Sample Category Title

(ECB) Monetary Policy Decisions

At today's meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

Regarding non-standard monetary policy measures, the Governing Council confirms that the net asset purchases, at the current monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem will reinvest the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

Euro Pares Losses ahead of ECB Rate Decision

Here are the latest developments in global markets:

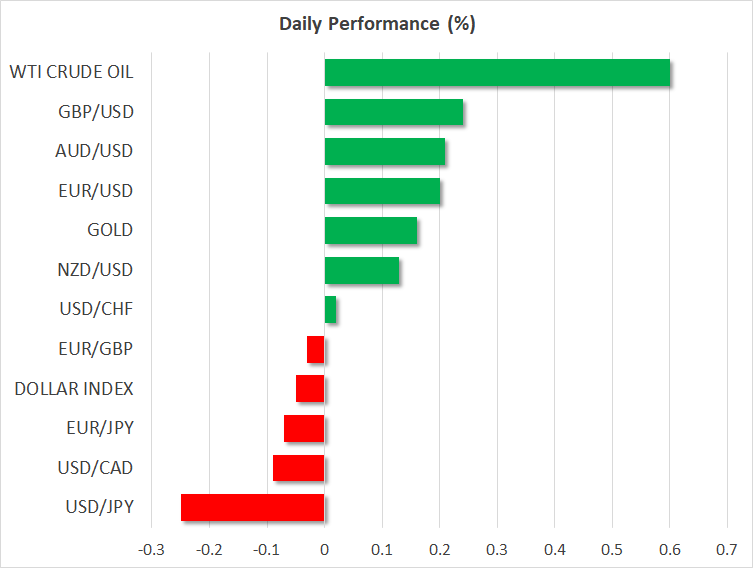

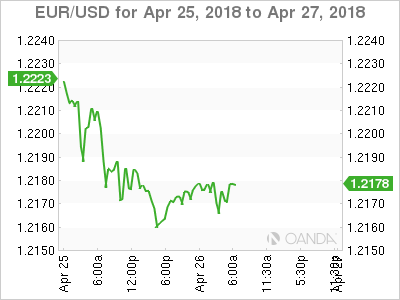

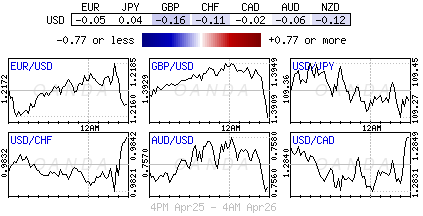

FOREX: The dollar index continued to trade near 3 ½ -month highs reached yesterday in the early European session on Thursday as the 10-year Treasury yields remained above 3.0% for the first time in four-years, last seen at 3.02%. Dollar/yen retained strength above the 109 key-level, with easing geopolitical and trade tensions supporting the pair as well but was slightly down on the day at 109.28 (-0.12%). Euro/dollar, posted limited gains ahead of the ECB rate decision later today, hovering at 1.2172 (+0.12%) as the rise in US treasury yields widened further the gap between US-German government bond yields. Investors were also scaling back long positions on the pair lately in expectations that the ECB would gradually move towards the end of its stimulus reduction program. Meanwhile, in Sweden, the central bank kept interest rates unchanged, saying that rates could rise towards the end of the year, later than previously thought due to a subdued inflation. In the wake of the news, dollar/krona rallied to 8.61 (+0.24%) the highest since the end of June, while euro/krona crawled up to a fresh 8-year high of 10.48 (+0.33%). Pound/dollar touched one-month lows at 1.3894 before a rebound towards 1.3943 (+0.09%) as traders remained cautious on whether the BoE will deliver a rate hike in May following dovish comments by the BoE governor earlier this month. Developments on the Brexit front were also not so bright either, with the House of Lords voting against the Brexit withdrawal bill which aims to leave the UK outside of the EU’s customs union. The antipodean currencies were trading flat, with aussie/dollar and kiwi/dollar fluctuating around 0.7575 and 0.7067. Dollar/loonie was also moving sideways around 1.2839.

STOCKS: European stocks were recovering from yesterday’s downfalls helped by encouraging corporate earnings results. At 0830 GMT, the pan-European STOXX 600 and the blue-chip Euro 50 were up by 0.27% and 0.24% respectively led by industrials, utilities, and consumer cyclicals. The German DAX 30 rose by 0.17%, the French CAC 40 climbed by 0.42%, the Italian FTSE MIB jumped by 0.56%, while UK’s FTSE 100 was flat. In Asia, stocks closed mixed, while futures tracking US stock indices were flashing red, pointing to a negative open. In corporate news, Phillips lighting, the world’s largest lighting maker, reported disappointing earnings numbers for the first quarter of 2018, with its shares tumbling by 12.6%. Deutsche Bank also saw its shares falling after its net profit declined by 79% y/y in Q1 2018, announcing its plans to reduce bond and equity trading in the US and Asia. Oil companies such as the Finish oil refining firm Neste and France’s Total were among gainers, with both companies recording an upbeat performance in the first three months of 2018.

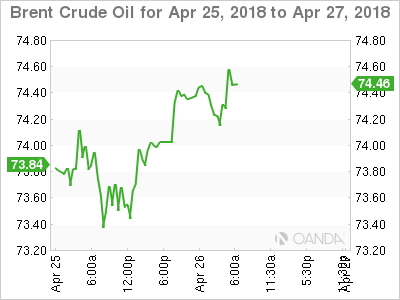

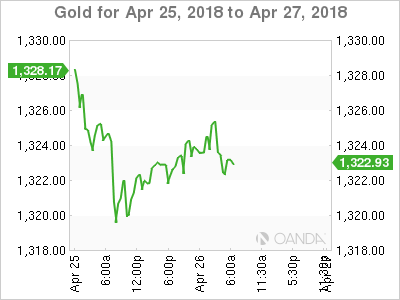

COMMODITIES: Oil prices were heading to the upside on the back of a declining output in Venezuela and growing concerns that the US would re-impose sanctions to Iran. Yesterday, the French President Emanuel Macron, who spend three days in the US to persuade the US President to remain on the 2015 nuclear deal, expressed that the US President would likely leave the deal. WTI crude and Brent rose to $68.45 (+0.59%) and $74.48 (+0.78%) per barrel respectively. In precious metals, gold reversed earlier gains, returning to $1,322.30 per ounce.

Day Ahead: ECB rate decision under the microscope; US durable goods & initial jobless claims coming up

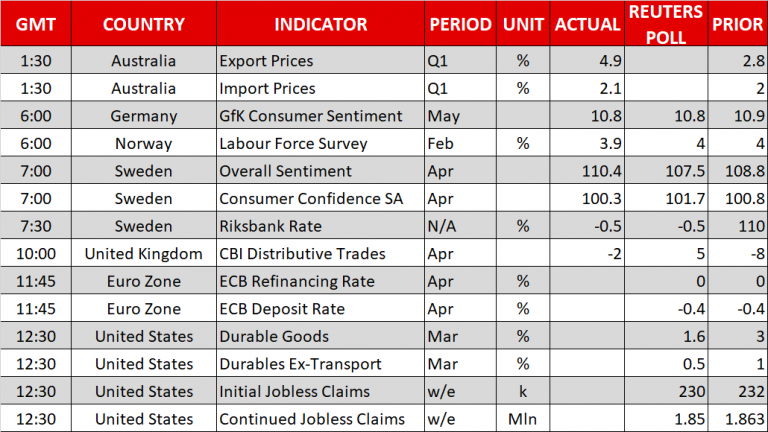

All eyes will be on the European Central Bank today. Although no change is expected to monetary policy, traders will be eager to hear whether policymakers feel more confident to end the quantitative program at the end of the year. Still, some analysts believe that the ECB Governor, Mario Draghi who will hold a press conference at 1230 GMT following the rate announcement at 1145 GMT, will probably avoid any comments that could signal adjustments on the current monetary strategy, though, he might acknowledge the weakness in the Eurozone’s economic performance mirrored by the latest disappointing figures. June’s meeting, which will be accompanied by new economic projections might attract a greater attention.

Turning to the US, durable goods for March are scheduled for release at 1230 GMT. Headline orders are expected to ease to +1.6% m/m from +3.0% m/m in the preceding month, whilst the core durable orders (excluding transportation) are forecasted to tick lower to 0.5% m/m from 1.0% m/m in the previous month. Initial jobless claims due at the same time will be in focus as well. The number of people applying for unemployment benefits for the first time is anticipated to edge down to 230k in the week ending April 20 compared to 232k in the preceding week.

Elsewhere, New Zealand will see the release of trade stats at 2245 GMT, while in Japan, employment figures and initial estimates on industrial production for the month of March as well as April’s CPI numbers will attract attention.

Euro Steady As Markets Eye ECB Rate Statement

EUR/USD has posted slight gains in the Thursday session. Currently, the pair is trading at 1.2175, up 0.12% on the day. On the release front, German GfK Consumer Confidence edged down to 10.8, close to the estimate of 10.9 points. Later in the day, the ECB releases a rate statement, with ECB President Mario Draghi following up with a press conference.

All eyes are on the ECB, which will announce its most recent monetary policy decision on Thursday. Eurozone indicators have softened in recent weeks, raising concerns that ECB President Mario Draghi could sound dovish about the eurozone economy. This could weigh on the euro. At the March meeting, policymakers made a minor move and dropped a pledge to increase stimulus if needed. Will we see additional ‘baby’ steps at the April meeting? The ECB has said it intends to continue bond purchases until at least September and will maintain interest rates at current levels until “well past” the end of the program. Traders shouldn’t expect any dramatic moves at the policy meeting, as the bank will likely continue to preach patience and prudence.

The euro has lost close to 1% this week, as the US dollar has flexed its muscles against its rivals. Much of the credit for the dollar rally goes to rising yields on US bonds, which have hit 4-year highs this week. On Wednesday, 10-year US Treasury notes climbed to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is good news for the US dollar. Another factor helping the US dollar has been a recent reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

GBPUSD Volatile Ahead Of GDP Report

The British pound continues to trade towards the lower bounds of its recent trading range against the U.S dollar, ahead of Friday’s key UK Q1 GDP report. The GBPUSD pair currently trades around the 1.3930 level, after earlier moving to a fresh weekly price-low, at 1.3894. Sterling traders are likely to react to the U.S Durable Goods Orders data release, and pay close attention to the ECB meeting later today.

The GBPUSD pair holds a medium-term bearish bias while trading below the 1.3992 level, key support is found at the 1.3917 and 1.3880 regions.

If the GBPUSD pair trades back above the 1.3992 level, buyers may be encouraged to test towards the 1.4046 and 1.4100 resistance areas.

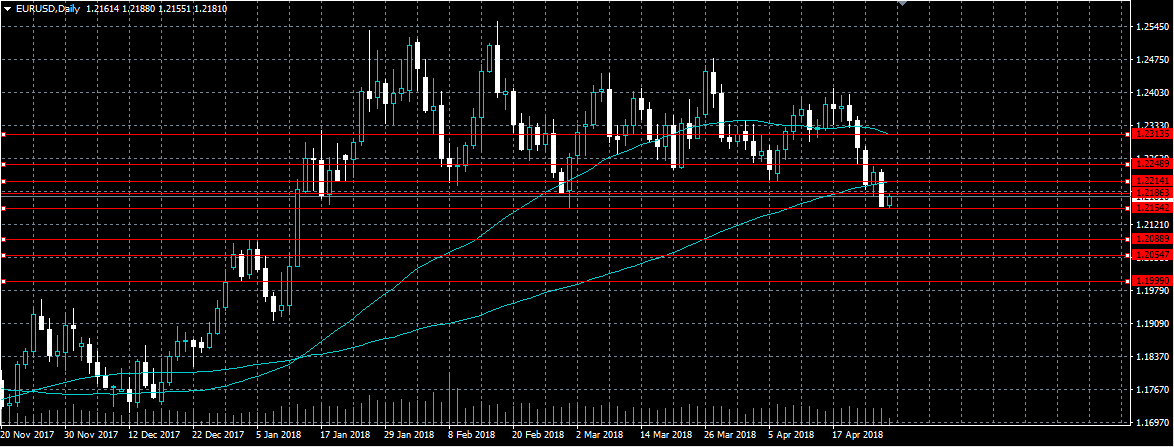

Key Euro Levels To Watch Ahead Of The ECB

The euro currency remains under pressure against the U.S dollar, heading into today’s key European Central Bank Policy Meeting. The EURUSD currently trades around the 1.2190 level, with bearish pressure building while price-action trades below the pairs 100-day moving average, found at the 1.2214 level. To the downside, a breach of the 1.2154 level may expose further losses towards 1.2088, while a clear move above the 1.2214 level may provide bulls the momentum to target the pairs 50-day moving average, at 1.2313.

The EURUSD pair is likely to sell-off sharply once below the key 1.2154 level, key support is then located at the 1.2088 and 1.2054 levels.

If the EURUSD pair starts to trade back above the 1.2214 level, buyers may test towards the 1.2248 and 1.2313 levels.

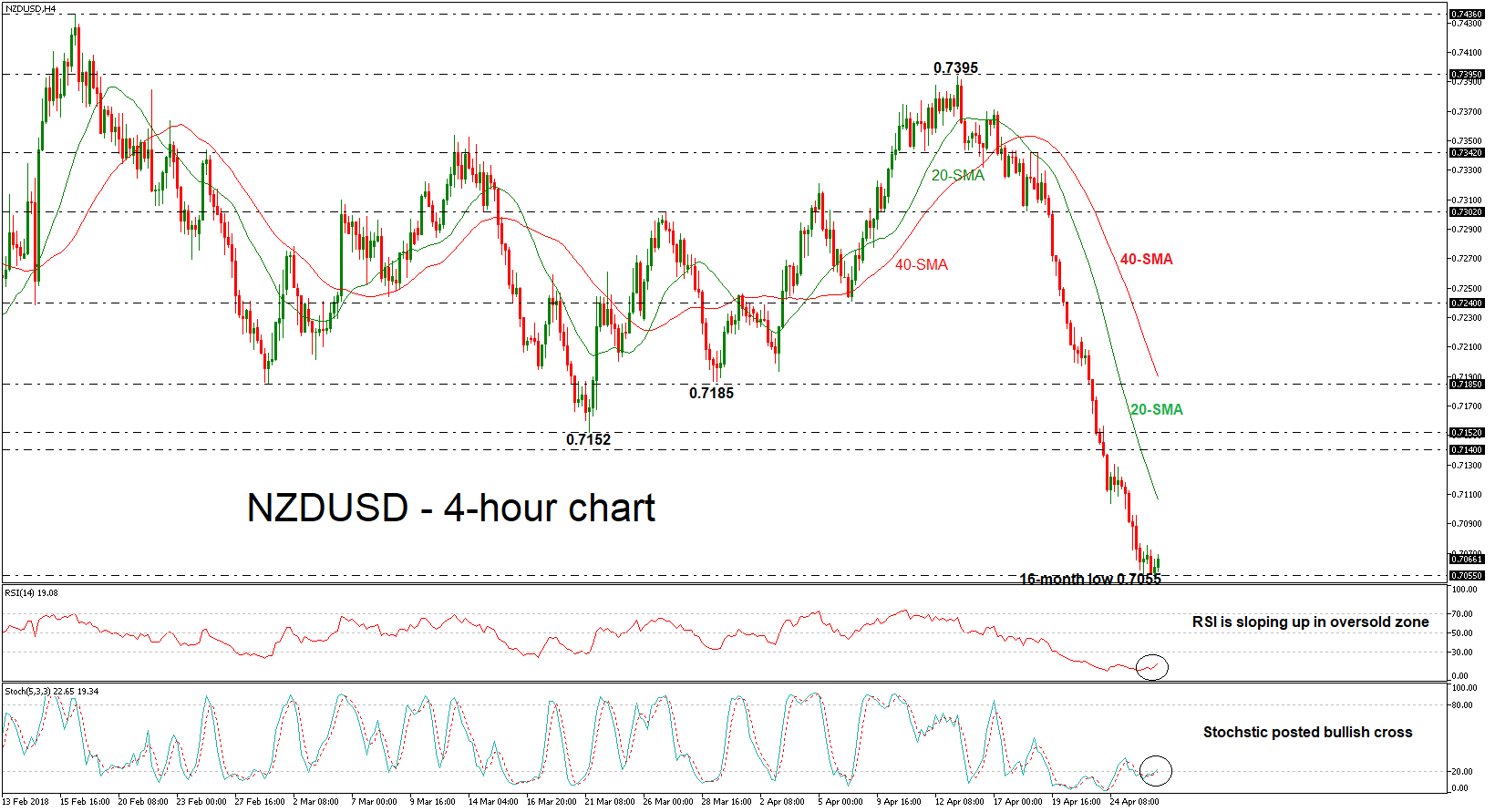

NZDUSD Erases Some Losses, Possibility Of Retracement In Near Term

NZDUSD has come under renewed selling pressure, completing a new 4-month low of 0.7055 earlier today. The pair has been plunging over the last seven trading days, losing more than 300 pips. Furthermore, the price slipped below the significant level of 0.7140, signaling a strong bearish sell-off.

Looking at momentum oscillators on the 4-hour chart, they suggest a possible retracement of the last aggressive downward movement. The RSI indicator is sloping upwards in the oversold zone, while the %K line of the stochastic oscillator posted a bullish crossover with the %D line in the negative territory.

In case of a potential upward pullback, the price could meet the 20-simple moving average around the 0.7100 psychological level in the short-term. A successful surpass of this barrier could open the door towards the 0.7140 – 0.7152 critical area.

On the flip side, if the bears retake control, price declines may stall initially near the 0.7030 support level, taken from the high on December 15 of 2017. If the market fails to hold above this level, the next stop could be at the 0.6950 hurdle identified by the low on December 20 of 2017.

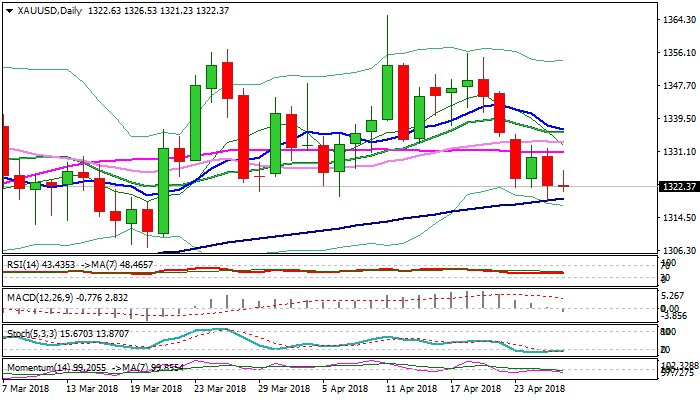

Spot Gold – Bearish Bias Under Daily Cloud

Gold remains at the back foot on Thursday as recovery attempts following previous day’s fall were limited and capped by daily cloud base ($1325) and subsequent weakness shifts near-term focus lower.

Bearish bias remains intact and showing scope for retest of rising 100SMA ($1319) which contained Wednesday’s attack.

Fresh strength of US dollar keeps gold under pressure for extension of bear-leg from $1355 (18 Apr lower top).

Firm break through 100SMA would open way towards very strong support at $1307 higher base (also floor of broader $1307/$1365 congestion), break of which is needed to generate stronger reversal signal.

Bearish setup of daily techs is boosted by freshly formed daily Tenkan-sen/Kijun-sen bear-cross), while the upside remains well protected by daily cloud ($1325/34) and a cluster of daily MA’s between $1331 and $1336, which are expected to maintain bearish bias while capping recovery attempts.

Res: 1326, 1331, 1334, 1336

Sup: 1321, 1319, 1317, 1310

Focus On Draghi – ECB To Be Positive

Thursday April 26: Five things the markets are talking about

Global equities traded mixed overnight, as the market digested the latest flood of company earnings ahead of the ECB monetary policy announcement (07:45 am EDT).

The ‘big’ dollar is steady, trading atop of its three-month highs. U.S Treasury prices have found a small foothold, while oil prices gained on the possibility that President Trump will withdraw from the Iran nuclear deal, casting a cloud over Middle East geopolitics.

At today’s ECB meeting, investors will be watching for any clues that Euro policy makers are preparing a shift in stimulus plans for their June meeting. Stateside, earnings season continues.

On Friday, the Bank of Japan (BoJ) announces its latest policy decision and releases updated economic projections, while in the U.S the market will be focusing on Q1 GDP data.

Elsewhere, in Asia, the leaders of North and South Korea meet on Friday.

1. Stocks mixed results

In Japan, the Nikkei share average rallied overnight, supported by tech shares, with index heavyweight Tokyo Electron jumping after it forecast strong profits for this fiscal year. The Nikkei ended +0.5%, while the broader Topix added +0.3%.

Down-under, Aussie shares ended slightly lower, as a decline in financial stocks, weighed by a fall in AUD (A$0.7567) and mortgage concerns, offset gains in healthcare. The S&P/ASX 200 index fell -0.2%. In S. Korea, the Kospi climbed +1.3%, with tech shares buoyed by news of a record quarterly profit from Samsung.

In China and Hong Kong stocks plummeted overnight, as tech shares came under pressure amid the U.S Huawei probe. The CSI300 index fell -1.9%, while the Shanghai Composite Index slipped -1.4%. In Hong Kong, the Hang Seng index dropped -0.7%, while the Hong Kong China Enterprises Index lost -0.6%.

In Europe, regional bourses trade mostly higher. The DAX trades little changed, with Deutsche Bank recovering from earlier losses after missing estimates. The market awaits a slew of corporate earnings.

U.S stocks are set to open in the ‘red’ (-0.1%).

Indices: Stoxx600 +0.2% at 380.8, FTSE flat at 7378, DAX -0.1% at 12406, CAC-40 +0.3% at 5428, IBEX-35 +0.3% at 9891, FTSE MIB +0.3% at 23884, SMI +0.4% at 8776, S&P 500 Futures -0.1%

2. Oil prices rise on Iran sanctions worries, gold prices unchanged

Oil prices are rallying ahead of the U.S open, supported by expectations that the U.S will re-impose sanctions against Iran, a decline in output in Venezuela and ongoing strong global demand.

Brent crude oil futures are at +$74.27 per barrel, up +27c, or +0.4%, from Wednesday’s close. U.S West Texas Intermediate (WTI) crude futures are up +14c, or +0.2%, at +$68.19 per barrel.

Dealers expect that the U.S will in May re-impose sanctions against Iran, who is a major oil producer and member of the OPEC.

Also aiding prices is French President Macron stating that he expected the U.S President to pull out of a deal with Iran reached in 2015, in which Iran suspended its nuclear program in return for the west to lift their crippling sanctions.

Note: Trump is expected to decide by May 12 whether to restore U.S sanctions on Iran.

Also supporting prices is global demand and the declining output in Venezuela, OPEC’s biggest producer in S. America.

Gold prices stuck to a narrow range overnight, trading atop yesterday’s five-week low print, pressured by a stronger U.S dollar and a rise in Treasury yields. Spot gold is up +0.1% at +$1,324.61 per ounce, a day after it fell to +$1,318.51, its lowest since March 21. U.S gold futures have rallied +0.3% to +$1,326.2 an ounce.

3. Riksbank and ECB monetary policy decisions

Swedish government bond yields are stable after the Riksbank left its repo rate unchanged earlier this morning at -0.50%, in line with market expectations.

The two-year bond yield trades at -0.49%, while the 10-year bond yield trades at +0.77%, same as before the rate decision.

In their statement, the Riksbank indicated that a rate increase is not expected until toward the end of the year, while government bond redemptions and coupon payments will be reinvested in the bond portfolio until further notice.

At today’s ECB press conference announcement (08:30 am EDT), President Draghi is expected to keep a positive tone despite the recent setback of some economic indicators. The combination of growth and inflation comments might signal rising awareness in favour of policy “normalization”. The consensus sees the probability of a ‘dovish’ surprise as “rather low,” while a “neutral” meeting should not obstruct a continued rise in bond yields.

The yield on U.S 10’s decreased -2 bps to +3.01%, the first retreat in more than a week and the biggest tumble in more than two weeks. In Germany, the 10-year Bund yield declined -2 bps to +0.62%, the largest decrease in more than a week, while in the U.K, the 10-year Gilt yield decreased -1 bps to +1.525%.

4. Market focus on ECB and EUR

The market consensus believe that unless ECB President Draghi puts a lot of emphasis on downside risks to the eurozone economic outlook this morning, justifying “a further dovish re-pricing of ECB policy expectations,” the EUR (€1.2170) has a chance to benefit. Despite the recent slowdown in E.U growth and inflation it’s going to be rather difficult to see a dovish Draghi in his press conference. The EUR/USD at the moment is finding it difficult to hold onto gains in the overnight session.

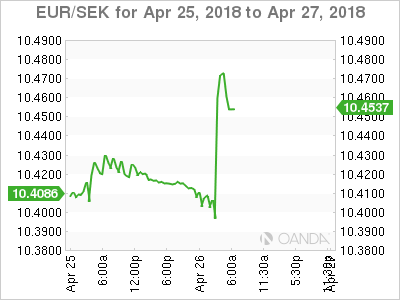

EUR/SEK (€10.4614) has moved higher after the Riksbank pushed slightly back its first potential rate hike from the beginning of H2 until the latter part of 2018.

5. German consumer sentiment set to weaken

Data this morning from the German market research group GfK showed that geopolitical issues and growing protectionism are souring German consumers’ mood.

GfK’s forward-looking consumer confidence index is set to drop to 10.8 points in May from 10.9 poiSnts in April, it said. The decrease is in line with a market forecast.

“The escalation of the Syrian crisis and the protectionist trade policies of the U.S are worrying consumers and could now also affect Germany’s previously excellent economic prospects,” GfK said.

Digging deeper, GfK noted that consumers’ economic optimism suffered a setback in April, falling to 37.4 points from 45.9 points in March, hit by geopolitical concerns and U.S. protectionist trade policies, negative exacerbated by major fluctuations on stock markets.

Income expectations “cannot escape the downward trend in economic outlook in April,” GfK said, as the sub-index fell to 53.5 points in April from 54.9 points in March.

Focus On ECB And Its Plan To Eventually End Its Stimulus

Notes/Observations

- Sweden Central Bank (Riksbank) pushed slightly back its 1st potential rate hike from H2 2018 until towards end of year

- ECB likely to shrugged of recent spat of soft growth and inflation data to keep its normalization path on track

- Germany seek to achieve a long-term delay for US steel tariffs for broader trade talks

Asia:

- Fitch affirmed Japan’s sovereign rating at A; outlook stable; Trade protectionism poses downside risk to outlook

- Japan PM Abe not considering calling snap election or dissolving parliament

- Japan Internal Affairs Min Noda: BoJ should drop 2% inflation target, should not further expand easing program

- South Korea President Moon and North Korea leader Kim to meet at border on Friday, Apr 27th for summit

- China said to consider cutting the levy on imported cars to either 10% or 15% vs 25% currently. An announcement could be made as soon as next month (May)

- China Commerce Min (MOFCOM) reiterated its opposition to all forms of unilateralism and protectionism

Europe:

- UK PM May said to issue 'wish list' regarding trade demands for Brexit

- Brexit-backing Conservatives said to have held private talks with PM May on Tuesday, Apr 24th to demand that she sticks to her plan for a clean break with the European Union. Tories said to have received assurances to satisfy the members (Note: could have the power to potentially trigger a leadership challenge and were concerned she was softening her Brexit position)

- German Fin Min Scholz: Still opposed to granting Greece debt relief without strict conditions

Americas:

- Moody’s affirmed the US sovereign rating at Aaa; outlook stable. country’s “exceptional” economic strength would counterbalance lower fiscal strength.

- Bank of Canada (BOC) Gov Poloz stated that the estimate for neutral rate was between 2.5-3.5% but not sure how far or quickly interest rates needed to rise. People needed to prepare for higher rates

Economic Data:

- (DE) Germany May GfK Consumer Confidence: 10.8 v 10.8e

- (FI) Finland Mar Preliminary Retail Sales Volume Y/Y: 3.8% v 2.8% prior

- (NO) Norway Feb AKU Unemployment Rate: 3.9% v 4.0%e

- (SE) Sweden Apr Consumer Confidence: 100.3 v 101.7e; Manufacturing Confidence: 120.3 v 113.3e, Economic Tendency Survey: 110.4 v 107.5e

- (ES) Spain Feb House Mortgage Approvals Y/Y: 13.8% v 9.2% prior; Total Mortgage Lending Y/Y: -2.5% v +18.5% prior

- (ES) Spain Q1 Unemployment Rate: 16.7% v 16.5%e

- (SE) Sweden Central Bank (Riksbank) left its Repo Rate unchanged -0.50% but pushed back slightly its 1st plan rate hike towards the end of 2018 (from H2)

- (SE) Sweden Mar PPI M/M: +1.2% v -0.5% prior; Y/Y: 4.0% v 2.8% prior

- (SE) Sweden Mar Trade Balance (SEK): +2.6B v -2.0B prior

- (AT) Austria Apr Manufacturing PMI: 58.0 v 58.0 prior (27th month of expansion)

- (UK) Mar BBA Loans for House Purchases: 37.6K v 37.2Ke

- (HK) Hong Kong Mar Trade Balance (HKD): -55.5B v -50.0Be; Exports Y/Y: +8.0% v +3.1%e; Imports Y/Y: +10.7% v +5.2%e

Fixed Income Issuance:

- (DK) Denmark sold total DKK300M in 1-month and 3-month Bills

- (IT) Italy Debt Agency (Tesoro) sold €6.0B vs. €6.0B indicated in 6-month Bills; Avg Yield: -0.426% v -0.430% prior; Bid-to-cover: 1.65x v 1.63x prior

- (SE) Sweden sold SEK500M in I/L 2027 bonds; Avg Yield: -1.2300% v -1.127% prior; Bid-to-cover: 2.51x v 3.99x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.2% at 380.8, FTSE flat at 7378, DAX -0.1% at 12406, CAC-40 +0.3% at 5428, IBEX-35 +0.3% at 9891, FTSE MIB +0.3% at 23884, SMI +0.4% at 8776, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

- European Indices trade mostly higher following weakness yesterday on another heavy day for corporate earnings. The Dax trades little changed, with Deutsche Bank recovering from earlier losses after missing estimates and announcing actions to reshape its CIB division whilst Kion Group, Lufthansa trade lower after missing estimates, VW trades higher after Q1 results. In France Total, Orange and Valeo reported results; In the UK Barclays reported a rise in adjusted profits, Rev did miss forecasts, with Royal Dutch Shell a faller after results.

Other notable earners included Philips Lighting which trades over 10% lower after a missing estimates, with Nokia also falling after missing on Revenues. - Looking ahead notable earners include General Motors, Raytheon and UPS.

Movers

- Consumer Discretionary [Lufthansa [LHA.DE] -6.2% (Earnings), Fielmann [FIE.DE] +2.8% (Earnings) ]

- Materials [Wacker Chemie [WCH.DE] +3.6% (Earnings) ]

- Financials [ Deutsche Bank [DBK.DE] +0.4% (Earnings)]

- Industrials [ Volkswagen [VOW.DE] +2.7% (Earnings), Kion Group [KGX.DE] -6.3% (Earnings), Aixtron [AIXA.DE] +4.9% (Earnings), Philips Lighting [LIGHT.NL] -11% (Earnings) ]

- Telecoms [Nokia [NOKIA.FI] -7% (Earnings) ]

- Healthcare [ Adocia [ADOC.FR] +28% (Announce a strategic Alliance for BioChaperone® Combo and BioChaperone® Lispro in China; To receive upfront payment of $50M)]

- Energy [ Shell [RDSA.NL] -2.6% (Earnings) ]

- Real Estate [Taylor Wimpey [TW.UK] -3.4% (Trading update)]

Speakers

- Sweden Central Bank (Riksbank) Policy Statement pushed back its 1st potential rate hike from H2 2018 until towards end of year (prior was in H2 of 2018). Dep Gov Ohlsson again dissented and called for a 25bps hike and entered a reservation against the lower Repo Rate Path. Recent SEK currency (Krona) weakness was seen as partly temporary and would strengthen going forward

- Sweden Central Bank (Riksbank) Gov Ingves post rate decision press conference stated that inflation still needed support from policy. If all wnt well than interest rates would be raised at the end of 2018. SEK currency (Krona) had weakened more than forecasted; weakness was seen as temporary

- Domestic growth to cool to a more normal pace

- EU chief Brexit negotiator Barnier: Many topics where both sides disagree; wanted to find a solution for the Irish border. UK govt red lines did close the door to options

- Greece PM Tsipras: Country to return to normality; close to achieving a clean bailout exit (aka no precautionary credit line needed)

- German govt said to consider stricter M&A rules for foreign companies

- German Chancellor Merkel said to propose to President Trump to renegotiate industry tariffs and sought a achieve a long-term delay for US steel tariffs

- Czech Central Bank Holub (chief economist): Inflation to stay below the 2% target for most of 2018

Currencies

- Focus was on ECB rate decision. Dealers noted that despite recent slowdown in EU growth and inflation it was difficult to see a dovish Draghi on Thursday. Markets will look for signs that ECB was preparing the ground for an announcement in June that stimulus was to come to an end by the end of the year. However, the EUR/USD found it hard to hold onto gains in the session. The pair was trading at 1.2175 just ahead of the NY morning and in the lower end of its 2018 trading range.

- EUR/SEK moved higher after the Riksbank pushed slightly back its 1st potential rate hike from H2 2018 until towards end of year. Cross moved above 10.4820 for fresh 9-year highs.

Fixed Income

- Bund Futures trade 23 ticks higher at 158.00 as European markets eye Thursday’s ECB meeting. Upside targets 159.75, while a return lower targets the157.25 level.

- Gilt futures trade at 121.26 higher by 22 ticks, tentatively breaking back above the 121 handle. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Thursday’s liquidity report showed Wednesday's excess liquidity rose to €1.863T from €1.850T prior. Use of the marginal lending facility fell from €40M to €30M.

- Corporate issuance saw 1 issuer raise $1.5B in the primary market

Looking Ahead

- (CA) Canada Apr CFIB Business Barometer: No est v 60.7 prior

- (AR) Argentina Apr Consumer Confidence: No est v 43.8 prior

- (IN) India to sell combined INR120B in 2023, 2031, 2035 and 2051 bonds

- (UK) House of Common debate on EU Withdrawal Bill

- 05:30 (ZA) South Africa Mar PPI M/M: No est v -0.3% prior; Y/Y: No est v 4.2% prior

- 05:30 (ID) Indonesia Central bank to hold press conference on IDR currency (Rupiah)

- 05:30 (HU) Hungary Debt Agency (AKK) to sell bonds (3 tranches)

- 06:00 (CZ) Czech Republic to sell Bills

- 06:00 (UK) Apr CBI Retailing Reported Sales: -3 v -8 prior, Total Distribution: No est v 5 prior

- 06:00 (IL) Israel Feb Manufacturing Production M/M: No est v 3.9% prior

- 06:30 (IS) Iceland to sell 3-month Bills

- 06:45 (US) Daily Libor Fixing

- 07:00 (RO) Romania to sell Bonds

- 07:00 (ES) Spain Mar YTD Budget Balance: No est v -€10.1B prior

- 07:45 (EU) European Central Bank (ECB) Interest Rate Decision: Expected to leave Main Refinancing Rate unchanged at 0.00%

- 08:00 (BR) Brazil Mar PPI Manufacturing M/M: No est v 0.3% prior; Y/Y: No est v 4.7% prior

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Initial Jobless Claims: 230Ke v 232K prior; Continuing Claims: 1.85Me v 1.863M prior

- 08:30 (US) Mar Advance Goods Trade Balance: -$75.0Be v -$75.9B prior (revised from -$75.4B)

- 08:30 (US) Mar Preliminary Durable Goods Orders: 1.6%e v 3.0% prior; Durables Ex-Transportation: 0.5%e v 1.0% prior, Capital Goods Orders (Non-defense/ex-aircraft): 0.6%e v 1.4% prior, Capital Goods Shipment (Non-defense/ex-aircraft): 0.4%e v 1.4% prior

- 08:30 (US) Mar Preliminary Wholesale Inventories M/M: 0.7%e v 1.0% prior; Retail Inventories M/M: No est v 0.4% prior

- 08:30 (US) Weekly USDA Net Export Sales

- 08:30 (EU) ECB’s Draghi post rate decision press conference

- 09:00 (RU) Russia Gold and Forex Reserve w/e Apr 20th: No est v $462.4B prior

- 09:00 (MX) Mexico Mar Unemployment Rate (seasonally adj): 3.3%e v 3.3% prior; Unemployment Rate: 3.1%e v 3.2% prior

- 09:30 (BR) Brazil Mar Total Outstanding Loans (BRL): No est v 3.062T prior; M/M: No est v -0.2% prior; Personal Loan Default rate: No est v 5.1% prior

- 10:00 (MX) Mexico Central Bank (Banxico) Apr Minutes

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (US) Apr Kansas City Fed Manufacturing Activity: 17e v 17 prior

- 13:00 (US) Treasury to sell $29B in 7-Year Notes

BoJ To Hold Rates, Stick With Inflation Outlook, Relief As Yen Falls

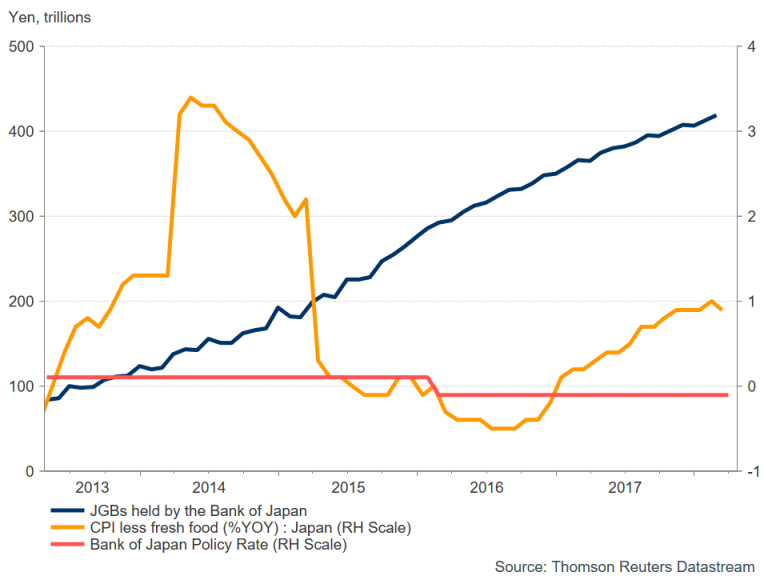

The Bank of Japan will announce its latest monetary policy decision on Friday after concluding a two-day meeting. The announcement could easily be a non-event as the Bank is widely expected to keep policy unchanged and not make any significant changes to its quarterly economic forecasts, which are published the same day. However, investors shouldn’t discount the possibility of a more dovish stance following the appointment of two new deputy governors.

With core inflation around 1%, the BoJ is not in a rush to begin preparations for an exit from its massive stimulus program. The 12-month CPI rate excluding fresh foods slipped to 0.9% in March from 1% previously, underscoring the long road ahead before the gauge hits the Bank’s 2% target. However, despite the lack of a build-up in inflationary pressures, the Bank will likely stick with its forecast of inflation reaching the target during the fiscal year 2019 in its latest quarterly projections.

The timing of when policymakers expect inflation to meet their 2% goal has been pushed back several times already and is still considered overoptimistic by many economists. Although another downgrade to the forecasts on Friday would come as a surprise, it is more probable now that another uber-dove, Masazumi Wakatabe, has joined the Bank’s board.

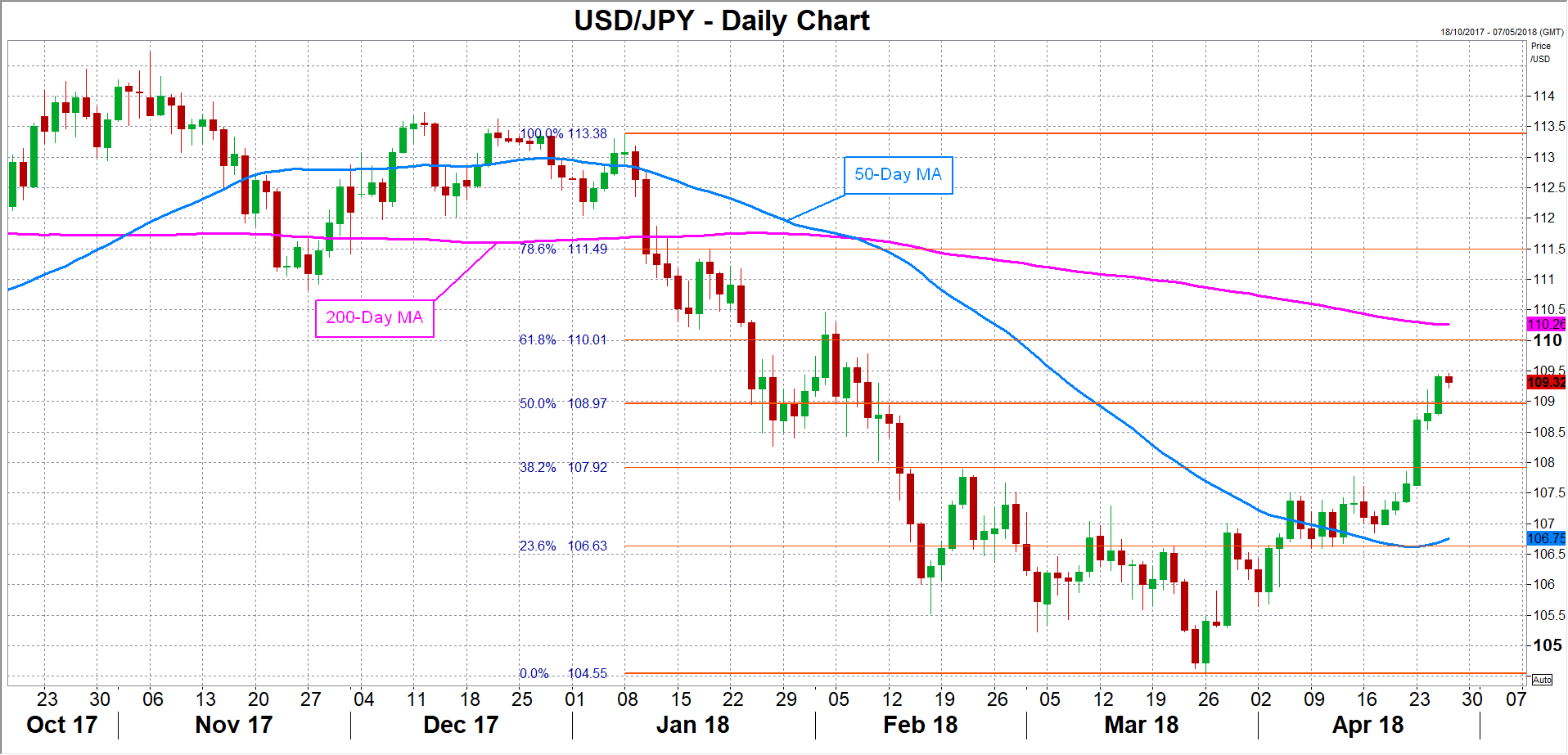

Wakatabe is one of two new deputy governors appointed in March, and along with Goushi Kataoka is the BoJ’s most dovish member. Kataoka has been quite vocal in calling for even looser monetary policy since joining the board in July 2017. Any signs of a fresh dovish tilt in the board’s views on Friday could extend the yen’s declines this week. The Japanese currency has been on the retreat in April, in a likely relief for Japanese policymakers and exporters, as geopolitical and trade war risks subside after fuelling safe-haven demand during much of the first quarter.

Further downside pressure on the yen could see the US dollar target the 110-yen level, having broken above the 109 level this week for the first time since February. Above that, the 111.50 level would come into focus as the next resistance to watch. However, were the BoJ to maintain its current forecasts and avoid giving out any new dovish signals, the yen could receive some short-term support, helping it settle just below the 109 level, while a deeper pull-back for the dollar could lift the yen closer to the 108 level.

Traders shouldn’t get their hopes up though for clues by Governor Haruhiko Kuroda on how soon to expect a scaling back of the BoJ’s asset purchases. Kuroda sent the yen soaring in early March after signalling that the Bank could begin tightening monetary policy in 2019. However, Kuroda has been more careful with his words since then and has repeatedly reiterated the need to maintain “powerful monetary easing” until inflation reaches 2%.

While Japan’s economy appears to have withstood the soft patch in global growth in the first three months of 2018, without a pickup in wage growth soon, households may start cutting back on spending again, dragging GDP growth lower. The threat of a global trade war is another risk weighing on the economy, given Japan’s status as a major exporting nation. Add to that, the Prime Minister, Shinzo Abe’s future is in doubt after a cronyism scandal involving himself and his finance minister erupted in March. Abe’s departure could spell the end to years of ‘Abenomics’ policies that have stimulated the economy, lifting it out of a deflationary cycle.

With all that in mind, the BoJ is unlikely to pull the plug on its ultra-loose monetary policy anytime soon and endanger the fragile recovery.