Sample Category Title

Currencies: EUR/USD Rebound To Slow Post-Fed Minutes

- Rates: Geopolitical tensions protect downside bonds short term

Risk sentiment will probably set the tone for trading. Rising geopolitical risks suggest short term downside protection for core bonds. Today's eco calendar won't move trading, but speeches by ECB Weidmann and Coeuré are wildcards. Will they follow fellow-hawk Nowotny who went off script on Tuesday, arguing in favour of a deposit rate hike soon after ending APP? - Currencies: EUR/USD rebound to slow post-Fed Minutes

Yesterday, the dollar remained in the defensive for most of the day. However, the US currency found a better bid after the publication of the Fed minutes. Is this a harbinger that the EUR/USD rally will slow? Today, the eco data will probably be only of intraday significance for USD trading. Geopolitics will remain a wildcard

The Sunrise Headlines

- US stock markets ended mixed with Dow (-0.25%) underperforming (energy stocks, lower oil price) and Nasdaq (+0.9% ahead of Apple earnings) outperforming. Asian equities record small losses overnight.

- A Tory fraction is considering withdrawing support for government bills in Parliament in opposition of the post-Brexit plans for a customs partnership with the EU, the Telegraph reports, citing unidentified sources.

- Special Counsel Mueller, in a meeting with US President Trump's lawyers in March, raised the possibility of issuing a subpoena for Trump if he declines to talk to investigators in the Russia probe, a former lawyer for the president said.

- The Chinese Caixin manufacturing PMI unexpectedly picked up in April (51.1) as output quickened slightly, though a decline in export orders reinforced risks to the outlook as firms continued to shed staff while inventories also rose.

- Apple flexed its financial muscle with a record $100 billion plan to buy back stock from investors, as it reported strong gains in revenue and profit even as growth in the number of iPhones sold remained weak. (WSJ)

- S&P lowered Turkey’s foreign currency credit rating to BB-, citing the deteriorating inflation outlook, the long-term depreciation and volatility of the nation’s exchange rate and the risk of a hard landing.

- Tonight’s Fed meeting takes center stage today. Data on offer include US ADP employment report, EMU Q1 GDP, EMU unemployment rate and final manufacturing PMI. Germany holds a Bobl auction and ECB Weidmann speaks.

Currencies: EUR/USD Rebound To Slow Post-Fed Minutes

FOMC statement: upbeat inflation assessment?!

The Bund didn’t trade yesterday with German markets closed for Labour Day Holiday. The US Note future lost marginally ground in a low-volume trading session ahead of tonight’s FOMC Meeting. Lower oil prices and a bigger-thanexpected setback in the US manufacturing ISM (57.3 from 59.3 vs 58.3 forecast) didn’t play a role of importance. The US yield curve bear flattened with yields 1.5 bps (2-yr) to 0.5 bps (30-yr) higher. The US 2-yr yield closed above 2.5% for the first time since August 2008. The US 5-yr yield sits close to the highest levels since 2009.

Most Asian stock markets trade with small losses, underperforming WS. The US Note future loses more ground while the dollar is mixed. We expect the Bund to open somewhat weaker in a catch-up move.

The FOMC meeting takes center stage today. We expect no policy changes. The market implied probability of a 25 bps rate hike stands at 35%, suggesting room for consolidation at the front end of the US yield curve. We think that the inflation assessment in the policy statement will be upgraded, adapting to most recent PCE prints (2% for headline and 1.9% for core). The soft Q1 GDP reading will likely be labeled transitory. The Fed will normally also flag a June rate hike. Overall, we thus expect the statement to boost chances of 3 additional rate hikes this year, our favoured scenario which should sustain the longer term uptrend in US yields. The immediate market reaction could be more muted as the above outlined scenario is probably discounted. The probability of 3 more hikes this year yesterday rose above the probability of 2 moves (current FOMC median) for the first time (37% vs 35%). Apart from the Fed meeting, Q1 EMU GDP data and ADP employment will be published.

The recent core bond sell-off lifted US yields towards key resistance in the 10- yr (3.05%/3.07%) and 30-yr yield (3.22%). A new surge in US price indicators or inflation expectations is probably necessary to trigger a real test. The German 10-yr yield bounced off key support levels (0.46%/0.48%), suggesting the start of a new upleg towards 0.8%. Last week’s ECB meeting shouldn’t be a structurally hampering factor. US 2-yr yield closes above 2.5% resistance for the first time since 2008 on the eve of the FOMC meeting

US 2-yr yield closes above 2.5% resistance for the first time since 2008 on the eve of the FOMC meeting

Equities Remain Quiet Ahead Of US Fed Meeting

General Trend:

- Asian equity markets trade mixed as various markets return from holiday

- Australia ASX 200 outperforms: Qantas rallies over 6% after guidance

- Australian retailer Woolworth’s expects deflation related to fruit and vegetable prices to remain high in Q4

- Aluminum producer Rusal rises over 4% after reprieve from US Treasury Dept.

- Standard Chartered Q1 adj pretax shy of ests

- HK-listed gaming companies trade higher on April Macau Casino Revs

- US equity futures trade mixed as traders digest Apple’s results and US political risks; Fed decision expected later on Wed

- Commodities trade generally higher ahead of Fed meeting; Silver Futures up over 1%

- China conglomerate HNA Group reports 2017 results

- China April Caixin PMI manufacturing export orders sub-index declines for first time since 2016

- South Korea April PMI contracts for 2nd straight month, hits 1-year low

- South Korea sells 30-year bonds at higher yield

- Japan monetary base rises at slowest pace since 2012

- USD/JPY trades below ¥110.00 ahead of upcoming Fed decision

- Japanese equity markets are closed on Thursday and Friday (May 3-4th)

- Trade talks between US/China due to begin on Thursday

- RBA Gov Lowe suggests no large changes in forecasts due for release on Friday

- PBOC sets weaker yuan setting ahead of US trade delegation visit

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.3%; closed -0.2%

- TOPIX Real Estate index -1.3%, Information/Communications -0.7%, Securities -0.4%, Retail Trade -0.3%; Marine Transportation +0.3%

- Automakers trade lower after release of monthly US auto sales

- Shares of Yamato Holdings [9064.JP] and Japan Tobacco [2914.JP] rise over 5% following their respective earnings reports

- (JP) Support for PM Abe revising constitution declines to 30% - Asahi Poll

- (JP) Japan govt plans to delay primary budget surplus target by five years to fiscal 2025 - Nikkei

- (JP) Japan Govt said to be considering fiscal FY25 as its new target for fiscal consolidation – Nikkei

- (JP) JAPAN APR PMI COMPOSITE: 53.1 V 51.3 PRIOR; SERVICES: 52.5 V 50.9 PRIOR (6-month high)

- Itochu, 8001.JP Reports FY17/18 Net ¥400.3B v ¥352.2B y/y; Op ¥316.9B v ¥288.4B y/y; Rev ¥5.51T v ¥4.84T y/y

Korea

- Kospi opened 0%

- (KR) SOUTH KOREA APR CPI M/M: 0.1% V 0.1%E; Y/Y: 1.6% V 1.5%E

- Samsung Biologics, [-15%], 207940.KR Financial Supervisory Service (FSS) finds accounting violation

- (KR) South Korea Apr PMI Manufacturing: 48.4 v 49.1 prior

- (KR) South Korea President Spokesperson: US troops in South Korea are not related to peace treaty with North Korea

- (KR) Bank of Korea sells KRW2.3T in 2-yr bonds; avg yield 2.145%

- (KR) South Korea sells KRW1.85T in 30-yr bonds, avg yield 2.75% v 2.66% prior

- (KR) South Korea Finance Min Kim: Most worried about jobs data recently

China/Hong Kong

- Hang Seng opened -0.1%, Shanghai Composite +0.2%

- Hang Seng Materials index -1.7%, Financials -1.2%, Property/Construction -1%; Services +1.6%

- (CN) China may soon release policies aimed at boosting consumption - China Daily

- (CN) China PBoC sets yuan reference rate at 6.3670 v 6.3393 prior (weakest setting since Jan 25th)

- (CN) China PBoC Open Market Operation (OMO): Injects CNY200B in 7-day reverse repos v CNY40B prior; Net: drains nil v nil prior

- (CN) CHINA APR CAIXIN PMI MANUFACTURING: 51.1 V 50.9E; Export orders sub component falls for the first time since Nov 2016

- (HK) Hong Kong 3-month HIBOR rises to 1.61607% (highest level since 2008, 13th consecutive daily increase)

- (US) US Treasury: Extends deadline for divestiture or transfer of debt and other financial holdings of sanction targets EN+, GAZ and Rusal to June 6th

Australia/New Zealand

- ASX 200 opened 0%, closed +0.6%

- ASX 200 Consumer Discretionary index +1.4%, REIT +0.7%, Utilities +0.6%, Financials +0.4%

- JB-HiFi,[-8%] JBH.AU Reports Q3 Rev +6.8% v 10.8% y/y; cuts FY18 guidance

- Woolworths, [+0.7%], WOW.AU Reports Q3 Rev A$14.2B v A$13.7B y/y

- Qantas[+6%], QAN.AU Reports Q3 (A$) Rev 4.25B, +7.5% y/y; Affirms FY18 guidance

- (NZ) NEW ZEALAND Q1 UNEMPLOYMENT RATE: 4.4% V 4.4%E;EMPLOYMENT CHANGE Q/Q: 0.6% V 0.6%E; Y/Y: 3.1% V 3.3%E

- (AU) Fitch affirms Australia sovereign rating at AAA; Outlook Stable

- (AU) Australia sells A$400M v A$400M indicated in 3.00% March 21 2047 bonds, avg yield 3.2741% v 3.3268% prior, bid to cover 3.06x v 3.00x prior

- (AU) Australia PM Turnbull: Free trade and open markets are good for jobs; Have signed cyber co-operation agreement with France

- (AU) Reserve Bank of Australia (RBA) Gov Lowe speaks at board dinner: latest forecasts due to be released Friday should not contain any surprises with only small changes from last set of forecasts

Other Asia

- (ID) Indonesia Central Bank: To purchase more government bonds in secondary market; seeks to stabilize domestic bond market

- (TW) Taiwan Apr PMI Manufacturing: 54.8 v 55.3 prior (6-month low)

- (TW) Taiwan said to plan to ease impact of rising retail gasoline prices – Local Media

- Taiwan Semi [2330.TW]: Nanjing plant said to have started mass production - Taiwanese Press

North America

- US equity markets ended mostly higher: Dow -0.3%, S&P500 +0.3%, Nasdaq +0.9%, Russell 2000 +0.6%

- S&P500 Technology +1.3%; Consumer Staples -0.9%

- Apple’s [AAPL] shares rise over 3% in the afterhours following results and announcement regarding shareholder returns

- Xerox [XRX]: Confirms Reaches Agreement with Carl Icahn and Darwin Deason: Keith Cozza of Icahn Enterprises to be Named Chairman; John Visentin to be Named Vice Chairman and CEO; to immediately discuss strategic alternatives

- (US) Special Counsel Mueller said to have raised possibility of subpoena if President Trump declines to talk to investigators in the Russia probe - Washington Post

- (US) White House Trade Adviser Navarro: every country granted an exemption from the steel and aluminum tariffs would still face an import quota and other restrictions - press

- (US) Crop Tour said to project Northern Kansas Wheat yield at 38.2 BU/acre v 43.0 y/y - US financial press

- (US) Weekly API Oil Inventories: Crude: +3.4M v +1.1M prior

Europe

- (UK) Prime Min May reportedly may endorse hybrid customs partnership – FT; Also PM May has been warned her government will "collapse" if she does not abandon plans for a post-Brexit customs partnership with the EU.

- (EU) EU plans to raise budget contribution to 1.14% of economic output - German press

- (TR) S&P cuts Turkey sovereign rating one notch to BB- from BB; outlook to Stable from Negative

Levels as of 02:00ET

- Hang Seng -0.7%; Shanghai Composite -0.4%; Kospi -0.5%

- Equity Futures: S&P500 -0.1%; Nasdaq100 +0.2%, Dax +0.2%; FTSE100 -0.1%

- EUR 1.2011-1.1987; JPY 109.92-109.65; AUD 0.7507-0.7475;NZD 0.7026-0.6992

- Jun Gold +0.3% at $1,310/oz; Jun Crude Oil +0.5% at $67.55/brl; Jul Copper +0.8% at $3.07/lb

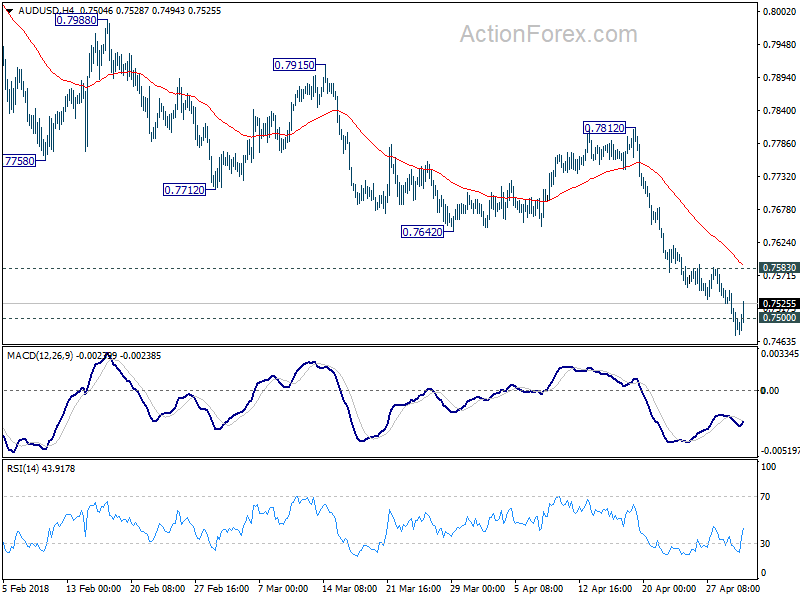

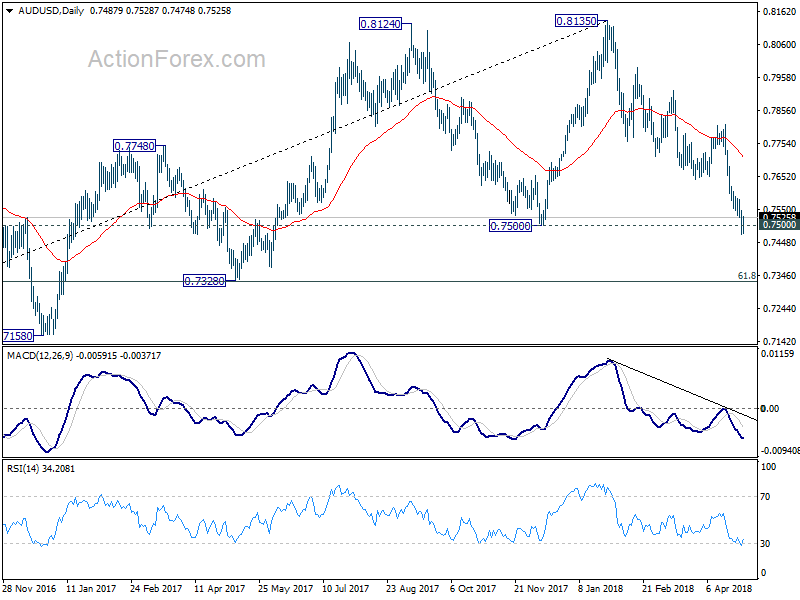

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7457; (P) 0.7502; (R1) 0.7531; More...

Deeper decline is expected in AUD/USD as long as 0.7583 minor resistance holds. Sustained break of 0.7500 key support level will indicate medium term reversal and target next support at 0.7328. Nonetheless, break of 0.7583 will suggest short term bottoming. In that case, stronger rebound would be seen back to 0.7642 support turned resistance.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Decisive break of 0.7500 key support will suggest that such correction is completed. In that case, deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

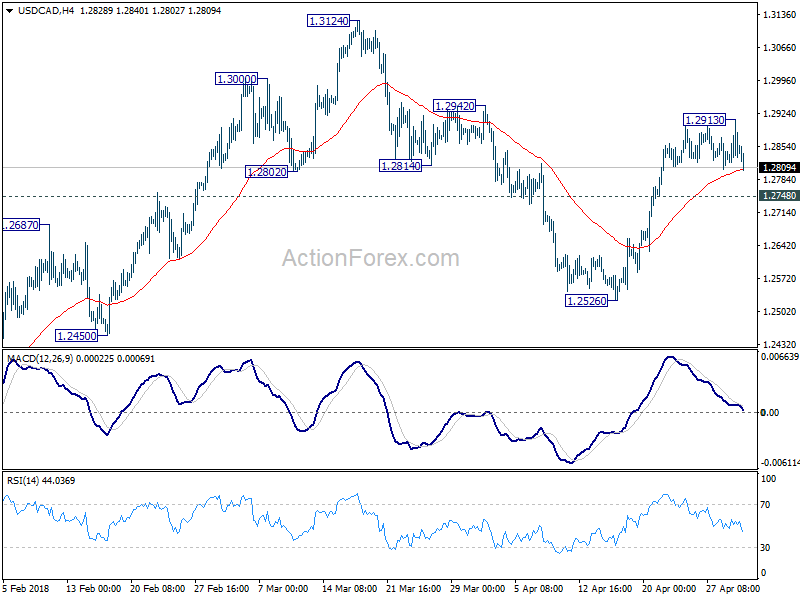

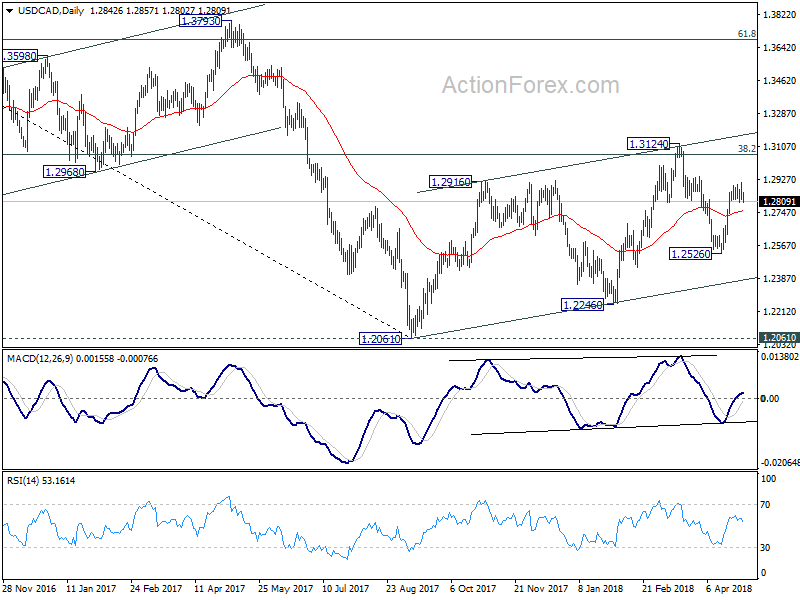

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2808; (P) 1.2860; (R1) 1.2902; More....

Despite edging higher to 1.2913, USD/CAD quickly retreated with 4 hour MACD staying below signal line. Intraday bias is turned neutral again for consolidations. For now, further rally is expected as long as 1.2748 minor support holds. Above 1.2913 will extend the rise from 1.2526 to retest 1.3124 high. However, break of 1.2748 will turn focus back to 1.2526 instead.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685.

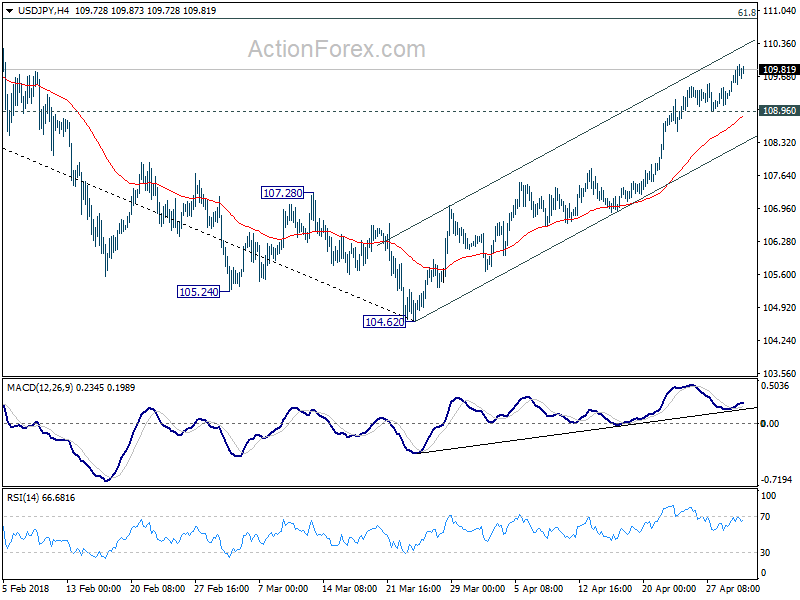

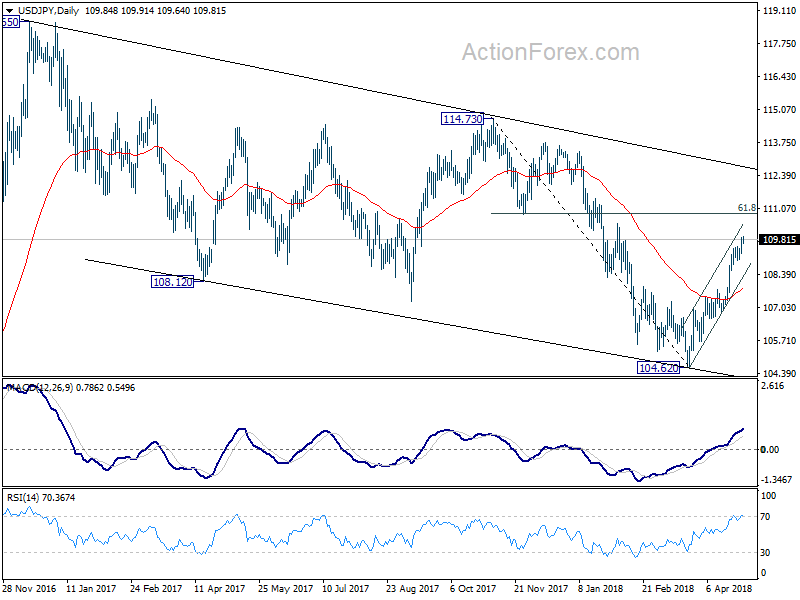

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.43; (P) 109.65; (R1) 110.09; More...

Intraday bias in USD/JPY remains on the upside at this point. Current rise from 104.62 should target 61.8% retracement of 114.73 to 104.62 at 110.86 next. On the downside, below 108.96 will turn intraday bias neutral again and bring consolidations.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.78).

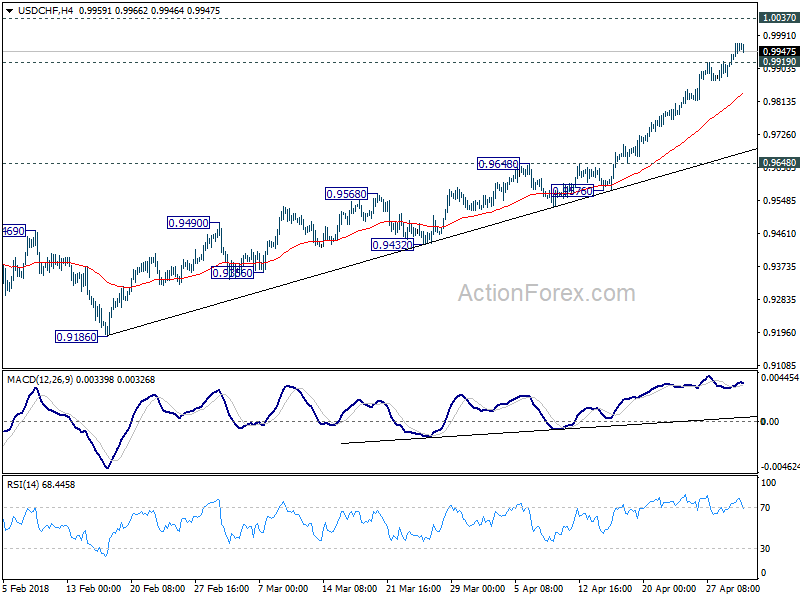

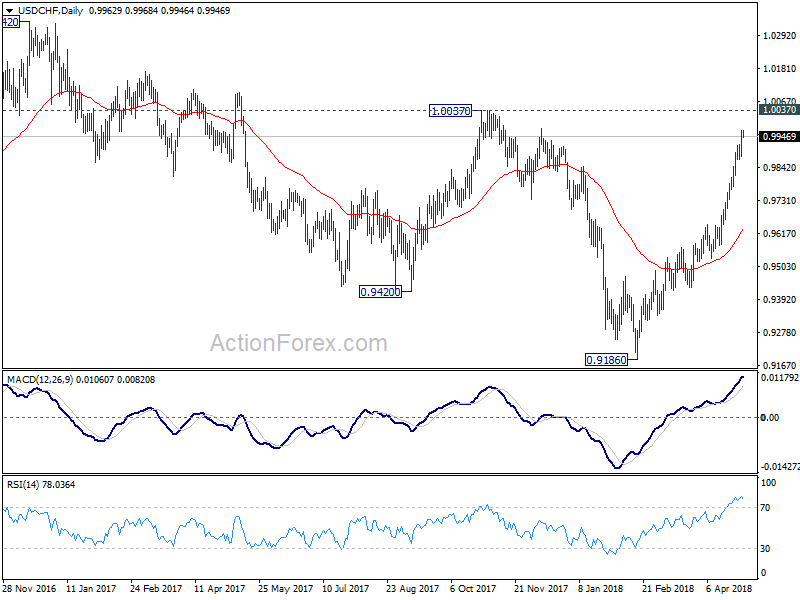

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9916; (P) 0.9943; (R1) 0.9992; More...

Intraday bias in USD/CHF remains on the upside and current rise from 0.9186 is in progress for 1.0037 resistance. Decisive break there will pave the way to key resistance level at 1.0342. On the downside, below 0.9919 minor support will turn intraday bias neutral again and bring consolidation, before staging another rise.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 0.9648 resistance turned support holds, even in case of pull back.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3544; (P) 1.3658; (R1) 1.3729; More...

GBP/USD reaches as low as 1.3579 so far and there is no sign of bottoming yet. Intraday bias remains on the downside and fall from 1.4376 should target 1.3448 fibonacci level next. On the upside, above 1.3665 minor resistance will turn intraday bias neutral first. Some consolidations could then be seen before another decline.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4248). Deeper decline should be seen to 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3955) holds, even in case of strong rebound.

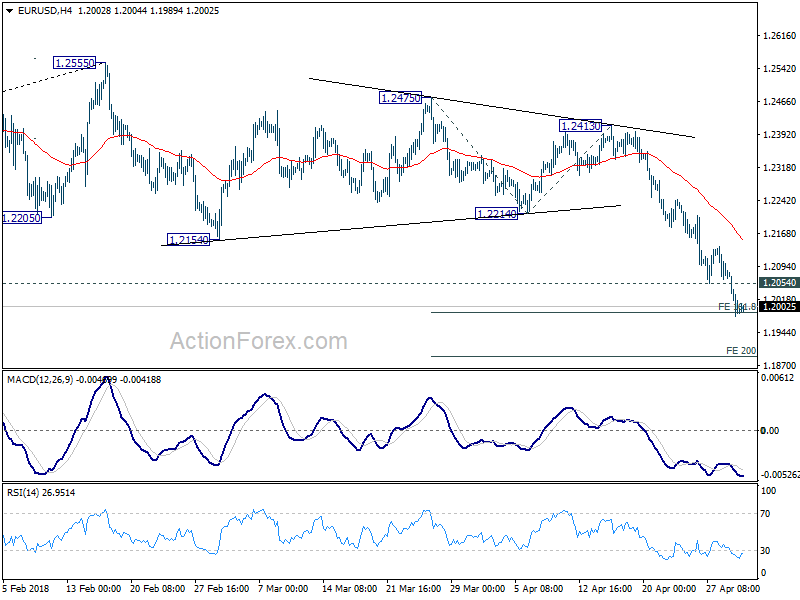

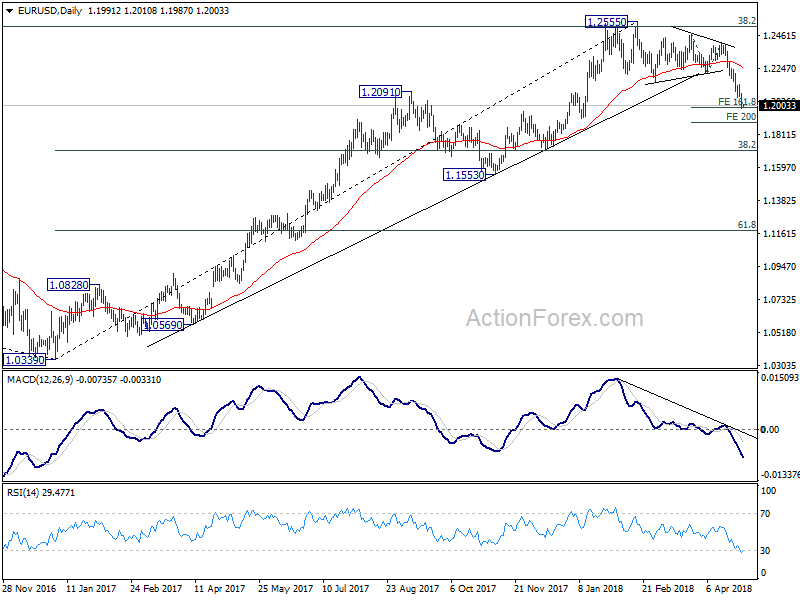

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1953; (P) 1.2018 (R1) 1.2056; More....

EUR/USD's fall is still in progress and is pressing 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991. Intraday bias remains on the downside and firm break of 1.1991 will target 200% projection at 1.1891 next. On the upside, above 1.2054 minor resistance will indicate temporary bottoming and turn bias neutral for consolidations. But upside of recovery should be limited well below 1.2214 support turned resistance to bring another decline.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Dollar Firm as FOMC Awaited, Euro and Sterling Shaky ahead of GDP and PMI

After yesterday's strong rally, Dollar retreats mildly today as markets await FOMC decision. For the week, the greenback remains the strongest one. Canadian Dollar follows as the second strongest, riding on better than expected GDP data. Sterling, on the other hand, is trading as the weakest one, as weighed down by disappointing PMI manufacturing. More tests are lining up there for the Pound with today's PMI construction and tomorrow's PMI services. New Zealand dollar is the second weakest for the week despite position employment data released today.

Technically, GBP/USD took out 1.3711 key support level yesterday while AUD/USD breached 0.7500. These developments solidified the case of medium term reversal in Dollar. Now that 1.2 handle is breached in EUR/USD, focus will be on whether there is further downside acceleration. In particular, Eurozone Q1 GDP will be a downside risk for the Euro.

Fed to leave rate hike for June FOMC meeting

There have been both positive and negative data released from the US since the March FOMC meeting. We expect policymakers to view slowdown in GDP growth as driven by temporary factors which should not affect the monetary policy outlook. Meanwhile, the central bank would likely acknowledge recent pickup in core inflation and wage growth, hailing them as reasons supporting further gradual rate hike: The median dot plot suggested three rate hikes this year while the market has increasingly priced in four. We expect the Fed to leave the policy rate unchanged at 1.50-1.75% at today's meeting, leaving the rate hike (+25 bps) for June, when the updated staff projections would also be published. More in FOMC Preview: Focuses on Inflation and Shrugs Off Temporary Disruption on Growth.

More on FOMC:

- FOMC Preview: No Rate Hike Expected, But Hawkish Fed Likely

- More Hawkish Fed Eyed at May FOMC Meeting as Dollar Headed for Best Month in a Year

Euro and Sterling to face event risks

Both Euro and Sterling are facing important event risks ahead. EUR/USD selloff accelerated after taking out 1.2154 key support last week. ECB president Mario Draghi's comments at the post meeting press conference was the trigger. Draghi sounded uncertain on the factors behind Q1's slowdown in Eurozone growth. And he even said that more time is needed to gauge whether the factors are temporary or permanent. The chance of getting a decision on whether to end the asset purchase program this year by June meeting is getting a bit slimmer. Euro suffered further selling after French GDP data, which showed growth slowed to 0.3% qoq, missing expectation of 0.4% qoq. Today's Q1 Eurozone GDP will show ECB how deep that slowdown was. And tomorrow's April CPI will tell ECB whether inflation was dragged down too.

Meanwhile, the Pound has been sold off after recent data misses dented the chance of a May BoE hike. BoE Governor Mark Carney also reminded people that there are "other meetings" in line. Last week's Q1 GDP miss, which showed only 0.1% qoq growth was the final straw in ruling out a May hike. But is the UK economy rebounding well in Q2 to support a BoE hike later in the year? Yesterday's PMI manufacturing was another miss. Markit noted that UK manufacturing sector "lose further steam" in Q2, with "growth of production, new business and employment all slowed." And "while adverse weather was partly to blame in February and March, there are no excuses for April's disappointing performance, making the chances of a near term hike in interest rates by the Bank of England look increasingly remote." Today's PMI construction and tomorrow's PMI services will give a fuller picture.

New Zealand unemployment rate dropped to lowest since 2008

New Zealand employment rose 0.6% qoq in Q1, in line with expectation. Unemployment rate dropped to 4.4%, below expectation of 4.5%. That's also the fifth consecutive quarter of decline in unemployment rate, and it hit lowest level since December 2008. In addition, the underutilization rate dropped to 11.9%, down from 12.2%. That reflects 9200 fewer people are were underemployed. Labour force participation rate dropped 0.1% to 70.8%. Employment rate was unchanged at 67.7%.

China Caixin PMI manufacturing: Uncertainty in exports increased significantly

The China Caixin PMI manufacturing rose to 52.5 in April, up from 51.0, above expectation of 50.9. Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group, warned that "manufacturers are facing a sharply deteriorating foreign demand environment as new export orders declined for the first time in 17 months in April." And, while overall operating conditions improved, "uncertainty in exports has increased significantly, and the dependence of the Chinese economy on domestic demand is rising."

BoC Poloz: Interest rates are headed higher

BoC Governor Stephen Poloz said in a speech overnight that seeing some good pickups in wages in the last 6-8 months, the Canadian economy is in a "phase we call the sweet spot". And, the policymakers are becoming "more confident" that less monetary stimulus is needed. There is a concern that interest rates are "really low" comparing to anything that can be described as neutral. Interest rates are "headed" higher and the question is just when.

Poloz cited some factors restraining growth, including uncertainty about US trade policies, renegotiation of NAFTA and new mortgage rules. But he noted that "those forces will not last forever". And, "as they fade, the need for continued monetary stimulus will also diminish and interest rates will naturally move higher."

But for now, Poloz indicated that the timing of the move will be guided by incoming data. And, it's too soon to judge the impact of the prior rate hikes on the economy yet.

Looking ahead

Swiss Retail sales and PMI manufacturing will be released in European session. Eurozone will release PMI manufacturing final, unemployment rate and Q1 GDP. UK will release construction PMI. Later in the day, US will release ADP employment, followed by FOMC rate decision.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1953; (P) 1.2018 (R1) 1.2056; More....

EUR/USD's fall is still in progress and is pressing 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991. Intraday bias remains on the downside and firm break of 1.1991 will target 200% projection at 1.1891 next. On the upside, above 1.2054 minor resistance will indicate temporary bottoming and turn bias neutral for consolidations. But upside of recovery should be limited well below 1.2214 support turned resistance to bring another decline.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Unemployment Rate Q1 | 4.40% | 4.50% | 4.50% | |

| 22:45 | NZD | Employment Change Q/Q Q1 | 0.60% | 0.60% | 0.50% | 0.40% |

| 23:01 | GBP | BRC Shop Price Index Y/Y Apr | -1.00% | -1.00% | ||

| 23:50 | JPY | Monetary Base Y/Y Apr | 7.80% | 9.20% | 9.10% | |

| 1:45 | CNY | Caixin PMI Manufacturing Apr | 52.5 | 50.9 | 51 | |

| 5:00 | JPY | Consumer Confidence Apr | 43.6 | 44.5 | 44.3 | |

| 5:45 | CHF | SECO Consumer Confidence Apr | 2 | 4 | 5 | |

| 7:15 | CHF | Retail Sales Real Y/Y Mar | 0.30% | -0.20% | ||

| 7:30 | CHF | PMI Manufacturing Apr | 59.8 | 60.3 | ||

| 7:45 | EUR | Italy Manufacturing PMI Apr | 54.5 | 55.1 | ||

| 7:50 | EUR | France Manufacturing PMI Apr F | 53.4 | 53.4 | ||

| 7:55 | EUR | Germany Manufacturing PMI Apr F | 58.1 | 58.1 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Apr F | 56 | 56 | ||

| 8:30 | GBP | Construction PMI Apr | 50.5 | 47 | ||

| 9:00 | EUR | Eurozone Unemployment Rate Mar | 8.50% | 8.50% | ||

| 9:00 | EUR | Eurozone GDP Q/Q Q1 A | 0.40% | 0.60% | ||

| 9:00 | EUR | Italian GDP Q/Q Q1 P | 0.30% | 0.30% | ||

| 12:15 | USD | ADP Employment Change Apr | 200K | 241K | ||

| 14:30 | USD | Crude Oil Inventories | 2.2M | |||

| 18:00 | USD | FOMC Rate Decision | 1.75% | 1.75% |

EUR/USD Dropped Below 1.20

Market movers today

The main events today are the euro area preliminary first quarter GDP and the FOMC meeting. At the May FOMC meeting, we expect the Fed to maintain the target range at 1.50-1.75%. We believe the Fed is unlikely to change i ts pol icy signal significantly. The expected June hike is almost already fully priced in.

After GDP growth beat expectations and showed growth of 0.7% q/q in the last three quarters of 2017 in the euro area, we expect a slowdown in Q1 18 to 0.4% q/q after some moderation, in particular in the latter part of the quarter. However, we are still in expansionary territory, expecting sol id GDP growth throughout 2018.

PMIs from Norway and Sweden are also due out. Swedish PMI manufacturing was quite close to the 2014-16 level at around 55 in March and could very well fall slightly below this. The same slowdown tendency is visible in services PMI but it is still a bit higher at close to 60. In Norway and Sweden, it is time for PMIs.

Selected market news

Many of the European markets were yesterday closed for Labour Day. However, the UK market was open and a new set of weak UK data was published, as the UK PMI dropped to the lowest level since November 2016. The weak PMI came after weaker CPI, retail sales and GDP data had been released in April and following soft comments from Bank of England Governor Mark Carney. The market is now pricing in just a 17% probability of a BoE rate hike next week. Just a few weeks ago a hike was priced in by more than an 80% probability. In the US market the ISM indicator edged lower to 57.3 in April from 59.3 in May. The ISM indicator peaked at 60.8 in February and the reading might be an indication that US economic activity – as we have seen in the eurozone and the UK – has weakened over the past couple of months.

In the FX market , attention was on the continued advance of the US dollar. EUR/USD dropped below 1.20 and USD/JPY rose towards 1.10. Implied FX volatility is going up and it seems that the market is now preparing it self for a larger move in EUR/USD compared to the range trading that so far has been the case in 2018. In the bond market , 10Y US Treasury yields are st ill trading just below the psychological important 3% level. If we see a ‘hawkish' Fed tonight we might see a break with this level. In the US equity market , at tention was on the Apple earnings that came after the market closed. Apple beat Wall Street expectations and the stock surged as much as 5% in after-hour trading.

In Italy, the political situation has worsened over the past couple of days. On Monday, the Five Star leader Luigi Di Maio said that the party was seeking new elections later this year , as the party talks between both the cent re-right alliance and the Democratic Party had failed. It will be up to President Sergio Mattarella to call a new election. However, yesterday, the media reported that the president had said that a new elect ion in the autumn would be a ‘disgrace', and that it risks not solving the problem of non-governability in Italy. Hence, the Italian elect ion impasse has not been solved, and the Italian bond market is expected to under perform today.