Sample Category Title

BoC lowers rates to 2.75%, warns monetary policy can’t counter trade war fallout

BoC delivered a widely expected 25bps rate cut, bringing the overnight rate down to 2.75%. In its statement, BoC highlighted that the rapidly evolving trade policies are injecting "more-than-usual uncertainty" into economic outlook.

The central bank acknowledged that escalating trade tensions and newly imposed US tariffs could dampen economic growth while simultaneously increasing inflationary pressures. It emphasized that monetary policy "cannot offset the impacts of a trade war".

Nonetheless, BoC noted that it is committed to preventing higher prices from driving ongoing inflation. Governing Council members will carefully monitor the downward pressures on inflation stemming from a weaker economy with the upward pressures resulting from higher costs tied to tariffs and other trade barriers.

(BOC) Bank of Canada reduces policy rate by 25 basis points to 2¾%

The Bank of Canada today reduced its target for the overnight rate to 2.75%, with the Bank Rate at 3% and the deposit rate at 2.70%.

The Canadian economy entered 2025 in a solid position, with inflation close to the 2% target and robust GDP growth. However, heightened trade tensions and tariffs imposed by the United States will likely slow the pace of economic activity and increase inflationary pressures in Canada. The economic outlook continues to be subject to more-than-usual uncertainty because of the rapidly evolving policy landscape.

After a period of solid growth, the US economy looks to have slowed in recent months. US inflation remains slightly above target. Economic growth in the euro zone was modest in late 2024. China’s economy has posted strong gains, supported by government policies. Equity prices have fallen and bond yields have eased on market expectations of weaker North American growth. Oil prices have been volatile and are trading below the assumptions in the Bank’s January Monetary Policy Report (MPR). The Canadian dollar is broadly unchanged against the US dollar but weaker against other currencies.

Canada’s economy grew by 2.6% in the fourth quarter of 2024 following upwardly revised growth of 2.2% in the third quarter. This growth path is stronger than was expected at the time of the January MPR. Past cuts to interest rates have boosted economic activity, particularly consumption and housing. However, economic growth in the first quarter of 2025 will likely slow as the intensifying trade conflict weighs on sentiment and activity. Recent surveys suggest a sharp drop in consumer confidence and a slowdown in business spending as companies postpone or cancel investments. The negative impact of slowing domestic demand has been partially offset by a surge in exports in advance of tariffs being imposed.

Employment growth strengthened in November through January and the unemployment rate declined to 6.6%. In February, job growth stalled. While past interest rate cuts have boosted demand for labour in recent months, there are warning signs that heightened trade tensions could disrupt the recovery in the jobs market. Meanwhile, wage growth has shown signs of moderation.

Inflation remains close to the 2% target. The temporary suspension of the GST/HST lowered some consumer prices, but January’s CPI was slightly firmer than expected at 1.9%. Inflation is expected to increase to about 2½% in March with the end of the tax break. The Bank’s preferred measures of core inflation remain above 2%, mainly because of the persistence of shelter price inflation. Short-term inflation expectations have risen in light of fears about the impact of tariffs on prices.

While economic growth has come in stronger than expected, the pervasive uncertainty created by continuously changing US tariff threats is restraining consumers’ spending intentions and businesses’ plans to hire and invest. Against this background, and with inflation close to the 2% target, Governing Council decided to reduce the policy rate by a further 25 basis points.

Monetary policy cannot offset the impacts of a trade war. What it can and must do is ensure that higher prices do not lead to ongoing inflation. Governing Council will be carefully assessing the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs. The Council will also be closely monitoring inflation expectations. The Bank is committed to maintaining price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is April 16, 2025. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR at the same time.

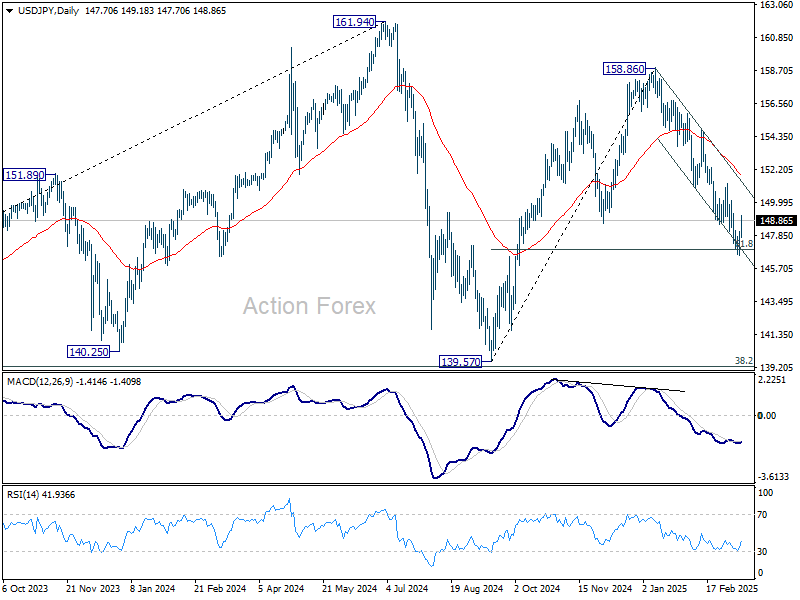

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.83; (P) 147.48; (R1) 148.41; More...

USD/JPY's recovery from 146.52 extends higher today, but it's still seen as part of a consolidation pattern. Intraday bias remains neutral for now. Upside should be limited by 150.92 support turned resistance. On the downside, sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

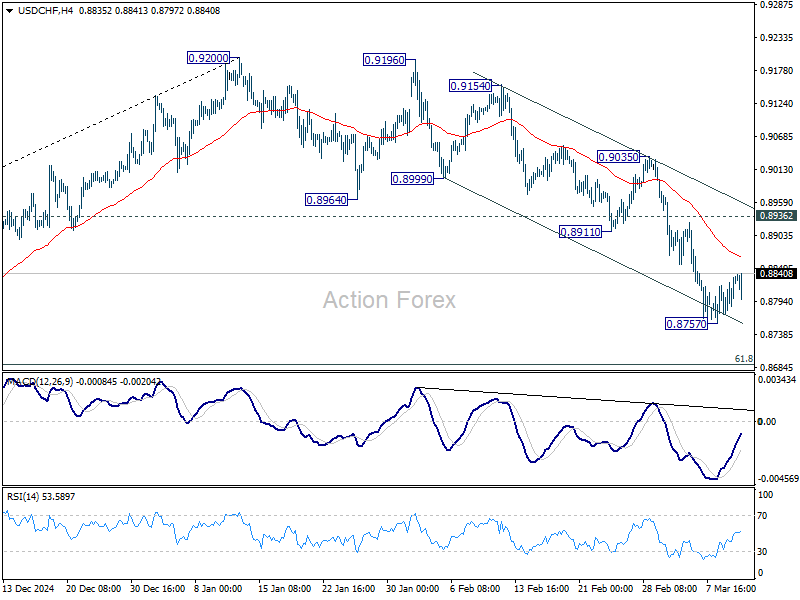

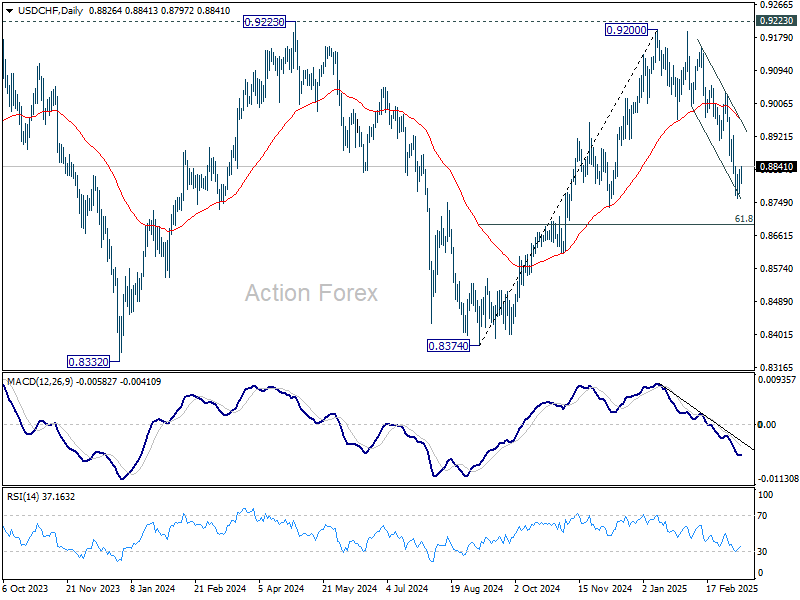

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8787; (P) 0.8812; (R1) 0.8850; More…

Intraday bias in USD/CHF remains neutral as consolidation from 0.8757 is in progress. Upside of recovery should be limited by 0.8911 support turned resistance to bring another fall. On the downside, below 0.8757 will resume the fall from 0.9200 and target 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

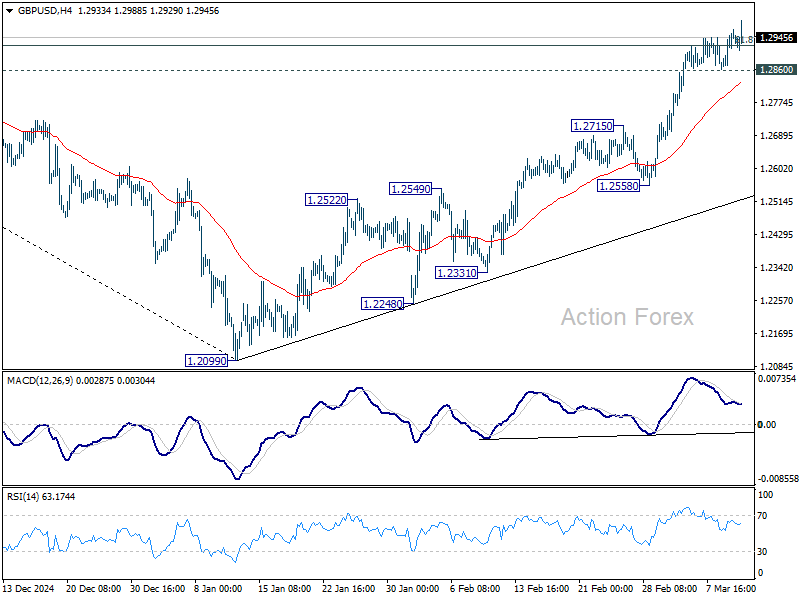

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2889; (P) 1.2927; (R1) 1.2989; More...

Intraday bias in GBP/USD is back on the upside for now. Sustained trading above 61.8% retracement of 1.3433 to 1.2099 at 1.2923 will resume the rise from 1.2099, and pave the way back to 1.3433 high. Nevertheless, break of 1.2860 support should indicate short term topping and bring deeper pullback.

In the bigger picture, fall from 1.3433 (2024 high) should have completed at 1.2099 as a corrective move. Up trend from 1.3051 (2022 low) is still in progress but it's too early to say that it's resuming. Corrective pattern from 1.3433 could extend with one more down leg. But after all, eventual upside breakout is expected at a later stage.

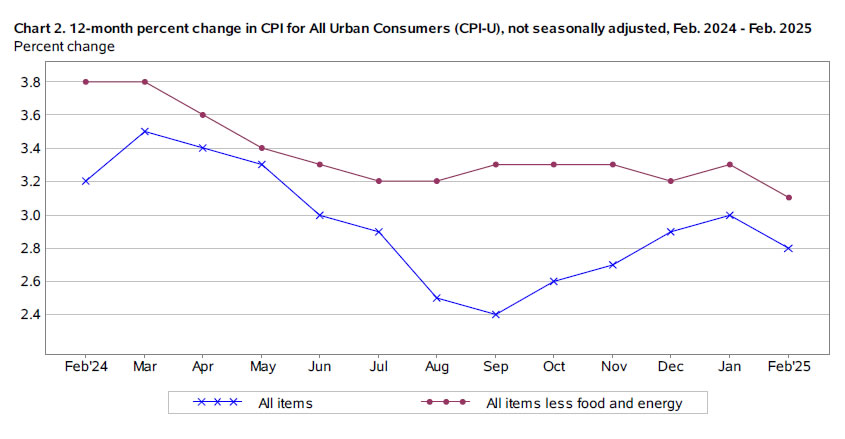

US: CPI Cools in February, But Likely to Pick Up Over the Coming Months as Tariff Effects Take Hold

The Consumer Price Index (CPI) rose 0.2% month-on-month (m/m) in February, or less than half of the monthly gain in January. On a twelve-month basis, CPI was up 2.8% (from 3.0% in January).

- Energy prices were relatively flat on the month, while food prices (+0.2% m/m) continued to edge higher and are up 2.6% on a year-ago basis.

Excluding food and energy, core inflation also rose 0.2% m/m – a tick below the consensus forecast – and a notable deceleration from the 0.45% m/m gain in January. The twelve-month change ticked down to 3.1% (from 3.3% in January), while the three-and-six-month annualized rates of change both sit at 3.6%.

A cooling in services price pressures was largely behind the slowdown in inflation last month, which were up a 'soft' 0.3% m/m (0.25% m/m unrounded) compared to a 0.5% m/m in January. On a year-ago basis, services prices remain somewhat elevated, up 4.1% y/y.

- Primary shelter costs rose 0.3% m/m and accounted for nearly half of the monthly increase in headline inflation.

- Meanwhile, price growth for non-housing services (aka "supercore") slowed to a modest 0.1% m/m gain following a hot 0.8% m/m rise in January. Encouragingly, price growth eased across categories that saw a significant uptick in January, including vehicle insurance (Feb: 0.3 m/m vs. Jan: 2.0% m/m) and travel costs (Feb: -1.5% m/m vs. Jan: +1.4% m/m).

Core goods prices rose 0.2% m/m, with notable gains in used vehicle prices (+0.9% m/m), apparel (+0.6% m/m), and home furnishings (+0.2% m/m).

Key Implications

Following a sharp uptick to start the year, price growth showed signs of cooling in February. While cooler services price pressures is welcome news, the uptick in apparel and home furnishing costs bear close watching in the months ahead. The additional 10% tariff on Chinese goods that came into effect on February 4th may be already having an impact on consumer prices.

Since February, the U.S. administration has imposed an additional 10% tariff on China (effective March 4th) as well as a 25% tariff on all steel & aluminum imports (effective March 12th). It remains to be seen whether the currently paused tariffs on Canada and Mexico as well as the reciprocal tariffs will be implemented on April 2nd. But both the ISM surveys showed a sharp uptick in the 'prices paid' sub-component in February, suggesting price pressures are building further up the supply chain. These are likely to show up in consumer prices over the coming months. As a result, the Federal Reserve is likely to sit tight for now and wait for more clarity on the policy and inflation front before making its next move. Fed futures barely budged post-CPI release and are still showing the next quarter-point rate cut to come in June.

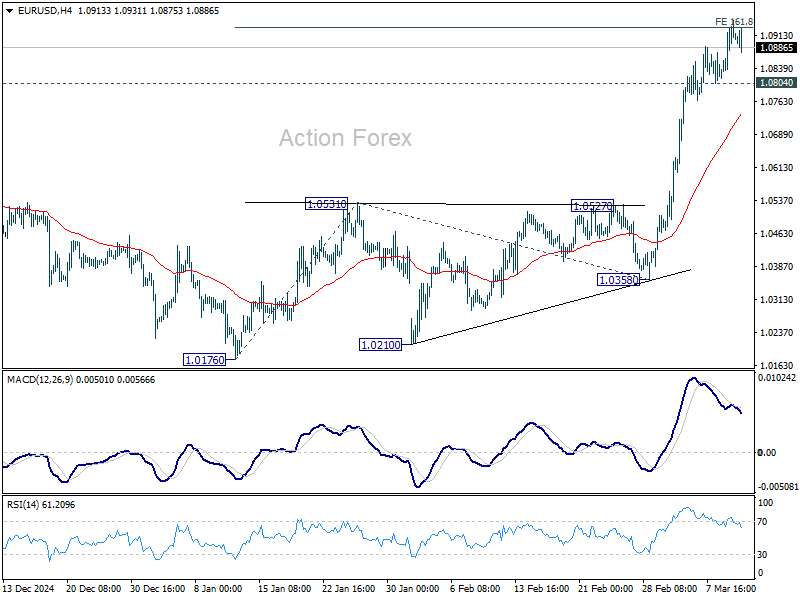

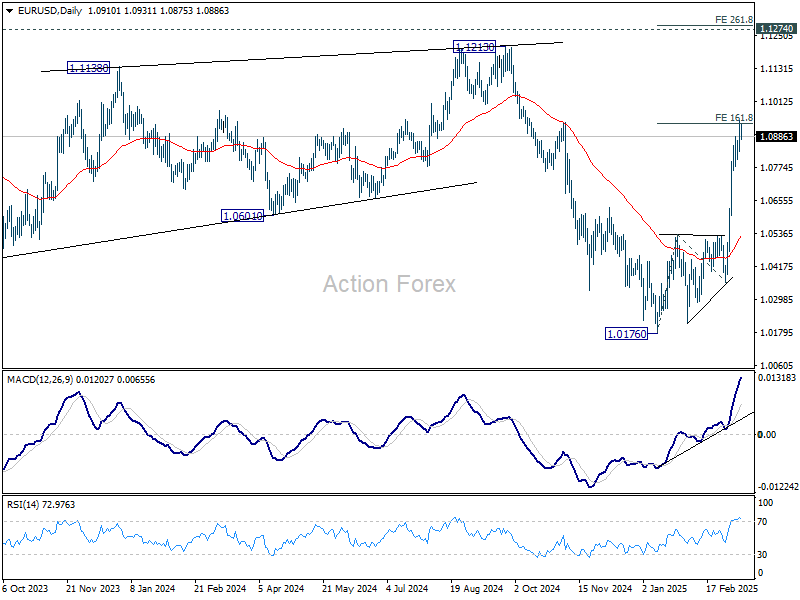

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0849; (P) 1.0898; (R1) 1.0968; More...

While EUR/USD continues to lose momentum as seen in 4H MACD, there is no clear sign that a correction is imminent yet. Further rise is in favor as long as 1.0804 support holds. Sustained trading above 161.8% projection of 1.0176 to 1.0531 from 1.0358 at 1.0932 will target 261.8% projection at 1.1287, which is slightly above 1.1274 key resistance. Nevertheless, firm break of 1.0804 should now indicate short term topping, and bring deeper pullback.

In the bigger picture, the strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

Dollar Struggles for Direction as Softer CPI Fails to Trigger Major Moves

Dollar is struggling to find a definitive direction in early US session, even after the softer-than-expected Consumer Price Index report offered fresh evidence of easing inflation pressures. Annual core CPI now sits at its lowest level since 2021, a development that should bring some relief to both the Fed and markets. However, the data release has not sparked a substantial move in the greenback, as lingering tariff concerns keep traders in a wait-and-see mode.

The most immediate market reactions have been more evident in equities and bonds. US stock futures are rebounding on the prospect of Fed easing sooner. Funds are flowing out of bonds, pushing the benchmark 10-year Treasury yield higher. Yet overall market caution remains elevated, with tariffs casting a shadow over trade and growth prospects.

For now, Canadian Dollar is currently in the lead for the day, although BoC’s upcoming rate decision could quickly change that dynamic. Dollar is the second-best performer on the day, followed by the British pound. At the other end of the spectrum, Japanese Yen is faring the worst, trailed by Euro, which is digesting recent strong gains, and then Australian Dollar. New Zealand Dollar and Swiss Franc are hovering in the middle of the pack.

Technically, USD/JPY's rebound today is much more due to Yen's pullback then Dollar's strength. Price actions from 146.52 are still viewed as a corrective pattern. Upside should be limited by 150.92 support turned resistance. Fall from 158.86 is expected to resume through 146.52 after the corrective pattern completes.

In Europe, at the time of writing, FTSE is up 0.50%. DAX is up 1.87%. CAC is up 1.35%. UK 10-year yield is up 0.054 at 4.684. Germany 10-year yield is up 0.038 at 2.934. Earlier in Asia, Nikkei rose 0.07%. Hong Kong HSI fell -0.76%. China Shanghai SSE fell -0.23%. Singapore Strait Times rose 0.19%. Japan 10-year JGB yield rose 0.017 to 1.524.

US core CPI falls to 3.1%, lowest since 2021

US consumer inflation slowed more than expected in February. Headline CPI rose just 0.2% mom, below forecasts of 0.3% mom. Core CPI, which excludes food and energy, also increased by 0.2% mom, missing expectations of 0.3% mom.

On an annual basis, inflation eased to 2.8% yoy from 3.0% yoy in January. Core CPI fell from 3.3% yoy to 3.1% yoy, the lowest level since April 2021. The deceleration in price pressures suggests that disinflationary momentum is gradually resuming after months of stubbornly high core readings.

ECB's Lagarde stresses commitment to price stability amid exceptional high uncertainty

ECB President Christine Lagarde highlighted the "exceptionally high" level of global uncertainty in her speech today, highlighting the challenges posed by trade policy shifts and geopolitical tensions.

She noted that an index measuring trade policy uncertainty is now close to 350—more than six times its average value since 2021. Geopolitical risk indicators are at levels unseen since the Cold War, aside from periods of war and major terrorist attacks.

Against this backdrop, Lagarde emphasized that ECB’s primary focus remains on maintaining price stability over the medium term, stressing that this commitment is "more important than ever" in an unpredictable economic environment.

To achieve this, Lagarde stressed the need for "agility to respond to new shocks" while maintaining a structured policy framework that prevents "short-sighted reactions and unbridled discretion".

She also noted the importance of combining agility with clarity, stating that while the ECB may not always be able to provide certainty about the exact path of interest rates, it can ensure "clarity about our reaction function".

BoJ’s Ueda acknowledges rising yields as market bets on policy shift

BoJ Governor Kazuo Ueda addressed the recent rise in bond yields, and noted, "I don't see a big divergence between our view and that of markets".

Speaking to parliament, Ueda emphasized the "biggest determinant" of long-term interest rates is market expectations regarding the central bank’s short-term policy rate.

He added, it is "natural for long-term rates to move in a way that reflects such market forecasts". His comments come as Japan’s benchmark 10-year bond yield surged to a 16-year high of 1.575% on Monday.

Separately, Japan’s latest inflation data showed that annual wholesale inflation slowed slightly in February. Corporate goods price index , which tracks the prices businesses charge each other for goods and services, rose 4.0% yoy, in line with market expectations, down from January’s 4.2% yoy increase.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0849; (P) 1.0898; (R1) 1.0968; More...

While EUR/USD continues to lose momentum as seen in 4H MACD, there is no clear sign that a correction is imminent yet. Further rise is in favor as long as 1.0804 support holds. Sustained trading above 161.8% projection of 1.0176 to 1.0531 from 1.0358 at 1.0932 will target 261.8% projection at 1.1287, which is slightly above 1.1274 key resistance. Nevertheless, firm break of 1.0804 should now indicate short term topping, and bring deeper pullback.

In the bigger picture, the strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

US core CPI falls to 3.1%, lowest since 2021

US consumer inflation slowed more than expected in February. Headline CPI rose just 0.2% mom, below forecasts of 0.3% mom. Core CPI, which excludes food and energy, also increased by 0.2% mom, missing expectations of 0.3% mom.

On an annual basis, inflation eased to 2.8% yoy from 3.0% yoy in January. Core CPI fell from 3.3% yoy to 3.1% yoy, the lowest level since April 2021. The deceleration in price pressures suggests that disinflationary momentum is gradually resuming after months of stubbornly high core readings.

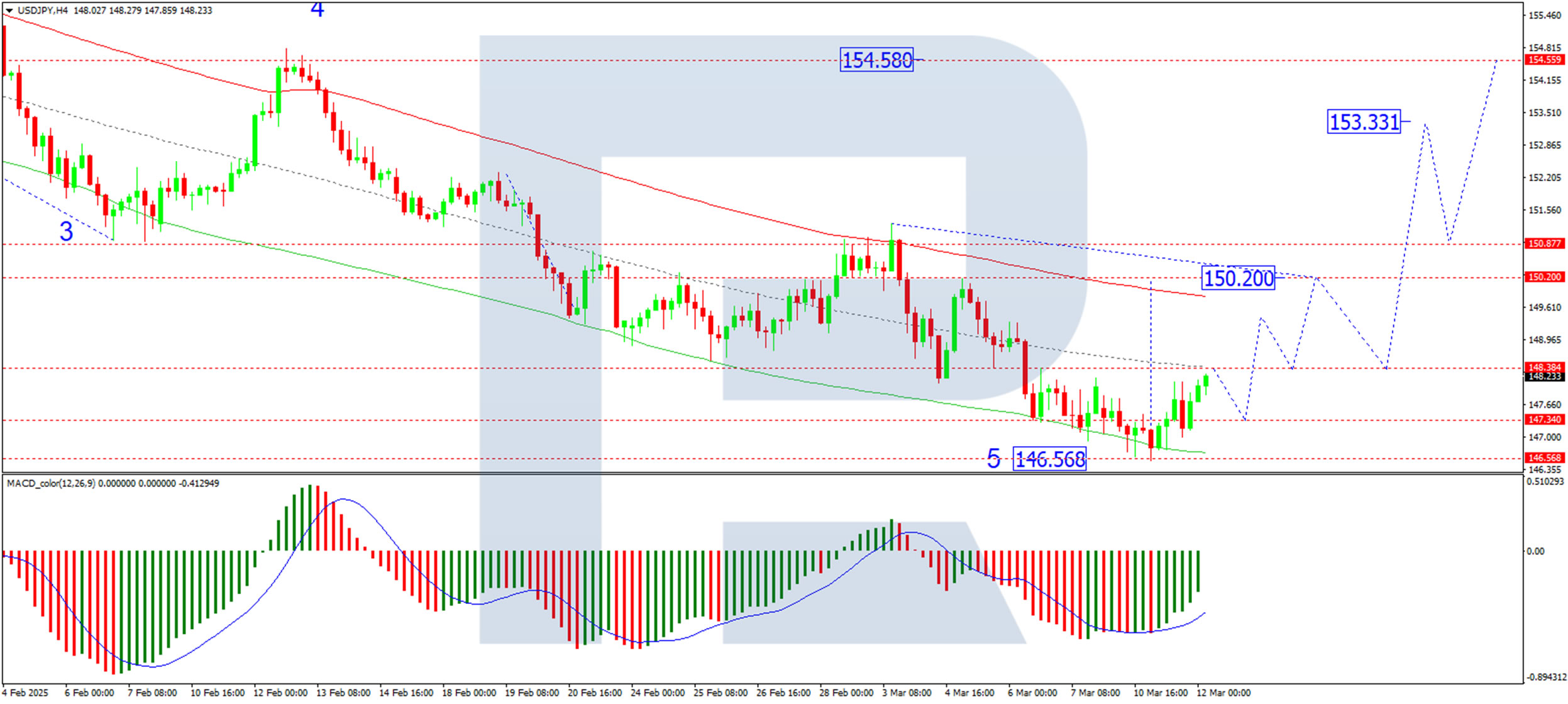

Japanese Yen Declines: Temporary Pause Amid Strong Long-Term Outlook

USD/JPY climbed to 148.19 on Wednesday, marking its second consecutive session of gains after touching a low of 146.53, its weakest level since 4 October 2024. While this movement partly resembles a technical rebound, broader market conditions appear to shift, influencing the yen’s trajectory.

Key market factors affecting USD/JPY

Bank of Japan (BoJ) Governor Kazuo Ueda stated that it is natural for bond yields to reflect market expectations regarding short-term interest rates. He downplayed the significance of any divergence between the BoJ’s stance and market sentiment.

Despite this, financial markets continue to bet on the BoJ sticking to its interest rate hike strategy for 2025. Japan’s latest inflation data further strengthens this view.

The Consumer Price Index (CPI) for January 2025 surged to 4.0%, the highest since January 2023. The primary driver was food prices, which spiked 7.8% y/y, while rising electricity and gas prices also contributed to overall inflation. Meanwhile, core inflation hit a 19-month high at 3.2%.

Given this inflationary environment, the BoJ remains pressured to maintain its tightening cycle, a strong supporting factor for the yen over the longer term.

Technical analysis of USD/JPY

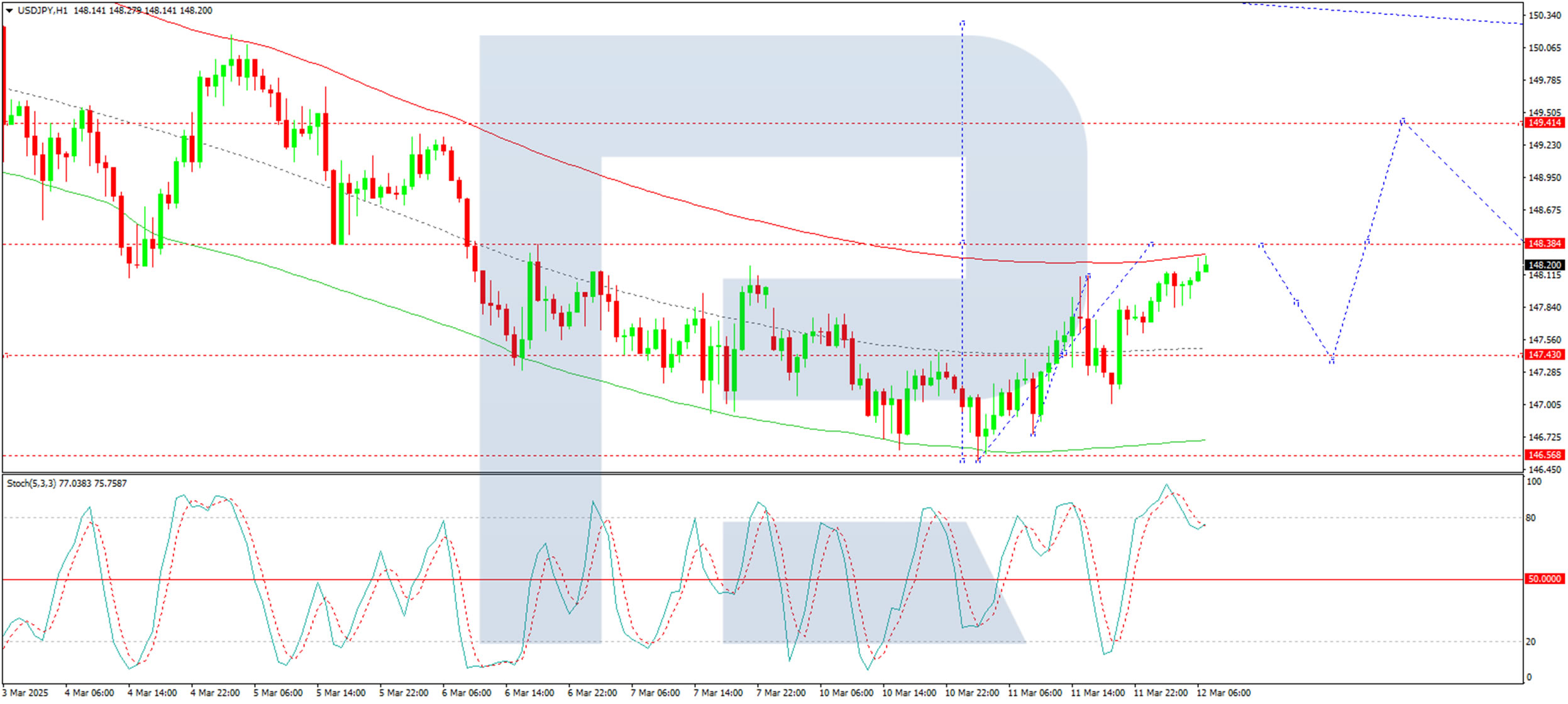

On the H4 chart, USD/JPY is developing a growth wave targeting 148.38. After reaching this level, a correction towards 147.34 may follow, outlining the consolidation range at the recent lows. If the price breaks upwards, the pair could extend gains towards 150.20, the next key resistance level. A correction to 148.38 could then occur. The MACD indicator supports this outlook, with its signal line below zero but pointing strictly upwards, indicating bullish momentum.

On the H1 chart, the pair is forming a growth wave towards 148.38, marking the first key target. A potential pullback to 147.34 may follow before a renewed push higher towards 149.40, the next local target. The Stochastic oscillator confirms this scenario, with its signal line above 50 and trending upwards, suggesting continued buying pressure.

Conclusion

USD/JPY is experiencing a short-term rebound, with market sentiment driving the pair higher amid shifting rate expectations. However, the BoJ’s stance and Japan’s strong inflation figures provide longer-term support for the yen, keeping the broader outlook mixed.

In the near term, 148.38 remains a key resistance level, with the potential for further gains towards 150.20 if bullish momentum persists. A corrective pullback to 147.34 could provide a buying opportunity before the next upward wave towards 149.40. Market participants will closely watch economic developments and BoJ policy signals to determine the yen’s next move.