Sample Category Title

German IFO, US Housing Data In Focus On Tuesday

A steady stream of economic data will make its way through the markets on Tuesday, with headline reports from Europe and the United States set to capture investors’ attention.

The economic calendar begins at 06:00 GMT with a report on Switzerland’s trade balance. The nation’s surplus is forecast to widen in March thanks to higher exports.

CESifo Group will report on German business confidence at 08:00 GMT. The business climate indicator for April is projected to weaken sharply to 102.6 from 114.7 the month before. The gauges for the current economic climate and future expectations are also expected to fall.

Shifting gears to New York, the S&0/Case-Shiller Home Prices Indices are scheduled for release at 13:00 GMT alongside the FHFA housing price index. Both indicators are expected to show positive growth in home prices.

Meanwhile, the Department of Commerce will issue its monthly report on new home sales, which is expected to show a gain of 1.9% month-on-month.

Wrapping up the data wire is the Federal Reserve Bank of Richmond, which is scheduled to release its manufacturing index at 14:00 GMT. The monthly gauge is expected to improve to 16 from a reading of 15 the month before.

Earlier in the day, the Reserve Bank of Australia reported headline inflation numbers that deviated slightly from met analysts’ forecasts. The consumer price index (CPI) rose 1.9% annually in the first quarter, unchanged from Q4. The Trimmed Mean CPI rose by a similar amount, compared with 1.8% the previous quarter.

In currency news, the US dollar surged on Monday to its highest level in over three months, as rising interest rates boosted the appeal of the greenback. The US dollar index (DXY) reached a high near 91.00 after gaining 0.7%.

EUR/USD

Europe’s common currency declined sharply on Monday, following the path of other dollar crosses. EUR/USD fell to the low 1.2200s and was last seen trading at 1.2210. The pair is down nearly 200 pips over the last three trading sessions. Immediate support is located at 1.2190. On the flipside, resistance is likely found at 1.2260.

GBP/USD

Cable’s meteoric decline continued Monday, with prices now falling more than 400 pips from last week’s multi-year high. At the time of writing, GBP/USD was trading at 1.3941, where it risks an even bigger pullback. The pair now faces immediate support at 1.3900. The initial resistance is found at 1.4130.

AUD/USD

Like other dollar pairs, AUD/USD crashed hard on Monday, falling to the low 0.7600 range. The Aussie is now trading at its lowest level since December. Immediate support levels include 0.7600 and 0.7565. On the opposite side of the ledger, resistance is located at 0.7640 and 0.7675.

Australian CPI Dampens Chances Of RBA Rate Hike

NZDUSD bucked the trend overnight, as most other currencies managed to retrace some of their declines against the USD. The pair hit fresh lows around the 0.71125 mark after it gapped lower through the 0.72000 level over the weekend. The strength in the USD is continuing to make its mark, but after large moves, a retracement could be on the cards. US Treasuries declined a little overnight, halting the slide in FX. WTI has moved back higher after declining early yesterday in response to US Rig count data on Friday. Equity Indices advanced overnight as the risk-on theme continues.

Australian Consumer Price Index (QoQ) (Q1) came in at 0.4% v an expected 0.5%, from 0.6% previously. RBA Trimmed Mean CPI (QoQ) (Q1) came in as expected at 0.5%, from a prior 0.4%. This data has been declining and continued to do so this quarter, showing some weakness in the economy, meaning the RBA will be unlikely to raise rates soon. AUDUSD bounced from a low of 0.75784 to 0.76132 in response, after sliding lower due to USD strength in the build-up to the release. However, AUD should weaken as rate hikes are delayed.

German Markit Manufacturing PMI (Apr) was 58.1 v an expected 57.5, from 58.2 previously. Markit Services PMI (Apr) was 54.1 v an expected 53.7, from 53.9 previously. Markit PMI Composite (Apr) was 55.3 v an expected 54.8, from 55.1 prior. The expectation was for a slip in these data points but, instead, the data beat expectations. The economists will be hoping that these data points can build a base here and recover after dipping for the last 3 months, albeit from high levels. EURUSD fell from a high of 1.22835 to a low of 1.22259 following this data release, as the USD strengthened.

Eurozone Markit Manufacturing PMI (Apr) was 56.0 v an expected 56.1, from 56.6 previously. Markit Services PMI (Apr) was 55.0 v an expected 54.6, from 54.9 previously. Markit PMI Composite (Apr) was 55.2 v an expected 54.9, from 55.2 prior. The manufacturing data continued to decline but Services and Composite beat expectations. This can potentially point to a bottom over the short term but US sanctions may have a knock-on effect for businesses that deal with Russian companies, e.g. Aluminium manufactures. EURGBP fell from 0.87620 to a low of 0.87444 after the data release hit the markets.

US Existing Home Sales (MoM) (Mar) was 5.60M v an expected 5.55M, against 5.54M previously. After reaching a seven-year high in November at 5.81M, this data point had slipped lower over the following two months, signalling a little softness in the sector, but had recovered somewhat last month. The recovery continued with this reading, as activity picks up heading into summer. USDJPY continued its rise as the data was released, moving from 108.366 to 108.454.

EURUSD is up 0.05% overnight, trading around 1.22151.

USDJPY is up 0.08% in early session trading at around 108.790.

GBPUSD is up 0.03% this morning, trading around 1.39441.

Gold is up 0.17% in early morning trading at around $1,326.70.

WTI is up 0.25% this morning, trading around $69.08.

German IFO Business Climate To Include Service Sector From Today

At 08:00 GMT, German IFO – Current Assessment (Apr) is expected to come in at 106.0 from 125.9 previously. IFO – Expectations (Apr) is expected to be 99.5 from 104.4 prior. IFO – Business Climate (Apr) is expected at 102.7 v 114.7 previously. This index will rebase today from the year 2005 to a base year of 2015. This means last month’s Business Climate reading of 114.7 will change to 103.2. This is to include the service sector for the first time, which makes up nearly 60% of GDP. The data is still expected to show a weakening business climate in Germany. This data cannot be ignored, as it surveys 7,000 businesses and is a leading indicator of economic direction. EUR crosses may see a spike in volatility should the actual data differ from the expected consensus.

At 13:00 GMT, US Housing Price Index (MoM) (Feb) is expected at 0.5% v 0.8% previously. This data is expected slip lower after a strong improvement last month. S&P/Case-Schiller Home Price Index (YoY) (Feb) is expected to come in at 6.3% against a prior 6.4%. This measure has been holding a steady improvement since the late 2014 low, with today’s data expected to be largely in line with expectations, if slightly weaker. USD crosses may be heavily traded as a result of this data.

At 14:00 GMT, US New Home Sales (MoM) (Mar) is expected to come in at 0.630M from 0.618M previously. New Home Sales Change (MoM) (Mar) is expected at 1.9% v -0.6% previously. On the back of strong Existing Home Sales data yesterday, Sales are expected to improve again after falling for three months since the November high. Further improvement in these figures shows a pickup in confidence in the US housing market. USD crosses may be heavily traded as a result of this data and could lead to further USD strength.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 150.94; (P) 151.29; (R1) 151.85; More...

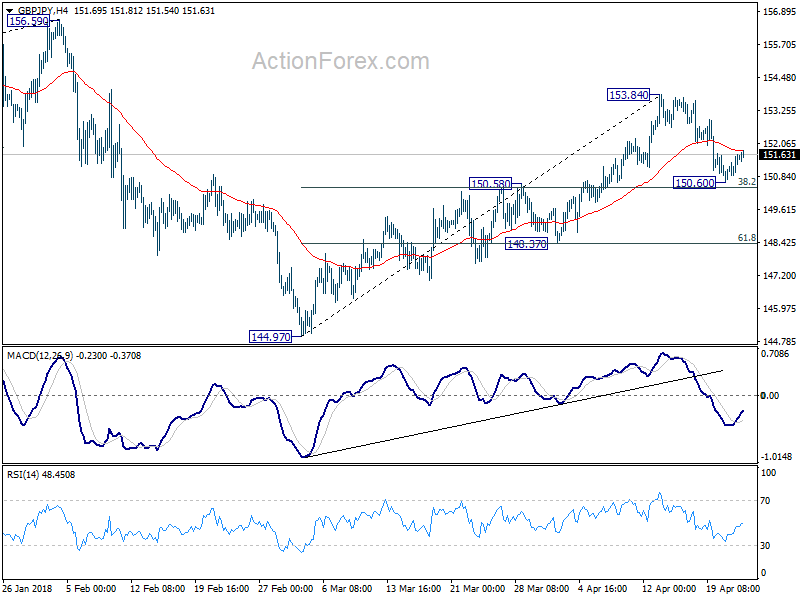

GBP/JPY recovered ahead of 150.48 resistance turned support and intraday bias is turned neutral first. We're holding on to the view that corrective rise from 144.97 should have completed at 153.84 already. Hence, another fall is expected in the cross. Break of 150.60 will target 148.37 support first. Break will bring retest of 144.97 low.

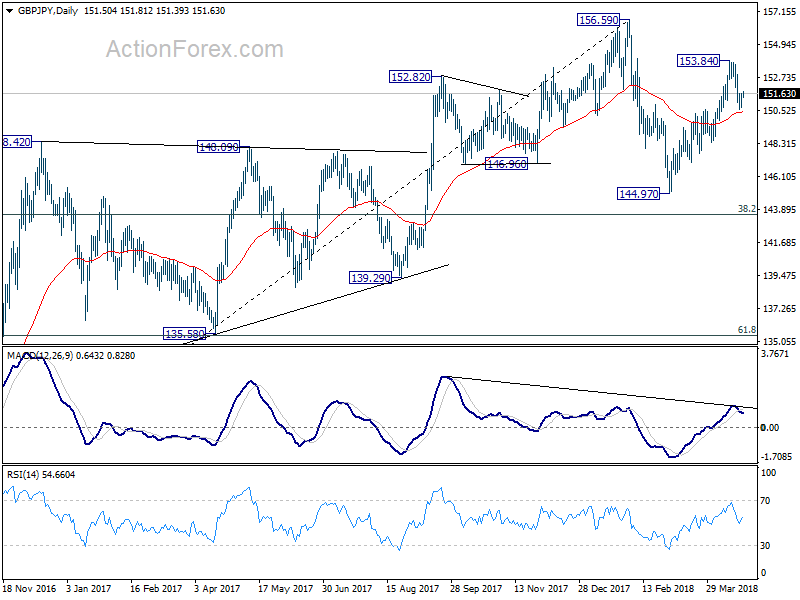

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

Investors No More Surprised By Earnings Surprises!

Wall Street ended mixed on Monday as tech stocks continued to lead the major indices. The S&P 500 finished flat at 2,670, with the 1.07% gain in materials offset by the 0.43% decline in the tech sector. The Dow Jones Industrial Average fell for a fourth straight day as the heavyweight Goldman Sachs declined 2.1%, while the Nasdaq was in the red for the third consecutive day.

So far, more than 80% of S&P 500 companies reporting actual results managed to beat earnings expectations; if this trend continues, it will be one of the best earning seasons ever. However, with markets not rewarding earning beats, the risk of a steep correction is high. When investors are no longer moved by positive surprises, it’s either because this positivity has been already priced in, or they believe the economy is due for a slowdown and will thus drag earnings in future quarters.

Previously, a rise in oil prices used to motivate investors as it indicated more demand and growth. Now, it’s becoming a source of concern, with prices hovering near a three-year high of $75. Investors are likely to question the implications of higher commodity prices on inflation and the wider economy.

U.S. 10-year yields will also be monitored closely this week, as they were less than 0.3 basis points from breaking the 3% benchmark yesterday. The 3% by itself is just a psychological level and not a significant threat, but if a break above leads to further selling in Treasury bonds, that’s going to be a serious warning signal for equity bulls. With a current world running on A.I and algorithms, a selloff may look ugly.

It was a steady trading session in currency markets early Tuesday. The dollar, which was influenced by the move in yields, paused after rallying over the past five trading days. After the correlation between interest rate differentials and currencies has been broken over the past couple of months, it appears to be working again. With the Fed continuing to be the most aggressive central bank, rate differentials are likely to widen further, thus providing a further boost to the USD. The dollar also benefited from easing geopolitical tensions and trade concerns. Unless President Trump surprises us with a new Tweet, we may see further greenback appreciation.

The economic calendar is relatively quiet today, but I’ll be interested in the German ifo Business Climate Index. The German Services PMI rose to 54.1 this month from 53.9 in March, ending two straight falls in business activity. The Manufacturing PMI fell by 0.1 to 58.1, however this was still better than the anticipated 57.5. The improved business activity may lead to a positive surprise in the ifo, however, due to changes in the calculation methodology, the number may vary widely from forecasts.

Xi Comments Spark Chatter China could adjust policy for further growth

General Trend:

- Nikkei rises as USD/JPY moved above ¥108

- Chinese equities outperform; Banks gain as PBoC seen as having more room to ease RRR

- Shanghai Composite property index rises over 3%

- Rusal rallies over 30% after US government said it could ease sanctions on the company

- Asian Aluminum producers decline following drop in prices after Rusal news

- Australian iron ore miner Fortescue drops over 3%; cautious on steel demand post Chinese Lunar New Year

- South Korean chipmaker Hynix declines over 3%, Q1 revs below ests amid mobile weakness

- Australia core CPI remains below RBA’s 2-3% target

- Aussie trades near 2018 low, later pares loss

- Australia and New Zealand markets closed for holiday on Wednesday April 25th

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.6%; closed +0.9%

- TOPIX Real Estate index +1.3%, Electric Appliances +1.2%

- Automakers gain as USD/JPY trades above ¥108.00

- Megabanks rise following gains in US 10-yr Treasury yield

- (JP) Japan Mar PPI Services y/y: 0.5% v 0.5%e

- Sharp [+1.6%], 6753.JP Sharp may report FY17/18 Net +50% y/y due to strong LCD sales; Rev +20% y/y to ¥2.5T – Nikkei

- (JP) Japan Econ Min Motegi: Japan/US minister meeting on new trade agreement framework to be after mid-June

- (JP) Japan Trade Min Seko: TPP 11 nations should prioritize ratifying deal

- (JP) Japan Finance Min Aso: Will make judgement on Fukuda after hearing both sides; not considering resigning

- (JP) Japan MoF sells ¥2.1T v ¥2.1T indicated in 0.10% (prior 0.10%) 2-yr JGBs; avg yield -0.134% v -0.160% prior; bid to cover 5.39x v 5.84x prior

Korea

- Kospi opened +0.2%

- Hynix [-1.5%], 000660.KR Reports Q1 (KRW) Net 3.12T v 3.3Te; Op 4.4T v 4.4Te; Rev 8.7T v 8.8Te

- USD/KRW Concerns over the possibility of capital outflow amid a widening gap between interest rates in Korea and the US are being eased by the strengthening of the won against the dollar - Korean press

China/Hong Kong

- Hang Seng opened +0.3%, Shanghai Composite +0.1%

- Hang Seng Property/Construction index +2.1%, Consumer Goods +1.9%, Industrials +1.4%, Financials +1.3%, Energy +1.2%

- (CN) China Political Bureau of the Communist Party of China (CPC) Central Committee (Politburo): China has seen a good start to its high-quality development – Xinhua

- (HK) Hong Kong 3-month HKD Hibor rises to highest level since 2008

- (CN) China has additional room to cut RRR and repay maturing MLF; China is likely to ease liquidity tension in week - China Securities Journal

- (CN) China banking and insurance regulator to conduct special investigations into the business activities of local asset management companies – press

- (CN) China PBoC sets yuan reference rate at 6.3229 v 6.3034 prior

- (CN) China PBoC Open Market Operation (OMO): Injects CNY30B in 7-day reverse repos v CNY80B prior; Net: injects CNY30B v CNY0B prior

- Rusal, [+33%], 486.HK US Treasury Sec Mnuchin: Weighing petition for sanction delisting

- (CN) China investors said to be finding it more difficult to finance offshore bond investment due to higher dollar funding costs and China govt crackdown on leverage, causing a slowdown in USD denominated debt - financial press

Australia/New Zealand

- ASX 200 opened -0.1%, closes +0.7%

- ASX 200 Consumer Discretionary index +1.7%, Utilities +1.4% Financials +1.2%, Energy +0.9%; Resources -1%

- (AU) RBA Assistant Gov Kent: Impact of interest only expires likely to be moderate, some borrowers may see genuine difficulty from I/O expiry

- Fortescue[-3.9%], FMG.AU Reports Q3 ore mined 41.6Mt v 44.7M y/y; total ore shipped 38.7Mt v 39Mte

- Beach Energy[+2.6%], BPT.AU Reports Q3 (A$) Rev 393M v 153M y/y

- (AU) AUSTRALIA Q1 CPI Q/Q: 0.4% V 0.5%E; Y/Y: 1.9% V 2.0%E; TRIMMED MEAN Q/Q: 0.5% V 0.5%E; Y/Y: 1.9% V 1.8%E

- Boral, [-9.4%], BLD.AU Q3 North America earnings below expectations, cites weather impact; Guides FY18 total EBITDA contribution from property at ~A$55-65M

- (NZ) New Zealand PM Arden: Very positive about prospects for FTA with EU, still work to be done

- (NZ) New Zealand sells NZ$100M in 6-month bills, avg yield 1.813%

Other Asia

- (ID) Indonesia Central Bank (BI) Gov Martowardojo: Intervened in FX market and bond market to help stabilize

North America

- US equity markets ended mostly lower: Dow -0.1%, S&P500 flat, Nasdaq -0.3%, Russell 2000 -0.1%

- S&P500 Energy +0.6%; Technology -0.4%

After market movers:

- Sanmina SANM, +16%, Reports Q2 $0.50 v $0.76 y/y, Rev $1.68B v $1.68B y/y

- Cadence Design Systems CDNS, +13%,Reports Q1 $0.40 v $0.38e, Rev $517M v $506Me

- Tivitv Health TVTY, -19%, Reports Q1 $0.49 v $0.49e, Rev $149.9M v $154Me

- Epizyme EPZM, -16%, FDA places partial clinical hold on tazemetostat trial, following a safety report of a pediatric patient who developed a secondary lymphoma

- GOOG, -1%, Reports Q1 ad $9.93* (ex $3.40 accounting adj) v $9.21e, Rev $24.9B (ex $6.29B TAC) v $24.2Be

- (US) Senate Foreign Relations Committee recommends approval of Pompeo nomination as Secretary of State

- (CA) Bank of Canada (BOC) Gov Poloz: protectionist trade policies remain biggest risk to the economic outlook; see some progress on inflation uncertainties

Europe

- (UK) House of Lords votes 316-245 to add an EU rights charter to UK law, another defeat for PM May; The amendment will be included in the bill when it goes back to the House of Commons

- (UK) UK Chancellor of Exchequer Hammond (Fin Min) said to accept proposal for GBP2 FOBT Limit - UK Press

- Michelin [ML.FR]: Reports Q1 Rev €5.22B v €5.23Be: affirms outlook

Levels as of 02:00ET

- Hang Seng +1.0%; Shanghai Composite +1.8%; Kospi -0.2%

- Equity Futures: S&P500 +0.3%; Nasdaq100 +0.2%, Dax +0.3%; FTSE100 +0.0%

- EUR 1.2219-1.2185; JPY 108.87-108.67; AUD 0.7614-0.7579;NZD 0.7157-0.7114

- Jun Gold +0.4% at $1,328/oz; Jun Crude Oil +0.7% at $69.14/brl; May Copper +0.8% at $3.13/lb

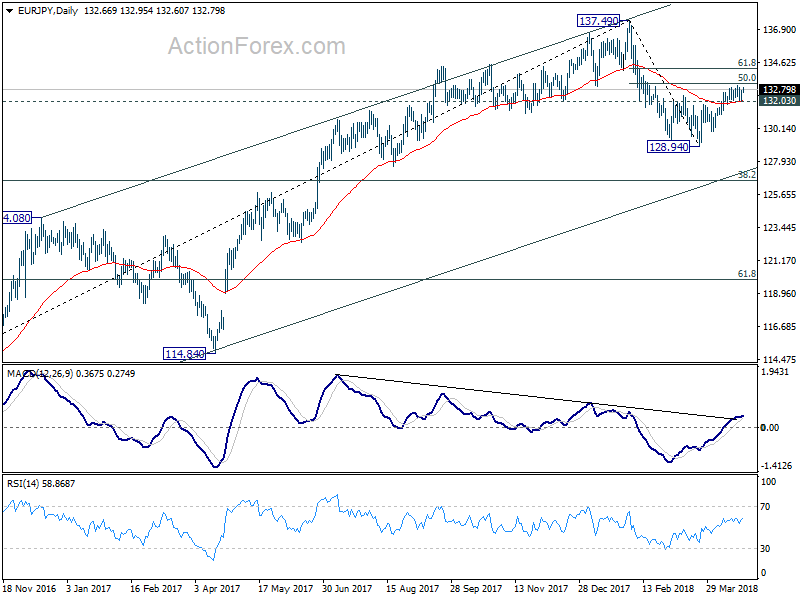

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.27; (P) 132.52; (R1) 132.95; More....

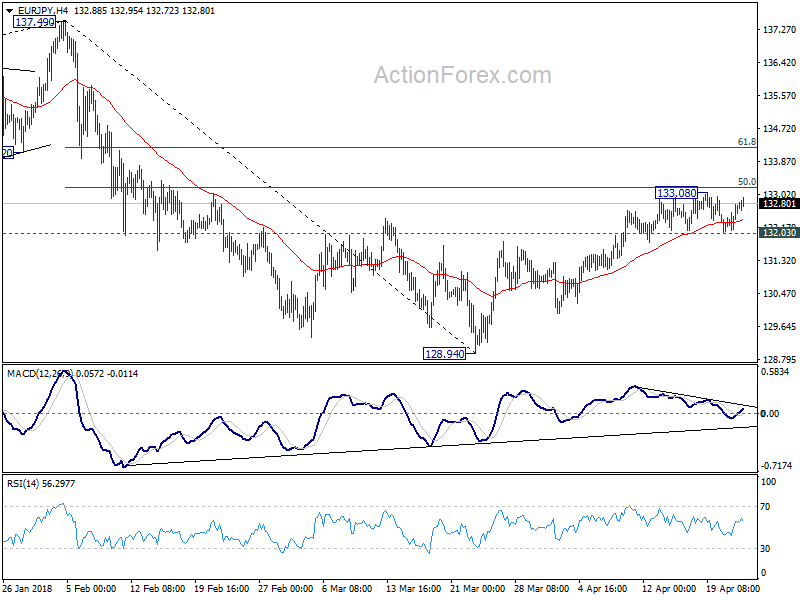

EUR/JPY recovered after drawing support from 4 hour 55 EMA and intraday bias is turned neutral. At this point, we're holding on to the view that rebound from 128.94 has completed at 133.08 already. Below 132.03 will target a test on 128.94 low. On the upside, above 133.08 will extend such rebound. But even in that case, upside will likely be limited by 61.8% retracement of 137.49 to 128.94 at 134.22.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. Strong support from 55 week EMA (now at 129.91) suggests that the first leg has completed at 128.94 already. Nonetheless, break of 137.49 is needed to confirm resumption of the rise from 109.03 (2016 low). Otherwise, we'd expect more corrective range trading, with risk of another fall to 38.2% retracement of 109.03 to 137.49 at 126.61 before completion.

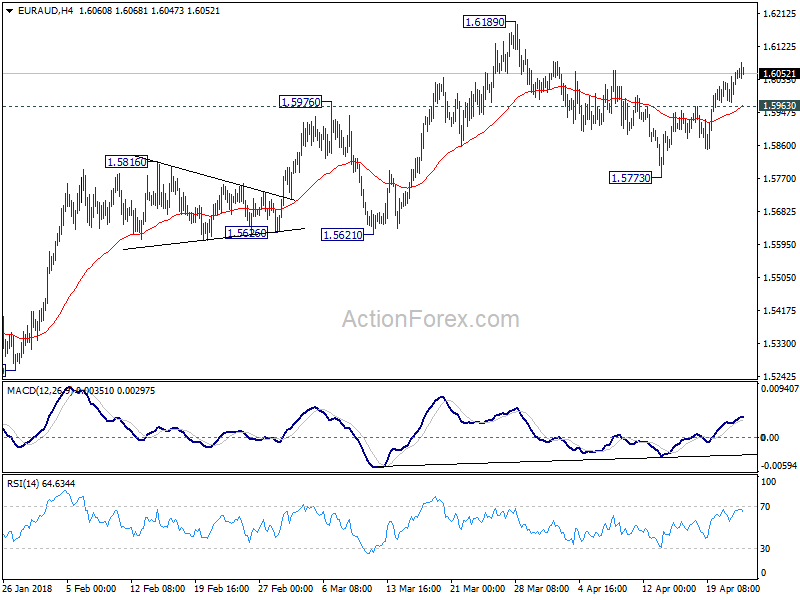

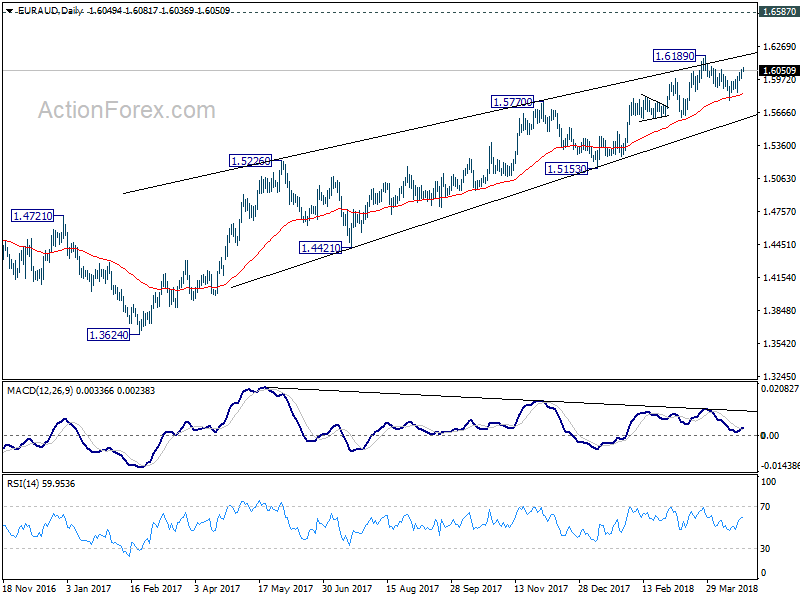

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5998; (P) 1.6029; (R1) 1.6083; More....

Break of 1.6059 resistance suggests that pull back from 1.6189 has completed at 1.5773 already. More importantly, larger rise from 1.3624 is likely still in progress. Intraday bias is now on the upside for 1.6189 first. Firm break there will target 1.6587 key resistance. On the downside, below 1.5963 minor support will turn focus back to 1.5773 instead.

In the bigger picture, while there is bearish divergence condition in daily MACD, there is no clear sign of reversal yet. EUR/AUD also drew strong support from 55 day EMA and rebounded. Current rally from 1.3624 could still extend to 1.6587 key resistance (2015 high). Nonetheless, we'd expect further loss of upside momentum, and strong resistance from 1.6587 to limit upside and bring reversal.

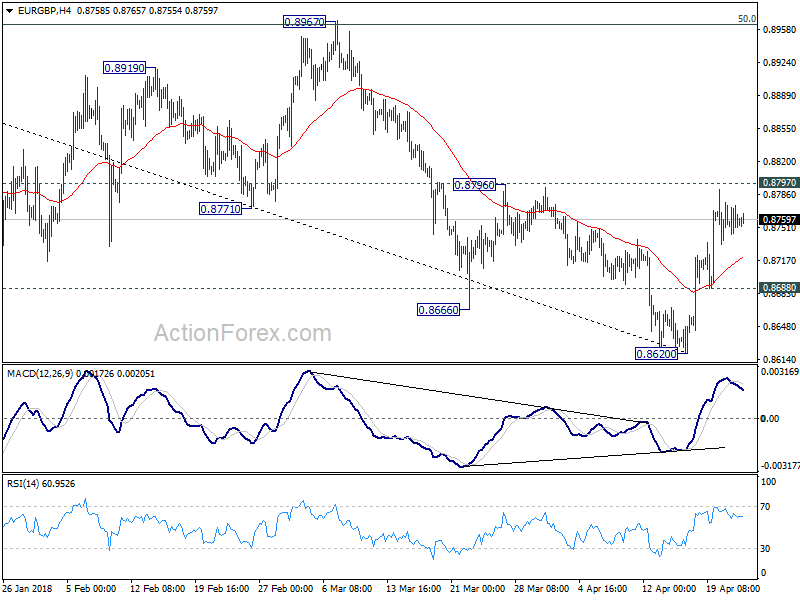

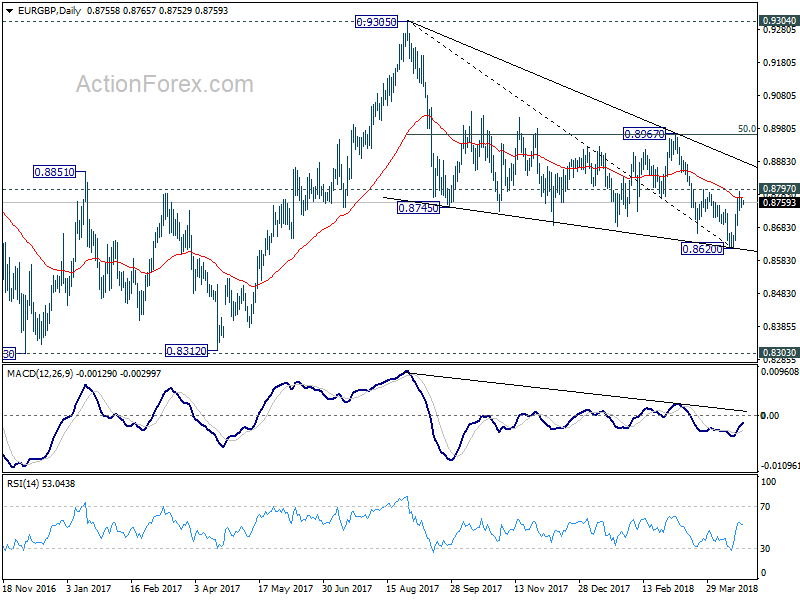

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8743; (P) 0.8758; (R1) 0.8773; More...

Intraday bias in EUR/GBP is turned neutral first with 4 hour MACD crossed below signal line. Further rise is expected as long as 0.8688 minor support holds. Break of 0.8797 will extend the rise from 0.8620 to key cluster resistance at 0.8967 (50% retracement of 0.9305 to 0.8620 at 0.8963) next. On the downside, break of 0.8688 minor support will dampen the bullish case and turn focus back to 0.8620 instead.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

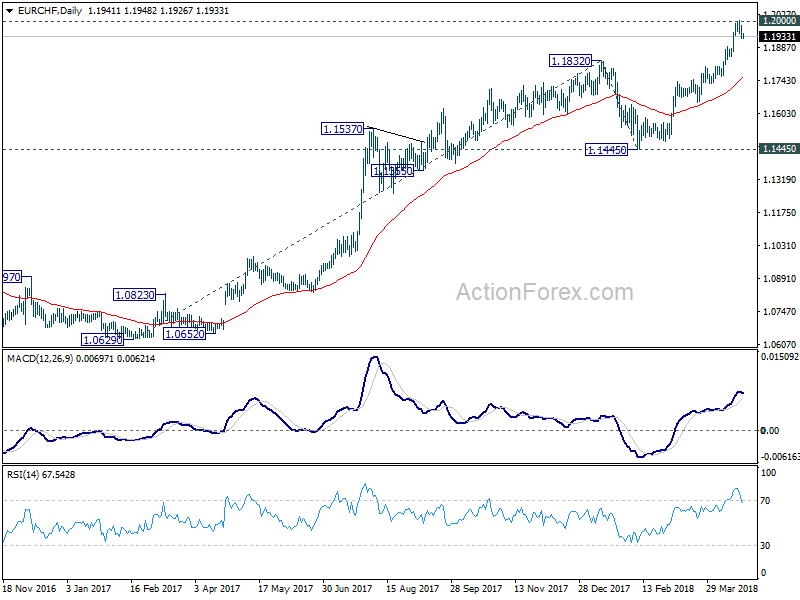

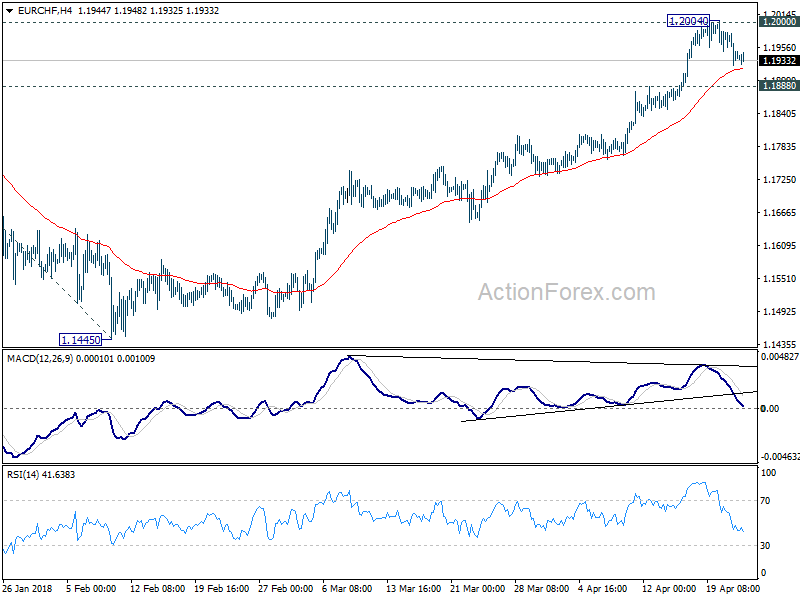

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1916; (P) 1.1950; (R1) 1.1973; More...

Intraday bias in EUR/CHF remains neutral at this point. Consolidation should be relatively brief as long as 1.1888 minor support holds and another rally is expected. Decisive break of 1.2 will pave the way to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. However, considering bearish divergence condition in 4 hour MACD, break of 1.1888 will indicate short term topping. In that case, deeper pull back would be seen back to 1.1445/1832 support zone.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2003 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2003 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next.