Sample Category Title

Dollar index targeting 91.90 projection level, building up trend reversal

Dollar index surged sharply overnight, thanks to the selloff in EUR/USD. The case of medium term reversal continued to build up after breaking of the trend line resistance as well as 91.01 medium term support turned resistance. Focus is now on 100% projection of 88.25 to 90.93 from 89.22 at 91.90. Decisive break there will add to the case that rise from 88.25 is an impulsive move. And thus, affirm the case of medium term trend reversal. However, rejection from 91.90 could make the rise corrective. For, we're favoring the former case.

There are a couple of events that could help unveil the development including today's Q1 GDP, next week's ISMs and NFP, and certainly treasury yields too.

JPY recovers ahead of BoJ, ignores mixed data

A batch of data is released from Japan today. Tokyo CPI slowed to 0.6% yoy in April, down from 0.8% yoy and missed expected of 0.8% yoy. Industrial production rose 1.2% mom in March, well above expectation of 0.5% mom. Retail sales rose 1.0% yoy in March, below expectation of 1.5% yoy. Unemployment rate was unchanged at 2.5%.

JPY showed little reaction to the set of mixed data and recovers broadly today.

While JPY remains the third weakest for the week, today's recovery can be attributed to the retreat in US yields. 10 year yield closed down -0.034 at 2.990 overnight. back below 3% handle.

BoJ will announce rate decision today and there is no expectation of any changes. Here are some previews:

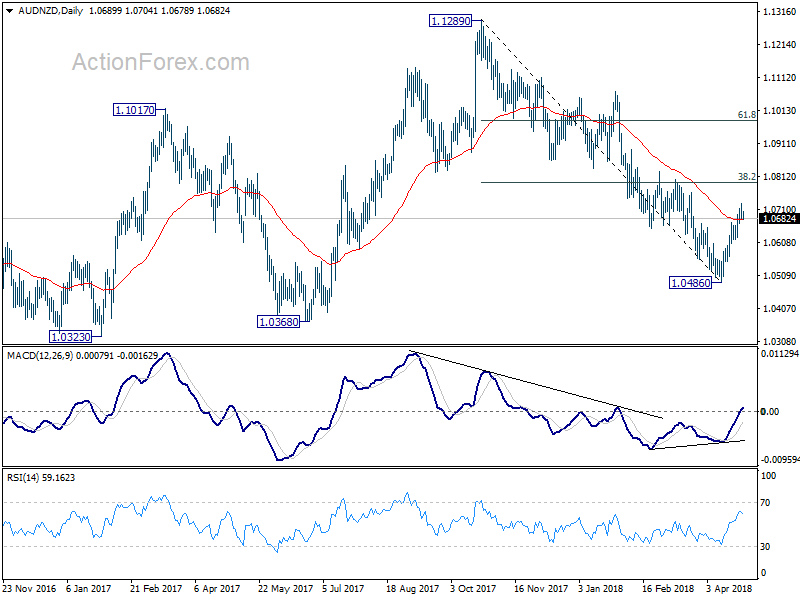

New Zealand recorded first March trade deficit in 10 years

New Zealand trade balance unexpectedly show NZD -86m deficit in April, versus expectation of NZD 200m surplus. That was also the first March deficit 10 years since 2008. Goods exports rose 5.8%, or NZD 265m while imports rose 14%, or NZD 612m.

From Australia, PPI rose 0.5% qoq, 1.7% Yoy in Q1 versus expectation of 0.4% qoq, 1.2% yoy.

NZD and AUD are the weakest major currencies this week, followed by EUR.

Comparing the two, AUD/NZD is in recovery mode since early April. For now, the rise from 1.0486 is seen as a correction and could target 38.2% retracement of 1.1289 to 1.0486 at 1.0793. But we'll start to look for topping signal around there.

The $ Continues To Test The Fringes Of Bullishness

Not to beleaguer the ongoing developments in the US Bond markets, but while ten years US yield count on the Greenbacks measuring tape, the unwinding of the USD geopolitical risk premium goes on and price action suggests we should expect the fringes of significant USD bullish structural levels to get tested.

With that in mind, today is all about pre-positioning for the dual summit of the Koreas headline risk, which should evolve into a market-friendly dynamic for both EM and DM economies.

On the ECB front, separating the wheat from the chaff is alway’s a challenging exercise when it comes to Mario Draghi, but the high bar for dovishness was met and perhaps vaulted as price action suggests

Not surprisingly earnings season continues to dominate the equity landscape as investor revel in the fantastic profit results and confirming a 3 % ten-year yield is of little concern to the markets.

Oil prices continue to rise as investors are waking up to the reality of global demand dynamics suggesting we’re in the midst of shifting from a supply overload to a shortage of crude in the years ahead.Trade wars are on the back burner, and geopolitical risk is unlikely to abate, so the path of least resistance should be higher for the foreseeable future

On the currency market, the song remains the same, and the greenback looks comfortable testing the bullish fringes. The BoJ is unlikely to shift the dial, but caution prevails given the robust economic number.

Gold remains a complete dollar trade but as we near the 1315 attraction zone I suspect buyer will emerge, but the tale of the tap suggest a wait and see approach ahead of tonights GDP print

Dollar Rally Shows Staying Power As ECB Delivers Neutral Comments

The US dollar is higher against major pairs except the JPY who is trading higher awaiting the Bank of Japan (BOJ) monetary policy statement and press conference. The European Central Bank (ECB) was less than forthcoming about its plans earlier today and in his press conference President Mario Draghi made some comments that cancelled each other out by highlighting growth moderation, but mentioning underlying strength in the EU economy. The US dollar continues to advance awaiting the release of the GDP data for the first quarter of 2018.

- US GDP forecasted at 2.0 percent in Q1

- UK GDP forecasted at 0.3 percent in Q1

- US dollar trading at 3.5 month high

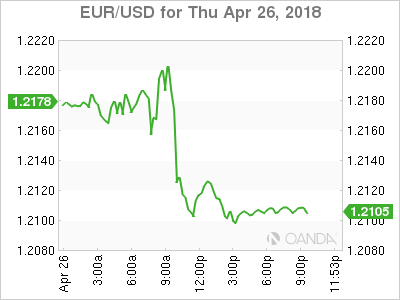

Euro Falls After ECB Cautious Words

The EUR/USD lost 0.46 percent on Thursday. The single currency is trading at 1.2104 after the European Central Bank (ECB) opted to leave its benchmark rate intact and made no announcements regarding the end of the quantitative easing program. ECB President Mario Draghi was neither hawkish nor dovish, which resulted in little support for the euro. The eyes of the market will now be fixed in the June and July meetings for some insights into the plans of the central bank. The euro is now at a monthly low versus the US dollar with the uncoming first estimate of the US gross domestic product (GDP) expected at 2.0 percent. The Bureau of Economic Analysis will release the advance US GDP at 8:30 am EDT.

Consumer spending in the US is thought to have slowed down which explains the lower forecast for the first quarter when the US economy grew by 2.9 percent in the last quarter of 2017. The first quarter has historically been a difficult one for US growth the 2.0 percent target would be a first at that level since 2015. This is only the first of three estimates, but given that it sets the expectations for the other two it is the one that has the most impact. A stronger than forecasted figure could boost the USD higher as the EUR is lacking traction after a non-eventful ECB statement. A weaker than anticipated GDP data point in the US could see the greenback giving some of the gains of this week ahead of next week’s May Federal Open Market Committee (FOMC) meeting.

US companies reported earnings this week with the good results driving stock prices higher in particular the tech sector. US yields continue to flirt with the 3.0 percent line, but this time it is under as the 10 year note fell to 2.990 percent. US unemployment claims fell to 209,000 fell to its lowest level in 48 years with next week’s U.S. non farm payrolls (NFP) to show if there is any impact of strong US employment on wage growth.

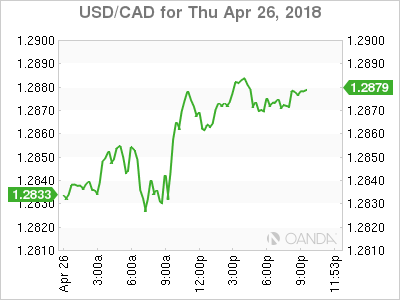

Loonie Caught Between Big Dollar and NAFTA Hopes

The USD/CAD gained 0.34 percent. The currency pair is trading at 1.2881 ahead of the release of US GDP growth for the first quarter. The loonie has traded in a range for the past two days as the positive price of oil pressures and NAFTA optimism have been neutralized by a strong dollar. The Bank of Canada (BoC) kept rates unchanged on April 18, but yesterday BoC governor Stephen Poloz was optimistic when addressing Parliament’s upper house. Poloz expects a rebound as the economy if finally positive, but he also warned about possible headwinds picking up.

Oil prices have helped the Canadian currency as WTI remains above $68 but is no match for the boost that US dollar is getting from upgraded growth expectations that have the U.S. Federal Reserve looking to add another rate hike to the three they had already forecasted for this year. The interest differential between the Canadian benchmark at 1.25 percent and the US Fed funds rate at 1.5–1.75 will only grow as the Bank of Canada (BoC) cannot match the Fed for fear of the impact higher rates could have on record borrowing levels of Canadian households.

Next week will have few opportunities for the CAD from economic releases with the market mostly focused on US employment and the FOMC statement. A NAFTA announcement in the near future could take the loonie from current ranges, but although some progress has been made there is nothing concrete for the market to use when valuing the currency.

Market events to watch this week:

Thursday, April 26

10:00pm JPY BOJ Policy Rate

10:00pm Monetary Policy Statement

Midnight JPY BOJ Outlook Report

Friday, April 27

Tentative JPY BOJ Press Conference

4:30am GBP Prelim GDP q/q

8:30am USD Advance GDP q/q

Eco Data 4/27/18

[php_everywhere instance="1"]

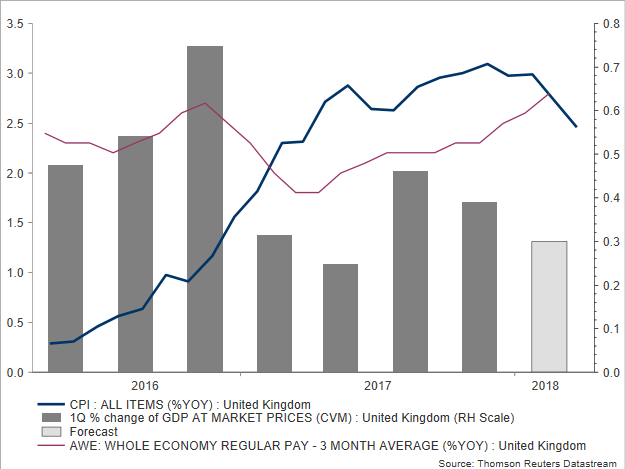

UK Flash GDP Growth to Ease in Q1 2018

Economic growth in the UK might have slowed down in the first quarter of 2018 as the heavy snowfall in February and in March kept consumers indoors, weighing on household spending. While this could be proven temporary later in the second quarter, another data miss this month could further cast doubt on whether a rate hike by the BoE next month is possible.

On Friday at 0830 GMT, the Office for National Statistics is expected to show that the British economy has grown by 0.3% q/q in the first three months of 2018, slightly slower than the 0.4% expansion delivered in the final quarter of 2017 due to the unusually cold weather which led retail sales sharply down by 1.2% m/m in March. Year-on-year, however, GDP growth is anticipated to remain unchanged at 1.4%, at the lowest rate seen since Q3 2013.

Earlier this month, the employment report for the month of February brought some good news to policymakers as average earnings increased more than prices did on a yearly basis, while the unemployment rate declined further, hinting that consumption could pick up steam in the upcoming months, at a time when households struggle to repay their debts.

Moreover, inflation numbers in March eased towards the central bank’s target of 2.0%. While this could come as music to policymakers’ ears, the fact that the above data fell short of expectations, in conjunction with retail sales tumbling along with the Markit Services PMI, caused some stress to the BoE Governor Mark Carney. The BoE chief surprisingly played down market expectations of a rate hike in May, saying that “there are other meetings over the course of this year” for a rate rise to be delivered. Furthermore, he cited Brexit risks as a drag to growth prospects.

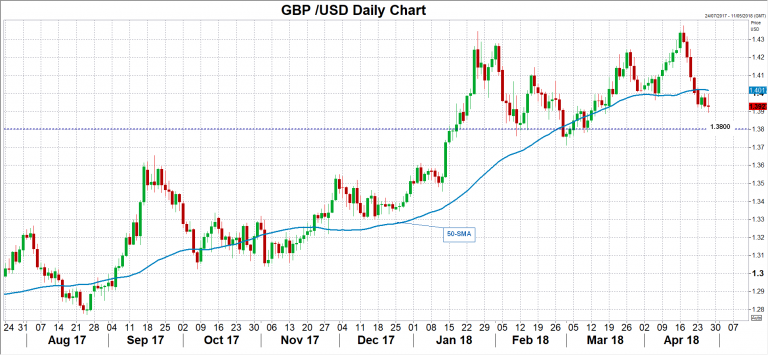

Carney’s comments put in question whether the BoE will finally raise borrowing costs by 25 basis points next month, pushing the odds for this to materialize down to 50% from around 80%. Should Friday’s GDP growth appear weaker than expected, chances for further monetary tightening could drop even lower, driving pound/dollar lower towards the 1.38 key-level. Conversely, an upside surprise could erase today’s losses, leading the pair up to the 50-day SMA, which currently stands at 1.4017.

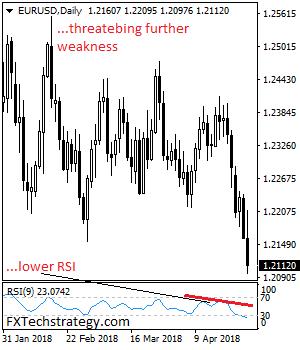

EURUSD: Bearish, Declines Further

EURUSD: The pair resumed its weakness on Wednesday and followed through lower on Thursday. On the upside, resistance comes in at 1.2150 level with a cut through here opening the door for more upside towards the 1.2200 level. Further up, resistance lies at the 1.2250 level where a break will expose the 1.2300 level. Conversely, support lies at the 1.2050 level where a violation will aim at the 1.2000 level. A break of here will aim at the 1.1950 level. Below here will open the door for more weakness towards the 1.1900. All in all, EURUSD faces further downside threats.

Gold’s Downward Spiral Continues

Gold prices continue to head south, as the base metal has recorded losses in five of the past six sessions. In Thursday’s North American trade, the spot price for an ounce of gold is $1317.27, down 0.42% on the day. On the release front, durable goods orders reports were mixed. Core Durable Goods Orders fell to 0.0%, missing the estimate of 0.5%. There was better news from Durable Goods Orders jumped 2.6%, crushing the estimate of 1.6%. Unemployment Claims dropped to 209 thousand, well below the estimate of 230 thousand. On Friday, the US releases Advance GDP and UoM Consumer Sentiment. Traders should be prepared for some movement from gold during the North American session on Friday.

The US dollar continues to shine, and gold has dropped to its lowest level since March 21. Much of the dollar rally can be attributed to rising yields on US bonds, which have hit 4-year highs this week. On Wednesday, 10-year US Treasury notes climbed to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is good news for the US dollar. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. At the same time, investor risk appetite has improved, with an easing of tensions between North and South Korea. A historic meeting between the leaders of the two countries is expected shortly, and there is even talk of a peace treaty being signed between the two countries.

Yen Steady Ahead of BoJ Rate Statement

The Japanese yen has steadied in the Thursday session, after posting six straight losing sessions. In North American trade, USD/JPY is trading at 109.33, down 0.09% on the day. On the release front, durable goods orders reports were mixed. Core Durable Goods Orders fell to 0.0%, missing the estimate of 0.5%. There was better news from Durable Goods Orders jumped 2.6%, crushing the estimate of 1.6%. Unemployment Claims dropped to 209 thousand, well below the estimate of 230 thousand. In Japan, there are a host of key indicators. Tokyo Core CPI is expected to remain unchanged at 0.8%. The Bank of Japan issues a policy statement and Governor Haruhiko Kuroda will host a press conference.

The US dollar continues to climb against its rivals, buoyed by rising yields on US bonds, which have hit 4-year highs. On Wednesday, 10-year US Treasury notes have risen to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is good news for the US dollar. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. The US currency has also benefited from a reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

The Japanese economy continues to expand, but inflation has lagged behind growth and remains well below the Bank of Japan’s target of around 2 percent. The markets have been speculating that stronger economic conditions might cause the BoJ to re-examine its ultra-accommodative monetary policy. However, on Monday, BoJ Governor Haruhiko Kuroda poured cold water over such sentiment, stating that in order to reach its inflation target, “the Bank of Japan must continue very strong accommodative monetary policy for some time”. The BoJ will issue an inflation forecast on Friday, with the bank expected to reiterate that the inflation target will be reached in fiscal year 2019. Kuroda’s dovish statement can be seen as an attempt to curb volatility in the yen following the release of the inflation forecast.