Sample Category Title

Oil Ticks Higher As Dollar Bulls Remain In Charge

When oil markets are headed towards rebalancing, any shocks due to supply shortage may lead to a huge spike in prices. Brent prices fell on Tuesday to a low of $73.47, indicating that $75 may be a short-term top. This was before Israeli Prime Minister Benjamin Netanyahu's intervention, who claimed to have proof that the 2015 Iran nuclear deal is based on ‘lies'. There are those who remain sceptical of the Iran nuclear deal, and it will be interesting to monitor if the European Union makes any comment following the claims of the Israeli Prime Minister.

Trump probably doesn't need a big push. He said that Netanyahu's news conference about Iran's nuclear program has helped prove that he has been right in his criticism of the deal. Now, the chances of the U.S. pulling out of the deal seems more likely, but his European friends don't seem to want to take the same path.

If the U.S. pulls out of the agreement on May 12th or before, Iranian oil exports are expected to plunge. Although it's difficult to assess the magnitude of the fall, it's estimated to be around 400,000 barrels a day. While this might not seem to be a significant amount, when taking into consideration the drop in global inventories, the robust demand, and the level of compliance of OPEC & partners, oil may quickly add an additional $5 to current prices.

While OPEC can easily cover this shortage, I don't think they are willing to. Venezuelan oil output has fallen by more than 500,000 barrels a day due to the country's current economic crisis, but we haven't seen any willingness from OPEC to pick up this shortage. The same is expected if Iran's output plunges.

Greenback steady at 15-week high

The dollar Index is trying to flirt with the 92 level, a price last seen on January 11th. A couple of months ago, it was thought the dollar would remain weak due to its robust economic performance in the E.U. and elsewhere; however, since the beginning of the year it seems the U.S. economy is firing on all cylinders, while the E.U. and the U.K. have started to show signs of slowing down.

Yesterday's data showed personal income rose 0.3% in March, while consumer spending hit 0.4%. More importantly, the PCE price index jumped 2% YoY in March to finally hit the Fed's target. However, this was widely anticipated by markets and doesn't seem to alter the Fed's gradual pace of interest rate hikes.

Going forward, interest rate differentials are likely to be a good indicator of how the dollar performs. The relationship between yields and the dollar has returned after breaking up at the beginning of the year. If the Fed sounds a little more hawkish tomorrow, and Friday's Non-Farms Payroll report surprises to the upside, the U.S. 10-year Treasury yields will easily retake the 3% level, providing a further boost to the U.S. currency.

A look at 10- and 30-year yield after yesteday’s sharp fall

The sharp fall in 10 year yield yesterday, down -0.021 to close at 2.936, is in line with our view that TNX has topped out in near term. And we'll likely see more downside in near term. First line of defence is at 55 day EMA (now at 2.827). But as mentioned in the weekly report, if fall from 3.035 is correcting the five wave sequence from 2.033, then it could drop further to 2.717 support before completion. We'll continue to see how it's playing out given the number of important events in US this week, including FOMC, ISMs and NFP. But after all, having some consolidations before another take on key resistance of 2013 high at 3.036 is not unreasonable.

30 year yield's sharp fall also confirmed short term topping at 3.219 after failing 3.221 near term resistance. For now TYX would dip lower back to 55 day EMA (now at 3.062). Or it would have another take on 50% retracement of 2.651 to 3.221 at 2.936.

Meanwhile, we'd like to point out again that while there is some downside for yields, we're not expecting it to drag down the Dollar. Instead, they might just give no support to the greenback.

EU: Should be fully and permanently exempted by US steel tariffs

Some responses from Europe regarding US extension of temporary exemptions on steel and aluminum tariffs.

European Commission criticized that the extension prolongs market uncertainty, which is already having an impact of business decisions. It also reiterated in a statement that "the EU should be fully and permanently exempted from these measures, as they cannot be justified on the grounds of national security."

UK Department for International Trade spokesman welcomed the "positive decision". And the government said in a statement that "We will continue to work closely with our EU partners and the US government to achieve a permanent exemption, ensuring our important steel and aluminum industries are safeguarded." But, "we remain concerned about the impact of these tariffs on global trade and will continue to work with the EU on a multilateral solution to the global problem of overcapacity, as well as to manage the impact on domestic markets."

RBA Leaves Rate On Hold

General Trend:

- Market participation in Asia remains limited given holidays in China, HK, South Korea, Singapore and Taiwan

- Earnings in focus: Hitachi rises after guiding FY19 results higher y/y; Sony, Honda decline after issuing outlook

- Australian financials ANZ Bank and ASX rise after earnings reports

- US President Trump delays decision on steel and aluminum tariffs for the EU, Canada and Mexico; decision now expected by June 1st; initial market reaction limited

- RBA sees 2018 and 2019 GDP growth to avg a bit above 3% v 2.4% in 2017; affirms CPI seen a bit above 2% in 2018

- Little initial bond market reaction to RBA statement; traders are looking ahead to the central bank’s upcoming quarterly statement on monetary policy (Friday, May 4th)

- In April, Australia’s combined capitals report first annual decline in dwelling values since late 2012, led by Sydney (Corelogic)

- Japan April Manufacturing PMI revised higher; sales to overseas clients however increased at a ‘markedly slower rate’, says IHS/Markit

- South Korea exports in April decline for first time since 2016, some cite difficult comparisons; exports to the US -1.8% y/y

- New Zealand March building permits rise on apartment projects

- New Zealand government announces a ‘Amazon tax’

- Apple expected to report Q2 results after US equity close on Tuesday May 1st

- US Treasury Sec Mnuchin confirms US trade delegation to hold talks in China on Thursday and Friday (May 3-4th)

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.1%; closed +0.2%

- TOPIX Marine Transportation index +1.5%, Iron & Steel +1.3%, Real Estate +1.2%, Retail trade +0.5%; Electric Appliances -0.6%

- Mega-banks trade generally lower

- Start Today, [+15%], 3092.JP Reports FY17/18 Net ¥20.2B v ¥17.0B y/y, Op ¥32.7B v ¥26.3B y/y, Rev ¥98.4B v ¥76.4B y/y To buy back up to 3.21% of shares for ¥25.0B

- (JP) Japan Apr Final PMI Manufacturing: 53.8 v 53.3 prelim

Korea

- Kospi opened closed for holiday

- (KR) North Korea nuclear test said to still be operational - Korean press

- (KR) SOUTH KOREA APR TRADE BALANCE: $6.6B V $8.5BE; Exports y/y: -1.5% v 3.3%e (1st decline in 18-months); Imports y/y: +14.5% v 16.0%e

- (US) Exempts South Korea, Argentina, Brazil and Australia from steel and aluminum tariffs

China/Hong Kong

- Hang Seng opened closed for holiday, Shanghai Composite closed for holiday

- (HK) Macau Apr Gaming Rev MOP25.7B v MOP24Be, y/y: 27.6% v 20.2%e (21st consecutive month of growth)

- (US) Treasury Sec Mnuchin: US delegation to hold trade talks in China on Thursday and Friday

- (HK) Hong Kong pre-owned home prices up for 2 consecutive years - SCMP

- SkyBridge Capital and HNA Capital confirm mutual agreement not to pursue transaction

- (CN) China Dalian Commodity Exchange (DCE) will open iron ore futures trading to foreign capital in May 4th

Australia/New Zealand

- ASX 200 opened +0.1%, closed %

- ASX 200 Financials index +1.4%, REIT +0.9%, Resources +0.6%, Energy +0.6%, Telecom +0.6%

- (AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50%; AS EXPECTED (18th straight pause in the current easing cycle)

- (AU) Fitch: Australia big four banks A$1.3T mortgage books can withstand an Ireland-style correction in property prices but the lenders' ability to deal with second-order impacts remains uncertain - AFR

- ANZ.AU Reports H1 (A$) Adj Cash profit 3.49B (un-adj 2.88B) v 3.6Be; Net interest income 7.35B v 7.46B y/y

- (AU) Australian Dairy Farmers lobby group has refused to back calls by the Australian Competition and Consumer Commission for a mandatory code of conduct for milk processors – AFR

- CBA.AU APRA applies A$1.0B add on to minimum capital requirement

- (AU) Australia Apr AIG Performance of Manufacturing Index: 58.3 v 63.1 prior

- FCG.NZ Reports Mar NZ Milk collection 143M kgms, -3% y/y; Dairy exports 11.0K MT, +4% y/y

- (NZ) New Zealand Mar Building Permits m/m: 14.7% v 6.4% prior

- (NZ) New Zealand Government: To tax low-value goods from abroad, effective Oct 20th

Other Asia

- (SG) Singapore PM Lee: Good chance 2018 GDP will exceed 2.5%

North America

- US equity markets ended lower: Dow -0.6%, S&P500 -0.8%, Nasdaq -0.8%, Russell 2000 -0.9%

- S&P500 Health Care -1.5%, Industrials -1.3%

- (US) Treasury Sec Mnuchin: Does not expect to see a lot of inflation

Europe

- (US) President Trump to postpone steel and aluminum tariff exemption decision for EU, Canada and Mexico until June 1st; finalizes deal to exempt South Korea on steel

- (UK) House of Lords votes 335-244 to restrict possibility of PM May choosing a no deal Brexit; Gives the Parliament extra powers over EU exit deal

- (EU) EU responds to US announcement extending EU's exemption from US tariffs on steel and aluminium imports to June 1st:The US decision prolongs market uncertainty, which is already affecting business decisions. The EU should be fully and permanently exempted from these measures, as they cannot be justified on the grounds of national security.

Levels as of 02:00ET

- Hang Seng closed; Shanghai Composite closed; Kospi closed

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.2%, Dax -0.2%; FTSE100 +0.3%

- EUR 1.2084-1.2067; JPY 109.40-109.24; AUD 0.7546-0.7527;NZD 0.7041-0.7031

- Jun Gold -0.5% at $1,312/oz; Jun Crude Oil +0.2% at $68.69/brl; Jul Copper -0.9% at $3.05/lb

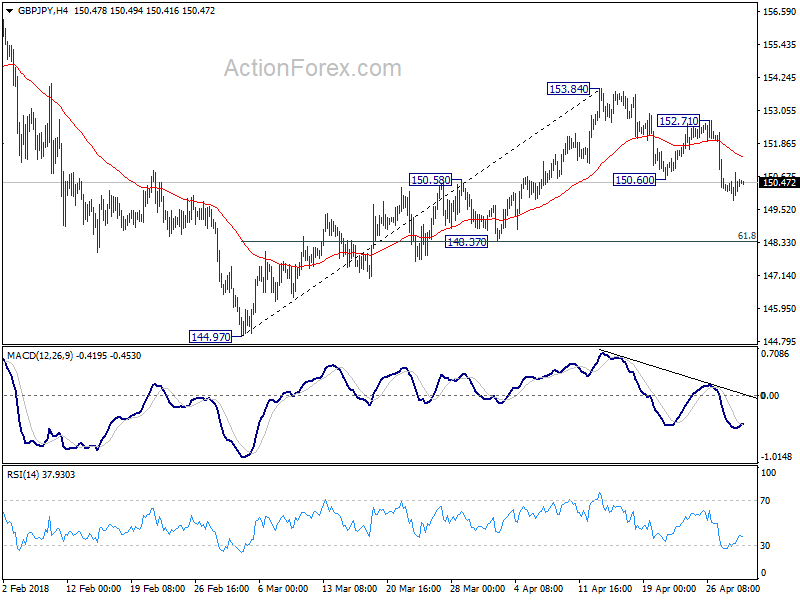

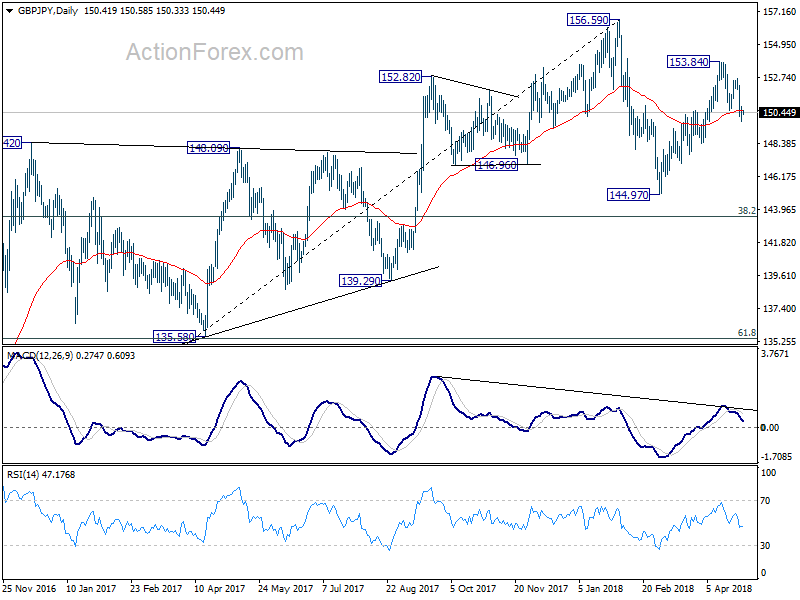

GBP/JPY Daily Outlook

Daily Pivots: (S1) 149.92; (P) 150.38; (R1) 150.92; More...

GBP/JPY's fall from 153.84 is still in progress and deeper decline would be seen to 148.37 support first. Current fall from 153.84 is seen as the third leg of the corrective pattern from 156.59. Break of 148.37 will pave the way to 144.97 and below. On the upside, break of 152.71 resistance is needed to indicate completion of the decline. Otherwise, near term outlook will remain cautiously bearish in case of recovery.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

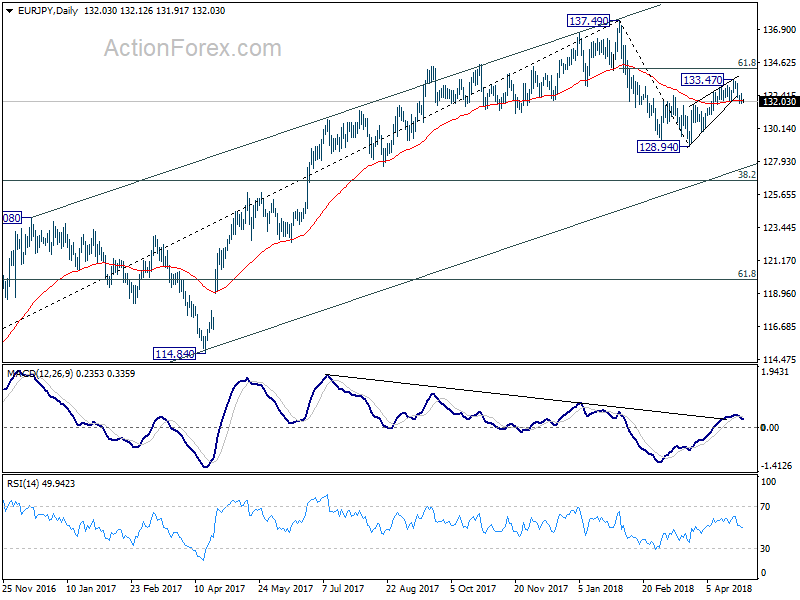

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.76; (P) 132.15; (R1) 132.44; More....

Outlook in EUR/JPY remains unchanged. Corrective rise from 128.94 has completed at 133.47 already. Deeper decline should be seen back to retest 128.94 low. Break there will resume whole decline from 137.49. On the upside, above 133.47 will extend the rebound. But we expect strong resistance from 61.8% retracement of 137.49 to 128.94 at 134.22 to limit upside and bring near term reversal eventually.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. The first leg has completed at 128.94. The second leg might be finished at 133.47 or it might extend. But after all, we'd expect another decline through 128.94 to 38.2% retracement of 109.03 to 137.49 at 126.61 before completing the correction.

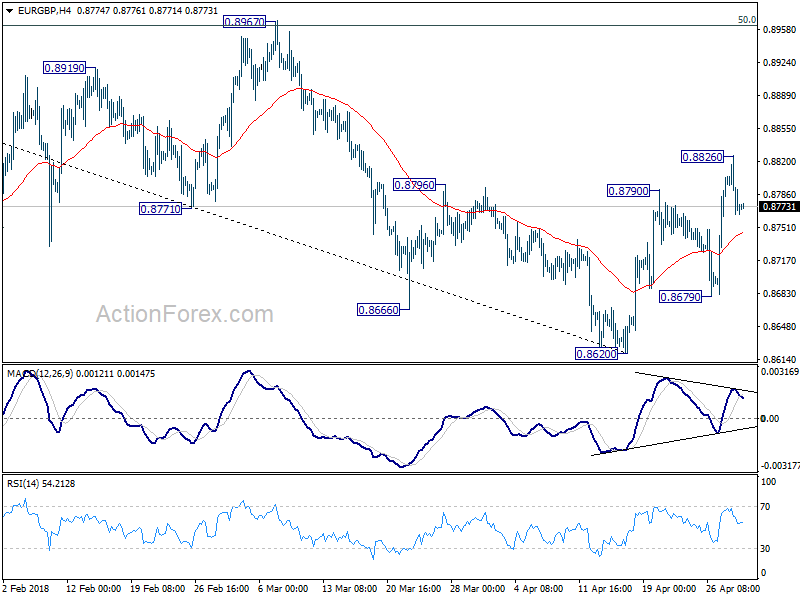

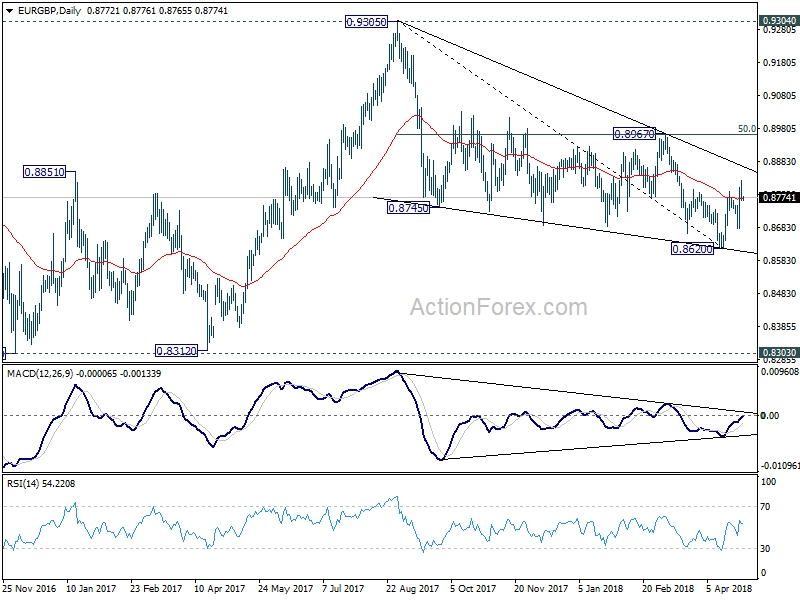

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8751; (P) 0.8788; (R1) 0.8812; More...

EUR/GBP retreated after hitting 0.8826 and intraday bias is turned neutral. On the upside, above 0.8826 will resume the rebound from 0.8620 and target 0.8967 cluster resistance next (50% retracement of 0.9305 to 0.8620 at 0.8963). Firm break there will confirm neat term reversal. On the downside, below 0.8679 will turn bias to the downside for 0.8620 instead.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

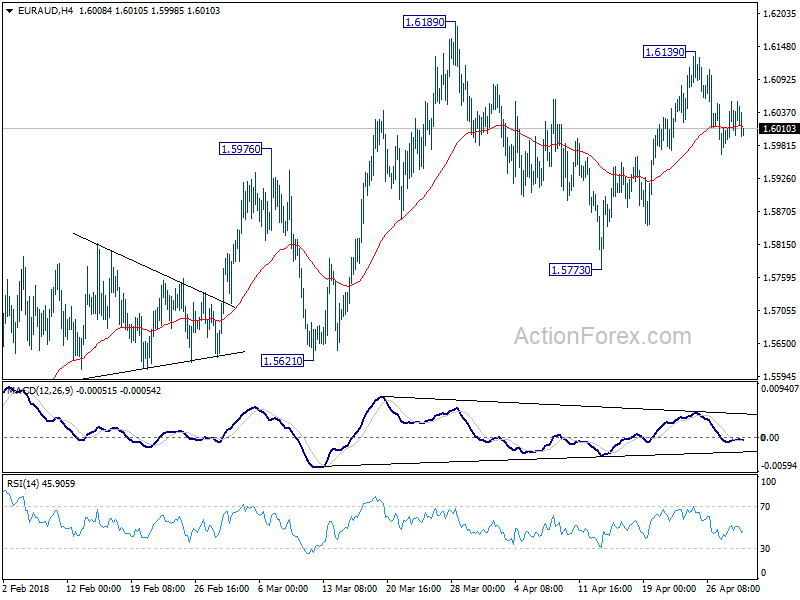

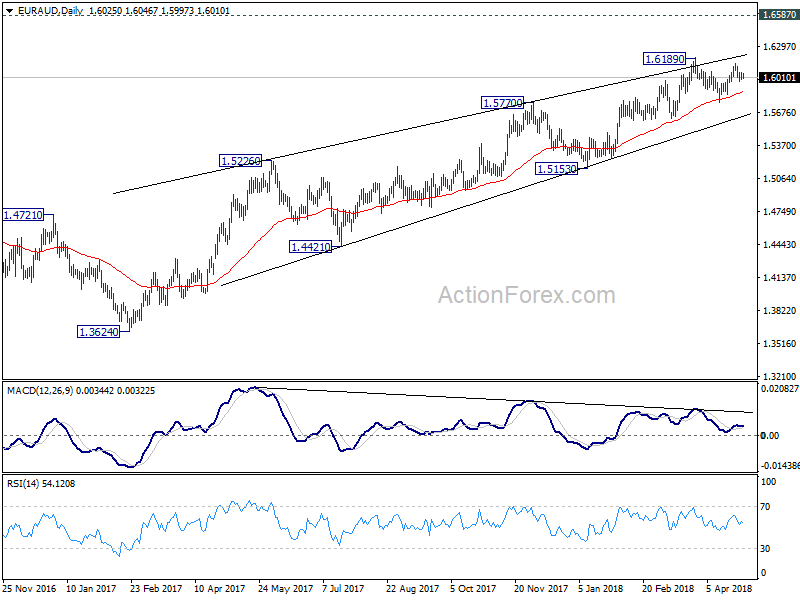

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6003; (P) 1.6030; (R1) 1.6067; More....

No change in EUR/AUD's outlook. Fall from 1.6139 is seen as the third leg of the consolidation pattern from 1.6189. Deeper decline could be seen back to 1.5773 support, and possibly below. But downside should be contained above 1.5621 to bring rise resumption. On the upside, above 1.6139 will target 1.6189 high again.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. EUR/AUD also drew strong support from 55 day EMA and rebounded. Current rally from 1.3624 could still extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal. On the downside, sustained break of 1.5621 support should confirm reversal and turn outlook bearish for 1.5153 support and below.

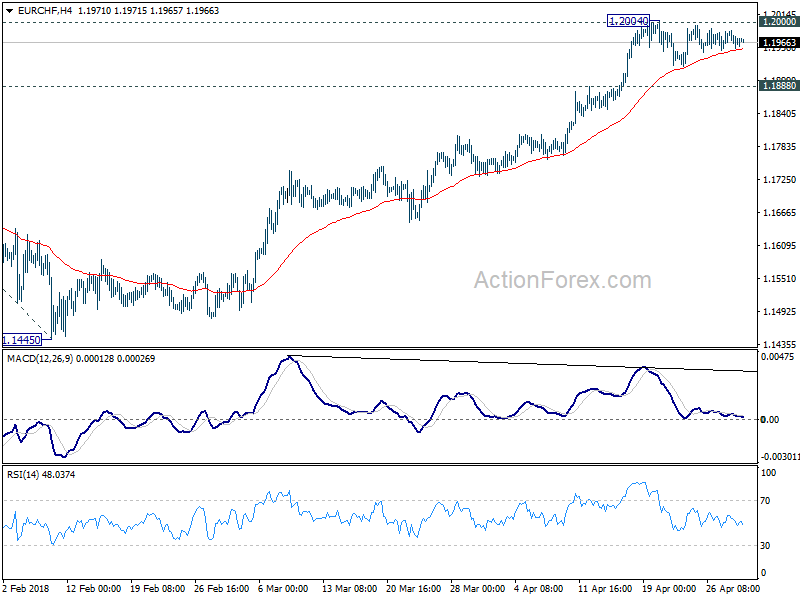

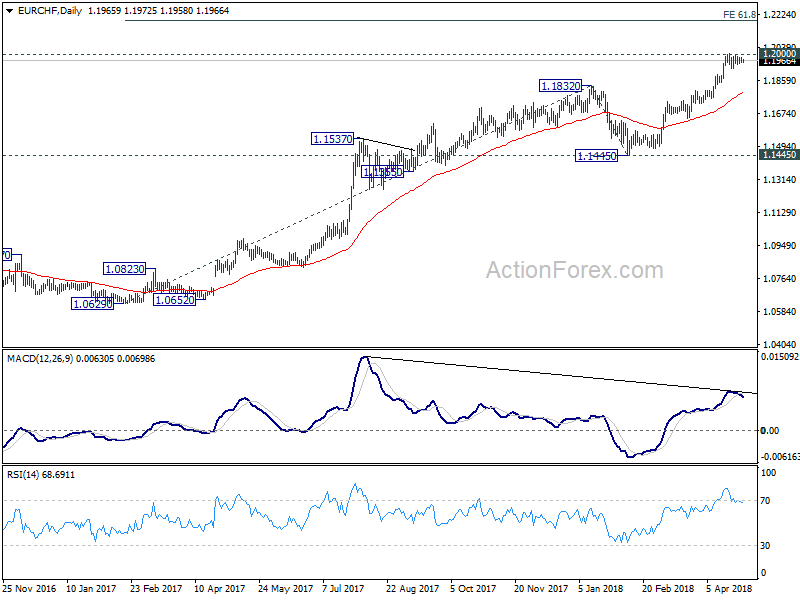

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1952; (P) 1.1969; (R1) 1.1984; More...

EUR/CHF's consolidation from 1.2004 is still unfolding and intraday bias remains neutral. Deeper retreat cannot be ruled out. But further rise is expected as long as 1.1888 minor support holds. Decisive break 1.2 will pave the way to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. However, consider bearish divergence condition in 4 hour MACD, break of 1.1888 will indicate short term topping. In that case, deeper pull back would be seen back to 1.1445/1832 support zone.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2003 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2049; (P) 1.2093 (R1) 1.2124; More....

Intraday bias in EUR/USD remains neutral and consolidation from 1.2054 temporary low could extend. In case of another rise, upside should be limited by 1.2214 support turned resistance to bring another decline. Below 1.2054 will target 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991 first. Break will target 200% projection at 1.1891.

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.