Sample Category Title

ECB Hold Steady As The BOJ Removes Inflation Target

The ECB held rates steady yesterday and stayed tight-lipped on everything, forcing analysts to concentrate on the June meeting for policy change, in a quiet before the storm scenario. EURGBP fell to a low of 0.86805 for the day, as Euro bears took control. The BOJ also held rates unchanged but removed their time target for inflation. The press conference from Tokyo is due to take place shortly and traders will look to it for direction.

North and South Korean Leaders are meeting today for the first time to discuss denuclearization, with the risk to the downside that they fail to reach an agreement. Markets are still in risk-on mode, despite the selling early this week. Gold has dropped to support around 1315.00 and equity indices have regained almost all their losses.

German Gfk Consumer Confidence Survey (May) was as expected at 10.8, from the previous 10.9. This number came in just under last month's figure. The February reading came in at the highest level in more than ten years at 11.0. Economic data in Germany has been showing slower growth, with Business confidence also taking a hit recently, but it has not come through in this release in any noticeable way. EURGBP moved up from 0.87300 to 0.87370 following this data release.

The ECB Deposit Rate Decision was announced, with the central bank leaving rates unchanged as expected at -0.4%. The ECB Interest Rate Decision was left unchanged at 0%. The ECB Press Conference and Monetary Policy Statement followed at 12:30 GMT. ECB President Mario Draghi explained away recent economic data, concluding that the weakness in the figures was likely to be temporary and growth continues to be solid and broad-based. On Inflation, he said that the ECB is confident in its target but that underlying inflation remains subdued. He was firm that normalisation should proceed at a gradual pace and chose not to speak about the Euro in any detail. As a result, EURUSD sold off from 1.22040 to 1.21000, as the June meeting is now being heralded as the decisive event for Interest Rates and QE going forward.

US Durable Goods Orders Ex-Transportation (Mar) were 0.0% against an expected 0.5%, from 0.9% previously, which was revised down from 1.2%. Durable Goods Orders (Mar) was 2.6% v an expected 1.6%, against 3.5% previously, which was revised up from 3.1%. This data series shows that transportation accounted for much of the beat in the headline number, but the series fell from last month's figures despite revisions. US Initial Jobless Claims (Apr 20) was 209K against an expected 230K, from 232K previously, which was revised up to 233K. Continuing Jobless Claims (Apr 13) was 1.837M against an expected 1.850M, from 1.863M previously, which was revised up to 1.866M. Jobless Claims had beaten expectations on the last three readings, but numbers have been decreasing from the 242K high three weeks ago. On this occasion, the data was less than expected, with new claims at a new multi-year low. GBPUSD hit 1.39515 after the release but rallied to 1.39975 in the following two hours.

EURUSD is up 0.05% overnight, trading around 1.21089.

USDJPY is down -0.04% in early session trading at around 109.248.

GBPUSD is up 0.12% this morning, trading around 1.39299.

Gold is up 0.03% in early morning trading at around $1,317.27.

WTI is down -0.40% this morning, trading around $67.92.

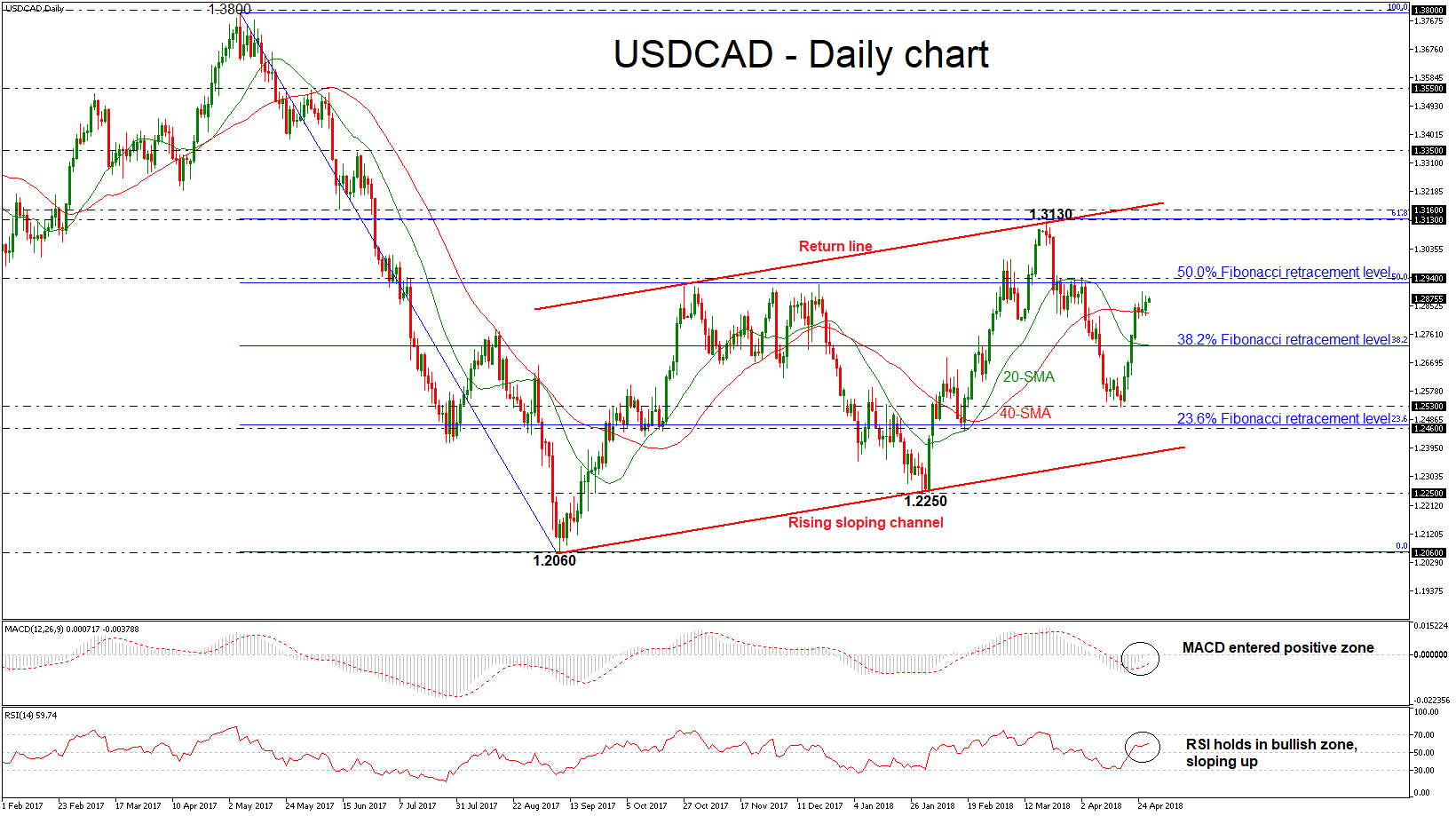

USDCAD Maintains Bullish Bias In Near Term, Immediate Resistance At 50.0% Fibonacci Mark

USDCAD is ready to complete two consecutive positive weeks after the rebound on the 1.2530 support level. When looking at the bigger picture, the pair has been trading within a rising sloping channel since September 2017, failing several times to exit from this range. The technical indicators, though, continue to send bullish signals, suggesting that the bullish market is not over yet.

The MACD oscillator has crossed above the zero line, indicating that the market could strengthen a little bit more in the short-term. The Relative Strength Index (RSI) is standing in the positive area and is pointing to the upside supporting a bullish picture as well. As a side note, the price successfully surpassed above the simple moving averages and the 38.2% Fibonacci retracement level around 1.2720 of the downleg from 1.3800 to 1.2060.

Should the pair manage to strengthen its positive momentum, the next resistance could come around the 50.0% Fibonacci level slightly below the 1.2940 strong resistance level. A break above this level would endorse the bullish bias and open the way towards the 1.3130 – 1.3160 resistance zone, which stands near the return line of the upward sloping channel.

In case of declines in the pair, immediate support may be found near the 38.2% Fibonacci of 1.2720, which coincides with the 20-day simple moving average (SMA). A downside break of this zone would open the way towards the 1.2530 support barrier. If sellers manage to push below that hurdle too, that would drive the price until the 23.6% Fibonacci neat 1.2460.

ECB: Wondering Rather than Worrying

- Draghi signaled that growth peak might be behind us

- Monetary policy wasn't discussed!

- ECB is assessing signs of slowing growth of late...

- ...but at this point and still 'confident' inflation will move towards target

- ECB clearly in no rush to point markets towards tightening.......

There was little or no expectation that yesterday's regular ECB policy meeting would send any major policy signals. There is an almost universal expectation that the ECB will be slow to embark on what is widely seen as a very gradual path towards normalising policy. The recent sequence of softer than expected activity indicators have convinced many in financial markets that the first steps in this process could have moved even further into the future.

The sense that we are still some distance from the first material move towards tighter ECB policy was firmly conveyed by ECB president Mario Draghi's unprompted indication at the start of the Q&A session that 'the interesting thing is that we didn't discuss monetary policy per se' at the meeting.

Softer data complicate the policy message

Mr Draghi indicated that they largely focused on a discussion of recent softer economic data. He elaborated that the ECB wanted to be sure to 'understand current developments before discussing future policy' and went on to indicate that its reading of current developments would be very important in deciding its next steps.

It should be said that Mr Draghi went on to say that any 'caution' implied by its current stance is 'tempered by an unchanged confidence that inflation will converge towards our aim over the medium term'. So, there is no signal that the ECB is backtracking in terms of its future intention. ECB vice‐president Constancio noted that the ECB is still moving on a path towards normalisation. However, recent developments may mean the ECB may be slower to send clear signals of its intentions than previously envisaged.

We think a couple of complementary reasons can be suggested for the note of 'caution' sounded by Mr Draghi. First of all, ahead of a major if likely gradual change in the stance of monetary policy, it is not unreasonable to want to clarify whether the recent softening in a range of indicators could be warning of a renewed weakening of the Euro area economy‐‐particularly in light of the ECB's missteps in mid‐2008 and early 2011.

Second, given a still significant shortfall in inflation relative to target, the ECB clearly wants to avoid any premature tightening of financial conditions and, in circumstances of increased uncertainty, would probably not protest too strongly against modest market movements that offered a little more support to activity in the short term.

For these reasons, we think Mr Draghi will not be too concerned if the exchange rate of the Euro or market interest rates ease a little in current circumstances but we don't see the ECB favouring a dramatic slide in either in the absence of unexpectedly weak economic data in coming weeks. We think the ECB is still largely of the view that the Euro area economy is set on a healthy growth path but it wants some clarification of the nature and extent of the slowdown suggested by recent indicators.

Differences in thinking

Mr Draghi's opening press statement acknowledged 'some moderation in the pace of growth since the start of the year and went on to note that the ECB now sees growth being 'solid' rather than the previously indicated 'strong'. This is consistent with an element of hesitation on the part of the ECB but we don't think it points to a fundamental change in view. The press statement also points to the healthy current momentum by referencing last year's growth rate as 'the highest since 2007' and underscores this further by indicating that in time 'the underlying strength of the Euro area economy' should deliver the ECB's inflation objective.

Mr Draghi gave some flavour by elaborating at some length on the discussion on current economic circumstances. He indicated that reports on recent developments had been given by representatives of the national central banks in all Euro area member states and acknowledged that the recent softening in the trajectory of growth was broad based across sectors and countries.

While Mr Draghi suggested that softer growth was largely unexpected and not fully understood, he set out a list of mitigating factors including the observation that the latest PMI data for April hinted at a possible stabilisation as well as highlighting that the pace of growth remains well above historic averages. He also mentioned a range of influences that might point towards a temporary rather than permanent slowdown of late including unusually poor weather, the impact of strikes and distorting effects related to the timing of Easter.

Having outlined a lengthy set of possible reasons why the recent slowdown would likely not prove significant, Mr Draghi also admitted that some indicators were at least hinting at a possible softening in demand that could prove more problematic and warranted 'monitoring'. Our sense is the latter would not be a major concern but for a significant shadow hanging over the future course of international trade relations.

While Mr Draghi noted problems in regard to trade prospects were still largely confined to 'rhetoric', he acknowledged the threat of disruptive actions. Such a possibility is more formally conceded in the opening press statement's indication that although upside and downside risks to the outlook for activity remain broadly balanced, 'risks related to global factors, including the threat of increased protectionism, have become more prominent'.

Our judgement is that interpretations of recent softer data and their implications for the ECB's policy path likely vary significantly across the ECB's governing council. In the absence of consensus in this regard and mindful of a continuing threat of disruptive developments in relation to global trade, it is understandable that the ECB might decide that discretion is the better part of valour and opt to delay any signalling of future plans.

An aberration rather than an apocalypse?

It is difficult to explain why the trajectory of economic growth in the Euro area (and elsewhere) might suddenly wilt in the absence of a marked change in economic policy or confidence drivers. It is entirely possible that the recent signs of moderation in a range of growth indicators point towards an easing towards a more sustainable if still robust rate of growth.

It is also possible that the signal to noise ratio in a range of indicators has deteriorated of late as occasionally happens. As the diagram below shows, the monthly fluctuations in PMI data (singled out here because Draghi specifically referred to them), would have signalled a number of 'false negatives' in recent years.

Policy implications may not be fully clear

More importantly, readings for the composite PMI series for the past couple of months would still appear consistent with an historically strong quarterly GDP growth rate for the Euro area close to 0.5%. Provided that we don't see some negative shock materialise in the next couple of months, markets may have to rethink how prepared they are for even a modest path towards ECB tightening.

A final consideration raised a couple of times by Mr Draghi is an element of uncertainty as to how to place the current apparent slowdown in growth and the exceptional pace that preceded it in a proper context. One possible if not entirely plausible explanation offered for the recent slowdown is the Euro area economy may already running into capacity constraints in specific areas such as construction. On that view, the path towards and along policy tightening might need to be accelerated before long.

A more interesting suggestion is that the acceleration in growth through 2017 could be pointing towards stronger potential growth than previously envisaged. While this might suggest more spare capacity and, hence, less urgency to tighten immediately, as Mr Draghi pointed out, this stronger growth capacity would also imply the longer term 'neutral ' or equilibrium rate that balances the economy would be somewhat higher than currently thought. In such circumstances markets might have to consider how to balance the implications of a later departure but a more distant final destination for ECB policy rates.

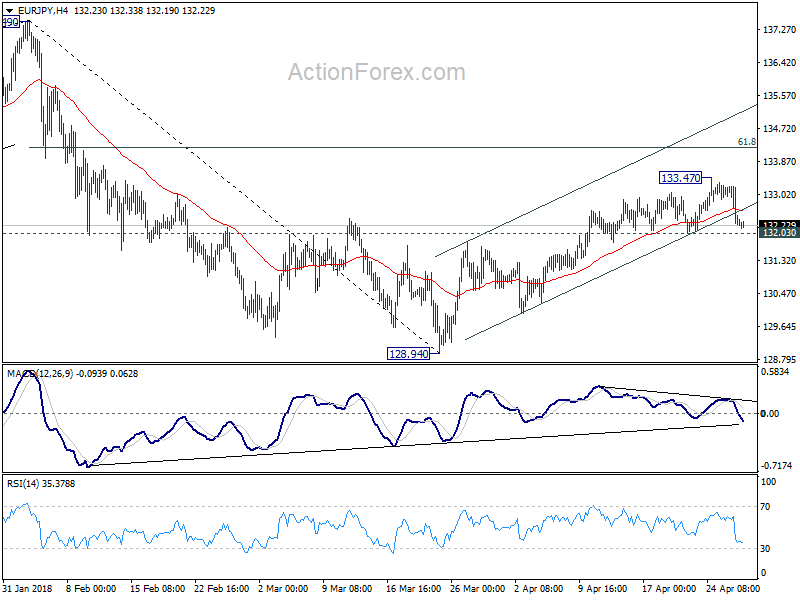

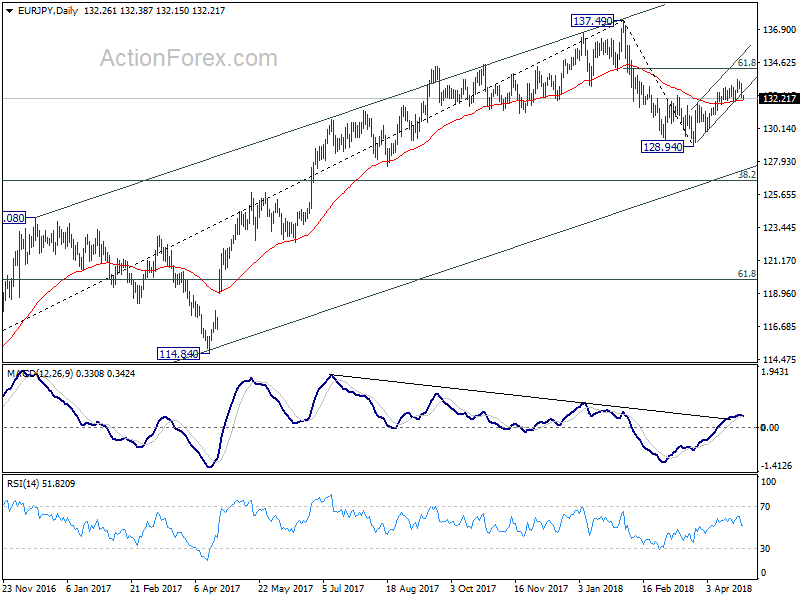

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.97; (P) 132.60; (R1) 132.93; More....

No change in EUR/JPY's outlook. EUR/JPY's recovery from 128.94 might still extend. But after all, it's seen as a corrective move. Therefore, we expect strong resistance from 61.8% retracement of 137.49 to 128.94 at 134.22 to limit upside. Break of 132.03 will turn bias to the downside for retesting 128.94 low. However, sustained break of 134.22 will turn focus back to 137.49 high instead.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. Strong support from 55 week EMA (now at 129.91) suggests that the first leg has completed at 128.94 already. Nonetheless, break of 137.49 is needed to confirm resumption of the rise from 109.03 (2016 low). Otherwise, we'd expect more corrective range trading, with risk of another fall to 38.2% retracement of 109.03 to 137.49 at 126.61 before completion.

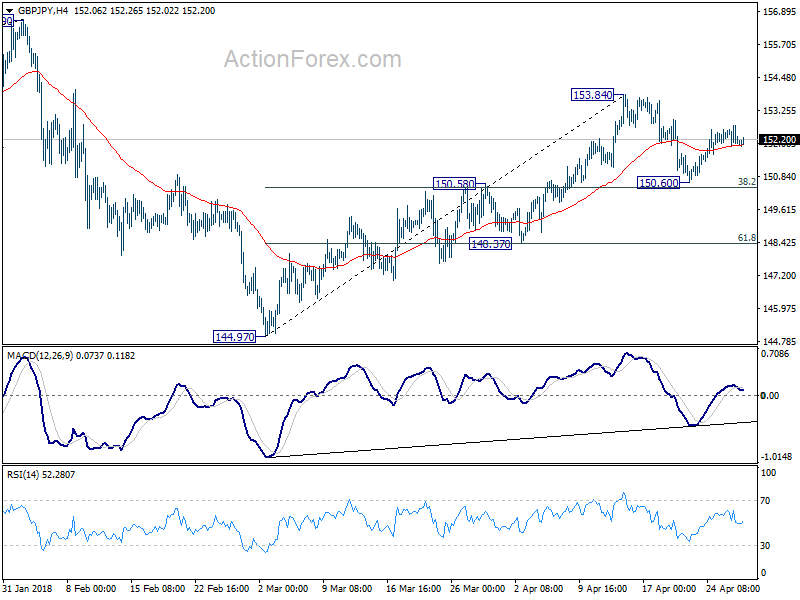

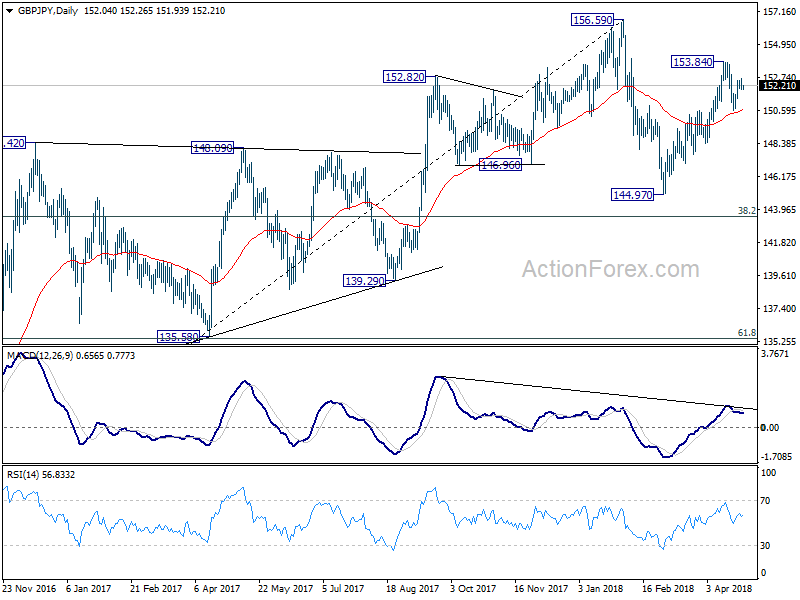

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.74; (P) 152.23; (R1) 152.55; More...

Intraday bias in GBP/JPY remains neutral at this point. We're holding on to the view that corrective rise from 144.97 should have completed at 153.84 already. Hence, another decline is expected in the cross. Break of 150.60 will target 148.37 support first. Break will bring retest of 144.97 low. However, firm break of 153.84 will invalidate our view and extend the rise from 144.97 towards 156.59 high.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

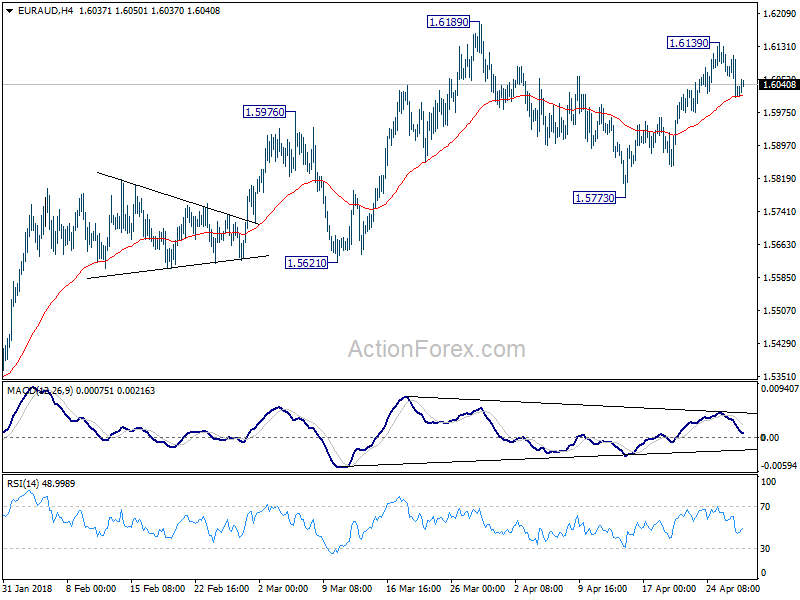

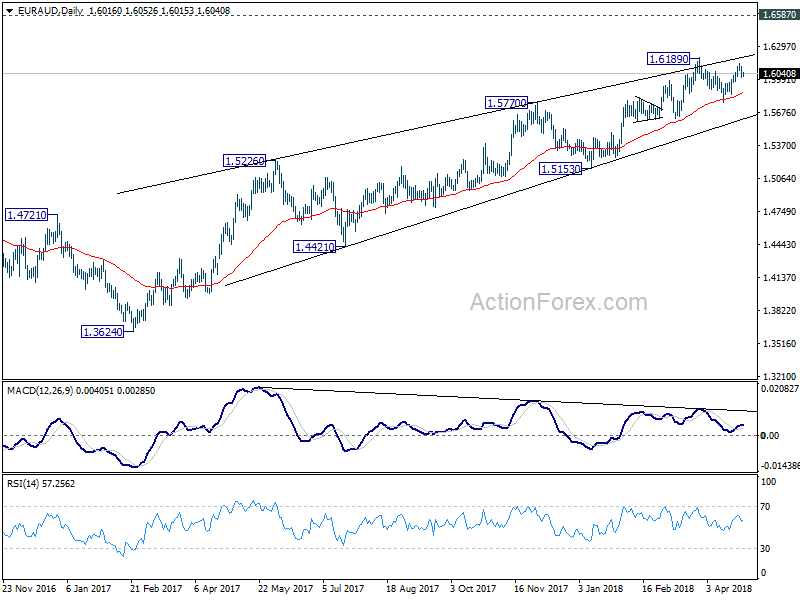

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5986; (P) 1.6048; (R1) 1.6083; More....

The rebound from 1.5773 should have finished at 1.6139 already. Intraday bias is mildly on the downside for 1.5773 and possibly below. Nonetheless, as long as 1.5621 support holds, we'll treat price actions from 1.6189 as a consolidation pattern and expect another rise through 1.6189. On the upside, above 1.6139 will target 1.6189 high again.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. EUR/AUD also drew strong support from 55 day EMA and rebounded. Current rally from 1.3624 could still extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal. On the downside, sustained break of 1.5621 support should confirm reversal and turn outlook bearish for 1.5153 support and below.

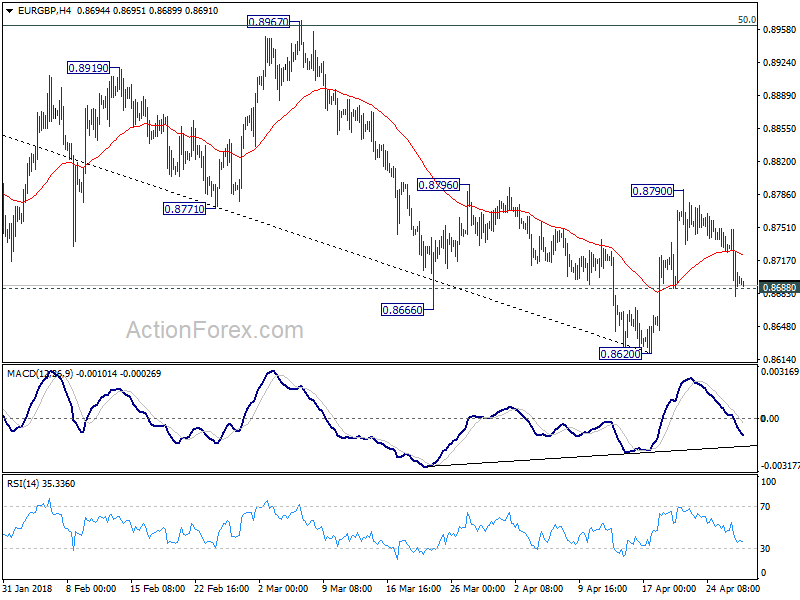

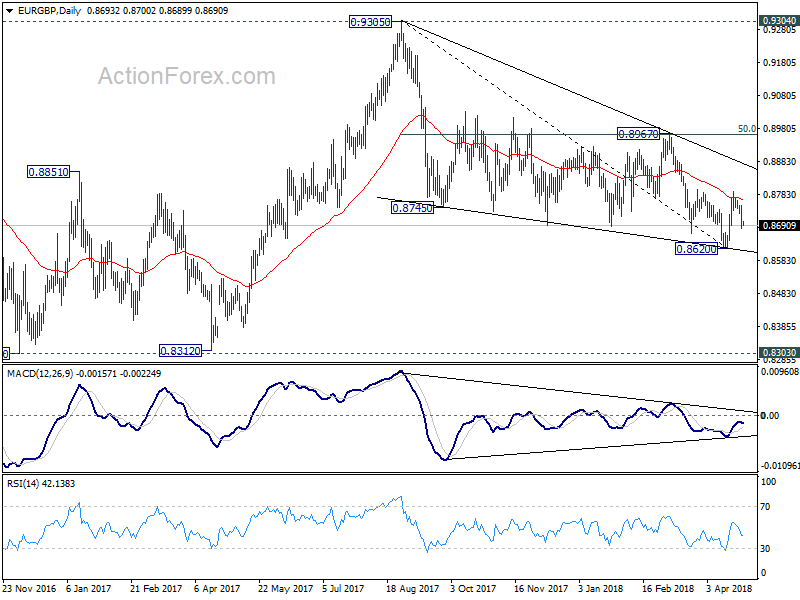

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8669; (P) 0.8709; (R1) 0.8739; More...

Intraday bias in EUR/GBP remains on the downside for the moment. Rebound from 0.8620 should have completed at 0.8790 already. Deeper fall would be seen back to 0.8620 low. As EUR/GBP was rejected by falling 55 day EMA, recent decline is possibly still in progress. Break of 0.8620 will resume the whole fall from 0.9305 and target 0.8303/12 support zone. On the upside, though, above 0.8796 will resume the rebound from 0.8620 instead.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

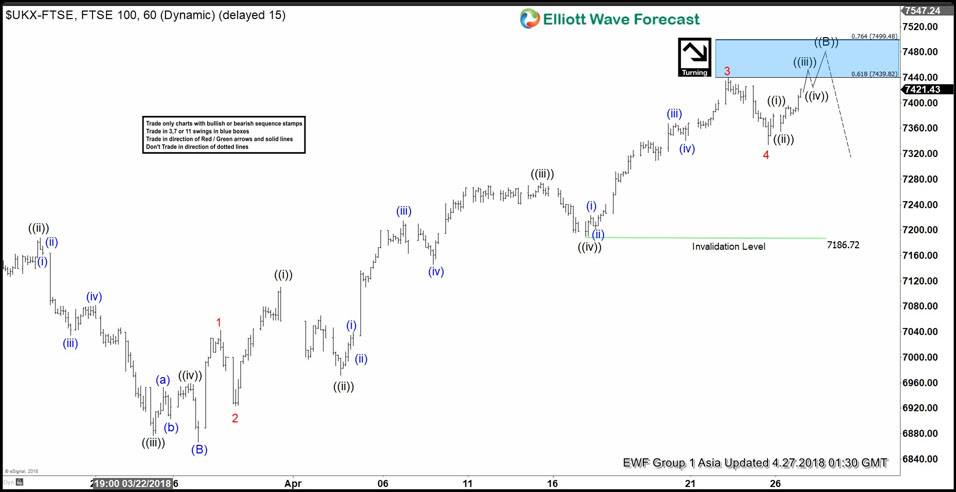

Does Elliott Wave View Suggest A Turn In FTSE Is Imminent?

Short-term Elliott Wave view in FTSE suggest that the decline to 3/26/2018 low 6866.94 ended intermediate wave (B). Above from there, Intermediate wave (C) of ((B)) remains in progress with a strong rally to the upside unfolding as Impulse Elliott Wave structure. The internal distribution of each wave within the rally is unfolding as 5 waves pattern with extension in third wave, thus confirming the impulsive sequence.

Up from 6866.94 low, the index ended Minor wave 1 of (C) ended at 70442.37, Minor wave 2 of (C) ended at 6923.33. From there, Minor wave 3 of (C) unfolded as an Impulse Elliott Wave sequence with extension where Minute wave ((i)) ended at 7109.93, Minute wave ((ii)) ended at 6971.75, Minute wave ((iii)) ended at 7274.99, Minute wave ((iv)) ended at 7190.46 low, and Minute wave ((v)) of 3 ended at 7439.58 high.

Minor wave 4 of (C) pullback appears complete at 7334.64 low and the Index has started Minor wave 5 of (C) looking to extend 1 more leg higher towards 7499.48 – 7575.68 area approximately before ending primary wave ((B)). Afterwards, the index should start the next leg lower or at least do a 3 waves reaction lower as per Elliott wave hedging. We don’t like buying it.

FTSE 1 Hour Elliott Wave Chart

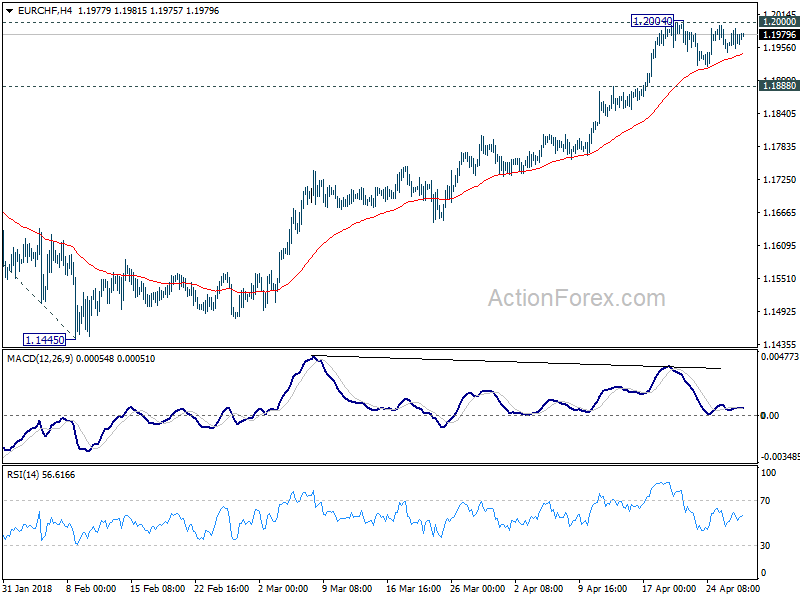

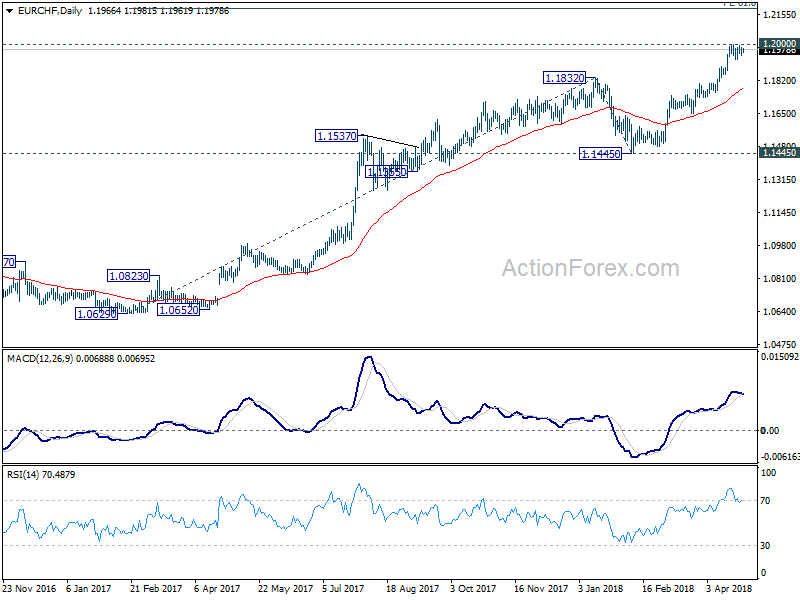

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1950; (P) 1.1970; (R1) 1.1991; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 1.2004 temporary top extends. Further rise is expected, though, as long as 1.1888 minor support holds. On the upside, decisive break of 1.2 will pave the way to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. However, considering bearish divergence condition in 4 hour MACD, break of 1.1888 will indicate short term topping. In that case, deeper pull back would be seen back to 1.1445/1832 support zone.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2003 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next.

ECB Unsurprisingly Gave No New Guidance

Market movers today

In the US, the preliminary Q1 GDP growth est imate is due for release today. There are signs that economic activity slowed in the first quarter, with growth in consumer spending coming out weaker than first expected and the investment indicator not as st rong as previously. The Atlanta Fed suggests GDP growth was 2.0% q/q AR while the NY Fed's GDP indicat or says 2.8%. We believe the former is more likely than the lat ter. However, we remain opt imistic about full-year GDP growth due to the tax package among others and hence we expect the Fed to cont inue its gradual hiking cycle.

In the UK, the first est imate of GDP growth in Q1 will be released. According to indicators, GDP growth slowed in Q1 compared to Q4 17, the quest ion is more by how much. While the PMIs suggest GDP growth is likely to have slowed to 0.3%, the NIESR GDP est imate is as low as 0.2%. We est imate GDP growth was 0.25%, implying an annual growth rate of 1.4% y/y (don't be surprised if it is only 1.3%), which is among t he lowest in t he advanced economies. Looking at real wage growt h and business investment s' int ent ion, it is difficult to see a scenario with much higher GDP growth in the UK this year despite the polit ical agreement on t ransit ion.

In the Scandies, we get Swedish retail sales data, which we expect to be on the weak side, reflect ing very soft sales figures from HUI earlier in the month. Moreover, the monthly household lending numbers are published, which remains upbeat just below 7% y/y but which we expect to moderate going forward amid a slowdown in the housing mark et .

In Norway, we expect the April NAV labour market report to show gross unemployment returning to fall by 1,000 people m/m after Easter distorted last month's release. T his should take the registered unemployment rate down to 2.3%, which would be in line with Norges Bank's project ions in t he March monetary policy report and, in isolat ion, lends support to expectat ions of a rate hike in September.

Selected market news

Yesterday, the Riksbank postponed the scheduled t iming of the first rate hike to Q4 this year. Specifically, the revised rate path suggested a 10bp rate hike in October with an addit ional c.55bp worth of hikes unt il the end of 2019. Overall, the decision was softer than expected by markets, which underpins our bearish SEK FX view. Indeed, even the revised inflation forecast seems too opt imist ic given subdued underlying inflation dynamics and we still do not expect any rate hikes this year. For more informat ion on the Riksbank meeting see our comment here.

The ECB unsurprisingly gave no new guidance at yesterday's meeting. Draghi acknowledged the recent softer data but kept his st rong and broad-based assessment on growth. The meeting confirmed our view that the next step in forward guidance will come in July. Overall pat ience, prudence and persistence remains the guiding ECB principles. See our review here.

This morning, the Bank of Japan (BoJ) kept monetary policy unchanged with an 8-1 vote. Interestingly, the BoJ removed the reference to hit t ing the 2% inflat ion target in the fiscal year 2019 (FY 2019). This is a slight ly dovish twist that should help put an end to exit speculations for some time. The JPY was little changed prior to the press conference (start ing 8:30 CET).