Sample Category Title

US Equities Drop amid US Growth Concerns

In focus today

Focus in the euro area is on the ECB watchers conference where several ECB officials will be present. We will particular pay attention to Lagarde's speech at 09:45 CET.

From the US, the January JOLTs labour turnover survey is due for release. The number of job openings is a key measure of labour demand for the Fed. Markets will also pay close attention to the NFIB's small business optimism survey given the ongoing political uncertainty and its negative impact on business confidence.

In Sweden, the Riksbank attends a parliamentary hearing on 2024 and current monetary policy. The hearing starts at 09.00 and ends at 11.30. All five board members will participate. We hope to get some clarity on how the individual members assess the risk balance between higher-than-expected inflation prints and the still fragile recovery.

Overnight, many large Japanese companies will announce their responses to their union's demands. Unions have requested a 6.1% pay increase this year, the highest in 32 years. Solid pay increases are key for the continued economic recovery in Japan and the outlook for a continuation of Bank of Japan hikes.

US and Ukrainian officials are meeting in Saudi Arabia today to discuss strategies to end the three-year conflict between Russia and Ukraine. Although Zelenskyy spoke with the Saudi Crown Prince yesterday, he will not attend today's meeting. However, he assured that Ukraine will participate constructively.

Economic and market news

What happened yesterday

In euro area, the Sentix investor confidence indicator increased more than expected in March to -2.9 (cons: -9.3) from -12.7 in February. Although the index remains low historically, the upward trend is positive, marking its highest level since June. Historically, the Sentix indicator has correlated well with the PMIs, suggesting an expected rise in PMIs for March as well.

In Germany, the Greens declared that they will not support the coming chancellor Merz's spending package and change of the debt brake. This announcement precedes the parliamentary vote next Tuesday, where the CDU and SPD requires support from the Greens for a two-thirds supermajority to pass the bill. However, we see the statement from The Greens as a negotiating tactic to get concessions e.g. on more green spending in the fund and not an outright refusal of the package. The proposal from the SPD and CDU/CSU aligns closely with the Greens' election campaign so we expect them to eventually back a package, which also seems to be the conviction in markets that moved only marginally on the news.

German industrial production exceeded expectations in January, increasing by 2.0% m/m (prior: -1.5%, cons: 1.5%). The less volatile three-month comparison shows stable production from November 2024 to January 2025 (0.0%). Although production has stabilised, it is premature to declare the end of the previous declining trend, given its volatility and PMIs below 50.

In Denmark, Danish CPI inflation rose to 2.0% (prior: 1.5%), slightly exceeding expectations. This marks a return to 2%, a level not seen since summer 2023. The increase was driven by rising electricity prices, and rent. Rent increases were partly due to adjustments in subsidised housing, indicating some costs are still being passed to tenants. Overall, Danish price pressure remains relatively muted.

In Sweden, the monthly indicators presented mixed signals. The GDP indicator, known for its unreliability, fell 0.5% m/m but showed positive y/y growth. Household consumption, typically volatile but reasonable measure, decreased from December, indicating a sideways movement overall. Industrial orders exceeded expectations, rising 16% y/y. Private production remained stable, with industrial production value down following a strong previous month. This aligned with our view that Sweden's business sector was performing well, while households continued to face challenges.

In Norway, core inflation increased to 3.4% y/y (prior: 2.8%, cons: 2.9%) in February, notably exceeding Norges Bank's estimate of 2.7%. This unexpected increase raises the question of whether Norges Bank will reconsider its plan to cut rates in March, especially as January figures also exceeded expectations, hinting at accelerating inflation. The likelihood of Norges Bank cutting rates in March has decreased (from almost 100%), and it has become a very close call by now. Markets are pricing 14bp worth of rate cuts for the March meeting and hence close to a 50/50 call. We still expect Norges Bank to deliver the 25bp cut.

Equities: US equities were in free fall yesterday. Nasdaq plunged -4%, marking its worst day since 2022. This was not a rotation into defensives or European shares, but a full-blown growth fear reaction from investors. Clearly, markets tested the Trump put. Or the Musk put for that matter, with Tesla leading the declines by dropping -15%, marking its worst day since 2020. Magnificent Seven all sharply lower, in the ballpark of 2-5%, thereby leading the declines. However, value cyclicals like banks and materials were hit as well. Hence, equal-weight S&P 500 was also dramatically lower, but outperforming cap-weighted index by 130bp. Unlike the last weeks, risk-off also spread to Europe, triggering a classic risk-off rotation leading cyclicals (banks, tech, industrials) to drop 2-3% while defensive stocks were higher. VIX rose to the highest level since August last year.

S&P 500 is now down -8.5% and we are therefore closing in on correction territory. Nasdaq is already there, down -12%. This means that we are inches away from a level where markets typically trough if we are not heading for recession. If this is indeed a correction, positioning is our best friend. Our correction monitor is turning closer to typical "oversold conditions" but not quite there. There are still many more calls in the market, CTA beta remains high, valuations are bloated, and LIBOR vs OIS (the banks stress indicator) is at normal levels. On top of this, markets are in the hands of Trump and not fundamentals. This combination does not make us bold. Hence, we stick to our Europe vs US allocation and do not recommend overweighting US shares just yet.

FI&FX: US yields resumed the decline in yesterday's session amid rising recession fears in markets sending US equities severely in red territory on the first trading day of the week. 10Y and 2Y US swap yields both fell by around ~8 bp which also contributed to stalling the EUR rates sell-off. The Bund ASW-spread is still trading around -12bp. In the Scandies the NOK CPI surprise drove a substantial flattening of the curve with 2s10s dropping 7bp amid markets now pricing the "promised" March Norges Bank rate cut as a close to 50/50-event. This also contributed to NOK being the big overperformer in FX markets even despite Brent Crude oil prices falling below USD 70/bbl on rising growth concerns. EUR/SEK rose somewhat in the early part of yesterday's session now trading just below the 11.00 mark. EUR/USD did little during yesterday's session.

Unwinding of US Exceptionalism Trade Continued and Even Intensified

Markets

There were hardly any (US) data with market moving potential yesterday. If anything, the NY Fed 1-year inflation gauge again drifted marginally higher (3.13%). US officials, including Donald Trump, also abstained from ‘high profile’ comments. Still, it didn’t change markets’ assessment. The unwinding of the US exceptionalism trade continued and even intensified. Major US equity indices declined between 2.08% (Dow) and 4.0% (Nasdaq). The latter cleared the 17468 support (23% retracement rally 2022/24) and reached the target of the ST multiple top formation (neckline 18831). A clear warning signal. Powell’s ‘guidance’ last Friday, that the Fed won’t be carried away by one or two softer data to remove its wait-and-see stance didn’t impress markets. US yields declined between 11.9 bps (5-y) and 5.7 bps (30-y). The US 2-y yield revisited last week’s correction low near 3.84%. Markets are moving further into 75 bps + territory regarding this year’s Fed rate cut expectations. Yields at longer maturities didn’t really test the ST lows. The decline in US yields and steepening of the yield curve in the first place probably mirrors market uncertainty on the impact of the Trump chaos on ST growth and the need/hope for the Fed to come to the rescue at some point. At the same time an ongoing underperformance/ bottoming out of yields at longer maturities at some point also might be an indication of the market questioning the LT US (economic and political) credentials. Whatever one sees as the reason for yesterday’s ‘sell USA repositioning’ (cyclical or structural) it also prevent the dollar from taking up its (usual/previous?) safe haven role. DXY closed little changed near 103.9. Idem for EUR/USD (close 1.0834). The safe haven role, if any, was taken up by the Japanese yen, with USD/JPY briefly dropping below the 147 big figure. Regarding the European side of the global repositioning, the German Greens ‘rejecting’ the proposed reform of the constitutional debt brake (cf infra) maybe to some extent tempered the rise in German/EU yields. Still German yields (2-y -3.1 bps; 30-y +0.7 bp) held up remarkably well given the sharp decline in the US.

Asian equity indices this morning mostly show losses of up to 1.0%/1.5%, with trading still developing rather orderly given yesterday’s WS sell-off US. US yields tentatively stabilize (minus 1/2 bps) , but nothing more than that. The dollar struggles to prevent further losses (DXY 103.7, EUR/USD 1.086, USD/JPY 147.3). Later today, the eco calendar ‘in normal times’ would be assessed as containing only second tier releases with only the US NFIB small business confidence and the JOLTS job openings scheduled for release. However, in current environment, negative surprises might further fuel the reversal of the ‘US exceptionalism trade’. In Europe, the objections of German Greens at least isn’t seen as profoundly changing the new framework of fiscal stimulus. The Bund future is again drifting lower. On FX markets, EUR/USD remains well bid. Las week’s correction top (1.0889) stays within reach with only 1.0937 (Nov top) last intermediate resistance on the path to a complete reversal to the 1.1214 2024 top.

News & Views

The German Green party presented a counter-offer after indicating that they wouldn’t support Chancellor-to-be Merz’s proposed constitutional reforms to raise deficit spending via the outgoing parliament (new Bundestag gets seated on March 25). The Greens want to raise the threshold for defense spending exemptions from debt rules to 1.5% of GDP instead of the 1% proposed by Merz. They don’t seem to have an issue with the two other pillars of the plan, setting up a €500bn infrastructure fund and loosing states’ fiscal rules. The main bills are interconnected and probably need to pass together through parliament. Afterwards, the Bundesrat, representing the states also needs to approve proposed legislature with a 2/3rd majority. Some more horse-trading will be needed as CDU/CSU/SPD/Greens lack the numbers in two of the 16 states.

UK consumer spending lost momentum in February after a bounce in January. Sales at member stores of the British Retail Consortium rose by 1.1% Y/Y, down from 2.6% Y/Y in January. BRC CEO Dickinson said that the weak performance makes many retailers uneasy, especially as they brace for GBP 7bn of new costs from the Budget and packaging levy in 2025, as well as the potential impact of the Employment Rights bill. The industry is already doing all it can to absorb existing costs, but they will be left with little choice but to increase prices or reduce investment in jobs and shops, or both.

America First to the Bottom

It’s both nothing and everything at the same time that sent the markets to a dark hole on Monday. The stock markets across the globe were heavily hit by the fears that Trump trade and international policies would have a terrible economic and geopolitical fallout in the US and beyond its borders. The recession bets are rising by the day, the companies are giving murkier forecasts due to tariffs, the US’ biggest trading partners respond. Ontario in Canada for example asked its grid operator to increase its prices on US exports by 25%. China imposed 10-15% tariffs on US agricultural imports, Delta headlines yesterday joined its peers in slashing its Q1 revenue forecast pointing at weak consumer and corporate travel, and all major US indices from small to big caps are making big moves to the downside. The Trump optimism is far gone. The S&P500 has now wiped out all the post-election gains. The index made a second and sharp dip below the 200-DMA and closed the session . Nasdaq 100 dropped 3.80% yesterday, extended losses below its own 200-DMA, below the 20’000 psychological mark, having tested the minor 23.6% Fibonacci retracement on the AI rally that started in 2023 and having lost more than 10% since its February ATH peak. It means that Nasdaq is officially in the correction zone. Tesla has lost more than 15% just yesterday, wiped out all the post-election gains and is down by more than 50% since the December peak on expectation that Musk’s involvement in world’s politics will have an ugly impact on its sales. Then, the most popular ‘America First’ indices, the mid and small caps are also hammered. The US mid cap index has now fallen below the major 38.2% Fibonacci retracement on last October-to-now rally and stepped into the bearish consolidation zone. And the small cap index, the Russell 2000, has already stepped below its own major 38.2% Fibonacci retracement at the start of the month and has now given back more than half of the Trump-led gains. All indices are now close or in the oversold condition territory, but the fact that we are coming from a very high optimism peak for the US equities and strong global long positioning, the pullback has room to deepen. The diving US yields on recession bets and the rising safe haven demand is no consolation. It tells a lot about how investors feel about what’s cascading from the White House: it’s the worst market sentiment since Covid. A softer-than-expected CPI update from the US tomorrow could eventually slow down the selloff on the thinking that the Federal Reserve (Fed) could - maybe - help soothing investors’ nerves. But a stronger-than-expected figure would be very bad news.

Now, the White House disaster has been a boon for the European stocks. The US’ decision to pull back its military support from under the feet of the Europeans unleased the European beast. The European countries led by Germany threw their budget discipline out of the window and pledged to spend hundreds of billions of euros to strengthen their defense budgets and the latter sent the DAX some 18% higher since the beginning of January, while the S&P500 lost more than 5% during the same period and almost 10% since its February peak. But even the DAX index looked sorry yesterday as the Greens in Germany rejected a debt-financed package because their green demands weren’t well responded in Merz’ plans. And Merz needs the Greens - as it needs a two-thirds majority - to pass a constitutional amendment to ease borrowing restrictions. But hey, German Greens’ co-leader said on Bloomberg TV this morning that there could be a deal on budget as early as this week and the EU is making the same moves to let the member states borrow more to throw at defense. As such, the European stocks will likely continue to outperform their US peers, although gains could become vulnerable if the global market sentiment gets worse from here.

The goodnews is that the selloff seems to have moderated in Asia and the futures are in the positive in Europe at the time of writing. The risks remain skewed to the downside for the US equities, cautiously to the upside for the European peers. Conversely, appetite for US sovereign bonds is rising on the expectation that the Fed can’t let the US economy collapse, while the European sovereign bonds are offered on the sudden end of the budget discipline on the old continent. Gold remains a popular hedge for investors seeking refuge from the agitated international waters, while Bitcoin has so far failed to give that sort of ‘safe haven’ comfort to investors.

In the traditional currency space, the USD selloff has somewhat slowed yesterday, but the dovish shift in Fed expectations and hawkish shift in other central bank expectations - like the European Central Bank (ECB) expectations for example on the thinking that the ECB must slow down rate cuts to temper the impact of massive government spending - continue to keep the outlook for the US dollar negative compared to major peers.

In energy, US crude is testing the $65pb level to the downside on waning growth expectations. The outlook remains skewed to the downside.

EUR/USD Daily Outlook

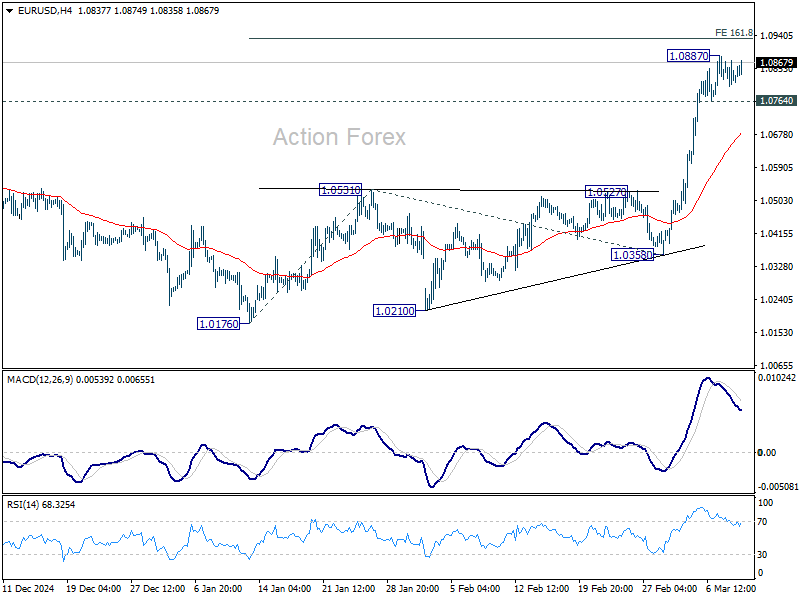

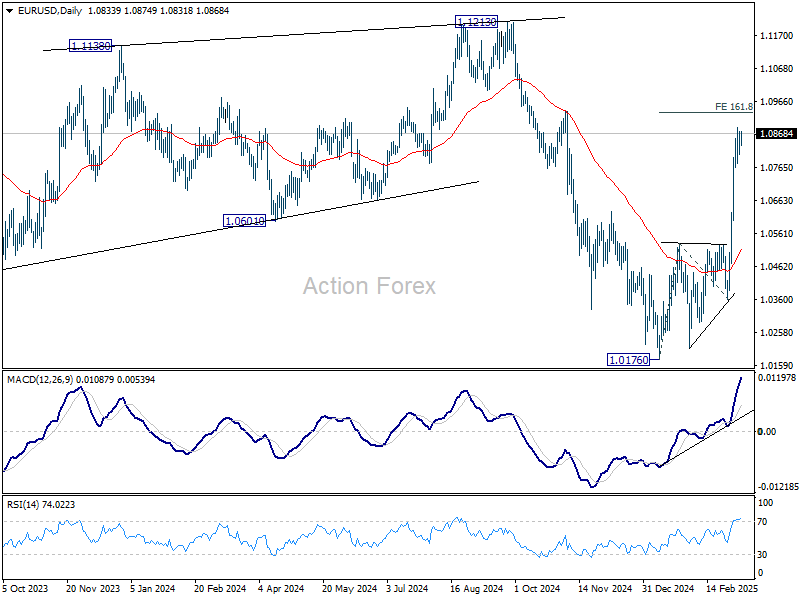

Daily Pivots: (S1) 1.0802; (P) 1.0839; (R1) 1.0872; More...

Intraday bias in EUR/USD is turned neutral first with current retreat. Some consolidations would be seen below 1.0887 temporary top. Downside should be contained by 55 4H EMA (now at 1.0682) to bring another rally. Above 1.0887 will resume the rise from 1.0176 to 161.8% projection of 1.0176 to 1.0531 from 1.0358 at 1.0932. Firm break there will pave the way back to 1.1274 key resistance next.

In the bigger picture, the strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

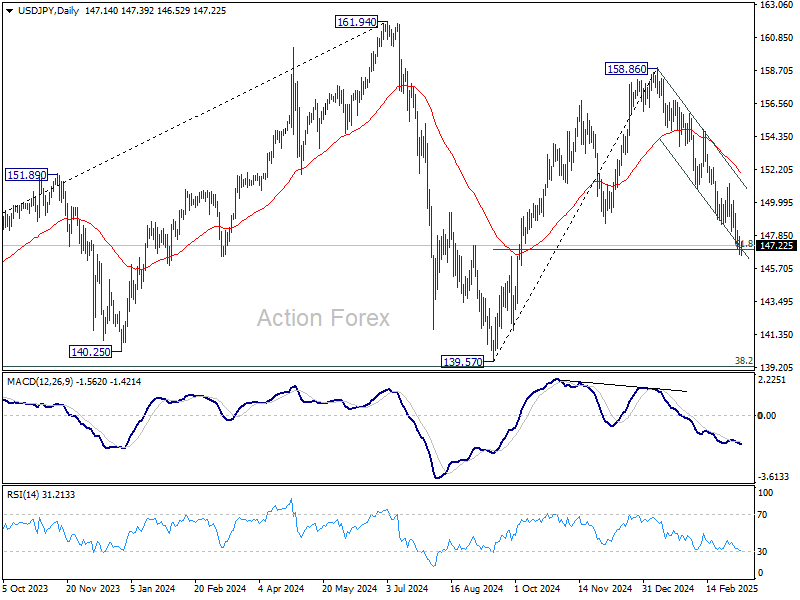

USD/JPY Daily Outlook

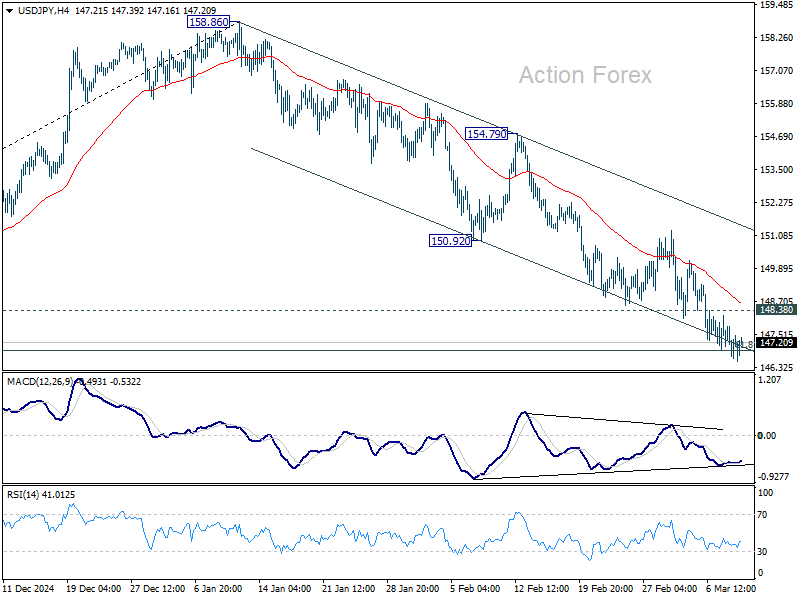

Daily Pivots: (S1) 146.59; (P) 147.30; (R1) 147.97; More...

Intraday bias in USD/JPY remains mildly on the downside for the moment. . Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support. On the upside, 148.38 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another fall.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

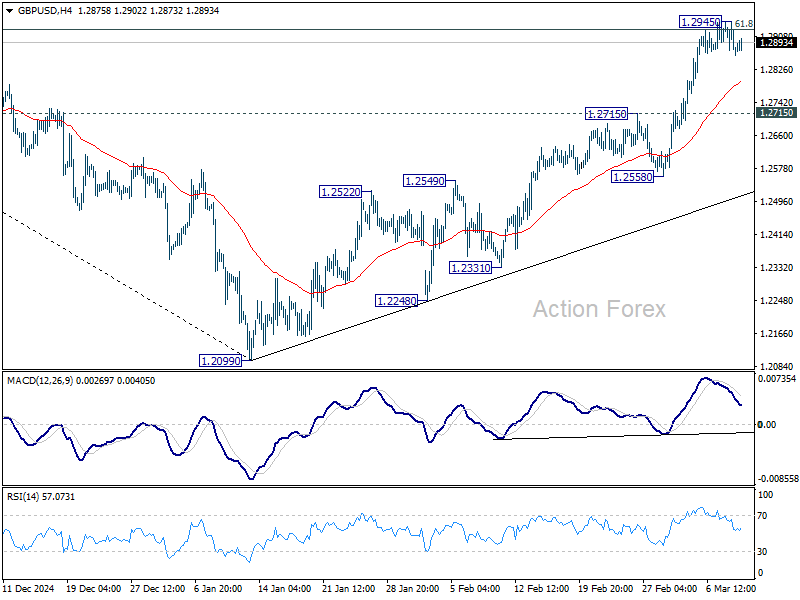

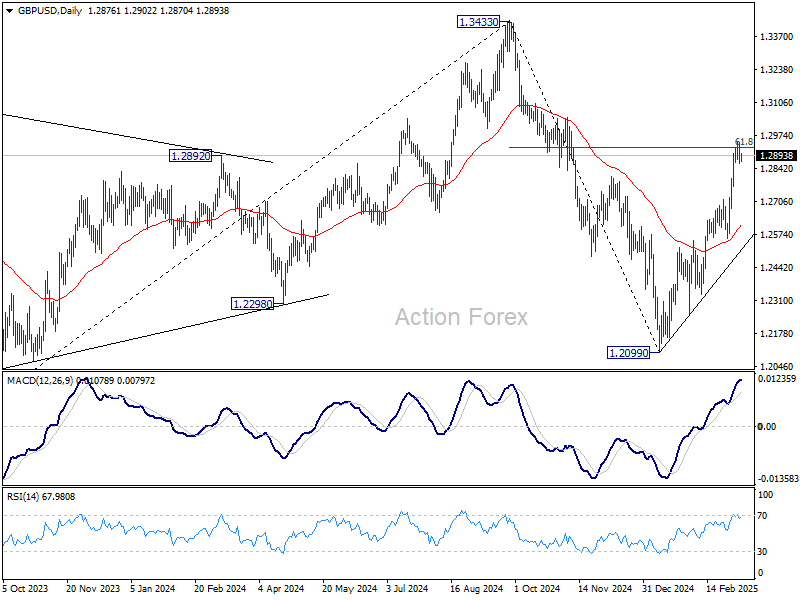

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2843; (P) 1.2895; (R1) 1.2928; More...

Intraday bias in GBP/USD stays neutral for consolidation below 1.2945 temporary top. Downside of retreat should be contained by 1.2715 resistance turned support to bring another rally. On the upside, sustained break of 61.8% retracement of 1.3433 to 1.2099 at 1.2923 will pave the way back to 1.3433 high.

In the bigger picture, fall from 1.3433 (2024 high) should have completed at 1.2099 as a corrective move. Up trend from 1.3051 (2022 low) is still in progress but it's too early to say that it's resuming. Corrective pattern from 1.3433 could extend with one more down leg. But after all, eventual upside breakout is expected at a later stage.

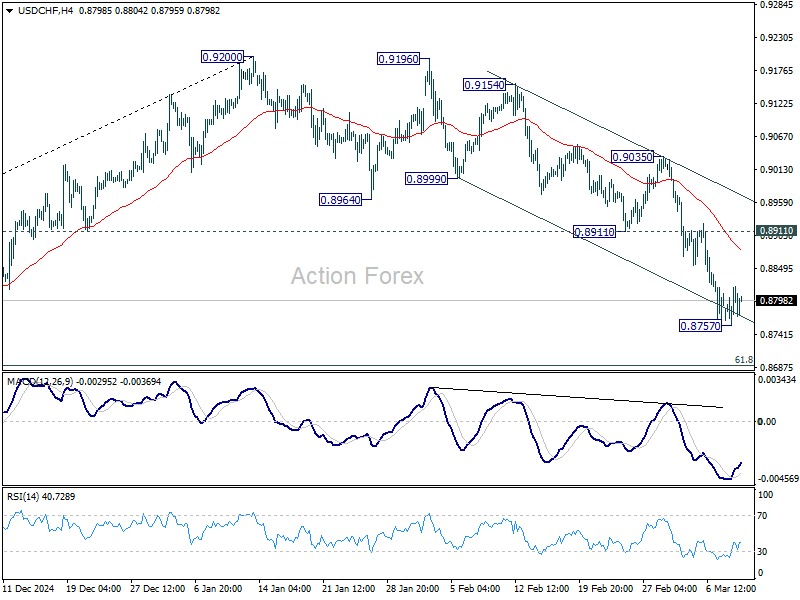

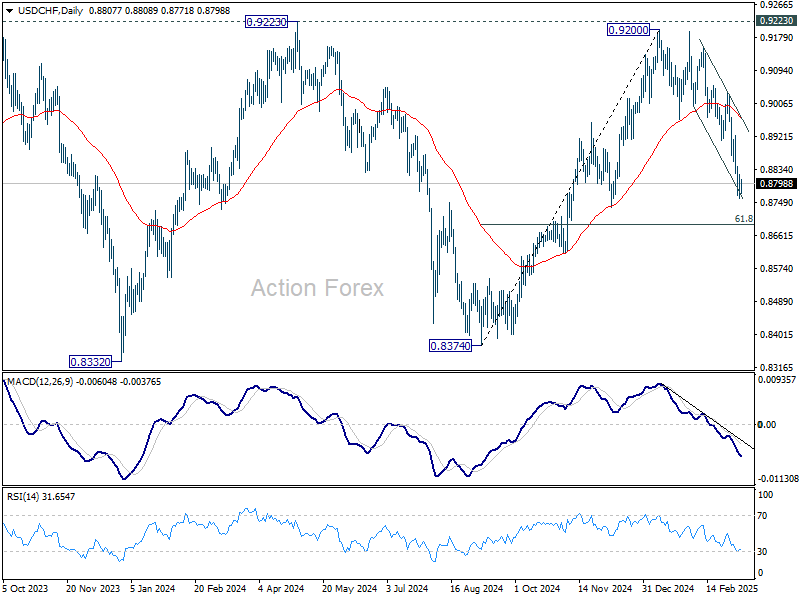

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8770; (P) 0.8796; (R1) 0.8834; More…

Intraday bias in USD/CHF is turned neutral with current recovery, and some consolidations would be seen above 0.8757 temporary low. Upside should be limited by 0.8911 support turned resistance to bring another fall. On the downside, below 0.8757 will target 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

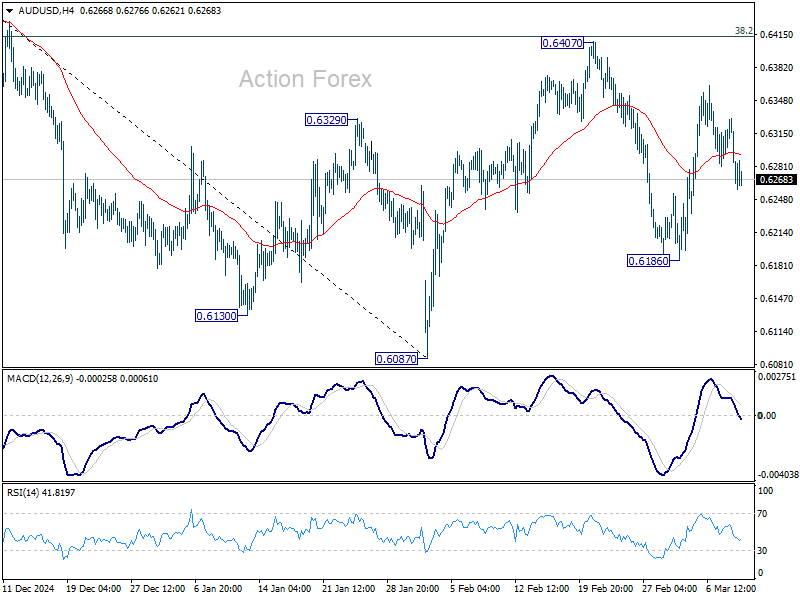

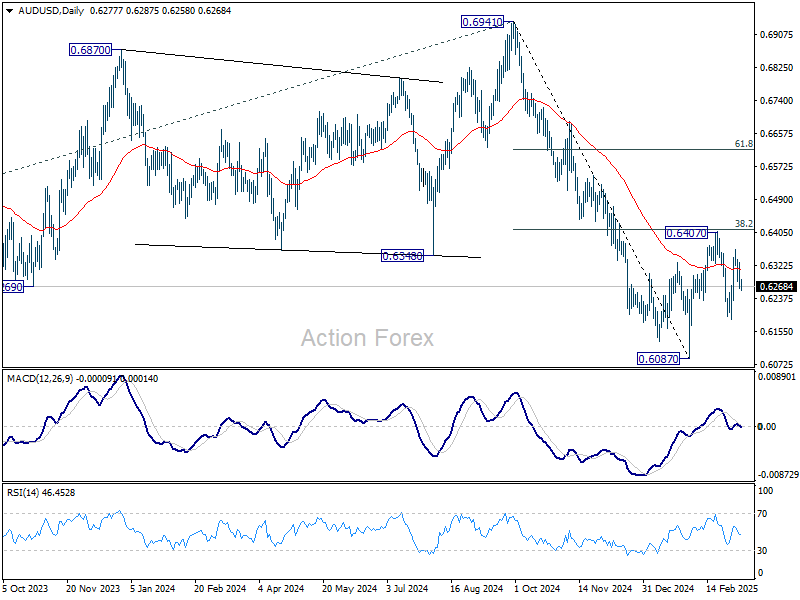

AUD/USD Daily Report

Daily Pivots: (S1) 0.6252; (P) 0.6292; (R1) 0.6318; More...

Intraday bias in AUD/USD stays neutral for now. On the downside, break of 0.6186 will target 0.6087 support first. Firm break there will resume whole decline from 0.6941. However, sustained trading above 38.2% retracement of 0.6941 to 0.6087 at 0.6413 will raise the chance of near term bullish reversal, and target 61.8% retracement at 0.6615 next.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6487) holds.

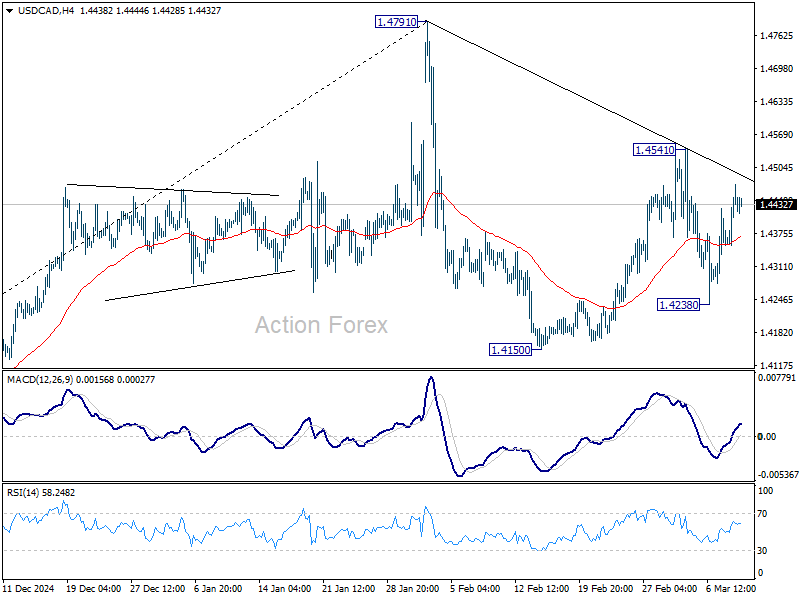

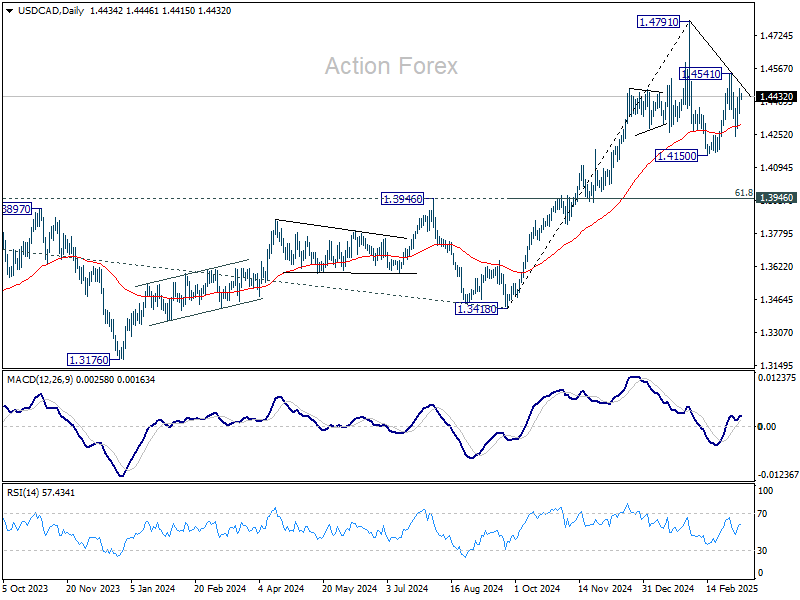

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4370; (P) 1.4422; (R1) 1.4490; More...

Intraday bias in USD/CAD remains neutral and outlook is unchanged. Overall, corrective pattern from 1.4791 should still be extending. Break of 1.3248 will target 1.4150 support and possibly below. Meanwhile, break of 1.4541 will bring stronger rise back to retest 1.4791.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

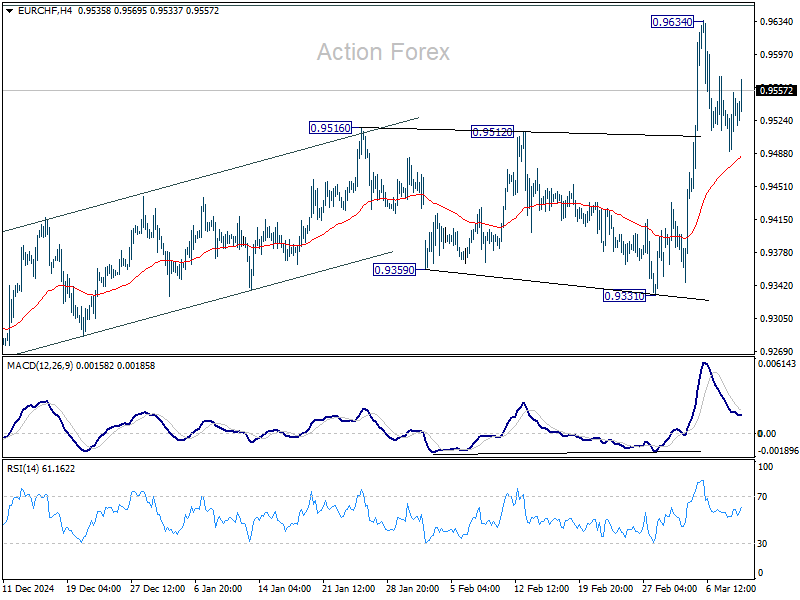

EUR/CHF Daily Outlook

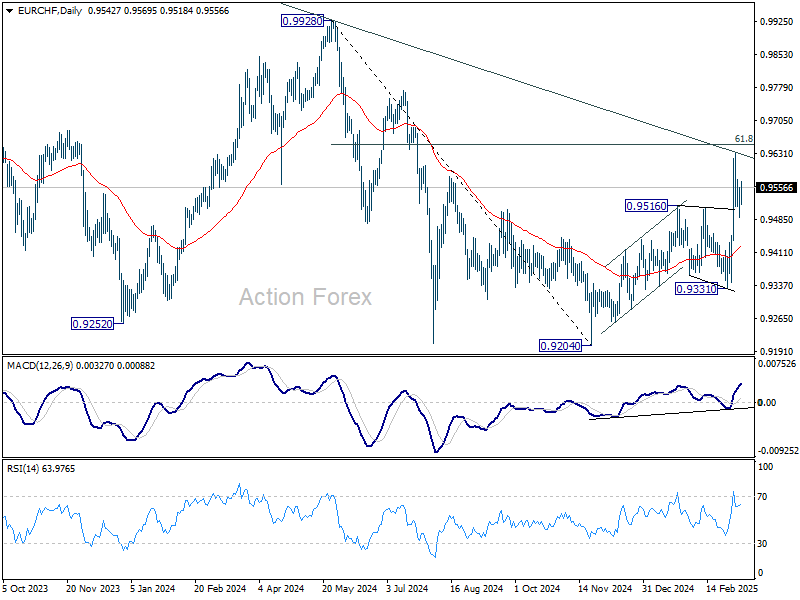

Daily Pivots: (S1) 0.9505; (P) 0.9531; (R1) 0.9571; More....

EUR/CHF is staying in consolidations below 0.9634 and intraday bias remains neutral. Further rally will be expected as long as 55 4H EMA (now at 0.9485) holds. On the upside, above 0.9634, and sustained trading above 61.8% retracement of 0.9928 to 0.9204 at 0.9651 will pave the way back to 0.9928 key resistance next.

In the bigger picture, the strong break of 55 W EMA (now at 0.9482) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9620) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be see to 0.9928 key resistance at least.