Sample Category Title

DXY Index is Going Nowhere

Markets

Markets yesterday saw the glass half full rather than half empty but for now its too early to draw any conclusion on a tentative bottoming out-process in (US) yields and/or equity markets. Regarding the multiple, often divergent storylines that markets have to cope with, the US trying to convince Russia to accept its proposal on a ceasefire for the war in Ukraine was a supportive factor for EMU equity markets (Eurostoxx 50 +0.97%). US markets also tentatively look for a bottom (Nasdaq +1.22%). A softer than expected US CPI (both February headline and core easing to 0.2% M/M vs 0.3% expected) also gave some comfort as investors are pondering the impact of tariffs further out. The EU retaliating against the US 25% tariff on steel an aluminum indicated that trade war is still a developing, highly unpredictable storyline, but next steps probably are only to be expected early April. The milder risk sentiment helped a further bottoming process on US interest rate markets. US yields rebounded further between 4.35 bps (2-y) and 3.25 bps (10-y) across the curve. European yields after last week’s sharp repositioning are in a (ST) consolidation phase. The German yield curve even slightly flattened with the 2-y yield adding 2.6 bps while the long end eased slightly (30-y -2.1 bps). We don’t draw any conclusions yet. At the ECB and its Watchers conference in Frankfurt, ECB chair Lagarde indicated that inflation might become more volatile and persistent in an era of several types of shocks. The ECB is examining the impact of the shocks. Lagarde didn’t given any concrete guidance on what this means for day-to-day monetary policy. Even so, the fiscal support that Germany/Europe is putting in place only suggest that there is a good reason for the ECB to move to a wait-and-see approach once policy is no longer restrictive. Markets remain divided on a next ECB rate cut in April (40-60 chance in favour of a pauze).

On FX markets, the pressure on the dollar also eased, at least temporarily. DXY ‘rebounded’ from 103.4 to 103.6. EUR/USD corrected back below 1.09 (close 1.089). USD/JPY also gained from 147.8 to 148.25, but closed well of the intraday top levels. Sterling outperformed both against the dollar and even more against the euro. EUR/GBP 0.8450/75is doing its job as a short-term resistance.

Despite yesterday’s rebound on WS, Asian equity markets show a hesitant picture this morning with several regional indices showing losses of 1.0%, Japan slightly outperforming. The DXY index is going nowhere (103.6). EUR/USD is correcting marginally further (1.0875). The yen outperforms (USD/JPY 147.8). BOJ governor Ueda in a response to questions in parliament, indicated that he remains confident that consumer spending will be further supported as wage rises are expected to continue. Later today, US PPI producer prices and weekly jobless claims probably will only be of intraday significance for trading. The EMU calendar is thin today. Still, a session with little high profile news might give some indication on underlying sentiment. In this respect, we look out how the recent EMU steepening trade evolves after yesterday’s pauze. On FX markets, we stay cautious on the dollar as US risk sentiment remains fragile. The risk of a US government shutdown at the end of the week in this respect probably doesn’t to help revive the dollar’s status as a solid reference/safe haven.

News & Views

The National Bank of Poland kept its policy rate yesterday unchanged at 5.75%. The expected inflation range for this year was slightly downwardly revised, from 4.2%-6.6% in November to 4.1%-5.7% while the one for next year faced an upward revision, from 1.4%-4.1% to 2%-4.8%. The NBP sees inflation between 1.1% and 3.9% in 2027. An additional inflationary source which featured a first time in the statement is a further economic recovery with a marked increase in domestic demand. References to the impact of already introduced increases in energy prices, rises in excise duties and administered services prices as well as the further unfreezing of energy prices in the second half of 2025 remain. This also shows up in upward revision to GDP projections: 2.9%-4.6% this year, 1.9%-4% next year and 1.1%-3.5% in 2027. NBP president Glapinski is expected to stick to his hawkish rhetoric at today’s press conference. The zloty obviously wasn’t impressed by the ongoing rate status quo, sticking near EUR/PLN 4.20.

The Bank of France cut its growth forecast from this year from 0.9% in December to 0.7%. It also downgraded next year’s prognosis from 1.3% to 1.2%. BdF chief economist warns to uncertainty on the international level linked to what is happening with US tariffs. The size of the negative impact will depend on targeting and duration. Upside risks come from additional defense spending. New inflation forecasts stand at 1.3% this year and 1.6% next, down from 1.6% and 1.7%.

The Tariff Ping Pong

The tariff hell broke lose yesterday after the US imposed 25% tariffs on all steel and aluminium imports triggering a swift response from the EU and Canada. The EU announced tariffs on around EUR 26bn worth of American goods, while Canadians slapped tariffs on CAD 30bn worth of US products. Voila, happy Thursday. Let’s see who blinks first.

Happily though, the US inflation ease more than expected in February on both monthly and annual basis. The prices of new cars and gas had a good easing impact on price pressures, while egg prices soared more than 10% (and apparently, the slowing demand there could help the producers catch up with strong demand). The market modestly cheered the news. The S&P500 recovered some 0.49%, Nasdaq 100 rebounded more than 1% while the Dow Jones retreated 0.20%. The volatility eased, but the worries remain as the tariffs will have implications. In the first place, they will cause a few jumps in price levels. You could argue that the price jumps due to tariffs will probably be limited in time, but bringing production sites back to the US will have a longer term impact on goods prices that are made in America, because obviously, it’s cheaper when things are made, or partly made in China or Mexico.

Then, tariffs mean the end of a free trade era that helped global economies, especially the rich Western nations including the US and the EU, benefit grandly from the so-called invisible hand – make the best do the job – which concentrated high value-added, well-paid jobs in the West and pushed low value-added, low-paid jobs to the others. In terms of amassing wealth in the long run, the end of the invisible hand is questionable.

Bur anyway, today, investors will keep focus on US producer price inflation; the headline PPI figure is also expected to have benefited from the latest weakening in energy prices. But the soft numbers will certainly be cheered with modest enthusiasm as the tariffs and their implications are unknown: no one knows how long they will stay and how far the retaliations extend. Trump already said that he will retaliate to the EU who dared to respond to his tariffs on metals.

If we are lucky, the softer-than-expected inflation figures could help taming the inflation expectations that have risen significantly with the tariff walkdown. But the outlook for the US indices remains negative. Funny enough, yesterday’s softer-than-expected CPI prints didn’t increase the probability of a May cut from the Federal Reserve (Fed). On the contrary, the chances of a May rate cut implied by activity on Fed funds futures fell to around 30% from around 40% where it stood yesterday morning, before the data release. Add to the mix that the Democrats and Republicans are having hard time agreeing on a spending bill increasing the chances of a government shutdown – one should really look carefully to find a good place to hide in the US equity space.

Inside Europe

The Stoxx 600 index jumped off its 50-DMA yesterday despite the tariff ping pong. The euro appreciation helps tame inflation expectations, and along with the prospects of high spending on defence and security, which should help boosting growth to some extent, gains here are certainly on a more solid footage than the US peers. The EURUSD tested the levels above the 1.09 level this week, but given the overbought market conditions, clearing a psychological level like the 1.10 mark could be hard to achieve. The euro could first see a minor pullback, catch its breath and jump above that level afterwards. Support to the positive trend building since mid-January is seen near 1.0730/70 level, including the minor 23.6% Fibonacci retracement and 200-DMA.

Across the Channel, Brits want to ink a trade agreement with the US and make the Brexit worth something better. But for now, the UK has only been the collateral damage of the global trade war and was also left out of the ample spending plans from the EU – the worse of both worlds. Cable is testing the 1.30 offers to the upside, and given the broad based USD depreciation, we could see Cable eventually break the back of the 1.30 offers, but the pound may have to say goodbye to its advance against the euro as the growth prospects are turning shinier in Europe than in the UK. The pair is now testing the upper band of a one-year downtrending channel, and a potential rise above the 0.85 level will confirm a medium-term bullish reversal in favour of the single currency. The UK will release its latest GDP figures tomorrow morning and are expected to show a slowdown in growth in February to just 0.1%.

In the equities space, the FTSE 100 also benefited from the rotation trade from the US toward the old continent, but underperformed the Stoxx 600 over the past weeks - a gap that could be attributed to the extra military spending budget that the EU benefits from that the UK doesn’t. The mining stocks weren’t necessarily hit by the tariff threats, as the threats increased demand from companies who were looking to frontload their purchases before the tariffs went live. Rio Tinto for example remained rangebound in the first two months of the year as we saw copper futures rise more than 20% since the beginning of the year despite the waning global growth prospects. But that rally looks vulnerable now that the tariffs are on. The impact of the latest tariffs could be heavier for the miner-heavy FTSE 100 than it is for the continental European peers.

Trump Tariffs Prompt Global Retaliation

In focus today

In the euro area, focus will be on the preliminary discussions of the proposed fiscal easing package in the German parliament. The Green party has so far refused the coming government's proposal, but we see this as a negotiating tactic to get concessions ahead of the final vote on the bill Tuesday next week. Also in the euro area, industrial production data for January is due. Production has continued a declining trend the past two years, but with the recent improvement in soft indicators it will be interesting to see if hard data also shows a smaller decline in production than previously.

In the US, February PPI and weekly jobless claims are due for release. Following yesterday's CPI, it will be interesting to see if PPI-figures comes in lower than expected as well. Markets expect an increase of 0.3% m/m, down from 0.4% in January.

In Sweden, we will receive the details for the Swedish inflation for February. The flash estimate last week was surprisingly high. The Riksbank's target measurement CPIF came in at 2.9% y/y (cons: 2.7%, prior 2.2%), and core inflation, CPIF ex energy 3.0% y/y (cons: 2.7%, prior 2.2%). Headline CPI 1.3% y/y (cons: 1.1%, prior: 0.9%).

Economic and market news

What happened yesterday

In the US, February inflation figures dropped more than expected to 2.8% (prior: 3.0%, cons: 2.9%), indicating that January's increase was likely a one-off. Core inflation fell to 3.1% (prior: 3.3%, cons: 3.2%). Although US inflation remains elevated, today's figures offer reassurance for both the Fed and consumers. We anticipate a gradual easing of monetary policy in the US, with the next interest rate reduction expected in June.

In the EU, in response to the US metal and steel tariffs that commenced yesterday, the EU commission announced a range of countermeasures against the US. The Commission's response intends to match the economic impact of the US tariffs on a 1:1 basis and can be lifted "at any time" if a resolution with the US is achieved, which remains the EU's goal. Both the US tariffs on steel and metals and the EU's counter tariffs are expected to have limited effect on growth in and inflation as they cover around 5% of total EU exports to the US.

In the euro area, the much-awaited speech by President Lagarde's speech at the ECB Watchers conference did not provide any signals on what to expect at the April meeting. The geopolitical uncertainty and changing fiscal outlook pose fundamental questions for monetary policy, and the ECB is clearly attentive to remaining flexible and agile in its policy response. Lagarde touched upon the risk of inflation volatility turning into persistently elevated inflation as wages adjust, which requires the ECB to not pre-commit to any rate path and remain agile in its communication. Overall, the speech underlined the uncertainty also visible in the vague guidance at last week's meeting. The upcoming data (inflation, PMIs), tariff announcement and fiscal negotiations in Germany will likely be decisive for the outcome. Markets are discounting a 45% probability of a cut in April.

In Canada, the BoC delivered a 25bp cut, as widely expected, setting policy rate at 2.75%. The market reaction was relatively subdued, with significant attention on the uncertainty and trade tensions stemming from US tariffs. The BoC highlighted that monetary policy cannot counteract the effects of a trade war, but it can be utilized to prevent higher prices from leading to persistent inflation. In response to yesterday's tariffs, Canada swiftly retaliated by imposing tariffs on nearly USD 21bn of US goods, labelling the US levies as "completely unjustified, unfair and unreasonable".

Equities: It was perhaps not a bounce, but at least a pause in the US selloff. Gains were driven by last weeks' worst performers. Thus, big difference between indices with S&P500 rising 0.5% but Nasdaq 1.2%. Europe also higher with Stoxx 600 0.8%. Big rotation underneath, with investors rotating out of defensives again (consumer staples -2.5%) and into the MAG7 names. However, risk appetite is worsening this morning again with futures lower.

FI&FX: Yesterday, we finally saw a modest widening of the US-Bund yield spread as European yields declined while US yields rose and the 10Y US-Bund yield spread rose some 5bp from 138bp to 143bp. It has been the same pattern in the 2Y US-Bund yield spread. EUR/USD remained around the 1.09 mark. As widely expected, BoC delivered a 25bp rate cut bringing its policy rate to 2.75%, resulting in a limited market reaction. EUR/NOK traded lower during Wednesday, currently around the 11.57 level, as market's price the probability for March cut close to 50/50. EUR/SEK rose from the 10.93 level to above 11.01 but are now back just below the 11.00 mark.

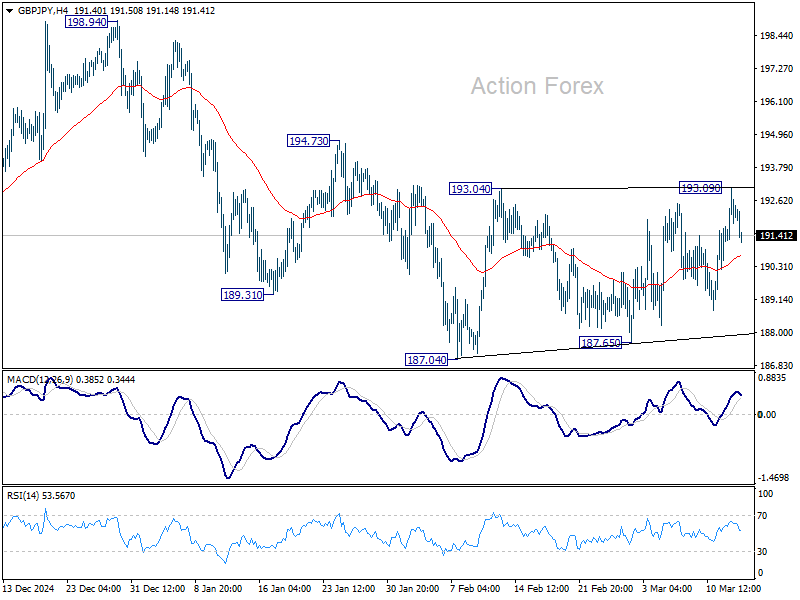

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.24; (P) 192.18; (R1) 193.15; More...

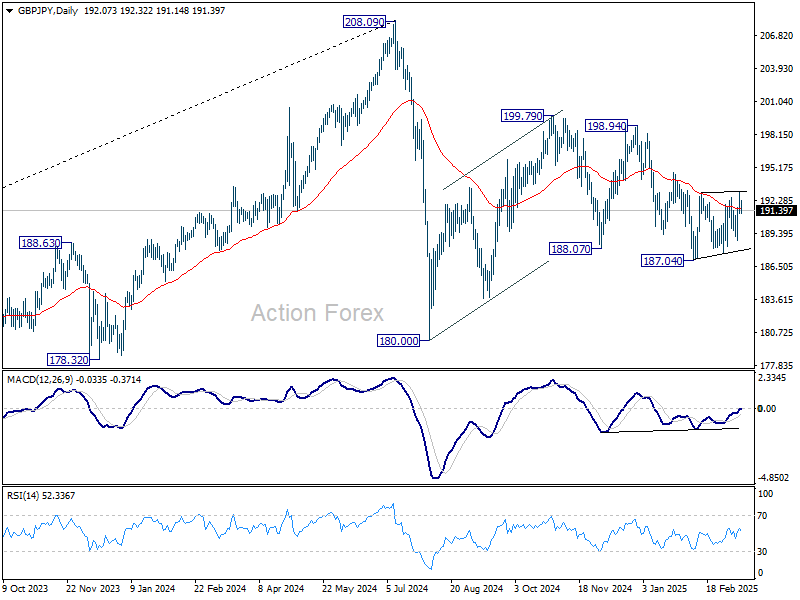

GBP/JPY edged higher to 193.09 but quickly retreat. Intraday bias stays neutral for the moment. On the upside, firm break of 193.09 will resume the rebound from 187.04 to 194.73 resistance, and then 198.94. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support. Overall, corrective pattern from 180.00 might still be extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

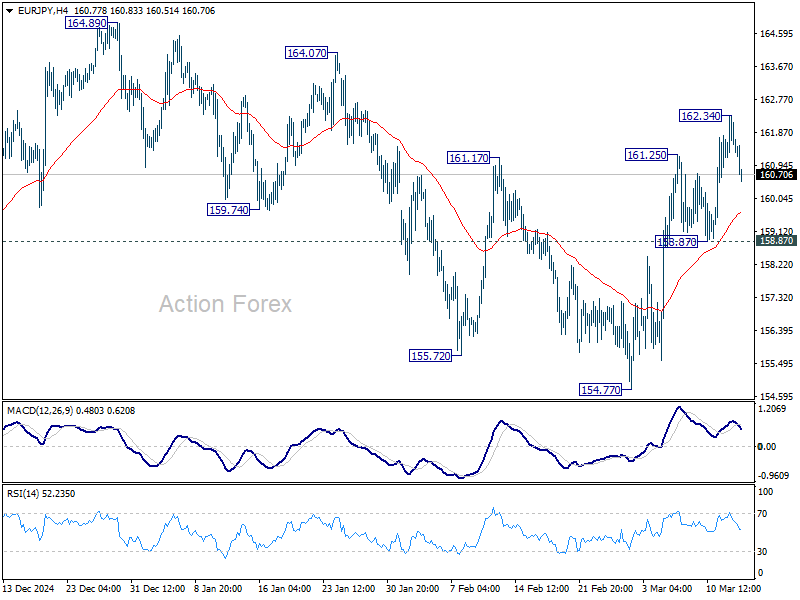

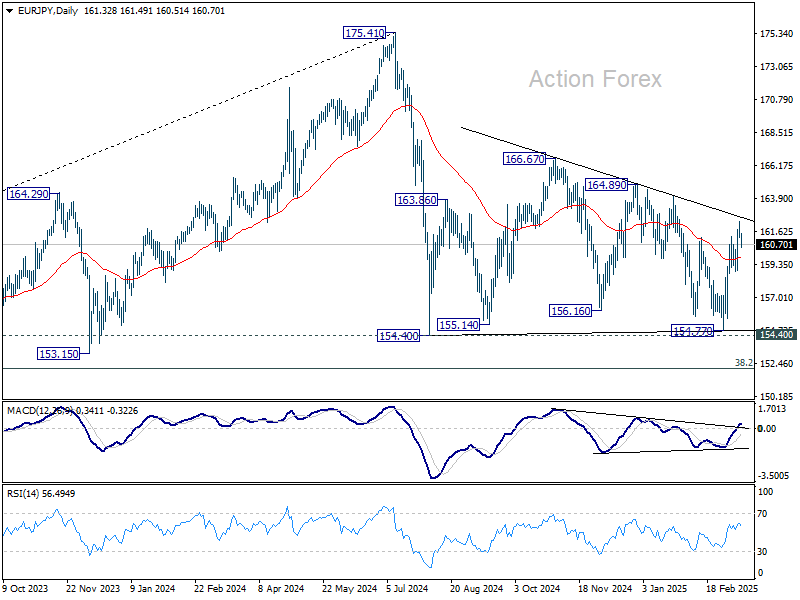

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.79; (P) 161.57; (R1) 162.21; More...

Intraday bias in EUR/JPY is turned neutral first with current retreat. Further rally is expected as long as 158.87 support holds. Above 162.34 will resume the rise from 154.77 to 164.89 resistance, as another rising leg in the consolidation pattern from 154.40.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

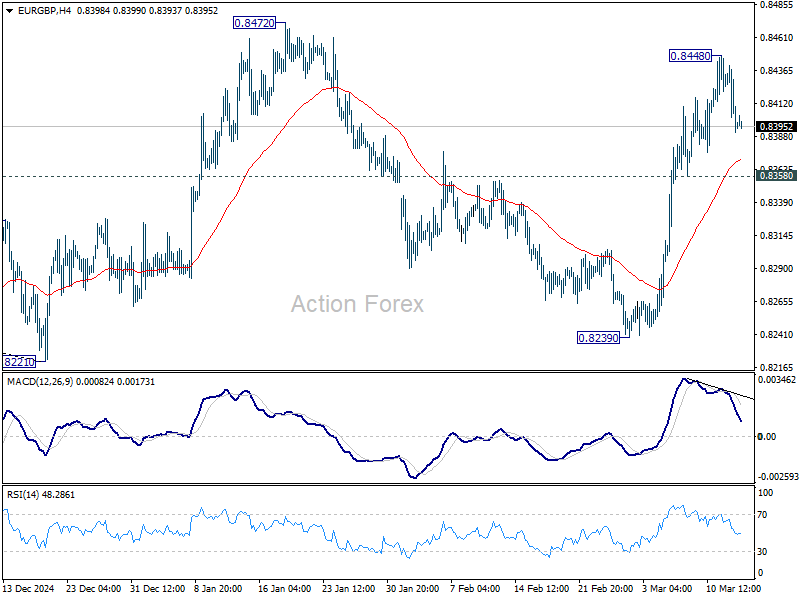

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8379; (P) 0.8411; (R1) 0.8429; More...

Intraday bias in EUR/GBP is turned neutral first with current retreat. Another rally is expected as long as 0.8358 support holds. Above 0.8448 will target 0.8472 resistance. Firm break there will resume whole rebound from 0.8221 to medium term falling channel resistance. Nevertheless, break of 0.8358 will suggest that rise from 0.8239 has completed and turn bias back to the downside instead.

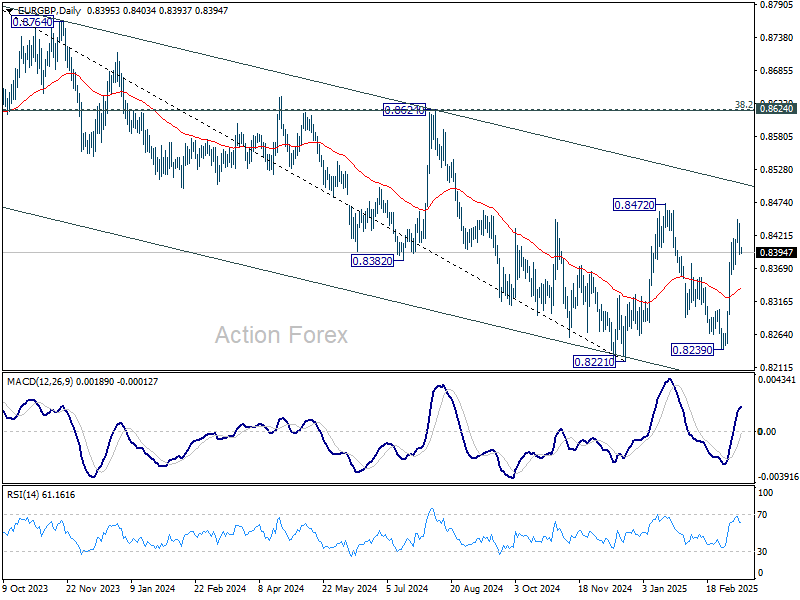

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8506).

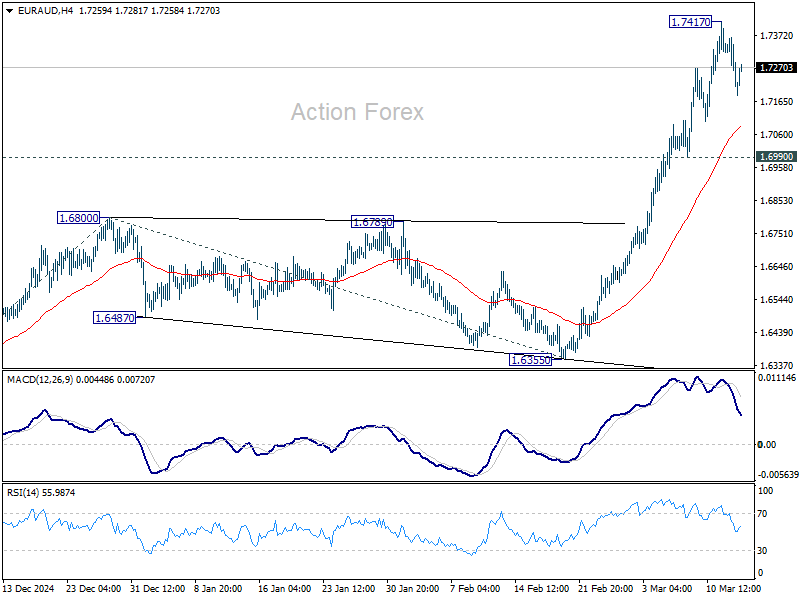

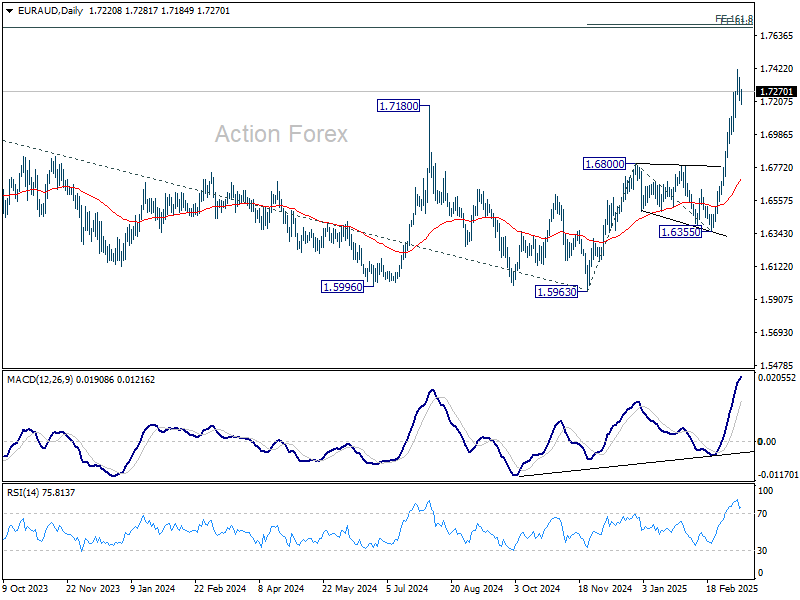

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7175; (P) 1.7271; (R1) 1.7321; More...

Intraday bias in EUR/AUD is turned neutral with current retreat. Some consolidations should be seen first. But downside should be contained by 0.6990 support to bring rebound. Meanwhile, break of 1.7417 will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

In the bigger picture, up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 key resistance will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6355 support holds, even in case of deep pullback.

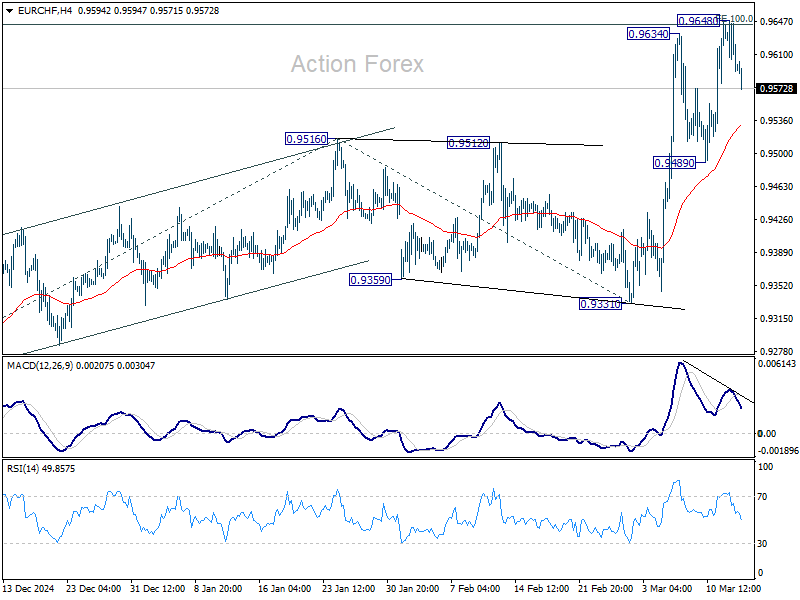

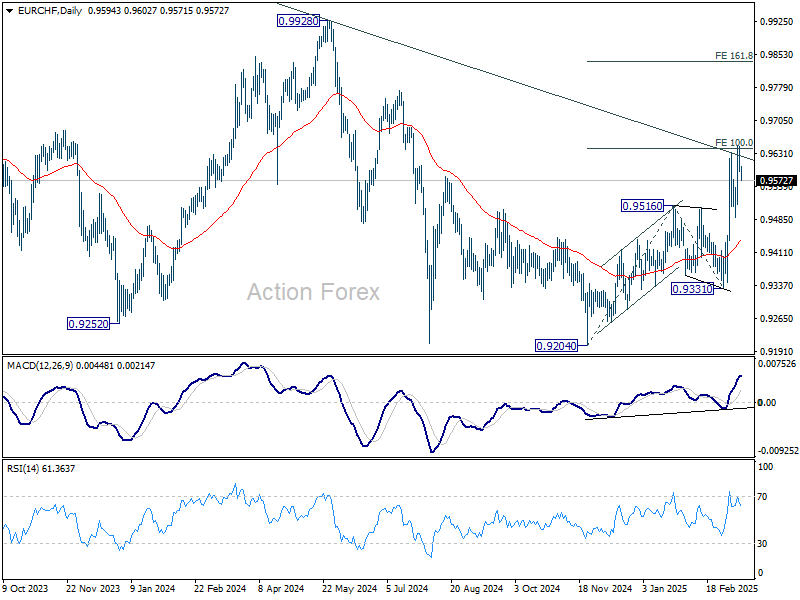

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9582; (P) 0.9617; (R1) 0.9635; More....

Intraday bias in EUR/CHF is turned neutral as it retreated after failing to sustain above 100% projection of 0.9204 to 0.9516 from 0.9331 at 0.9643. Further rally is expected as long as 0.9489 support holds. Firm break of 0.9643 will pave the way to 161.8% projection at 0.9836 next.

In the bigger picture, the strong break of 55 W EMA (now at 0.9482) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9620) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be see to 0.9928 key resistance at least.

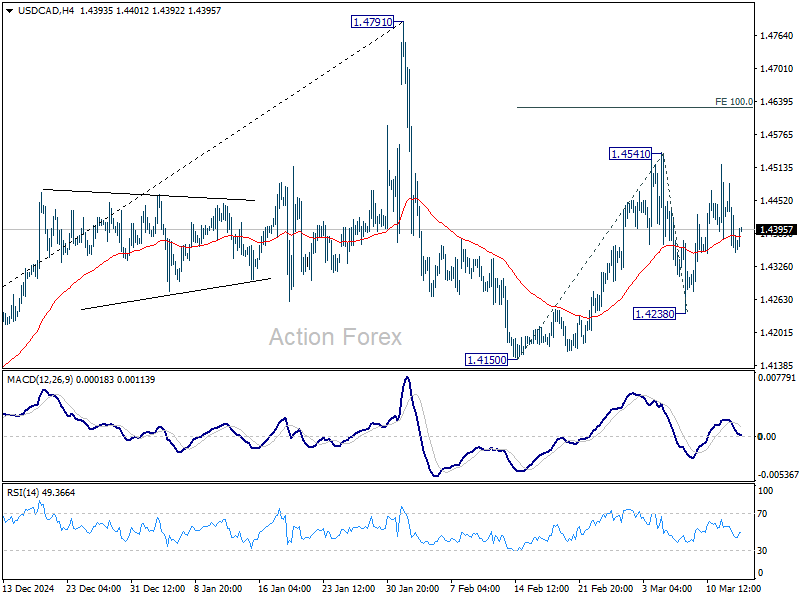

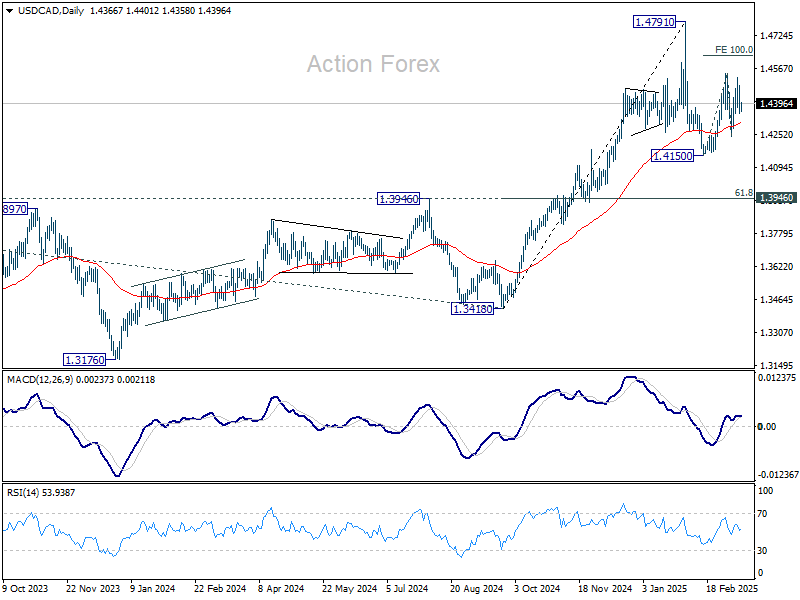

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4322; (P) 1.4404; (R1) 1.4454; More...

Intraday bias in USD/CAD remains neutral for the moment. Price actions from 1.4791 high are seen as a corrective pattern, with rebound from 1.4150 as the second leg. On the upside, break of 1.4541 will target 100% projection of 1.4150 to 1.4541 from 1.4238 at 1.4629 and above. But for now, strong resistance is expected from 1.4791 to limit upside to bring the third leg. On the downside, break of 1.4238 will confirm that the third leg has started through 1.4150 support.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

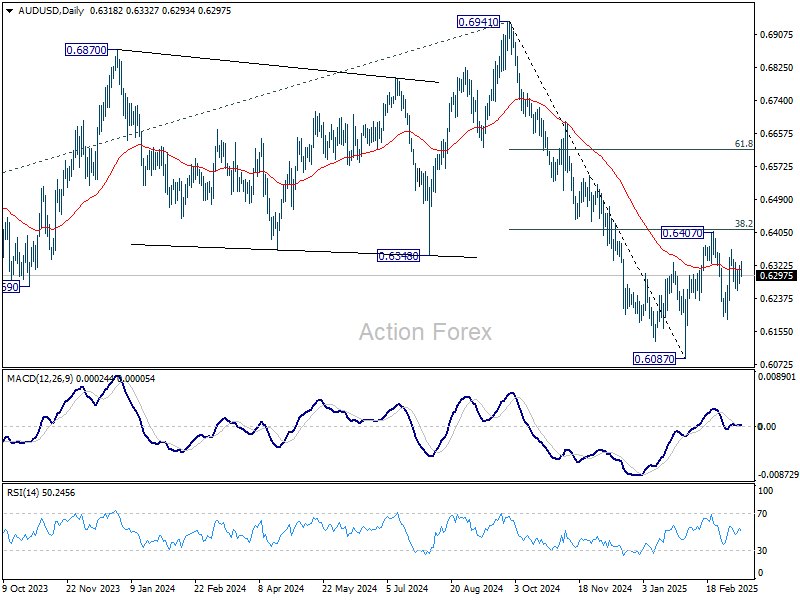

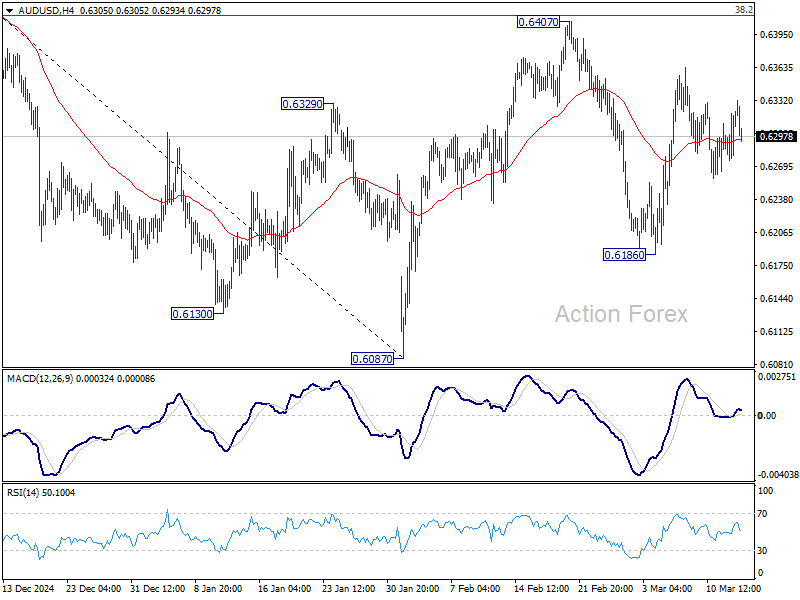

AUD/USD Daily Report

Daily Pivots: (S1) 0.6290; (P) 0.6307; (R1) 0.6337; More...

Intraday bias in AUD/USD remains neutral as range trading continues. On the downside, break of 0.6186 will target 0.6087 support first. Firm break there will resume whole decline from 0.6941. However, sustained trading above 38.2% retracement of 0.6941 to 0.6087 at 0.6413 will raise the chance of near term bullish reversal, and target 61.8% retracement at 0.6615 next.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6487) holds.