Sample Category Title

GBPUSD Intraday Analysis

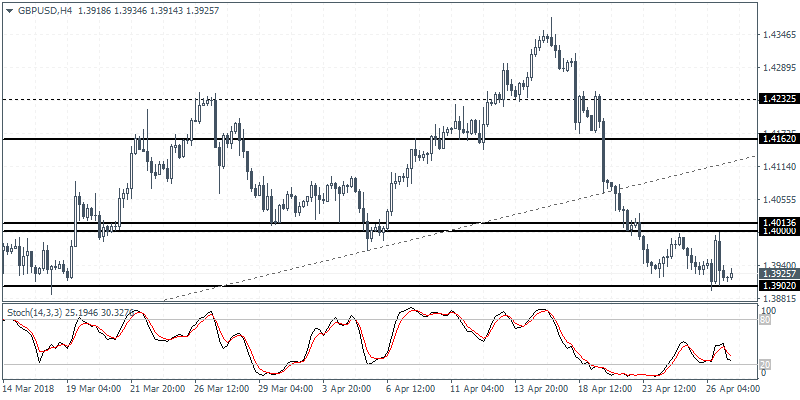

GBPUSD (1.3925): The British pound was seen trading in a range within 1.4000 and 1.3900 levels. The sideways range is expected to trigger a breakout in the near term with the UK's preliminary GDP data on the tap today. To the upside, a breakout above 1.4000 could signal a potential correction back to 1.4162 level. To the downside, a breakdown below 1.3900 could mark a correction towards the 1.3800 round number support. The Stochastics is currently pointing to a bullish divergence that is being formed, which could signal a correction to the upside.

EURUSD Intraday Analysis

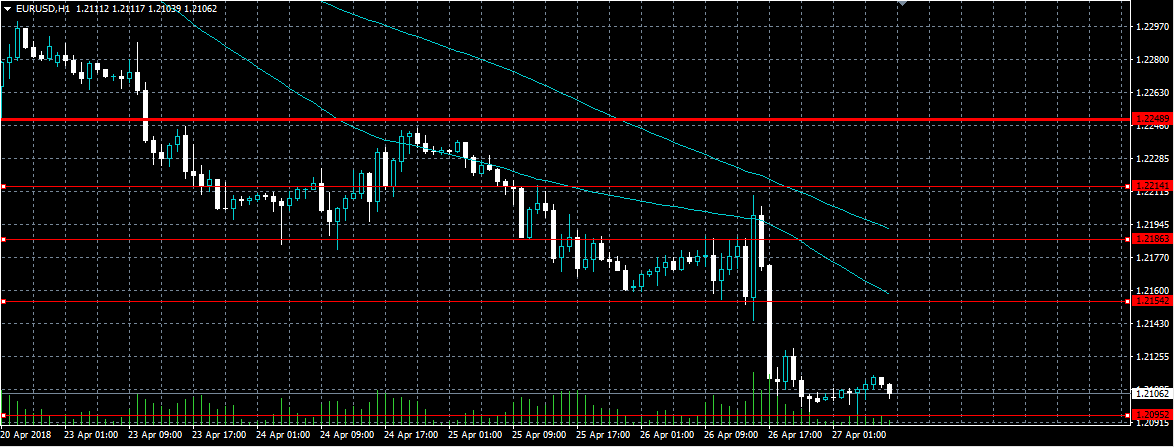

EURUSD (1.2111): The EURUSD currency pair posted strong losses on the day after price action failed to find support at 1.2180 level. The breakdown below this level signaled a decline with the EURUSD now seen trading close to the lower support level at 1.2090. We expect to see some consolidation at this level and could potentially mark a short term reversal. The short term correction could see the EURUSD test the 1.2180 level where resistance could be established.

Euro Drops On ECB, U.S. And UK GDP On Tap

The European Central Bank left monetary policy unchanged at its meeting yesterday as widely expected. The central bank retained the same language from the previous monetary policy meeting. At the press conference, the ECB President Draghi said that the central bank was monitoring the developments in the economy while he downplayed the recent soft patch in the economy. The euro was seen posting strong losses on the day.

Elsewhere, economic data over the day saw the release of the core durable goods orders which remained flat and fell short of expectations of 0.5%. Previous month's data was revised down to 1.0%. Durable goods orders however increased 2.6% on the month. This beat forecasts of 1.6% on the month.

Looking ahead, the GDP data from the U.S. and the UK will be coming out today. The U.S. economy is forecast to rise 2.0% on the month while the UK's GDP is forecast to rise at a slower pace of 0.3%. Later in the day, the Bank of England Governor Carney is expected to speak.

Fresh selling in Euro as France Q1 GDP missed, rose 0.3% qoq only

Fresh selling seen in Euro after French data miss. French GDP growth slowed to 0.3% qoq in Q1, down from prior quarter's 0.7% qoq and missed expectation of 0.4% qoq. Annual rate decelerated to 2.1% yoy, down from 2.6% yoy, and missed expectation of 2.3% yoy.

The title of this report ECB: Wondering Rather than Worrying summed up yesterday's ECB press conference rather well. And with French GDP miss, dovish expectation on next week's Eurozone GDP release could pile up. We'll see if the coming data clear up the picture for ECB so that policymakers don't need to wonder any more, but start to worry.

For now, EUR/USD is on course for 1.2 handle. Selling in EUR/USD also spill over to other pairs and lifted the USD. USD/CHF takes out 0.99 and would now be heading back to 1.000. GBP/USD breaks yesterday's low at 1.3894, just ahead of UK GDP data, an hour away.

EURUSD Medium-Term Bearish Below 1.2154 Level

The euro had fallen to its lowest trading level in three-month against the U.S dollar, hitting 1.2095, after the key 1.2154 support level was finally breached on Thursday. The EURUSD pair tumbled lower as the U.S dollar index surged higher on much better than expected U.S economic data, as U.S Initial Jobless claims hit a forty-eight year low. Sellers may target the key 1.2050 and 1.2000 levels, with the euro now medium-term bearish while trading below the 1.2154 level.

The EURUSD pair is strongly bearish while trading below the 1.2154 level, further intraday losses towards 1.2054 and 1.2030 appear possible.

If the EURUSD pair starts to trade back above the 1.2154 level, a correction back towards the 1.2200 and 1.2248 levels may occur.

USDJPY Upside Intact After BoJ Meeting

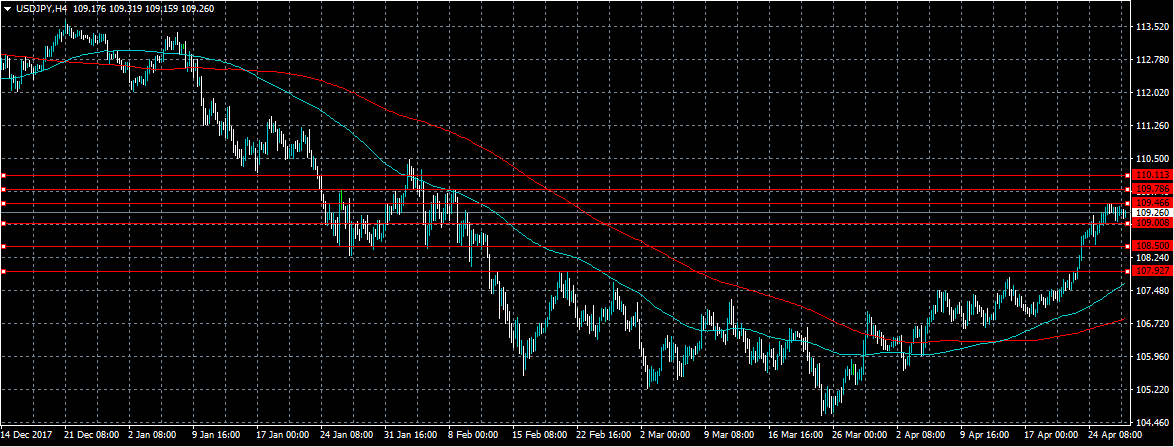

The U.S dollar continues to move higher against the Japanese yen currency, after the Bank of Japan Policy Meeting offered few surprises to traders early today. The USDJPY pair currently trades around the 109.30 level, after finding further dip-buying demand from just above the 109.00 handle. Traders are likely to focus on the psychological 110.00 level if the pair continues to move higher, and the release of key GDP and Consumer Confidence data from the United States economy later today.

The USDJPY pair remains bullish while trading above the pivotal 109.30 level, intraday resistance is now found at the 109.78 and 110.11 levels.

If the USDJPY pair moves below the 109.30 level for a sustained period, sellers may target the 109.00 and 108.50 support levels.

US And European Data Will Draw Headlines On Friday

The economic calendar will end the week with a bang, as governments in the Eurozone, United Kingdom and United States release headline indicators.

The economic calendar will end the week with a bang, as governments in the Eurozone, United Kingdom and United States release headline indicators.

The first major report of the day comes our way at 08:00 GMT when the German government reports on the labour market. Germany's unemployment rate is forecast to hold steady for the month of April.

At 08:30 GMT, the UK's Office for National Statistics will report on first-quarter gross domestic product (GDP). Analysts are forecasting quarterly growth of 0.3%, which translates into a year-over-year gain of 1.4%.

A slew of sentiment indicators covering the Eurozone will make their way through the financial markets at 09:00 GMT. The European Commission's statistical agency will report on consumer confidence, services sentiment, industrial confidence, business confidence and the economic sentiment indicator.

The North American session begins with a high-profile report on US first-quarter GDP, which is scheduled for release at 12:30 GMT. The US economy is forecast to have grown 2% annually between January and March, well below Q4's 2.9% annual pace.

The core personal consumption expenditures (PCE) index, which is the Federal Reserve's preferred measure of inflation, is forecast to climb 2.4% in the first quarter. That's well above the central bank's target of 2% and much higher than the 1.9% pace seen in Q4.

At 14:00 GMT, the University of Michigan will release its final reading of the April consumer sentiment index.

In terms of monetary policy, Bank of England (BOE) Governor Mark Carney will deliver a speech at 14:00 GMT. Colleague and fellow Monetary Policy Committee (MPC) member Andrew Haldane will also deliver a speech at 14:15 GMT.

Later in the day, Baker Hughes Inc. will release its weekly report on active US rig counts. Energy traders will be closely monitoring this report.

EUR/USD

Europe's common currency fell to fresh three-month lows on Thursday following a dovish reading of the ECB's policy decision. EUR/USD was last seen trading just above 1.2100, having declined roughly 300 pips from this month's high. The pair is now holding on to the immediate support of 1.2092, which corresponds with the 2017 high.

GBP/USD

Cable is bracing for an active session headlined by multiple GDP reports. GBP/USD attempted a rally on Thursday but was pushed back at the 1.3985 level. Prices are back to trading in the low 1.3920 region. Immediate support is located at 1.3895. Resistance is seen at 1.3990.

USD/JPY

The Japanese yen steadied on Thursday following a series of brutal declines, as investors turned their attention to the BOJ policy meeting. Speculation about Japanese monetary policy will likely drive the USD/JPY exchange rate on Friday. The pair was last seen trading at 109.27.

Currencies: Will US Data Be Strong Enough To Confirm EUR/USD 1.2155 Break?

Rates: Side-lined ahead of next week's key US eco data

The ECB wants to spend time finding out whether the recent setback in EMU eco data is temporary. It suggests that markets will be more sensitive to eco numbers as well. Draghi's overall message shouldn't have a permanent impact though. We expect a neutral session today, with especially US investors side-lined ahead of next week's key data and Fed meeting.

Currencies: Will US data be strong enough to confirm EUR/USD 1.2155 break?

EUR/USD dropped below the 1.2155 range bottom yesterday. Draghi kept a wait-and-see approach. Combined with underlying USD strength, this was apparently enough for some stale euro longs to throw the towel. From here, the focus returns the US side of the story. Will upcoming US data be strong enough to support a further rise in US yields and the USD?

The Sunrise Headlines

- US stock markets eked out gains of 1% with Nasdaq outperforming (+1.64%) following strong tech earnings (eg Facebook, Amazon, Microsoft). Asian equity indices gain less ground with China again underperforming.

- The BoJ left its stimulus program unchanged, while removing language from its statement declaring that it would reach 2% inflation around fiscal 2019. The Japanese yen remains remarkably strong. (BB)

- North Korean leader Kim Jun Un met with South Korean President Moon Jae-in. Their meeting is set to determine the future of relations on the Korean Peninsula and lay the groundwork for the US/North Korean Summit. (WSJ)

- China is open to negotiating with the US to resolve trade tensions, Premier Li Keqiang was quoted as saying by state media, noting that the countries should manage their conflicts through dialogue. (Reuters)

- Both headline (0.5% Y/Y) and core (0.6% Y/Y) Tokyo CPI printed significantly below consensus in April. March retail sales (-0.7% M/M) fell short of forecast as well, while industrial production (1.2% M/M) did manage to beat the bar.

- Profit growth at Chinese industrial firms slowed to its weakest pace in over a year in March, in a sign of increasing headwinds for the Chines economy as policy makers navigate debt risks and a heated trade row with the US. (Reuters)

- Today's eco calendar contains German labour market data, EZ economic confidence and Q1 GDP readings in the UK and the US. BoE Carney is scheduled to speak. Italy sells bonds

Currencies: Will US Data Be Strong Enough To Confirm EUR/USD 1.2155 Break?

US data strong enough to confirm 1.2155 break?

The rise of core/US yields and of the dollar slowed yesterday ahead of the ECB's policy decision. The ECB left policy unchanged and Draghi didn't give new info on a future change in policy. First tests of 1.2155 support before and during the press conference failed. Later, the break finally succeeded. The constructive underlying USD momentum was the main driver. The lack of new guidance on ECB normalization probably discouraged euro longs. EUR/USD was already on a down trajectory. The topside in the likes of EUR/GBP and EUR/JPY was blocked. More euro longs finally threw the towel. EUR/USD closed the session at 1.2103. USD/JPY finished the day little changed at 109.30. EUR/JPY finished at 132.30 (from 133.07).

Asian equities mostly show modest gains overnight supported by good results from several technology bellwethers, including Amazon. The underperformance of Chinese stocks is again striking. The BOJ maintains its policy stimulation, as expected, but changed its language on inflation. It removed the assessment for inflation to reach 2% around fiscal year 2019. For now, the impact on the yen is close to non-existent. USD/JPY trades in the 109.15 area. EUR/USD hovers in the low 1.21 area.

The eco calendar heats up today with the EC confidence data, Q1 growth figures in France, Spain and Belgium and German labour data. The key data feature is the US advance Q1 GDP report. A modest 2.0% Q/Qa is expected. So, the bar of consensus is not that high. We keep also a close eye at the price series of the report. The core PCE deflator is expected to rise from 1.9% to 2.5%! Quarterly growth data are always a bit backward looking. In this respect, we assume that next week's US early month data are more important for the fate of the dollar. However, a constructive report might support further USD gains. From a technical point of view, we look for confirmation of yesterday's break below 1.2155. If confirmed, next support comes in at 1.2055 (50% retracement) and the 1.1936/16 area (62 % retracement/jan 2018 low).

EUR/GBP dropped from the mid 0.87 area to fill bids north of 0.8680 yesterday. We see the move mainly as euro softness. UK Q1 GDP is expected at a soft 0.3% Q/Q and 1.4% Y/Y today. BoE Carney and Haldane speak. We don't expect any high profile news for sterling. However, market expectations are already low. Further euro (EUR/USD) weakness might still filter through in the EUR/GBP momentum.

EUR/USD rebound to slow?

Markets Focus On US And UK GDP

At 08:30 GMT, UK Gross Domestic Product (QoQ) (Q1) is expected to come in at 0.3% from 0.4% previously. Gross Domestic Product (YoY) (Q1) is expected to be unchanged at 1.4%. UK GDP has been moving lower since the highs of 1.1% and 1.0% in 2010 and 2012 respectively. On the positive side, the last two readings beat expectations, with this quarter’s number expected to show a 0.1% decrease and the yearly number holding steady. GBP crosses can see a spike in volatility should the data differ from the expected consensus.

At 12:30 GMT, US Gross Domestic Product Annualized (Q1) is expected to be 2.0% from 2.9% previously. Gross Domestic Product Price Index (Q1) is expected to be 2.2% from 2.3% previously. These GDP figures are expected to fall this time, as growth moderates. Core Personal Consumption Expenditures (QoQ) (Q1) is expected to be 2.4% v a prior 1.9% reading from Q4. Personal Consumption Expenditure Prices (QoQ) (Q1) are expected to be 2.6% v a previous 2.7%. This data is expected to show a slight drop in headline inflation but the core data is expected to be higher. USD crosses may be heavily traded as a result of this data.

BoJ Suggests Uncertainty About When Inflation Target Will Be Met

General Trend:

- Asian equity markets trade generally higher after US gains; Shanghai lags

- Japanese automation machinery company Fanuc declines over 7% after outlook

- Bank of Japan (BoJ) policy statement omits prior reference related to reaching 2% inflation target around FY19/20

- China March industrial profits grow at slowest rate in more than 1-year, holiday effect cited

- At Inter-Korean summit, North Korea Leader Kim suggests possibility of more meetings with South Korea

- Markets are now looking ahead to BoJ Gov Kuroda’s post rate decision press conference (0630 GMT)

- Q1 Advance GDP data due out of the US and UK

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened +0.1%; closed +0.7%

- Mineral Deposits [MDL.AU] rises over 25% after receiving bid from Eramet

- (AU) AUSTRALIA Q1 PPI Q/Q: 0.5% V 0.6% PRIOR; Y/Y: 1.7% V 1.7% PRIOR

- (AU) Australia sells A$500M v A$500M indicated in Nov 2022 bonds, avg yield 2.4294%, bid to cover: 6.1x

China/Hong Kong

- Shanghai Composite opened +0.2%, Hang Seng +1%

- (CN) China yuan (CNY) exchange rate faces unchanged two-way movement trend; CNY faces depreciation pressures but not large – China Securities Journal

- (CN) CHINA MAR INDUSTRIAL PROFITS Y/Y: 3.1% V 10.8% PRIOR (more than 1-year low)

- (CN) China Daily Commentary Piece: Property controls should be targeted

- (CN) China PBoC Open Market Operation (OMO): Injects CNY40B in 7-day reverse repos v CNY100B prior; Net: drains nil v CNY150B prior

- (CN) China PBoC sets yuan reference rate at 6.3393 v 6.3283 prior

Japan

- Nikkei 225 opened +0.7%; closed +0.7%

- (JP) BANK OF JAPAN (BOJ) LEAVES INTEREST RATE ON EXCESS RESERVES (IOER) UNCHANGED AT -0.10%, AS EXPECTED

- (JP) BOJ Quarterly Outlook for Economic Activity and Prices: Removes wording on reaching 2% inflation target around FY19/20

- (JP) JAPAN MAR JOBLESS RATE: 2.5% V 2.5%E

- (JP) JAPAN MAR PRELIMINARY INDUSTRIAL PRODUCTION M/M: 1.2% V 0.5%E; Y/Y: 2.2% V 2.0%E

- (JP) Japan Apr Tokyo CPI Y/Y: 0.5% v 0.8%e; Ex-Fresh Food (Core) Y/Y: 0.6% v 0.8%e

- (JP) JAPAN MAR PRELIMINARY RETAIL SALES M/M: -0.7% V 0.0%E; RETAIL TRADE Y/Y: 1.0% V 1.5%E

- (JP) JAPAN MAR ANNUALIZED HOUSING STARTS: 895K V 930KE; Y/Y: -8.3% V -4.8%E

Korea

- Kospi opened +0.9% ahead of Inter-Korean summit

- Kia Motors [000270.KR] reported Q1 results above ests, shares rise over 2%

- (KR) South Korea President’s Office Official: Confirms North Korea leader Kim said he would visit South Korea’s presidential house at any time; Hopes summit leads to meetings in North Korea and South Korea.

North America

- US equity markets ended higher: Dow +1%, S&P500 +1%, Nasdaq +1.6%, Russell 2000 +0.5%

- S&P500 Technology +1.8%, Consumer Discretionary +1.6%

Europe

- Shire [SHP.UK]: A top 10 shareholder said to seek improved offer - UK Press

Levels as of 02:00ET

- Hang Seng +0.6%; Shanghai Composite -0.2%; Kospi +1.4%

- Equity Futures: S&P500 -0.2%; Nasdaq100 +0.2%, Dax -0.1%; FTSE100 -0.3%

- EUR 1.2095-1.2117; JPY 109.13-109.37 ; AUD 0.7538-0.7561 ;NZD 0.7051-0.7072

- Jun Gold flat at $1,318/oz; May Crude Oil -0.3% at $67.97/brl; May Copper -0.3% at $3.106/lb