Sample Category Title

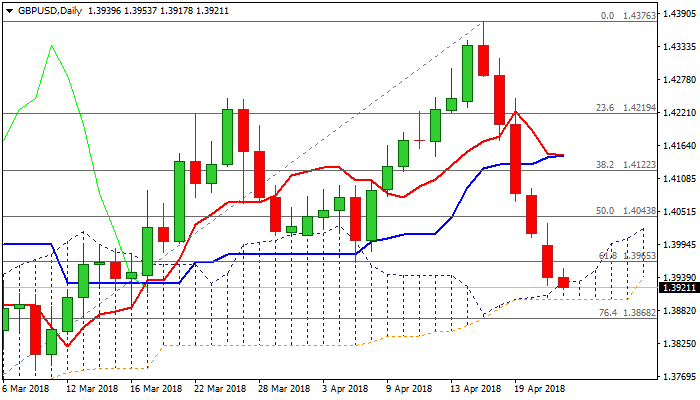

GBPUSD Looks To Extend Steep Descend Through Daily Cloud Top, But Limited Corrective Upticks Not Ruled Out

Cable holds in red for the sixth straight day and attempts to extend steep descend from last week’s peak at 1.4376 (the highest level after Brexit vote).

Strong bearish signal was generated on Monday’s break and close below pivotal support at 1.3965 (Fibo 61.8% of 1.3711/1.4376 rally / 05 Apr trough).

Fresh extension lower today penetrated thin daily cloud (spanned between 1.3931/01) but stalled above cloud base and returned above the cloud.

This could be initial signal of bounce as slow stochastic turned sideways in deep oversold territory, suggesting bears may take a breather.

Formation of daily Tenkan-sen/Kijun-sen bear-cross and firmly bearish momentum studies signal limited corrective action before bears resume.

Break through cloud base would open rising 100SMA (1.3854) and could trigger further bearish acceleration on break.

Broken pivot at 1.3965 marks solid resistance, with extended upticks expected to hold below psychological 1.40 barrier (also 55SMA).

Res: 1.3931, 1.3953, 1.3965, 1.4000

Sup: 1.3901, 1.3868, 1.3854, 1.3780

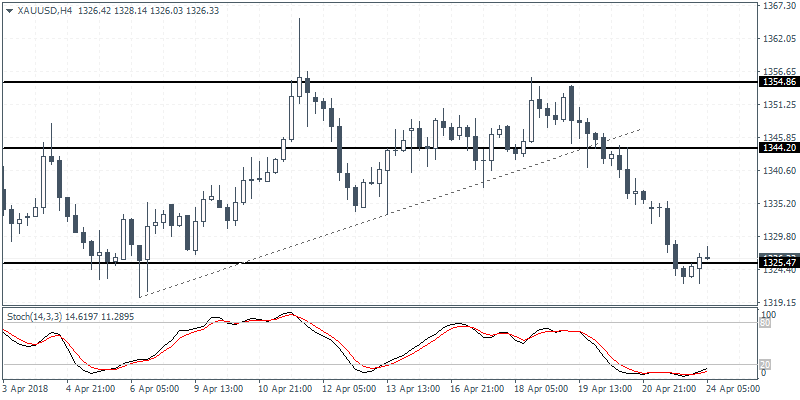

XAUUSD Intraday Analysis

XAUUSD (1326.33): Gold prices fell sharply on the day as price action touched down to 1325.50 level of support. We see price action attempting to consolidate at the current levels. If a temporary bottom is formed at this level, we expect price action to retrace the losses to 1335 level which marks the 38.2% retracement level. Further gains could push gold prices to post a sharper correction toward 1344 which would mark the 61.8% Fib retracement from the highs of 1355.74 from 18 April and the current low at 1322.19 from earlier today.

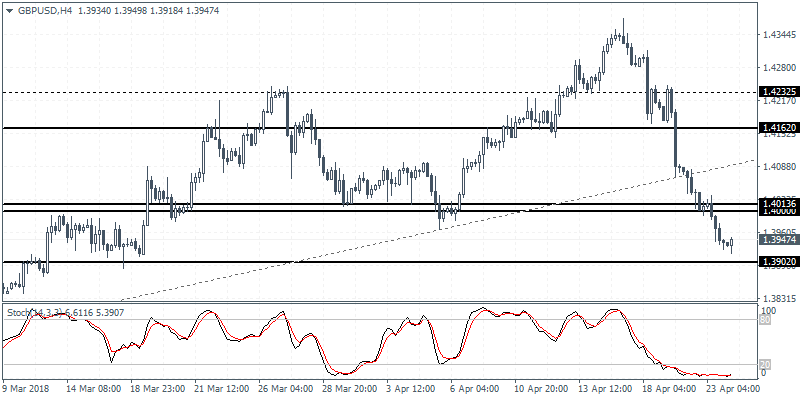

GBPUSD Intraday Analysis

GBPUSD (1.3947): The British pound was seen giving up the gains made over the past few weeks as the major support level at 1.4000 failed to stall the declines. The breakdown below the 1.4000 support signaled further losses. Price action is seen reversing the losses just above the next main support level at 1.3902 level. The current rebound could be seen extending back to 1.4000 where it is likely for resistance to be established. The GBPUSD currency pair is expected to maintain its range within these levels for the moment.

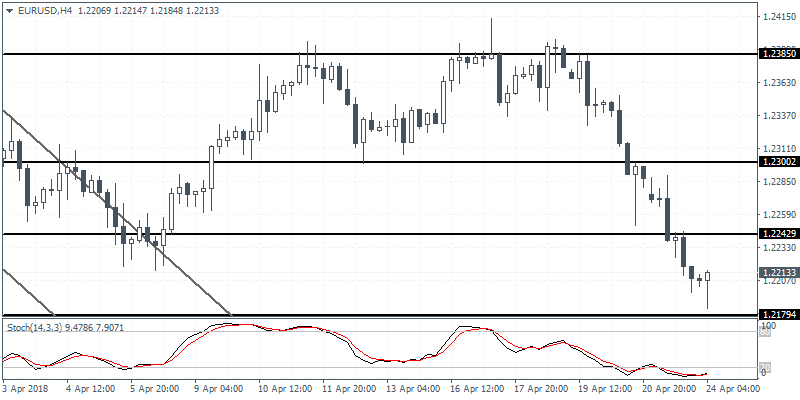

EURUSD Intraday Analysis

EURUSD (1.2213): The EURUSD currency pair was seen extending the declines for the third consecutive day. Price action was seen breaking below the 1.2241 level of support on the daily chart before reversing the declines, just a few pips off the 1.2180 level of support. In the near term, we expect price to retrace the losses to test the breached support level at 1.2250 on the 4-hour chart. Establishing resistance at this level could potentially keep EURUSD range bound within the 1.2180 level of support. Due to the fact that the EURUSD failed to test the previously breached support level at 1.2300, a breakout above 1.2250 will see the EURUSD testing this level for resistance.

USD Maintains Strong Gains

The U.S. dollar was seen posting strong gains on the day across the board. The gains came amid data from the Eurozone showing that manufacturing PMI might have eased to 56.0 in April. Services PMI data was seen registering a print of 55.0, slightly higher from 54.8 that was forecast.

The U.S. 10-year yields were seen rising close to the 3% threshold at 2.973%. This was the highest level in the 10-year yields since January of 2014.

Canadian wholesale sales were seen falling 0.8% on the month following a revised 0.3%increase the month before.

Looking ahead, the economic calendar for the day will see the release of the German Ifo business climate data. Economists forecast that after the Ifo business climate fell sharply, it is expected to pick up modestly to 104.7.

Data from the UK will see the release of the public sector net borrowing data which is expected to expand to 1.1 billion GBP. The data from the U.S. is rather limited with the CB consumer confidence data that is expected to show a decline to 126.0 compared to 127.7 previously. New home sales are expected to rise to 625k, up from 618k that was registered in the month before.

Currencies: USD Maintains Gain. EUR/USD Is Nearing MT Range Bottom

- Rates: Technical hurdles and ECB looming on horizon

Core bond sentiment remains negative, but the sell-off seems to be losing steam as the US 10-yr yield approaches key resistance levels slightly above the psychological 3% mark and with the ECB meeting looming on the horizon. - Currencies: USD maintains gain. EUR/USD is nearing MT range bottom

The dollar remained well bid yesterday, supported by higher yields. German IFO confidence and US consumer confidence take center stage today. However, both series probably won't change the balance between the euro and the dollar. The dollar rebound might slow at least temporary as the rise in US yields slows

The Sunrise Headlines

- US stock markets ended nearly unchanged with Nasdaq slightly lower (-0.25%). Asian equity indices are stronger this morning with China outperforming (+2%), anticipating policy measures to boost liquidity and improve growth.

- Australian CPI stayed soft last quarter as core inflation (slightly higher than forecast) began a third year below the central bank's target, cementing expectations any hike in interest rates is a long distance off. (Reuters)

- Italian President Mattarella asked lower house Speaker Fico to find out whether the anti-establishment Five Star Movement could govern with the center-left Democratic Party, in the latest attempt to break a seven-week impasse. (BB)

- Strong growth in ad sales on Google search and YouTube were not enough to offset a surge in costs at parent Alphabet that shrank the first-quarter operating margin, leaving shares flat after hours. (Reuters)

- Liquidity tensions from last week will likely be eased as RRR cut to take effect while fiscal spending will increase this week, according to a front-page commentary in China Securities Journal. (BB)

- A US Senate committee endorsed Mike Pompeo to be the next secretary of state, sending him to the full Senate for his expected confirmation, after Sen. Rand Paul reversed himself and withdrew his opposition. (WSJ)

- Today's eco calendar contains German Ifo business sentiment, US new home sales, consumer confidence and Richmond Fed manufacturing index. Italy, Germany, Finland and the US tap the bond market.

Currencies: USD Maintains Gain. EUR/USD Is Nearing MT Range Bottom

EUR/USD 1.2155 support coming with reach?

The USD rebound continued yesterday. It was supported by a gradual further rise in US yields with the 10-y yield nearing the 3% barrier. The EMU April PMI's were slightly above consensus. However, they were not really able to remove the feeling that the EMU growth momentum might be over its peak. Markets apparently assume that the assessment at Thursday's ECB meeting might remain rather soft. EUR/USD drifted below intermediate support at 1.2215 (close at 1.2209). USD/JPY also succeeded a nice break higher and closed the session at 108.71.

Overnight, Asian equities mostly show good gains with Taiwan and Korea underperforming. China outperforms as markets expect the Chinese authorities to keep a rather easy policy in place. The dollar maintains yesterday's gains, but for now there is no follow-through. EUR/USD is holding in the low 1.22 area. USD/JPY hovers in the 108.75 area. Australian CPI inflation was close to expectations. Headline inflation was unchanged at 1.9% Y/Y (2.0% expected). AUD/USD slipped temporary to the 0.7580 area, but soon returned to the 0.76 area.

Today, in Europe several national confidence indices (including the IFO) will be published. IFO confidence is expected to rebound from 103.2 to 104.7. In the US, housing data, the Richmond manufacturing index and consumer confidence will be published. The latter is probably most important for markets. The headline confidence is expected to ease slightly from a multi-year peak. Over the previous days, the dollar finally profited from higher US yields with the 2-yr USD /German spread widening above 300 bp. Markets keep a close eye whether US 10-y yield might rise above 3%. The test is ongoing, but maybe there won't be trigger for a break anytime soon. If so, this might slow the USD rise with markets awaiting Thursday's ECB meeting. A soft ECB assessment might be needed to push EUR/USD below the 1.2155 support.

Yesterday, EUR/GBP basically held a consolidation pattern in the mid 0.87 area as the post-Carney correction slowed. There was also again plenty of noise on Brexit as the poltical debate inside the UK is heating up. Today, CBI business optimism and trends orders will be published. We expect these data to be only of intraday significance. The sterling decline slowed with EUR/GBP holding below the 0.88 resistance. Some consolidation might be on the cards. Friday's UK Q1 GDP data are a potential next reference. Brexit noise remains a wildcard

EUR/USD: nearing/testing first support area at 1.2215/1.2155

No Change to ECB Guidance Yet

- Draghi signaled that growth peak might be behind us

- A lot of questions on ECB Nowotny's slip of the tongue

- No policy changes; expectations are low

- Risk for more optimist/hawkish tone in communication?

Status quo in March

The March ECB policy meeting saw a small step on what promises to be a long journey towards policy normalization but any possibility that this might prompt significant adverse market reaction was more than countered by the very dovish wording emphasised by Mario Draghi in explaining the change in the ECB's thinking.

The ECB opted to remove a commitment to increase the scale or duration of the Asset Purchase Programme in the event of a deterioration in economic or financial conditions at the previous policy meeting in March. This small change in forward guidance didn't come as any surprise because of the strong EMU growth performance. Moreover, the removal of the easing bias was balanced by comments from ECB president Draghi and new ECB economic projections arguing in favour of keeping in place an ample degree of monetary stimulus.

Mr Draghi reassured markets by underlining that a very accommodative policy stance will remain necessary if underlying inflation pressures are to build to the point where they support headline inflation developments moving towards the ECB's target of below but close to 2% over the medium term. Current ECB forecasts project headline CPI at 1.4% this year and in 2019, before accelerating to 1.7% in 2020.

The recently released minutes of that March meeting pointed out that some governors put forward the view that enough progress had already been made to put inflation on a sustained path towards the medium‐term policy goal of just under 2%. This possibly important signal eventually didn't feature in the ECB's statement. The bloc around the architects of the current extraordinary monetary policy – President Draghi, Vice‐President Constancio and Chief Economist Praet – still holds the majority and is still of a more dovish disposition. They argue that sufficient slack remains for the EMU economy to grow without exerting upward price pressure and appear to take the view that premature policy tightening or comments that prompt a tightening of financial conditions by markets anticipating aggressive ECB action are risks the ECB must avoid at present.

A second notable highlight of the account of the March 7‐8 meeting was widespread concern about a potential trade war: "the risk of trade conflicts, which could be expected to have an adverse impact on activity for all countries involved, had increased." ECB president Draghi strengthened this view in recent comments by pointing out that positive developments in the euro area are not independent of the global growth momentum. "Preserving openness is crucial if the global economy is to thrive and to secure its growth potential."

EMU growth peak behind us?

Draghi warned in that same speech at the International Monetary and Financial Committee (Apr 20) for the first time that latest EMU economic indicators suggest that the growth cycle might have peaked (in Q4 2017), even if growth momentum is expected to continue. PMI's seem to underwrite that view of a natural tipping over of the economic cycle. The EMU composite PMI peaked in January at 58.8. The latest, April reading, showed a stabilization at 55.2 after two consecutive declines in February and March. That's close to the three uninterrupted drops which are considered as a change in trend. Other confidence indicators, as well as hard data, at least tentatively point in the same direction.

The slight tweak in growth rhetoric was accompanied by confirmed confidence in the inflation outlook. Underlying inflation is expected to rise gradually supported by the ECB's monetary measures and in line with the ongoing reabsorption of economic slack and rising wage growth. Last week's German public sector pay deal, following the agreement reached by IG Metall earlier this year, is at least a pointer towards a rising trend in domestic costs in some parts of the Euro area economy. However broader and sustained evidence of rising costs may be needed to confirm that a persistent pick‐up in inflation is in sight.

Without reading too much into it, the slight shift in the tone of recent comments could be interpreted as signaling a growing awareness on the part of at the ECB of an argument in favor of policy normalization stemming from the need to build in room to act in the event of a future downturn. The Fed in more or less similar vein turned the argument at the start of the normalization process. Initially, they focused on the lack of actual inflation pressure despite US growth momentum. That thinking subtly shifted to confidence that US economy became strong enough to expect inflation to pick up.

Market expectations are low

There is little prospect of any substantive changes to the ECB's forward guidance or monetary policy this week. In the absence of such developments, any slight shift in tone could be the most important thing to watch at Thursday's ECB meeting. From a market point of view, it suggests that risks are marginally tilted to the hawkish side because expectations going into the meeting are very low. Consensus has been building that the ECB will end its net asset purchases by the end of the year, but communication on the issue will probably only come in June (with new growth/inflation forecasts) or, as hinted in recent ECB 'sources' newswire reports, in July. Current economic conditions still warrant a first ECB rate hike by mid‐2019, in line with what president Draghi flagged during the Q&A after one of the previous press conference. The (rate) market remains more dovish positioned, only expecting positive 3m Euribor rates by the end of 2019.

While it is unlikely to feature in the ECB's opening press statement, an important feature of this week's meeting could be a focus in the Q&A session on the Austrian central bank governor Nowotny's April 10 Reuters interview. Nowotny suggested a 20 bps deposit rate hike was feasible shortly after the ECB ends its net asset purchases, narrowing the interest rate corridor. Subsequently, the ECB could hike its main policy rates simultaneously. Nowotny is the first governor to give any detail on the practical stages entailed when the ECB moves onto a normalization path, even if the ECB officially distanced itself from his views. Markets proved to be sensitive to the issue with higher (short term) European rates and a stronger euro as a consequence. The official ECB stance on the issue remains rather vague, hanging on to the broader idea of a sequencing" principle: first ending net asset purchases and next start hiking interest rates. We expect Draghi to hold on to that official line for now.

The market expects little excitement from the ECB this week and reaction to what is likely to be little more than a repeat of previous commentary will probably be muted. The recent negative momentum on bond markets suggests that a sell‐off might continue if Draghi deviates slightly from the dovish scenario that markets have in mind. From a technical point of view, we initially eye a return towards the 0.80% 2018 top in the German 10‐yr yield. The euro could be less sensitive on this stage as long as Draghi doesn't elaborate on the post‐APP period. A more optimistic ECB could nevertheless slow EUR/USD's downward momentum and complicate a test of first support at 1.2215/1.2155.

EURUSD Strongly Bearish Below 1.2202 Level

The euro has fallen to a new monthly trading-low against the greenback, hitting 1.2184, after better than expected U.S macroeconomic data lifted the U.S dollar broadly higher. The EURUSD pair currently trades around the 1.2214 level, marking the single currencies lowest trading level against the U.S dollar since, March 1st. Traders now look towards the release of German IFO data, and the EURUSD pairs key 100-day moving average, found at the 1.2202 level.

The EURUSD pair is strong bearish while trading below 1.2202 level, further downside towards the 1.2184 and 1.2150 levels remains possible.

If the EURUSD pair starts to trade above the 1.2214 resistance level, a correction back towards the 1.2230 and 1.2248 level cannot be ruled out.

USDJPY Intraday Bullish Above 108.50 Level

The U.S dollar continues to strengthen against the Japanese yen, after better than expected economic data from the U.S economy further boosted the greenback. The USDJPY pair currently trades around the 108.70 level, after earlier moving to its highest level since early February, hitting 108.84. USDJPY traders are likely to follow the intraday direction of the U.S dollar index, and longer-dated U.S treasury yields.

The USDJPY pair is strongly bullish while trading above the 108.50 level, key resistance is now found at the 108.88 and 109.31 levels.

Should the USDJPY pair decline below 108.50 level, sellers will likely test towards the 107.92 and 107.45 support levels.

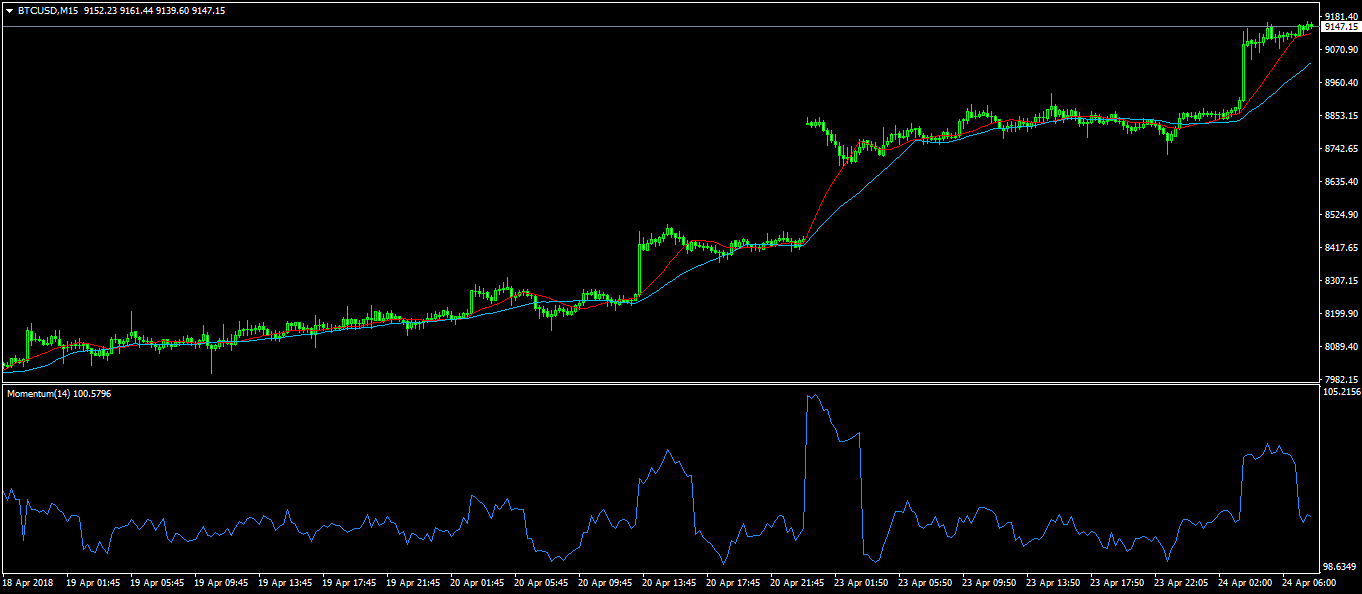

Bitcon Flies After Bullish Comments By Tim Draper

As one of the most successful venture capitalists in the world and the founder of Draper Associates based in Silicon Valley, Tim Draper is a highly influential figure within the finance sector. He was among the first investors in companies like Hotmail, Skype and Tesla and is now worth more than $1 billion.

Therefore, when Tim speaks, people listen.

Yesterday, in a debate titled “Bitcoin Is More Than a Bubble and Here to Stay,” he reiterated his bullish call on bitcoin, saying that the currency would hit $250,000 in the next four years.

He argued that bitcoin was probably the biggest invention in centuries because of its scalability. In years to come, he said, people will no longer need to carry fiat currencies, especially when they are travelling. He boldly called bitcoin bigger than both the Industrial Revolution and the internet.

Draper bought nearly 30,000 bitcoins back in 2014 when they were trading at less than $700. He is believed to still be holding all coins meaning his investment has soared. Draper also invested in multiple crypto-related companies such as BitPesa, Bancor, and Authenteq among others.

After his statement, the price of bitcoin surged, reaching a multi-weekly high of $9,200. Other currencies like ethereum, litecoin, and ripple too jumped to $678, $165, and $0.93.

The upward moves also followed the end of the American tax season. The downward momentum of the past few weeks came as most Americans sold their holdings to settle their capital gains taxes.

Bitcoin is now trading at $9150. This momentum could continue until the BTC/USD pair tests the $10,000 level.