Sample Category Title

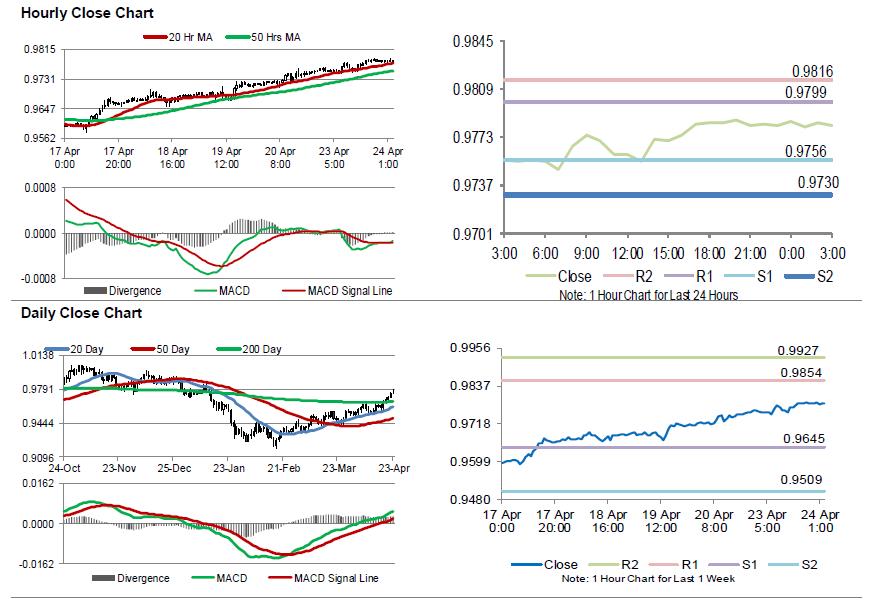

Swiss Franc Trading Flat In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.26% against the CHF and closed at 0.9782.

In economic news, Switzerland’s total sight deposits inched up to a level of CHF575.4 billion in the week ended 20 April, from CHF575.1 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9782, with the USD trading flat against the CHF from yesterday’s close.

The pair is expected to find support at 0.9756, and a fall through could take it to the next support level of 0.9730. The pair is expected to find its first resistance at 0.9799, and a rise through could take it to the next resistance level of 0.9816.

Going ahead, market participants would eye Switzerland’s trade balance data for March, due to release in a while.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

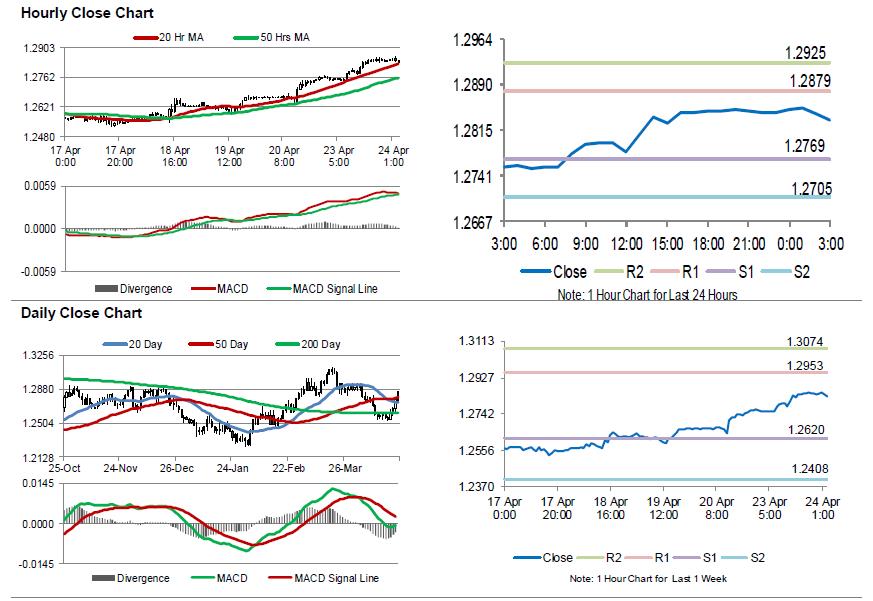

Loonie Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.69% against the CAD and closed at 1.2844.

In the Asian session, at GMT0300, the pair is trading at 1.2833, with the USD trading 0.09% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2769, and a fall through could take it to the next support level of 1.2705. The pair is expected to find its first resistance at 1.2879, and a rise through could take it to the next resistance level of 1.2925.

Amid no macroeconomic releases in Canada today, investor sentiment would be determined by global macroeconomic news.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

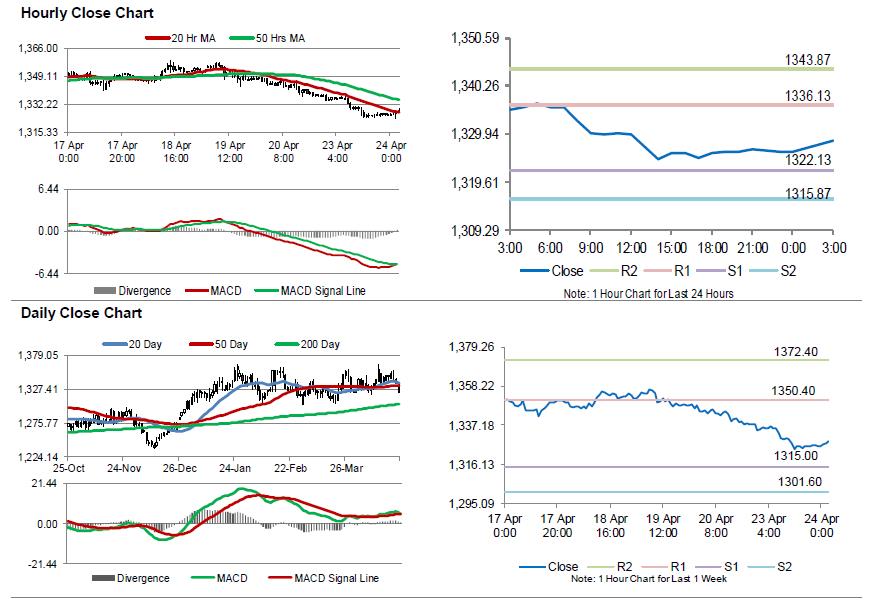

Gold: Yellow Metal Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, Gold declined 0.75% against the USD and closed at USD1326.30 per ounce, as a stronger greenback dented demand for the precious yellow metal.

In the Asian session, at GMT0300, the pair is trading at 1328.40, with gold trading 0.16% higher against the USD from yesterday’s close.

The pair is expected to find support at 1322.13, and a fall through could take it to the next support level of 1315.87. The pair is expected to find its first resistance at 1336.13, and a rise through could take it to the next resistance level of 1343.87.

The yellow metal is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

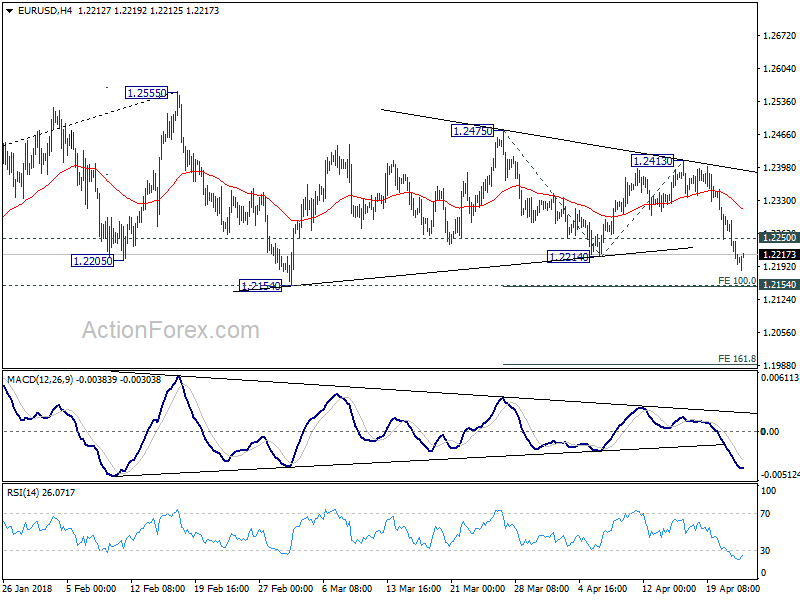

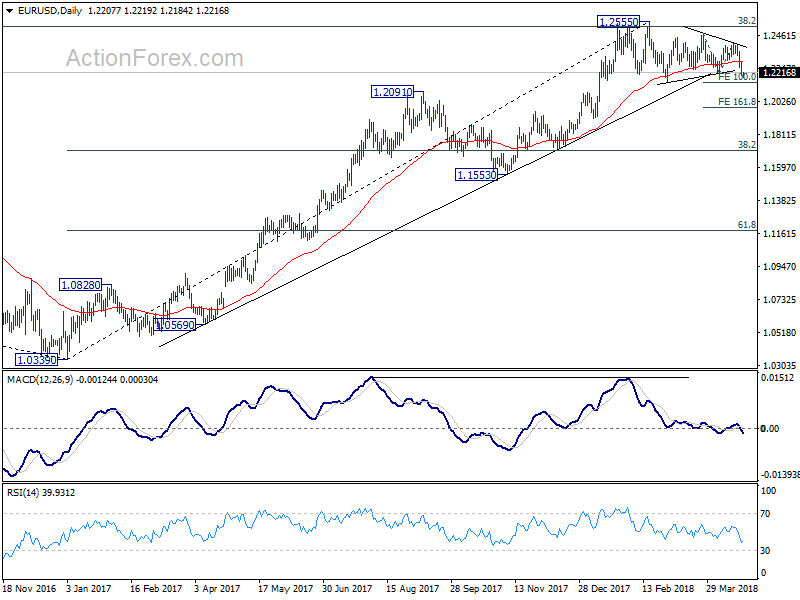

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2231 (R1) 1.2265; More....

EUR/USD drops to as low as 1.2184 so far and the break of 1.2214 support revived the case of medium term reversal. Intraday bias remains on the downside for 1.2514 support first. Decisive break there will confirm the bearish case and target 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991. On the upside, 1.2250 minor resistance will turn bias neutral first. But risk will now stay on the downside as long as 1.2413 resistance holds.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Dollar Pares Gain as Yield Hesitated ahead of 3%, German Ifo Watched

Dollar pares back some gains in Asian session today after yesterday's yield driven rally. 10 year yield hit as high as 2.990 during regular trading hour before closing at 2.973, up 0.022. However, that was below open at 2.975 and thus, showed a bit of hesitation ahead of 3% handle. US stocks closed mixed, with DOW down -0.06%, S&P 500 up 0.01% and NASDAQ down -0.25%. Weaker Yen helped lifted Nikkei as it's trading up 0.76% at the time of writing. China SSE is also recovery and is up 2% while Hong Kong HSI is up 1%.

In the currency markets, New Zealand Dollar is so far the weakest one for the week as selloff extends today. Yen is not much better as it's closely following as the second weakest. On the other hand, Swiss Franc is the second strongest one, as helped by EUR/CHF's rejection from 1.2 handle. But the Franc is losing momentum in Asian session as it turned mixed. We might see EUR/CHF revisit 1.2 again pretty soon.

Technically, EUR/USD's break of 1.2214 support now revived the case of medium term trend reversal. That also helped lifted Dollar index to 91, with medium term trend line resistance taken out. The firm break of 108 resistance in USD/JPY and 1.2814 in USD/CAD also aligned Dollar's near term bullish outlook with others. Yen would be a focus today as USD/JPY's yield drive rally might take other Yen crosses higher. In particular, EUR/JPY is having last week's high of 133.08 in sight.

Aussie spiked lower CPI, but quickly recovered

Australia CPI was unchanged at 1.9% yoy in Q1, below expectation of 2.0%. RBA trimmed mean CPI rose to 1.9% yoy, up from 1.8% yoy and beat expectation of 1.8% yoy. RBA weighted median CPI was unchanged at 2.0% yoy, beat expectation of 1.9% yoy. The Australian Bureau of Statistics noted in the release that "while the annual CPI rose 1.9 per cent, most East Coast cities have continued to experience annual inflation above 2.0 per cent, due in part to the strength in prices related to Housing and Food. Softer economic conditions in Darwin and Perth have resulted in annual inflation remaining subdued at 1.1 and 0.9 per cent respectively."

AUD/USD spiked lower to 0.7576 after the release but quickly recovered. Firstly, the decline is a bit stretched after AUD/USD fell for three days. Secondly, the CPI data just affirmed the case that RBA is in no rush to raise interest rate.

German Ifo expected to drop in April

German Ifo business climate will be a major focus for today. The headline Business climate index is expected to drop from 103.2 to 102.8 in April. Expectation index is expected to drop from 100.1 to 99.5 while current assessment index is expected to drop to from 106.5 to 106.0. Eurozone PMIs released yesterday were indeed quite solid. While they still indicate slight slowdown from stellar growth in Q4, the dip might not be as deep as some expected. And Eurozone could quickly regain momentum again in Q2. But after all, we're not expecting the data to chance ECB's cautious stance. More on ECB in ECB Preview: Caution over Recent Slowdown Won't Affect QE Schedule

Elsewhere

Swiss trade balance and UK public sector net borrowing will be featured in European session. US will release house price indices, new home sales and consumer confidence later in the day.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2173; (P) 1.2231 (R1) 1.2265; More....

EUR/USD drops to as low as 1.2184 so far and the break of 1.2214 support revived the case of medium term reversal. Intraday bias remains on the downside for 1.2514 support first. Decisive break there will confirm the bearish case and target 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991. On the upside, 1.2250 minor resistance will turn bias neutral first. But risk will now stay on the downside as long as 1.2413 resistance holds.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Y/Y Mar | 0.50% | 0.50% | 0.60% | 0.70% |

| 1:30 | AUD | CPI Q/Q Q1 | 0.40% | 0.50% | 0.60% | |

| 1:30 | AUD | CPI Y/Y Q1 | 1.90% | 2.00% | 1.90% | |

| 1:30 | AUD | CPI RBA Trimmed Mean Q/Q Q1 | 0.50% | 0.50% | 0.40% | |

| 1:30 | AUD | CPI RBA Trimmed Mean Y/Y Q1 | 1.90% | 1.80% | 1.80% | |

| 1:30 | AUD | CPI RBA Weighted Median Q/Q Q1 | 0.50% | 0.50% | 0.40% | 0.50% |

| 1:30 | AUD | CPI RBA Weighted Median Y/Y Q1 | 2.00% | 1.90% | 2.00% | |

| 6:00 | CHF | Trade Balance (CHF) Mar | 3.23B | 3.14B | ||

| 8:00 | EUR | German IFO Business Climate Apr | 102.8 | 103.2 | ||

| 8:00 | EUR | German IFO Expectations Apr | 99.5 | 100.1 | ||

| 8:00 | EUR | German IFO Current Assessment Apr | 106 | 106.5 | ||

| 8:30 | GBP | Public Sector Net Borrowing (GBP) Mar | 1.1B | -0.3B | ||

| 10:00 | GBP | CBI Trends Total Orders Apr | 4 | 4 | ||

| 13:00 | USD | House Price Index M/M Feb | 0.60% | 0.80% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Feb | 6.30% | 6.40% | ||

| 14:00 | USD | New Home Sales Mar | 625K | 618K | ||

| 14:00 | USD | Consumer Confidence Index Apr | 126 | 127.7 |

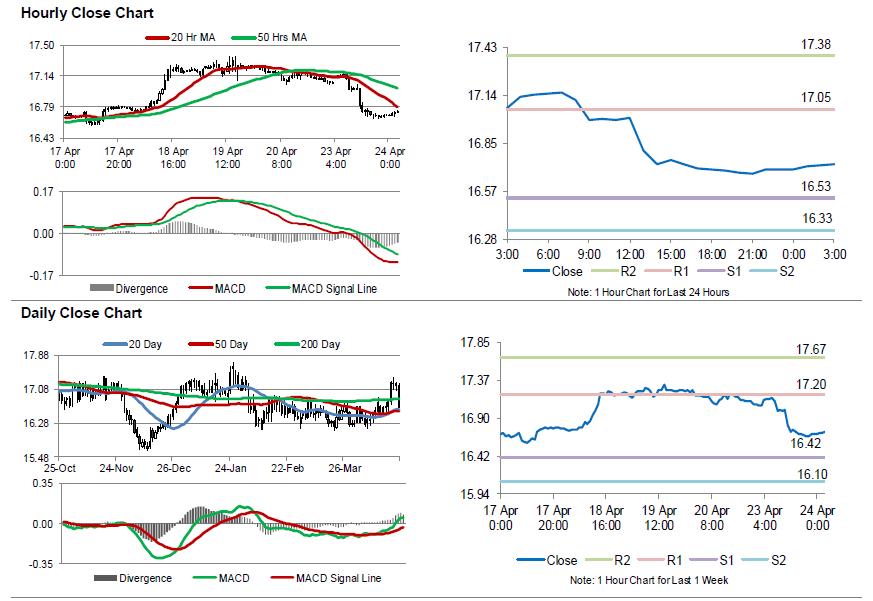

Silver: White Metal Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, Silver declined 2.17% against the USD and closed at USD16.70 per ounce, tracking losses in gold prices.

In the Asian session, at GMT0300, the pair is trading at 16.73, with silver trading 0.21% higher against the USD from yesterday’s close.

The pair is expected to find support at 16.53, and a fall through could take it to the next support level of 16.33. The pair is expected to find its first resistance at 17.05, and a rise through could take it to the next resistance level of 17.38.

The white metal is trading below its 20 Hr and 50 Hr moving averages.

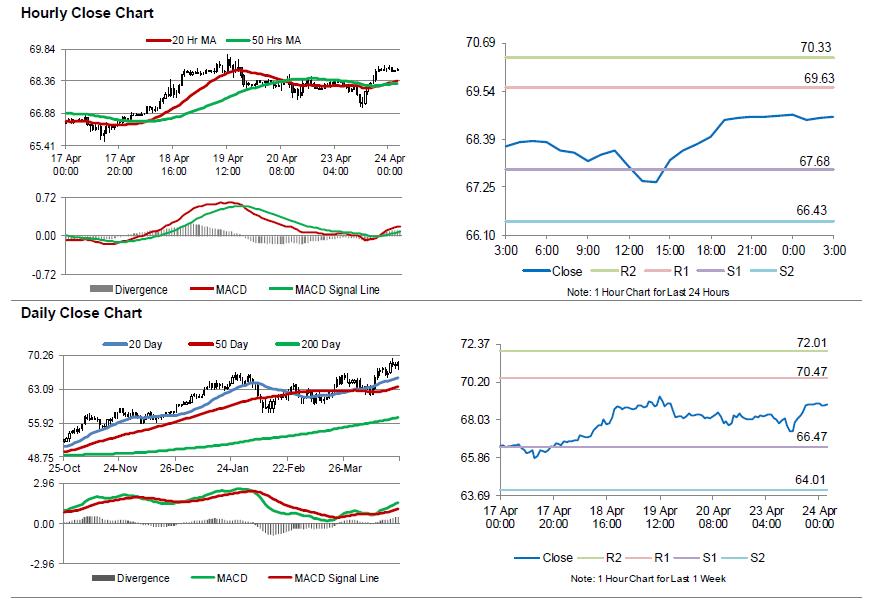

Crude Oil: Oil Trading Lower, Ahead Of API’s Weekly Crude Oil Inventories Data

For the 24 hours to 23:00 GMT, Crude Oil rose 0.98% against the USD and closed at USD68.96 per barrel, as an escalation in geopolitical tensions in the Middle East raised fears over potential supply disruptions. Additionally, fears over Iran sanctions further boosted prices.

In the Asian session, at GMT0300, the pair is trading at 68.92, with oil trading 0.06% lower against the USD from yesterday's close.

The pair is expected to find support at 67.68, and a fall through could take it to the next support level of 66.43. The pair is expected to find its first resistance at 69.63, and a rise through could take it to the next resistance level of 70.33.

Crude oil is trading above its 20 Hr and 50 Hr moving averages.

Dollar index broad medium term trend line resistance, pressing 91

Dollar index finally broke the medium falling trend line resistance after yesterday's solid rally. And focus is now on 91.01 support turned resistance. Firm break there will then be another sign of medium term reversal.

That is, the down trend from 103.82 has completed at 88.25, after hitting 50% retracement of 72.69 to 103.82, on bullish convergence condition in weekly MACD. Next hurdle will be 55 week EMA (now at 92.93). But we'd expect the rally to extend to 38.2% retracement of 103.82 to 88.25 at 94.19 at least. Ideally, is should be accompanied by a solid break of 3% in 10 year yield.

10 year yield showed hesitation ahead of 3%

10 year yield jumped to as high as 2.990 during regular trading hour overnight but struggled to extend further higher. TNX then closed at 2.973, up 0.22, but below open at 2.975. The development showed some hesitation ahead of key 3.000 level. It looks like the market might have to take a bit more time to digest the sharp move since last week.

But for now, there is no change in the near term up trend. And we'd expect a test the real key resistance zone soon. That is, 2014 high at 3.036 and 100% projection of 1.336 to 2.621 from 2.034 at 3.318. This is the key area that will define the long term trend.

ECB Preview: Caution over Recent Slowdown Won’t Affect QE Schedule

Despite expectations that the ECB would only announce adjustments on QE and interest rate in June the earliest, the upcoming meeting is not a non-event. Since the March meeting, Eurozone’s economic data have surprised to the downside. It would be of great interest to see the policymakers’ interpretation of the situation. All in all, we expect the members to view the first quarter slowdown as driven by temporary factors, e. g.: weather, which do not affect the monetary stance.

Headline HICP inflation rose to +1.3% y/y in March, from +1.1% in February. However, the final reading had not only missed consensus but was also revised lower from the flash reading. Core inflation, as +1% y/y, was unchanged from the disappointing flash reading released earlier this month. The softer reading was partly a result of weaker-than-expected positive effect of Easter.

Economic activities in the bloc also slowed. The final composite PMI fell -1.9 points to 55.2 in March, following a -1.7 points drop in February. The April report showed that the flash reading stayed unchanged this month. As such, the composite PMI now stands at 55.2, compared with a cyclical peak of 58.8 in January.

According to Markit/ IHS, “the Eurozone economy remained stuck in a lower gear in April, with business activity expanding at a rate unchanged on March, which had in turn been the slowest since the start of 2017. Growth has downshifted markedly since the peak at the start of the year, but importantly still remains robust”.

Separately, industrial production contracted -0.8% m/m in February, after a revised -0.6% drop in January. The slowdown was partly due to the severe weather condition in the first few months of the year. With a negative IP reading likely recorded in the first quarter of the year, after a +1.4% jump in 4Q17, the 1Q18 GDP growth would likely have eased from the previous quarter.

We do not expect the slowdown in economic growth during the inter-meeting period would affect the monetary policy outlook. Indeed, the members would still see the risks to growth “remain broadly balanced”.

Over the past weeks, ECB officials have downplayed the significance of the recent slowdown in economic activities. Couré affirmed that he was “not worried about Eurozone growth” while Praet noted that "weaker data has no reason to change ECB's assessment", although he acknowledged "some moderation of late, following several quarters of very strong growth". Villeroy also suggested that “recent growth data don't alter inflation outlook".

That said, we suspect the members might want to amend the language that “the strong cyclical momentum, underpinned by continued positive developments in sentiment indicators, could lead to further positive growth surprises in the near term".

On the monetary policy outlook, there are two issues in focus: updates on the future path of QE beyond September 2018 and interest rate guidance after the end QE. We do not foresee any change in the language at the upcoming meeting. It is more likely for the members to make such announcements in June, accompanied by the latest set of economic projections. There are risks for the announcements to be postponed to July, though.