Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.04; (P) 109.25; (R1) 109.52; More...

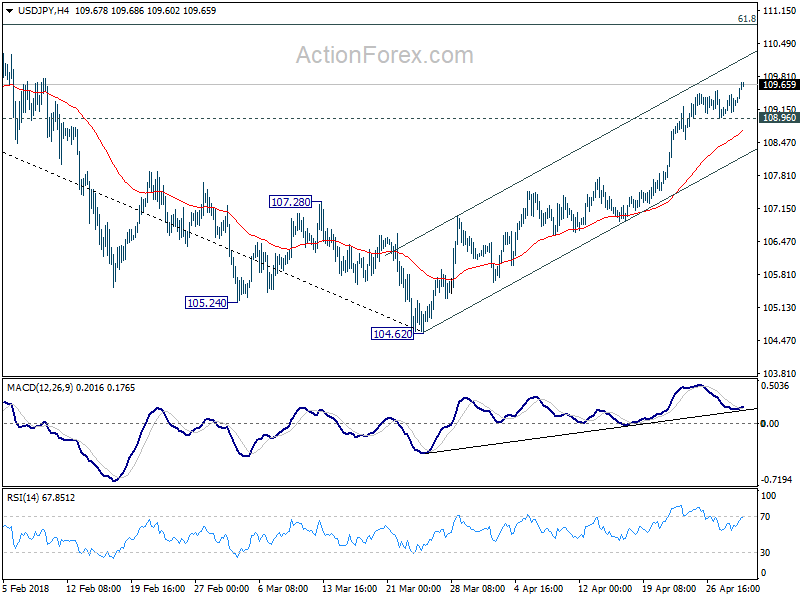

USD/JPY's really resumes today and reaches as high as 109.69 so far. Intraday bias is back on the upside. Current rise from 104.62 should target 61.8% retracement of 114.73 to 104.62 at 110.86 next. On the downside, below 108.96 will turn intraday bias neutral again and bring consolidations.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.78).

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9875; (P) 0.9898; (R1) 0.9927; More...

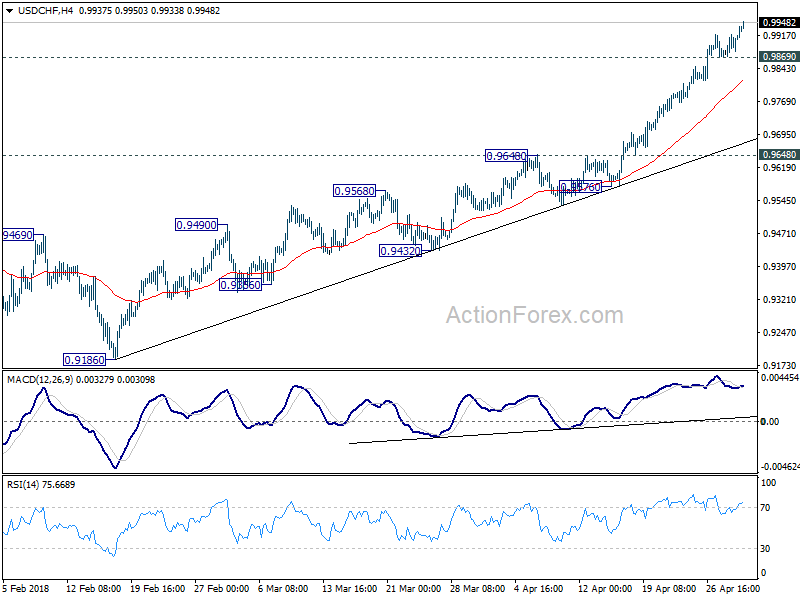

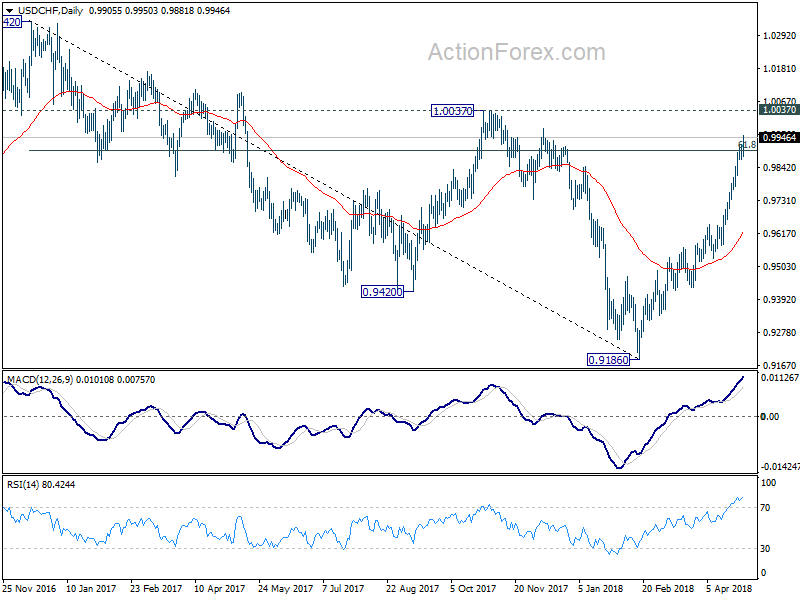

USD/CHF's rally resumes today and reaches as high as 0.9950 so far. Intraday bias is back on the upside for 1.0037 resistance next. Firm break there will pave the way to key resistance level at 1.0342. On the downside, below 0.9869 minor support will turn intraday bias neutral again and bring consolidation, before staging another rise.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 0.9648 resistance turned support holds, even in case of pull back.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2049; (P) 1.2093 (R1) 1.2124; More....

EUR/USD's decline resumes after brief consolidation and reaches as low as 1.2010 so far. Intraday bias stays on the downside for 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991 first. Break will target 200% projection at 1.1891 next. On the upside, break of 1.2138 minor resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Canadian Economy Sprang Back to Life in February

Canadian GDP rose 0.4% month-on-month in February, helped by the resolution of earlier setbacks in several industries. While the strong outturn was driven by a few outsized gains, there was nevertheless solid breadth to the expansion as 15 of 20 major industries reported increased output.

Goods producing industries did well in February, led by mining, quarrying and oil and gas extraction, up 2.4% following a 2.9% drop in January. Production began to move back to normal in February following some issues in the month prior. Manufacturing also turned in a solid performance (+1.0%), as transportation equipment manufacturing picked back up following unusual plant shutdowns in January. Rounding out the broader sector were solid gains construction (+0.7%) and agriculture (+0.5%). Utilities output was down 0.9% in February owing to warmer than normal weather in Central and Eastern Canada.

The service side of the economy eked out a small gain (+0.1%), although revisions to January mean that the 21 month expansion streak came to an end last December. On the negative side of the ledger was, unsurprisingly, real estate (-0.2%), which fell for a second month, consistent with the soft resale activity seen in February. The bulk of sub-industries saw expansions however, with notable gains in professional services (+0.6%), arts and entertainment (+1.4%), and transportation (+0.5%).

Key Implications

What a pleasant surprise. While a rebound in growth was likely given the one-off disruptions that held back January, in the event, the Canadian economy saw a healthy pop back in growth in February. Even better, the outturn came on the back of fairly widespread growth, suggesting healthy underlying momentum.

As it stands, February's performance points to an expansion of about 1.7% annualized in the first quarter. This is roughly in line with Canada's underlying potential and a modest improvement over our initial expectation for the quarter. We remain of the view that some modest pick-up of growth is likely through the middle of the year, but with economic slack effectively absorbed, the first quarter's growth rate represents the pace that Canadians can expect in coming years.

For the Bank of Canada, today's report will not be a huge surprise, with our growth tracking of 1.7% not too far off their forecast of a 1.3% quarterly expansion. More important will be the evolution of the economy over the remainder of the year. Not only do the 'standard' metrics such as core inflation, wages, and business investment matter, but so too does the reaction of Canadian borrowers to higher borrowing costs. We will receive more insight on this latter point this afternoon when Governor Poloz speaks in Yellowknife.

GBPUSD: Remains Vulnerable, Extends Weakness

GBPUSD - The pair remains vulnerable to the downside with more weakness expected. Support lies at the 1.3600 level where a break will turn attention to the 1.3550 level. Further down, support lies at the 1.3500 level. Below here will set the stage for more weakness towards the 1.3450 level. Conversely, resistance stands at the 1.3700 levels with a turn above here allowing more strength to build up towards the 1.3750 level. Further out, resistance resides at the 1.3800 level followed by the 1.3850 level. On the whole, GBPUSD remains biased to downside.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3720; (P) 1.3755; (R1) 1.3799; More...

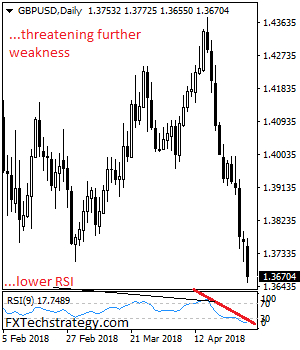

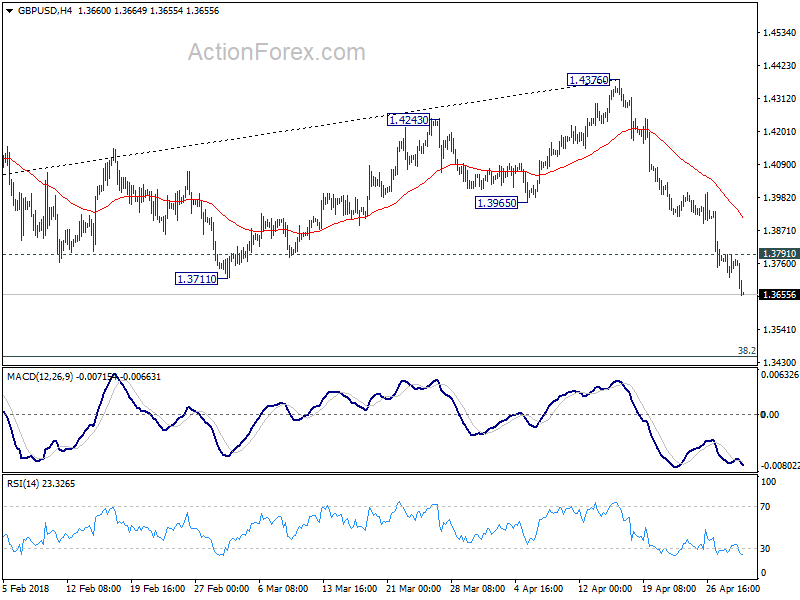

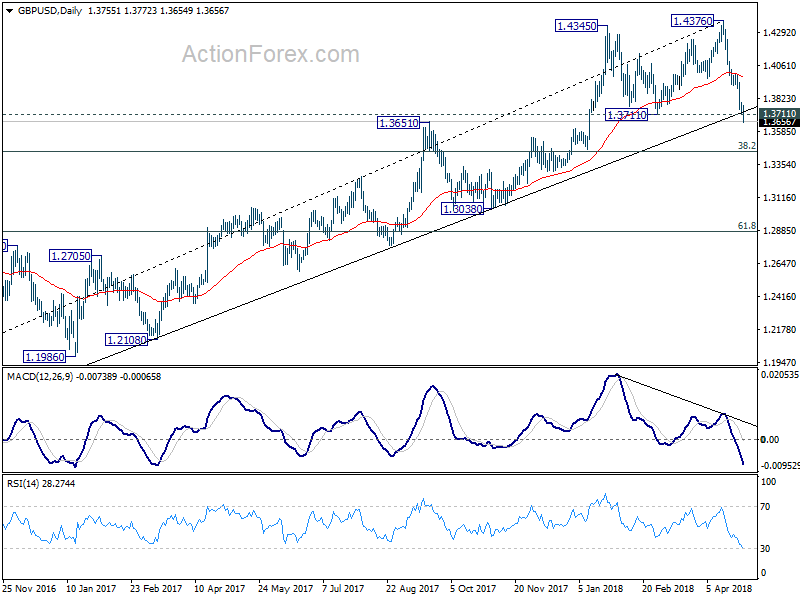

GBP/USD's decline continues today and reaches as low as 1.3654 so far. The break of 1.3711 key support indicates medium term reversal. That is, whole rally from 1.1946 has completed. Intraday bias remains on the downside for 1.3448 fibonacci level next. On the upside, break of 1.3791 resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will remain bearish even in case of recovery.

In the bigger picture, bearish divergence condition in daily MACD is raising the chance of medium term reversal. Also, note that GBP/USD has just failed to sustain above 55 month EMA (now at 1.4248) again. Focus is back on 1.3711 support. Firm break there will confirm medium term reversal and target 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. For now, sustained break of 55 month EMA is needed to confirm medium term upside momentum. Otherwise, we won't turn bullish even in case of strong rebound.

Dollar Resuming Recent Rally, Sterling Tumbles after PMI, Canadian Up on GDP

Dollar resumes recent rally today and breaks last week's high against all major currencies except Canadian Dollar. In particular, GBP/USD has taken out 1.3711 key support level after UK PMI manufacturing missed market expectations. The development is in line with the view of medium term reversal. AUD/USD also breached 0.7500 key support after RBA rate decision provided no support to the Aussie. Nonetheless, Canadian Dollar also picks up some solid buying after GDP beat expectations. Canadian GDP grew 0.4% mom in February versus consensus of 0.3% mom. That's a solid rebound from January's -0.1% mom contraction. Focus will turn to ISM manufacturing from US next.

UK PMI manufacturing dropped to 17 month low, increasingly remote chance for near term BoE hike

UK PMI manufacturing dropped to 53.9 in April, down from 55.1, below expectation of 54.8. That's also the lowest level in 17 months. Rob Dobson, Director at IHS Markit, said in the release that the UK manufacturing sector "lose further steam" in Q2, with "growth of production, new business and employment all slowed." And he added that "while adverse weather was partly to blame in February and March, there are no excuses for April's disappointing performance, making the chances of a near term hike in interest rates by the Bank of England look increasingly remote. And looking ahead " the trend in manufacturing production is likely to remain subdued." "Concerns about Brexit, trade barriers and the overall economic climate remained widespread."

Also from UK, mortgage approvals dropped to 62.9k in March, down from 63.8k, missed expectation of 63.0k. M4 money supply dropped -1.4% mom in March, below expectation of 0.2% mom.

EU warns Trump: We will not negotiate under threat

Just before the temporary exemptions on the steel and aluminum tariffs expire today, Trump announced to a 30-day extension on European Union, Mexico and Canada, allowing for further negotiation. Meanwhile, the US has reached trade agreements-in-principle with Argentina, Australia and Brazil and details with be finalized "shortly".

European Commission criticized that the US decision "prolongs market uncertainty, which is already affecting business decisions". It reiterated that EU should be given full and permanent exemptions as the tariffs "cannot be justified on the grounds of national security". Also, EU warned that "as a longstanding partner and friend of the US, we will not negotiate under threat."

UK Department for International Trade spokesman welcomed the "positive decision". And the government said in a statement that "We will continue to work closely with our EU partners and the US government to achieve a permanent exemption, ensuring our important steel and aluminum industries are safeguarded." But, "we remain concerned about the impact of these tariffs on global trade and will continue to work with the EU on a multilateral solution to the global problem of overcapacity, as well as to manage the impact on domestic markets."

RBA left cash rate unchanged at 1.50% as widely expected

Extending the streak for a 19th month, RBA left the cash rate unchanged at 1.50% in May. Benign inflation and recent slowdown in employment growth are allowing policymakers to keep the monetary policy accommodative. The accompanying statement was largely unchanged from the previous one, with the key positive coming from the forecast that GDP growth would rose above 3% this year. All in all, we retain the view that RBA would leave the policy rate unchanged for the full 2018. More in RBA More Upbeat on Growth, Likely on Hold for 2018.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3720; (P) 1.3755; (R1) 1.3799; More...

GBP/USD's decline continues today and reaches as low as 1.3654 so far. The break of 1.3711 key support indicates medium term reversal. That is, whole rally from 1.1946 has completed. Intraday bias remains on the downside for 1.3448 fibonacci level next. On the upside, break of 1.3791 resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will remain bearish even in case of recovery.

In the bigger picture, bearish divergence condition in daily MACD is raising the chance of medium term reversal. Also, note that GBP/USD has just failed to sustain above 55 month EMA (now at 1.4248) again. Focus is back on 1.3711 support. Firm break there will confirm medium term reversal and target 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. For now, sustained break of 55 month EMA is needed to confirm medium term upside momentum. Otherwise, we won't turn bullish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Mar | 14.70% | 5.70% | 6.40% | |

| 00:30 | JPY | PMI Manufacturing Apr F | 53.8 | 53.3 | 53.3 | |

| 04:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 08:30 | GBP | Mortgage Approvals Mar | 62.9K | 63.0K | 63.9K | 63.8K |

| 08:30 | GBP | Money Supply M4 M/M Mar | -1.40% | 0.20% | -0.30% | |

| 08:30 | GBP | PMI Manufacturing Apr | 53.9 | 54.8 | 55.1 | |

| 12:30 | CAD | GDP M/M Feb | 0.40% | 0.30% | -0.10% | |

| 13:30 | CAD | RBC Manufacturing PMI Apr | 55.7 | |||

| 13:45 | USD | Manufacturing PMI Apr F | 56.5 | 56.5 | ||

| 14:00 | USD | Construction Spending M/M Mar | 0.50% | 0.10% | ||

| 14:00 | USD | ISM Manufacturing Apr | 58.5 | 59.3 | ||

| 14:00 | USD | ISM Prices Paid Apr | 76.8 | 78.1 |

CAD steals the show as GDP beat expectation, EURCAD diving

Canadian GDP rose 0.4% mom in February, a solid rebound from January's -0.1% contraction and beat expectation of 0.3% mom.

As seen in D heatmap, CAD is trading as the second strongest one for today, just next to USD. GBP remains the weakest one after today's PMI miss, followed by EUR and JPY.

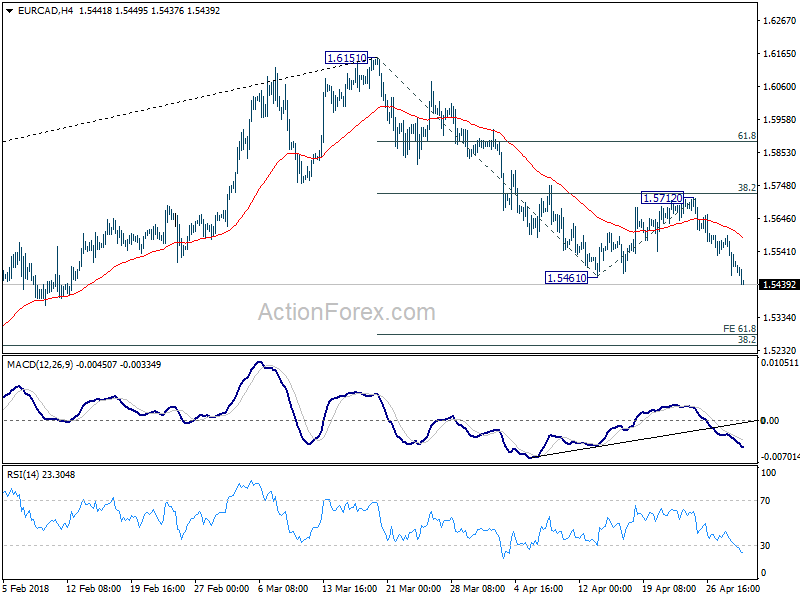

Following up on a post here, EUR/CAD drops through 1.5461 support today. Decline from 1.6151 has resumed and further fall should be seen to 61.8% projection of 1.6151 to 1.5461 from 1.5712 at 1.5286 next.

This is also in line with downside red action bias as seen in EUR/CAD 6H and D action bias charts.

EU warns Trump: We will not negotiate under threat

More on EU's response to US steel tariffs exemption. European Commission criticized that the US decision "prolongs market uncertainty, which is already affecting business decisions". It reiterated that EU should be given full and permanent exemptions as the tariffs "cannot be justified on the grounds of national security". Also, EU warned that "as a longstanding partner and friend of the US, we will not negotiate under threat."

Full statement below

Commission statement following US announcement of an extension until 1 June of the EU's exemption from US tariffs on steel and aluminium imports

The European Commission takes note of the decision of the United States to prolong the European Union's exemption from import tariffs on steel and aluminium for a short period of time, until 1st June 2018.

The US decision prolongs market uncertainty, which is already affecting business decisions. The EU should be fully and permanently exempted from these measures, as they cannot be justified on the grounds of national security.

Overcapacity in the steel and aluminium sectors does not originate in the EU. On the contrary, the EU has over the past months engaged at all possible levels with the US and other partners to find a solution to this issue.

The EU has also consistently indicated its willingness to discuss current market access issues of interest to both sides, but has also made clear that, as a longstanding partner and friend of the US, we will not negotiate under threat. Any future transatlantic work programme has to be balanced and mutually beneficial.

European Commissioner for Trade Cecilia Malmström has been in contact with US Commerce Secretary Wilbur Ross and US Trade Representative Robert Lighthizer over the past weeks, and these discussions will continue.

GBP/USD Proceeds With A Downtrend On Bad Manufacturing PMI Numbers

The GBP/USD performed exactly as expected. Today’s worse than expected Manufacturing PMI numbers, rejected the price below the W L3 – 1.3700. We might see a continuation of a downtrend if the price manages to stay below 1.3750. Targets will be 1.3622 and 1.3581. Have in mind that M L3 -1.3581 is the strong support and I expect buyers to show up around the level, if the price gets close. At this point there are no signs that downtrend price action might break to the upside, ending the bearish move.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

M H4 - Monthly Camarilla Pivot (Very StrongMonthly Resistance)

ML3 – Monthly Camarilla Pivot (Monthly Support)

ML4 – Monthly H4 Camarilla (Very Strong Monthly Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)