Sample Category Title

France PMI manufacturing revised up to 53.8, growth rate broadly unchanged after three months of softening

France PMI manufacturing was finalized at 53.8 in April, revised up from 53.4. Markit noted that overall growth broadly unchanged having slowed in previous three months. Rates of expansion in output and employment quicken. And, inflationary pressures remain elevated.

Comments from Alex Gill, Economist at IHS Markit:

"Having softened in the previous three months, the rate of growth in the French manufacturing sector was broadly unchanged at the start of the second quarter. Encouragingly, output and employment rose at sharper rates than in March.

"On a less positive note, the pace of expansion in new orders continued to moderate, in turn leading to the weakest degree of business confidence for seven months.

"The slowdown in client demand growth seen since the start of 2018 can be partially linked to poor weather conditions, while the recent train strikes may also have played a part. The degree to which these factors can explain the slowdown or whether the cause is something of greater concern will become more apparent in the coming months."

EURUSD Intraday Analysis

EURUSD (1.2005): The EURUSD currency pair was seen testing fresh monthly lows on Tuesday. The common currency touched lows of 1.1981 before recovering only modestly. The breakdown below the 1.2090 - 1.2070 level indicates that any near-term gains would be limited to this level where resistance could be established. The 4-hour Stochastics remains in the oversold region which indicates a potential rebound in prices in the near term.

Eurozone GDP And FOMC Meeting In Focus

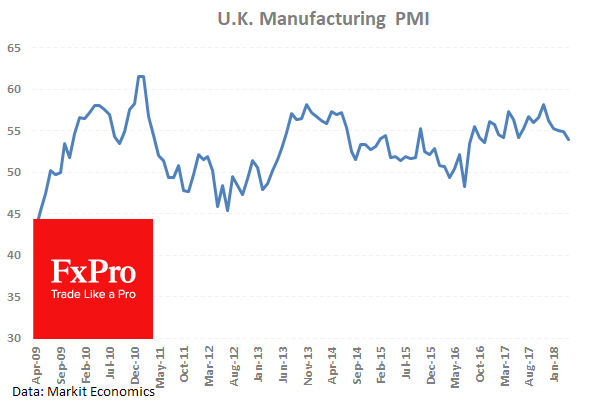

The U.S. dollar was seen maintaining the bullish momentum on the day. European markets were closed on account of the 1st May bank holiday. Economic data showed that the UK’s manufacturing PMI was weaker than expected at 53.9.

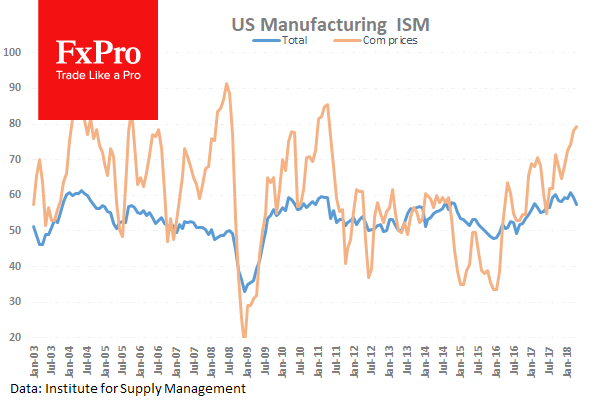

In the U.S. the ISM manufacturing PMI was seen falling to 57.3 missing forecasts of 58.4 and slower than the March PMI reading of 59.3.

On the political front, the U.S. administration was seen exempting South Korea, Mexico, Canada and the EU from the steel and aluminum tariffs that were due to come into effect from the 1st of May. However, the exemption is not long term as the U.S. only delayed the tariffs by 30 days for the above nations.

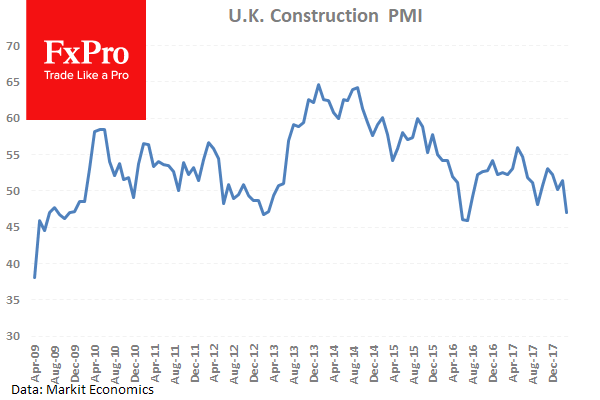

Looking ahead, the economic calendar today will mark the release of the UK's construction PMI data which will conclude the monthly PMI's for April. Economists forecast that the UK's construction activity slightly improved to 50.5 after falling into contraction the month before.

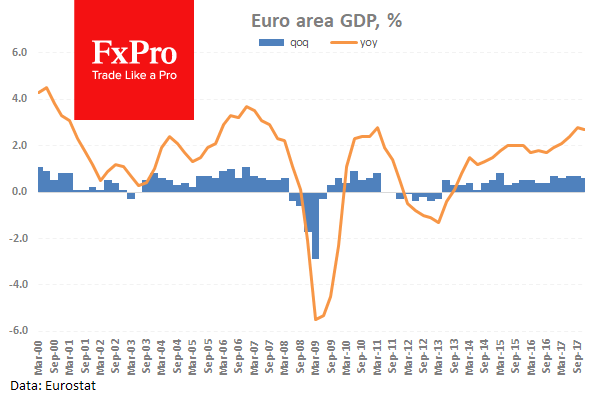

The Eurozone will be releasing the manufacturing and services PMI data for the month of April. No major changes are expected but activity is expected to remain subdued. The flash GDP estimates for the first quarter will also be released this week. The Eurozone GDP is forecast to rise 0.4% on the quarter, marking a slower pace of increased from 0.6% in the previous quarter.

The FOMC statement will take center-stage today. No changes are expected to the short-term interest rates. There will be no press conference or any economic projections.

Italy PMI manufacturing dropped to 53.5, growth took another tumble

Italy PMI manufacturing dropped to 53.5 in April, down from 55.1, below expectation of 54.5. Markit noted that Weaker domestic market conditions restrict growth, both output and new orders rise at slower rates and, further job gains leads to slight fall in backlogs.

Comments from Paul Smith, Director at IHS Markit:

"Growth of Italy's manufacturing sector took another tumble during April, with output and new orders both increasing at noticeably slower rates.

"A third successive monthly fall in the headline PMI represents a clear turning point in growth since the start of the year and cannot simply be attributed to Q1's weather-related disruptions.

"On the contrary, anecdotal evidence in recent months has pointed to global supply-side constraints as a factor limiting growth, and these issues in April were exacerbated by increased weakness in domestic market conditions.

"These issues have undermined confidence about the future as well, although one bright spot remains the export market where demand for Italy's high end capital goods continues to flourish."

GBPUSD Medium-Term Bearish Below 1.3665 Level

The British pound continues to trade to the downside against the U.S dollar, after weaker than expected UK Manufacturing data caused the pair to tumble below the 1.3600 level. The GBPUSD pair currently trades just above the 1.3600 level, after finding interim technical support from the 1.3587 level, following Tuesday’s large decline. Traders now look towards more important economic data from the United Kingdom, with UK Services and Construction PMI data set to be released during the European trading session.

The GBPUSD pair is strongly bearish while trading below the 1.3655 level, further losses towards 1.3587 and 1.3550 remain likely.

If the GBPUSD pair moves back above the 1.3655 level, buyers may push price-action back towards the 1.3710 level.

EURUSD 200-Day Moving Average In Focus

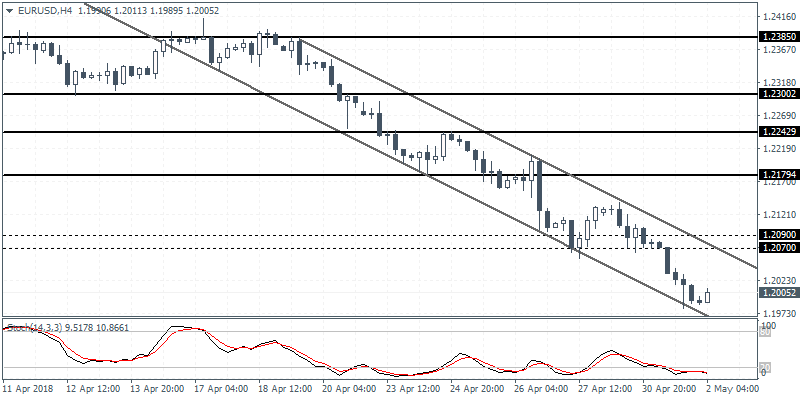

The euro currency has fallen sharply lower against the greenback, hitting 1.1980, after the U.S dollar index strengthened broadly on the first trading day of May. The EURUSD pair currently trades around the 1.2000 level, with traders now turning their attention to further losses below the pair’s 200-day moving average, at 1.2010. Investors now look towards a raft of key eurozone economic data this morning, with PMI Manufacturing and the official EU Unemployment rate headlining.

The EURUSD pair is strongly bearish while trading below the 1.2054 level, further losses towards 1.1980 and 1.1955 appear likely.

If the EURUSD pair starts to trade back above the 1.2054 resistance level, a technical correction back towards the 1.2100 and 1.2138 levels may occur.

Ethereum Falls As Regulatory Fears Return

In 2017, cryptocurrencies were the best performing asset class, with many currencies gaining by more than 1000%. This year, the trend has been somewhat broken as traders start to worry about scrutiny from regulators.

So far, there have been no major crypto-related regulations in the United States. Other countries like China have ordered the shutdown of cryptocurrency exchanges while South Korea has implemented a thorough scrutiny of the exchanges. In the US, the Commodity Futures Trading Commission (CFTC) has ruled that bitcoin is a commodity and should therefore be subject to the same rules applicable to all participants in the commodity derivatives market.

Yesterday, the Wall Street Journal reported that the Securities and Exchange Commission (SEC) was looking at whether cryptocurrencies like ethereum should be regulated as securities. Regulators are due to meet on 7 May 2018 to discuss the matter further.

If cryptocurrencies such as ethereum are viewed as securities, they will be required to adhere by all the guidelines set by the SEC. Traders fear that such regulations, coming from the biggest economy, would lead to increased selling, affecting their prices. Just last week, J. Christopher Giancarlo, the Chairman of the CFTC called ethereum and ripple non-compliant securities.

As a result of regulatory fears, the price of ethereum dropped sharply from $700 to $618 yesterday. Today, the pair has recovered some of the losses and is trading at $665. The pair will likely remain under pressure as traders wait for the final ruling on the classification of the virtual currency.

US Payrolls Data In The Spotlight On Wednesday

US employment data is in the headlines on Wednesday, kicking off a highly active second half of the week that will be dominated by American releases. The conclusion of the Federal Reserve's two-day policy meeting will also draw interest from traders all over the world.

The economic calendar picks up at 07:15 GMT with a report on Spanish manufacturing PMI. Over the next hour, investors can expect final April PMI numbers for Italy, France, Germany and the broader Eurozone.

The Eurozone manufacturing PMI is forecast to come in at 56 for April. Germany's manufacturing gauge likely registered 58.1.

Eurostat, the European Commission's statistical agency, will report on gross domestic product at 09:00 GMT. Eurozone GDP is forecast to grow 2.5% annually in the second quarter compared with 2.7% in Q1. On a quarterly basis, the euro area economy is forecast to grow 0.4% compared with 0.6% in Q4.

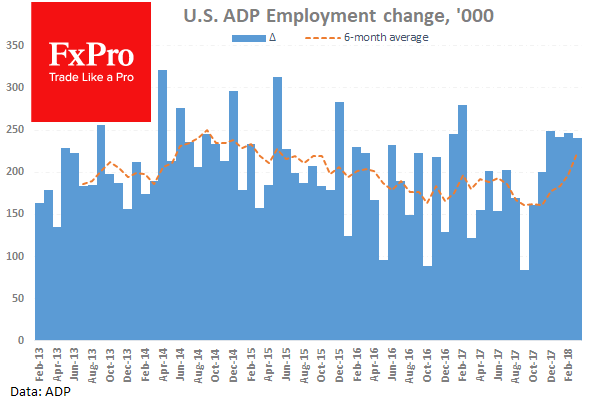

Shifting gears to North America, the ADP payrolls institute will report on US private sector job creation at 12:15 GMT. Employers are forecast to have added 215,000 private sector jobs last month, compared with 241,000 in March.

ADP numbers are considered an accurate gauge of the official nonfarm payrolls report due 48 hours later.

The Federal Open Market Committee (FOMC) will conclude its policy meeting on Wednesday, where officials are widely expected to leave interest rates on hold. The official rate statement is due at 18:00 GMT. Although no change in policy is expected, the Fed could provide some guidance on its plans for June and beyond.

Last week, the Commerce Department reported the biggest quarterly surge in core inflation since 2007, all but assuring investors that higher interest rates are looming over the horizon.

EUR/USD

Europe's common currency fell further into correction on Tuesday, as the EUR/USD broke below 1.200 for the first time since January. The pair, which is now trading around 1.2004, has crossed below the 200-day simple moving average (SMA). For traders, this is a strong signal that further downside risks are in store.

GBP/USD

Cable also fell on Tuesday as the dollar extended its recovery against a basket of global peers. GBP/USD was last trading around 1.3615, which is not far from Tuesday's swing low. The pair is currently hovering at three-month lows, having declined a staggering 750 pips from last month's high.

USD/JPY

The USD/JPY made a strong push toward 110 on Tuesday but failed to cross that psychological barrier. The pair is currently trading at 109.66, where it has declined 0.2% from the previous session. At the time of writing, the pair remains rangebound in the 1.0900 region with fundamental factors needed to drive prices significantly higher or lower.

Dollar FX Pairs At Key Levels Ahead Of Fed Interest Rate Decision

The USD is unwinding some of its moves from yesterday, with the EURUSD back above 1.20000 and GBPUSD back above 1.36000. Trading overnight was sluggish but some pairs are at decisive levels, with the AUDUSD back above 0.75000 and NZDUSD back above 0.70000, as New Zealand jobs data came in largely as expected. The market is awaiting the FOMC Monetary Policy Statement and Rate Hike this evening, with a hawkish hold expected. After falling yesterday, Indices rebounded late in the US trading session but Asian indices are lower again this morning. Gold has bounced off support close to the $1300.00 level.

UK Markit Manufacturing PMI (Apr) came in at 53.9 v an expected 54.8, from 55.1 prior, which was revised down to 54.9. This miss sent the data point to a seventeen-month low, continuing to soften from the high created in December at 58.2. This is despite a beat in the previous two readings. Seasonally, Q1 is a time where this data point has tended to weaken over the last few years. Slower output growth was a factor cited in the weakening number, despite stronger new order inflows, strengthening job creation and demand. Also released at this time were UK Mortgage Approvals (Mar) which came in at 62.914K, softer than the 63.000K expected and down against a previous reading of 64.000K, which was revised down to 63.781K. GBPUSD fell from 1.37308 to 1.36661 after the data release.

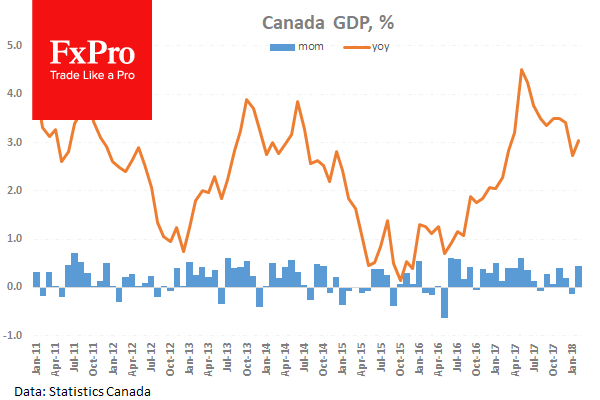

Canadian Gross Domestic Product (MoM) (Feb) was 0.4% against an expected 0.3%, from -0.1% prior. This data shows that growth remains in expansion and is turning higher from last month’s low. USDCAD fell from 1.38667 to 1.38312 after being moved by this release.

US ISM Prices Paid (Apr) came out at 79.3 against a consensus of 78.3, from a previous reading of 78.1. This shows a continued increase in the cost of goods and services. ISM Manufacturing PMI (Apr) was also out at this time coming in at 57.3 against an expectation of 58.4, from 59.3 prior. This number is falling after reaching a high of 60.8 in February. Finally, Construction Spending (MoM) (Mar) was down at -1.7% against an expected 0.5%, from the previous reading of 0.1%. EURUSD fell from 1.20200 to a low of 1.19810 following the data release.

EURUSD is up 0.09% overnight, trading around 1.20021.

EURUSD is up 0.09% overnight, trading around 1.20021.

USDJPY is down -0.09% in early session trading at around 109.765.

GBPUSD is down -0.06% this morning, trading around 1.36047.

Gold is up 0.41% in early morning trading at around $1,309.10.

WTI is unchanged this morning, trading around $67.50.

US Fed Expected To Maintain A Hawkish Hold On Rates

At 08:30 GMT, UK Construction PMI (Apr) will be out with an expected headline number of 50.5 from 47.0 prior. The consensus is for a recovery in the numbers today, after a softening from the high created in December at 53.1. The industry has slipped below 50.0 from the high level of 64.6 reached in 2014, showing a contraction in the index. GBP pairs may see an impact from this data release.

At 09:00 GMT, Eurozone Unemployment Rate (Mar) is expected to be unchanged at 8.5%. The Unemployment Rate is expected to remain in line with last month’s reading, at a level not previously seen since April 2009. Gross Domestic Product s.a. (QoQ) (Q1) is expected to be 0.4% against 0.6% previously. Gross Domestic Product s.a. (YoY) (Q1) is expected to be 2.5% against 2.7% previously. GDP estimates are also down on the previous reading but, as these are quarterly figures, the decline can be explained somewhat by severe weather in Europe. EUR crosses may be impacted by this data release.

At 12:15 GMT, US ADP Employment Change (Apr) is expected to be 200K against 241K previously. This data has remained above 200 for the last four months, showing that the US economy is continuing to add jobs, but this reading is expected to show a decline to that number today. USD pairs may be moved by this data.

At 15:30 GMT, German Buba President Weidmann will deliver a speech titled “Central bank communication as a Monetary Policy Instrument” at the Centre for European Economic Research, in Mannheim. EUR crosses may be moved by this data.

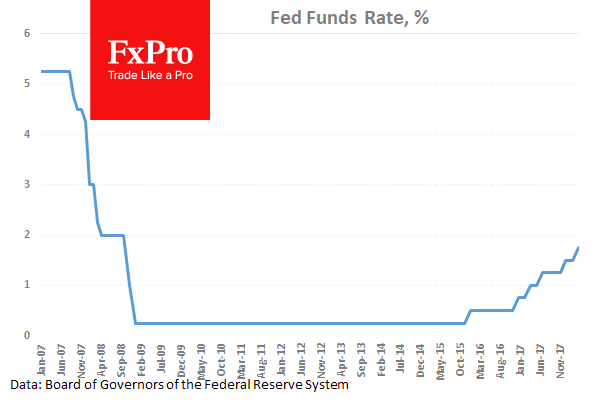

At 18:00 GMT, The US Fed’s Monetary Policy Statement and Interest Rate Decision will be released, with the rate expected to be left unchanged at 1.75%. The hike in rates in March had been more or less priced into markets and marked the first in a series of expected increases in 2018. The market is pricing in two to three hikes in 2018, with a slight bias for three to four that could strengthen the dollar position. The Monetary Policy Statement is expected to set a hawkish tone and may catch some in the market off guard. There will not be an FOMC Press Conference after this event. USD crosses may experience volatility during this time.