Sample Category Title

Dollar Enjoys Gains ahead of Core PCE Inflation

Here are the latest developments in global markets:

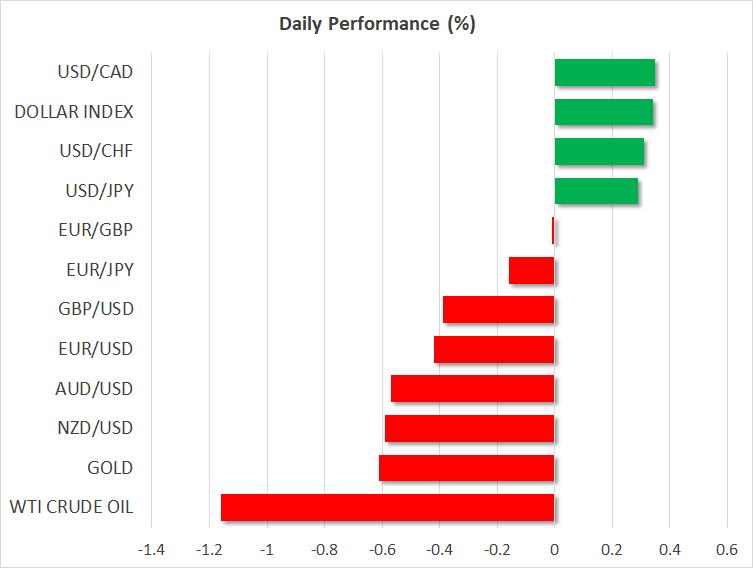

FOREX: The dollar index, which gauges the greenback’s strength versus six major currencies, edged up to 91.76 (+0.25%) during the early European afternoon, heading towards the 3 ½ -month high of 91.90 reached on Friday. Dollar/yen also climbed higher to touch an intra-day high of 109.29 ahead of the release of the core PCE index later today. On Wednesday, the Fed will announce its rate decision, while the famous Nonfarm payrolls will bring further volatility to the greenback on Friday. Pound/dollar stretched lower to a two-month low of 1.3716 (-0.41%), extending last week’s losses made after the UK GDP growth missed forecasts, casting even more doubt on whether the BoE will finally pick up rates in May. Euro/dollar was on the back foot as well, declining to 1.2081 (-0.40%). In antipodean currencies, aussie/dollar and kiwi/dollar were in a bearish mode with the former slipping by 0.37% ahead of the RBA’s interest rate decision early on Tuesday, and the latter falling by 0.40%. Dollar/loonie continued to recover, crawling up to 1.2868 (+0.32%).

STOCKS: European stocks traded higher on Monday. The benchmark European STOXX 600 rose marginally by 0.11% at 0900 GMT, being in the green for the third day in a row. The blue-chip Euro STOXX 50 was up by 0.16%, while the German DAX 30 and the French CAC 40 were moving higher by 0.18%. Also, the British FTSE 100 jumped by 0.38%. In Asia, markets in Japan and China will be closed for holidays today. In the US, even though the S&P, Dow Jones were mixed on Friday, futures tracking these indices are currently in the green, pointing to a higher open today.

COMMODITIES: Oil prices dived on Monday after Friday’s Baker Hughes indicated that the US oil rig count rose for the fourth consecutive week, pointing to higher production in the US. Despite the pullback, oil prices held near 3-year highs and are on track to post gains for the second straight month. WTI plummeted by 1.07%, to $67.37 per barrel, while Brent declined by 1.09% to $73.83 per barrel. In precious metals, silver fell by 0.64% and gold dipped by 0.41%.

Day ahead: US core PCE to head higher; RBA to stand pat on rates on Tuesday

Day ahead: US core PCE to head higher; RBA to stand pat on rates on Tuesday

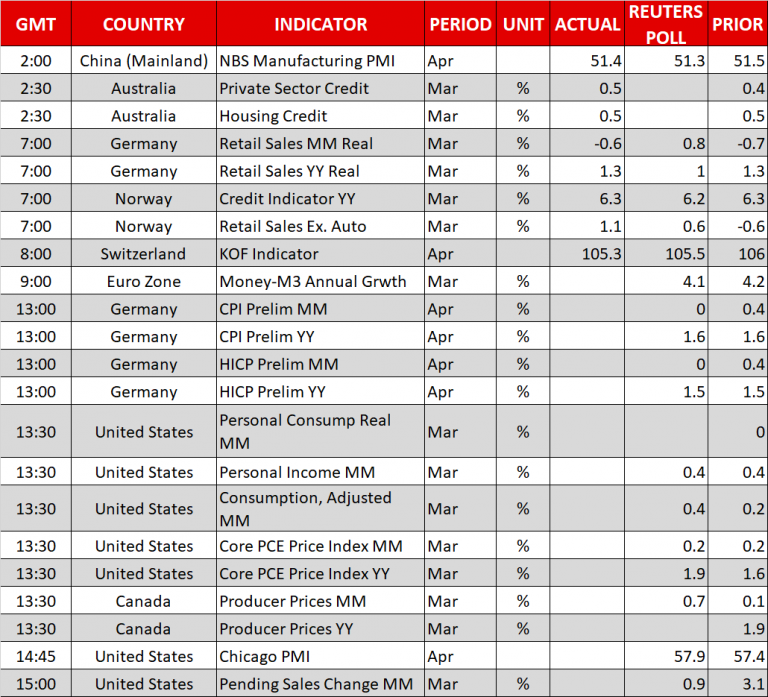

Economic releases will continue to attract attention in the remainder of the day, with inflation numbers out of Germany, the US and Canada being in the spotlight.

At 1200 GMT, Germany will publish initial CPI estimates for the month of April and in the absence of other major releases out of the Eurozone, the numbers could spark some volatility to the euro if they significantly deviate from forecasts. According to analysts, German consumer prices are expected to grow at the March pace of 1.6% year-on-year, while on a monthly basis, the measure is projected to slow down from 0.4% in March to 0.0%. Harmonized CPI readings (HICP), which are comparable to CPI data in other EU countries, are anticipated to follow the same pattern.

Meanwhile in the US, investors will be eagerly waiting for the core PCE as well as for the personal income and consumption figures to come into view at 1230 GMT. The Fed’s favorite inflation measure is expected to advance for the second consecutive month, rising from 1.6% to 1.9% y/y in March. Should the gauge surprise to the upside, the dollar could extend today’s rally on the back of prospects that the Fed could appear more confident to tighten monetary policy even further at the conclusion of its two-day policy meeting on Wednesday. Markets are currently pricing in two more rate hikes this year and an upbeat inflation report later today could lift the odds for a third one which stand at 20.0% at the moment. Note that on Wednesday, FOMC policymakers are said to stand pat on interest rates, though, they might turn more hawkish on the view of higher inflation numbers.

Other US data due later in the day include April’s Chicago PMI (1345 GMT) and pending home sales for March (1400 GMT).

Canadian producer prices for March will be made public at the same time the US sees the release of core PCE price data (1230 GMT).

Fast-food chain McDonald’s is among companies releasing quarterly results today; the company’s report is scheduled for release before the opening bell on Wall Street.

On Tuesday, many parts of the world will be on holiday to celebrate Labor day. The calendar, however, will be relatively busy in some major economies.

At 0430 GMT, the focus will turn to Australia and the RBA’s decision on interest rates. Unlike its US counterpart, the RBA is in no rush to raise its borrowing costs from record lows probably not until mid-2019 as households are still struggling to repay their mounting debts according to the central bank’s latest financial stability statement delivered a few weeks ago. Last week’s data were not encouraging either, as inflation fell short of expectations of meeting the RBA’s target of 2.0%.

UK manufacturing PMIs will follow up at 0830 GMT, while the US will see its ISM manufacturing PMIs as well later at 1400 GMT. Forecasts are for both indicators to ease on April.

Elsewhere, GDP growth readings will be of greater interest in Canada (1230 GMT) as analysts wait to see whether the Canadian economy will turn back to growth in February after contracting by 0.1% m/m in the previous month. Particularly, projections are for the Canadian GDP growth to reach 0.3% m/m. In case, the numbers undershoot forecasts, the loonie could follow a downtrend.

In New Zealand, global dairy prices delivered at a tentative time will have the potential to move the kiwi to the upside if they rise for the third consecutive time.

In oil markets, the American Petroleum Institute will issue its weekly report on US crude oil inventories at 2030 GMT. It will be interesting to see whether the results will back fears of rising US production that could harm OPEC’s efforts to curb supply. Recall that on Friday Baker Hughes indicated an increase in the number of US oil drillings.

Canadian Dollar Dips, Inflation Data Next

The Canadian dollar has lost ground in the Monday session, erasing the gains seen on Friday. Currently, USD/CAD is trading at 1.2873, up 0.34% on the day. In Canada, the focus is on inflation data. The Raw Materials Price Index is expected to rebound with a gain of 0.6%, while the Industrial Product Price Index is forecast to edge higher to 0.2%. In the US, Personal Spending is predicted to improve to 0.4%, while the markets are braced for Pending Homes to slip by 0.6%. On Tuesday, Canada releases GDP and BoC Governor speaks at an event in Yellowknife. In the US, the main event is ISM Manufacturing PMI.

The US released the first GDP report for the first quarter, with a respectable gain of 2.3% which beat the estimate of 2.0 percent. Still, this was a significant drop from GDP in the fourth quarter of 2018, which came in at 2.8 percent. Analysts also took note of the Employment Cost Index, which rose from 0.6% to 0.8%, another indication that inflation is moving higher. There is growing sentiment that the Federal Reserve will raise interest rates four times this year, although Fed policymakers continue to project a total of three increases in 2018. One scenario envisions the Fed raising rates once each quarter until the economy shows signs of slowing down. If inflation continues to move higher and economic conditions remain strong, the US dollar could continue to make headway against its Canadian counterpart.

Bank of Canada Governor Stephen Poloz testified on Parliament Hill last week and delivered a message of cautious optimism about economic conditions. Poloz said that he expected the economy to improve after a disappointing first quarter and projected that inflation would push above BoC's target of 2% later in 2018. The bank maintained the benchmark rate at 1.25% at its April meeting but is expected to raise rates as early as May. However, policymakers would prefer to see the NAFTA negotiations concluded before making any rate moves. The talks have made significant progress, but the critical auto pact remains a stumbling block. It is likely that a tentative agreement will be hammered out, perhaps as early as May.

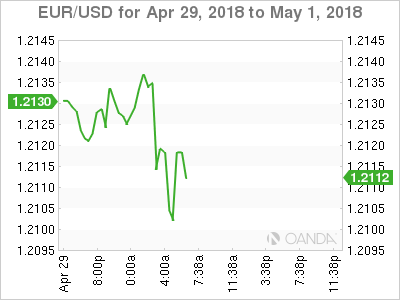

EURO Testing Demand Around The 1.2100 Level

The euro has come under another round of selling pressure against the greenback during the European trading session, following softer than expected EU inflation data. The EURUSD pair is currently trading around the key 1.2100 level, after being strongly rejected from the 1.2138 level. A loss of the 1.2100 level may provoke further selling towards the 1.2000 level, while a breach of the 1.2138 level should encourage buyers to test the 1.2154 level.

The EURUSD pair remains bearish while trading below the 1.2138 level, key intraday support is now found at the 1.2054 and 1.2000 levels.

If the EURUSD pair starts to trade back above the 1.2138 level, buyers may test towards the 1.2154 and 1.2200 levels.

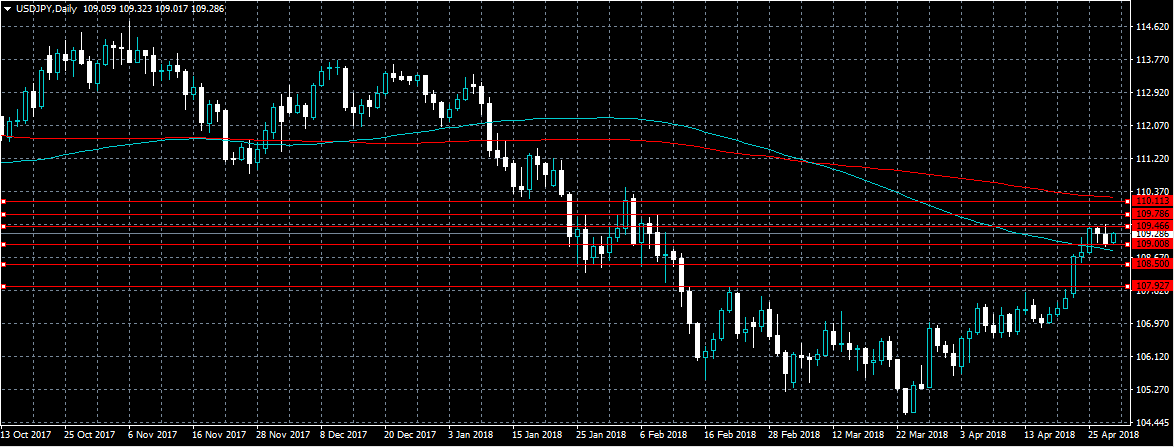

USDJPY Awaits US Inflation Data

The US dollar continues to trade to the upside against the Japanese yen, as buyers again stepped in from the psychological 109.00 level early today. The USDJPY pair currently trades around the 109.30 level, with buyers now trying to negate the two bearish daily reversal candles. Moving into the U.S session, traders await key US inflation data, with the 109.46 level the key upside level to watch.

The USDJPY pair remains bullish while trading above the pivotal 109.00 handle, key resistance is now located at the 109.48 and 109.78 levels.

If the USDJPY pair moves below the 109.00 level for a sustained period, sellers are likely to target the 108.80 and 108.50 levels.

EU Malmström to talk to US Ross on steel tariff exemptions

Regarding the US steel tariffs, EU Trade Commissioner Cecilia Malmström will speak with US Commerce Wilbur Ross today. Malmström will try to get last minute consent from the US to exempt the tariffs on EU, which temporary exemption expires tomorrow. However, it's reported that EU officials are concerned with impossible demands from the US.

European Commission spokes Margaritis Schinas said in a news conference calmly that "we are patient but we are also prepared." EU's stance was made clear after German Chancellor spoke with French President Emmanuel Macron and UK Prime Minister Theresa May on Sunday. Merkel said Europe was "resolved to defend its interests within the multilateral trade framework".

On April 16, EU has already submitted a request to WTO to determine how the US can compensate if trade flows into the EU are affected by the new tariffs. That's request was under TWO's Safeguard Agreements. EU also plans to join another separate WTO complaint against the US, arguing that the steel tariffs violate the most-favored nation principle, which forbid discrimination between their trading partners. In addition, it's reported that EU could retaliate by imposing levies on EUR 2.8b of American goods. And that could start as soon as on June 21, 90 days after the US steel tariffs took effect.

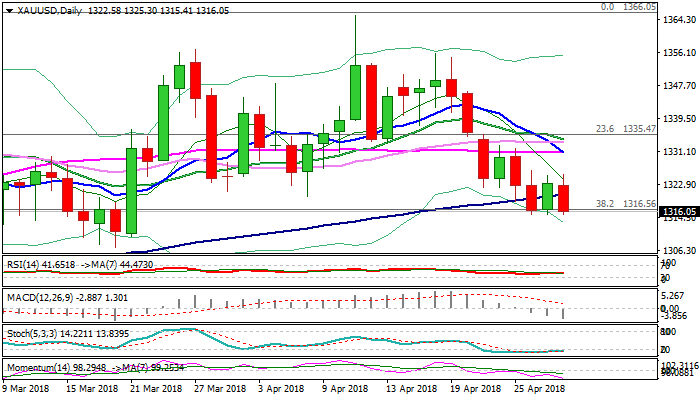

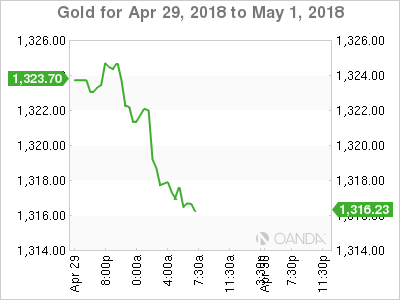

SPOT GOLD – Fresh Bears Pressure $1315 Base And Could Extend Towards Key Supports At $1307/03

Gold price fell on Monday and fully reversed last Friday’s recovery to $1325, as fresh weakness retested new five-week low at $1315, posted last Thursday.

Easing geopolitical tensions over Koreas, as peace talks progress, reduced demand for safe-haven assets, while dollar regained traction on Monday after pulling off recent highs last week, bringing gold price under renewed pressure.

Daily techs returned to full bearish setup after short-lived probes above 100SMA, while falling 10SMA formed multiple bear-crosses (20,30,55SMA) and momentum continues to head lower, keeping bearish structure intact for eventual push towards key supports at $1307/03 (20 Mar low / 200SMA).

Weakening daily studies show increased risk for break below pivotal $1307/03 zone which also marks the lows of short-term $1303/66 congestion) which would confirm reversal and open way for further retracement of $1236/$1366 ascend.

Close below $1315 base (also Fibo 38.2% of $1236/$1366 rally) is seen as initial requirement for bearish scenario.

Broken 100SMA marks initial resistance at $1320, guarding upper pivot at $1326, where recent recovery attempts were repeatedly rejected.

Res: 1320, 1326, 1331, 1334

Sup: 1315, 1310, 1307, 1303

DAX Quiet Ahead Of German CPI

The DAX index is showing little movement in the Monday session. Currently, the DAX is trading at 12,583 points, up 0.02% on the day. On the release front, German Retail Sales declined 0.6%, well off the estimate of 0.8%. Later in the day, Germany releases Preliminary CPI, with an estimate of -0.1%.

German Retail Sales, the primary gauge of consumer spending, continues to struggle. The indicator dropped 0.6% in April, marking a fourth consecutive decline. At the same time, the German consumer remains very optimistic, as underscored by the well-respected GfK consumer confidence reports. The Frankfurt stock market remains at high levels, another sign of favorable sentiment towards the robust German economy.

It was more of the same from the ECB on Thursday, as the bank held the course with its monetary policy and guidance. With an interest rate hike not in the cards until 2019, the euro lost ground, while the DAX improved sharply, gaining 1.2% on Thursday. The ECB rate statement said that “the Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases”. The stimulus program of EUR 30 billion/month is scheduled to remain in place until September, so investors shouldn’t even think about an interest rate hike until sometime in 2019. In his press conference, Mario Draghi said that the eurozone economy had slowed in the first quarter, but expressed “caution tempered by an unchanged confidence” that the ECB would realize its target of around 2 percent inflation. Although the ECB has said that it plans to wind up stimulus in September, this is not a date set in stone – if second-quarter numbers are not strong, the ECB could continue to the stimulus scheme into 2019.

EUR/USD – Steady Euro Shrugs Off Soft German Retail Sales

EUR/USD has started the week with small losses. In the Monday session, the pair is trading at 1.2118, down 0.10% on the day. On the release front, German Retail Sales declined 0.6%, well off the estimate of 0.8%. Later in the day, Germany releases Preliminary CPI, with an estimate of -0.1%. In the US, Personal Spending is expected to improve to 0.4%, while Pending Homes is forecast to slip to 0.6%. On Tuesday, the US releases ISM Manufacturing PMI.

The US released the first GDP report for the first quarter, with a respectable gain of 2.3% which beat the estimate of 2.0 percent. Still, this was a significant drop from GDP in the fourth quarter of 2018, which came in at 2.8 percent. Analysts also took note of the Employment Cost Index, which rose from 0.6% to 0.8%, another indication that inflation is moving higher. There is growing sentiment that the Federal Reserve will raise interest rates four times this year, although Fed policymakers continue to project a total of three increases in 2018. One scenario envisions the Fed raising rates once each quarter until the economy shows signs of slowing down. If inflation continues to move higher and economic conditions remain strong, the dollar should continue to perform well against the euro and other major currencies.

The euro had a disappointing week, losing 1.2% percent. Investors were not impressed with the drab announcement from the ECB on Thursday, as the bank held the course with its monetary policy and guidance. The rate statement said that “the Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases”. The stimulus program of EUR 30 billion/month is scheduled to remain in place until September, so investors shouldn’t even think about an interest rate hike until sometime in 2019. In his press conference, Mario Draghi said that the eurozone economy had slowed in the first quarter, but expressed “caution tempered by an unchanged confidence” that the ECB would realize its target of around 2 percent inflation. Although the ECB has said that it plans to wind up stimulus in September, this is not a date set in stone – if second-quarter numbers are not strong, the ECB could continue to the stimulus scheme into 2019.

Dollar Bulls Lack Conviction

The week offers a plethora of new data along with monetary policy announcements from the Reserve Bank of Australia (RBA) later this evening and the Federal Open Market Committee (FOMC) on May 2. No policy changes are anticipated.

U.S trade policy will be markets focus this week with U.S Treasury Secretary Mnuchin visiting China for high-level trade talks.

In Europe, it’s a holiday shortened trading week, however, both the April manufacturing and composite PMI’s will be released along with quarterly growth data (May 2) from the Eurozone and Italy.

Stateside, despite the Fed expected to keep rates unchanged, the market will be watching for any clues on Treasury yields and GDP. Apple Inc. dominates the week in earnings when it reports on Tuesday.

U.S personal spending is expected to have accelerated last month, while manufacturing may have expanded at a slower pace in April.

On Friday, the U.S will be posting the granddaddy of all economic indicators, its non-farm payroll (NFP) report at 08:30 pm EDT.

1. Stocks in favor

Global equities have kicked off the week broadly higher as solid corporate earnings is boosting investor sentiment and as geopolitical worries ease.

Note: Liquidity has been low overnight due to its Golden Week in Japan, with public holidays Monday, Thursday and Friday. China is shut Monday and Tuesday.

Down-under, Aussie shares advanced to a seven-week high on Monday, led by broad based gains, with banks being the dominant contributor. The S&P/ASX 200 index rose +0.5% at the close of trade. The benchmark added +0.7% on Friday. In South Korea, the Kospi jumped +0.9% and is set to end April more than +2.5% higher following record profits from tech giant Samsung and after a spectacularly successful inter-Korean summit.

In Europe, regional indices are trading slightly higher across the board buoyed by a flurry of M&A deals. U.K supermarkets are in focus after Sainsbury’s and Asda agreeing to merge. Elsewhere, Germany’s Deutsche Telekom trades higher after T-Mobile and Sprint agreed to merge with Deutsche Telekom.

U.S stocks are set to open in the ‘black’ (+0.3%).

Indices: Stoxx600 +0.1% at 384.9, FTSE +0.4 at 7528, DAX +0.2% at 12605, CAC-40 +0.2% at 5491, IBEX-35 +0.4% at 9965, FTSE MIB +0.2% at 23982, SMI +0.4% at 8881, S&P 500 Futures +0.3%.

2. Oil slips on rising U.S. rig count, gold higher

Oil prices have eased a tad overnight after a rising rig count in the U.S pointed to higher production there. Nevertheless, markets trade within striking distance of recent highs on supply concerns amid prospects that the U.S could re-impose sanctions on Iran, while OPEC-led producers continue to withhold output.

Brent crude futures have dipped -50c, or -0.7% to +$74.14 a barrel. Prices climbed as high as +$75.47 last week, levels not seen since November 2014. U.S West Texas Intermediate (WTI) crude futures are at +$67.82 a barrel, down -28c, or about -0.4%, from Friday’s close.

According to Baker Hughes, U.S drillers added five oilrigs in the week to April 27, bringing the total count to +825, the highest level since March 2015.

Note: U.S President Trump has until May 12 to decide whether to restore the sanctions on Iran that was lifted after an agreement over its disputed nuclear program.

Gold prices have inched up ahead of the U.S open, as the mighty U.S dollar trades steady after it’s recent run of gains, weighed down by a decline in the benchmark U.S. 10-year Treasury yield. Spot gold rose +0.1% to +$1,323.20 per ounce, while U.S gold futures for June delivery were up +0.1% at +$1,324.40 per ounce.

3. Sovereign yields back up

A softening in eurozone economic data and signs that inflationary pressures remain subdued, has been encouraging the European Central Bank (ECB) to hold off from raising interest rates until well into next year, and therefor supported the bond markets in recent weeks.

Despite this, E.U Government bond yields have nudged a tad higher this morning as the markets focus turns to preliminary inflation data from Germany and Italy, two of the bloc’s biggest economies.

Note: Consumer prices in the German state of Saxony rose by +1.6% y/y in April, up from +1.5% in March.

Germany’s 10-year Bund yield is up almost +2 bps at +0.58%, above a one-week low of +0.56% print on Friday. In addition to inflation data, bond investors also waiting for this week’s U.S Fed meeting, although no major changes to monetary policy are expected.

Elsewhere, the yield on U.S 10-year Treasuries gained less than +1 bps to +2.96%, while the U.K’s 10-year Gilt yield decreased -3 bps to +1.445%, hitting the lowest in more than a week with its fifth straight decline.

4. Dollar little changes amidst lack of geopolitical risks

The dollar rose in the past couple of weeks because of the squeeze in short positioning and because of the U.S. yield curve steepening, but the curve is flattening again, and so this should moderate the supportive momentum in the dollar. Smart money is expecting the currency to return on offer and remain under pressure on a multi-quarter basis.

However, the USD is holding onto its recent gains as German inflation data (see below) highlighted the headwinds in reaching the ECB’s +2% target while political woes accompany recent soft UK data.

EUR/USD (€1.2107) continues to probe the lower end of the €1.21 level as the recent ECB cautious tone was reiterated in this morning’s German April CPI data.

GBP/USD (£1.3730) is a tad softer and trading atop of some key support levels after U.K Home Secretary Rudd resigned over an immigration scandal. Recent sterling pressure has come from politics and soft economic data that suggest that the Bank of England (BoE) should not be in any hurry to hike rates any time soon.

5. Fall in German core inflation supports ECB’s cautious stance

Regional CPI data from German states for April published this morning suggest that German HICP inflation was unchanged at +1.5% as increases in energy and food prices were offset by a fall in the core-rate.

Analysts note that the decline in core inflation is not as worrying as it sounds – it reflects the fact that Easter fell earlier this year than last, meaning that average package holiday prices in particular were lower than last April. This effect is expected to be temporary.

Digging deeper, inflation in other core components (clothing and transportation) was broadly stable. However, with German wage growth finally edging higher, core inflation is expected to rise further in time.

Today’s data goes someway to justify the ECB’s latest decision not to make any major changes in its forward guidance for now.

Merger Monday Sees Stocks Better Bid

Notes/Observations

- German inflation data highlight the headwinds in reaching the ECB 2% target

- Political woes accompany recent soft UK data

Asia:

- China Apr Manufacturing PMI: 51.4 v 51.3e

- China Securities Regulatory Commission (CSRC) eased restrictions on foreign investment in security joint ventures, removing the restriction of single foreign investors to a 30% stake in JVs

Europe:

- UK PM May accepted resignation of Home Sec Amber Rudd (Note: Resignation said to be because her department had targets for deportations and this was something that she should have been aware of, but had denied)

- EU Commissioner Malmstrom: EU Commission was preparing to respond with punitive measures if US tariffs took effect next week and stressed that its priority was high-level dialogue. Preparing 3-fold response which would be compatible with WTO rules

- German Govt Spokesperson: Chancellor Merkel/ French President Macron UK PM May agreed that US should take no trade measures against the EU, or else EU should be ready to defend its interests within the framework of the multilateral trade order

- EU Commission said to be inclined to give Italy more time to comply with budget rules. To wait for final 2018 economic data before making final decision on whether Italy was in breach of this year’s target

- Republica poll said to show that Italian politics was moving to the right wing as a political impasse carried on in the two months after the general election. Northern League Party: 22% vs 17.4% election results; Five Star support was approx. 33% and Democratic Party (PD): 17.8% vs 18.7% election result

Sovereign ratings:

- S&P affirmed Germany sovereign rating at AAA; outlook Stable

- S&P affirmed United Kingdom sovereign rating at AA; outlook Negative

- S&P affirmed Italy sovereign rating at BBB; outlook Stable

- Fitch affirmed United Kingdom sovereign rating at AA; outlook Negative

- Fitch affirmed Netherlands sovereign rating at AAA; outlook Stable

- Moody's affirmed Finland sovereign rating at Aa1; outlook Stable

Americas:

- Expected meeting between US President Trump and North Korea's Kim said to be expected to be held in either May or early June

- Commerce Sec Ross: White House plans to extend the steel and aluminum tariffs to some countries, but not all, following the scheduled expiration on May 1st

Economic Data:

- (DE) Germany Mar Retail Sales M/M: -0.6% v +0.8%e; Y/Y: 1.3% v 1.2%e

- (FI) Finland Feb Final Trade Balance: -0.3B v -€0.3B prelim

- (NO) Norway Mar Retail Sales W/Auto Fuel M/M: 1.1% v 0.6%e

- (NO) Norway Mar Credit Growth Indicator Y/Y: 6.3% v 6.2%e

- (DK) Denmark Mar Gross Unemployment Rate: 4.1% v 4.1%e; Unemployment Rate (Seasonally adj): 3.3% v 3.2% prior

- (ZA) South Africa Mar M3 Money Supply Y/Y: 6.4% v 7.0%e; Private Sector Credit Y/Y: 6.0% v 5.8%e

- (DE) Germany Apr CPI Saxony M/M: 0.0% v 0.4% prior; Y/Y: 1.6%v 1.5% prior

- (CH) Swiss Apr KOF Leading Indicator: 105.3 v 106.0e

- (AT) Austria Mar PPI M/M: No est v 0.0% prior; Y/Y: No est v 1.2% prior

- (TR) Turkey Mar Trade Balance: -$5.8B v -$5.8Be

- (TH) Thailand Mar Current Account: $5.8B v $4.4Be; Trade Account Balance: $3.0B v $2.3B prior, Overall Balance of Payments (BOP): $3.0B v $0.0B prior; Exports Y/Y: 6.3% v 7.7% prior; Imports Y/Y: 6.7% v 21.8% prior

- (EU) Euro Zone Mar M3 Money Supply Y/Y: 3.7% v 4.0%e

- (DE) Germany Apr CPI Bavaria M/M: -0.1% v +0.5% prior; Y/Y: 1.7 v 1.7% prior

- (DE) Germany Apr CPI Brandenburg M/M: -0.1% v +0.4% prior; Y/Y: 1.6 v 1.6% prior

- (DE) Germany Apr CPI Hesse M/M: 0.0% v 0.4% prior; Y/Y: 1.5 v 1.5% prior

- (DE) Germany Apr CPI Baden Wuerttemberg M/M: 0.0% v 0.4% prior; Y/Y: 1.7% v 1.7% prior

- (ES) Spain Feb Current Account: -€0.5B v -€0.4B prior

- (CH) SNB Total Sight Deposits for Week Ended Apr 27th (CHF): 575.2B v 575.4B prior

- (CZ) Czech Mar Money Supply Y/Y: 5.6% v 7.2% prior

- (NO) Norway Central Bank (Norges) May Bank Daily FX Purchases (NOK): -800M v -800Me

- (PT) Portugal Apr Preliminary CPI M/M: 0.7% v 1.9% prior; Y/Y: 0.4% v 0.7% prior

- (PT) Portugal Apr Preliminary CPI EU Harmonized M/M: 1.0% v 2.2% prior; Y/Y: 0.3% v 0.8% prior

- (DE) Germany Apr CPI North Rhine Westphalia M/M: 0.0% v 0.4% prior; Y/Y: 1.5%e v 1.6% prior

- (IT) Italy Apr Preliminary CPI (NIC incl. tobacco) M/M: 0.1% v 0.2%e; Y/Y: 0.5% v 0.7%e

- (IT) Italy Apr Preliminary CPI EU Harmonized M/M: 0.5% v 0.6%e; Y/Y: 0.6% v 0.8%e

- (GR) Greece Feb Retail Sales Volume Y/Y: -0.4% v +0.1% prior

- (IS) Iceland Mar Final Trade Balance (ISK): -14.0BB v -8.2B prelim

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.1% at 384.9, FTSE +0.4 at 7528, DAX +0.2% at 12605, CAC-40 +0.2% at 5491, IBEX-35 +0.4% at 9965, FTSE MIB +0.2% at 23982, SMI +0.4% at 8881, S&P 500 Futures +0.3%]

Market Focal Points/Key Themes:

- European Indices trades slightly higher across the board buoyed by a flurry of M&A deals. UK supermarkets are in focus after Sainsburys and Walmart owned Asda agreed to merge in a deal which valued Asda at £7.2B. Sainsburys shares trade sharply higher following the announcement, with Tesco and Morrisons trading lower in negative sympathy. Deutsche Telekom trades higher after T-Mobile and Sprint agreed to merge with Deutsche Telekom to hold ~40% of the combined company. Elsewhere IC Group and Amer Sports trade higher after IC group divested its Peak Performance unit to Amer in a DKK1.9B deal. On the earnings front WPP outperforms after a 1 update; SEB trades lower after missing on the top and bottom line. Interseve trades sharply lower after a substantial profit fall.

- In the US shares Andeaver shares to be in focus after talks Marthon Petroleum plans to acquire the company for more than $20B, Baidu to divest its Financial Services business, while DCT Industrial trust is to be acquired by Prologis in an $8.4B deal.

- Looking ahead notable earners include Dow components McDonalds, Allergan and Loews.

Movers

- Consumer Discretionary [IC Group [IC.DK] +5% (Amer Sport [AMEAS.FI] +2.1% (IC to divest Peak Performance for DKK1.9B to Amer Sports), WPP [WPP.UK] +7.3% (Earnings), Sainsburys [SBRY.UK] +15% (To merge with Asda), Tesco [TSCO.UK] -1.2% (Negative sympathy from Sainsburys/Asda merger), Morrisons [MRW.UK] +0.1% (Negative sympathy from Sainsburys/Asda merger)]

- Materials [ Glencore [GLEN.UK] -2.7% (Congo freezes assets)]

- Financials [SEB [SEBA.SE]-4.1% (Earnings) ]

- Industrials [Interserve [IRV.UK] -16.4% (Earnings), Wastec [WSH.DE] +3.0% (Earnings)]

- Telecoms [ Telit Communication [TCM.UK] +4.6% (Earnings), Deutsche Telekom [DTE.DE] +1.2% (T-Mobile and Sprint merge)]

Speakers

- EU chief Brexit negotiator Barnier: Must not have a gard border on Ireland. Determined to find a Brexit solution but risks remained. Needed rapid progress on backstop. need to use time to find operational solutions

- Ireland PM Varadkar: Progress was needed on Brexit in June and needed to finalize legal text on backstop. Barnier had unique understanding of Ireland; united with him on issue . No backstop then no withdrawal accord

- Ireland Dep PM Coveney (also foreign Min): Wanted a sensible and managed Brexit and saw extraordinary unity on Brexit. No with drawal accord without backstop

- Italy Five Star leader Di Maio said to signal that no government was possible with Democratic Party (PD)

- Turkey Central Bank (CBRT) Quarterly Inflation Report (QIR) reiterated its stance to maintain the current tight monetary policy and would tighten policy further if needed. To use all available tools. The forecasts raised 2018 CPI from 7.9% to 8.4% while maintaining 2019 CPI at 6.5%

- Turkey Dep PM Simsek: single-digit inflation is hard to achieve in the short term:

Currencies

- The USD held onto recent gains as German inflation data highlighted the headwinds in reaching the ECB 2% target while political woes accompany recent soft UK data

- EUR/USD was probing the lower end of the 1.21 level as recent ECB cautious was thus echoed in German April CPI data.

- GBP/USD was softer and trading in the mid-1.37 area as UK Home Secretary Rudd resigned over an immigration scandal. The political turmoil accompanied the recent spat of soft economic data.

Fixed Income

- Bund Futures trade 15 ticks lower at 158.45 ahead of Thursday’s Euro Zone CPI flash estimate. Upside targets 159.75, while a return lower targets the 157.25 level.

- Gilt futures trade at 122.08 higher by 5 ticks, as investors no longer pricing in a May rate hike. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Monday’s liquidity report showed Friday's excess liquidity fell to €1.859T from €1.879T prior. Use of the marginal lending facility declined from €40M to €37M.

- Corporate issuance saw the primary market sell $26B last week

Looking Ahead

- (IL) Israel Central Bank (BOI) Mar Minutes

- (MX) Mexico Mar YTD Budget Balance (MXN): No est v -67.8B prior

- 06:00 (PT) Portugal Mar Industrial Production M/M: No est v -2.3% prior; Y/Y: No est v 2.1% prior

- 06:00 (PT) Portugal Mar Retail Sales M/M: No est v -1.1% prior; Y/Y: No est v 3.7% prior

- 06:00 (IL) Israel Mar Unemployment Rate: No est v 3.8% prior

- 06:00 (IL) Israel to sell Bonds

- 06:45 (US) Daily Libor Fixing

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 08:00 (DE) Germany Apr Preliminary CPI M/M: -0.1%e v +0.4% prior; Y/Y: 1.5%e v 1.6% prior

- 08:00 (DE) Germany Apr Preliminary CPI EU Harmonized M/M: -0.1%e v +0.4% prior; Y/Y: 1.5%e v 1.5% prior

- 08:00 (ZA) South Africa Mar Trade Balance (ZAR): 3.8Be v 0.4B prior

- 08:00 (ZA) South Africa Mar Budget Balance (ZAR): No est v 20.2B prior

- 08:00 (CL) Chile Mar Unemployment Rate: 6.8%e v 6.7% prior

- 08:00 (CL) Chile Mar Industrial Production Y/Y: 12.0%e v 8.9% prior; Manufacturing Production Y/Y: 0.7%e v 3.7% prior; Total Copper Production: No est v 456.0K tons prior

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Mar Personal Income: 0.4%e v 0.4% prior; Personal Spending: 0.4%e v 0.2% prior

- 08:30 (US) Mar PCE Core M/M: 0.2%e v 0.2% prior; Y/Y: 1.9%e v 1.6% prior

- 08:30 (US) Mar PCE Deflator M/M: 0.0%e v 0.2% prior; Y/Y: 2.0%e v 1.8% prior

- 08:30 (CA) Canada Mar Industrial Product Price M/M: 0.7%e v 0.1% prior; Raw Materials Price Index M/M: No est v -0.3% prior

- 08:55 (FR) France Debt Agency (AFT) to sell combined €4.2-5.4B in 3-month, 6-month and 12-month bills

- 09:00 (MX) Mexico Q1 Preliminary GDP Q/Q: 0.7%e v 0.8% prior; Y/Y: 1.7%e v 1.5% prior

- 09:30 (BR) Brazil Mar Nominal Budget Balance (BRL): -58.4Be v -45.8B prior; Primary Budget Balance: -24.2Be v -17.4B prior

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

- 09:45 (US) Apr Chicago Purchasing Manager: 58.0e v 57.4 prior

- 10:00 (MX) Mexico Mar Net Outstanding Loans (MXN): No est v 4.056T prior

- 10:00 (US) Mar Pending Home Sales M/M: 0.5%e v 3.1% prior; Y/Y: No est v -4.4% prior

- 10:30 (US) Apr Dallas Fed Manufacturing Activity: 25.0e v 21.4 prior

- 11:00 (CO) Colombia Mar National Unemployment Rate: No est v 10.8% prior

- 11:30 (US) Treasury to sell 3-Month and 6-Month Bills

- 15:00 (AR) Argentina Mar Industrial Production Y/Y: 4.9%e v 5.3% prior

- 16:00 (US) Weekly Crop Progress Report