Sample Category Title

Japan’s Manufacturing Sector Growth Revised Higher In April

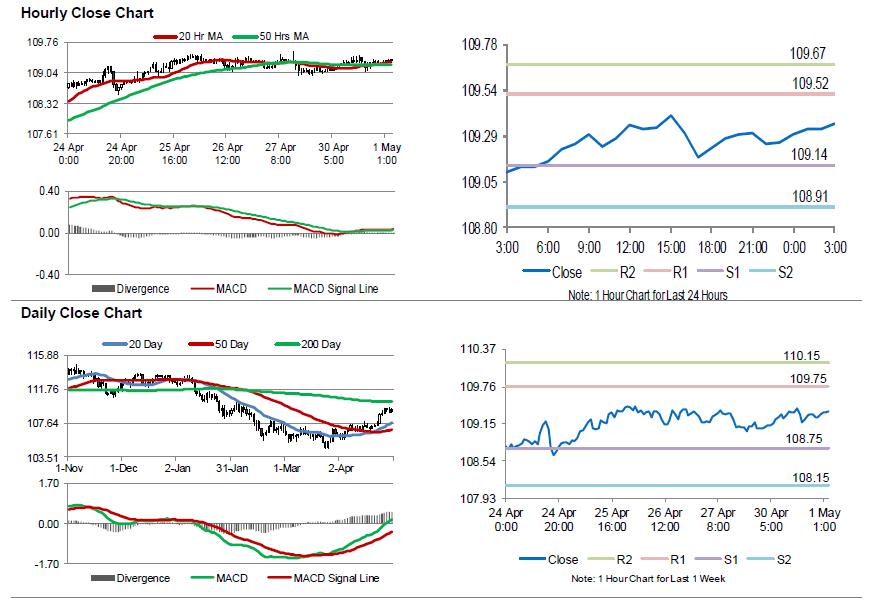

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the JPY and closed at 109.26.

In the Asian session, at GMT0300, the pair is trading at 109.36, with the USD trading 0.09% higher against the JPY from yesterday's close.

Overnight data indicated that Japan's final Nikkei manufacturing PMI advanced more than initially estimated to a level of 53.8 in April, compared to a level of 53.1 in the prior month, while the preliminary figures had indicated an advance to a level of 53.3.

The pair is expected to find support at 109.14, and a fall through could take it to the next support level of 108.91. The pair is expected to find its first resistance at 109.52, and a rise through could take it to the next resistance level of 109.67.

Going ahead, Japan's Nikkei services PMI as well as consumer confidence index, both for April, slated to release overnight, will garner a lot of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss KOF Leading Indicator Rose Less-Than-Anticipated In April

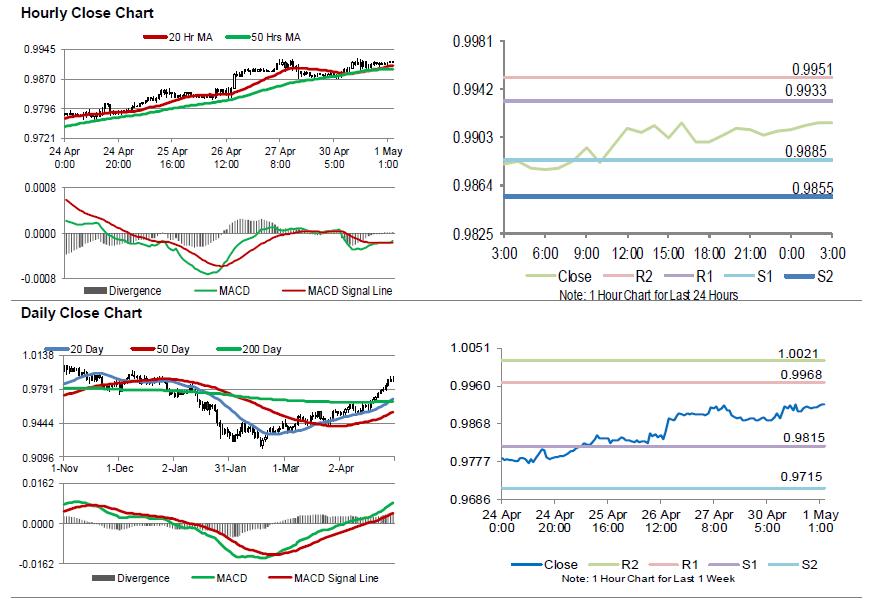

For the 24 hours to 23:00 GMT, the USD rose 0.31% against the CHF and closed at 0.9908.

On the macro front, Switzerland’s KOF leading indicator advanced less-than-expected to a level of 105.3 in April, compared to a revised level of 105.1 in the previous month. Market participants had expected the index to rise to a level of 106.0.

Meanwhile, the nation’s total sight deposits fell to a level of CHF575.2 billion in the week ended 27 April, compared to a level of CHF575.4 billion reported in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9915, with the USD trading 0.07% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9885, and a fall through could take it to the next support level of 0.9855. The pair is expected to find its first resistance at 0.9933, and a rise through could take it to the next resistance level of 0.9951.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading Higher, Ahead Of Canada’s GDP Data

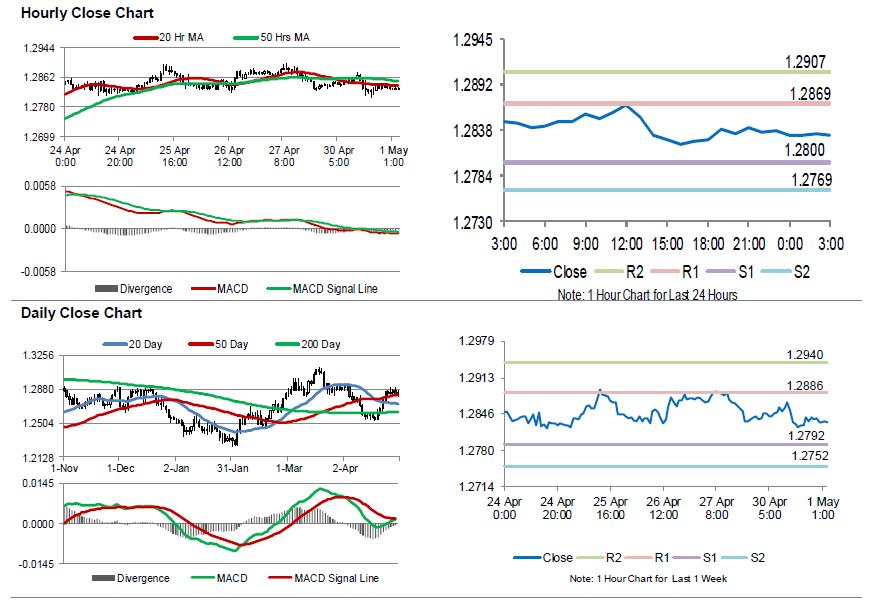

For the 24 hours to 23:00 GMT, the USD declined 0.01% against the CAD and closed at 1.2838.

In the Asian session, at GMT0300, the pair is trading at 1.2832, with the USD trading 0.05% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2800, and a fall through could take it to the next support level of 1.2769. The pair is expected to find its first resistance at 1.2869, and a rise through could take it to the next resistance level of 1.2907.

Ahead in the day, traders would keep a close watch on Canada's crucial GDP figures for February as well as Markit manufacturing PMI for April.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

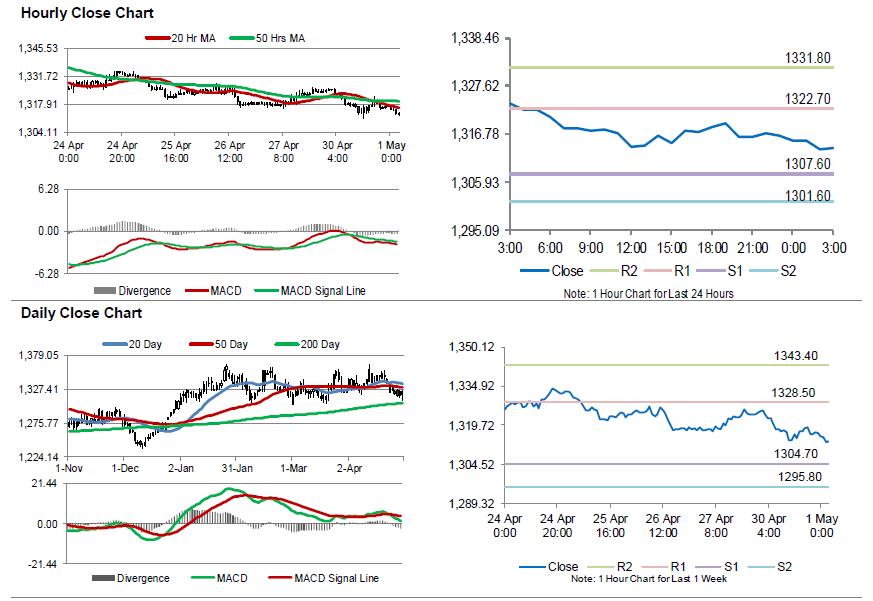

Gold: Yellow Metal Extends Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, Gold declined 0.65% against the USD and closed at USD1317.00 per ounce, as strength in the greenback and easing Korean tensions, dented demand for the precious yellow metal.

In the Asian session, at GMT0300, the pair is trading at 1313.60, with gold trading 0.26% lower against the USD from yesterday’s close.

The pair is expected to find support at 1307.60, and a fall through could take it to the next support level of 1301.60. The pair is expected to find its first resistance at 1322.70, and a rise through could take it to the next resistance level of 1331.80.

The yellow metal is trading below its 20 Hr and 50 Hr moving averages.

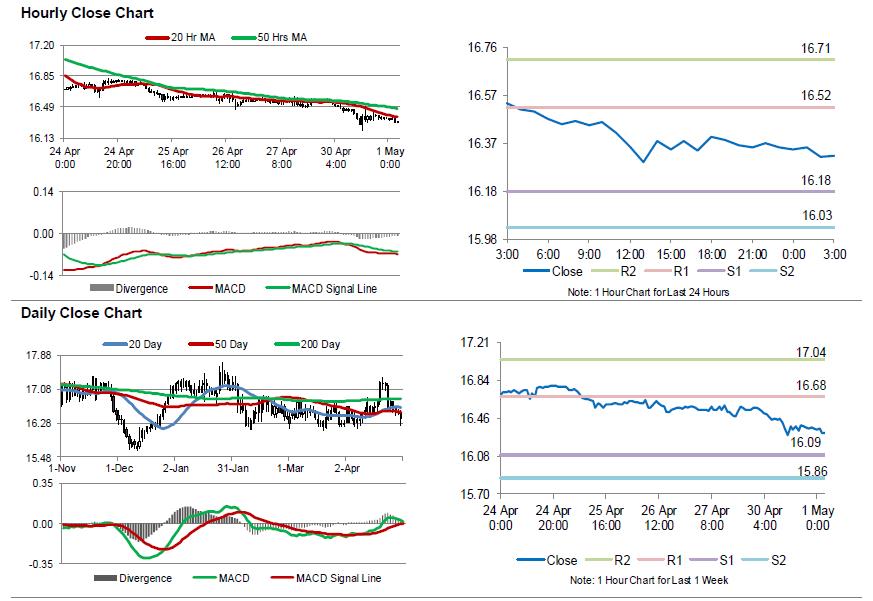

Silver: White Metal Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, Silver declined 1.24% against the USD and closed at USD16.36 per ounce, tracking losses in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.32, with silver trading 0.21% lower against the USD from yesterday’s close.

The pair is expected to find support at 16.18, and a fall through could take it to the next support level of 16.03. The pair is expected to find its first resistance at 16.52, and a rise through could take it to the next resistance level of 16.71.

The white metal is trading below its 20 Hr and 50 Hr moving averages.

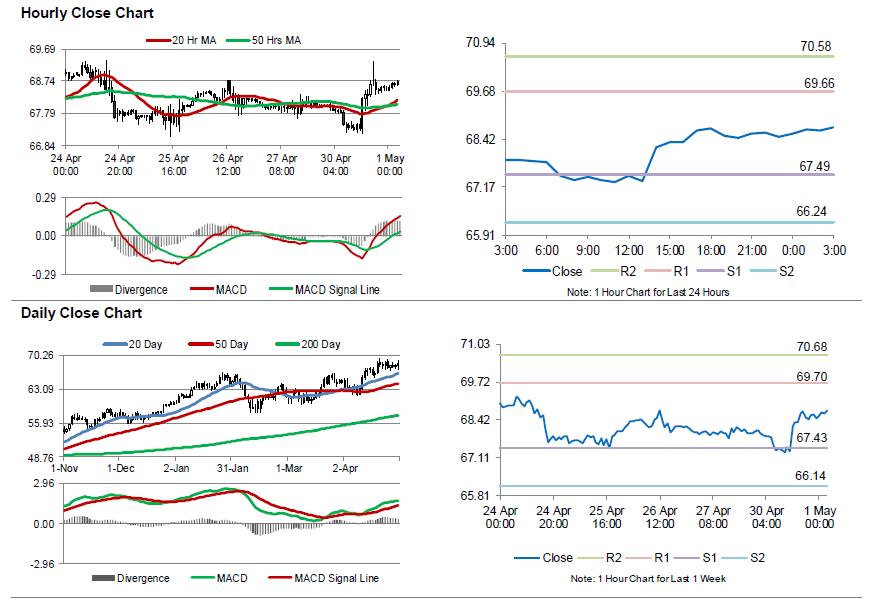

Crude Oil: Oil Trading Higher, Ahead Of API’s Weekly Crude Oil Inventories Data

For the 24 hours to 23:00 GMT, Crude Oil rose 0.77% against the USD and closed at USD68.47 per barrel, buoyed by increased tension in the Middle East, after Israeli Prime Minister, Benjamin Netanyahu, accused Iran of lying about its nuclear ambitions.

Separately, the Energy Information Administration (EIA) reported that US crude oil production jumped 260,000 barrels per day (bpd) to 10.26 million bpd in February.

In the Asian session, at GMT0300, the pair is trading at 68.73, with oil trading 0.38% higher against the USD from yesterday's close.

The pair is expected to find support at 67.49, and a fall through could take it to the next support level of 66.24. The pair is expected to find its first resistance at 69.66, and a rise through could take it to the next resistance level of 70.58.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

RBA left cash rate unchanged at 1.50% as widely expected. Full statement.

RBA left cash rate unchanged at 1.50% as widely expected. Full statement below

Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus and further steps in this direction are expected.

Long-term bond yields have risen over the past six months, but are still low. Equity market volatility has increased from the very low levels of last year, partly because of concerns about the direction of international trade policy in the United States. Credit spreads have also widened a little, but remain low. Financial conditions generally remain expansionary. Conditions in US dollar short-term money markets have, however, tightened over the past few months, with US dollar short-term interest rates having increased for reasons other than the increase in the federal funds rate. This has flowed through to higher short-term interest rates in a few other countries, including Australia.

The price of oil has increased recently, as have the prices of some base metals. Australia's terms of trade are expected to decline over the next few years, but remain at a relatively high level.

The Bank's central forecast for the Australian economy remains for growth to pick up, to average a bit above 3 per cent in 2018 and 2019. This should see some reduction in spare capacity in the economy. Business conditions are positive and non-mining business investment is increasing. Higher levels of public infrastructure investment are also supporting the economy. Stronger growth in exports is expected. One continuing source of uncertainty is the outlook for household consumption, although consumption growth picked up in late 2017. Household income has been growing slowly and debt levels are high.

Employment has grown strongly over the past year, although growth has slowed over recent months. The strong growth in employment has been accompanied by a significant rise in labour force participation, particularly by women and older Australians. The unemployment rate has declined over the past year, but has been steady at around 5½ per cent for some months. The various forward-looking indicators continue to point to solid growth in employment in the period ahead, with a further gradual reduction in the unemployment rate expected. Notwithstanding the improving labour market, wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation remains low. The recent inflation data were in line with the Bank's expectations, with both CPI and underlying inflation running marginally below 2 per cent. Inflation is likely to remain low for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

The Australian dollar has depreciated a little recently, but on a trade-weighted basis remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

The housing markets in Sydney and Melbourne have slowed. Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. APRA's supervisory measures and tighter credit standards have been helpful in containing the build-up of risk in household balance sheets, although the level of household debt remains high.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

(RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus and further steps in this direction are expected.

Long-term bond yields have risen over the past six months, but are still low. Equity market volatility has increased from the very low levels of last year, partly because of concerns about the direction of international trade policy in the United States. Credit spreads have also widened a little, but remain low. Financial conditions generally remain expansionary. Conditions in US dollar short-term money markets have, however, tightened over the past few months, with US dollar short-term interest rates having increased for reasons other than the increase in the federal funds rate. This has flowed through to higher short-term interest rates in a few other countries, including Australia.

The price of oil has increased recently, as have the prices of some base metals. Australia's terms of trade are expected to decline over the next few years, but remain at a relatively high level.

The Bank's central forecast for the Australian economy remains for growth to pick up, to average a bit above 3 per cent in 2018 and 2019. This should see some reduction in spare capacity in the economy. Business conditions are positive and non-mining business investment is increasing. Higher levels of public infrastructure investment are also supporting the economy. Stronger growth in exports is expected. One continuing source of uncertainty is the outlook for household consumption, although consumption growth picked up in late 2017. Household income has been growing slowly and debt levels are high.

Employment has grown strongly over the past year, although growth has slowed over recent months. The strong growth in employment has been accompanied by a significant rise in labour force participation, particularly by women and older Australians. The unemployment rate has declined over the past year, but has been steady at around 5½ per cent for some months. The various forward-looking indicators continue to point to solid growth in employment in the period ahead, with a further gradual reduction in the unemployment rate expected. Notwithstanding the improving labour market, wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation remains low. The recent inflation data were in line with the Bank's expectations, with both CPI and underlying inflation running marginally below 2 per cent. Inflation is likely to remain low for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

The Australian dollar has depreciated a little recently, but on a trade-weighted basis remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

The housing markets in Sydney and Melbourne have slowed. Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. APRA's supervisory measures and tighter credit standards have been helpful in containing the build-up of risk in household balance sheets, although the level of household debt remains high.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

New Zealand FM Robertson: We will stick to Budget Responsibility Rules and deliver surplus

New Zealand's Finance Minister Grant Robertson emphasized is his pre-budget speech today that the center-left coalition government will stick to the "Budget Responsibility Rules". He added that means Budget 2018 will deliver a surplus, and surpluses in subsequent years."

Robertson added that ""we will reduce the level of net core Crown debt to 20 per cent of GDP within five years of taking office.: And, "we owe it to future generations to be fiscally responsible, given the risks New Zealand faces in terms of natural disasters and global economic shock."

The budget will be announced on May 17.

AiG Australia performance of manufacturing: Slower but still buoyant expansion

The Australian Industry Group Australian Performance of Manufacturing Index dropped -4.8 pts to 58.3 in April. AiG noted in the release that it indicated a "slower - but still buoyant - rate of expansion", after reaching a record high in march. April was also the nineteenth month of expanding or stable conditions, the longest run of continuous expansion since 2005.

Looking at the sub-indexes, sales dropped -1.4 to 62.5. Production dropped -0.1 to 62.1. new orders dropped -5 to 61.6. Employment dropped -3.9 to 56.1. Deliveries dropped sharply by -12.8 to 53.8.

Stocks dropped -6.2 to 49.8. Exports dropped -10.9 to 48.0, first contraction since October 2017. AiG noted that "Exports weakened in the food and beverages and the petroleum, coal, chemicals and rubber products sub-sectors."