Sample Category Title

FOMC Preview: Focuses on Inflation and Shrugs Off Temporary Disruption on Growth

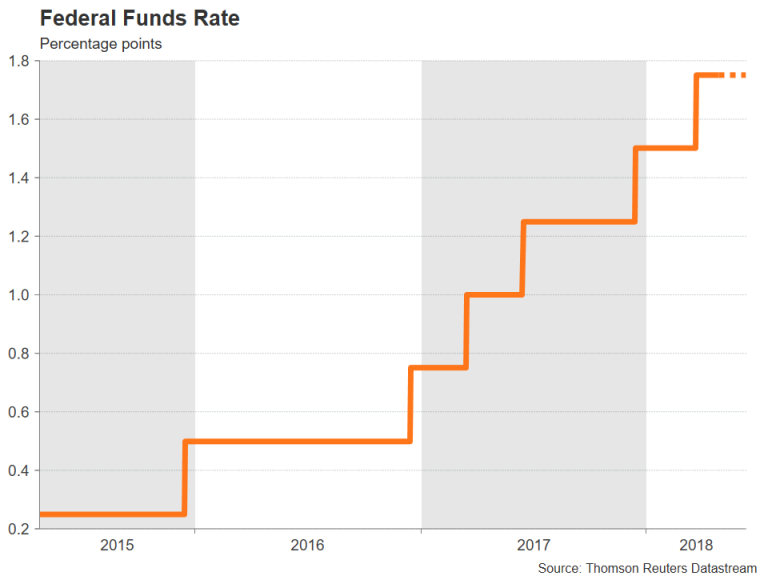

There have been both positive and negative data released since the March FOMC meeting. We expect policymakers to view slowdown in GDP growth as driven by temporary factors which should not affect the monetary policy outlook. Meanwhile, the central bank would likely acknowledge recent pickup in core inflation and wage growth, hailing them as reasons supporting further gradual rate hike: The median dot plot suggested three rate hikes this year while the market has increasingly priced in four. We expect the Fed to leave the policy rate unchanged at 1.50-1.75% at the May meeting, leaving the rate hike (+25 bps) for June, when the updated staff projections would also be published.

Real GDP grew +2.3% (annualized) in 1Q18, easing from +2.9% in the prior quarter. However, from a year ago, 1Q18 GDP actually expanded +2.9% from 1Q17. In this sense, US economy has accelerated in the first quarter of the year, compared with +2.6% y/y in 4Q17 and +2% y/y in 1Q17. While the headline reading is subjected to two revisions in coming months, the slowdown can be attributed to severe weather in the first quarter and the delayed tax refund. On the job market, nonfarm payrolls increased +103K in March, significantly missing consensus of a +193K addition. However, the unemployment rate stayed at 4.1% for the fifth consecutive month. While both the ISM manufacturing and non-manufacturing indices moderated in March from the prior month, the reading stayed in elevated levels of 59.3 and 58.8 respectively, indicating strong momentum in economic activities.

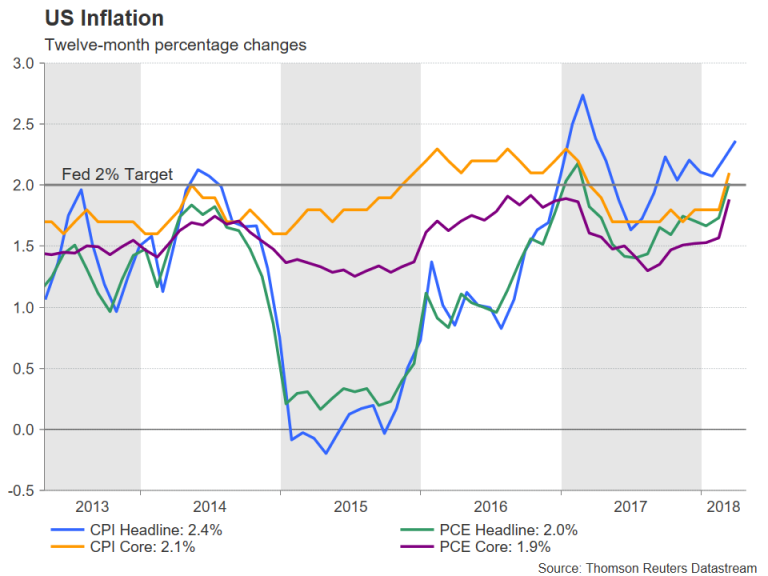

The key positive note has come from inflation. Headline CPI jumped to +2.4% y/y in March, highest in a year. Core CPI also rose to +2.1% during the month. PCE, the Fed’s preferred inflation gauge hit the +2% target again in March. We believe the Fed welcomes these developments as they support further gradual interest rate normalization. Backing the price dynamics is the pickup in wage growth. Thanks to the decade-low unemployment rate, average wage growth increased +2.7% y/y in March. Indeed, a report by the Labor Department, released last week, suggested that said wages and salaries jumped +0.9% q/q in 1Q18, compared with +0.5% in 4Q17. This also marks the biggest increase since 1Q07.

As noted above, the intermeeting dataflow largely allow the Fed to maintain its confidence over the economic outlook. Trade tensions would probably be discussed at the meeting but we do not expect the situation would have any effect on the current outlook. Another topic would be tighter credit conditions. 10-year US Treasury yield breached 3% last week for the first time since December 2013. The 2-year yield have risen 16 bps, while 10-year yield up +5 bps, from the March meeting, as of April 27. This also suggests that the yield curve has reached the flattest level in 6 years. We expect the Fed to discuss the possible consequences in the upcoming, though the details would unlikely be revealed until publication of the minutes.

Shaky Shaky

Shaky Shaky

Holiday thinned trading conditions in Singapore and the rest of Asia today suggests liquidity will be tight. However, with headline riks evolving, traders will remain ever so vigilant.

Global equity sentiment remains a bit shaky as concerns over rising commodity prices and higher interest rates continue to suggest lower corporate margins for the remainder of 2018. While trade concerns and uncertainty over Iran policy continue to weigh.

China has made it clear they will not be a pushover when it comes to trade discussions while Israeli Prime Minister Benjamin Netanyahu pulled few punches accusing Iran of lying about its nuclear intentions and ratcheting up geopolitical concerns in the process.

Trade negotiations were never going to be a walk in the park, but as long as both parties remain at the table, despite both sides rolling out their respective masters in the art of brinkmanship, there remains a light at the end of the tunnel. However, not surprisingly there remains much focus on these high-level discussions.

The Dollar continued to make headway in thinly traded markets ignoring softer US data prints and lower US Treasury yields. However, traders continue to rely on a favourable USD bounce on the back of the plethora of top-tier data later this week – with ISM, and of course, NFP/AHE to top off the week. USD traders have been reacting favourably to the fortifying in US data flow relative to that from other major economies and in particular the EU given that expectations on the EU data landscape had been running high amongst investors.

Given the massive short positions in US Treasuries, and as evidenced by the lack of following through above 3 % ten year UST, traders are looking for reliable economic data to support the fundamental economic landscape. If yields were indeed driving the recent US dollar revival, the near term plight of the US dollar would most likely hang on the balance of this week tier one US economic data.

Oil Prices

After going through the ritualistic Monday morning downside test on the back of rising oil drilling rig counts, WTI rallied around $2 towards $69.35 in NY, as traders remain singularly focused on the Iran nuclear deal. Prices put in their high of the day when Israeli Prime Minister Benjamin Netanyahu stocked the geopolitical fires by accusing Iran of lying about its past nuclear intentions. Nevertheless, Netanyahu’s hawkish retort not only increases the odds the US will pull out of the deal but raises the spectre of Israel taking military action against Iranian nuclear facilities.

As expected, the pace of rhetoric as we near the May 12 deadlines continues to intensify.

Gold Prices

The recent US dollar revival has negatively impact gold as the intensity of the USD correction has caught most traders by surprise. However, sentiment does suggest we are little more than a trade war or Middle East escalation headline away from sending price higher. With so much unpredictability in play on these two important fronts, gold prices are likely to remain supported.

Currency Markets

EUR: The single currency unit received little support from the German CPI report and continued to trade poorly as stale USD positions continue to get flushed

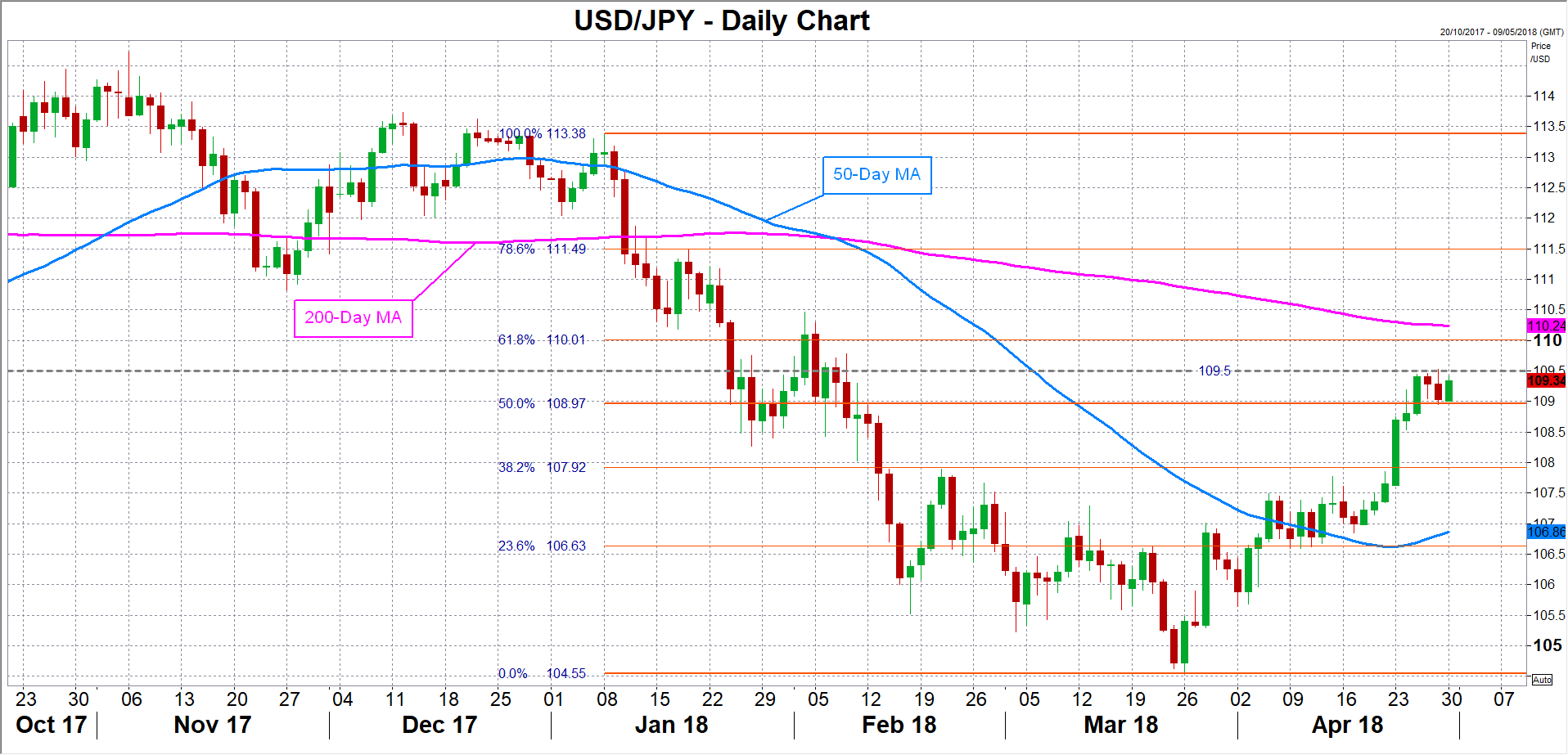

JPY: Between correlation shift and breakdowns all the while considering the broader US dollars impressive run we are still only trading at 109.25. Certainly, dealers are looking for more clear signals as everyone to a tee is painting a different picture in dollar-yen these days.

MYR: Growing election uncertainty continues to keep investors at bay. While the chances of the opposition to pull off a surprise result remain low, a large scale knee-jerk negative repricing of Malaysian assets suggests foreign bond buyer will stay on the sidelines. As such, the MYR will continue to trade defensively due to their heightened domestic political risk.

Gold Prices Start Week With Losses – Are We Headed To $1300?

Gold prices continue to head south, as the base metal has resumed its losing ways on Monday, erasing the gains seen on Friday. In North American trade, the spot price for an ounce of gold is $1316.80, down 0.52% on the day. On the release front, key US indicators were mixed. Personal Spending improved to 0.4%, matching the forecast. This marked a 3-month high. The news was not as positive from the housing sector, as Pending Home Sales dropped to 0.4%, down sharply from 3.1% in the previous release. On Tuesday, the key event is ISM Manufacturing PMI.

As the US dollar continues to shine, gold prices have been under pressure, losing 2.0% since April 16. The symbolic $1300 level is in sight, a support level not breached since late December. There are a number of factors weighing on gold prices. Investor risk appetite remains strong, as tensions in the Korean peninsula have dropped rapidly. The leaders of North and South Korea met last week for a historic meeting, and US President Trump is scheduled to meet with North Korean leader Kim in the near future. On the domestic front, the US economy continues to perform well and inflation is moving higher. This has raised expectations that the Federal Reserve will raise rates four times in 2018, which is bullish for the US dollar.

US indicators ended the week with the first GDP report for the first quarter. Advance GDP posted a respectable gain of 2.3% which beat the estimate of 2.0 percent. Still, this was a significant drop from GDP in the fourth quarter of 2018, which came in at 2.8 percent. Analysts also took note of the Employment Cost Index, which rose from 0.6% to 0.8%, another indication that inflation is moving higher. There is growing sentiment that the Federal Reserve will raise interest rates four times this year, although Fed policymakers continue to project a total of three increases in 2018. One scenario envisions the Fed raising rates once each quarter until the economy shows signs of slowing down. If inflation continues to move higher and economic conditions remain strong, the US dollar could continue to make headway against its major rivals, including gold.

Oil Nudged By Nukes

We warned earlier to watch the Iran nuclear situation closely, and it became the dominant theme to start the week with Israeli prime minister Netanyahu arguing for action against Iran. The US dollar was the top performer on the day while the New Zealand dollar lagged. We take a look at May seasonals as the new month begins. A new Premium trade in a major index was posted earlier today. It is currently 150 pts in the green.

Geopolitics is always a guessing game. The talk always exceeds the action but people and markets are fearful by nature. On Monday, Netanyahu revealed that Israeli intelligence uncovered a trove of documents showing how Iran had worked on nuclear weapons from 1995-2003 and had preserved the knowledge it acquired in that time.

Without getting into the details, there are two questions: 1) Will anyone attack Iran? 2) Will there be new sanctions with the US leaving the Iran nuclear deal at the May 12 deadline.

The first remains extremely unlikely at this point, despite some hawks in the White House. War is unpopular in the US and would have no support in Europe. On the second question, the market is leaning towards expecting sanctions, despite opposition from European leaders. Oil jumped more than $1 from the lows Monday on Netanyahu's speech.

That might be the wrong takeaway. Instead, this could be the next wave of a coordinated US-Israel PR campaign aimed at new sanctions against Tehran. If so, it didn't appear very coordinated Monday. In comments after Netanyahu's speech, Trump said the same things he's been saying about Iran for more than a year and highlighted that all options were still on the table. More likely, it was a solo attempt by Israel to influence leaders in the west who are reluctant and that perhaps Trump himself is reluctant.

We will be watching Trump's twitter closely for clues. The calendar now turns to May for the forex market. Seasonal patterns performed well in April and some seemed to get a head start on May.

One is Australian and New Zealand dollar weakness. They were strong to start April but cratered late in the month. The seasonal picture remains dark with May as the worst month for AUD and third-worst for NZD. It shouldn't be a surprise that it's also a tough month for base metals.

Global equity markets were strong in April, especially outside the United States. The old adage about selling in May doesn't really apply. It's a weaker month than April, but by no means a poor month.

It is, however, the weakest month on the calendar for the euro and with EUR/USD testing 1.20, it could get weak in a hurry.

Eco Data 5/1/18

[php_everywhere instance="1"]

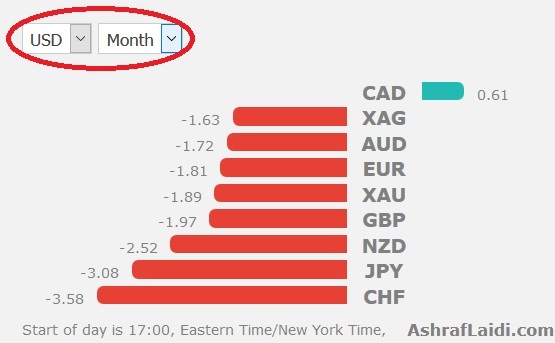

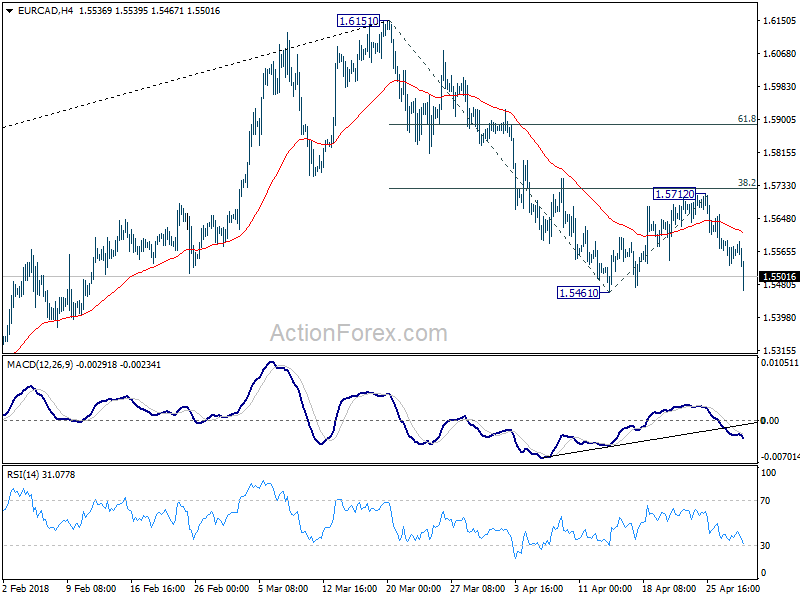

CAD surges with help from oil, a look at AUDCAD and EURCAD

CAD overtakes USD's place as the strongest major currency today as helped by rebound in oil prices.

Just after we said here that AUDCAD's decline seemed to be slowing, it accelerated. But after all, there is no change in the view that it's clearly in a near term down trend. The major target is 0.9578 key support (2017 low). We'll monitor the reaction there.

Another one to watch is EURCAD. We pointed out here that the corrective rise from 1.5461 could be ending. Subsequent decline proved that it has indeed ended at 1.5172. EUR/CAD is now heading to 1.5461 low with solid downside momentum.

Break of 1.5461 should be seen soon and next target is 61.8% projection of 1.6151 to 1.5461 from 1.5712 at 1.5286.

Eurozone’s GDP and Jobs Data Gather Attention ahead of Inflation Prints

The Eurozone will see the release of its preliminary GDP for Q1 as well as its unemployment rate for March, both on Wednesday at 0900 GMT. Forecasts point to a slowdown in economic growth, something that would likely vindicate the European Central Bank’s (ECB) recent shift to a more cautious stance.

It’s no secret that economic growth in the Eurozone probably slowed in the first quarter of the year. Business surveys such as the Purchasing Managers Indices (PMIs) have been pointing to a slowdown for months now, and even ECB President Draghi acknowledged as much at last week’s policy meeting, when he noted economic data have moderated recently. Still, investors will probably keep a close eye on the release of the official GDP figures, in order to gauge whether the slowdown was more or less pronounced than originally thought, and to what extent that will impact the ECB’s thinking.

In terms of forecasts, the bloc’s preliminary GDP estimate for Q1 is projected to show that the economy grew by 0.4% on a quarterly basis, a much slower pace than the 0.6% recorded in Q4. In yearly terms, growth is anticipated to have slowed to 2.5%, from 2.7% in Q4. Meanwhile, the unemployment rate is expected to have held steady at 8.5%, after ticking down in February.

While the ECB still looks set to begin scaling back its massive stimulus program later this year, with some signaling of that likely to come in the summer meetings, economic data will be critical to watch as continued deterioration could make the Bank more cautious to head towards the exit door.

Thus, in case these data disappoint – for instance if growth slows by more than expected – that could reinforce speculation that the Bank may choose to delay its normalization plans until the economy rebounds, potentially bringing the euro under renewed selling pressure. Looking at euro/dollar, in case of further declines support may be found near the 1.2030 hurdle, marked by the peak of September 20. A downside break of that zone could open the way for the 1.1960 area, defined by the top of November 27.

On the flip side, should these figures – and particularly the GDP print – come in better than expected, that could dispel some concerns that the ECB will be hesitant to normalize its policy and thereby, help the euro to recover some of its latest losses. Advances in euro/dollar could initially stall near 1.2140, the April 30 high. If buyers overcome that barrier, the next territory to offer resistance may be near 1.2245, a hurdle that capped the rally on April 24.

Finally, besides the GDP and unemployment prints, the other key data release from Eurozone this week will be the preliminary inflation data for April, which are due out on Thursday.

More Hawkish Fed Eyed at May FOMC Meeting as Dollar Headed for Best Month in a Year

The Federal Open Market Committee (FOMC) begins a two-day monetary policy meeting on Tuesday, with a decision expected on Wednesday at 18:00 GMT. No change to the federal funds rate is expected this month, which now stands at a target range of 1.50-1.75%. The Committee last raised rates in March and indicators for the US economy have been consistently solid since then. But with no new quarterly projections scheduled in May and policymakers committed to a gradual rate hike path, the Fed is not likely to break the recent tradition and deliver a surprise rate increase at a non-press conference meeting.

Data last week showed US GDP growth slowed during the first three months of 2018, with the economy expanding at an annualized rate of 2.3% compared to 2.9% in the prior quarter. However, the figure was better than the consensus forecasts of 2.0% and growth is expected to quicken considerably in the coming quarters. Meanwhile, the US labour market continues to go from strength to strength, and the country’s unemployment rate is forecast to fall to an 18-year low of 4.0% in April in this week’s jobs report.

The inflation picture has also been improving, with all key price gauges jumping higher in March. The 12-month consumer price index rose to a one-year high of 2.4%, while the Fed’s preferred measure, the core PCE price index advanced to 1.9% – the highest since February 2017 and just shy of the Fed’s 2% target. The acceleration in price growth is likely to be welcome news for the Fed, which some have accused of moving too fast with rate hikes amid elusive inflationary pressures.

The recent run of upbeat data may tilt the tone of Wednesday’s policy statement to a slightly more hawkish one, with some possible tweaks to the language to illustrate a more confident inflation outlook and/or improving growth prospects.

A more hawkish-than-anticipated statement could drive the US dollar to break above the key 110 level against the yen, which at the moment is being capped by the 109.50 resistance level. The dollar is on track to enjoy its strongest month since February 2017 in April, following a sharp rebound at the end of March. However, if the Fed disappoints by not making any alteration to its wording, the greenback’s rally could lose some steam and dollar/yen could struggle to hold above the 109 level. A breach of the 109 handle would open the way towards the 108 level.

A bigger test for the dollar though will probably be Friday’s nonfarm payrolls report, and in particular, the wage growth data. The Fed is keen to see a pick-up in earnings in order to be convinced that inflation is on a sustained path upwards. Growth in average hourly earnings is expected to hold steady at 2.7% in April. A near-term challenge of the 110-yen level looks difficult as long as pay increases remain below 3% as the Fed is unlikely to shift out of ‘gradual’ mode without clear signs that wage pressures are building up.

British Pound Under Pressure as Rate Hike Could be Delayed

The British pound is steady in the Monday session, after recording sharp losses on Friday. In North American trade, the pair is trading at trading at 1.3765, down 0.13% on the day. On the release front, there are no British events on the schedule. In the US, Personal Spending improved to 0.4%, matching the forecast. This marked a 3-month high. The news was not as positive from the housing sector, as Pending Home Sales dropped to 0.4%, down sharply from 3.1% in the previous release. On Tuesday, the both the UK and the US release Manufacturing PMI reports.

British Preliminary GDP for the first quarter disappointed last week, with a paltry gain of 0.1%. This missed the estimate of 0.3%, and well short of Final GDP for Q4, which came in at 0.4%. The poor performance of the economy in the first quarter has dampened expectations that the BoE will raise rates at the upcoming May rate meeting, with the odds of a hike plunging to 20%, compared to 90% at the beginning of April. Most analysts expect the BoE to stay pat on rate hikes until the second half of the year, with August or November being the most likely months for a rate hike. This sentiment sent the pound lower on Friday and the currency declined 1.6% last week. Currently, GDP/USD is trading at its lowest level since the end of February.

US indicators ended the week with the first GDP report for the first quarter. Advance GDP posted a respectable gain of 2.3% which beat the estimate of 2.0 percent. Still, this was a significant drop from GDP in the fourth quarter of 2018, which came in at 2.8 percent. Analysts also took note of the Employment Cost Index, which rose from 0.6% to 0.8%, another indication that inflation is moving higher. There is growing sentiment that the Federal Reserve will raise interest rates four times this year, although Fed policymakers continue to project a total of three increases in 2018. One scenario envisions the Fed raising rates once each quarter until the economy shows signs of slowing down. If inflation continues to move higher and economic conditions remain strong, the US dollar could continue to make headway against its major rivals, including the Japanese yen.

RBA Meeting: Neutral, With a Hint of Caution?

The Reserve Bank of Australia (RBA) will announce its policy decision on Tuesday, at 0430 GMT. The Bank is widely expected to keep rates on hold, so once again, attention will be on the accompanying statement. Given mixed developments since the latest meeting, the RBA is likely to stick to its neutral script overall. In case there is a shift in language though, it may be towards a more cautious direction.

Economic developments since the RBA last met in early April have been mixed, on balance, reaffirming the Bank’s stance that interest rates in Australia are likely to remain unchanged for a long time still.

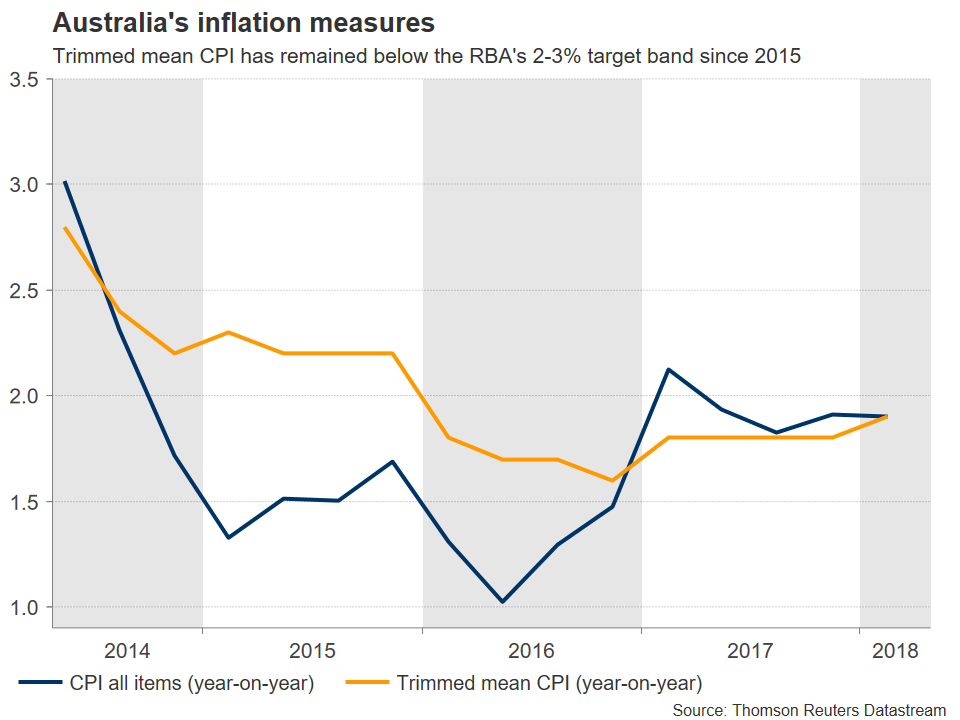

Kicking off with economic data, the labor market cooled in March. Although the unemployment rate held steady, the labor force participation rate fell while the net change in employment barely rose, pointing to a labor market that is moderating. On the inflation front, the headline CPI rate for Q1 remained unchanged at 1.9% in yearly terms, missing the market consensus of an increase to 2.0%. That said, the Bank’s own forecasts expect the CPI rate to rest only at 2.0% in Q2, so a 1.9% print in Q1 will hardly be surprising or worrisome for policymakers. On a positive note, consumer spending appears to have picked up some steam in Q1, with retail sales for February rising by more than projected.

In other developments, the Australian dollar fell in the latter part of April, touching fresh lows for 2018. A depreciating currency is often viewed as a pleasant development for central banks struggling to hit their inflation targets, as it boosts the price of imports and thereby, the broader inflation rate. Indeed, the RBA has been vocal about the aussie lately, consistently noting that an appreciating exchange rate could weigh both on inflation and growth. Thus, the currency’s tumble will likely be welcomed by policymakers.

What will be unwelcomed, however, is the tightening in financial conditions that has occurred in April. Even though the RBA is maintaining its own borrowing costs unchanged, the rising bond yields and expectations for faster tightening in the US appear to be spilling over into slightly higher interest rates for Australian banks too. This is likely to be worrisome for the RBA, as it could slowly begin to manifest itself into the real economy, for example via higher mortgage rates for Australian borrowers.

All the above suggest the RBA is unlikely to make any major changes to its communication this week. The Bank is likely to stick to its neutral script, indirectly reaffirming that there’s no move in interest rates on the horizon. If anything, a change in language may see the assessment become slightly more cautious, amid signs of cooling in the labor market and rising interest rates internationally. Not to mention the still-looming trade frictions between the US and China.

At the time of writing, market pricing implies a mere 18% probability for a rate increase this year. Should the RBA’s assessment reinforce the narrative that rates will remain on hold throughout 2018, that probability could edge even lower, and the Aussie may come under renewed selling interest. Declines in aussie/dollar could encounter initial support near the psychological barrier of 0.7500, which also halted the pair’s decline on December 7. Further down, the 0.7450 barrier could come into play, defined by the lows of September 13.

On the upside, and in case the RBA’s tone is seen as containing a hint of optimism, advances in aussie/dollar could meet immediate resistance around 0.7585, the high of April 27. If the bulls manage to overcome that zone, then sell orders may be found near 0.7640, an area marked by the March 29 lows.

Finally, it should be noted that besides the rate decision, RBA Governor Lowe will also be speaking at a dinner organized by the RBA on the same day, a few hours after the decision. Any remarks on policy are likely to attract attention, and could impact price action in aussie/dollar.