Sample Category Title

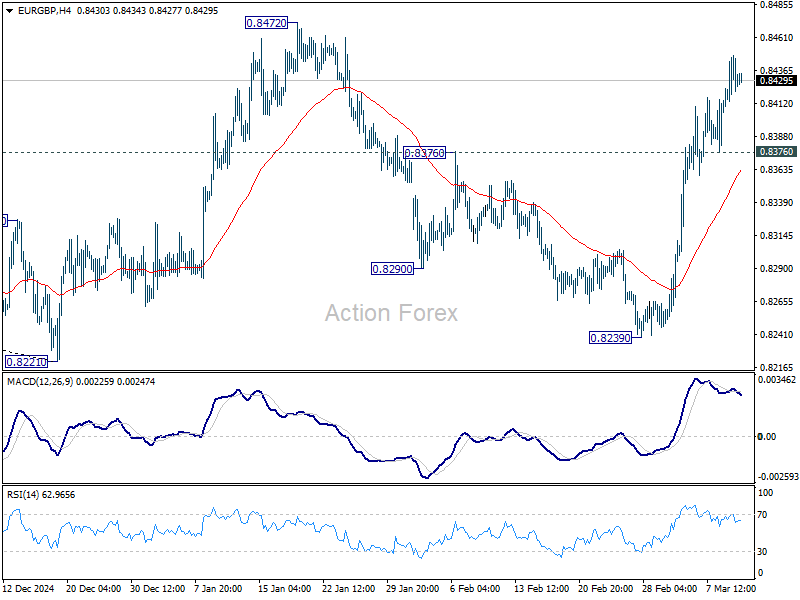

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8409; (P) 0.8429; (R1) 0.8453; More...

Intraday in EUR/GBP remains on the upside as rise from 0.8239 is still in progress for 0.8472 resistance. Firm break there will remain whole rebound from 0.8221 to medium term falling channel resistance. On the downside, below 0.8376 will turn bias neutral and bring consolidations again.

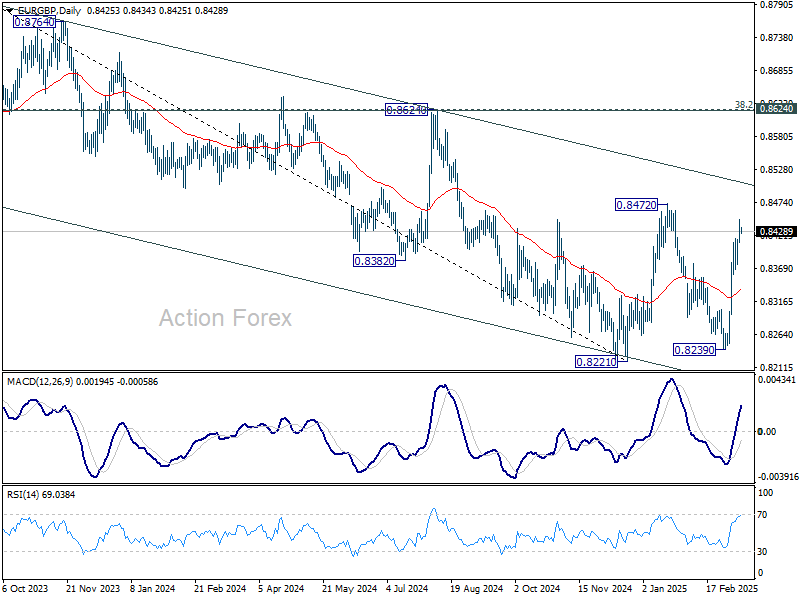

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8506).

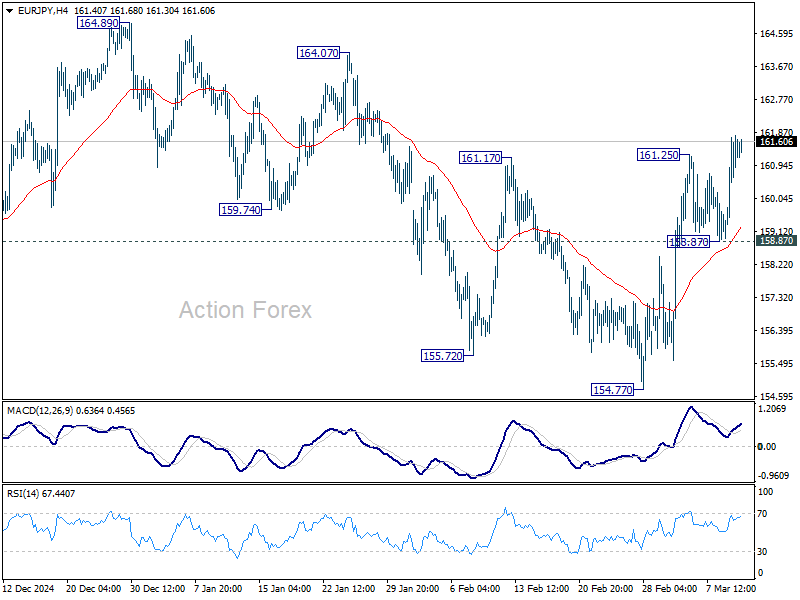

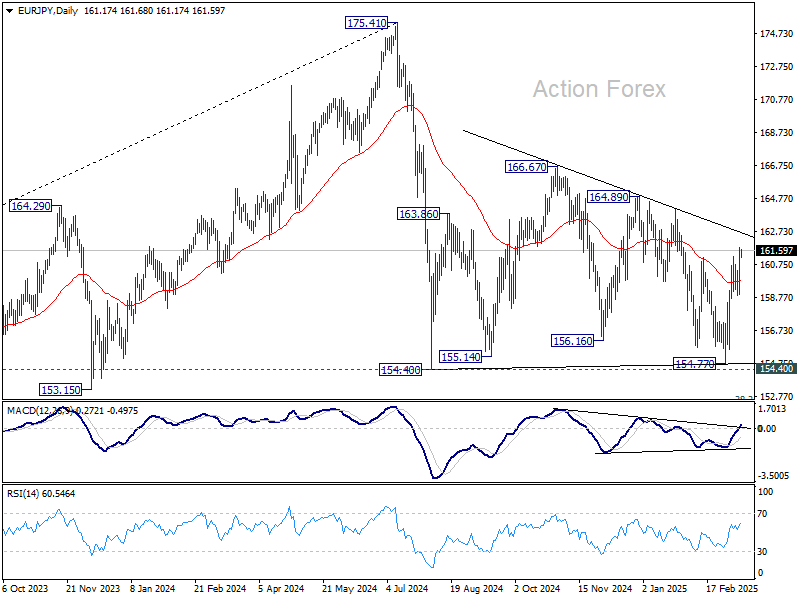

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.62; (P) 160.71; (R1) 162.44; More...

Intraday bias in EUR/JPY stays on the upside for the moment. Rise from 154.77 is seen as another rising leg in the consolidation pattern from 154.40. Next target is 164.89 resistance. For now, further rally is expected as long as 158.87 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

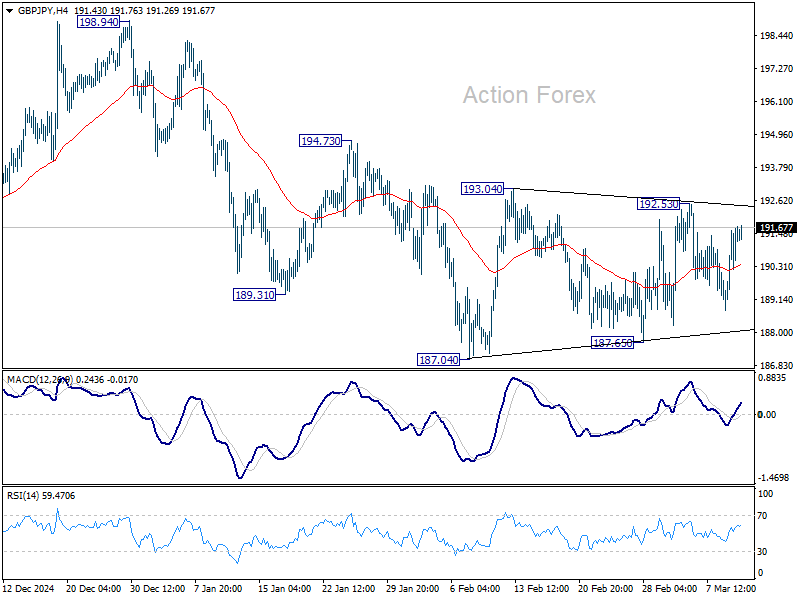

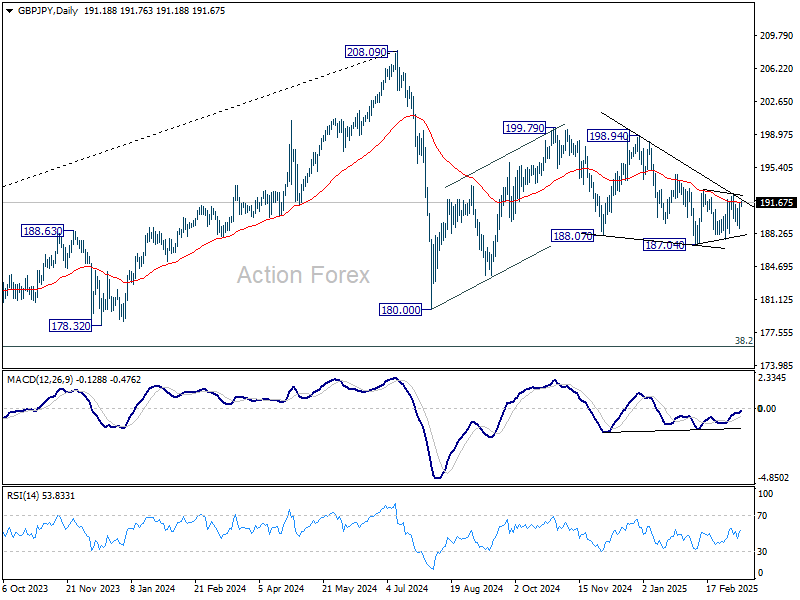

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.56; (P) 190.62; (R1) 192.44; More...

Intraday bias in GBP/JPY stays neutral as range trading continues. On the upside, firm break of 192.53 will resume the rebound from 187.04 to 194.73 resistance, and then 198.94. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support. Overall, corrective pattern from 180.00 might still be extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

Talk Is Not Cheap

American and Canadian officials have spent the last few hours imposing tariffs on each other—only to roll them back —adding to the absurdity of the tariff situation. The problem is that this tariff charade has real-time consequences and that’s weighing on investor sentiment and pressuring market valuations.

American manufacturers are already paying significantly more for aluminum, steel, and copper than their overseas rivals as they rush to accumulate stocks before tariffs go live – which could happen overnight. The widening gap between the raw material prices paid by Americans versus their European and Asian peers is making the American manufacturers less cost-efficient compared to rivals, weighs on business confidence and fuels inflation even before the tariffs are imposed. And the expectation for squeezed profit margins due to actually rising raw material prices is weighing on market valuations.

As a consequence, the market volatility is rising as visibility becomes cloudier by the day, any market rebound may not be viable unless there is a form of stability in the White House – but that doesn’t seem to be on the menu du jour. The higher volatility will likely convince more investors to step out of their bullish positions. Given the high long positioning in the US assets, we could see the selloff extend.

All eyes on US CPI

The US will update its inflation numbers today and tomorrow, and the data is important. It’s important because the tariff situation will probably start to show in producer prices, then impact consumer prices in the continuation. As such, today’s CPI data is expected to show a slight easing for both headline and core inflation in February, and for both monthly and yearly figures. On Thursday, the PPI data may also show slower inflationary pressures for February. Afterall, the energy prices have been tumbling since the start of the year and that could counter the rise in food prices, especially the egg crisis. But whether the disinflation could continue is yet to be seen.

A set of inflation numbers in line with expectations, or ideally softer-than-expected, won’t guarantee that inflation will remain under control but will give a bigger margin to the Federal Reserve (Fed) to act if necessary. A set of inflation numbers above expectations, on the other hand, would be the sour cherry on top of an already staling cake. The higher the inflation the less likely the Fed will cut the rates, unless the market selloff gets ugly to an extent to threaten the financial stability.

The US dollar continues to lose value across the board on the expectation of a sharp US economic slowdown that could even lead to a recession in the second half. Activity on Fed funds futures hints that the first rate cut from the Fed is seen in June, but acceleration of the market selloff could pull the timeline to May. For now, the probability of a May cut is given around 60% chance.

Across the Atlantic, yesterday saw the selloff in the Stoxx 600 index accelerate. The initial sugar high due to massive spending plans is now replaced by negotiations across the political spectrum as the parties involved are trying to get a bigger part of the cake for themselves... But in fine, security comes first. Therefore, the European stocks should continue to outperform their US peers on converging growth expectations between the two continents. The convergence trade between the S&P500 and the Stoxx 600 should remain in play. Inflation from European defence spending could – at least in the short run - remain limited for specific sectors, which could eventually allow the European Central Bank (ECB) to keep its rates at a sweet spot to growth across Europe.

Anticipation Builds for US CPI

In focus today

Today's most important data release will be the US February CPI. We think headline CPI grew by +0.2% m/m SA and 2.8% y/y (Jan. +0.5% m/m SA and 3.0% y/y) and core CPI by +0.3% m/m SA and 3.2% y/y (Jan +0.4% m/m SA and 3.3% y/y). The previous January release surprised sharply to the topside and markets will closely follow if this was driven by one-off annual price increases at the beginning of the year, or if it was a sign of more persistent inflation pressures.

In Canada, the BoC is set to announce its policy rate decision, with markets and consensus favouring a 25bp rate cut. We also expect a 25bp rate rut, bringing the policy rate to 2.75%, as we anticipate the BoC will ensure the Canadian economy is well-protected against the impact of US tariffs.

Economic and market news

What happened overnight

In Japan, many of the big Japanese corporates, such as Toyota, the largest carmaker in the world, have decided to fully meet their labour unions' wage demands, which on average amounted to 6.1% this year. This follows what is expected to be very strong financial results for 2024. The big question is now whether the smaller companies, which employs most of the Japanese, also find room to meet wage demands. Strong wage growth is key for supporting domestic demand in Japan and a prerequisite for further rate hikes from the BoJ.

In geopolitics, delegations from Ukraine and the United States concluded discussions, with Ukraine agreeing to a 30-day US-brokered ceasefire. This led the US to agree to reinstate military assistance and intelligence sharing with Ukraine. The proposed ceasefire still requires Russia's acceptance. Both countries stated they had agreed to finalise a comprehensive agreement to develop Ukraine's critical mineral resources as soon as possible, following uncertainty after Zelenskyy's meeting at the White House.

In the US, 25% tariffs on steel and aluminium imports came into effect as exemptions concluded, despite increasing worries about the risk of a domestic recession. Yesterday, Trump initially threatened to increase tariffs to 50% on all steel and aluminium imports from Canada but later retracted after Ontario agreed to suspend the 25% surcharge. This caused fluctuations in financial markets, which were already unsettled by Trump's extensive tariff measures.

What happened yesterday

In the US, the JOLTs report showed that job openings remained relatively stable at 7.74m in January (cons: 7.63m, prior: 7.508m). Involuntary layoffs decreased, potentially boosting consumer sentiment despite prevailing uncertainties. Meanwhile, the NFIB index, measuring small business sentiment, weakened for a third straight month, marking its lowest reading since before the November election. This drop reflects owners' concerns over tariff and spending cut plans, showcasing increased uncertainty among business owners.

Equities: The sell-off did not make Trump cave in, frankly the opposite as Trump doubled up on steel import tariffs at the US opening bell only to retreat at closing. As a result, the rebound in futures was absent and replaced by another day of declines. S&P 500 fell -0.8% - which means we are flirting with correction levels - Dow -1.1% while Nasdaq shaved off only -0.2% and Russell 2000 even rose 0.2%. Sector performance was a more buoyant reading than the headline though. Cyclicals outperformed defensives, although both were lower, with MAG 7 the notable outperformers, while equal-weighted S&P 500 was down more. European equities sold off heavily, Stoxx 500 -1.7%, but interestingly this was also a reflection of defensives selling off. Health care and consumer staples were actually the worst performing sectors, although cyclicals were weak as well. Futures are significantly higher in Europe this morning, as a potential ceasefire could be imminent in Ukraine. This could de-risk European equities and warrant more foreign equity inflows. US futures also a notch higher this morning.

FI & FX: Yesterday's FX session was generally characterized by an outperformance of European FX with the EUR, CEEs, SEK and NOK all being the outperformers while the JPY at the other end of the spectrum saw a slight setback. In FI-space the sell-off continued in the US and European markets as government bond yields rose and the curves steepened from the long end. 10Y German government bond yields rose some 6bp, while the 2Y segment declined 2bp. Furthermore, the Bund ASW-spread widened towards -13bp. In the US 10Y yields also rose 6bp like the move in the 2Y segment. Furthermore, there has been a rise in interest rate volatility, but we are not seeing much flight-to-quality as the 10Y BTPS-Bund spread remains fairly stable.

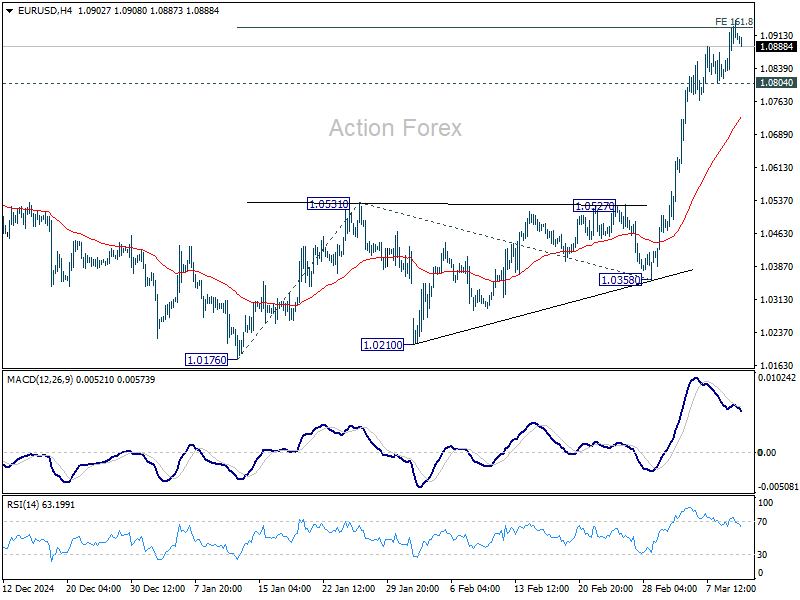

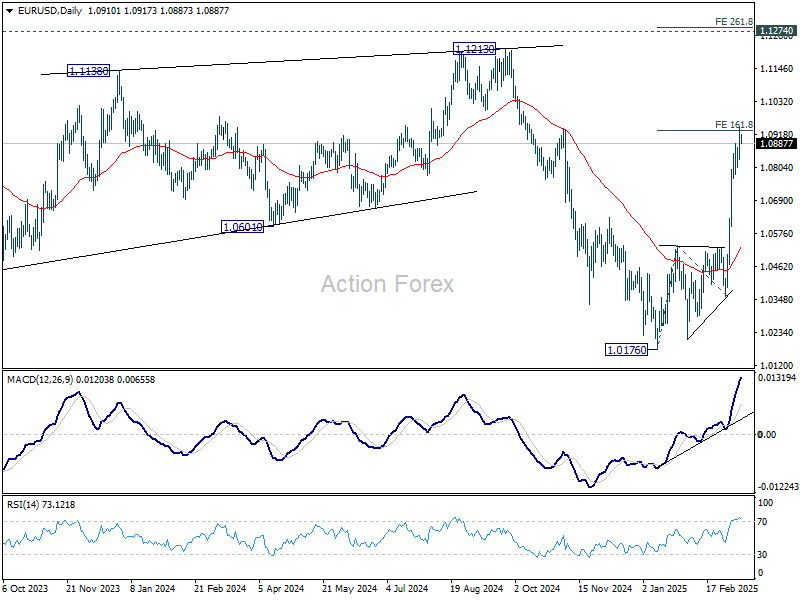

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0849; (P) 1.0898; (R1) 1.0968; More...

EUR/USD's rally continued and met 161.8% projection of 1.0176 to 1.0531 from 1.0358 at 1.0932 already. There is no clear sign of topping yet and intraday bias stays on the upside. Sustained trading above 1.0932 will target 261.8% projection at 1.1287, which is slightly above 1.1274 key resistance. On the downside, below 1.0804 support will turn intraday bias neutral again and bring consolidations.

In the bigger picture, the strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

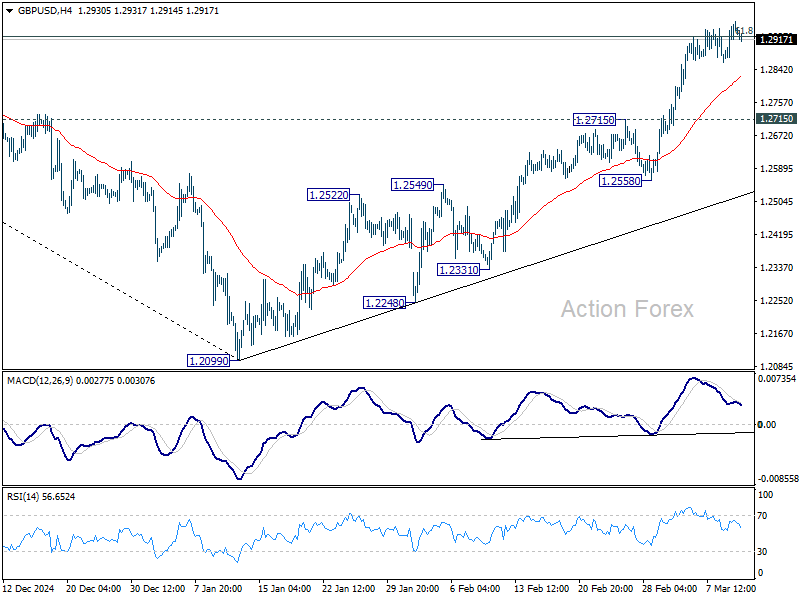

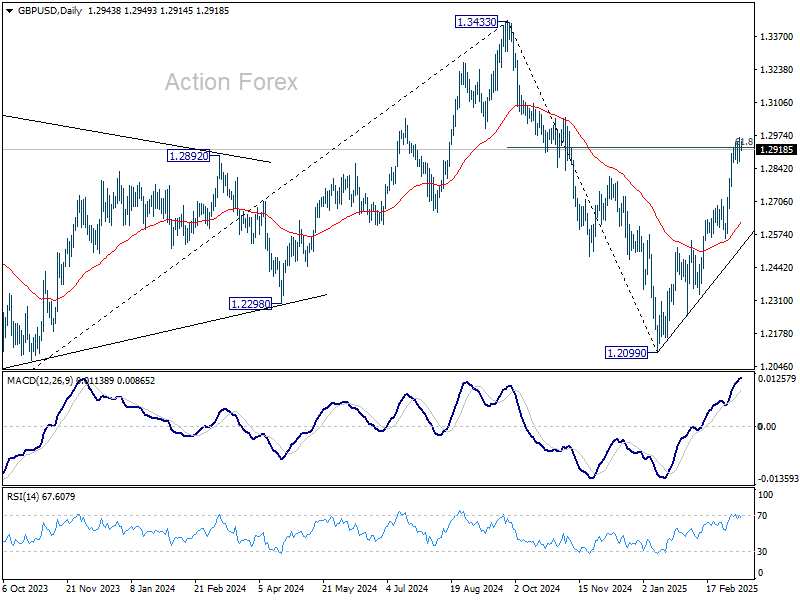

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2889; (P) 1.2927; (R1) 1.2989; More...

GBP/USD edged higher but failed to sustain above 61.8% retracement of 1.3433 to 1.2099 at 1.2923 so far. Intraday bias stays neutral first. IN case of another retreat, downside should be contained by 1.2715 resistance turned support to bring rebound. Sustained trading above 1.2923 will resume the rise from 1.2099, and pave the way back to 1.3433 high.

In the bigger picture, fall from 1.3433 (2024 high) should have completed at 1.2099 as a corrective move. Up trend from 1.3051 (2022 low) is still in progress but it's too early to say that it's resuming. Corrective pattern from 1.3433 could extend with one more down leg. But after all, eventual upside breakout is expected at a later stage.

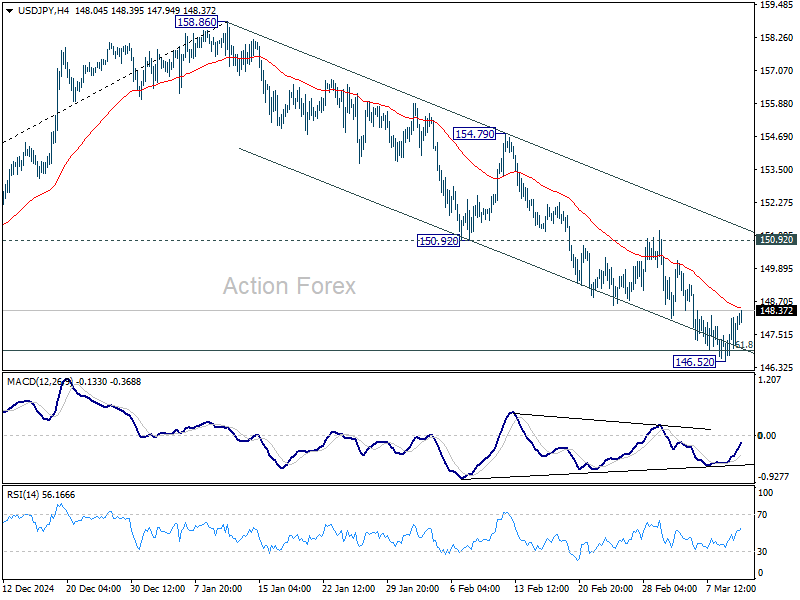

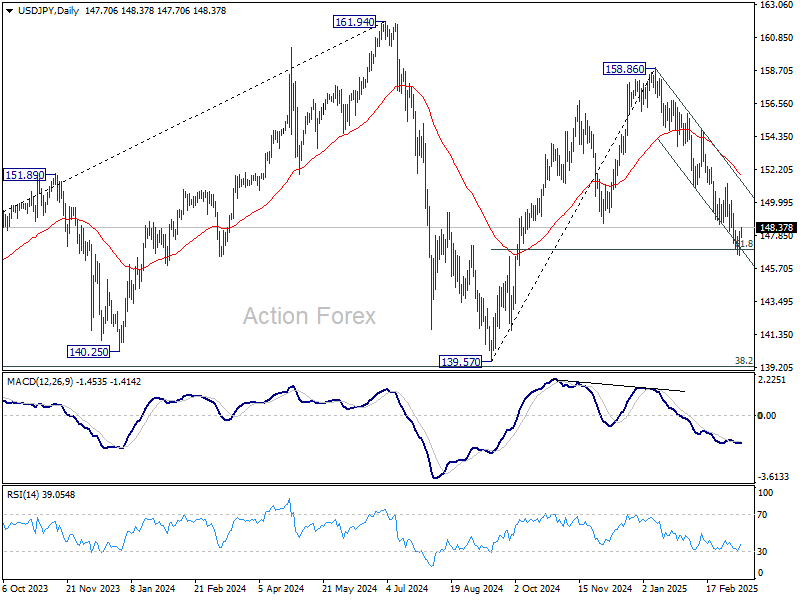

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.83; (P) 147.48; (R1) 148.41; More...

USD/JPY is extending consolidations above 146.52 and intraday bias remains neutral. Upside of recovery should be limited by 150.92 support turned resistance. On the downside, sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

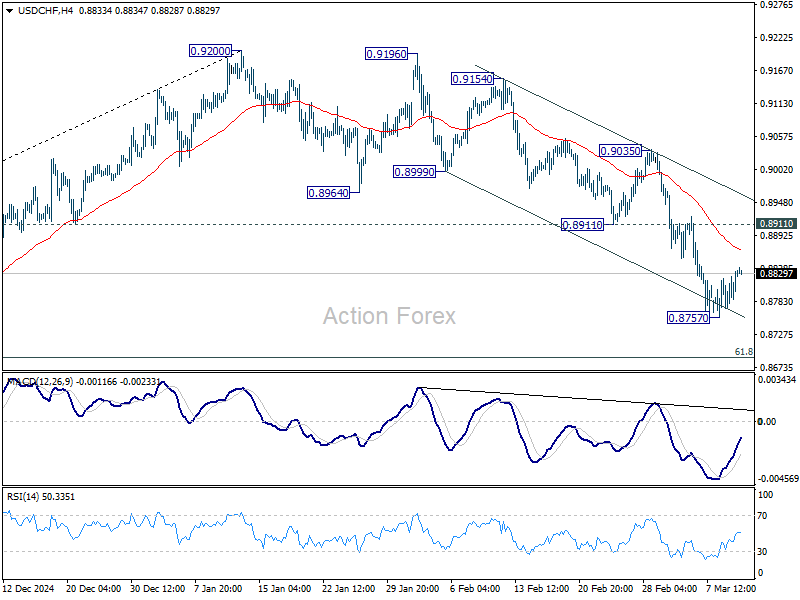

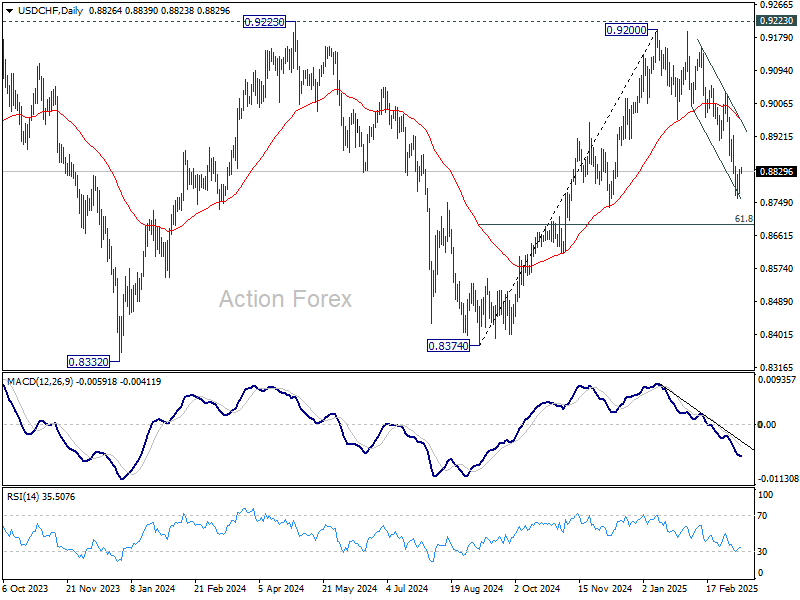

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8787; (P) 0.8812; (R1) 0.8850; More…

USD/CHF is extending consolidations above 0.8757 and intraday bias remains neutral. Upside of recovery should be limited by 0.8911 support turned resistance to bring another fall. On the downside, below 0.8757 will resume the fall from 0.9200 and target 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

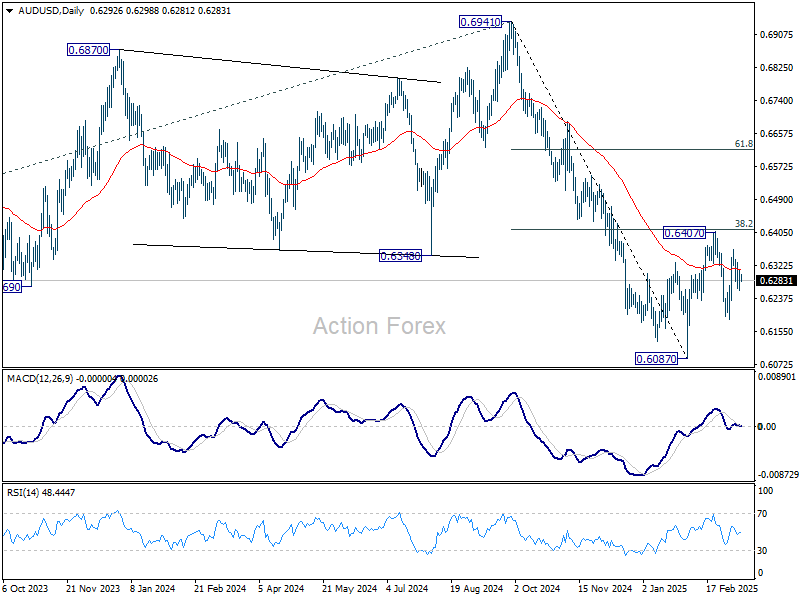

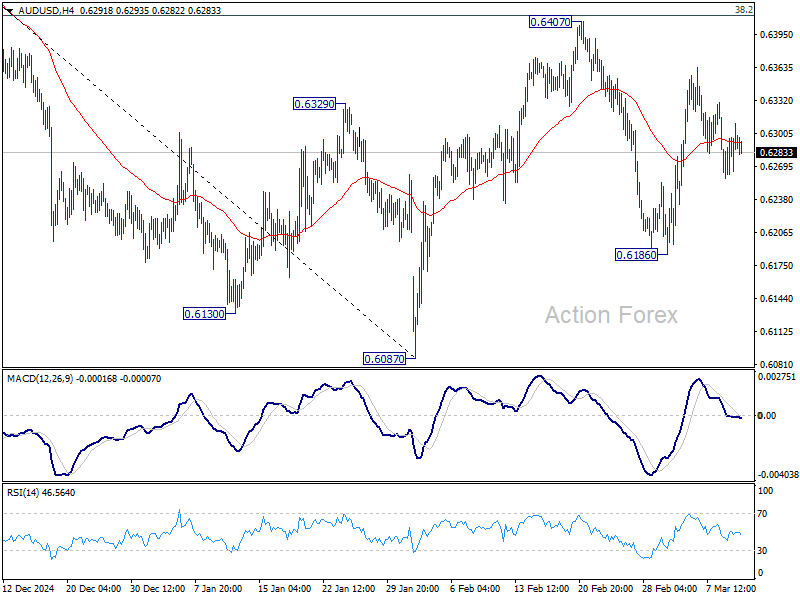

AUD/USD Daily Report

Daily Pivots: (S1) 0.6267; (P) 0.6290; (R1) 0.6320; More...

No change in AUD/USD's outlook as range trading continues. Intraday bias remains neutral at this point. On the downside, break of 0.6186 will target 0.6087 support first. Firm break there will resume whole decline from 0.6941. However, sustained trading above 38.2% retracement of 0.6941 to 0.6087 at 0.6413 will raise the chance of near term bullish reversal, and target 61.8% retracement at 0.6615 next.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6487) holds.