Sample Category Title

EURUSD Hits Multi-Month Low after Draghi; Psychological 1.20 Support Comes in Focus

The Euro spiraled to the lowest levels since Jan 12 after the ECB President Draghi’s press conference today.

Draghi did not say anything significantly different from Central Bank’s last meeting, but market initially took his comments as not dovish as expected and sent Euro to the session high at 1.2209, but gains proved to be short-lived.

Draghi said that underlying inflation remains subdued but expected to pick up and move towards projected levels.

Eurozone growth remains solid, with recent softer than expected indicators require caution but some normalization of growth could be expected.

Regarding bond buying program, which was focused today, Draghi pointed again that ample degree of monetary stimulus is still needed.

With Draghi’s comment being insufficient to produce stronger thrust, the Euro fell lower, also driven by stronger dollar on higher US yields.

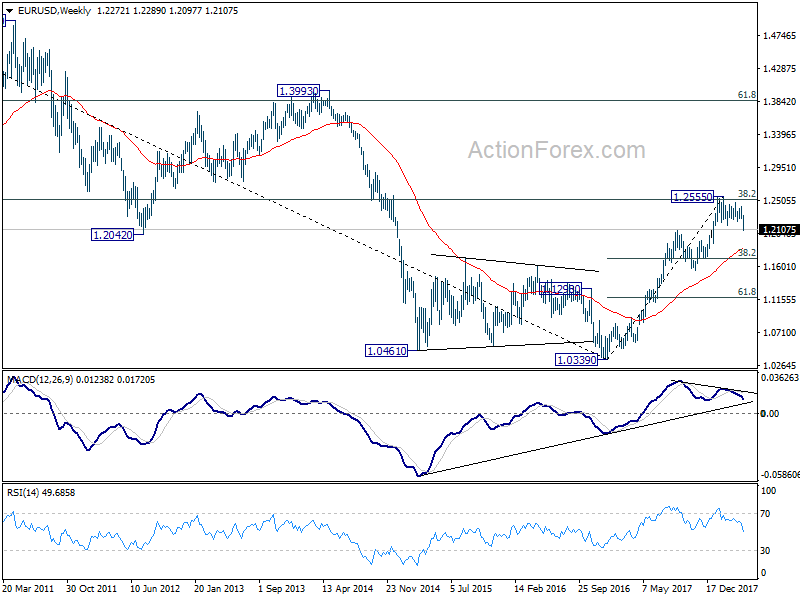

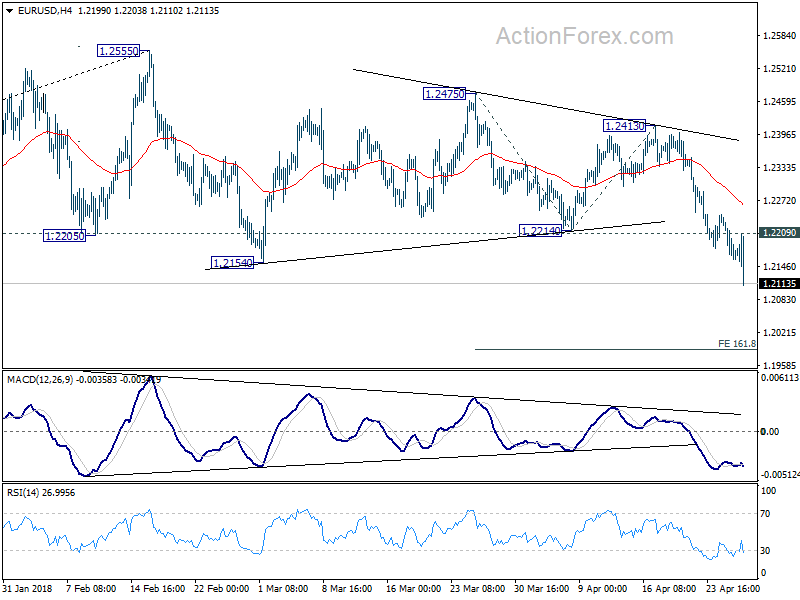

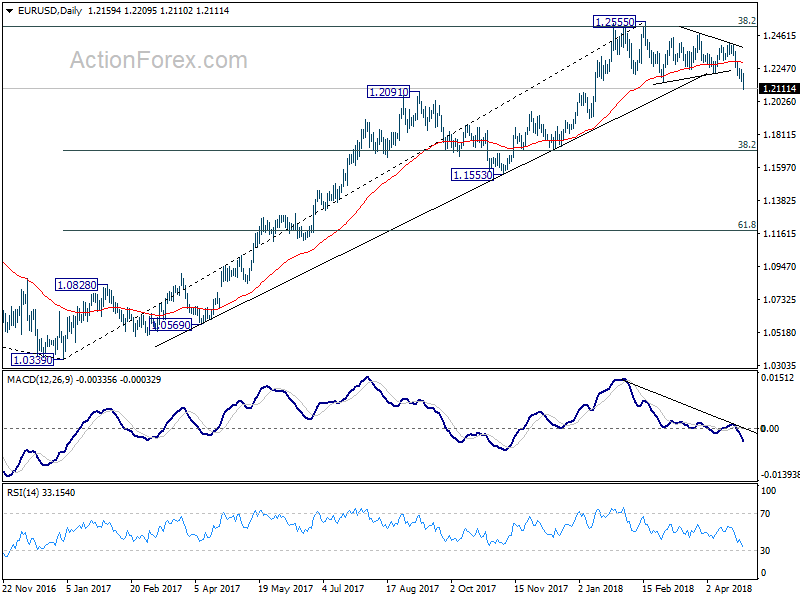

Strong bearish signal is developing on daily chart as fresh weakness probes below the floor of multi-month congestion (1.2150/1.2555), with firm break lower expected to spark fresh acceleration lower, in extension of recent steep descend from 1.2413 (17 Apr high).

If the greenback extends its rally, the Euro could easily fall to strong support at 1.2000 (psychological support / 200SMA).

The pair is on track for another bearish end of the day, as red daily candle with long upper shadow is forming and expected to further weigh on the Euro.

On the other side, oversold techs continue to warn of corrective action, but without any firmer bullish signal seen so far.

Upper pivots lay at 1.2213/35 (broken 100SMA / daily cloud base) and only clear break higher would sideline strong downside risk.

Res: 1.2153; 1.2172; 1.2213; 1.2235

Sup: 1.2092; 1.2054; 1.2000; 1.1936

Euro breaks down after reassessing ECB Draghi, where next?

We've pointed out in the quick comment updates that there was no follow through buying in Euro despite the rebound attempt. That rebound was initially triggered by ECB President Mario Draghi's introductory statement that talked about the "solid and broad-based expansion" despite weaker than expected data. However, there was a lot of cautious tones in the Q&A section of the press conference.

Draghi said the Governing Council didn't even discuss monetary policy "per se" during the meeting. And that's because more time is needed to assess whether the slowdown in Q1 was "temporary or permanent". And Draghi also cautioned that understanding the factors behind the moderation in growth is "essential for informing our next decisions."

That was indeed more cautious than being cautious, as ECB policy makers now look more uncertain than before about the outlook. It should be noted that there will be Q1 GDP data to be released next week on May 2. And by then, ECB and the market would have a clearer idea on how deep the moderation was. Then on May 3 there will be April CPI flash, which will show how well inflation is picking up again.

Even more importantly, ECB's June meeting on June 14 is less than two months away. It rather unsure whether Draghi and his colleagues could have enough assessment on the outlook. That is, barring some strong rebound in data, Draghi could maintain his usual cautious noncommittal tone and stance even after June meeting.

It seems like Euro traders have made up their mind after some thoughts and choose not to sit their long positions through all the uncertainties.

Technically, today's sharp fall should have confirmed the rejection from key fibonacci level of 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be formed at 1.2555 already. The depth of the fall from there depends on the structure, impulsive or corrective. And that, in turn, will depend on incoming Q2 data. But in any case, for medium term, 38.2% retracement of 1.0339 to 1.2555 at 1.1708 is the minium downside target.

US Economic Activity Expected to Ease in Q1; Fed Course Unlikely to be Affected

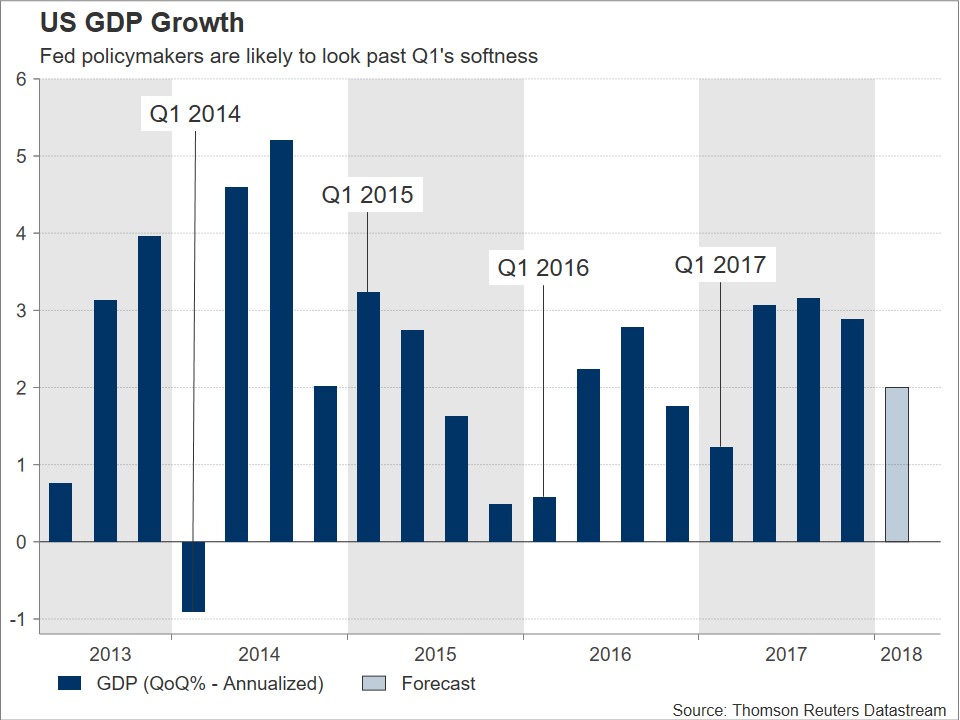

The US will see the release of its advance Q1 2018 GDP growth estimate on Friday at 1230 GMT. Economic activity is projected to have slowed considerably relative to the previous quarter, though the softness is unlikely to trouble Fed policymakers much.

According to analysts’ forecasts, the preliminary GDP growth rate for the first quarter of the year is expected to stand at 2.0% on an annualized basis, significantly below Q4 2017’s respective figure of 2.9%.

The US economy tends to underperform in the beginning of a given year – with the exception of 2015, this can be observed from the chart above as well – and FOMC members are likely to look past first-quarter weakness, focusing on the bigger picture when they gather next week for their two-day monetary policy meeting concluding on May 2.

In terms of the bigger picture, the economy is likely to post stronger growth further ahead on the back of the fiscal stimulus enacted by the Trump administration. April PMI data published on Monday by IHS Markit seem to support the case for stronger expansion in Q2, with Markit’s chief business economist making reference to an economy that is picking up pace at the start of the second quarter. Beyond this though, another factor contributing to FOMC policymakers probably sticking firmly to a path of policy normalization are rising inflation expectations, this also being reflected by the recent jump in Treasury yields. Indicatively, the return on the 10-year Treasury Note rose to its highest since early 2014 on Wednesday, exceeding the widely-touted 3% mark.

In terms of Fed hike expectations, Fed funds futures are projecting that market participants have fully priced in two more percentage-point rate increases by the US central bank, while they currently see a more than 20% chance for a third interest rate hike, something which would bring the total for 2018 to four. For perspective, a few days ago, only one additional hike was fully priced in.

Turning back to tomorrow’s growth figures, the latest forecast of the Atlanta Fed’s GDPNow model puts it at 2.0% on an annualized basis, in line with the previously mentioned GDP estimate, while interestingly, the New York Fed expects it to remain unchanged at 2.9%.

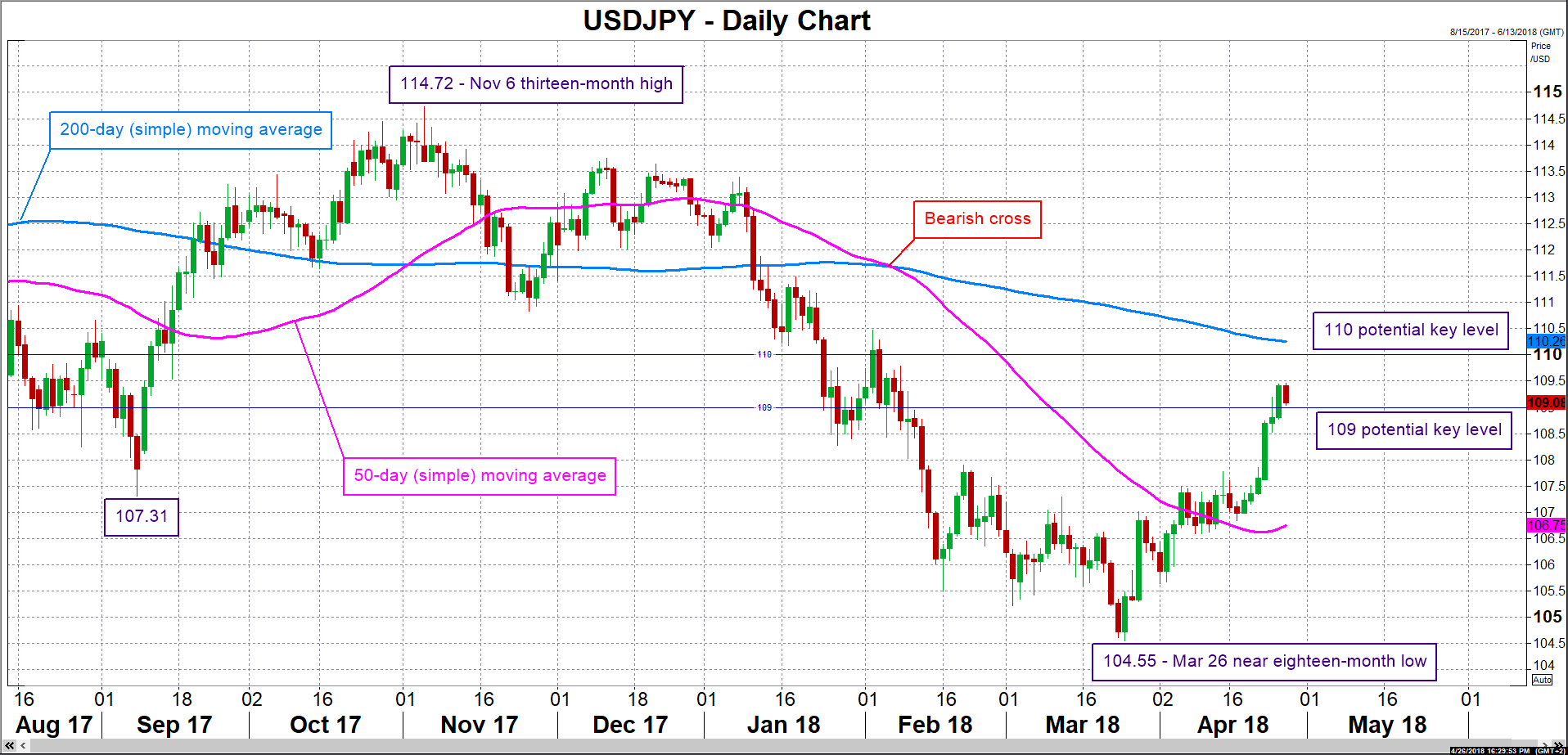

Should an upbeat release be delivered, then such an outcome is likely to spur buying interest for dollar/yen, pushing it to fresh highs; the pair reached a two-and-a-half-month high of 109.46 earlier on Thursday. Resistance to advances might come around the 110 handle which may act as a psychological hurdle. Notice that the current level of the 200-day moving average lies not far above at 110.26. On the downside and in case of weaker-than-anticipated growth numbers, support could be met around the 109 round figure – price action is close to this level at the moment. Further below and if the data disappoint by a large margin, pushing investors to take additional profits after the recent surge in the pair, then the 108 handle would be eyed next.

Other releases that will be made public alongside numbers on the pace of economic activity are Q1 employment costs, as well as the advance estimate of core PCE prices for the same quarter. In terms of reaction in the dollar/yen pair, one should take into account that ahead of the US releases, Japan will also be on receiving end of important data on employment, industrial production and retail sales, while a Bank of Japan decision on monetary policy is due on Friday as well.

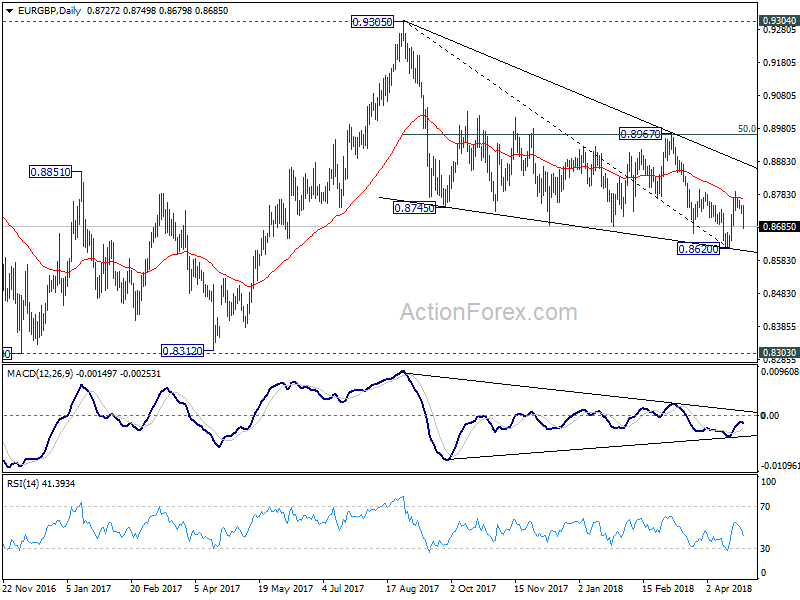

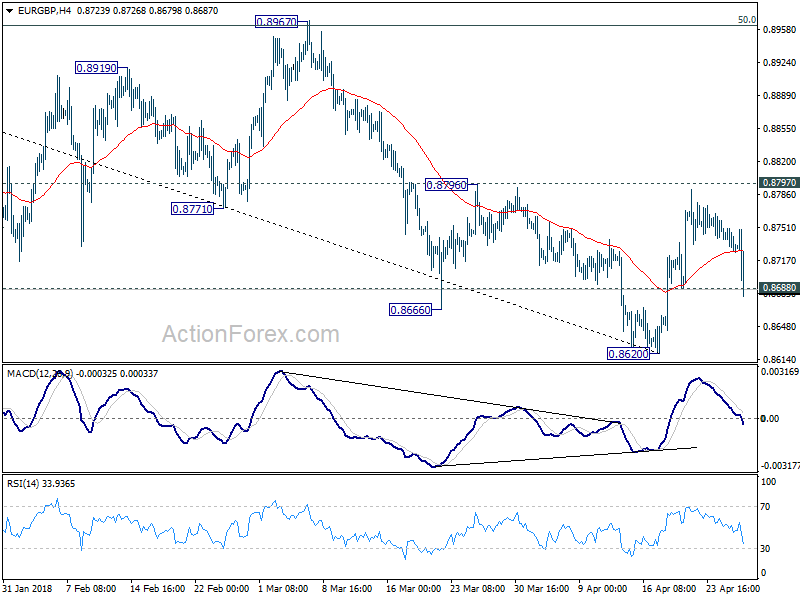

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8722; (P) 0.8736; (R1) 0.8744; More...

EUR/GBP's sharp decline and break of 0.8688 minor support suggests that rebound from 0.8620 has completed at 0.8790 already, ahead of 0.8796 resistance, limited by 55 day EMA. The development also dampens the bullish case of near term reversal. Intraday bias is turned back to the downside for 0.8620 low first. Break there will resumed the whole decline from 0.9305. On the upside, though, above 0.8796 will resume the rebound from 0.8620 instead.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

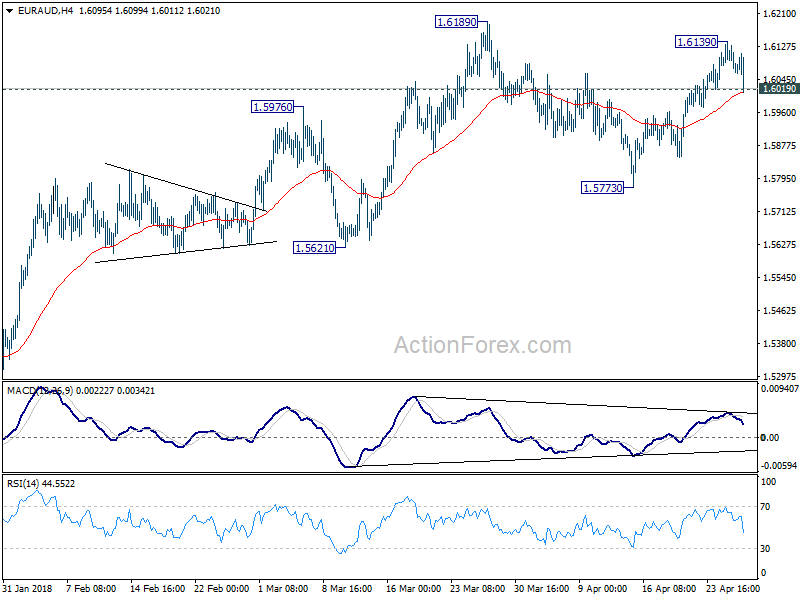

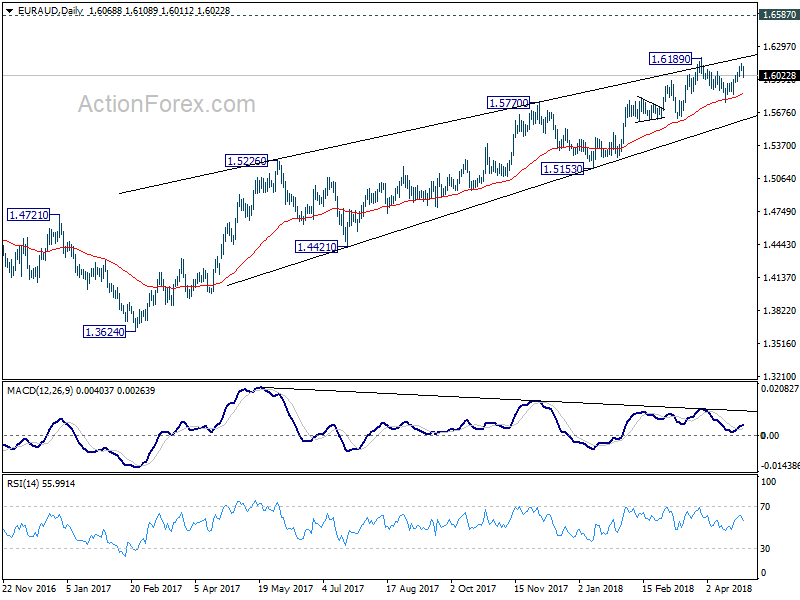

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.6053; (P) 1.6096; (R1) 1.6119; More....

EUR/AUD's break of 1.6019 minor support suggests that rebound from 1.5773 is completed. Intraday bias is turned back to the downside for this support and possibly below. As long as 1.5621 support holds, we'll treat price actions from 1.6189 as a consolidation pattern and expect another rise through 1.6189. On the upside, above 1.6139 will target 1.6189 high again.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. EUR/AUD also drew strong support from 55 day EMA and rebounded. Current rally from 1.3624 could still extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal. On the downside, sustained break of 1.5621 support should confirm reversal and turn outlook bearish for 1.5153 support and below.

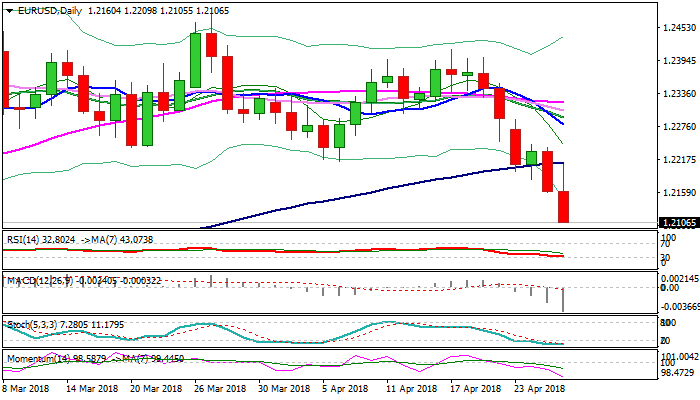

EUR/USD Mid-Day Outlook (Update)

Daily Pivots: (S1) 1.2135; (P) 1.2186 (R1) 1.2213; More....

EUR/USD finally takes out 1.2154 key support level decisively. The development, with downside acceleration should confirm medium term reversal. Intraday bias is back on the downside for 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991 next. ON the upside, break of 1.2209 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current decline and firm break of 1.2154 support should confirm rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

ECB Review: Keep Walking, Nothing to See Here, Keep Walking

- Unsurprisingly, there was no new guidance from Draghi at today's ECB meeting. He acknowledged the recent softer data but kept his strong and broad-based assessment on growth

- The meeting confirms our view that the next step in forward guidance will come in July, as we did not get any new information.

- Both FX and rates markets were broadly range-trading through the press conference, with 10Y Bunds trading within a 1bp range.

Overall, our ECB view has not changed, as today's press conference did not provide new information about the next change in the forward guidance. The introductory statement was on the margin slightly hawkish, as Draghi chose to keep the strong and broad-based growth assessment, while pointing to some moderation of late. Rising protectionism was mentioned as a downside risk.

The GC remains cautious about reading the developments behind the growth moderation. However, despite the acknowledgement of a loss of growth momentum, Draghi tried to downplay the implications, stressing that the ECB has unchanged confidence in the convergence of inflation towards its aim. Although inflation measures have moved sideways without a clear upward trend, Draghi mentioned encouraging signs that wage growth has picked up, which might support price pressures in coming months.

The 10Y Bund traded in a very narrow range through the press conference within a 1bp high/low.

While EUR/USD edged lower to test January lows in the 1.2150 area into the press conference, the overall less soft-than-hoped-for tone from Draghi on growth sent the cross back towards the 1.22 mark yet again. With the ECB eager not to steer any new EUR direction amid cyclical weakness and trade uncertainty, we continue to stress that EUR/USD remains at risk from stretched positioning and US cyclical outperformance on growth and rates alike. These USD positives could put the 2017 high of 1.2092 at risk in coming months and we still see the pair as a tactical sell on rallies short term. That said, we remain strategically long the cross via options for a move towards the high 1.20s in 6-12M.

To sum up; overall patience, prudence and persistence will remain the guiding principles of the ECB.

Sunset Market Commentary

Markets:

The ECB kept its monetary policy and forward guidance as expected unchanged. The tone of Draghi’s press conference reflected recent comments made in a speech. The central bank admits that recent data point to some moderation, coming off exceptionally high levels. Data remain consistent with a solid and broad-based expansion, but there are more prominent risks coming from global factors. The ECB now builds in some caution in reading recent developments tempered by an unchanged confidence that inflation will converge to the central bank’s 2% inflation aim over the medium term. That’s why the council didn’t discuss the monetary policy stance today. The ECB wants to know if the current setback is temporary or permanent and if potential output growth increased or not. Prudence, patience and persistence remain the key words. Headline inflation is expected around 1.5% for the rest of the year while the ECB sees some encouraging signs from wage growth. Finally, president Draghi stepped up his usual rhetoric for implementing structural reforms. Overall, today’s ECB meeting didn’t contain much new info. The fact that monetary policy wasn’t discussed might imply that changes to the forward guidance could only occur in July rather than in June.

The rise of core/US yields and of the dollar took a breather this morning as markets looked forward to the ECB’s policy decision. The ECB as expected left its policy unchanged. Markets apparently feared a soft assessment from president Draghi. EUR/USD tested the 1.2155 range bottom while European/US yields declined before the start of the press conference. ECB president Draghi gave a balanced assessment on recent developments with respect to growth and inflation. In the end, he brought little new for markets. Core US and German yields declined in a daily basis, but this was probably a repositioning/correction on the recent rise in global interest rates, rather than a reaction to Draghi. The US yield curve bull flattens with yields declining by 1 bp (2-y) to 3.5 bps (10-y). The European yield curve shows a similar pattern with yields easing between 0.5 bps and 2 bps (30-y). EUR/USD rebounded off the 1.2155 support and trades again in the high 1.21 area. Draghi was not soft enough to trigger a sustained break of EUR/USD below 1.2155. Some ST moderation in the recent USD rally was maybe also (slightly) at work. USD/JPY hovers in the low 109 area. The upcoming US data rather the ECB assessment will probably decide on the next move on core yields and the dollar.

Sterling succeeded a cautious rebound against the euro over the previous days, reversing part of the sterling losses that occurred after BoE Carney questioned a May rate hike last week. At the same time, the UK currency lost ground against a strong dollar. Sterling sentiment improved further today. We didn’t see any important news. UK eco data were second tier and close to expectations. Regarding Brexit, the debate on the customs union continues. EU negotiator Barnier again opposed the idea that the UK might get a tailor-made solution. Sterling still succeeded a constructive intraday performance though. EUR/GBP trades in the 0.8715 area. Cable rebounded off the 1.39 area and trades again in the 1.3985 area.

News Headlines:

The Riksbank, Sweden’s central bank, kept its main (repo-)rate unchanged at -0.50%, saying underlying inflation has been unexpectedly low recently. Due to inflation uncertainty, it postponed its guidance on the first rate hike until the end of the year. The Swedish krona weakened and is testing the cyclical 10.48 top in EUR/SEK.

EURUSD breaks 1.2154 as Euro gives up

It looks like Euro bulls are finally giving up. We're unsure of the reason yet. But the selling has a lot of intensity.

EUR/USD powers through 1.2154 key support level. That's an important indicate of medium term trend reversal. For the near term, 161.8% projection of 1.2475 to 1.2214 from 1.1991 in the next target.

EUR/GBP's break of 0.8688 also indicates that rebound from 0.8620 has completed. And deeper fall should be seen back to this support level.

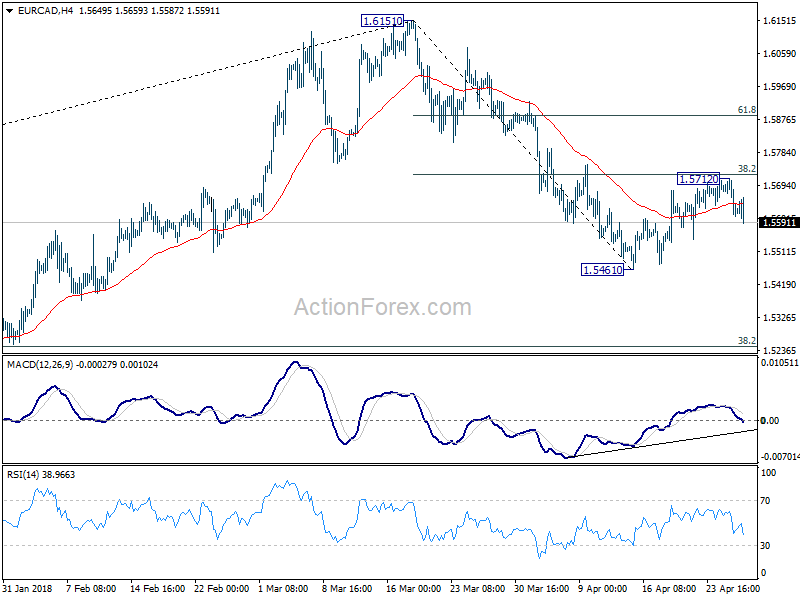

EUR/CAD's rebound from 1.5461 should also be completed at 1.5712, ahead of 38.2% retracement of 1.6151 to 1.5461. Deeper fall would be seen back to retest 1.5461 first.

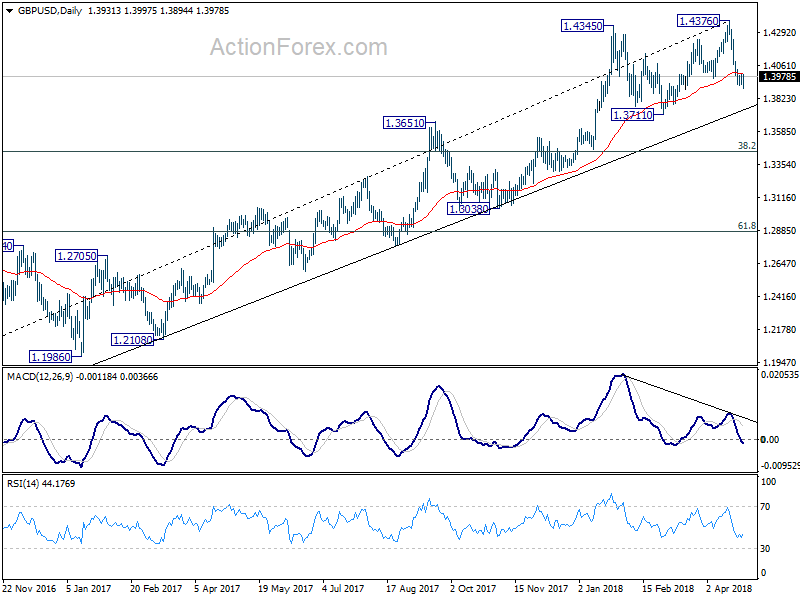

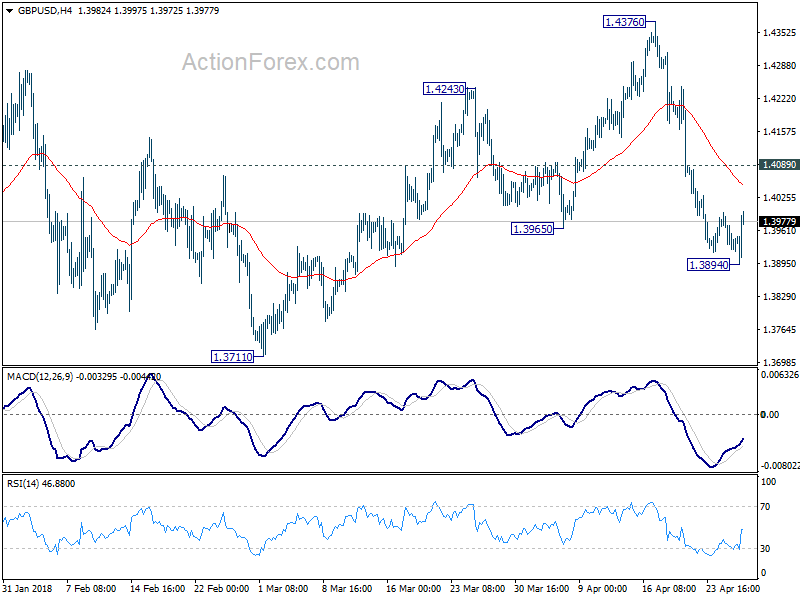

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3899; (P) 1.3965; (R1) 1.4004; More...

Despite dipping to 1.3894, GBP/USD quickly recovered with 4 hour MACD staying above signal line. Intraday bias remains neutral for more consolidative trading. Upside of recovery should be limited by 1.4089 minor resistance to bring fall resumption. Below 1.3894 will target 1.3711 key support next. However, firm break of 1.4089 will turn focus back to 1.4376 high instead.

In the bigger picture, bearish divergence condition in daily MACD is raising the chance of medium term reversal. Also, note that GBP/USD has just failed to sustain above 55 month EMA (now at 1.4257). Focus is back on 1.3711 support. Firm break there will confirm medium term reversal and target 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. For now, sustained break of 55 month EMA is needed to confirm medium term upside momentum. Otherwise, we won't turn bullish even in case of strong rebound.