleg from 1.1445 to 1.2004, around 1.1790, as prices bounced back above this level after briefly tumbling below it. However, should prices dip lower again, the next support would likely come from the 50% Fibonacci retracement around 1.1725. A drop below the 50% Fibonacci level would signal the start of a deeper bearish phase.

In case of an upward attempt, EURCHF would likely meet resistance at the 50-day moving average (MA), currently around 1.1835. A break above the 50-day MA would ease the downside pressure, while a climb above the 23.6% Fibonacci level at 1.1870 would help turn the short-term bias to a bullish one.

In the medium term, the bullish outlook remains intact, with the moving averages all pointing upwards. However, should prices decline towards the 100-day MA, this would risk shifting the medium-term picture to a more neutral one.

White Hourse Sanders: We’ll continue the maximum pressure if Kim-Trump meting doesn’t take place

In response to North Korea's threat of cancelling the Kim-Trump summit, White House press secretary Sarah Huckabee Sanders said Trump is still hopeful that the meeting will take place. She said on Fox news that "we're ready to meet and if it happens, that's great. And if it doesn't, we'll see what happens."

And she added "we've been prepared that these could be tough negotiations. The president is ready if the meeting takes place and if it doesn't, we'll continue the maximum pressure campaign that's been ongoing."

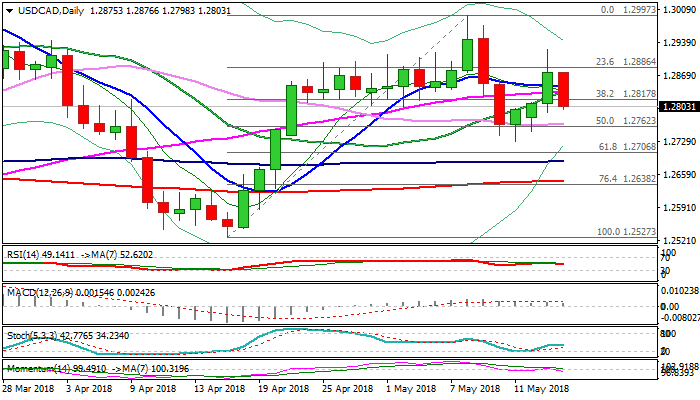

USDCAD Falls on Strong Canadian and Weak US Data

The pair fell back to 1.28 zone on better than expected Canada’s Manufacturing sales (Mar 1.4% vs 1.2% f/c) and strong fall in US housing starts (Apr -3.7% vs -0.7% f/c and upward-revised March figure from 1.9% to 3.6%).

Fresh weakness commenced after three-day rally stalled at 1.2924 and tested top of narrowing daily cloud (1.2810) so far.

Cloud twists next week (1.2765) and may attract for further weakness, with return below converged 10/20/55SMA and 14-d momentum breaking into negative territory, supporting the notion. Return into daily cloud and close below 1.2803 (Fibo 61.8% of 1.2729/1.2924 recovery leg) would generate fresh bearish signal and risk deeper fall.

Next support lays at 1.2766 (30SMA) ahead of key near-term support at 1.2729 (11 May trough), loss of which would confirm reversal on completion of daily failure swing pattern.

Res: 1.2833; 1.2844; 1.2876; 1.2924

Sup: 1.2803; 1.2766; 1.2729; 1.2706

Sunset Market Commentary

Markets:

Core bonds traded mixed today. The German Bund gained ground while the US Note future more or less flat-lined. Bunds profit from European safe haven flows. Italian media reported that 5SM & Lega, who are on the brink of a coalition deal, discussed a €250bn debt forgiveness plan. More specifically, they eye government debt held by the ECB under its asset purchase programme. Both parties in a joint statement denied that this was the latest version of the proposal, but the news suggests that they might hold on to some of their more radical ideas apart from favouring huge fiscal stimulus. The news sent a shiver through the BTP market. Italian yields rose by 15 bps to 10 bps, bear flattening the Italian yield curve. The Italian 10-yr yield spreads adds 16 bps. There’s some spill-over effect to other peripherals with the Greek spread 26 bps higher and the Spanish/Portuguese one 7 bps. German Chancellor Markel unfortunately (?) added fuel to the fire while calling for structural reforms because the ECB’s ultra-easy monetary policy won’t last forever. German yields decline by 2.2 bps (2-yr) to 4.6 bps (5-yr & 10-yr) at the time of writing. The US yield curve flattens with yield changes varying between +0.2 bps (2-yr) and -1.5 bps (30-yr). US yields remain below key resistance levels (3.07% 10yr & 3.22% 30yr) despite strong April industrial production data and comments by Atlanta Fed Bostic who’s gradually shifting from being in favour of 2-3 rate hikes this year to 3-4.

After a pause late last week and on Monday, EUR/USD resume its downtrend. The move was mainly due to broad-based USD strength, supported by higher US yields. The 1.1820/25 support area came within reach. This morning, the rise of the dollar/decline of the euro looked like taking a breather. However, the calm didn’t last long. Mid-morning, EUR/USD tumbled lower again. The move was triggered by press headlines on some unconventional measures that might be part of the program of a 5SM/Lega government in Italy. The coalition parties downplayed the headlines, but couldn’t restore market confidence. The impact on markets outside Italy remains modest. However Italian equities and BTP’s underperformed and there was some fall-out on the single currency. EUR/USD dropped below the 1.18 big figure. The USD/JPY rally also ran into resistance contrary to the buoyant performance of late. Investor caution restored the balance between the dollar and the safe haven yen. USD/JPY is drifting back to the low 110 area. US eco data (housing starts, permits and production) were close to expectations with limited impact on USD.

There were no important eco data in the UK today. Sterling trading was mostly technical in nature. The UK currency strengthened against the euro as the single currency suffered from political uncertainty on the program of a populist Italian government. The decline of EUR/USD also dragged EUR/GBP lower. EUR/GBP further reversed the post-BoE rise. The pair trades in the 0.8740 area. Cable (high 1.34 area) is holding near recent lows as uncertainty on Brexit and relative USD strength are weighing on this cross rate. The UK government promised to publish a detailed plan next month on the nature of their relationship with the EU post-Brexit. There is an important EU summit on June 28.

News Headlines:

The Turkish lira reversed a drop to a record low (EUR/TRY 5.2 from 5.3) after the central bank said it was monitoring markets and would take necessary steps, a sign policy makers are getting closer to action to stem a rout. (BB)

The Polish central bank kept its interest rate unchanged at 1.5%, as expected. Central bank governor Glapinski and two other MPC members will holds a press conference at 4pm CET.

UK PM May has announced plans to publish a Brexit white paper ahead of a key European Council meeting next month, setting out for the first time in detail what Britain is seeking from its future relationship with the EU. (FT)