Sample Category Title

USD rally resumes, a look at GBPUSD and AUDUSD

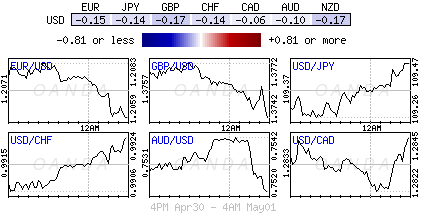

USD's rally resumed in European session today, breaking through last week's high against all major currencies, except CAD.

Momentum is also solid as seen in USD action bias table.

Momentum is also solid as seen in USD action bias table.

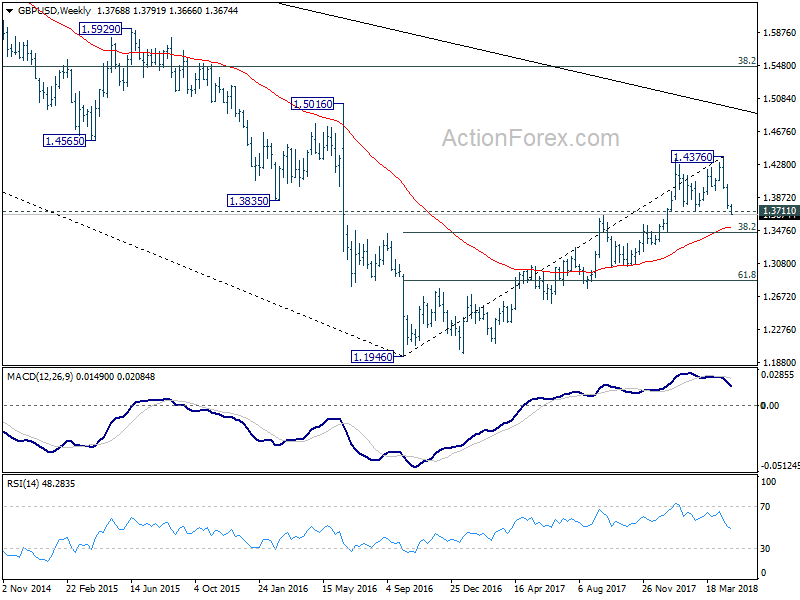

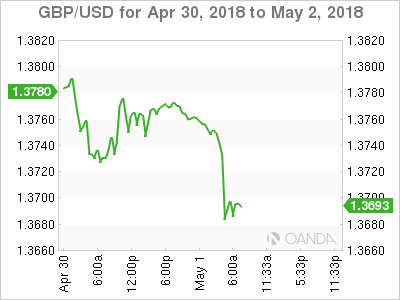

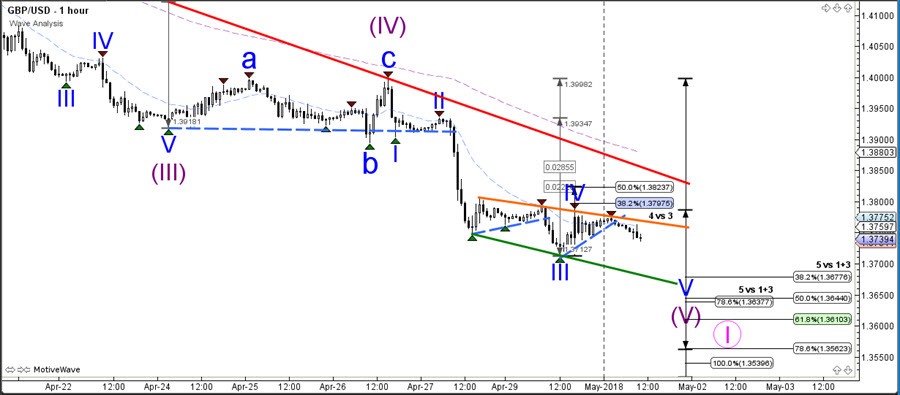

In particular, GBP/USD takes out 1.3711 key support level which indicates medium term reversal. With 6H action bias in downside red all the way through, and D action bias staying in red too, we'd now expect GBP/USD to sustain below this level to confirm the bearish case.

In particular, GBP/USD takes out 1.3711 key support level which indicates medium term reversal. With 6H action bias in downside red all the way through, and D action bias staying in red too, we'd now expect GBP/USD to sustain below this level to confirm the bearish case.

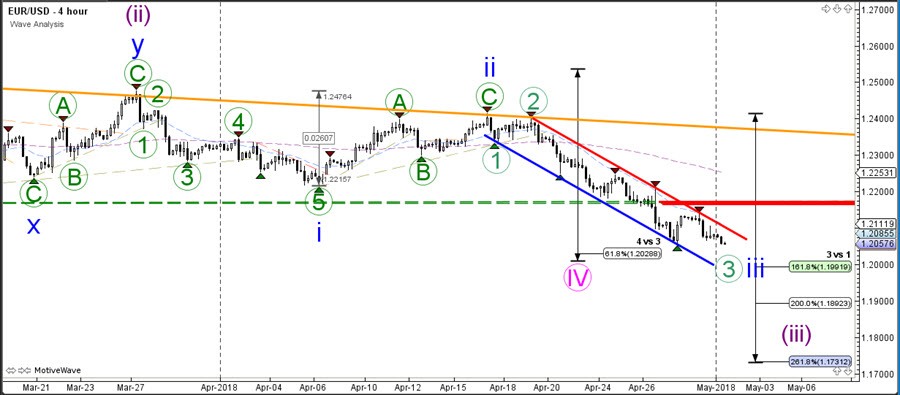

38.2% retracement of 1.1946 (2016 low) to 1.4376 at 1.3448 will be next target.

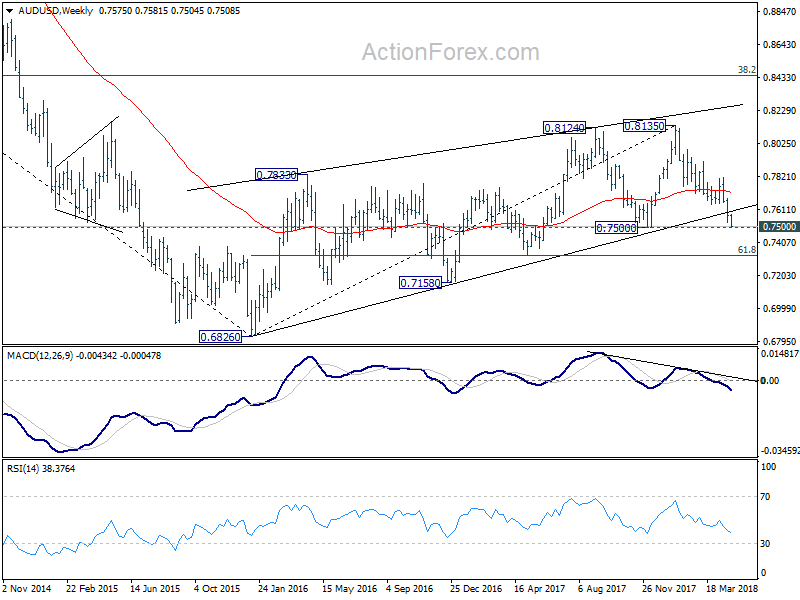

AUD/USD will be a pair to watch as it's heading to 0.7500 key support. 6H action bias is staying neutral so far, due to the deceleration late last week and on Monday. But firm break of 0.7500, with 6H action bias turning downside red will indicate solid downside momentum. And the by then, the medium term corrective rise from 0.6826 should be considered finished.

U.S Dollar Shines Despite Labour Day Recognition

Tuesday May 1: Five things the markets are talking about

Global equities again nudge a tad higher during a holiday shortened trading week in which many markets across both Europe and Asia are shut in observance of Labour Day.

The 'mighty' dollar is again supported, while sovereign bond prices edge lower, and most commodities slipp. One exception is crude oil, it's found support, and stimulated by Israel's accusation that Iran has a secret plan to continue building nuclear weapons.

Note: Markets are closed in Germany, France, Italy, Spain, China, Hong Kong, Singapore, India, and a host of other countries.

As the month of May gets underway, focus turns to central bank policy and economic data. The Federal Open Market Committee begins its two-day meeting today with a rate decision tomorrow (2:00 pm EDT).

Investors and dealers will closely watch for whether the Fed will make more explicit its threat to hike interest rates another three times this year.

On Tap: Canada will release its latest GDP numbers later this morning (08:30 am EDT).

1. Stocks find limited support in quiet trading

Market participation in Asia remained limited given holidays in China, Hong Kong, S. Korea, Singapore and Taiwan.

In Japan, the Nikkei eked out modest gains in holiday-thinned trade overnight, supported by buying in index-heavy stocks. The Nikkei ended +0.2% higher, while the broader Topix dropped -0.2%.

Down-under, Aussie shares firm to a seven-week high as financials rally. The S&P/ASX 200 index rose +0.5% at the close of trade. The benchmark added +0.7% on Friday.

Note: The Reserve Bank of Australia (RBA) sees 2018 and 2019 GDP growth to average a bit above +3% vs. +2.4% in 2017 and also affirmed that CPI will be a bit above +2% for this year. There was little reaction to the central banks statement (see below) as dealers are looking ahead to the bank's Friday's upcoming quarterly statement on monetary policy (May 4).

In Europe, regional bourses are mostly shut today in observance of May Day Bank Holiday with the exception of the U.K, Ireland and Denmark. The FTSE trades slightly higher following positive results from BP, which reported profits slightly ahead of consensus.

U.S stocks are set to open in the 'red' (-0.1%).

Indices: FTSE 100 +0.2% at 7524, S&P 500 Futures -0.1%

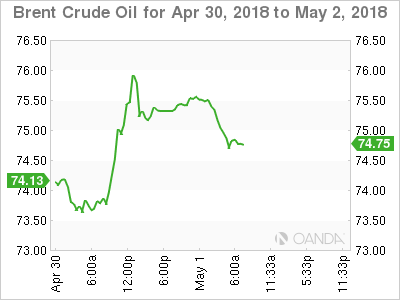

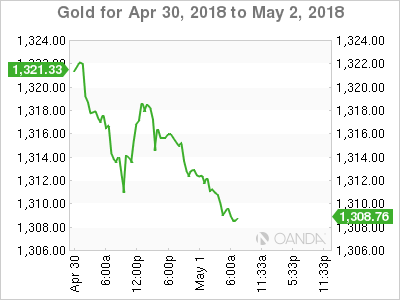

2. Oil pares gains, market supported by Iran worries, gold lower

Oil prices held steady overnight as the dollar remained near a four-month high, with crude supported by worries that President Trump may pull out of the Iran nuclear deal.

Brent crude oil for new July delivery is up +1c at +$74.70, while U.S West Texas Intermediate crude (WTI) for June delivery is up +2c at +$68.59 a barrel, after settling up +47c yesterday.

Note: Brent June contract expired on Monday, settling up +53c at +$75.17.

Oil prices have been better bid this week after Israeli Prime Minister Netanyahu stepped up pressure on the U.S to pull out of the 2015 nuclear deal with Iran – he presented so called evidence of a secret Iranian nuclear weapons program.

Temporarily capping prices is the rise in U.S production. According to Baker Hughes data on Friday, U.S drillers added five oilrigs in the week to April 27, bringing the total count to +825, the highest level since March 2015.

Note: U.S President Trump has until May 12 to decide whether to restore the sanctions on Iran that was lifted after an agreement over its disputed nuclear program.

Gold prices have inched lower ahead of the U.S open, trading atop of its six-week low touched yesterday, as the U.S dollar holds firm atop of its four month highs. Spot gold has fallen -0.1% to +$1,314.00 per ounce. U.S. gold futures for June delivery eased 0.3 percent to $1,315.10 per ounce.

Note: Prices slipped to +$1,310.11 on Monday, their lowest since March 21.

3. RBA on hold, credit crunch fears grow

Earlier this morning, the RBA left its cash rate target at +1.5% as expected, and continued to point to a solid pace of GDP growth this year and next.

Nevertheless, a number of analysts are warning of a mini housing crash – significant house price falls over coming years – which would put a dent in confidence, spending and growth. This in turn, would force many banks to adopt conservative lending practices, just like in Canada and Ireland.

In Europe, a softening in regional economic data and signs that inflationary pressures remain subdued, has been encouraging the European Central Bank (ECB) to hold off from raising interest rates until well into next year, and therefor supported the bond markets in recent weeks.

The yield on 10-year Treasuries have increased +1 bps to +2.96%, while in the U.K the 10-year Gilt yield backed up +1 bps to +1.418%, the biggest advance in more than a week.

4. Dollar in demand

The 'mighty' U.S dollar continues its firm tone against G10 currency pairs. The driver behind the greenback's strength has been the divergence between economic data in the U.S and the rest of the world. This has led to higher rate expectations in the U.S in the medium term.

The EUR/USD (£1.2032) continues to probe its four-month lows ahead of the psychological €1.2000 handle.

GBP/USD (£1.3693) is trading below £1.3700 handle and about 100 pips from its key support level of £1.3600, which was the breakout level from January. U.K data (see below) continues to disappoint (Apr PMI and Mar Mortgage Lending data miss expectations) as any BoE rate hike for this year seems to be priced out.

USD/JPY (¥109.62) is firmer by +0.35% just ahead of the NY open.

5. U.K consumer borrowing falls to a five-year low

Data this morning showed that U.K citizens cut back sharply on new borrowing in March, a fresh sign of economic weakness that makes it less likely that the BoE will hike later this month.

Total new lending to households fell to +£4.3B from +£5.5B in February.

Digging deeper, mortgage lending was slightly up from January at +£4.0B, but borrowing through credit cards and other forms of unsecured loans fell to +£254m from +£1B. It was the lowest level in six years.

Note: In February, the BoE signalled it was considering a rise in its key interest rate as early as a policy announcement scheduled for May 10. However, very weak growth at the start of the year has persuaded fixed income to reprice their curves to show a rate hike in late 2018.

USD/CAD – Canadian Dollar Steady Ahead Of Canadian GDP

The Canadian dollar continues to trade quietly. In the Tuesday session, USD/CAD is trading at 1.2869, up 0.20% on the day. On the release front, Canada releases GDP, which is expected to rebound with a gain of 0.3%. Later in the day, Bank of Canada Governor will speak about household debt an event in Yellowknife. In the US, today’s key event is ISM Manufacturing PMI, which is expected to drop to 58.4 points. The focus will shift to US employment indicators in the latter part of the week, starting with ADP Nonfarm Employment Change on Wednesday. As well, the Federal Reserve will release a rate statement.

US President Trump has extended exemptions for steel and aluminum tariffs for Canada and Mexico for another 30 days. The exemptions come at a sensitive time, with the US, Canada and Mexico neck deep in negotiations over a new NAFTA trade agreement. The talks have made significant progress, but the critical auto pact remains a stumbling block. It is likely that a tentative agreement will be hammered out, perhaps later this month. The Bank of Canada has dropped strong hints that it plans to raise interest rates later this year, but policymakers would like the NAFTA issue to be resolved before the next rate hike.

The Federal Reserve will be on center stage on Wednesday when it concludes a 2-day policy meeting. The markets are expecting the Fed to maintain the benchmark rate at a range between 1.50% and 1.75%, and analysts will be keeping a close eye on the rate statement – a hawkish statement could propel the US dollar to higher levels. There is growing sentiment that the Federal Reserve will raise interest rates four times this year, although Fed policymakers have not changed their forecast of three increases in 2018. One scenario envisions the Fed raising rates once each quarter until the economy shows signs of slowing down. If inflation continues to move higher and economic conditions remain strong, the dollar should continue to perform well against its Canadian counterpart.

EUR/USD – Weak Euro Heading To 1.20, European Markets Closed For May Day

EUR/USD continues to lose ground this week. In the Tuesday session, the pair is trading at 1.2037, down 0.36% on the day. On the release front, European markets are closed for May Day, so there are no eurozone or German releases. In the US, today’s key event is ISM Manufacturing PMI, which is expected to drop to 58.4 points. On Tuesday, the eurozone releases Preliminary Flash GDP, and Germany and the eurozone will publish PMI reports. The US will release ADP Nonfarm Employment Change and the Federal Reserve will release a rate statement.

German Retail Sales, the primary gauge of consumer spending, continues to struggle. The indicator dropped 0.6% in April, marking a fourth consecutive decline. At the same time, the German consumer continues to show optimism regarding the economy, as underscored by recent GfK consumer confidence reports. The indicator edged lower to 10.8, just shy of the estimate of 10.9 points. The indicator has hovered close to the 11-point level since July 2017.

The Federal Reserve winds up its monthly policy meeting on Wednesday. The markets are expecting the Fed to maintain the benchmark rate at a range between 1.50% and 1.75%, and analysts will be keeping a close eye on the rate statement – a hawkish statement could propel the US dollar to higher levels. There is growing sentiment that the Federal Reserve will raise interest rates four times this year, although Fed policymakers have not changed their forecast of three increases in 2018. One scenario envisions the Fed raising rates once each quarter until the economy shows signs of slowing down. If inflation continues to move higher and economic conditions remain strong, the dollar should continue to perform well against the euro and other major currencies.

Trade Tariffs, UK Data And Geopolitical Concerns Weigh

- White House announced that it has reached a better deal

- UK manufacturing number printed a reading which wasn’t overwhelming

- The precious metal itself is under pressure

Trump decided to extend relief from steel tariffs. Apparently, he is still in a process of striking a better deal with European Union, Mexico and Canada and this is why the deadline is pushed until 1st of June. There has been some fruit to his labour as White House announced that it has reached a better deal (agreement in principle) with like of Argentina, Australia and Brazil.Overall, these negotiations are mainly about quotas which would limit the amount of imports or in other words more protectionism.

Having said this, there is still very little when it comes to actually finding the details on this deal. Nonetheless, European markets have taken this as a sign of relief. We are seeing all the major indices in Europe firmly in green, however, investors over in the US aren’t feeling this optimism as the US futures are still trading lower.

Back in the UK, the manufacturing number printed a reading which wasn’t overwhelming at all. UK manufacturing sector is facing feeble growth and the spillover effects from the first quarter could easily impact the bottom line figure for the second quarter. Looking at Sterling, it is just falling off the cliff, it has fallen from its high of 1.4345 to 1.3673 (at the time of writing this article) in no time.

The upward move for the GBP/USD was purely driven due to the reason that investors were thinking that the Bank of England would hike the interest rate once again when they will meet next. This is because the economic data is supporting their stance. However, the reality was very different and today’s number has also confirmed that traders were clearly on the wrong side of the trade because the economy is no-where ready for another rate hike.

The precious metal itself is under pressure despite the fact that Israel has ranched up the geopolitical tensions yesterday. President Benjamin Netanyahu not only attached on Iran during his speech but an actual attack on Syria is also imminent. If that happens, we expect the geopolitical tensions to take a completely new dimension and gold would become the most favourite asset.

Expectations For BOE Rate Hike In 2018 Diminishes

Notes/Observations

- May Day holidays keeps market participation light in both Asia and Continental Europe

- UK data continues to disappoint making any hope of a BOE rate hike in 2018 a fantasy (Apr PMI and Mar Mortgage Lending data miss expectations)

- Focus on FOMC statement on Wed for fresh clues on rate path

Asia:

- (AU) Reserve Bank of Australia (RBA) left the Cash Rate Target unchanged at 1.50% (as expected); rhetoric unchanged (no rush to change policy stance)

- Japan Apr Final PMI Manufacturing: 53.8 v 53.3 prelim

- (JP) Japan Apr Domestic Vehicle Sales Y/Y: +0.5% v -4.9% prior

Europe:

- House of Lords votes 335-244 to restrict possibility of PM May choosing a no deal Brexit. Gives the Parliament extra powers over EU exit deal. Amendment 'would force PM May to let parliament bind ministers’ hands if the terms of the final deal had not been approved by the House of Commons, and discussed by the House of Lords, by the end of January 2019. The same conditions would apply if the withdrawal agreement with the EU was not finalized by 28 February 2019'

- UK govt said to propose a new plan to kick start Brexit talks and make progress on the issue of the Irish border as negotiations resume in Brussels on Tuesday, May 1st . UK said to have drafted a new template for how the UK/EU should work together on the UK’s two favored options for resolving the border issue

- PM May said to be considering signing up Britain to a “catch-all” agreement with Brussels that Brexiteers fear will amount to “EU Mark II”

- Greece growth strategy document: assumes GDP growth above 2% over the medium term and maintain primary surplus at 3.5% of GDP until 2022

Americas:

- US President Trump delays decision on steel and aluminum tariffs for the EU, Canada and Mexico (Argentina, Brazil and Australia were also granted extensions); decision now expected by June 1st

- Treasury Sec Mnuchin: President Trump was still considering the Iran deal. US delegation to hold trade talks in China on Thursday and Friday to discuss trade imbalance, IP rights, joint technology and joint ventures with Chinese officials. Reiterated about being optimistic about trade talks with China

Economic Data:

- (PE) Peru Apr CPI M/M: -0.1% v +0.1%e; Y/Y: 0.5% v 0.7%e

- (IE) Ireland Apr Manufacturing PMI: 55.3 v 54.1 prior (59th month of expansion)

- (AU) Australia Apr Commodity Index (AUD): 109.0 v 112.4 prior; Commodity Index SDR Y/Y: -1/4% v -2.5% prior

- (NL) Netherlands Apr Manufacturing PMI: 60.7 v 60.5e (56th month of expansion but lowest since Oct)

- (UK) Apr Manufacturing PMI: 53.9 v 54.8e (21st month of expansion but lowest since Nov 2016)

- (UK) Mar Mortgage Approvals: 62.9K v 63.0Ke

- (UK) Mar Net Consumer Credit: £0.3B v £1.4Be; Net Lending: £4.0B v £3.6Be

- (UK) Mar M4 Money Supply M/M: -1.4% v -0.4% prior; Y/Y: 2.2% v 4.2% prior; M4 Ex IOFCs 3M Annualized: 1.2% v 3.0% prior

- (DK) Denmark Apr PMI Survey: 53.3 v 62.3 prior

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [FTSE 100 +0.2% at 7524, S&P 500 Futures -0.1%]

- Market Focal Points/Key Themes: European Markets are mostly shut today in observance of May Day Bank Holiday with the exception of the UK, Ireland and Denmark. The FTSE trades slightly higher following positive results from BP, which reported profits slightly ahead of consensus. In other earners, Plus500 trades sharply higher after strong Q1 results, Just Eat, Virgin Money and Carlsberg other names trading higher following results. Looking ahead, a busy morning for US corporate earnings with healthcare names Pfizer and Merck expected to report, with other notable names including Emerson Electric, Cummins, Autonation, Anthem, HCA and Under Armour.

Movers

- Consumer Discretionary [Carlsberg [CARLB.DK] +0.5% (Earnings), Just Eat [JE.UK] +4.3% (Trading update), Connect Group [CNCT.UK] -4.0% (Earnings)]

- Financials [Plus500 [PLUS.UK] +6% (Earnings), Virgin Money [VM.UK] +3.7% (Earnings) ]

- Energy [BP [BP.UK] +0.7% (Earnings)

Speakers

- Italy President Mattarella said to decline the request for new elections in June

Currencies

- USD continued its firm tone against the major pairs. The driver behind the greenback strength has been the divergence between economic data in the US and the rest of the world.

- EUR/USD probing 3 ½ month lows at 1.2035 area with psychological support pegged at 1.2000

- GBP/USD trading below 1.3700 handle and about 100 pips from its key support level of 1.36 (breakout from Jan). UK data continued to disappoint (Apr PMI and Mar Mortgage Lending data miss expectations) as any BOE rate hike in 2018 seems to be dissipating from radar.

- USD/JPY firmer by 0.2% at 109.55 just ahead of the NY morning.

Fixed Income

- Gilt futures finished yesterday at 122.37 higher by 34 ticks, as the spread between the 10-year reaches a 34-year high. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Corporate issuance saw 6 issuers raise $8.2B in the primary market

Looking Ahead

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (AU) RBA Gov Lowe

- 05:30 (UK) BOE allotment in 6-month GBP-enhanced liquidity repo operation (ILTR)

- 06:00 (IE) Ireland Apr Unemployment Rate: No est v 6.1% prior

- 06:45 (US) Daily Libor Fixing

- 07:30 (IN) India Mar Eight Infrastructure (Key) Industries: No est v 5.3% prior

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (CA) Canada Feb GDP M/M: +0.3%e v -0.1% prior; Y/Y: 2.8%e v 2.7% prior

- 08:30 (CA) Canada Mar MLI Leading Indicator M/M: No est v 0.2% prior

- 08:55 (US) Weekly Redbook Sales

- 09:00 (EU) Weekly ECB Forex Reserves

- 09:30 (CA) Canada Apr Manufacturing PMI: No est v 55.7 prior

- 09:30 (NZ) Fonterra Global Dairy Trade Auction

- 09:45 (US) Apr Final Markit Manufacturing PMI: 56.5e v 56.5 prelim

- 10:00 (US) Mar Construction Spending M/M: 0.5%e v 0.1% prior

- 10:00 (US) Apr ISM Manufacturing: 58.4e v 59.3 prior; Prices Paid: 78.5e v 78.1 prior

- 11:30 (US) Treasury to sell 4-Week Bills

- 14:30 (CA) Bank of Canada (BOC) Gov Poloz

- 16:30 (US) Weekly API Oil Inventories

Dollar Rally Continues, RBA Stays On Hold

RBA stays on the sidelines

As broadly expected, the Reserve Bank of Australia held the Cash Rate Target at 1.5%. Amid the release of the statement, the volatility increase temporarily as investors try to read between the lines; however, the Aussie quickly stabilised and even eased slightly as the greenback rose across the board. AUD/USD slid to 0.7520 during the European morning as the dollar kept pushing higher. Indeed, after increasing 0.35% on Monday, the dollar index rose 0.15%.

The RBA maintained its well-known caution, especially regarding developments in the FX market, saying “on a trade-weighted basis [the Australian dollar] remains within the range that it has been in over the past two years” and adding, “An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast”. Nevertheless, Governor Lowe was quite optimistic regarding the growth outlook and remained confident that China’s growth will stay solid. The Bank expects that growth will average “a bit above 3% in 2018 and 2019“ as non-mining business investment continues to increase. Nevertheless, the institution expressed reserves about the outlook for household consumption, naming high debt level and slowing growth of income as source of uncertainties.

Overall, the RBA seems to be happy with the current situation and sees no reason to change the monetary environment at the moment. Therefore, AUD/USD will most likely be driven by the US dollar in the near term. Given the fact that investors have turned more optimistic about the buck lately, we expect further downside in AUD/USD.

German core inflation slowdown amid manufacturing activity decline

German inflation data supports last Thursday Draghi’s ECB meeting view of a slowdown in European economy. April inflation remained stable, given 1.60% (consensus: 1.50%) while core inflation declined, at 1.40% (prior: 1.50%) due to a decline in services and manufacturing activities. The situation remains however comfortable for the German economy and the EU as a whole. Supported by an unemployment rate at historical lows (March: 5.30%), consumer confidence at its highest level and wage growth above 4% (Eurozone: 2% range), German underlying inflation is expected to accelerate in the near term.

As Italian and Portuguese inflation data also disappointed in April, we expect Eurozone March inflation data published on May 3, 2018 to decline below the 1% threshold, most probably at 0.90%. We remain however confident that this inflation downturn should not be worrisome for the EU economy. Expansion in the EU shall continue.

Due to disappointing inflation data among EU members, we expect the single currency to decline further against most peers. EUR/USD strong decline continues, approaching hourly support at 1.2028 (11/01/2018 low) and heading along the 1.2035 range.

Breakouts And Wave Patterns For EUR/USD, GBP/USD, And USD/JPY

The EUR/USD made a bullish retracement which respected the broken support and new resistance zone (red). Price is now continuing with the downtrend and testing the previous bottom plus 1.20 round level. The bearish wave 3 (blue) needs to reach at least the 161.8% Fibonacci target which is the minimum for an impulsive wave 3. A break below would 1.20 would make the downtrend scenario more likely whereas a failure to break could still indicate that the 61.8% Fib is holding of the bullish wave 4 (pink) scenario.

The EUR/USD bounced at the 23.6% Fibonacci retracement level and broke below several support levels. Price is now on its way to test the 1.20 psychological round level.

The GBP/USD is still pushing lower. The bearish momentum remains active and the downtrend is expanding the wave 5 (purple). A bearish break below 1.37 could see price make an extension towards the Fibonacci targets.

The GBP/USD is probably completing a wave 4 (blue) correction.

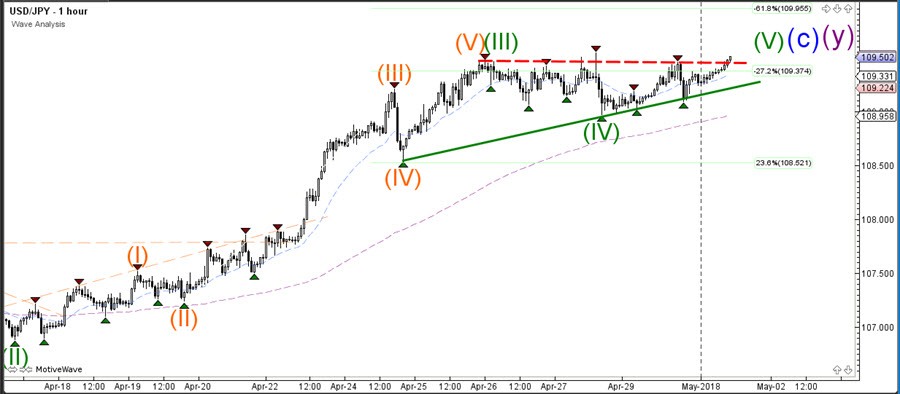

The USD/JPY uptrend seems to be ready for a bullish continuation towards the psychological round level of 110, which is also a 38.2% Fibonacci level of the potential wave D (light purple). This could be a resistance zone where price completes a wave W (pink).

The USD/JPY has completed a wave 4 (green) correction and is extending the wave 5 (green).

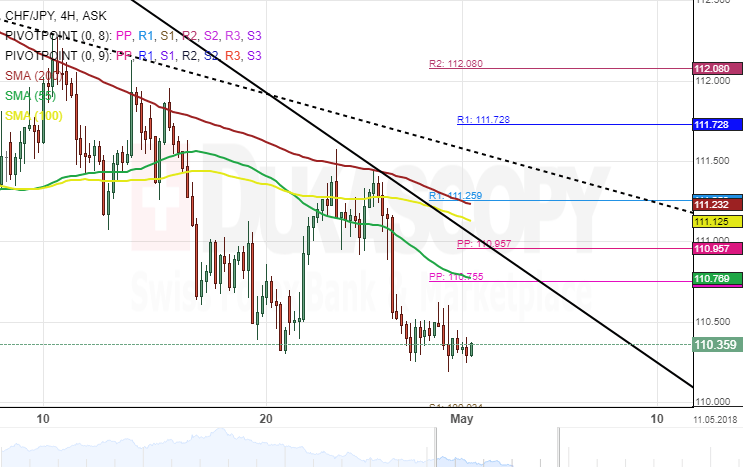

CHF/JPY 4H Chart: Further Decline In Sights

The Swiss Franc has depreciated substantially against the Japanese Yen during the past one month. This bearish movement has been stranded in a three-month descending pattern whose upper boundary was hit on April 24.

The 200– hour simple moving average has provided strong resistance for the currency pair and thus sending the pair further south. However, this fall could encounter a support formed by the monthly S1 at 109.93.

As for near future, the CHF/JPY exchange rate is likely to continue to losing strength. Meanwhile, technical indicators demonstrate that bears could grow stronger during the following trading sessions.

UK PMI manufacturing dropped to 17 month low, GBP/USD breaks 1.3711 key support

GBP/USD breaks 1.3711 key support today, partly due to USD's broad based rally, partly due to another data miss. The development suggests that GBP/USD's medium term rally from 1.1946 has completed and the trend is reversing.

UK PMI manufacturing dropped to 53.9 in April, down from 55.1, below expectation of 54.8. That's also the lowest level in 17 months.

Comments from Rob Dobson, Director at IHS Markit:

"The start of the second quarter saw the UK manufacturing sector lose further steam. The headline PMI dipped to a 17-month low as growth of production, new business and employment all slowed.

"While adverse weather was partly to blame in February and March, there are no excuses for April's disappointing performance, making the chances of a near term hike in interest rates by the Bank of England look increasingly remote.

"On this footing, the sector is unlikely to see any improvement on the near-stagnant performance signalled by the opening quarter's GDP numbers.

"Looking ahead, the trend in manufacturing production is likely to remain subdued. Weak demand meant firms are seeing backlogs of work fall and stocks of unsold goods rise, limiting the need for output to rise in May. Business optimism has also dipped to a five-month low as concerns about Brexit, trade barriers and the overall economic climate remained widespread."

Also from UK, mortgage approvals dropped to 62.9k in March, down from 63.8k, missed expectation of 63.0k. M4 money supply dropped -1.4% mom in March, below expectation of 0.2% mom.