Sample Category Title

Market Morning Briefing: Euro Has Seen A Low Of 1.2185

STOCKS

Dow (24448.69, -0.058%) closed slightly higher after testing low of 24324. The 21-day MA near 24300 could be a decent near term support which could push the index a bit towards 24600-24700 in the next few sessions. Overall there could be some movement within 24700-24300 region for the coming sessions.

Dax (12572.39, +0.25%) has not been able to break above 12650 and while that holds, some sideways trade within 12650-12400 is possible. A break above 12650 would be necessary to take the index higher in the medium term.

22500 is a crucial resistance on Nikkei (22229.68, +0.64%) which could be tested in a few sessions. Thereafter a sharp fall can be expected back towards 22000 or lower.

Shanghai (3124.06, +1.83%) has risen sharply from levels near 3050 instead of breaking lower. If the rise sustains, the index could move higher towards 3150 or higher in the coming sessions.

Nifty (10584.70, +0.20%) was stable yesterday and is likely to spend some time ranged within 10650-10500 region.

COMMODITIES

Brent (74.20) has been trying to move up and could test 76 on the upside. 76 is likely to be a decent top for the medium term and the price could then be pushed off to lower levels of 72-71.

Nymex WTI (68.18) is stable after coming off from just above 69. But there could be some more scope towards 69.50-70.00 in the medium term with some interim corrective dips.

Gold (1325.20) dipped further and while below 1340, it could test 1315 before trying to move up again.

Copper (3.1150) is trading within the clear upward channel and could move up to test 3.1750 on the upside. On the weekly chart, 3.20 is an important resistance.

FOREX

Dollar index (90.907) has seen a high near 91.08, thereby breaching crucial resistances on 3 day candles and daily line chart near 90.50-90.75. We had said yesterday that the 90.5-91.0 zone is a crucial resistance zone, whose breach could imply a bullish Dollar in the medium term. We need to see if this breach sustains in the coming sessions or the Dollar Index stays below 91. As per our Apr ’18 Euro report, we currently prefer Dollar bearishness till May/Jun, after which it could turn bullish. Whether the downmove from 103 since Dec ’16 ends immediately, or later in this quarter, would have to be seen.

Euro (1.2207): Euro has seen a low of 1.2185 and is testing the 21 week moving average on weekly line chart, which could provide some support. As mentioned yesterday, 1.225-1.215 is a crucial support zone for the Euro and a break below 1.215 could prove to be seriously bearish. However, our Apr ’18 Euro report prefers some bullishness for the Euro till May/Jun and bearishness after that. The upmove from 1.045 since Dec ’16 could start seeing a significant correction later this quarter.

Dollar Yen (108.74) : Amongst the 2 possibilities we mentioned yesterday, the first one ie a breach past 107.8 to target 21 week moving average near 108.88 (now, 108.92) has happened. We need to see if the 21 WMA provides resistance or the Dollar Yen rises past it to target 110. Upside could be restricted by 110 in the short term, after which it should turn bearish.

Euro Yen (132.75) has risen slightly from yesterday’s levels near 132.3 due to the Dollar Yen’s bullishness. It could however continue to stay below 133 as the Euro sees a possible dip towards 1.215 and the Dollar Yen stays below 109. A break below support on daily candles (near 132.5) could happen if Euro breaks below 1.215.

Pound (1.3938) after breaking support on daily line chart near 1.408 yesterday has, as per our expectation, dipped further and could test crucial long term support level near 1.385 on weekly line chart in the next 1-2 sessions. If this support also breaks, Pound could turn very bearish in the medium term. However, if it holds, we could see a rally towards long term resistance level of 1.46 in the weeks ahead.

Dollar Rupee (66.48): Overbought at current levels. Possible Resistance at 66.30-50. Might dip to 66.30 or maximum 66.00.

INTEREST RATES

The US 10 Year Yield almost touched the psychologically important 3% level yesterday as US yields continued their rally after the last two weeks’ data releases indicated continued growth in the US economy. In the last 2 weeks the following releases had all come out positive: Industrial Production, Capacity Utilization, US Retail Sales data, unemployment claims data and the Fed minutes. In addition, Crude’s rise towards 74 has increased inflation expectations and is fuelling the rise in US yields. The US treasury is auctioning almost 370 billion dollars worth of notes and short term bonds this week – this could further raise yields in the short term.

US 10 Yr Yield (2.96%), 30 Yr (3.13%), 5 Yr (2.8087%), 2 Yr (2.474%):

The US 2 year yield (2.47%), after having reached its highest levels since 2008 could move towards 2.50% and then see a dip towards 2.40%-2.35% soon.

The 10 Year yield (2.96%), as we predicted yesterday, saw a high near 2.99%, thereby almost touching the 3% mark. However it has come off from those levels and is trading near 2.96% currently. It had breached resistance near 2.92% on medium term chart day before yesterday and if it doesn’t dip back below that resistance, it could breach the 3% level soon.

The 30 yr yield has dipped slightly after seeing a high near 3.17% yesterday. A breach of 3% on the 10 year yield could correspond with a breach of 3.2% by the 30 year yield (seen as horizontal resistance on short term chart).

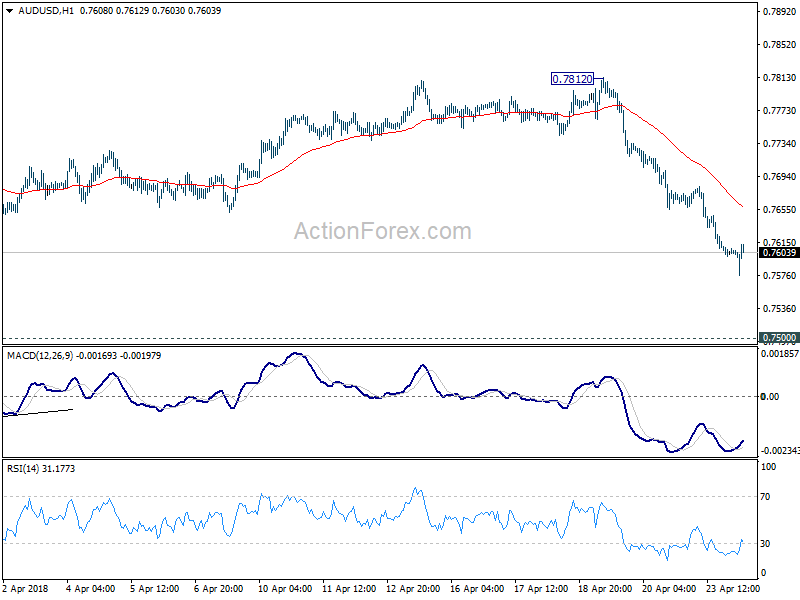

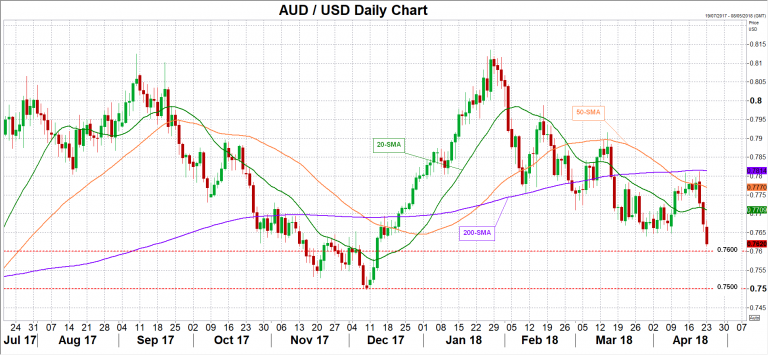

AUDUSD spikes lower after Australia CPI miss, but quickly recovered

Australia CPI was unchanged at 1.9% yoy in Q1, below expectation of 2.0%. RBA trimmed mean CPI rose to 1.9% yoy, up from 1.8% yoy and beat expectation of 1.8% yoy. RBA weighted median CPI was unchanged at 2.0% yoy, beat expectation of 1.9% yoy.

The Australian Bureau of Statistics noted in the release that "while the annual CPI rose 1.9 per cent, most East Coast cities have continued to experience annual inflation above 2.0 per cent, due in part to the strength in prices related to Housing and Food. Softer economic conditions in Darwin and Perth have resulted in annual inflation remaining subdued at 1.1 and 0.9 per cent respectively."

AUD/USD spiked lower to 0.7576 after the release but quickly recovered. Firstly, the decline is a bit stretched after AUD/USD fell for three days. Secondly, the CPI data just affirmed the case that RBA is in no rush to raise interest rate. For now, AUD/USD is on track for 0.7500 key support level in near term.

Gold Price Broke Key Supports Near $1,335

Key Highlights

- Gold price started a downside move from the $1,355 level against the US Dollar.

- There was a break below two bullish trend lines at $1,345 and $1,335 on the 4-hours chart of XAU/USD.

- The US Existing Home sales in March 2018 grew 1.1%, more than the +0.2% forecast.

- Today, the US New Home Sales report for March 2018 will be released, which is forecasted to post a 1.9% rise in sales.

Gold Price Technical Analysis

There was a major top formed above the $1,355 level in gold price against the US Dollar. The price declined sharply and broke many important supports near $1,335 to move into a bearish zone.

Looking at the 4-hours chart, there were back to back bearish candles from the $1,354 swing high. The price declined and broke the 50% Fib retracement level of the last wave from the $1,319 low to $1,365 high.

More importantly, there was a break below two bullish trend lines at $1,345 and $1,335 on the 4-hours chart of XAU/USD. It also declined below $1,330, and the 200 simple moving average (green, 4-hour) and the 100 simple moving average (red, 4-hour).

These are negative signs, which could ignite more declines in Gold price in the near term. The next stop for sellers could be near the 1.236 Fib extension of the last wave from the $1,319 low to $1,365 high.

On the upside, the broken support near $1,335 and the 200 simple moving average (green, 4-hour) will most likely act as resistances if the price corrects higher.

Recently, the US Existing Home Sales report for March 2018 was released by the National Association of Realtors. The market was looking for a 0.2% rise in sales compared with the previous month.

The actual result was better as there was a rise of 1.1% in sales to a seasonally adjusted annual rate of 5.60 million. However, the current reading was less than the last +3.0%.

Overall, gold price has moved into a bearish zone and it may perhaps decline further towards the $1,310 level.

Economic Releases to Watch Today

- German IFO Business Climate Index for April 2018 – Forecast 102.6, versus 114.7 previous.

- US New Home Sales for March 2018 (MoM) – Forecast +1.9% versus -0.6% previous.

USD Back With A Vengeance

USD Back with a vengeance.

The USD has put on a compelling show overnight as the stars align on the back of higher US Yields and a considerable reduction in the US dollars geopolitical risk premium as an outwardly calmer mood surrounding trade and geopolitical risk takes hold.

While its a bit early for investors to pack in the consensus short dollar view, the weaker shorts are indeed getting pared as the USD is showing some vigour tracking US Bond yields higher. Without question, this Friday’s US GDP data will be crucial for an extension of the current dollar move as US economic strength in the face of synchronised economic slowdowns in both China and Europe are playing into the resurgent US dollar hand.

Also, the rising yields are negatively impacting equity sentiment as US markets extend their retreat. The Bond markets are now within a whisker of testing the critical technical and psychological 3% ten-year level. With higher oil prices in addition to tax reform bump factoring into he inflation calculus, rates could reprice higher to 3.25 %( 10 UST) driven by the prospects of higher inflation above-potential growth and a worsening supply-demand dynamic.

If 3 % is indeed a line in the sand for equity investors, we should expect increasing sector rotation out of equities into bond markets which should accelerate significantly on the 3% break.

Oil Markets

Oil prices rebounded from an early NY session skid as investors continue to focus on the main issues at hand, Iran sanctions amidst falling US crude inventories. Genscape showed a decline in Oil supply stocks at the Cushing, Oklahoma storage hub which overshadowed Friday’s increase in the Baker Hughes US crude oil drilling rig cont .

News broke early that Iran’s oil minister Bijan Zanganeh said there would be no need to extend a pact between the Organization of the Petroleum Exporting Countries and non-OPEC producers if oil prices strengthened, the ministry’s official website SHANA reported. The reports caused some interday long positions to buckle but the news was quickly digested as little more than wishful thinking, and institutional investors bid back with a vengeance taking Oil prices to 3-year highs.

Also, the apparent easing of Russia aluminium sanctions saw the metal fall over 10% in early NY headlines which triggered hard commodities to crumble across the board and dragged oil lower in the wake.

But the stay long oil narrative continues to echo in dealing rooms as traders are content to play the waiting game for probably oil sanctions against Iran, which could push oil prices up as much as $5- per barrel. Also, factor in last weeks Saudi jawboning targetting $80 or $ 100 per barrel it suggests prices will remain firm for the foreseeable future and should continue to gravitate higher.

Gold Markets

Gold prices cratered as rising US Bond Yields, and a firming US dollar took the shine off gold. But Gold markets are indeed at a bit of an inflexion point given that rising inflationary pressures driven by higher oil prices could lead to a global inflation spark which could be supportive for Gold prices. However, while traders try to figure out if this current USD dollar rally is ” Live or Memorex.” Gold investors will remain perched in a very precarious position awaiting clearer signals on the USD dollar front.

Currency Markets

Higher US yields have played a role in supporting the USD as surging oil prices make for a compelling inflationary storyline.

With both the BoE and BoC waxing dovish, the markets are betting that ECB will kick the policy can further down the road in an attempt to stall for more time stall for more time – the press conferences should be reasonably quite also.

There has been a reduction in the Trump USD dollar risk premium after Deputy Attorney General Rod Rosenstein told President Donald Trump last week that he is not a target of any part of Special Counsel Robert Mueller’s investigation or the probe into his long-time lawyer, Michael Cohen, according to several people familiar with the matter.

The improving geopolitical landscape in Korea and no further escalation in Syria has removed some geopolitical risk premia from the Dollar.

The Euro and Pound

The Euro and Pound are getting hammered due to an unwinding of consensus positioning. Similar to the BOE view softer EU economic data suggests the ECB will likely to kick the can down the road on the policy front, the Euro prints near 1.2200. But make no mistake we are some severe levels as this 1.2200-1.2150 level has held stable dating back to Mid Jan. But the current momentum indicates the markets could be poised to break lower

The Japanese Yen

Kuroda has stuck to his well worn dovish script overnight but this is old news, and the USDJPY continues to climb due to the US dollar bid while triggers some stops along the way above 108.30 level.

The Australian Dollar

The Australian dollar is getting hammered by the abrupt rise in US Treasury Yields. But there are other negative implications for the Aussie brewing on the back burner.

The recent downturn in global economic data is suggesting we are moving from a state of global synchronised growth to a synchronised slowdown.

There been increasing maker chatter about an economic slowdown in China which is being viewed USD positive on the surface as Chinese authorities may shift towards weaker yuan policy to buffer the negative growth( Q2 GDP) impact from deleveraging and trade wars with the US.

The Malaysian Ringgit

Local Bonds continued to sell off throughout yesterday session around weakening risk sentiment of the upcoming election and rising US Treasury yields. The Malaysian bond market look poised to continue declining ahead of the vote and even more so as US yields look poised to move even higher. Liquidy has been quite weak in both Bond and Currency markets suggesting that investors are taking to the sidelines

Despite the long-term supportive underlying structure from higher oil prices, the short-term election drivers and a broadly stronger USD will continue to put downward pressure on the MYR near term, and we could see a test of the critical 3.90 level.

Eco Data 4/24/18

[php_everywhere instance="1"]

Gold Slumps as Treasury Bills Hit 3 Percent

Gold has recorded sharp losses in the Monday session. In the North American session, the spot price for an ounce of gold is $1323.67, down 0.93% on the day. In economic news, Existing Home Sales improved to 5.60 million, above the estimate of 5.55 million. This marked a 4-month high. On Tuesday, the key event is CB Consumer Confidence.

What’s good for the greenback is often bad news for gold, and this has been the case on Monday. The US dollar has posted road gains to start the week, courtesy of US Treasury bills, which pushed above the 3-percent threshold for the first time since January 2014. With treasury spreads widening over European and Japanese yields, investors have propped up the greenback, and gold prices have slipped to their lowest level in 2 weeks.

The stock markets have been rocked by volatility in recent weeks, in response to tariffs which the US and China have imposed on the other. US President Trump has threatened to slap tariffs on up to $150 billion on Chinese goods, and China has promised to respond with heavy tariffs on US imports. The escalating crisis has raised fears that a trade war between the two economic giants could slow down Chinese growth and trigger a global recession. However, US Treasury Secretary Steven Mnuchin sought to lower the rhetoric on the weekend, saying that he was considering a trip to China, adding he was “cautiously optimistic” that the two sides could resolve the trade dispute. If the US and China can patch up their differences, the safe-haven Japanese currency could continue to lose ground.

Pound Slides to 5-Week Low as T-Bills Boost Dollar

The British pound has lost ground in the Monday session, as the pound’s woes continue after sharp losses last week. In North American trade, GBP/USD is trading at 1.3947, down 0.40% on the day. On the release front, there are no British events on the schedule. In the US, Existing Home Sales improved to 5.60 million, beating the estimate of 5.55 million. This marked a 4-month high. On Tuesday, the UK releases Public Sector Net Borrowing and the US publishes CB Consumer Confidence.

The US dollar has posted broad gains to start the week, sending the pound lower for a fifth straight day. GBP/USD slipped 1.6% last week, and the pound is again below the symbolic 1.40 line. The greenback received a boost on Monday from US Treasury bills, which punched past the 3-percent threshold for the first time since January 2014. With treasury spreads widening over European and Japanese yields, investors have propped up the greenback.

Is the US-China trade war headed to a trade truce? The markets have been marked by volatility in recent weeks, in response to tariffs which the US and China have imposed on the other. US President Trump has threatened to slap tariffs on up to $150 billion on Chinese goods, and China has promised to respond with heavy tariffs on US imports. The escalating crisis has raised fears that a trade war between the two economic giants could slow down Chinese growth and trigger a global recession. However, US Treasury Secretary Steven Mnuchin sought to lower the rhetoric on the weekend, saying that he was considering a trip to China, adding he was “cautiously optimistic” that the two sides could resolve the trade dispute. If the US and China can patch up their differences, the safe-haven Japanese currency could continue to lose ground.

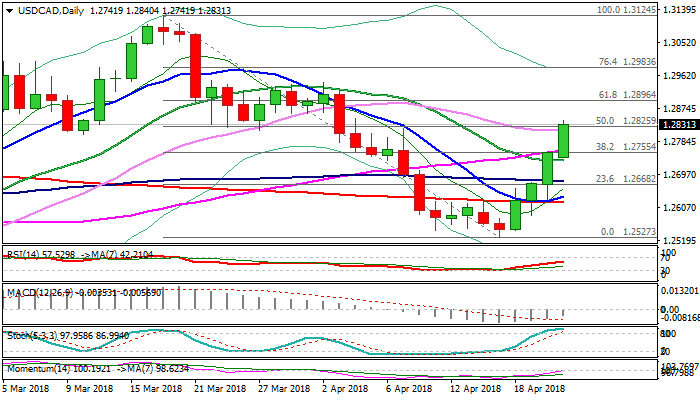

USDCAD – Extended Recovery Pressures Daily Cloud Top

The pair remains firmly in green for the fourth straight day and hit new recovery high at 1.2840 (the highest since 04 Apr).

Fresh extension higher on Monday marked over 50% retracement of 1.3124/1.2527 bear-leg) and pressures key barrier at 1.2875 (top of widening daily cloud).

Canadian dollar was hit by downbeat data on Friday, while the greenback received additional support from better than expected US existing home sales on Monday.

Daily MA’s turned to bullish setup while momentum is breaking into positive territory, however, strongly overbought slow stochastic on daily chart warns that bulls may hesitate at daily cloud top.

Corrective dips could be seen as positioning for fresh upside and should be ideally contained by 20SMA (1.2732).

Firm break through cloud top at 1.2875 and Fibo 61.8% of 1.3124/1.2527 at 1.2896, would spark fresh acceleration higher and expose psychological 1.30 barrier.

Res: 1.2875; 1.2896; 1.2943; 1.3000

Sup: 1.2813; 1.2761; 1.2732; 1.2678

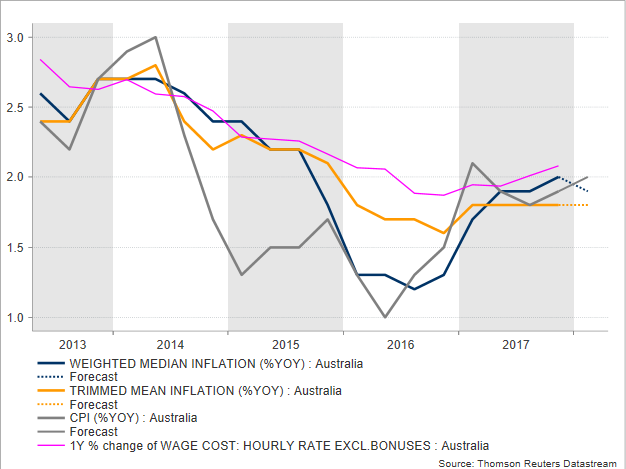

Australian Core CPI to Undershoot RBA’s Inflation Target

Inflation in Australia failed to meet the Reserve Bank of Australia’s price target in the fourth quarter of 2017, similar to many other major economies, and updates on consumer prices adjusted for volatility early on Tuesday are expected to say the same story, kicking any hopes of a rate hike further into the future.

At 0130 GMT on Tuesday, data prepared by the Australian Bureau of Statistics are expected to show that the headline Consumer Price Index (CPI) has ticked up to 2.0% on a yearly basis in the first quarter of 2018, compared to 1.9% seen in the previous quarter. This, however, could likely be attributed to seasonal effects such as price rises in large seasonal components like pharmaceuticals and educational fees, rather than to permanent factors. Besides, the core measures, which trim for volatility and are paramount for monetary policy are said to have clocked in below the RBA’s target range of 2-3.0%. Particularly the weighted mean CPI is anticipated to inch down to 1.9% y/y after touching a 2.0% growth in Q4 2017, while the trimmed mean CPI is anticipated to remain unchanged at 1.8% y/y.

On April 3, RBA policymakers decided to maintain interest rates at a record low of 1.5% for the 18th consecutive time. Although they acknowledged improvements in the labour market, saying that the unemployment rate has “declined over the past year”, they admitted that household consumption remains a source of uncertainty as the meeting’s minutes indicated. Retail sales, a proxy for household spending, managed to gain momentum at the end of 2017 but wage growth continued to rise only modestly, hinting that inflationary pressures are unlikely to rise much at times when households are struggling to repay their overloaded debt obligations. Still, they remained hopeful that the unemployment rate could drop gradually, and wages could pick up steam as companies have already started facing difficulties finding skilled workers.

Besides the above, external risks to the economy also support no change in policy by the Bank. The US trade protectionism and specifically the US standoff with China raised fears for Australian exporters who are largely dependent on Chinese sales, despite their exemptions from aluminum and steel US import tariffs. While both countries have recently shown the willingness to resolve their differences through dialogue, a failure to reach an agreement on the trade front could find both countries activating their import tariffs. Under this scenario, economies linked to the Chinese economy such as Australia could see their terms of trade narrowing. Moreover, apart from trade politics, US monetary strategy seems to be a headache to the RBA given that rising US interest rates force Australian banks to raise their mortgage rates, even though the country faces a mounting debt burden.

Currently, the markets are pricing in a 0.41% probability for a rate hike in May, while they only see a 25-basis point increase only by mid-2019. Should Tuesday’s inflation readings surprise to the upside, this probability could increase, and investors could turn more optimistic on future monetary tightening, pushing aussie/dollar probably up to the 20-day SMA which currently stands at 0.7703. A bigger positive surprise could drive the market even higher towards the 50-day SMA at 0.7770, paring most of the losses made over the past three days. On the other hand, a worse-than-expected report could add further pressure to the currency, leading aussie/dollar down to the 0.7600 and 0.7500 psychological levels. Note that traders are currently betting a 25 basis point increase in rates coming by the mid-2019.

Yen Slips to 10-Week Low as Trade War Rhetoric Softens

USD/JPY has posted strong gains in the Monday session. In North American trade, USD/JPY is trading at 108.57, up 0.86% on the day. On the release front, Japanese Flash Manufacturing PMI inched up to 53.3, just shy of the estimate of 53.4 points. Later in the day, Japan releases Services Producer Price Index, which is expected to drop to 0.5%. In the US, Existing Home Sales improved to 5.60 million, beating the estimate of 5.55 million. This marked a 4-month high. On Tuesday, the Bank of Japan releases Core CPI and the US publishes CB Consumer Confidence.

Is the US-China trade war headed to a trade truce? The markets have been marked by volatility in recent weeks, in response to tariffs which the US and China have imposed on the other. US President Trump has threatened to slap tariffs on up to $150 billion on Chinese goods, and China has promised to respond with heavy tariffs on US imports. The escalating crisis has raised fears that a trade war between the two economic giants could slow down Chinese growth and trigger a global recession. However, US Treasury Secretary Steven Mnuchin sought to lower the rhetoric on the weekend, saying that he was considering a trip to China, adding he was “cautiously optimistic” that the two sides could resolve the trade dispute. If the US and China can patch up their differences, the safe-haven Japanese currency could continue to lose ground.

Japan’s economy continues to grow and key indicators are generally performing well. At the same time, inflation has lagged and remains well below the Bank of Japan’s target of around 2 percent. The markets have been speculating that stronger economic conditions might cause the BoJ to re-examine its ultra-accommodative monetary policy. However, on Monday, BoJ Governor Haruhiko Kuroda poured cold water over such sentiment, stating that in order to reach its inflation target, “the Bank of Japan must continue very strong accommodative monetary policy for some time”. The BoJ will issue an inflation forecast on Friday, with the bank expected to reiterate that the inflation target will be met in fiscal year 2019-2020. Kuroda’s dovish statement can be seen as an attempt to curb volatility in the yen after the inflation forecast is released.