Sample Category Title

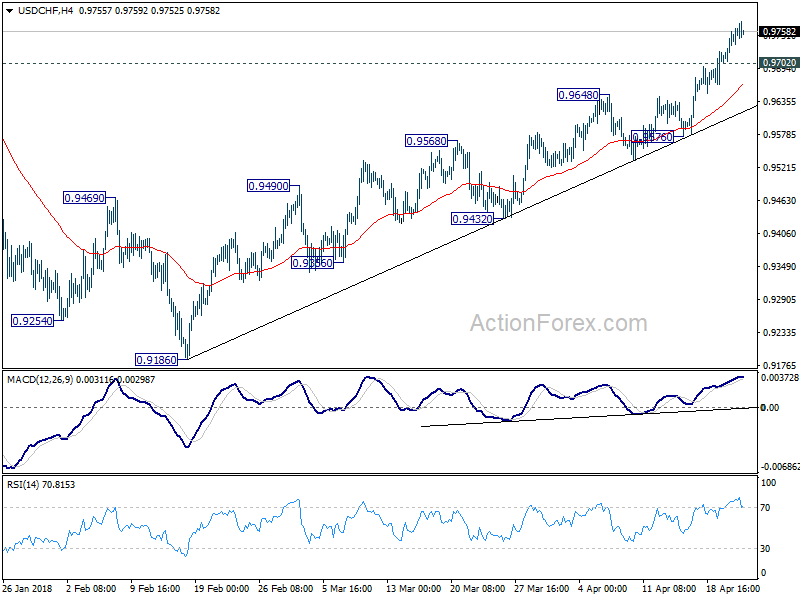

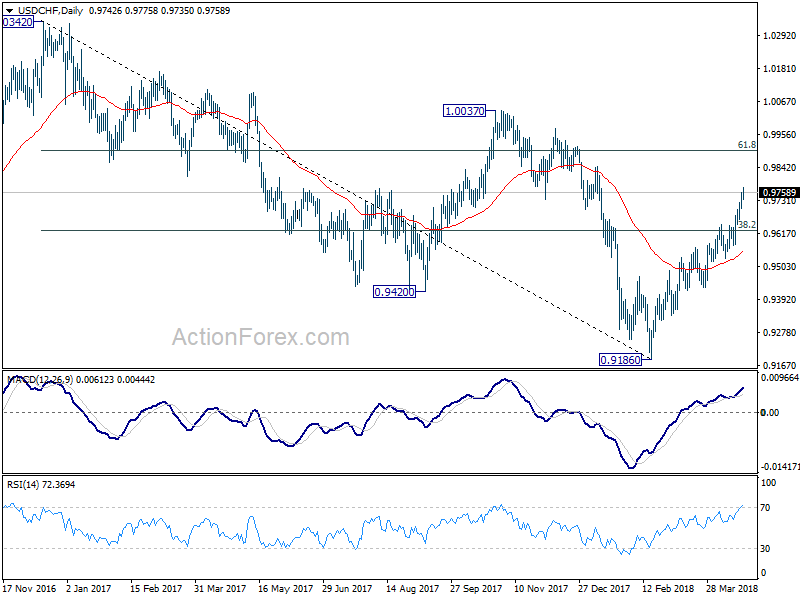

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9711; (P) 0.9735; (R1) 0.9770; More...

Intraday bias in USD/CHF stays on the upside with 0.9702 minor support intact. Current rally from 0.9186 should extend to 0.9900 fibonacci level next. On the downside, below 0.9702 minor support will turn bias neutral and bring consolidations. But outlook will stay bullish as long as 0.9576 support holds.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next. This will now be the preferred case as long as 0.9576 support holds.

DAX Steady at Start of Week, German and Eurozone Manufacturing PMIs Dip

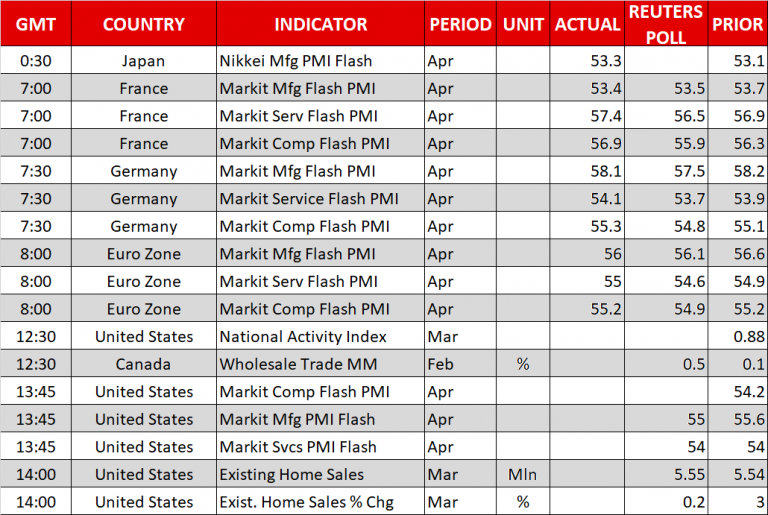

The DAX index is steady in the Monday session. Currently, the DAX is trading at 12,547 points, up 0.05% on the day. On the release front, German and eurozone manufacturing PMIs dropped in March, but still pointed to expansion. In the US, Existing Homes is expected to inch up to 5.55 million. On Tuesday, Germany releases Ifo Business Climate

The eurozone manufacturing sector softened in March, as underscored by PMI reports. German Manufacturing PMI dropped from 58.4 to 58.1, but beat the estimate of 57.6 points. Eurozone Manufacturing PMI dropped from 56.6 to 56.1, short of the forecast of 56.6 points. The readings remain well above the 50-point level, which separates expansion and contraction. At the same time, there is some concern as manufacturing activity (and general growth) in the eurozone was stronger earlier the year. If second-quarter numbers soften compared to Q1, the euro could respond with losses.

The markets are keeping a close eye on the ECB, which holds a policy meeting on Thursday. Despite stronger economic conditions in the eurozone, the ECB has been in cautious mode. At the March meeting, policymakers took a small step, dropping a pledge to increase stimulus if needed. Will we see additional ‘baby’ steps at the April meeting? The markets are not expecting any change in forward guidance, and concerns over recent trade disputes could mean a dovish statement from ECB President Mario Draghi. Traders shouldn’t expect any dramatic moves next week, as the bank will likely continue to preach patience and prudence.

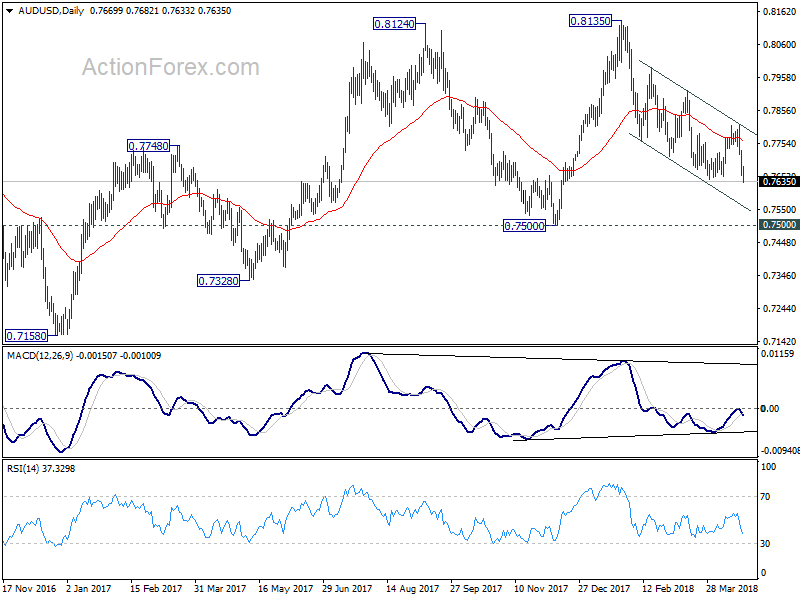

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7639; (P) 0.7685; (R1) 0.7715; More...

AUD/USD drops to as low as 0.7633 so far today. Break of 0.7642 confirms resumption of whole decline from 0.8135. Intraday bias remains on the downside for 0.7500 key support level next. Break there will indicate medium term reversal. On the upside, above 0.7682 minor resistance will turn intraday bias neutral and bring consolidations. But recovery should be limited below 0.7812 resistance to bring fall resumption.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Dollar Marches on as 10 Year Yield Presses 3%

Dollar's broad based rally extends today with the support of surging US treasury yield. 10 year yield hit as high as 2.99% in premarket, and is flirting with 3% level. Meanwhile, Japanese yen are trading as the weakest one. Euro suffered some selling earlier today after mixed PMI data. In particular, EUR/CHF's rejection from 1.2 key level become clearer. But selloff Euro is overwhelmed by weakness in Yen, Aussie and Kiwi. Movement in US yields will remain the main focus in US session as US PMIs and existing home sales are the only feature in the calendar.

Technically, GBP/USD and AUD/USD have taken key near term support at 1.3965 and 0.7642 respectively, mentioned in our daily report. Both developments indicate more upside in the greenback. The focus will now shift to 108.12/48 resistance zone in USD/JPY, 1.2814 in USD/CAD and 1.2214 support in EUR/USD. Break of these levels will further solidify the momentum for Dollar's rally.

Eurozone PMIs: Growth has downshifted markedly since the peak at the start of the year

Eurozone PMI manufacturing dropped to 56.0 in April, down from 56.6, miss expectation of 56.1. Eurozone PMI services rose to 55.0, up from 54.9 and beat expectation of 54.6. PMI composite unchanged at 55.2. Chris Williamson, Markit Chief Business Economist, noted that " growth has downshifted markedly since the peak at the start of the year, but importantly still remains robust." April's data is consistent with 0.6% at the start of Q2.

Germany PMI manufacturing dropped to 58.1, down from 58.2 and beat expectation of 57.5. Germany PMI services rose to 54.1, up from 53.9 and beat expectation of 53.7. PMI composite rose to 55.3, up from 55.1. Markit noted that "the data show the economy making a solid start to the second quarter."

France PMI manufacturing dropped to 53.4 in April, down from 53.7 and missed expectation of 53.5. France PMI services rose to 57.4, up from 56.9, beat expectation of 56.5. PMI composite rose to 56.9, up from 56.3. Markit noted that "the French private sector remained firmly in expansionary mode according to latest flash data."

Mexico agreed bilateral trade deal with EU, still working with Canada and US on NAFTA

In a joint statement published on Saturday, EU and Mexico had "reached an agreement in principle" on trade and investment between the two entity, as part of the modernisation of the bilateral legal framework. European Commission President Jean-Claude Juncker, welcomed the news saying: "With this agreement, Mexico joins Canada, Japan and Singapore in the growing list of partners willing to work with the EU in defending open, fair and rules-based trade."

Separately, Mexico is still working on NAFTA renegotiation with Canada and US. Mexican Central Bank Governor Alejandro Diaz de Leon expressed his optimism that "in the baseline scenario of the central bank, we have that there will be a version of NAFTA." He added that "we know that there have been ups and downs in the negotiation … (But) we do hope that the advantages for the three countries will prevail in some version of the agreement." Senior officials from the three countries will meet again in Washington to push for a deal within a couple of weeks.

Fed Williams: Trade war will lower growth, raise inflation and lower quality of life

San Francisco Fed President John Williams told Spanish newspaper El Pais that it's too soon to tell if there will be a trade war. He pointed out "the reality is that it is not so serious as some headlines suggest". However, Williams also warned that "if the conflict increases there will be less growth, more inflation and lower quality of life all over the world."

Regarding central bank communications on stimulus exit, Williams said "it should be repeated until people have had enough of hearing the message."

Japan PMI manufacturing: Stronger yen begins to impact price competitiveness

Japan PMI manufacturing rose to 53.3 in April, up from 53.1 but missed expectation of 53.4. Joe Hayes, Economist at IHS Markit, noted in the release that the survey data depicted a positive backdrop in the Japanese manufacturing sector during April. And the improvements in the headline number was "underpinned by stronger rates of growth in output, new orders and employment." Business confidence also "strengthened". On the other hand, new export orders dropped for the first time since August 2016 as "stronger yen begins to impact price competitiveness". But rise in total new business inflows also indicated "stronger domestic demand".

BoJ Kuroda: Inflation to meet target in fiscal 2019, but risks are skewed to the downside

BoJ Governor Haruhiko Kuroda repeated his usual rhetoric that the central bank "must continue very strong accommodative monetary policy for some time" in order to reach the 2% inflation target. He pointed out that "if you exclude energy items, then inflation rate is only about 0.5 percent." And, there is "still a long way to go to achieve the 2 percent inflation target." Kuroda is still expecting inflation to hit target in fiscal 2019 but "risks are skewed to the downside."

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7639; (P) 0.7685; (R1) 0.7715; More...

AUD/USD drops to as low as 0.7633 so far today. Break of 0.7642 confirms resumption of whole decline from 0.8135. Intraday bias remains on the downside for 0.7500 key support level next. Break there will indicate medium term reversal. On the upside, above 0.7682 minor resistance will turn intraday bias neutral and bring consolidations. But recovery should be limited below 0.7812 resistance to bring fall resumption.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | PMI Manufacturing Apr P | 53.3 | 53.4 | 53.1 | |

| 07:00 | EUR | France Manufacturing PMI Apr P | 53.4 | 53.5 | 53.7 | |

| 07:00 | EUR | France Services PMI Apr P | 57.4 | 56.5 | 56.9 | |

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 58.1 | 57.5 | 58.2 | |

| 07:30 | EUR | Germany Services PMI Apr P | 54.1 | 53.7 | 53.9 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 56 | 56.1 | 56.6 | |

| 08:00 | EUR | Eurozone Services PMI Apr P | 55 | 54.6 | 54.9 | |

| 12:30 | CAD | Wholesale Trade Sales M/M Feb | -0.80% | 0.80% | 0.10% | |

| 13:45 | USD | US Manufacturing PMI Apr P | 55.2 | 55.6 | ||

| 13:45 | USD | US Services PMI Apr P | 54.1 | 54 | ||

| 14:00 | USD | Existing Home Sales Mar | 5.55M | 5.54M |

Dollar Posts Fresh High as Long-Term Treasury Yields Flirt with 3.0%; European Stocks Down

Here are the latest developments in global markets:

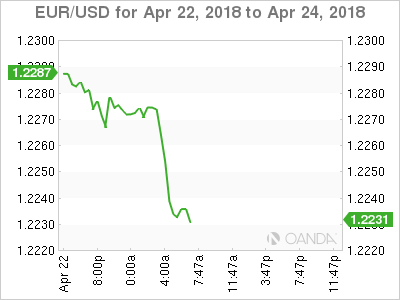

FOREX: The dollar picked up speed as the 10-year US Treasury yield continued to trend near 3.0%, the highest since early 2014, underpinned by concerns that increasing oil prices could spread inflationary pressures, while a rise in US debt issuance was also supportive for the jump in yields. Besides that, Saturday’s news out of North Korea increased appetite for riskier investments. The North Korean leader said that he would suspend nuclear and intercontinental ballistic missiles tests ahead of a crucial meeting with South Korea and the US in late May or early June. In response, the dollar index jumped to a near 2-month high of 90.64 (+0.37%) today, while dollar/yen crawled up to a 2 ½-month high of 108.03 (+0.34%). Euro/dollar tumbled to a two-week low of 1.2236 (-0.44%) on the face of a strengthening dollar, unable to gain from an encouraging composite PMI out of the Eurozone. Pound/dollar was also trading at two-week lows, last seen at 1.3975 (-0.22%) as traders remained cautious on whether the BoE will deliver a rate hike in May, following the BoE governor’s dovish comments on Thursday. Euro/pound was on the back foot after four days of rising, changing hands at 0.8756 (-0.24%). The antipodean currencies were among the worst performers, with aussie/dollar and kiwi/dollar extending declines towards 0.7635 (-0.47%) and 0.7171 (-0.50%) respectively. Dollar/loonie stretched its uptrend to 1.2796 (+0.31%).

STOCKS: European equities turned lower on Monday on the back of rising US Treasury yields, while disappointing statements by UBS, Switzerland’s biggest bank, weighed on equity market sentiment. The pan-European STOXX 600 was down by 0.27% at 0800 GMT, with all sectors except healthcare and energy being in the red. The German retailer Metro AG was leading the losses after the company cut its earnings projections for the 2017/2018 year, saying that earnings from its Russian operations could ease more than expected in the second half of the year. UBS also stood cautious about the coming quarter despite upbeat reports on Q1 2018 earnings, citing geopolitical and trade risks as threats to the outlook. The German DAX 30 fell by 0.28%, the Swiss SMI declined by 0.58% and the French CAC 40 dropped by 0.21%. The UK’s FTSE 100 was steady, supported by basic materials. Indices tracking US stock futures were flashing red, pointing to a negative open.

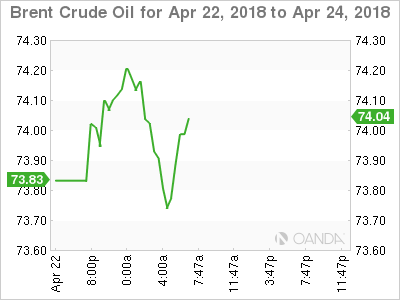

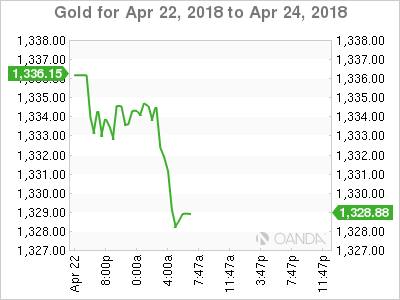

COMMODITIES: Oil prices weakened further on Monday despite the United Arab Emirates saying that the OPEC’s mission “is not complete” yet and supply cuts by OPEC and non-OPEC members including Russia will continue until the end of the year. WTI crude and Brent retreated to $67.95 (-0.66%) and $73.69 (-0.50%) per barrel respectively. In precious metals, gold declined to a two-week trough of $1,327.02 per ounce (-0.50%).

Day Ahead: US flash PMIs and existing home sales in the calendar; Australian CPI in focus

Monday will be a relatively quiet day ahead of a week featuring central bank meetings, important data releases, and possibly developments on the geopolitical front.

The day continues with the Canadian wholesale sales for the month of February scheduled for release at 1230 GMT.

The US will see the release of April’s preliminary PMIs out of Markit at 1345 GMT, with analysts expecting the manufacturing PMI to tick marginally lower to 55.0 compared to 55.6 seen in March, while the composite index is anticipated to inch higher by 1.1 points to 55.3.

Remaining in the US, at 1400 GMT, existing home sales data for the month of March will be attracting interest. Growth in sales is said to have slowed down from 3.0% m/m to 0.2%.

Turning to today’s public appearances, European Central Bank Executive Board member Benoit Coeure will be speaking at a conference at 1400 GMT. Later at 1930 GMT, Bank of Canada Governor Stephen S. Poloz and Senior Deputy Governor Carolyn A. Wilkins will be making comments in front of the House of Commons Standing Committee on Finance, while at 2200 GMT a speech by RBA Assistant Governor Christopher Kent will be in focus.

During Tuesday’s early Asian session, the Australian Bureau of Statistics will deliver data on consumer prices (0130 GMT). Forecasts are for the headline CPI to rise by 2.0% y/y in the first quarter of 2018 from the 1.9% seen in the previous quarter, probably due to seasonal effects. The core measures however, which are closely watched by the RBA, are projected to remain on average slightly below the central bank’s inflation target range of 2-3.0%, signaling that a rate hike is not likely to happen anytime soon, as subdued wage growth and high debt levels continue to hang in the background.

Should inflation numbers surprise to the upside, bringing some relief to RBA policymakers, the Australian dollar could recoup losses made the past couple of days. On the other hand, disappointing prints could push the currency to fresh lows.

In stock markets, Google-parent Alphabet will be releasing quarterly results today after the US market close.

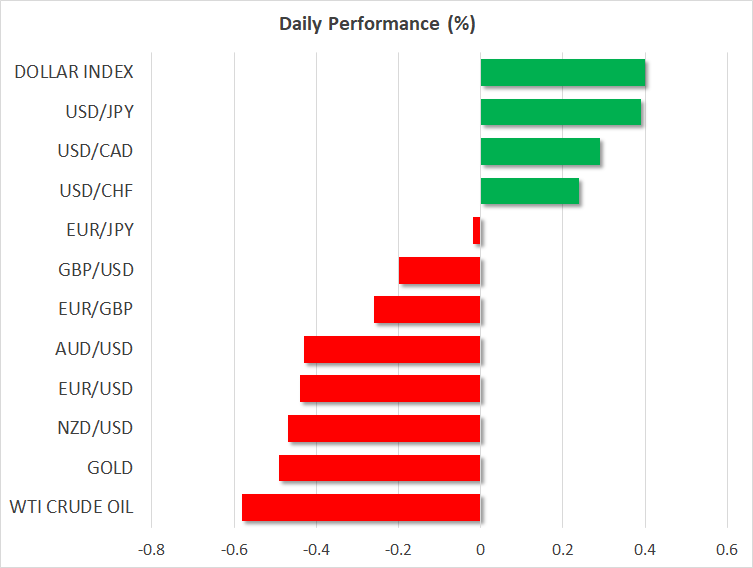

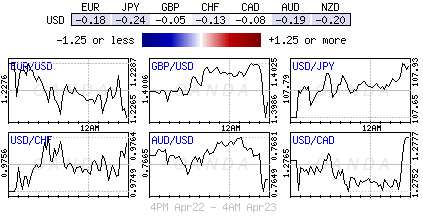

USD strongest followed by CHF, JPY weakest into US session

USD's rally extends today and is trading firm entering into US session. Technically, both GBP/USD and AUD/USD have taken out recent support at 1.3965 and 0.7642 respectively, suggesting more upside in USD in near term.

Looking at D heatmap, we can see that JPY is the weakest one for the day while CHF is the second strongest one. This may look a bit counter intuitive. But it makes sense after giving a bit deeper thoughts.

Firstly, EUR/CHF is finding it difficult to break through 1.2 historical level. It's being rejected from there after last week's attempt and is back at 1.1930 at the time of writing. That helps lift CHF elsewhere.

Secondly, European's stocks are fluctuating between gains and losses today, suggesting that's is no underlying strong risk appetite yet. Thus, at least, there is no additional selling pressure on the CHF.

Thirdly, surging US treasury yield is a key underlying theme in the markets. That's a main force in boosting USD up. Weakness in the Yen, at the time when US stocks fall (risk aversion), is indeed affirming that yield is the factor.

Going forward, 108.12/48 resistance zone in USD/JPY is the main focus, which would determine if bullish reversal has already occurred. And, EUR/USD could be testing 1.2214 if the pull back in EUR/CHF gains momentum.

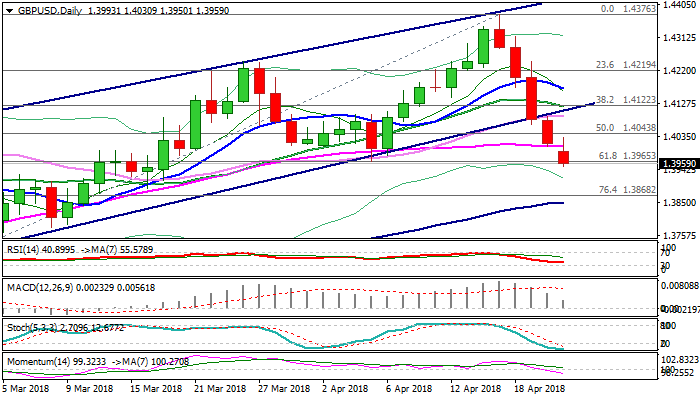

GBPUSD – Extension Through 1.40/1.3965 Supports Is Strong Bearish Signal

Cable remains in steep descend which extended into fifth straight day and broke below key supports at 1.4000/1.3965 (psychological support / Fibo 61.8% of 1.3711/1.4376 / 05 Apr trough) on fresh bearish acceleration on Monday.

Sterling maintains strong bearish sentiment on fading hopes about BoE rate hike next month, following downbeat key UK data (wages, CPI, retail sales) and dovish comments from BoE’s chief Carney last week.

Bears pressure next supports at 1.3931/01 (thin daily cloud) which is seen as not strong obstacle.

Close below 1.3965 would generate bearish signal for extension through daily cloud towards 1.3868 (Fibo 76.4% of 1.3711/1.4376 ascend) and 1.3850 (rising 100SMA).

Slow stochastic is in deeply oversold territory on daily chart but continues to trend lower, suggesting bears remain uninterrupted for now, but may take a breather soon.

Broken 1.40 support is reinforced by 55SMA and marks initial barrier, guarding 1.41 zone (broken bull-channel support line / broken 30SMA).

Res: 1.4008, 1.4030, 1.4094, 1.4103

Sup: 1.3931, 1.3901, 1.3868, 1.3850

U.S Dollar Responds To Higher Yields

Monday April 23: Five things the markets are talking about

U.S Treasuries begin the week on the back foot, trading atop of the key psychological +3% level at +2.994%, prolonging last week’s price decline as capital markets continue to evaluate the global outlook for trade and growth.

Note: Trade dominated discussions at an IMF gathering in Washington last weekend – the U.S/Sino trade row, coupled with global debt concerns, were named as threats to the global growth outlook.

Higher yields are supporting the U.S dollar against G7 currency pairs. Sterling had briefly been the exception, however, PM Theresa May is trying to squash a cabinet revolt.

Elsewhere, crude oil prices have eased a tad after rising for a second consecutive week on a commitment from OPEC to rebalance the market.

On tap for this week – the European Central Bank (April 26) and the Bank of Japan (April 27) meet and neither is expected to adjust their respective monetary policy.

Note: The market will be looking for any sign that E.U officials are preparing a shift in stimulus plans for their June meeting.

Down-under, Japan releases its industrial production and employment data while the Aussie’s report their Q1 CPI data (April 23).

Stateside, the U.S releases its first estimate of Q1 GDP (April 27) and weekly jobless claims (April 26).

1. Stocks mixed start to the week

European shares are following their peers in Asia down.

In Japan, the Nikkei started the week in the ‘red’ as index heavyweight stocks lost ground, offsetting gains from financials, which rallied on higher sovereign yields. The Nikkei ended down -0.3%, while the broader Topix traded flat.

Down-under, Aussie shares rallied overnight, , with financials accounting for most of the gains, while materials rose on the back of firmer commodities prices. The S&P/ASX 200 index ended up +0.3%. In S. Korea, the Kospi traded little changed.

In Hong Kong, equities traded lower, led by tech stock on trade-spat worries. The Hang Seng index fell -0.5%, while the China Enterprises Index lost -0.4%.

In China, major stock indexes ended Monday unchanged, although tech firms again were sold. The blue-chip CSI300 index ended up +0.2%, while the Shanghai Composite Index slipped -0.1%.

In Europe, regional indices trade lower across the board, following on from a weaker session in Asia and weaker U.S futures.

U.S stocks are set to open in the ‘red’ (-0.2%).

Indices: Stoxx600 -0.2% at 381.3, FTSE flat at 7367, DAX -0.3% at 12503, CAC-40 -0.2% at 5401, IBEX-35 flat at 9887, FTSE MIB -0.1% at 23798, SMI -0.4% at 8773, S&P 500 Futures -0.2%

2. Oil dips as U.S drilling eases bullish sentiment, gold prices lower

Oil prices have eased a tad as a rising U.S rig count suggests a further increase in production.

Brent crude futures are at +$73.91 per barrel, down -15c, or -0.2% from Friday’s close. U.S West Texas Intermediate (WTI) crude futures are down -18c, or -0.3% at +$68.22 a barrel.

Note: Brent is up by +20% from this year’s February low.

Baker Hughes data Friday showed that U.S drillers added five rigs drilling for new production in the week ended April 20, bringing the total to +820, the highest in three years. The rising rig numbers point to further increases in U.S. crude production, which is already up +25% in two-years to a record +10.54m bps.

Note: Only Russia produces more, at almost +11m bpd.

Prices are also being supported by supply cuts led by the OPEC to prop up the market.

Ahead of the U.S open, gold prices slip to a new two-week low as rising bond yields support the dollar. Spot gold is down about -0.1% at +$1,334.11 per ounce, after earlier touching its lowest since April 10 at +$1,331.70. U.S gold futures fell -0.2% to +$1,336.30 per ounce.

3. Sovereign yields back up

The U.S 10-year Treasury yields are within touching distance of the key psychological +3% handle.

Higher U.S yields are also supporting many regional yields. Germany’s 10-year Bund yield has climbed +4 bps to +0.63%, the highest in six-weeks, while the U.K’s 10-year Gilt yield has backed up +4 bps to +1.518%.

Note: The last time yields traded atop of current yield levels it hurt investor risk appetite and sent equities tumbling. It also came shortly before crude oil prices plummeted -75%.

The European Central Bank (ECB) guidance later this week (April 26), about the future of its stimulus programme, is the next thing that may cause some yield movement.

Last Friday, ECB’s Draghi said he was confident that the inflation outlook has picked up, but uncertainties “warrant patience, persistence and prudence.”

4. Dollars firm hand

Higher yields are supporting the ‘big’ dollar across the board. However, if the rise in U.S yields is “not” sustained and if market talk becomes one of concern about U.S debt levels, then this recent dollar bounce higher may not be sustainable.

The EUR/USD is down -0.4% at €1.2236 and U.S. 10-year Treasury yields are at +2.9944%. Dollar ‘bulls’ argue that if U.S 10’s yields were to break above 3% and stay there, and if volatility were to remain low, avoiding a sell-off in risk assets, the EUR is likely to trade beck towards the key support level at €1.2150.

Higher U.S yields could generate some problems for the most vulnerable in the emerging market space.

GBP/USD has moved below the £1.40 level to £1.3960. Market focus for the pound will shift to the House of Commons debate later this week (April 26) on the Withdrawal Bill. Sterling is also under pressure on rumours that PM May maybe forced to accept staying in the E.U’s customs union.

Note: On Apr 18 PM May’s government suffered defeat on the E.U Withdrawal Bill in the House of Lords

USD/JPY (¥108.23) rise is aided by the rise of the U.S yields. Japanese officials noted that Finance Minister Aso and U.S Treasury Sec Mnuchin did not discuss exchange rate moves at a bilateral meeting last Friday. The BoJ meets on Friday will update its forecasts and include fiscal year 2020 for the first time.

Note: There has been speculation that the BoJ might have to cut its inflation forecasts this week but maintain its timeline in achieving the 2% inflation target in the next fiscal year.

5. Eurozone private sector growth steady in April

Data this morning showed that E.U activity in private sector grew at a steady pace this month after two straight months of easing. This may suggest that a Q1 slowdown may be coming to an end.

E.U Purchasing Managers Index (PMI) was unchanged at 55.2 in April from March. The market had expected to see a decline to 54.8.

Digging deeper, today’s report continues to record some worrying developments. While activity in the services sector picked up, the more export-oriented manufacturing sector continued to slow. This may be due to the EUR’s appreciation against most currencies in the past 12-months.

On Friday, ECB’s Draghi warned that the eurozone’s growth cycle may have peaked, and suggested that the ECB would move only slowly to phase out QE.

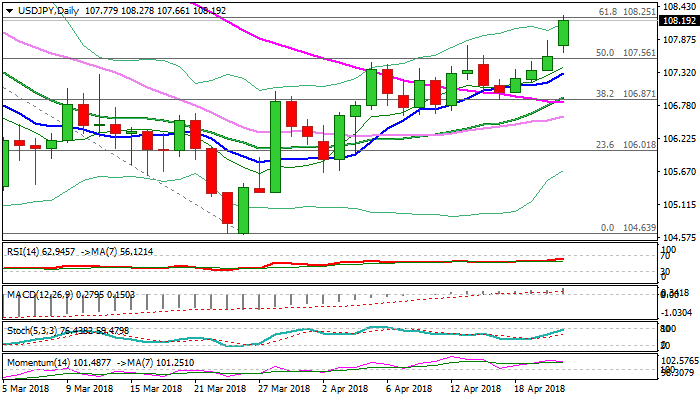

USDJPY – Bulls Extend And Crack 108.25/49 Fibo Resistance Zone

Bulls accelerated through psychological 108 barrier and cracked target at 108.25 (Fibo 61.8% of 110.48/104.63 bear-leg), the lower boundary of Fibo resistances zone between 108.25 and 108.49 (Fibo 38.2% of 114.73/104.63 fall).

Break and close above these barriers would generate strong bullish signal and open way for test of 109.02 (falling 100SMA) and more significant barrier provided by top of thick daily cloud at 109.31.

Bullish techs are supported by positive dollar’s sentiment and expected to further underpin the advance.

Broken Fibo barrier at 107.56 now acts as support and should keep the downside protected.

Res: 108.49, 108.77, 109.02, 109.31

Sup: 107.77, 107.56, 107.31, 106.92

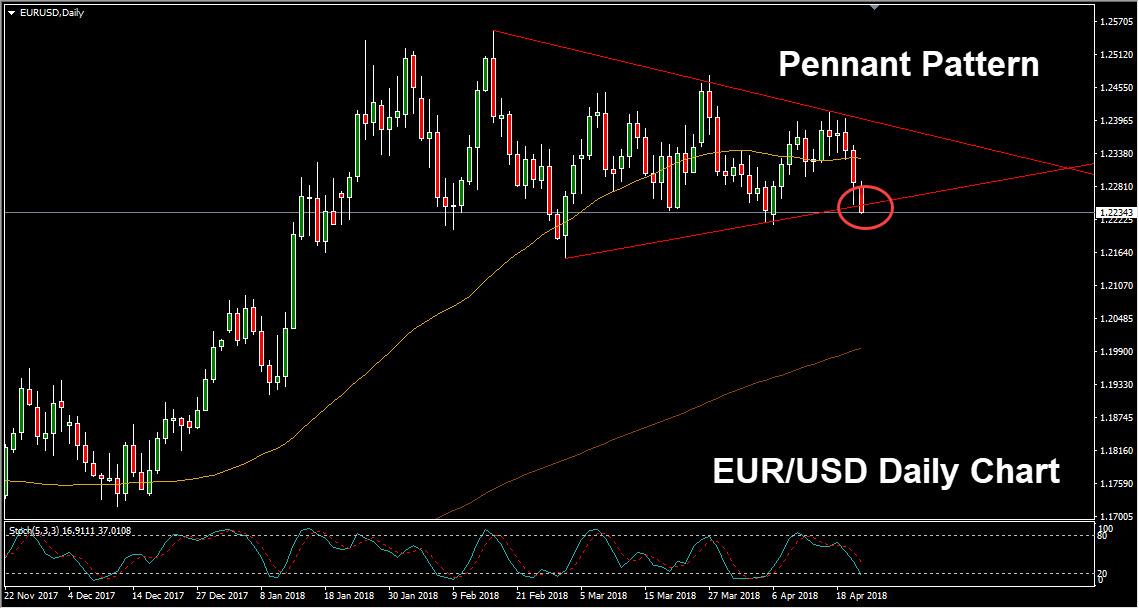

Chart Of The Day: Euro Begins Week On Back Foot Ahead Of ECB Meeting

The Euro continued to weaken on Monday morning, entering a third day of losses against the US dollar. The slide continued despite Monday's news that Eurozone Composite PMI was unchanged for April at 55.2, holding above the 50-point level that indicates expansion.

A rise in U.S. Treasury yields to 3 percent has helped boost the greenback to its highest levels in over two weeks. The US dollar has also been underpinned by a hawkish stance from the Federal Reserve. Fed officials have signalled additional interest rate increases in 2018 based on signs of positive economic growth.

The European Central Bank (ECB) holds its monetary policy meeting on Thursday. Policymakers are widely expected to signal no change in key interest rates and the central bank's quantitative easing program. Analysts expect a dovish stance from ECB president Mario Draghi amid the recent slowdown in inflation.

EUR/USD has been in an uptrend since January of 2017 and remains above the 200 period simple moving average on the daily timeframe. However, the pair has been range bound between 1.2154 and 1.2554 for three months. On Monday morning EUR/USD broke below the lower trendline of a pennant pattern. A break below the 1.2154 level would expose the next major level of support at the 200 period simple moving average.