Sample Category Title

Dollar index showed impulsive power

The dollar index's strong rally yesterday showed its true color. With 100% projection of 88.25 to 90.93 to 89.22 firmly taken out, we're more confident that it's an impulsive move. Further rise is expected in near term to 161.8% projection at 93.55. Reaction from there, as well as 94.19 fibonacci level, will reveal how powerful the impulse is. For now, near term outlook will remain bullish as long as 90.93 resistance turned support holds.

The impulsive nature of the rebound from 88.25 is a critical element to the case of medium term trend reversal. We'd believe that fall from 103.82 has completed at 88.25 after drawing support from 50% retracement of 72.69 to 103.82 at 88.25, on bullish convergence condition in weekly MACD. It's early to say whether rise from 88.25 is resuming the long term up trend. But for now, there should at least be a solid break of 38.2% retracement of 103.82 to 88.25 at 94.19. And prospect of reaching 61.8% retracement at 97.87 and above is high.

China Caixin PMI manufacturing: Uncertainty in exports increased significantly

The China Caixin PMI manufacturing rose to 52.5 in April, up from 51.0, above expectation of 50.9.

Comments from Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group:

"The Caixin China General Manufacturing PMI edged up to 51.1 in April. Output increased at a faster rate last month from March, while the contraction in employment narrowed. However, growth of new business moderated for the second straight month, reflecting weakening demand across the manufacturing sector. Manufacturers are facing a sharply deteriorating foreign demand environment as new export orders declined for the first time in 17 months in April. The rate of output charge inflation eased slightly while growth in input costs posted its first acceleration since September, likely due to increases in crude oil prices. This may squeeze the profit margins of manufacturers and has thus contributed to a decline in the sub-index of future output, a gauge of companies' confidence in their business outlook over the next 12 months. Stocks of finished goods expanded at a faster rate in April compared to March, suggesting that inventory levels for manufacturers have remained rather high.

"Overall, operating conditions across China's manufacturing sector continued to improve in April. But uncertainty in exports has increased significantly, and the dependence of the Chinese economy on domestic demand is rising."

New Zealand unemployment rate dropped to lowest since 2008

New Zealand employment rose 0.6% qoq in Q1, in line with expectation. Unemployment rate dropped to 4.4%, below expectation of 4.5%. That's also the fifth consecutive quarter of decline in unemployment rate, and it hit lowest level since December 2008.

In addition, the underutilization rate dropped to 11.9%, down from 12.2%. That reflects 9200 fewer people are were underemployed. Labour force participation rate dropped 0.1% to 70.8%. Employment rate was unchanged at 67.7%.

Below is a video explanation by Stats NZ on the data.

https://www.youtube.com/watch?v=n8bXmq3mW98

BoC Poloz: Interest rates are headed higher

BoC Governor Stephen Poloz said in a speech overnight that seeing some good pickups in wages in the last 6-8 months, the Canadian economy is in a "phase we call the sweet spot". And, the policymakers are becoming "more confident" that less monetary stimulus is needed. There is a concern that interest rates are "really low" comparing to anything that can be described as neutral. Interest rates are "headed" higher and the question is just when.

Poloz cited some factors restraining growth, including uncertainty about US trade policies, renegotiation of NAFTA and new mortgage rules. But he noted that "those forces will not last forever". And, "as they fade, the need for continued monetary stimulus will also diminish and interest rates will naturally move higher."

But for now, Poloz indicated that the timing of the move will be guided by incoming data. And, it's too soon to judge the impact of the prior rate hikes on the economy yet.

Market Morning Briefing: Euro Weakened Further Yesterday

STOCKS

Dow (24099.05, -0.27%) faces strong buying near 23750 and while that continues, the index could be pushed up towards 24750-25000 levels. Overall near term looks sideways to bullish while above 23750.

Dax (12612.11, +0.25%) moved up from levels near 12300 as expected and is now heading to re-test important resistance near 12650. Watch price action here; if a break above 12650 is seen, Dax could turn bullish for the coming sessions targeting 12800 on the upside; else a rejection from 12650 would bring it back towards 12300-12200 levels.

Nikkei (22436.46, -0.32%) has dipped from immediate resistance at 22600 and while that holds, a fall is possible towards 22200-22000 in the near term. If the index manages a break above 22600, it could test 23000 on the upside in the medium term. A fall from here could be in line with a fall from 110 on Dollar Yen.

Shanghai (3073.72, -0.28%) continues to accumulate some buying near 3050 and while that holds, 3050 could produce bounce towards 3125-3150 levels. Broad trade within 3150-3050 levels is possible in the near term. A break on either side of the 3050-3150 range would indicate further market direction in the longer run.

No immediate resistance is visible on the Nifty (10739.35, +0.44%). Looking at the slow and gradual rise in the past few sessions, if the index breaks above 10800, it could move up towards 11000 in the medium term.

COMMODITIES

Geo-political tensions about the Trump sanctions to Iran are in the air and increasing US supplies are expected to cap market gains. Brent (73.22) and Nymex WTI (67.50) are trading lower just now. Brent could get some support near 72.15 and while tat holds, another up leg in the prices is likely. A break below 72.15-72.00 would indicate an immediate top formation leading to some more dips in the medium term. WTI on the other hand has scope of testing 66 on the downside but could soon move up towards 68 in the medium term.

Gold (1310) has been coming off as expected. A fall towards 1300 is on its way in the next few sessions.

Copper (3.0770) looks bearish while below 3.08 and could move down towards 3.00-2.90% in the coming sessions. A break above 3.08 could keep the upside limited to 3.12-3.15.

FOREX

Dollar index (92.3650), as we had predicted, has risen to 92.5 (seeing a high of 92.57 yesterday) and might get some resistance here for a few sessions. The next few sessions could also depend upon the perception of the FOMC’s stance in its meeting later today. Although a rate hike isn’t expected today, expectation of further hawkish intent from the Fed could help the Dollar strengthen. Its next target on the upside in the medium term could be 94-95 (which corresponds to the 5th wave starting point of the downmove since Dec ’16). The upside could be capped till 94-95 after which the Dollar could dip.

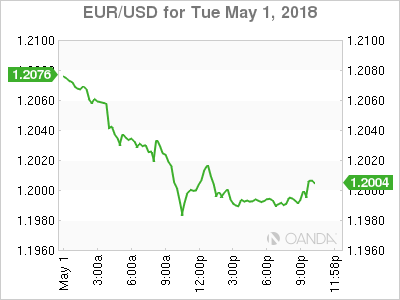

Euro (1.2006) weakened further yesterday, seeing a low of 1.1981 and thereby testing support on daily candles near 1.198-1.200. There could now be a pause in the Euro’s downtrend for a couple of sessions. We don’t prefer a bounce for the Euro from these levels currently; rather it could creep down lower towards 1.195 in this week. The Euro’s medium term target corresponding to the Dollar Index’s target of 94-95 would be levels near 1.16 (which is the 5th wave starting point of the Euro’s upmove since Dec ’16) .

Dollar Yen (109.71) : Dollar Yen has moved up further in the upward channel on 3 day candles instead of dipping to 108.5 (which we had expected). As mentioned earlier as well, the current uptrend could be capped till 110.0-110.5, after which Dollar Yen could dip. In the next 2-3 sessions, we prefer a dip to 109 (support on daily candles) and rise back towards 110 thereafter.

Euro Yen (131.74) : In line with our prediction on Friday, Euro Yen has moved further down towards 131 (seeing a low near 131.5 yesterday). Our targets of 1.195 on the Euro and 109.0 on the Dollar Yen for this week suggests that Euro Yen could break below 131 to target 130. However, there is support near 131 on weekly candles which could prevent a test of 130. In that case, our prediction of 109 on the Dollar Yen could possibly go wrong, with levels of 110 being tested this week itself. Lets wait and watch.

Pound (1.3614), against our expectation, has broken below crucial long term support level near 1.385 on weekly line chart. This could prove to be a crucial break, making the Pound very bearish in the medium term. Next target on the downside could possibly be 1.35 (seen on daily candles).

Dollar Rupee (66.665): Overbought conditions had corrected to a considerable degree on Friday. Watch Support at 66.60 today.

INTEREST RATES

Draghi’s dovishness last week had led to a dip in US yields with the 10 Year moving back below 3%. However with the FOMC later today, we are expecting the Fed to express some hawkish intent (rate hike however is not expected), which could thereby again take yields higher this week. Our Apr ’18 US Treasury (available on demand) report predicts a medium target of 3.2%-3.3% (10 Year), 3.4%-3.5% (30 Year), 3.15% (5 Year) and 2.75% (2 Year). We also expect some more yield curve flattening in the next month followed by steepening after that, as yields bounce from long term supports.

We repeat that the upmove in US yields in April had happened on back of positive sentiment around the US economy’s growth and due to the rise in Crude towards 74-75.

US 10 Yr Yield (2.97%), 30 Yr (3.13%), 5 Yr (2.81%), 2 Yr (2.50%):

The US 2 year yield (2.5) has moved to the psychologically important 2.5% level and could now see a short term correction towards 2.45%.

The 10 Year yield (2.97%) had dipped below 3% last week but could possibly react to the FOMC today by rising back above 3%. Any sign of dovishness however could mean a retreat back towards 2.95%-2.90%.

Can USD/CAD Break 1.2900 Resistance?

Key Highlights

- The US Dollar traded higher and moved above 1.2750 against the Canadian Dollar.

- There is a major bullish trend line forming with support at 1.2720 on the daily chart of USD/CAD.

- The Canadian GDP in Feb 2018 (MoM) grew 0.4%, more than the forecast of +0.3%.

- Today, the ADP Employment Change for April 2018 will be released, which is forecasted to post 200K.

USDCAD Technical Analysis

The US Dollar started a nice upside move from the 1.2520 swing low against the Canadian Dollar. The USD/CAD pair gained traction and broke a major resistance at 1.2750.

During the upside move, the pair succeeded in settling above the 100 (red) and 200 (green) simple moving averages (daily). There was also a break above the 50% Fib retracement level of the last decline from the 1.3124 high to 1.2521 low.

However, there is a crucial resistance waiting on the upside near 1.2900-1.2920. The stated zone is a key pivot and acted as a hurdle for buyers many times. It now coincides with the 61.8% Fib retracement level of the last decline from the 1.3124 high to 1.2521 low.

Therefore, a break above 1.2900-1.2920 won’t be easy. Should buyers succeed, the pair could move past 1.3000 in the short term. On the flip side, an initial support is at 1.2750. Moreover, there is a major bullish trend line forming with support at 1.2720 on the daily chart.

Recently, the Canadian GDP for Feb 2018 was released by the Statistics Canada. The market was looking for a rise of 0.4% in the GDP compared with the previous month.

The actual result was better as there was a rise of 0.4% in the GDP, well above the last decline of 0.1%. The report added:

The output of goods-producing industries grew 1.2% as manufacturing and construction rose in addition to the rebound in mining and oil and gas extraction. Services-producing industries edged up 0.1% as increases in most sectors more than offset declines in wholesale trade and in the real estate and rental and leasing sector.

Overall, there could be a downside correction in USD/CAD, but the pair remains supported near 1.2750 and 1.2720.

Economic Releases to Watch Today

- Germany’s Manufacturing PMI for April 2018 – Forecast 58.1, versus 58.1 previous.

- Spanish Manufacturing PMI for April 2018 – Forecast 54.2, versus 54.8 previous.

- Euro Zone Manufacturing PMI April 2018 – Forecast 56.0, versus 56.0 previous.

- UK Construction PMI for April 2018 – Forecast 50.5, versus 47.0 previous.

- Euro Zone Gross Domestic Product Q1 2018 (QoQ) (Prelim) – Forecast 0.4%, versus 0.6% previous.

- Euro Zone Gross Domestic Product Q1 2018 (YoY) (Prelim) – Forecast 2.5%, versus 2.7% previous.

- US ADP Employment Change April 2018 – Forecast 200K, versus 241K previous.

Are Dovish Central Bank’s Doing The USD Heavy Lifting ?

Currency Markets

The US Dollar Bulls continued to lead the charge as traders remain centred favourably on the entrenched US data flow, despite a slightly softer ISM, relative to that from other major economies that are cooling quickly. Suggesting central bank policy divergence and the widening interest rate differentials have G-10 traders taking the dollar bull by the horns. It's now over to the FOMC to hold up their side of the bargain as so far, the heavy lifting for the greenback has fallen on the global central bank community which has turned dovish on the first hint of economic slack.

Equity Markets

After initially grumbling on Pfizer results and dropping oil prices, US equity market rebounded convincingly in Tuesday's NY session, But investors remain cautious that tariffs and higher oil prices could increase cost pressures and weigh on corporate profits. Not to mention the negative equity market connotations from the prospects of higher US interest rates as the Federal Reserve Board concludes its two-day policy meeting continues to weigh.

Oil Markets

As May 12 Iran nuclear deadline nears, headline risk continues to speak volumes. The market turned lower after peaking post-Israeli Prime Minister Benjamin Netanyahu's televised exposé which accused Iran of lying about its past nuclear intentions when in fact the existence of a covert Iranian program was divulged in a 2011 report from the International Atomic Energy Agency

Geopolitical developments will continue to drive sentiment. However, a stronger US dollar, soft ISM and a refocusing on rising US production have caused traders to turn profit taking mode and capped upticks so far.

The API reported a larger than expected crude inventory build while the U.S. Energy Information Administration said Monday that oil production rose to a record 10.264 million barrels a day in February.

Gold Markets

Gold market melted as the surging US dollar takes hold. The revitalised greenback has all but crushed demand for bullion, and as we near the critical $1300 level, the spectre of stop losses getting triggered on an upbeat FOMC statement has traders now positioning for that path of least resistance, which appears lower.

We're in a lull between geopolitical developments which is also offering little support for gold prices.

G-10

The USD is bid across the board after testing some significant levels as the market sits tight ahead of the FOMC, but more significantly now pivots to this week's NFP which could make or break the resurgent dollar.

EUR: Some traders had not entirely positioned for downside exposure so on a break of the psychological key 1.2050 there was a mad dash for downs exposure which toppled the EUR below the 200 days moving average which set up a test of this year's low print, 1.1915.

JPY: Interest rate differential and positive developments in the Korea Peninsula suggest a test of 110 is on the cards

AUD: The RBA was a non-event and was more or less a replay of past statements. With the RBA continuing to err dovish and barring a surprise uptick in global growth and commodities, the market continues to favour the Aussie short vs USD amongst G-10 peers.

USDASIA

MYR: Stronger dollar narrative coupled with political uncertainty should continue to pressure the Ringgit.

Growing election uncertainty continues to keep investors at bay. While the chances of the opposition to pull off a surprise result remain low, a large scale knee-jerk negative repricing of Malaysian assets suggests foreign bond buyer will stay on the sidelines. As such, the MYR will continue to trade defensively due to their heightened domestic political risk.

Dollar Stronger On Possibility Fed To Step Up Tightening Pace

The US dollar rose on Tuesday against all major pairs. The greenback started to rally in April and even though the ISM manufacturing index was lower than expected it did little to dent the advance of the currency. Employment data will start trickling in on Wednesday with the release of the ADP non-farm private payrolls report at 8:15 am EDT. Later in the day the U.S. Federal Reserve will wrap up its two day Federal Open Market Committee (FOMC) meeting and issue a rate statement at 2:00 pm EDT.

- US dollar higher due to strong data and faster rate hike path

- ADP private payrolls to show rise above 200,000 jobs

- U.S. Federal Reserve expected to leave rates unchanged

Fed to Hold in May with June Meeting Likely Candidate for a Hike

The EUR/USD lost 0.68 percent on Tuesday. The single currency is trading at 1.1996 despite the only economic indicator released that day the ISM manufacturing PMI came in under expectations at 57.3. The USD is getting a lot of support from the Fed’s comments on more rate hikes than originally priced in by the market. The CME Fedwatch tool has a small probability of a rate move in May, with 94.3 percent of staying at 150-175 basis points. The June odds are the same number but for a 25 basis points lift at 94.3 percent and even an outside chance of 5.7 percent of the benchmark reaching 200-225.

The Fed has stuck to an unwritten policy of raising rates only during FOMCs that feature press conferences to give more details on the decision. With three more rate hikes forecasted after the March rate hike (with press conference) and three press conferences left in the calendar (June, September and December) they become the most obvious candidates. Employment has been one of the strongest pillar of the economic recovery and the release of the ADP will be the preamble for the publication of the U.S. non farm payrolls (NFP) report on Friday, although the focus has shifted from job numbers to wage growth indicators.

The Personal Consumption Expenditures (PCE) was released on Tuesday and recorded an annual gain of 1.9 percent. Wage growth on Friday will be another insight into how strong is the inflationary pressure. GDP growth in the first quarter was better than expected, specially after the first three months of the year are seasonally sluggish and still they showed a 0.9 percent gain in wages and salaries, the largest increase since Q1 in 2017.

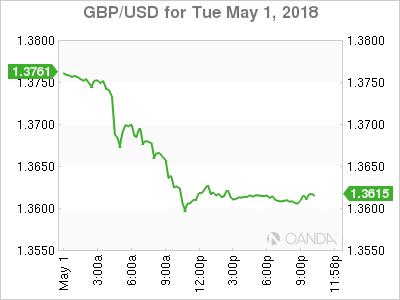

UK Manufacturing PMI Disappointment Sinks Pound

The GBP/USD lost 1.00 percent in the last 24 hours. The currency pair is trading at 1.3618 after the release of manufacturing and consumer lending data on Tuesday. The activity in UK factories grew at the slowest rate in 17 months at the same time that net lending to individuals slowed down as they opted to repay their loans.

The British economy had a slow start to 2018. Purchasing manager indices (PMIs) for manufacturing, construction and services have disappointed this year. With Bank of England (BoE) Governor Mark Carney surprising investors last week with comments suggesting the central bank could not hike rates in May, economic indicators, specially leading ones such as PMIs gain more relevance in trying to forecast the moves of the central bank. Carney has pointed out that mixed data could push out a rate rise until later this year.

The first PMI release this week does not bode well for a May rate hike by the BoE and the GBP paid the price. The currency reached a post Brexit high in April, but weak data in particular GDP and now manufacturing the market will be eyeing the Services sector that is due on Thursday, May 3 at 4:30 am EDT. The index is expected to improve on last month’s reading with a final 53.5 anything below will sound alarm bells for the pound and beating expectations could have limited upside.

Market events to watch this week:

Tuesday, May 1

6:45pm NZD Employment Change q/q

Wednesday, May 2

4:30am GBP Construction PMI

8:15am USD ADP Non-Farm Employment Change

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Statement

9:30pm AUD Trade Balance

Thursday, May 3

4:30am GBP Services PMI

8:30am CAD Trade Balance

10:00am USD ISM Non-Manufacturing PMI

12:00pm CHF SNB Chairman Jordan Speaks

9:30pm AUD RBA Monetary Policy Statement

Friday, May 4

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

Cable Calamity Continues

Sterling took another beating on Tuesday after the UK manufacturing PMI. The US dollar was the top performer once again while cable fell more than 1%. The US dollar is suddenly knocking down some major technical levels. A new USD trade has been posted to Premium clients. The member video is posted below, highlighting the rationale for existing and potential trade.

It was all about the 200-day moving average on Tuesday. EUR/USD, gold and the dollar index all fell below the key marker while cable neared it. It's part of the rapid reversal in the US dollar of the past two weeks. Disappointing US manufacturing ISM went unnoticed and so did conerns about the US expansion being in a late cycle.

The combination of higher Treasury yields and jitters about global growth started a trickle into the dollar that's grown into a flood as USD-shorts squeezed as the Fed remains hawkish while other global central bankers waiver.

The BoE will now almost-certainly blink at the May 10 meeting. The probability of a hike has fallen to 16% from 96% two week ago. Cable has fallen 800 pips in that time starting with some less hawkish hints from Carney and followed by a series of poor data releases and Brexit woes. The latest was a drop in the UK manufacturing PMI to a 17-month low on Tuesday. Cable fell more than a full-cent on the day and came within a half-cent of the 200-dma.

It was a cascade of US dollar technical victories to start the month. The euro fell below 1.20 for the first time since January 10, albeit on a day with large parts of Europe on holiday. AUD/USD broke the December low to the worst since June in a move that was helped by an altogether dovish stance from the RBA.

Going ahead, the question is whether this was a blow off move or a continuation? The dollar has three tailwinds at the moment, depending on what comes next in markets. If jitters continue, it benefits from a save-haven bid, especially from emerging markets. If Treasury yields rise, it benefits from rate differentials. And if the momentum continues, it can benefit from a continued short squeeze.

Eco Data 5/2/18

[php_everywhere instance="1"]