Sample Category Title

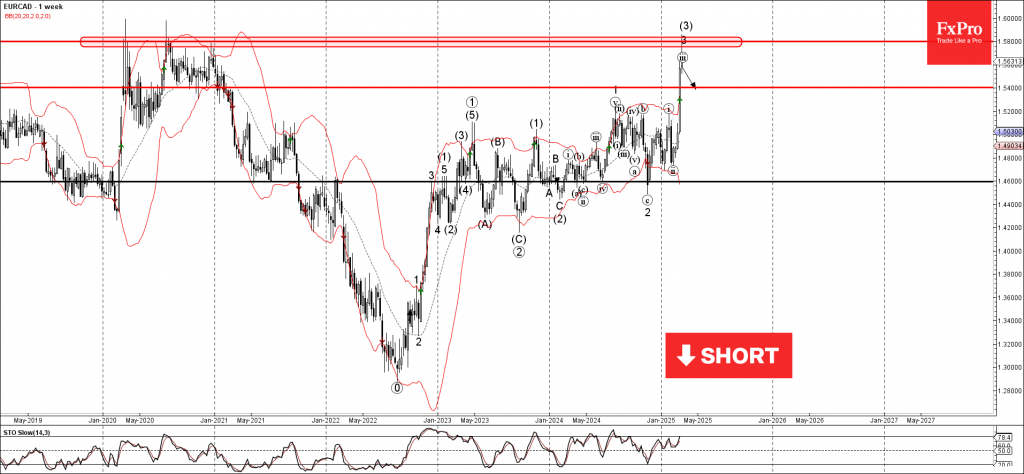

EURCAD Wave Analysis

EURCAD: ⬇️ Sell

- EURCAD reversed from the resistance area

- Likely to fall to support level 14.20

EURCAD currency pair recently reversed from the resistance area between the long-term resistance level 1.5800 (which has been reversing the price since the start of 2020) and the upper daily Bollinger Band.

The downward reversal from this resistance area stopped the previous upward impulse wave (3).

Given the strength of the resistance level 1.5800, EURCAD currency pair can be expected to fall to the next support level 14.20.

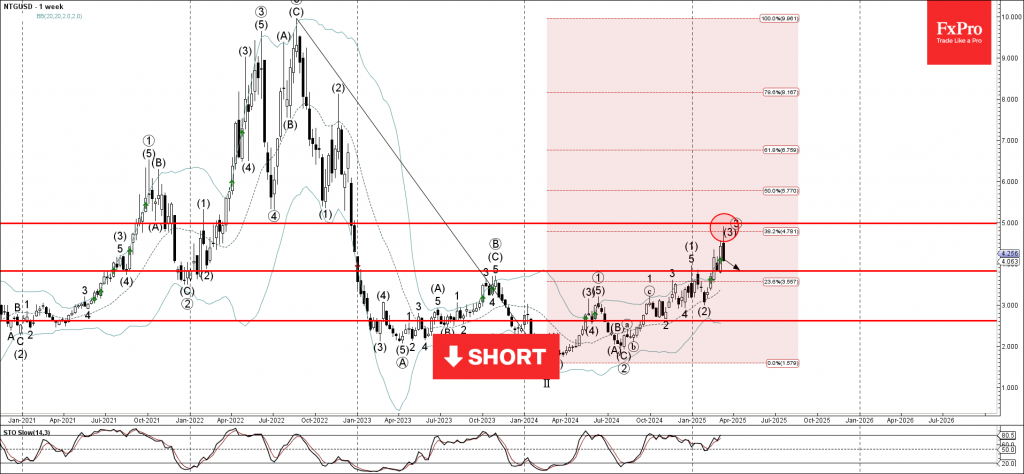

Natural Gas Wave Analysis

Natural gas: ⬇️ Sell

- Natural gas reversed from round resistance level 5.0000

- Likely to fall to support level 3.815

Natural gas recently reversed from the resistance area between the round resistance level 5.0000, the upper weekly Bollinger Band and the 38.2% Fibonacci correction of the downward impulse from 2022.

The downward reversal from this resistance area stopped the earlier weekly upward impulse sequence (3) from the start of 2025.

Given the recent formation of the daily Shooting Star and the overbought weekly Stochastic, Natural gas can be expected to fall to the next support level 3.815.

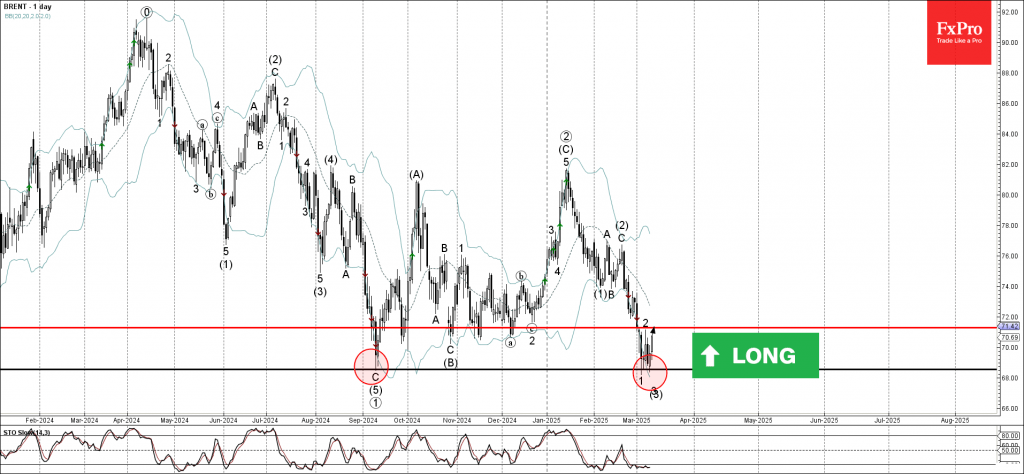

Brent Crude Oil Wave Analysis

Brent crude oil: ⬆️ Buy

- Brent crude oil reversed from the pivotal support level 68.55

- Likely to rise to resistance level 71.30

Brent crude oil recently reversed from the support area between the pivotal support level 68.55 (former multi-month low from September) and the lower daily Bollinger Band.

The upward reversal from this support area stopped the earlier downward impulse waves 3 and (3).

Given the strength of the support level 68.55 and the oversold daily Stochastic, Brent crude oil can be expected to rise to the next resistance level 71.30.

CADCHF Outlook

The Canadian Dollar (CAD) showed strength following the Bank of Canada's (BoC) 25 basis point rate cut, pushing USDCAD lower to the 1.4400 region. However, CAD's upside may be limited as the broader market remains cautious. Short-term technical patterns suggest USDCAD could see a further downside if it remains below key resistance at 1.4425/50. However, any weakness in CAD could be seen as a retracement toward the 1.4500 level.

Fundamental Factors Affecting CAD

- The BoC's decision to cut rates to 2.75% was widely expected, marking the seventh consecutive reduction.

- Trade tensions with the US remain a key risk, with the threat of tariffs affecting sentiment and growth.

- Inflation is projected to rise to 2.5% in March, driven in part by the expiration of a sales tax break.

- Business spending and consumer confidence have weakened, adding to downside risks.

- The BoC emphasized its cautious approach, balancing inflation concerns with economic uncertainty.

Market Reaction & Outlook

Following the BoC's decision, the CAD strengthened against major currencies, particularly the Japanese Yen. However, further gains may be limited unless trade tensions ease or economic data surprises to the upside.

Key Takeaway for Traders

While the rate cut was expected, ongoing trade concerns and inflation pressures created uncertainty for CAD. Traders should watch upcoming inflation data and BoC commentary for signals on future policy moves.

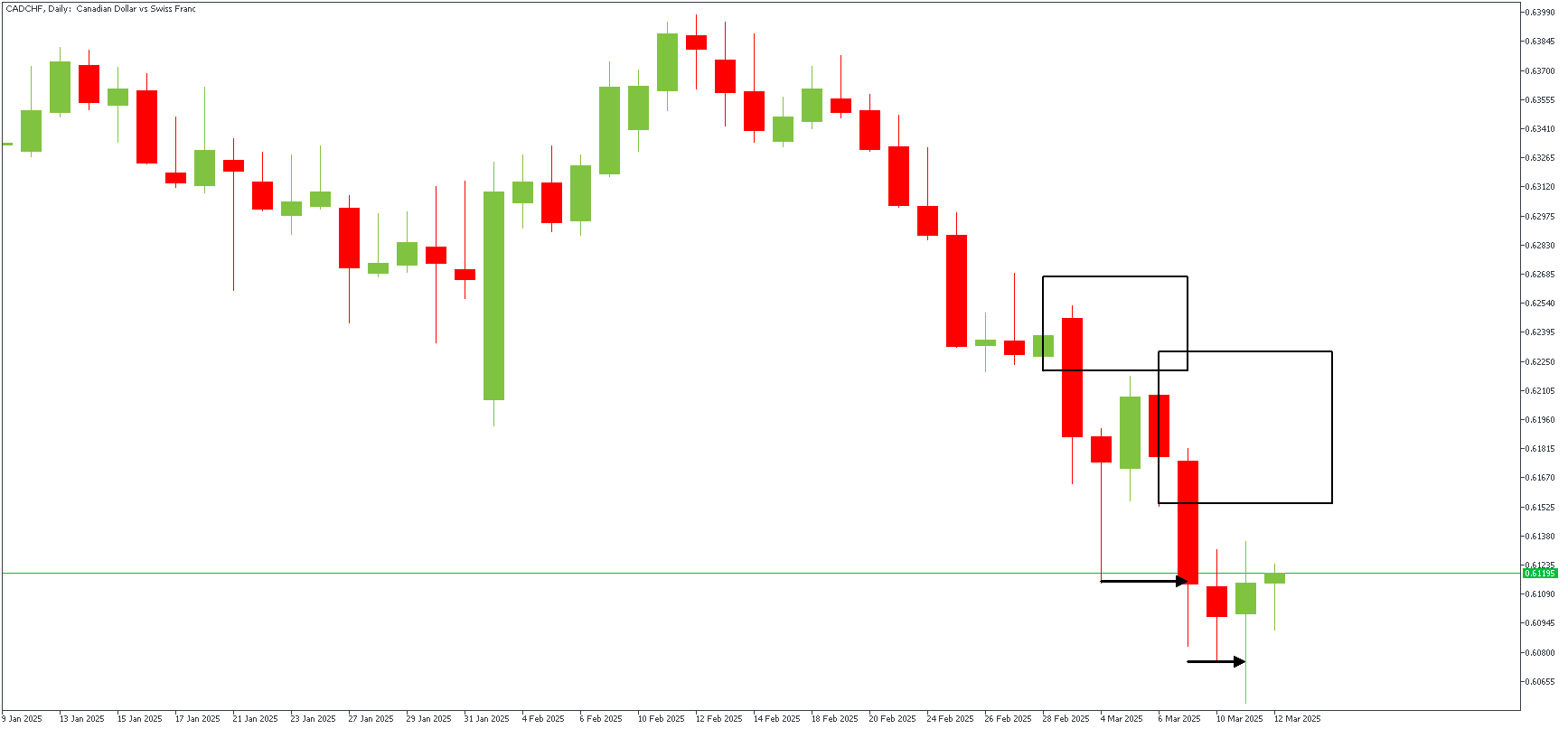

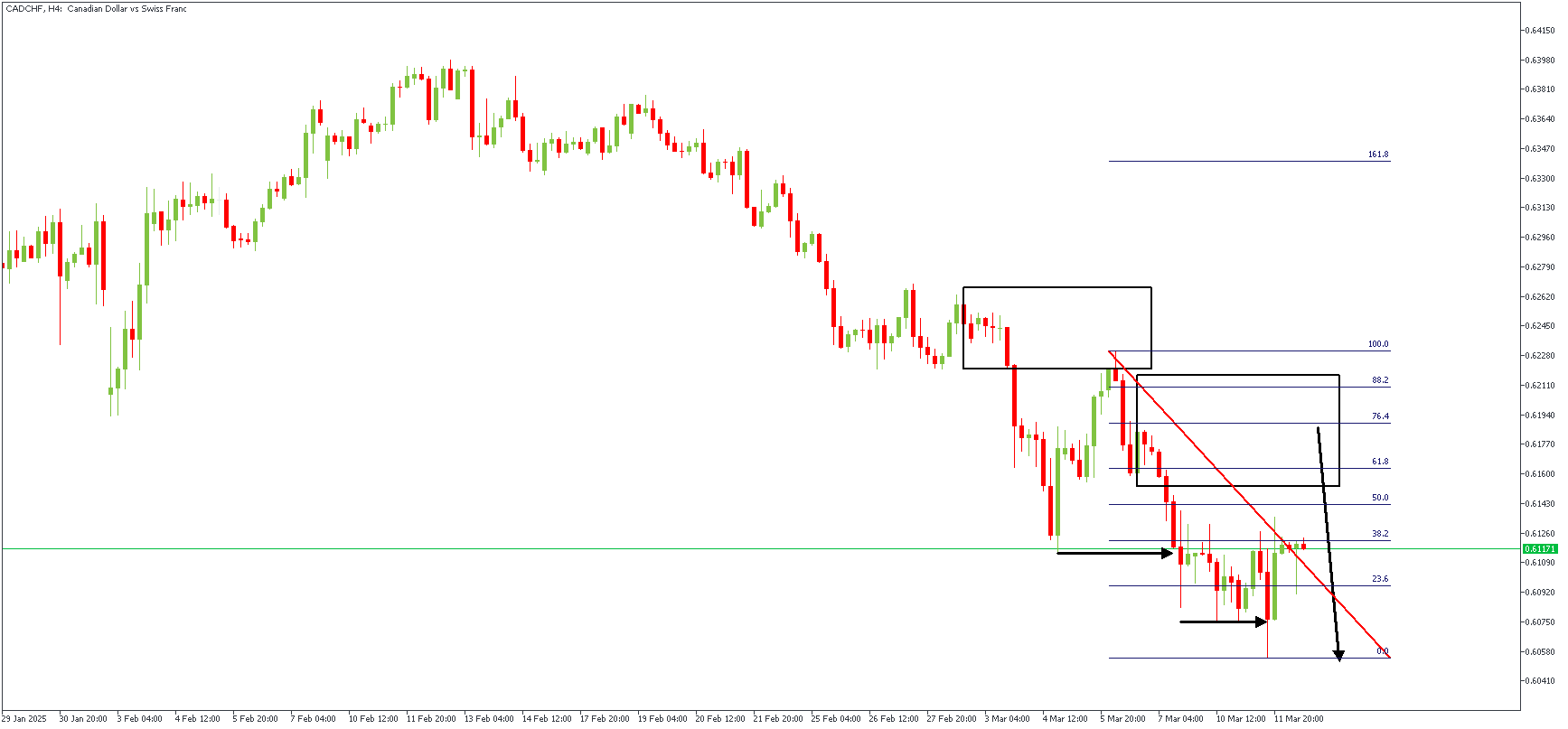

CADCHF – D1 Timeframe

The exchange rate has been steadily dropping in the daily timeframe of CADCHF, with minor retracements occasionally. Currently, the price is prepping another retracement aimed at retesting the immediate supply zone.

CADCHF – H4 Timeframe

The 4-hour timeframe chart of CADCHF shows that the supply zone falls perfectly between the 76% and 88% Fibonacci retracement levels. The presence of an FVG (Fair Value Gap) and inducement contribute to the bearish leaning of the market sentiment.

Analyst's Expectations:

- Direction: Bearish

- Target- 0.60510

- Invalidation- 0.62311

AUDCHF Outlook

After three consecutive daily declines, the Australian Dollar (AUD) traded around 0.6280-0.6270. Despite a broad sell-off in the US Dollar (USD), AUD/USD struggled to gain traction. The US Dollar Index (DXY) slipped to 103.30, its lowest since early October, but the Aussie remained under pressure.

Fundamental Factors Affecting AUD

Trade tensions weigh on market sentiment, with the US considering a 25% tariff on Canadian and Mexican goods and a 20% duty on Chinese imports. This raises the risk of retaliatory measures and could weaken demand for Australian exports. Given China's importance as Australia's top trade partner, any slowdown in Chinese demand could negatively impact the Aussie. However, a rebound in copper and iron ore prices provided short-term relief.

Central Banks and Rate Outlook

The Federal Reserve (Fed) faces a balancing act between keeping rates high to combat inflation and the rising risk of a US economic slowdown. Meanwhile, the Reserve Bank of Australia (RBA) cut rates by 25 basis points in February but signaled this may not mark the start of a prolonged easing cycle. Governor Michele Bullock emphasized that future decisions will depend on inflation data, while Deputy Governor Andrew Hauser downplayed expectations of multiple cuts. Markets, however, anticipate up to 75 basis points of further easing over the next year.

Key Takeaway for Traders

AUD remains pressured by trade tensions and global uncertainty. While Australia's inflation remains subdued at 2.5%, the RBA's cautious approach suggests rate cuts may be limited. Traders should watch for further developments in US-China trade relations and US economic data to gauge the next moves.

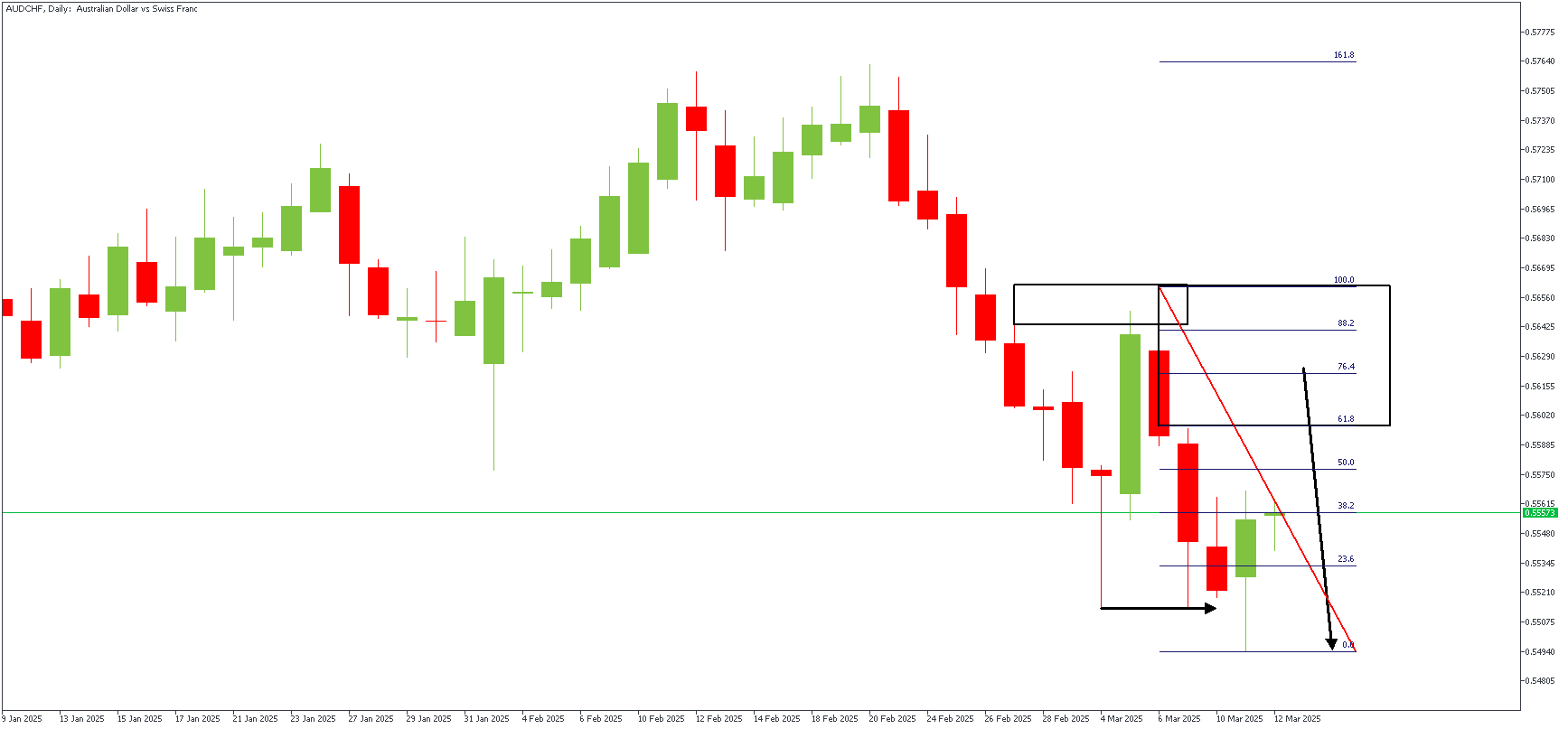

AUDCHF – D1 Timeframe

The daily timeframe chart of AUDCHF shows the price retracing after breaking below the previous low. A rally-base-drop supply zone around the key levels of the Fibonacci retracement tool leaves ample room for the sellers to intervene with an outright bearish outcome.

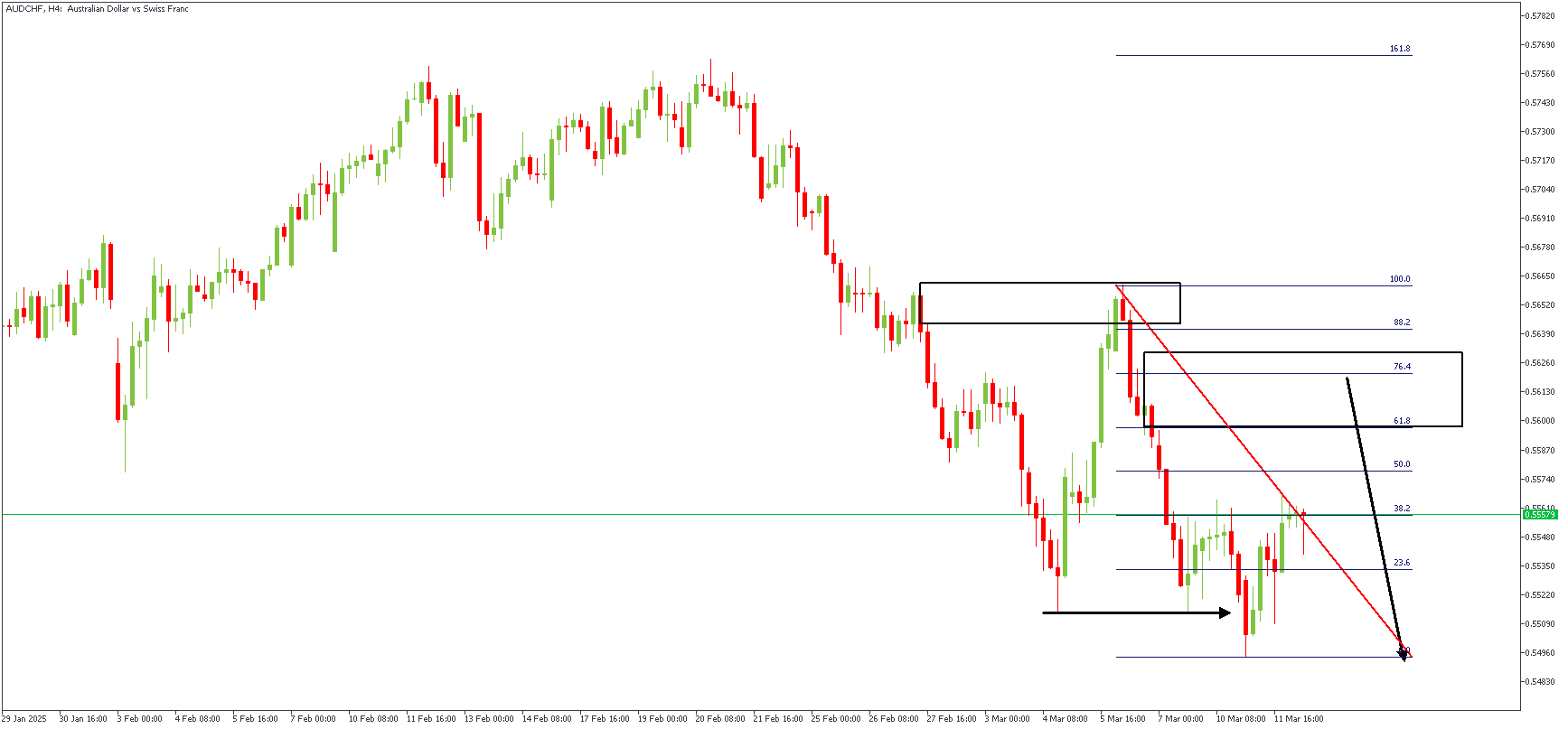

AUDCHF – H4 Timeframe

The lower timeframe chart of AUDCHF gives further details into the daily timeframe outlook, with the drop-base-drop supply zone fitting snugly within the daily timeframe supply zone and on top of the 76% Fibonacci retracement level.

Analyst's Expectations:

- Direction: Bearish

- Target- 0.54919

- Invalidation- 0.56566

Brent Crude Update – Oil Prices Rally as EIA Reduces Oil Surplus Estimates

- Brent crude prices are rising due to lower-than-expected U.S. oil and fuel supplies and revised EIA forecasts for smaller oil surpluses in 2025 and 2026.

- Libya has restarted oil production at the Mabruk field, aiming to increase output significantly, while Kuwait also plans to boost its production.

- OPEC expects strong global oil demand growth in 2025, despite potential trade policy impacts.

Brent crude prices are up around 1.55% at the time of writing as the commodity attempts a sustained recovery.

U.S. government data revealed that oil and fuel supplies are lower than expected. U.S. government data on Wednesday showed crude oil stockpiles increased by 1.4 million barrels last week, which was smaller than the 2-million barrel increase that experts had predicted.

The U.S. Energy Information Administration (EIA) has updated its forecast for oil surpluses in 2025 and 2026, lowering the expected surplus due to sanctions. The EIA now predicts a surplus of 100,000 barrels per day in 2025, down from the earlier estimate of 500,000 barrels per day. For 2026, the surplus outlook was reduced from 1 million barrels per day to 500,000 barrels per day. These updates, especially the 2025 updates could be a contributing factor to Oils recovery over the last two days.

This news comes after the American Petroleum Institute (API) said on Tuesday that U.S. crude Oil stockpiles grew by 4.247 million barrels, even as there were strong reductions in product supplies. Brent oil prices rose by 1.32%, reaching $70.48 at 10:20 a.m. ET, which is $1 higher than last week. Meanwhile, WTI prices increased by 1.55% to $67.28, just under $1 more compared to last week.

However, investors are still worried about a possible U.S. economic slowdown and how tariffs could hurt global economic growth.

Libya’s Mabruk Field Restarts Production After a Decade – Supply Concern?

Libya has started producing oil again at the Mabruk oilfield after being shut down for ten years, the Government of National Unity announced on Wednesday. Production began on Sunday at 5,000 barrels per day and is expected to grow to 25,000 barrels per day by July.

The Chairman of Libya’s National Oil Corporation, Masoud Sulaiman, said the country aims to boost its oil production from the current 1.4 million barrels per day to 2 million barrels per day by 2028. To reach 1.6 million barrels per day as a short-term goal, Libya will need $3 to $4 billion. A new bidding round for oil licenses is planned, with cabinet approval expected before the end of January. Oil is crucial to Libya’s economy, making up more than 95% of its income.

Kuwait is also planning to increase its oil production. The CEO of Kuwait Petroleum Corp., Sheikh Nawaf al-Sabah, said at last year’s CERAWeek conference that the country wants to almost double its output. Kuwait aims to raise production from about 2.4 million barrels per day now to over 4 million barrels per day by 2035, working with international oil companies to achieve this goal.

The question is whether this will have any impact on the OPEC+ output increases scheduled to start in April. A lot of that appears to have been priced into Oil prices with the recent fall we saw, thus when the output increases begin the impact might be limited.

OPEC announced earlier today that it expects strong global oil demand growth in 2025, driven by air and road travel. The group noted that trade policies could cause ups and downs in the market, but they believe the global economy will adapt to these changes.

Week Ahead and Final Thoughts

Market sentiment is in a constant state of flux at the moment with new tariff announcements and proposals coming out daily. If this continues it would be wise to keep an eye on any comments which may have a negative impact on global growth forecasts. This in turn will weigh on Oil prices as demand concerns will increase.

Another area to keep an eye is the proposed deal with Russia and Ukraine with markets waiting to hear whether the rRussians will be willing to accept a ceasefire deal proposed by the US and Ukraine after their meeting in Saudi Arabia. A deal could alleviate sanctions on Russian crude and thus see an excess of supply enter the marker.

Technical Analysis – Brent Crude

This is a follow-up analysis of my prior report “Brent Oil Price Analysis: Six-Month Lows Amid OPEC Output, Tariffs & Russia-Ukraine Negotiations” published on 25 February 2025.

From a technical analysis standpoint, Brent has now achieved a change in structure at a key psychological level around the 69.00-70.00 mark.

Today’s daily candle close above the swing high at 70.83 puts bulls in charge for now, but there are a host of hurdles to navigate if Oil prices are to stage a sustained recovery.

The 14-period RSI has also moved away from oversold territory and approaching the neutral level at 50. If the RSI breaks above 50, this could embolden bulls even further as it could be seen as another sign that momentum may be shifting once more.

Immediate resistance rests at 72.38 and 74.68 before the psychological 75.00 handle comes into focus.

If the bullish momentum fades, immediate support rests at 70.00 and 69.52 before the 69.00 handle becomes an area to keep an eye on.

Brent Crude Oil Daily Chart, March 12, 2025

Source: TradingView (click to enlarge)

Support

- 70.00 (psychological level)

- 69.52

- 69.00

Resistance

- 72.38

- 74.68 (100-day MA)

- 75.00 (psychological level)

Bank of Canada Cuts Again on Tariff Risks

The Bank of Canada (BoC) cut its policy rate by another 25 basis points today, to 2.75%. This is the seventh straight meeting that the bank cut rates.

The bank's outlook recognized that the "economy entered 2025 in a solid position, with inflation close to the 2% target and robust GDP growth." Yet, heightened trade uncertainty "will likely slow the pace of economic activity and increase inflationary pressures".

The BoC also published an update on businesses' and households' reactions to the current trade conflict. It found that businesses are seeing orders and sales inquiries decline. This has many firms expecting to decrease hiring and investment. At the same time, consumers are pulling back on spending as fears of job losses and higher inflation mount.

Regarding the future path of policy, the statement reinforced that "Monetary policy cannot offset the impacts of a trade war", but that the BoC will be attuned to both the "downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs."

Key Implications

The BoC is taking out insurance that tariffs will persist and put significant downward pressure on the Canadian economy. While recent strength in economic data would argue that the BoC could have elected to pause rate cuts, past outperformance won't matter much with the narrative now fully altered to incorporate a trade war. Our updated forecast will reflect a shallow recession under the assumption that Canadian exporters will face an effective tariff rate of 12.5% for at least the next six months. That's a massive overhaul from the past when it sat below 2%.

As long as the pressure on tariffs remains in place, the BoC should keep its dovish bias. We have the overnight rate getting to 2.25% by June, but see limitations in going further due to the delicate balance in managing inflation expectations.

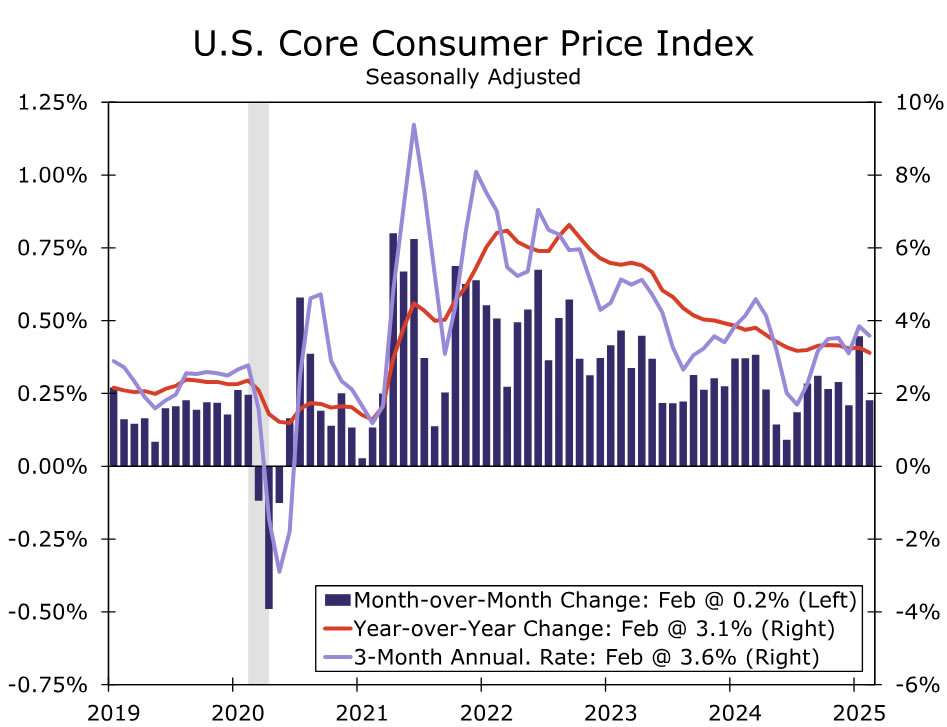

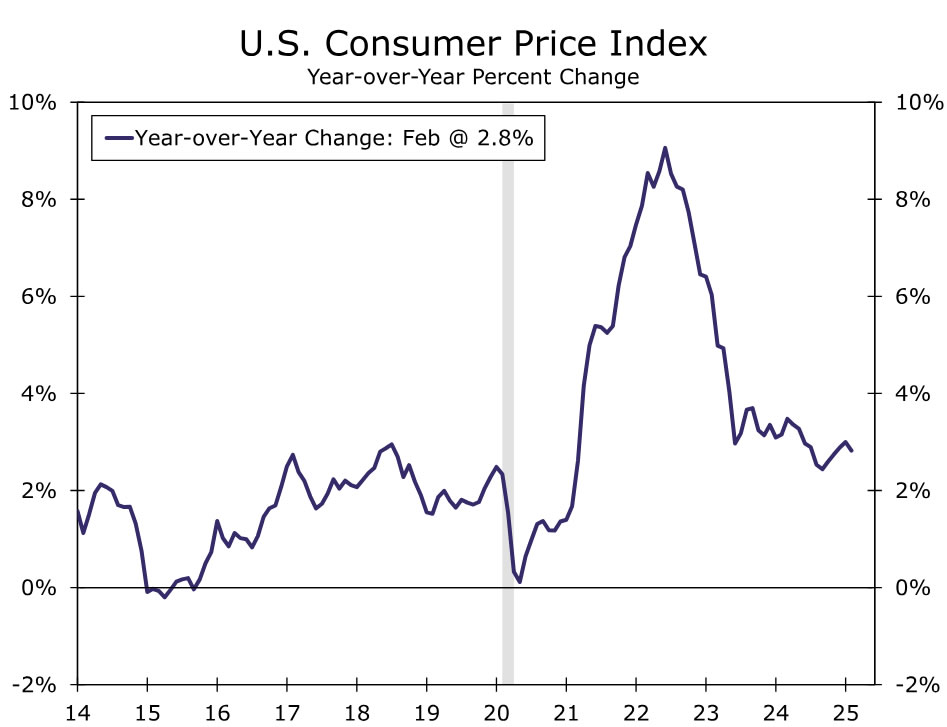

February CPI: A Little Relief

Summary

The Consumer Price Index came in slightly softer than expected, with both the headline and core indices advancing 0.2% in February. Slower growth in food and energy costs, as well as an easing in core goods and services inflation, helped overall price growth cool. The outturn is a welcome development after January's unexpectedly strong print.

Stepping back from the month-to-month noise, inflation has essentially moved sideways since early 2024. New and potential tariffs are poised to stoke goods inflation in the coming months, which is unlikely to be offset by further slowing in shelter and other services inflation.

With today's data in hand, we expect the core PCE deflator to increase around 0.35% in February, which would keep the Fed's preferred inflation measure running closer to 3% than its 2% goal. This presents a challenging situation for the FOMC, but we expect the Committee to respond with a gradual pace of monetary policy easing later this year amid slower growth and a somewhat softer labor market.

Good, but not Eggcellent

After a hot half-a-percentage-point increase in January, the Consumer Price Index rose 0.2% in February, a touch softer than consensus expectations. The more temperate gain pushed down the annual rate of inflation two tenths to 2.8%. Despite the slight reprieve, the CPI has essentially moved sideways since early 2024 (chart).

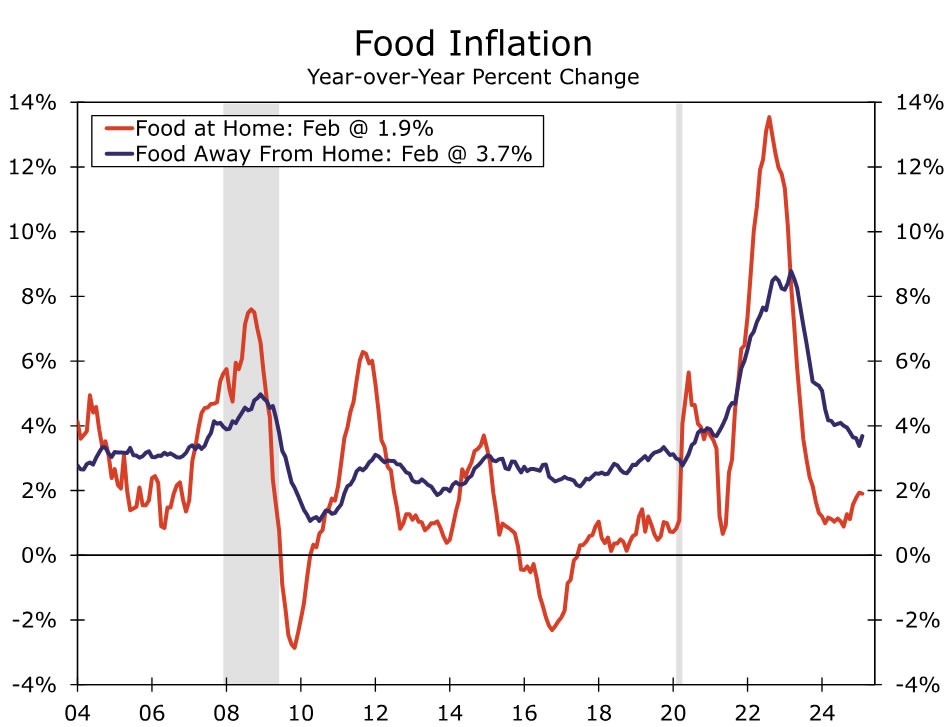

A slowing in energy and food inflation helped the headline CPI's monthly moderation. Overall energy prices rose 0.2%, as a 1.4% increase in energy services was largely offset by a 1.0% drop in gasoline prices. Grocery store prices were flat over the month despite the 10.4% monthly rise in egg prices, as prices for fruits & vegetables, dairy products and "other" food products fell. Relief at the grocery store, however, was partially offset by prices for food away from home picking up with a 0.4% gain.

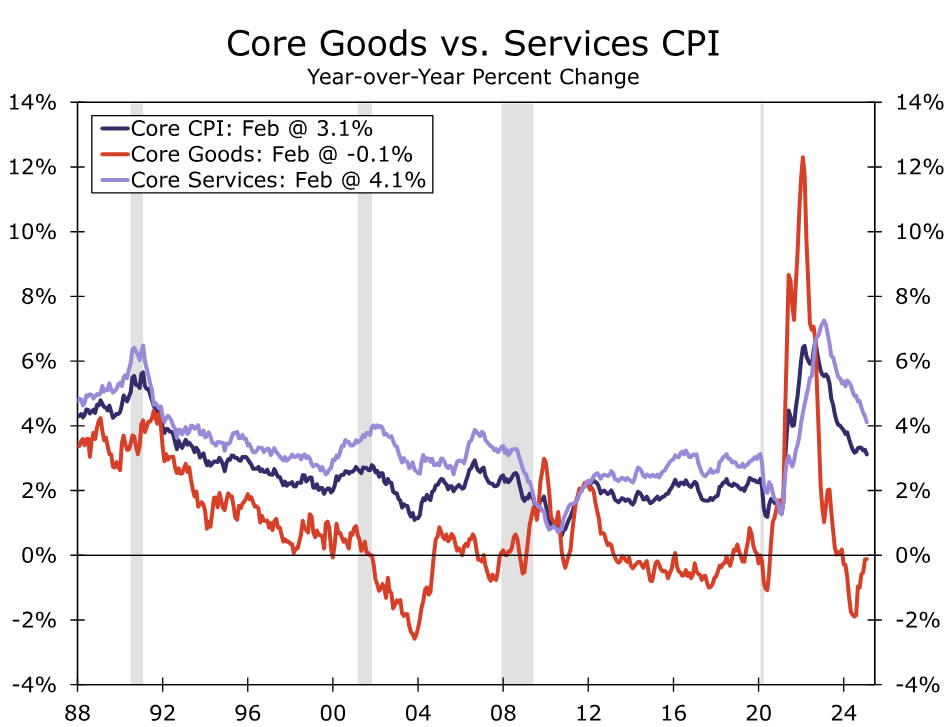

Excluding food and energy, the core CPI also came in a bit softer than expected. The 0.2% monthly increase (0.23% on an unrounded basis) was about half of January's 0.45% increase. Both goods and services contributed to the moderation. Core goods inflation slowed to 0.2% month-over-month after a 0.3% increase in January. Overall vehicle inflation (+0.3%) ebbed from the prior month, with new vehicle prices slipping (-0.1%) and used car and truck prices (+0.9%) easing back below its average increase of 1.1% over the past six months. Elsewhere, recreational goods prices fell 0.7% and prescription drug prices were flat after a jump in January.

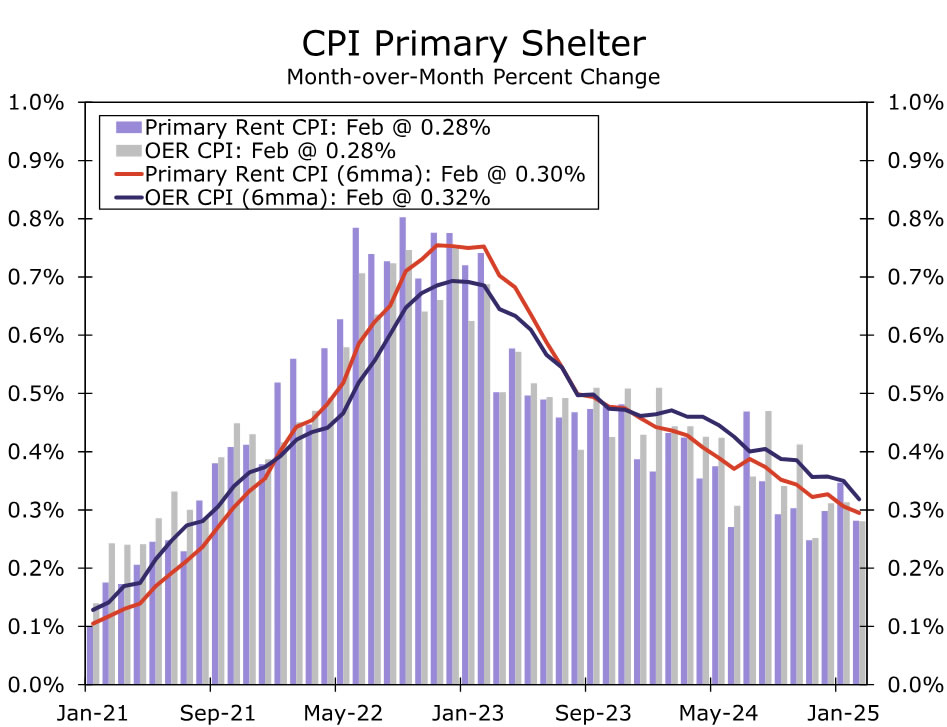

On the services side, the slowdown in primary shelter continued, with both rent of primary residences and owners' equivalent advancing 0.28% last month (chart). Transportation services decreased 0.8% amid a price declines for airline fares and vehicle rentals, as well as a smaller rise in motor vehicle insurance (0.3%) after a 2% jump in January.

Taking a step back, progress has continued on the inflation front through the month-to-month noise. The ongoing downtrend in services remains enough to offset the firmer trend in goods inflation. The core CPI slowed to a three-and-a-half year low of 3.1% in February, indicating inflation continues to gradually recede. But with upward pressure on goods prices intensifying with tariffs, a further reduction in inflation this year is likely to be hard to come by.

The FOMC likely will welcome a CPI report that came in a bit softer than expected and shows disinflation proceeding. Yet, the year-ago pace of core CPI inflation is still ~75 bps above its February 2020 level, and the three-month annualized change in the core CPI is still an uncomfortably high 3.6%. Moreover, the details of the report suggest that the core PCE deflator may come in slightly higher than what we were anticipating heading into today's report. Based on the February CPI data, the core PCE looks set to pickup with a 0.35% monthly gain, but we will know more after tomorrow's PPI data. Higher tariffs threaten to raise spot inflation and inflation expectations in the months ahead, but they also threaten a labor market that has shown some small signs of weakness. This presents a challenging situation for the FOMC, and we expect the Committee to respond with a gradual pace of monetary policy easing later this year.

Sunset Market Commentary

Markets

Risk sentiment improved today as markets welcomed the US-brokered Ukrainian backing of 30-day full truce along the entire frontline even as the US still needs to convince Russia to do the same. It could mark the start of broader peace talks. The US’s universal 25% tariff on steel and aluminum was expected and met with European countermeasures. In theory, the tariff story could move to the background for some days with the next deadline for reciprocal tariffs coming on April 2nd. In the Trump-era, that’s a lifetime away. Main European stock markets recover up to 1% after a two-day beating, but intraday sentiment is waning. German/European yields stuck to recent gains, with the front end of the curve this time slightly underperforming. Eyes were on Frankfurt for the start of the ECB and its watchers conference. In her key note speech, ECB President Lagarde warned for exceptionally high uncertainty related trade policy and geopolitics. Inflation may become more volatile and persistent due to larger shocks to inflation. She avoided giving any specific guidance on future policy though: maintaining stability in a new era requires a strong commitment to the inflation target, the ability to identify which shocks require a monetary reaction, and the agility to respond appropriately. EMU money markets are tilting to a rate cut pause at the April meeting (60-40). We think tactics will eventually decide on the outcome instead of economics. In a compromise to hawks on the MPC, the ECB could lower rates a final time and simultaneously flag a larger pause to await how fiscal developments play out. The Fed used the same playbook around the turn of the year. In any case, we see it more likely that 2.25% will be the bottom instead of the currently discounted 2%. Focus in the US turned to February inflation numbers. Both headline and core inflation slowed down to 0.2% on a monthly basis while consensus expected a 0.3% pace. On an annual basis, inflation slowed slightly more than hoped, respectively from 3% to 2.8% and from 3.3% to 3.1%. Core goods inflation went from 0.3% M/M in January to 0.2% M/M with core services down to 0.3% M/M from 0.5% M/M. The February data suggest that the disinflationary impact from Trump’s explosive policy mix, weighing on spending, for now outweighs the inflationary impact from tariffs. The dollar and short-term US yields spiked lower, but the move didn’t last for five minutes. US yields currently trade around 3 bps higher across the curve. EUR/USD trades a tad softer today, changing hands near 1.0880. US stock markets opened flat (Dow) to 1.5% higher (Nasdaq).

News & Views

The ECB’s updated wage tracker confirmed January’s projection of rising by an annual 1.5% in the fourth quarter of this year. It’s a sharp deceleration from the 5.3% peak in 2024Q4 and adds to the evidence the ECB is looking for that the current strong wage growth should ease eventually. This is expected to usher in a more marked disinflation in the labor-intensive services sector (currently 3.7%), in theory paving the way for further rate cuts. The recent fiscally-related developments could thwart those monetary easing intentions, though. The ECB also added a technical disclaimer to the steep decline the tracker projects later on. “The steeply downward trend of the forward-looking wage tracker in 2025 partly reflects the mechanical impact of large one-off payments (that were paid in 2024, but drop out in 2025) and the front-loaded nature of wage increases in some sectors in 2024.”

The Bank of Canada cut policy rates by 25 bps to 2.75% today. The statement makes multiple references to the trade conflict, with the “pervasive uncertainty created by continuously changing US tariff threats (…) restraining consumers’ spending intentions and businesses’ plans to hire and invest.” The resulting slowing growth will offset the stronger Canadian performance seen at the end of last year (2.6% Q/Qa). “Recent surveys suggest a sharp drop in consumer confidence and a slowdown in business spending as companies postpone or cancel investments.” The central bank refrained from giving any guidance. It does stress that it cannot offset the impact of a trade war (which in nature is a supply shock) but that it must ensure that higher prices do not lead to sustained inflation. In setting policy it will balance both the downward pressures on inflation from a weaker economy and the upward pressures from tariff-related higher costs. The Canadian dollar reacts muted to the expected policy decision with USD/CAD hovering north of 1.44. Swap yields add a few bps across the curve.