Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.97; (P) 109.21; (R1) 109.66; More...

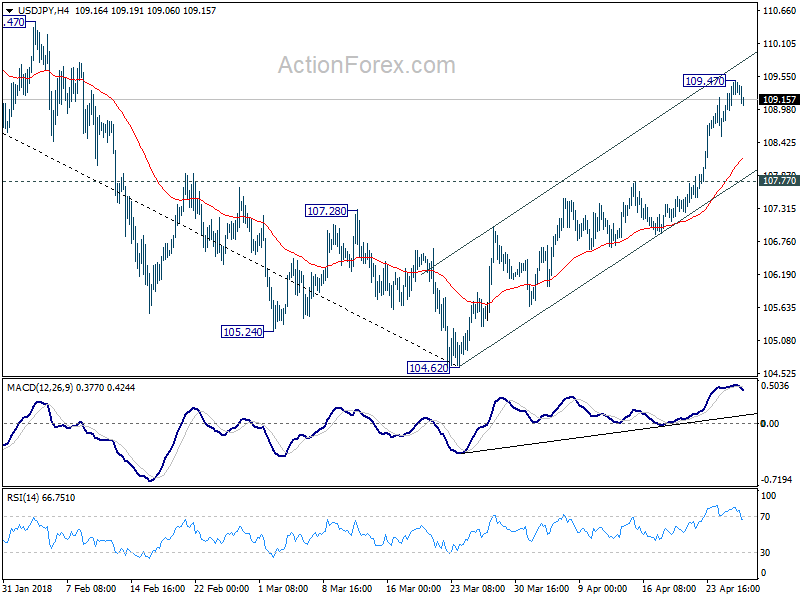

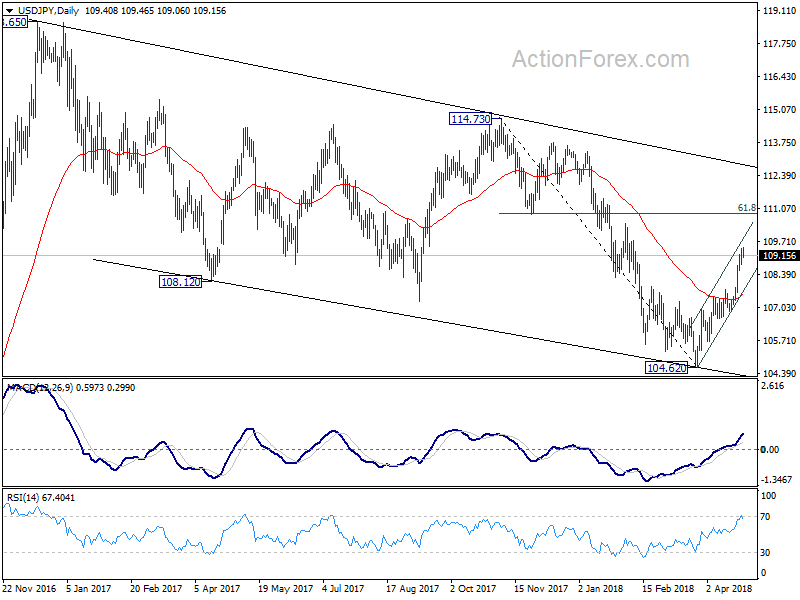

A temporary top is in place at 109.47 in USD/JPY and intraday bias is turned neutral for consolidation. Downside of retreat should be contained by 107.77 resistance turned support to bring another rally. Above 109.47 will resume the rise from 104.62 and target 61.8% retracement of 114.73 to 104.62 at 108.48 9 110.86 next.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.47).

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9792; (P) 0.9819; (R1) 0.9859; More...

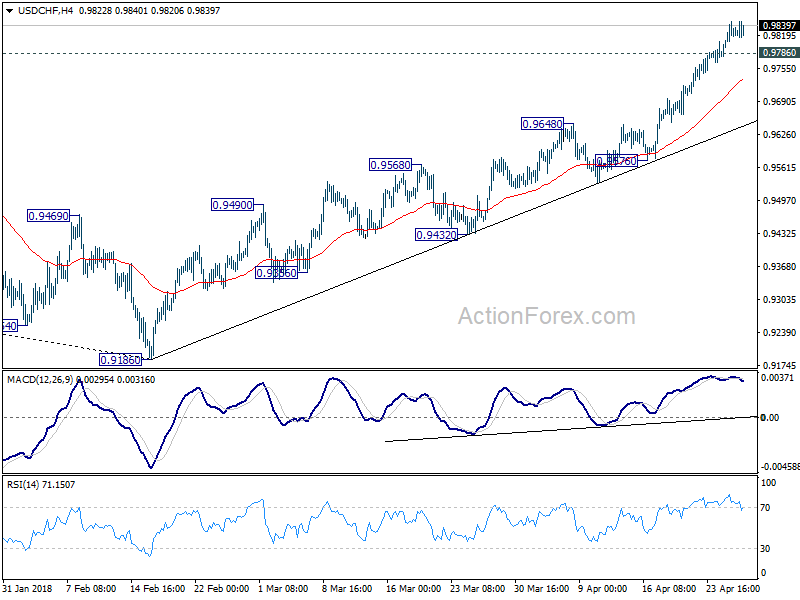

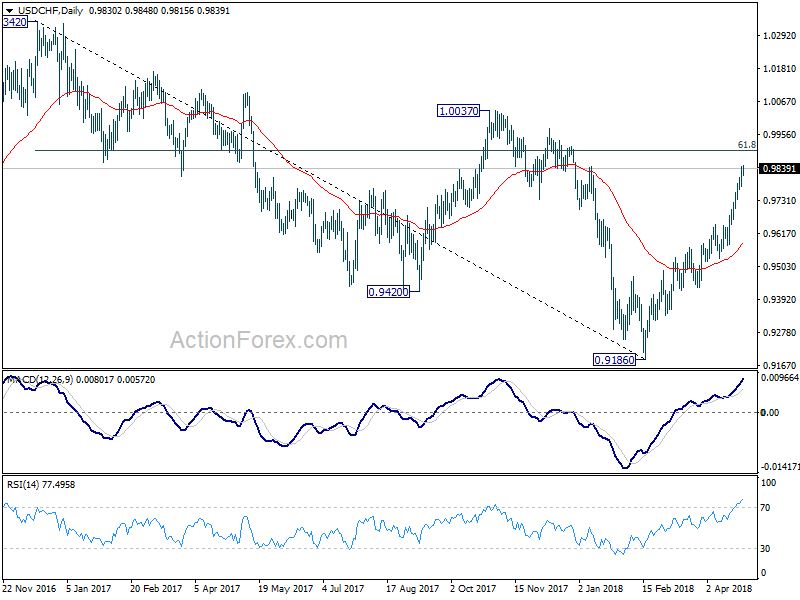

Despite diminishing upside momentum as see in 4 hour MACD, there is no sign of retreat yet. Intraday bias in USD/CHF remains on the upside for 0.9900 fibonacci level first. Break will target 1.0037 resistance next. On the downside, below 0.9786 minor support will turn bias neutral and bring consolidations. But outlook will stay bullish as long as 0.9576 support holds.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next. This will now be the preferred case as long as 0.9576 support holds.

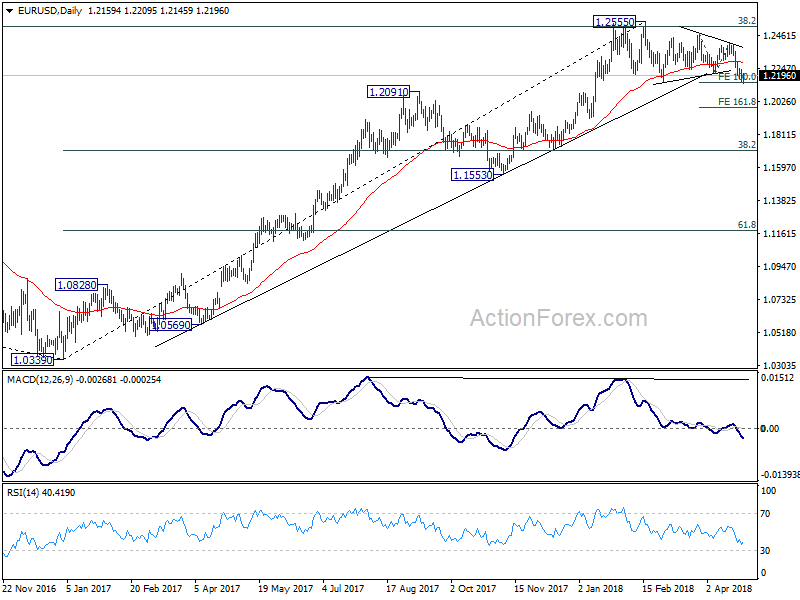

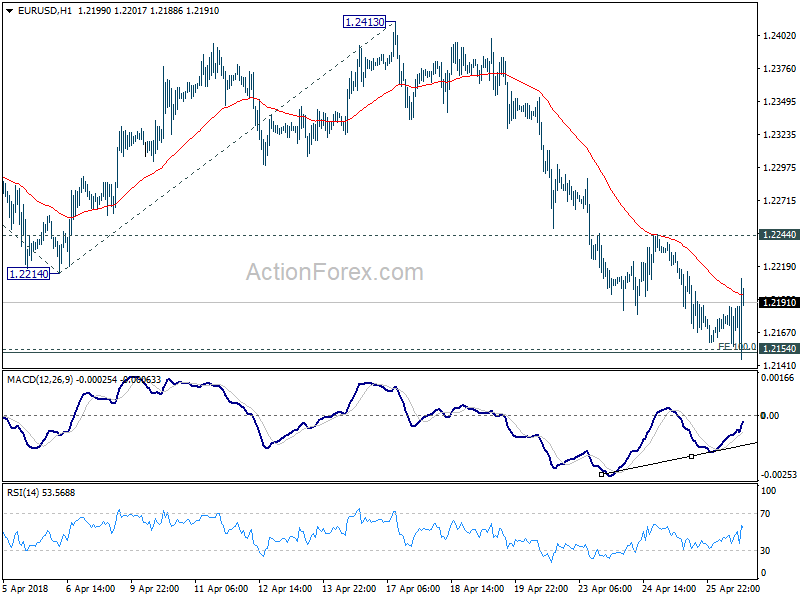

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2135; (P) 1.2186 (R1) 1.2213; More....

Despite breaching 1.2154 key support to 1.2145, EUR/USD quickly recovered. Intraday bias is turned neutral first. But further decline is still expected as long as 1.2244 minor resistance holds. As noted before, decisive break of 1.2154 should confirm the bearish case of medium term reversal. In addition, the break of 100% projection of 1.2475 to 1.2214 from 1.2413 will indicate downside acceleration. In that case, EUR/USD should target 161.8% projection at 1.1991 next. However, break of 1.2244 will indicate strong support from 1.2154 and turn intraday bias back to the upside for 1.2413, to extend recent range trading.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Euro Holding on to 1.2154 against Dollar on Cautiously Upbeat ECB Draghi, Dollar Weakens as Yields Retreat

Euro recovers against Dollar after ECB president Mario Draghi tried to play down concerns over recent weak Eurozone data. But his usual cautiousness is so far capping Euro buying. On the other hand, Dollar's rally also loses some steam, in particular against Yen as 10 year yield dips back below 3% handle. Despite upbeat job data from the US, the impact is offset by disappointing core durable goods orders too. Technically, the focus will stay on whether EUR/USD would break through 1.2154 key support to confirm medium term reversal, or it will break through 1.2244 minor resistance to indicate short term bottoming.

Quick update: EUR/USD breaks down around an hour after Draghi's press conference ended. Updated technical outlook here.

ECB stands pat, Draghi cautiously plays down weak data

ECB left main refinancing rate unchanged at 0.00% as widely expected. Deposit facility rate is held at -0.40% and marginal lending facility rate at 0.25%. Also, the EUR 30B monthly asset purchase program will continue through end of September. Euro is lifted mildly following President Mario Draghi's upbeat comments in the introductory statement. But no follow through buying is seen after his cautious remarks during the Q&A.

In particular, Draghi noted in the introductory statement that data since March "points towards some moderation" in growth. However, they are still "consistent with a solid and broad-based expansion of the euro area economy". Also, Draghi added that "the underlying strength of the euro area economy continues to support our confidence that inflation will converge towards our inflation aim of below, but close to, 2% over the medium term." But later, Draghi turned back into his cautious mode and said it's important to determine if softer data temporary or permanent.

US jobless claims dropped to lowest since 1969, trade deficit narrowed sharply

Initial jobless claims dropped 24k to 209k in the weekended April 21, below expectation of 230k. That's also the lowest level since 1969. Four week moving averaged dropped to 229.25k, down fro 231.50k. Continuing claims dropped 29k to 1.84m in the week ended April 14.

Trade deficit narrowed sharply by -10.3% to USD 68B in March, way lower than expectation of USD -74.8B. Headline durable goods orders jumped 2.6%, much higher than expectation of 1.4%. But that's mainly due to a big increase in contracts for Boeing. Ex-transport orders was flat, below expectation of 0.40%.

SNB Q1 USD holding unchanged at 35%, EUR holding dropped 1%

SNB reported CHF 6.8B loss in Q1 of 2018.That includes CHF 7.0B loss on currency positions and CHF 0.2B loss on gold holdings. The losses were partly offset by CHF 0.5B gain in Swiss Franc positions, mainly from negative interest rates. Current allocations in the foreign exchange reserves were largely unchanged. USD holdings was at 35%, GBP holding at 7%, JPY holdings at 8% and CAD holdings at 3%. EUR holdings, on the other hand, dropped 1% to 39%.

German Gfk consumer climate dropped 0.1 to 10.8.

German Gfk consumer climate dropped to 10.8 in May, down 0.1 from 10.9, met expectations. GFK noted in the release that "the increasingly insecure state of geopolitics now also seems to be influencing the mood of consumers." It pointed to "escalation of the Syrian crisis and the protectionist trade policies of the United States" that could affect Germany's "previously excellent economic prospects." Also, "increasing protectionism in international trade would hit Germany, as an export nation, resulting in employees fearing they may lose their jobs and again being more reluctant to buy."

Elsewhere

UK BBA mortgage approvals dropped to 37.6k in March. CBI reported sales dropped improved to -2 in April. Australia import price index rose 2.1% qoq in Q1.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2135; (P) 1.2186 (R1) 1.2213; More....

Despite breaching 1.2154 key support to 1.2145, EUR/USD quickly recovered. Intraday bias is turned neutral first. But further decline is still expected as long as 1.2244 minor resistance holds. As noted before, decisive break of 1.2154 should confirm the bearish case of medium term reversal. In addition, the break of 100% projection of 1.2475 to 1.2214 from 1.2413 will indicate downside acceleration. In that case, EUR/USD should target 161.8% projection at 1.1991 next. However, break of 1.2244 will indicate strong support from 1.2154 and turn intraday bias back to the upside for 1.2413, to extend recent range trading.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Import price index Q/Q Q1 | 2.10% | 1.20% | 2.00% | |

| 06:00 | EUR | German GfK Consumer Confidence May | 10.8 | 10.8 | 10.9 | |

| 08:30 | GBP | BBA Loans for House Purchase Mar | 37.6K | 37.1K | 38.1K | 38.0K |

| 10:00 | GBP | CBI Reported Sales Apr | -2 | -2 | -8 | |

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | USD | Initial Jobless Claims (APR 21) | 209K | 230K | 232K | 233K |

| 12:30 | USD | Advance Goods Trade Balance Mar | -68.0B | -74.8B | -75.9B | |

| 12:30 | USD | Wholesale Inventories M/M Mar P | 0.50% | 0.60% | 1.00% | |

| 12:30 | USD | Durable Goods Orders Mar P | 2.60% | 1.40% | 3.00% | 3.00% |

| 12:30 | USD | Durables Ex Transportation Mar P | 0.00% | 0.40% | 1.00% | 1.00% |

| 14:30 | USD | Natural Gas Storage | -11B | -36B |

Euro trying to recover as ECB Draghi downplays data. Confident on solid and broad-based growth

Euro initial dipped but recovered after ECB President Mario Draghi's comments (in the introducatory statement) on the economy. The point that triggered the reaction is that while data since March "points towards some moderation" in growth, the data were still "remaining consistent with a solid and broad-based expansion of the euro area economy". And, he added that "the underlying strength of the euro area economy continues to support our confidence that inflation will converge towards our inflation aim of below, but close to, 2% over the medium term."

The comments are rather upbeat comparing to the usual standard cautious tone of Draghi.

However, strength in the Euro is limited after the "normal" cautious Draghi comes back saying that it's important to determine if softer data temporary or permanent.

EUR/USD's breach of 1.2154 key support is brief so far. And the recovery could turn focus back to 1.2244 minor resistance. But it will take more time for traders to make up their mind. For now, more downside is still expected as long as 1.2244 holds and a break of 1.2154 is still more likely than not.

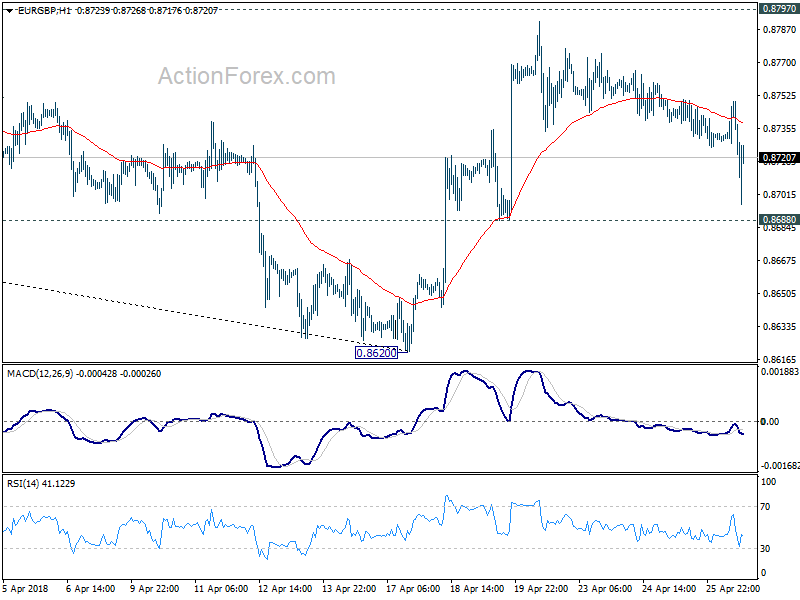

On other hand, EUR/GBP is still pressured despite the recovery attempt. Focus is back on 0.8688 minor support. Break will indicate completion of rebound from 0.8620. That could trigger EUR selling elsewhere.

ECB President Mario Draghi’s press conference statement

ECB President Mario Draghi's full press conference statment below:

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases.

Regarding non-standard monetary policy measures, we confirm that our net asset purchases, at the current monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem will continue to reinvest the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

Following several quarters of higher than expected growth, incoming information since our meeting in early March points towards some moderation, while remaining consistent with a solid and broad-based expansion of the euro area economy. The underlying strength of the euro area economy continues to support our confidence that inflation will converge towards our inflation aim of below, but close to, 2% over the medium term. At the same time, measures of underlying inflation remain subdued and have yet to show convincing signs of a sustained upward trend. In this context, the Governing Council will continue to monitor developments in the exchange rate and other financial conditions with regard to their possible implications for the inflation outlook. Overall, an ample degree of monetary stimulus remains necessary for underlying inflation pressures to continue to build up and support headline inflation developments over the medium term. This continued monetary support is provided by the net asset purchases, by the sizeable stock of acquired assets and the ongoing and forthcoming reinvestments, and by our forward guidance on interest rates.

Let me now explain our assessment in greater detail, starting with the economic analysis. Real GDP increased by 0.7%, quarter on quarter, in the fourth quarter of 2017, following similar growth in the previous quarter. This resulted in an average annual growth rate of 2.4% in 2017 – the highest since 2007. The latest economic indicators suggest some moderation in the pace of growth since the start of the year. This moderation may in part reflect a pull-back from the high pace of growth observed at the end of last year, while temporary factors may also be at work. Overall, however, growth is expected to remain solid and broad-based. Our monetary policy measures, which have facilitated the deleveraging process, should continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by growing household wealth. Business investment continues to strengthen on the back of very favourable financing conditions, rising corporate profitability and solid demand. Housing investment continues to improve. In addition, the broad-based global expansion is providing impetus to euro area exports.

The risks surrounding the euro area growth outlook remain broadly balanced. However, risks related to global factors, including the threat of increased protectionism, have become more prominent.

Euro area annual HICP inflation increased to 1.3% in March 2018, from 1.1% in February. This reflected mainly higher food price inflation. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around 1.5% for the remainder of the year. Measures of underlying inflation remain subdued overall. Looking ahead, they are expected to rise gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

Turning to the monetary analysis, broad money (M3) continues to expand at a robust pace, with an annual growth rate of 4.2% in February 2018, slightly below the narrow range observed since mid-2015. M3 growth continues to reflect the impact of the ECB's monetary policy measures and the low opportunity cost of holding the most liquid deposits. Accordingly, the narrow monetary aggregate M1 remained the main contributor to broad money growth, continuing to expand at a solid annual rate.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations stood at 3.1% in February 2018, after 3.4% in January and 3.1% in December 2017, while the annual growth rate of loans to households remained unchanged at 2.9%. The euro area bank lending survey for the first quarter of 2018 indicates that loan growth continues to be supported by increasing demand across all loan categories and a further easing in overall bank lending conditions for loans to enterprises and loans for house purchase.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing ‒ notably for small and medium-sized enterprises ‒ and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need for an ample degree of monetary accommodation to secure a sustained return of inflation rates towards levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Against the background of overall limited implementation of the 2017 country-specific recommendations, greater reform effort is necessary in euro area countries. Regarding fiscal policies, the ongoing broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt remains high. All countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

We are now at your disposal for questions.

(ECB) Introductory Statement to the Press Conference

Mario Draghi, President of the ECB,

Vítor Constâncio, Vice-President of the ECB,

Frankfurt am Main, 26 April 2018

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases.

Regarding non-standard monetary policy measures, we confirm that our net asset purchases, at the current monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem will continue to reinvest the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

Following several quarters of higher than expected growth, incoming information since our meeting in early March points towards some moderation, while remaining consistent with a solid and broad-based expansion of the euro area economy. The underlying strength of the euro area economy continues to support our confidence that inflation will converge towards our inflation aim of below, but close to, 2% over the medium term. At the same time, measures of underlying inflation remain subdued and have yet to show convincing signs of a sustained upward trend. In this context, the Governing Council will continue to monitor developments in the exchange rate and other financial conditions with regard to their possible implications for the inflation outlook. Overall, an ample degree of monetary stimulus remains necessary for underlying inflation pressures to continue to build up and support headline inflation developments over the medium term. This continued monetary support is provided by the net asset purchases, by the sizeable stock of acquired assets and the ongoing and forthcoming reinvestments, and by our forward guidance on interest rates.

Let me now explain our assessment in greater detail, starting with the economic analysis. Real GDP increased by 0.7%, quarter on quarter, in the fourth quarter of 2017, following similar growth in the previous quarter. This resulted in an average annual growth rate of 2.4% in 2017 – the highest since 2007. The latest economic indicators suggest some moderation in the pace of growth since the start of the year. This moderation may in part reflect a pull-back from the high pace of growth observed at the end of last year, while temporary factors may also be at work. Overall, however, growth is expected to remain solid and broad-based. Our monetary policy measures, which have facilitated the deleveraging process, should continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by growing household wealth. Business investment continues to strengthen on the back of very favourable financing conditions, rising corporate profitability and solid demand. Housing investment continues to improve. In addition, the broad-based global expansion is providing impetus to euro area exports.

The risks surrounding the euro area growth outlook remain broadly balanced. However, risks related to global factors, including the threat of increased protectionism, have become more prominent.

Euro area annual HICP inflation increased to 1.3% in March 2018, from 1.1% in February. This reflected mainly higher food price inflation. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around 1.5% for the remainder of the year. Measures of underlying inflation remain subdued overall. Looking ahead, they are expected to rise gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

Turning to the monetary analysis, broad money (M3) continues to expand at a robust pace, with an annual growth rate of 4.2% in February 2018, slightly below the narrow range observed since mid-2015. M3 growth continues to reflect the impact of the ECB's monetary policy measures and the low opportunity cost of holding the most liquid deposits. Accordingly, the narrow monetary aggregate M1 remained the main contributor to broad money growth, continuing to expand at a solid annual rate.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations stood at 3.1% in February 2018, after 3.4% in January and 3.1% in December 2017, while the annual growth rate of loans to households remained unchanged at 2.9%. The euro area bank lending survey for the first quarter of 2018 indicates that loan growth continues to be supported by increasing demand across all loan categories and a further easing in overall bank lending conditions for loans to enterprises and loans for house purchase.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing ‒ notably for small and medium-sized enterprises ‒ and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need for an ample degree of monetary accommodation to secure a sustained return of inflation rates towards levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Against the background of overall limited implementation of the 2017 country-specific recommendations, greater reform effort is necessary in euro area countries. Regarding fiscal policies, the ongoing broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt remains high. All countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

We are now at your disposal for questions.

US jobless claims dropped to lowest since 1969, trade deficit narrowed sharply

Dollar shows little reaction to a mixed batch of data from the US.

Initial jobless claims dropped 24k to 209k in the weekended April 21, below expectation of 230k. That's also the lowest level since 1969. Four week moving averaged dropped to 229.25k, down fro 231.50k. Continuing claims dropped 29k to 1.84m in the week ended April 14.

Trade deficit narrowed sharply by -10.3% to USD 68B in March, way lower than expectation of USD -74.8B. Headline durable goods orders jumped 2.6%, much higher than expectation of 1.4%. But that's mainly due to a big increase in contracts for Boeing. Ex-transport orders was flat, below expectation of 0.40%.

DAX Stems Slide, Markets Eye ECB Statement

The DAX index has steadied in the Thursday session, after recording sharp losses in Wednesday trade. Currently, the DAX is trading at 12,437 points, up 0.12% on the day. On the release front, German GfK Consumer Confidence edged down to 10.8, close to the estimate of 10.9 points. Later in the day, the ECB releases a rate statement, with ECB President Mario Draghi following up with a press conference. On Friday, the US releases Advance GDP for the first quarter.

European stock markets were in red territory on Wednesday, as higher bond yields saw investors ditch equities in favor of US bonds. Treasury notes have hit 4-year highs this week. On Wednesday, 10-year US Treasury notes climbed to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is making bonds more attractive at the expense of the stock markets.

The ECB will be on center stage on Thursday, with a rate state announcement and a Mario Draghi press conference. Eurozone indicators have softened in recent weeks, raising concerns that ECB President Mario Draghi could sound dovish about the eurozone economy. At the March meeting, policymakers made a minor move and dropped a pledge to increase stimulus if needed. The ECB has said it intends to continue bond purchases until at least September and will maintain interest rates at current levels until “well past” the end of the program. Traders shouldn’t expect any dramatic moves at the policy meeting, as the bank will likely continue to preach patience and prudence as it continues to gauge economic activity in the eurozone.

ECB kept main refinancing rate unchagned at 0.00% as widely expected

ECB left main refinancing rate unchagned at 0.00% as widely expected. Deposit facility rate is held at -0.40% and marginal lending facility rate at 0.25%. Below is the statement. ECB's press conference could be watched here if you're interested.

Monetary policy decisions

At today's meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

Regarding non-standard monetary policy measures, the Governing Council confirms that the net asset purchases, at the current monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem will reinvest the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.