Sample Category Title

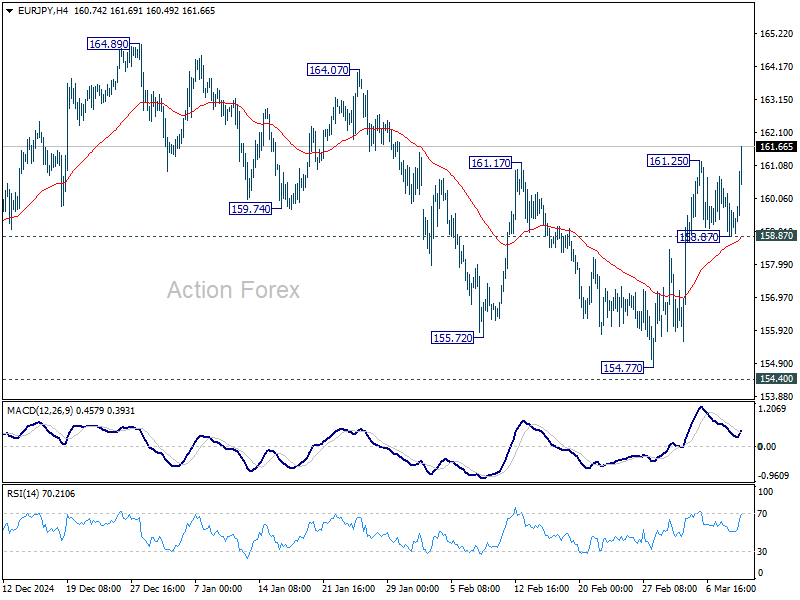

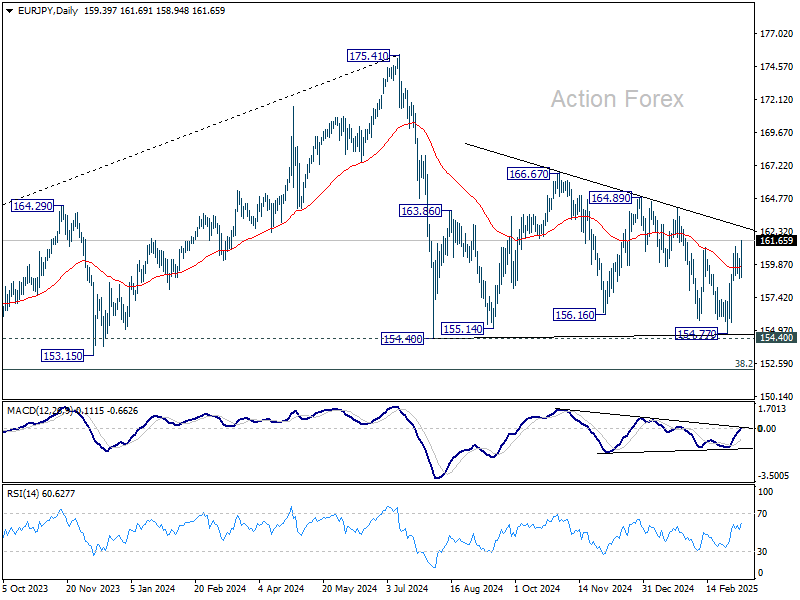

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.86; (P) 159.62; (R1) 160.35; More...

EUR/JPY's rally resumed by breaking through 161.25 temporary top and intraday bias is back on the upside. Rise from 154.77 is seen as another rising leg in the consolidation pattern from 154.40. Next target is 164.89 resistance. For now, further rise is expected as long as 158.87 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

Euro Rally Extends as German Greens Eye Defense Spending Deal This Week

Euro's rally continues after a brief pause, boosted by signs of political breakthrough in Germany over major defense and infrastructure spending. Consensus appears to be emerging around the large-scale funding deal, a game-changer toward bolstering Europe’s economic and defense resilience, especially amid ongoing geopolitical conflicts in Ukraine.

Germany’s Green party is reportedly prepared to reach an agreement as early as this week with prospective Chancellor Friedrich Merz of CDU/CSU. Greens co-leader Franziska Brantner indicated in a Bloomberg TV interview that negotiations could move quickly, citing the urgent need for Europe to "speed up" its defense capabilities given the "dire" situation in Ukraine. An influx of hundreds of billions of Euros in spending could act as a significant stimulus for the German economy, thereby supporting the broader Eurozone.

On the other hand, Dollar is generally weaker against European majors, reflecting a cautious mood. US futures are also sluggish, reversing earlier recovery and struggling to find direction in a narrow trading range. Many investors appear to be sidelined, waiting for tomorrow’s CPI release to guide the next market move.

Expectations point to core CPI remaining sticky, albeit with a modest decrease from 3.3% to 3.2%. The pace of disinflation has clearly lost momentum in recent months, suggesting that inflationary pressures are far from fully contained. Should the data confirm a slow decline in inflation, it would solidify Fed’s case to hold rates steady at the upcoming March 19 meeting.

Even so, market participants are increasingly betting that Fed will need to ease policy in Q2, as the economic impact of tariffs and weaker sentiment gradually translate into weaker hard data. The uncertainty surrounding trade policy, coupled with signs of slowing economic momentum, has kept Dollar on the back foot.

Looking at weekly performance, Euro remains the strongest currency so far. British Pound and Yen are also holding up well. On the other end of the spectrum, Canadian Dollar is the worst performer this week, followed by Australian and New Zealand Dollars, as risk sentiment remains weak and commodity-linked currencies struggle. Dollar and Yen are currently positioned in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is up 0.21%. CAC is up 0.03%. UK 10-year yield is up 0.024 at 4.626. Germany 10-year yield is up 0.046 at 2.883. Earlier in Asia, Nikkei fell -0.64%. Hong Kong HSI fell -0.01%. China Shanghai SSE rose 0.41%. Singapore Strait Times fell -1.88%. Japan 10-year JGB yield fell -0.065 to 1.506.

ECB’s Rehn warns US tariffs could cut global output by 0.5% in both 2025 and 2026

In a speech today, Finnish ECB Governing Council member Olli Rehn highlighted the potential damage that US tariffs could inflict on global economic activity.

According to Bank of Finland estimates, import tariffs of 25% on US imports from the Eurozone and 20% on imports from China, along with reciprocal measures by those regions, would shave more than 0.5% off global output this year and next

Rehn stressed that this looming trade conflict would carry both deflationary and inflationary implications for Europe. "It's worth recalling that if growth were to slow down in the world economy and euro area economy compared to forecasts, that would weigh on inflation downwards," Rehn said.

Given this uncertainty, he noted that ECB will assess fresh economic data ahead of its April meeting before committing to additional rate cuts or a pause.

Australia Westpac consumer sentiment jumps to 95.9, soft landing achieved

Australian consumer sentiment saw a strong rebound in March, with Westpac Consumer Sentiment Index jumping 4.0% mom to 95.9, the highest level in three years and not far from neutral 100 mark.

Westpac attributed the improvement to slowing inflation and February’s RBA interest rate cut which have lifted confidence across households. positive views on job security suggest that "soft landing has been achieved". Nevertheless, "unsettling overseas news" continues to weigh on the broader economic outlook.

Looking ahead to RBA's upcoming meeting on March 31-April 1, Westpac expects the central bank to keep the cash rate unchanged. RBA was clear that the 25bps cut in February "did not mean further reductions could be expected at subsequent meetings."

Westpac added, "further slowing in inflation will give the RBA sufficient confidence to deliver more rate cuts this year with the next move coming at the May meeting".

Australia’s NAB business confidence slips back into negative as cost pressures persist

Australia’s NAB Business Confidence fell from 5 to -1 in February, erasing last month’s gain and returning to below-average levels. While business conditions improved slightly from 3 to 4, the decline in confidence suggests that businesses remain cautious despite RBA’s recent rate cut and positive Q4 GDP data.

NAB Chief Economist Alan Oster noted that the lift in sentiment seen in January was not sustained, signaling ongoing uncertainty in the business environment. Persistent cost pressures and subdued profitability appear to be key factors weighing on sentiment, keeping confidence below long-term norms.

Within business conditions, trading conditions ticked up from 7 to 8, and profitability conditions rose slightly from -2 to -1, though still remaining in negative territory. Employment conditions, however, weakened from 5 to 4.

Cost pressures remain a concern, with purchase cost growth accelerating from 1.1% to 1.5% in quarterly equivalent terms. On the positive side, labor cost growth eased from 1.7% to 1.5%, indicating that wage price pressures are gradually cooling. Meanwhile, final product price growth slowed from 0.8% to 0.5%, though retail price inflation held steady at 1.0%.

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.86; (P) 159.62; (R1) 160.35; More...

EUR/JPY's rally resumed by breaking through 161.25 temporary top and intraday bias is back on the upside. Rise from 154.77 is seen as another rising leg in the consolidation pattern from 154.40. Next target is 164.89 resistance. For now, further rise is expected as long as 158.87 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

ECB’s Rehn warns US tariffs could cut global output by 0.5% in both 2025 and 2026

In a speech today, Finnish ECB Governing Council member Olli Rehn highlighted the potential damage that US tariffs could inflict on global economic activity.

According to Bank of Finland estimates, import tariffs of 25% on US imports from the Eurozone and 20% on imports from China, along with reciprocal measures by those regions, would shave more than 0.5% off global output this year and next

Rehn stressed that this looming trade conflict would carry both deflationary and inflationary implications for Europe. "It's worth recalling that if growth were to slow down in the world economy and euro area economy compared to forecasts, that would weigh on inflation downwards," Rehn said.

Given this uncertainty, he noted that ECB will assess fresh economic data ahead of its April meeting before committing to additional rate cuts or a pause.

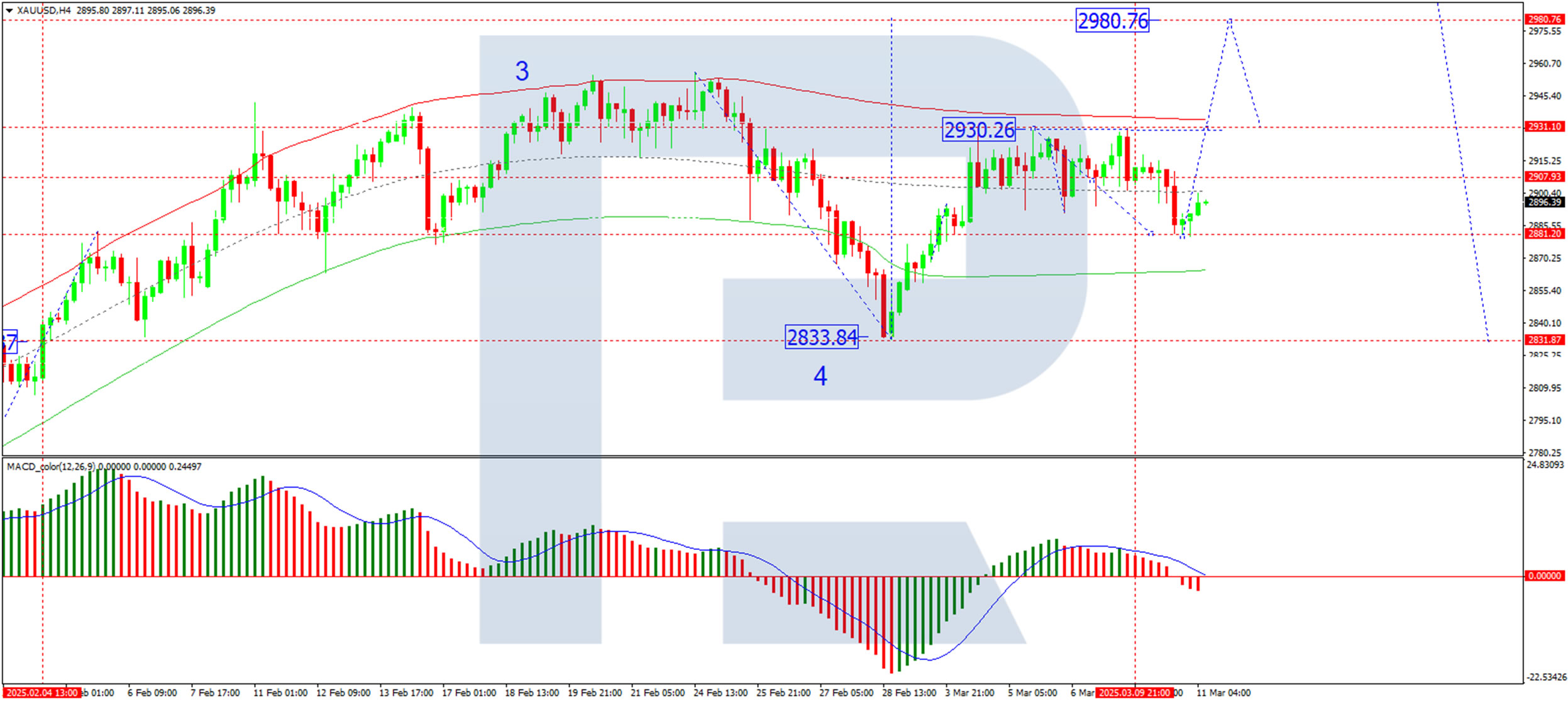

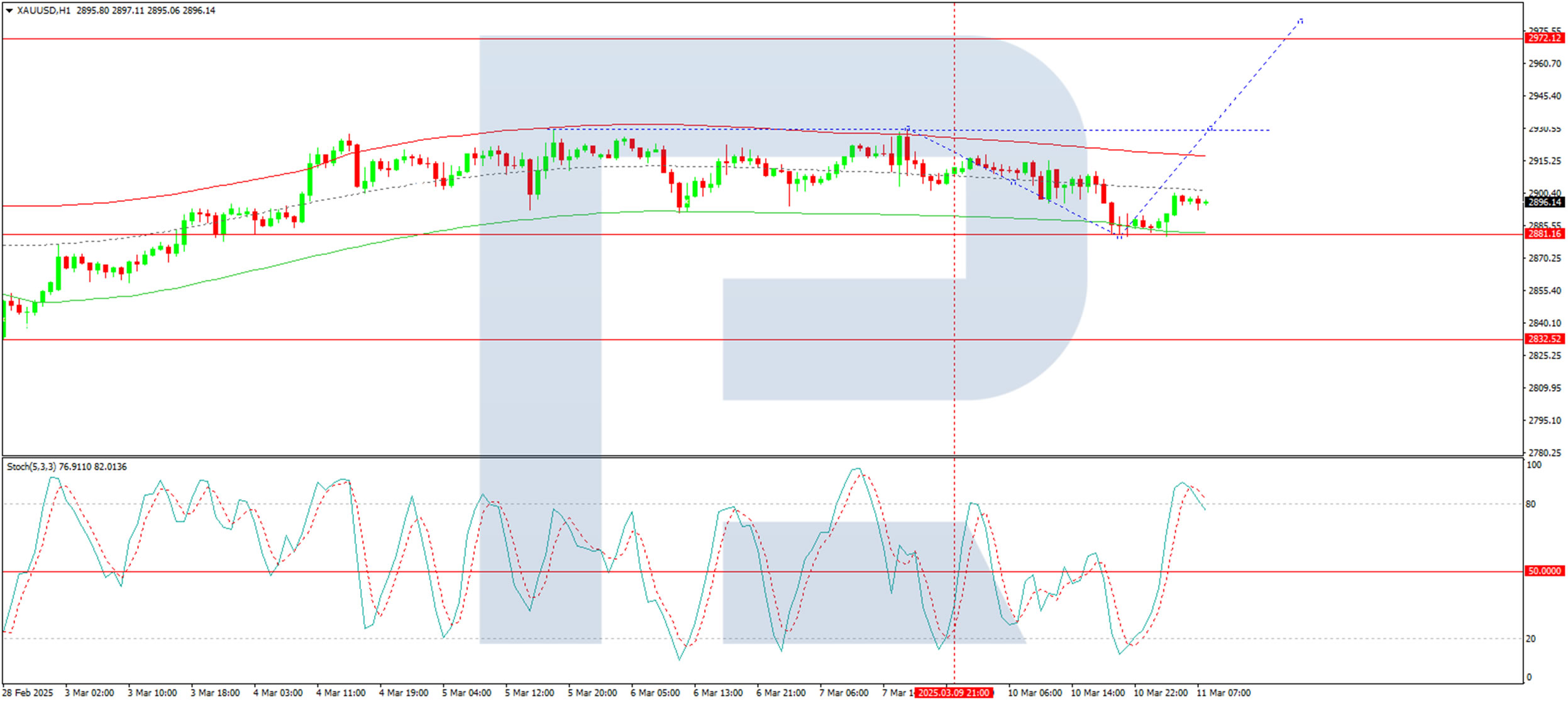

Gold Remains in Consolidation Amid Ongoing Market Uncertainty

On Tuesday, Gold prices hovered near 2,900 USD per troy ounce, holding steady as the US dollar weakened and demand for safe-haven assets rose. Concerns about the US economic outlook and escalating trade tensions continue to support Gold’s consolidation.

Key market drivers for Gold

Fears of an economic downturn intensified after President Donald Trump referred to the current situation as a "period of transition" in an interview with Fox News, implying that current policies may lead to a recession.

Meanwhile, trade tensions remain elevated. The US had recently delayed imposing a 25% tariff on select Canadian and Mexican goods for a month while Canada maintained its retaliatory measures. China imposed additional tariffs on some American agricultural products in response to the US tariff hikes.

Federal Reserve Chair Jerome Powell acknowledged increasing economic uncertainty but refrained from signalling an imminent interest rate cut.

This week, US inflation data will be in focus, as it may shape the Fed’s future policy outlook. The next Federal Reserve meeting is scheduled for 19 March.

Technical analysis of XAU/USD

On the H4 chart, Gold recently formed a growth wave to 2,931 USD, followed by a correction to 2,880 USD. An upward move towards 2,906 USD is forming a consolidation range around this level. A breakout to the upside could trigger a further rise towards 2,980 USD, the local target. After reaching this level, a correction back to 2,900 USD is likely. If the price moves downward from the consolidation range, a correction to 2,860 USD is possible. This scenario is supported by the MACD indicator, with its signal line positioned above zero and pointing sharply upward.

On the H1 chart, Gold completed a correction wave to 2,880 USD, and the market is now forming a new growth wave towards 2,906 USD, which is expected to be reached today. A subsequent potential pullback to 2,891 USD may occur, forming a consolidation range around this level. If Gold breaks downward from this range, a correction to 2,860 USD is possible before a renewed upward move. However, an upward breakout would open the path towards 2,980 USD. The Stochastic oscillator confirms this scenario, with its signal line above 80 and pointing firmly upward.

Conclusion

Gold remains in consolidation, balancing between a weakening US dollar and ongoing economic uncertainties. Technical indicators suggest a likely upward move towards 2,980 USD, though short-term corrections to 2,900 USD or 2,860 USD could occur before further gains. Market sentiment largely depends on upcoming US inflation data and its potential impact on Federal Reserve policy expectations.

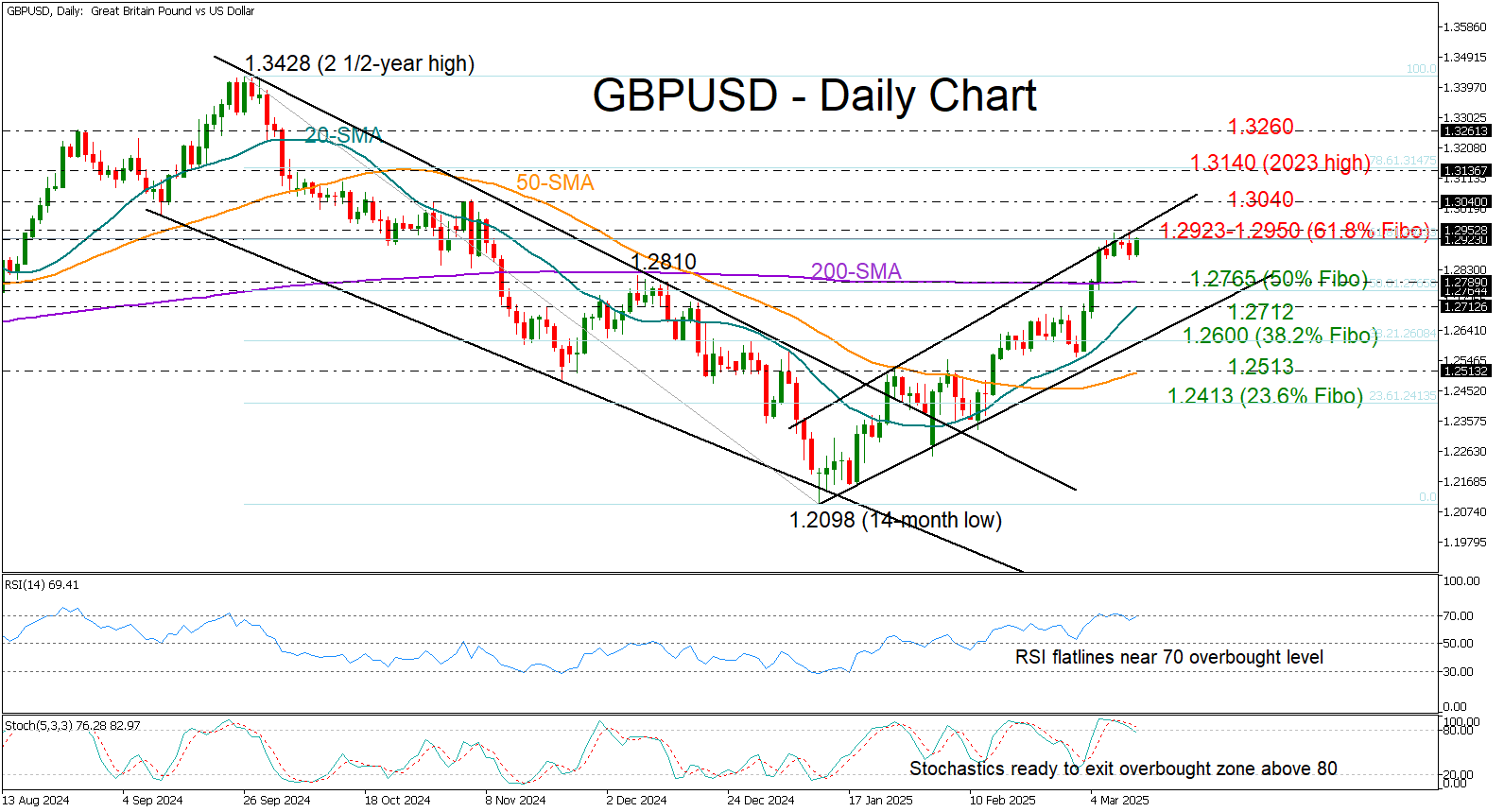

GBP/USD Flatlines Near Channel’s Upper Band

- GBP/USD takes a breather after hitting a five-month high.

- Overbought signals strengthen as price tests key resistance.

GBPUSD has been treading water around the 1.2923 level, struggling to gain further traction after its March bull run stalled near the upper boundary of its bullish channel.

The pair surged as high as 1.2945 last week, marking its highest level since November 2024. However, strengthening overbought signals suggest the recent rally may be losing steam, as the RSI and the stochastic oscillator seem to have peaked above 30 and 20, respectively.

A decisive breakout above the 1.2923-1.2950 resistance—aligned with the 61.8% Fibonacci retracement of the prior downtrend—could reignite buying interest. If the November peak of 1.3040 is surpassed, momentum could build toward the 2023 high of 1.3140, with the next resistance possibly emerging near 1.3260, a key barrier from August 2024 and March 2022.

On the flip side, if sellers regain control, the pair may retreat toward the 200-day simple moving average (SMA), which hovers just above the 50% Fibonacci level of 1.2765, and the 20-day SMA at 1.2712. Further losses could bring the lower band of the bullish channel into play around the 38.2% Fibonacci level of 1.2600, ahead of the 50-day SMA at 1.2513.

In summary, GBPUSD is at a crucial juncture. A push beyond 1.2950 and out of the bullish channel could inject fresh momentum. Otherwise, the next move could see the pair sliding backwards.

Nasdaq 100 Enters Correction

As shown on the Nasdaq 100 (US Tech 100 mini on FXOpen) index chart today:

→ The index has fallen below the psychological 20,000-point level, reaching its lowest in approximately six months.

→ The decline from the December peak now exceeds 10%, officially marking the start of a correction.

Why the Nasdaq 100 Is Falling Today

Bearish sentiment stems from a combination of factors, including (according to Zacks analysts):

→ The Trump administration’s tariff policies and their potential economic impact. Concerns increased after the latest jobs report showed unemployment rising from 4.0% to 4.1%.

→ Worries about AI investment costs and their long-term profitability.

→ Market anticipation of tomorrow’s Consumer Price Index (CPI) release at 15:30 GMT+3.

Technical Analysis of the Nasdaq 100 Chart

Price movements indicate that the steeper growth channel (marked in black), which had been in place since last August, has lost relevance. A broader view of the chart reveals that the index has now approached the lower boundary of a long-term channel (marked in blue), which has been forming since early 2024. Key price formations that helped define this channel are highlighted in orange.

Given that the index is at the lower boundary of the blue channel and the RSI indicator on the daily chart has dropped to multi-year lows, a short-term recovery may be likely. However, the fundamental backdrop will play a decisive role—clear signs of U.S. economic stability could support a rebound, while extreme fear (as reflected in CNN’s Fear & Greed Index) may continue to weigh on sentiment.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

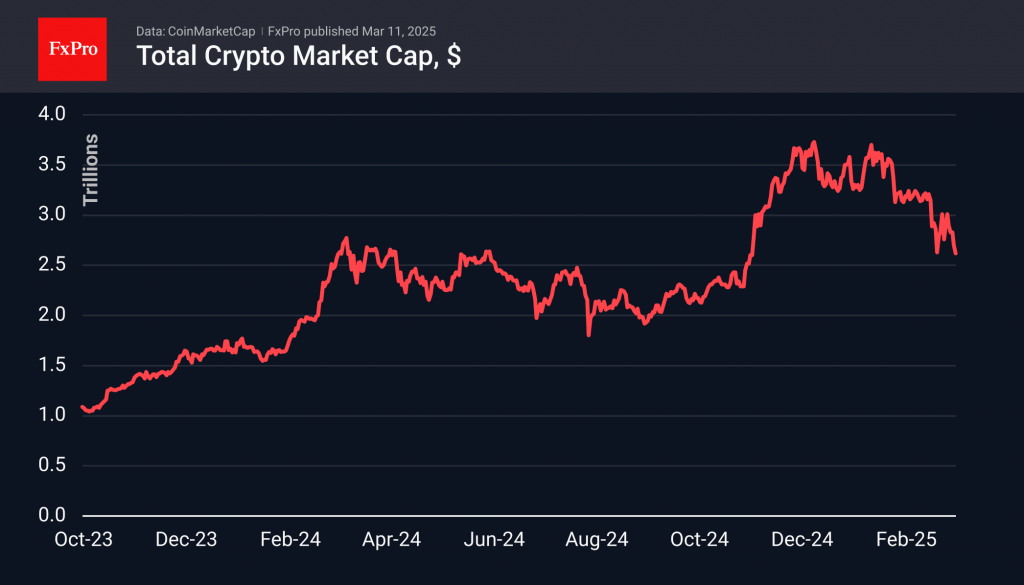

Crypto Market Tumbles After Stocks

Market picture

Crypto market capitalisation has been falling to $2.5 trillion following the rumbling fall of the US stock market. It is dipping below the peaks of early 2024 and late 2021. Previously, a similar decline would complete a corrective pullback, attracting buyers. However, the chances of such an outcome are now lower than in previous years due to the powerful influence of traditional financial companies, which has strengthened the link between the crypto market and stock dynamics.

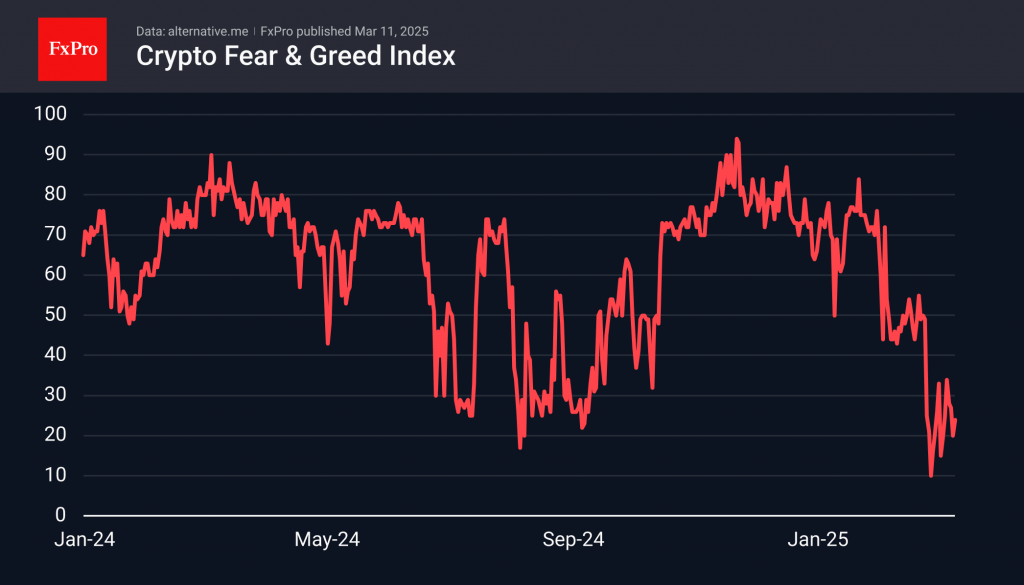

For now, though, we can argue that there is less terror in crypto. The Fear and Greed Index is at 24 (+4 points for the day), while the low point was a week earlier at 10.

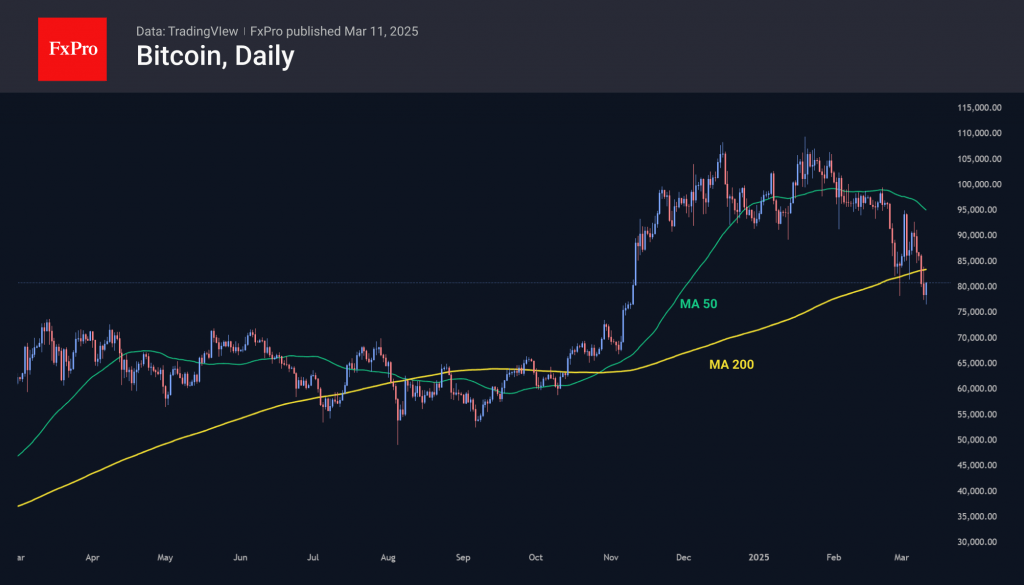

Bitcoin slipped towards $76.5K in the early hours of Tuesday but has popped above $80K at the time of writing, approaching Monday’s consolidation levels. A bearish pattern persists on the daily timeframes, which suggests a strengthening sell-off after a failure under the 200-day moving average. The scenario of a pullback to the $70-74K area still looks the most probable for us. This is all the truer as the consolidation and rebound in early March has taken the short-term oversold stance out of the market.

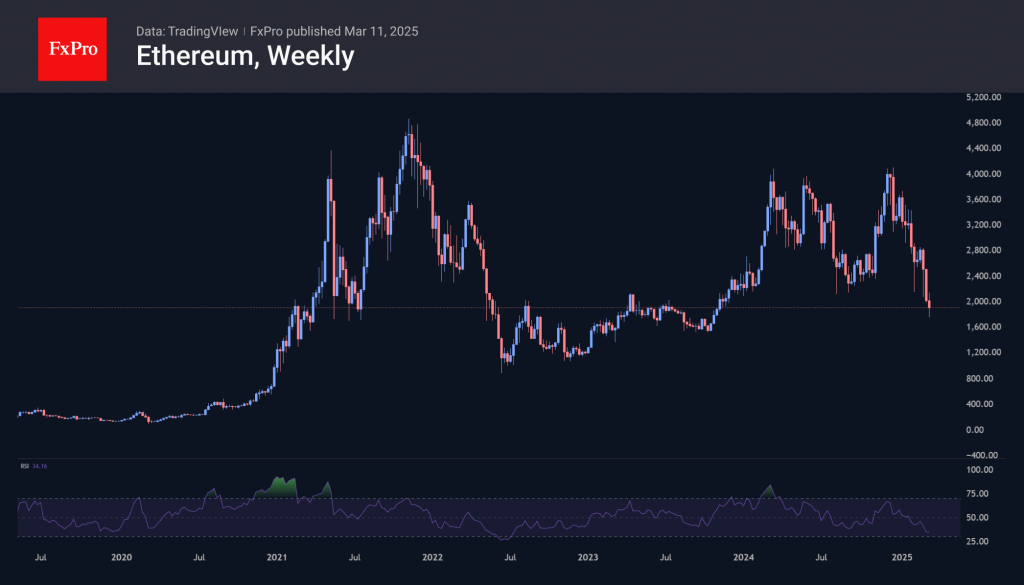

Ethereum is trying to find a pivot point after falling towards $1750 at the start of Tuesday. These were the lowest values in the last 17 months. On weekly timeframes, the RSI oscillator hit its lowest point since mid-2022 – near the bottom of the bear market. Does this signify an opportunity for the recklessly bold or a breakdown in the leading altcoin? We will find out in the coming days.

News background

According to CoinShares, global crypto fund investments fell by $876 million last week after record outflows of $2.911 billion a week earlier. Investments in Bitcoin fell by $756 million; in Ethereum, by $89 million. Investments in Solana rose by $16 million, in XRP by $6 million, and in Sui by $3 million.

Another recalculation increased Bitcoin mining difficulty by 1.43% to 112.15T. The growth did not compensate for a 3.15% drop two weeks ago. However, the figure came close to the all-time high of 114.17T reached in January.

Strategy (former MicroStrategy) intends to raise $21bn through the sale of preferred shares as part of its At-The-Market program. The proceeds will be used to buy Bitcoin and other corporate purposes.

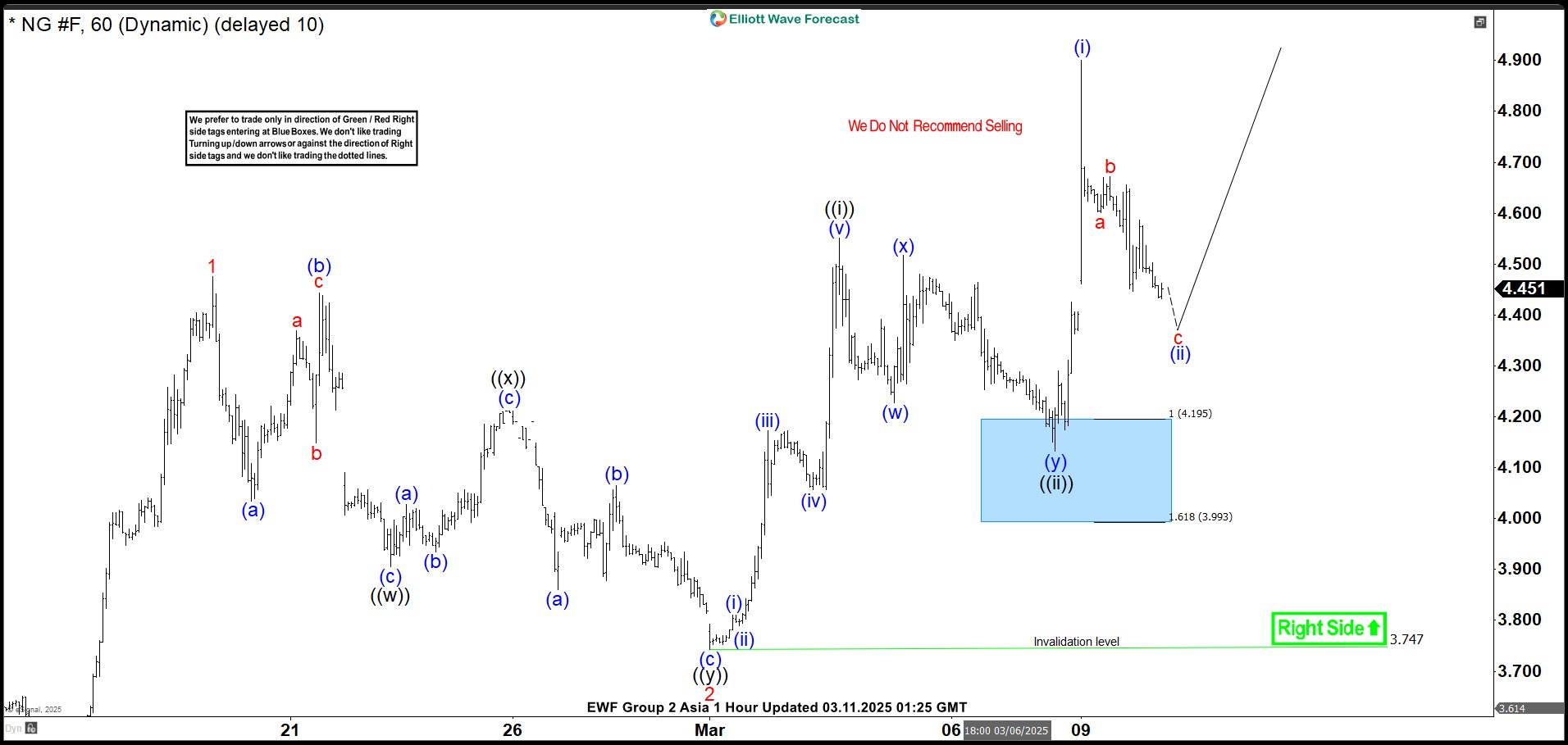

Natural Gas Reacted Strongly From The Blue Box Area

In this technical blog, we will look at the past performance of the 1-hour Elliott Wave Charts of the Natural Gas futures ticker symbol: $NG_F. The rally from the 31 January 2025 low showed a higher high sequence & provided a short-term opportunity at the blue box area. In this case, the pullback managed to reach the Elliott wave blue box area & reacted strongly. So, we advised members not to sell Natural Gas but to buy the pullbacks in 3, 7 or 11 swings. We will explain the structure & forecast below:

Natural Gas 1-Hourr Elliott Wave Chart From 3.07.2025

Here’s the 1-hour Elliott wave Chart from the 3.07.2025 Asia update. In which, the rally to $4.551 high ended wave ((i)) & made a pullback in wave ((ii)). The internals of that pullback unfolded as Elliott wave zigzag structure where wave (a) ended at $4.227 low. A short-term bounce to $4.518 high then ended wave (b) & started the next leg lower in wave (c) towards $4.195- $3.993 blue box area. From there, buyers were expected to appear looking for new highs ideally or for a 3-wave bounce minimum.

Natural Gas Latest 1-Hour Elliott Wave Chart From 3.11.2025

Above is the Latest 1-hour Elliott Wave Chart from the 3.11.2025 Asia update. In which the Natural Gas is showing a perfect reaction higher taking place from the blue box area. Allowed members to create a risk-free position shortly after taking a long position. Since then, the $NG_F has already made a new high above $4.551 high confirming the next extension higher towards $5.226- $5.577 target area.

Dollar Remains in Downtrend: More Weakness to Come After Rally

We saw another big drop in the stock market yesterday, with SP500 pulling back now around 10 percent from all-time highs. This type of correction has always been proved to be a healthy one since 2023, as each similar pullback was later fully reversed. This suggests we could still see some price stabilization this week. As discussed in yesterday’s webinar, tomorrow could bring interesting price movements, especially if inflation data in US softens due to lower energy prices since mid-January.

On another note, trade tarrfis tensions remain a key market driver, with reports that Canada may take also some actions against US tariffs. This reinforces the idea that no one wins in a trade war, but it could still keep the US dollar bearish as other countries continue responding.

The dollar index is pushing lower, breaking lower with an extended wave three, with an interesting target around the 103 area.Next wave four bounce is a sell.

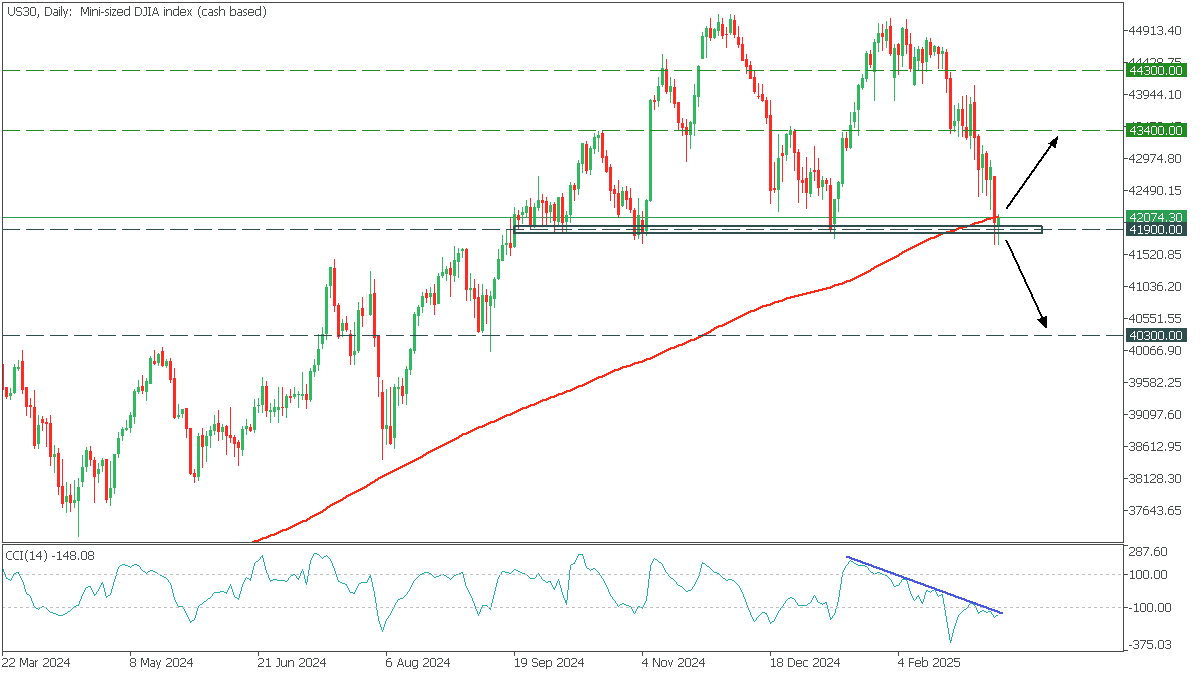

US30: Beginning of a correction?

US30, Daily

In the Daily timeframe, US30 fell to the critical support area, testing MA200. The CCI confirms the market weakness and forms a trend line, a break above, which will indicate the possibility of a rebound.

- If the price breaks through 41900 and MA200, the decline will continue to 40300;

- A rebound from the support will bring US30 back to 43400;