Sample Category Title

Elliott Wave Analysis: USDJPY and USDCHF Update

Hello traders!

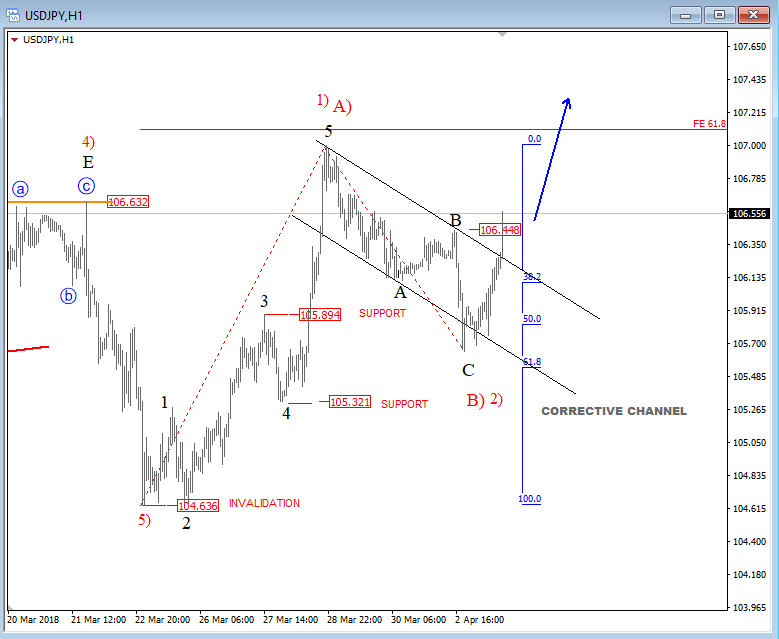

Current strong recovery and a break above the upper corrective channel line on USDJPY suggests a completed three-wave correction since the end of March and a new bullish cycle to be in play. At the same time, we also see price trading above the 106.45 level which can confirm more upside on the pair.

USDJPY, 1h

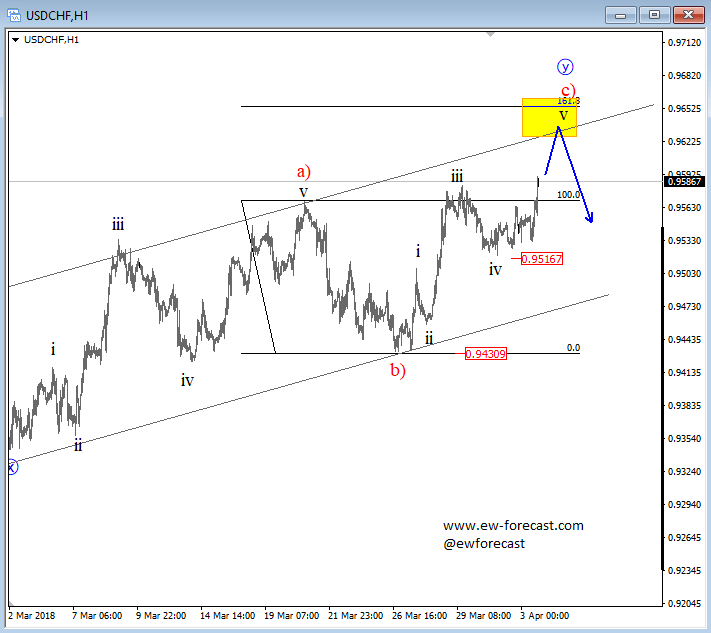

USDCHF is still trading higher in a complex correction w-x-y and we say correction because of overlapped wave structure, so currently can be in the final stages in c) of y that can stop around 1.9650 level.

USDCHF is still trading higher in a complex correction w-x-y and we say correction because of overlapped wave structure, so currently can be in the final stages in c) of y that can stop around 1.9650 level.

USDCHF, 1h

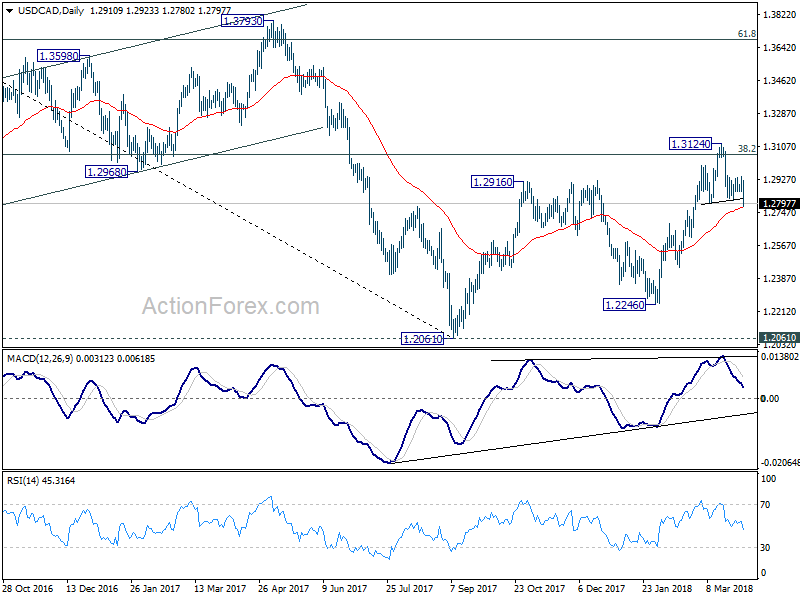

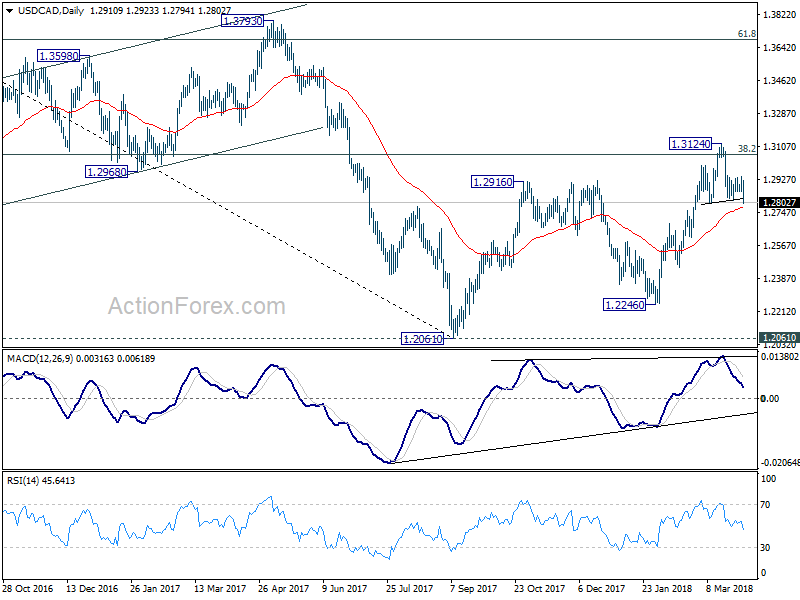

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2868; (P) 1.2906; (R1) 1.2949; More....

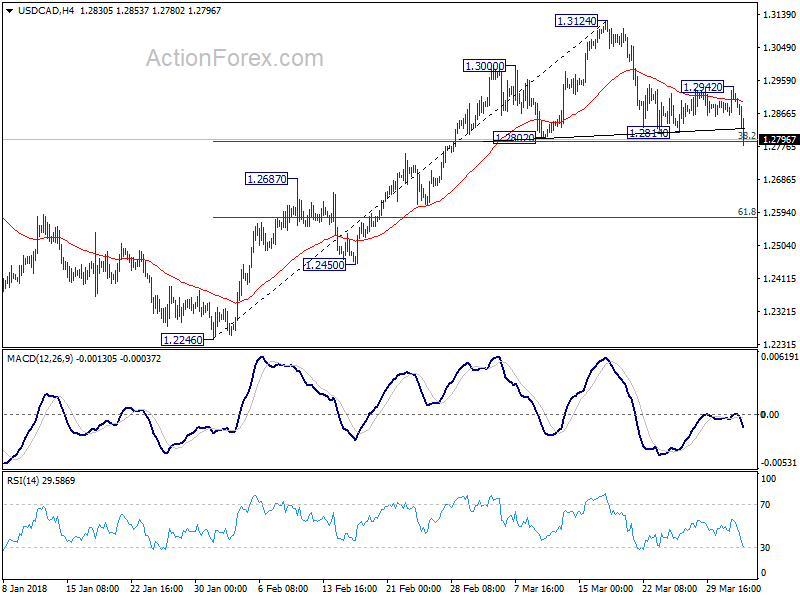

USD/CAD's sharp decline today now puts 38.2% retracement of 1.2246 to 1.3124 at 1.2789 into focus. Sustained break there should confirm near term reversal, on head and shoulder top pattern (ls: 1.3000; h: 1.3124; rs: 1.2942). That will also indicate rejection by 1.3065 fibonacci level. Deeper fall would than be seen back to 1.2246 support next. On the upside, though, break of 1.2942 will indicate support from 1.2789 and turn bias back to the upside for 1.3124.

In the bigger picture, outlooks is turned a bit mixed again. Strong support was seen from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. But there was no follow through buying above 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

Pound Edges Higher as UK Manufacturing PMI Beats Estimate

The British pound has posted small gains in the Tuesday session. In the North American session, GBP/USD is trading at 1.4070, up 0.20% on the day. On the release front, British Manufacturing PMI ticked lower to 55.1, beating the estimate of 54.8 points. Later in the day, the UK releases BRC Shop Price Index. In the US, there are no major events. IBD/TIPP Economic Optimism dropped to 52.6, well below the estimate of 55.2 points. This marked a 4-month low. On Wednesday, the UK releases Construction PMI and the US publishes ADP non-farm payrolls and the ISM Non-Manufacturing PMI.

The Brexit negotiations have been bumpy and often acrimonious, but last month there was some positive news in March, with the announcement of a transition period. This phase will take effect at the end of March 2019, when Britain leaves the European Union and will run until December 2020. It is meant to serve as a “cushion” to allow businesses to adjust to Britain’s departure. Broadly speaking, EU rules will still apply to the UK, but Britain will no longer have a seat at the table with regards to EU decision-making. However, according to a report in the Times newspaper on Tuesday, EU regulators have warned UK banks operating on the Continent not to rely on the transition deal, and to prepare for a “hard Brexit”, in which the UK would simply depart the EU without any agreement. This position is in stark contrast to that of the Bank of England, which has embraced the transition agreement. The status of financial services in the post-Brexit era remains a key sticking point between the sides, and the stakes are very high, as Paris and Frankfurt are hoping to lure thousands of financial jobs away from the City of London.

Investors continue to monitor the tariff battle between China and the US. The week started with China retaliating and imposing its own duties on a range of US goods, including frozen pork and wines. For its part, the US is expected to list which Chinese product will be subject to US tariffs. With the two economic giants showing no signs of backing down, there are growing fears that a new global trade war could be underway. If the tit-for-tat measures continue, both the US and Chinese economies could suffer, which could lead to a global recession.

Yen Dips Lower, Investors Eye ADP Nonfarm Payrolls

USD/JPY has posted considerable gains in the Tuesday session, after starting the week with losses. In the North American session, USD/JPY is trading at 106.54, up 0.61% on the day. It’s quiet on the release front, with no Japanese events. In the US, IBD/TIPP Economic Optimism dropped to 52.6, well below the estimate of 55.2 points. This marked a 4-month low. On Wednesday, the US releases two major indicators – ADP non-farm payrolls and the ISM Non-Manufacturing PMI.

The Japanese economy continues to perform well, and predictably, business confidence remains strong. The Tankan indices pointed to solid optimism in the fourth quarter, in both the services and manufacturing sectors. The manufacturing indicator edged down from 25 to 24 points, and confidence in the services sector was unchanged at 23 points. The Japanese economy continues to perform well, boosted by stronger global demand. However, the Tankan indices also reported that many businesses are reporting a shortage of skilled labor. Unemployment levels in Japan have fallen to 25-year lows, as the economy has improved while the working-age population continues to shrink.

Investors continue to monitor the tariff battle between China and the US. The week started with China retaliating and imposing its own duties on a range of US goods, including frozen pork and wines. For its part, the US is expected to list which Chinese product will be subject to US tariffs. With the two economic giants showing no signs of backing down, there are growing fears that a new global trade war could be underway. If the tit-for-tat measures continue, both the US and Chinese economies could suffer, which could lead to a global recession. The yen is a key safe-haven asset, and nervous investors could snap up the Japanese currency if there is no quick resolution to the tariff spat unleashed by US President Trump.

Yen Rising As Safe Haven Demand Increases

The Japanese yen confirmed its safe haven status again. The previous correction was quite technical, as the market was trying to balance the USD/JPY pair without any significant fundamentals published. Now, the economic events are flowing into the market again, and the news are very much negative, which, as a rule, does influence the Japanese currency.

First and foremost, the markets are very wary about the 'trader war' between the US and China, which can start any time. The US government imposed some customs duties unilaterally against steel and aluminum a few weeks ago. Donald Trump said this was just for boosting the internal production and making the competition easier for the local manufacturers. Additionally, the US also imposed duties on the goods manufactured in China.

It did not take Middle Kingdom too long to respond, as recently a list of 100 US goods was published; these goods will be liable to customs duties if imported into China. As much as expected, this piece of news still caused a massive hunt for the safe haven assets, including the yen.

The markets are now considering whether these 'trade wars' will lead to some conflicts and daring moves involving other participants of the world trade process. It's all very quiet for Japan for now, as the US previously told they were ready to negotiate everything peacefully. Still, these are no more than just talk for now.

If the markets suspect any possibility of the world trade processes facing some issues, the yen may rise once more against the greenback.

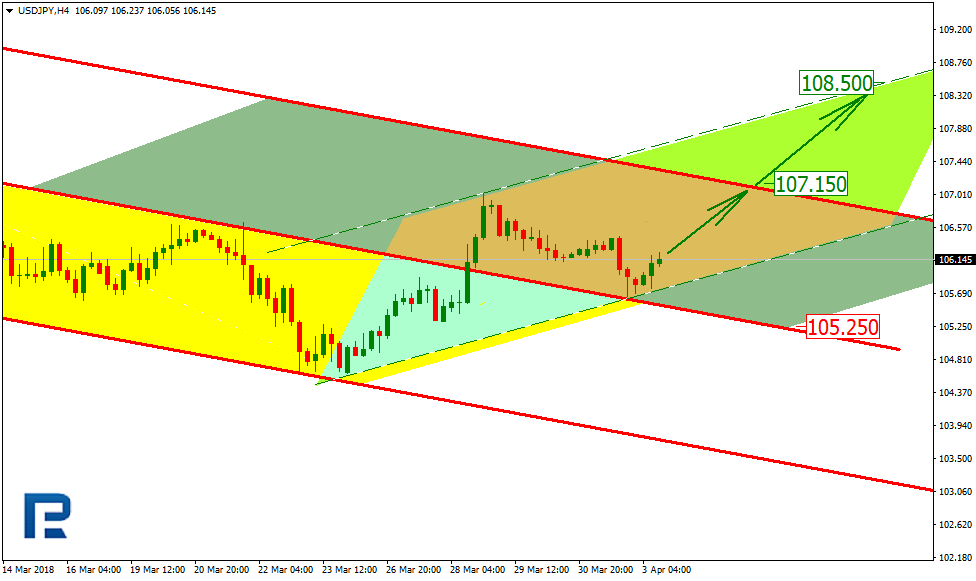

On H4, USD/JPY has overcome the resistance and moved to the upper projection channel. At the same time, the price tested the broken out resistance and turned it into a support. Technically, this enables locating an ascending channel. The first move may target the current resistance at 107.15. After breaking out the projection channel resistance, the price may go well ahead to the upside channel resistance at 108.50. The support for the current move is at 105.25.

Sunset Market Commentary

Markets:

The German Bund opened stronger this morning after a long Easter weekend, catching up with the Note future’s gains in yesterday’s risk-off climate. The contract traded volatile in the first European trading hours which coincided with moves on European stock markets. The Bund returned towards last Thursday’s closing level (previous trade date) by European noon. Risk sentiment improved going into the start of US dealings, capping Bund gains. There was no escalation of the Chinese/US trade war. The US Note future underperforms, coming off yesterday’s highs with key events later this week keeping many investors sidelined (US ADP employment report, non-manufacturing ISM, payrolls & speech by Fed chair Powell). Today’s eco calendar only contained the final EMU manufacturing PMI (confirmed at 56.6) which didn’t leave traces on markets. The US yield curve bear steepens at the time of writing with yields 2.4 bps (2-yr) to 4.6 bps (30-yr) higher. The German yield curve flattens with yield changes ranging between +0.8 bps (2-yr) and -0.8 bps (30-yr). 10-yr yield spreads versus Germany barely moved with Portugal underperforming (+3 bps) and Greece outperforming (-4 bps).

The (intraday) improvement in risk sentiment was mostly visible in a setback for the Japanese yen even if BoJ governor Kuroda said that the BoJ is internally discussing its exit options from the current very easy monetary policy. The timing will of course depend on what happens with the economy, markets and prices at the time and the exit won’t occur in the near future. The BoJ is expected to normalize monetary policy only after the ECB. USD/JPY rebounds from 105.7 to 106.3, while EUR/JPY bounced off the 130-mark towards 130.80. EUR/USD mostly remained an island of calm today. The dollar gradually gained some more momentum with the US/German yield spread widening in favour of the greenback. EUR/USD dropped below the downside of the extremely thin sideways range of the past days (1.2282) just ahead of the US opening bell. Strong US car sells might have delivered the final push, while technical elements were probably at play as well. Main US stock markets rebound around 0.5% at the start of US trading.

Sterling gained marginally ground today with EUR/GBP moving from 0.8760 to 0.8730. The UK manufacturing PMI stabilized at 55.1 in March, while consensus expected a small setback towards 54.7. The PMI suggests that the Bank of England indeed has room to gently hike rates to fight inflation without risking a major setback for the UK economy. GBP/USD showed some intraday price swings, but maintains north of 1.4050.

News Headlines:

German monthly retail sales unexpectedly declined in February (-0.7% M/M). The third monthly fall in a row signalled that private consumption may remain weak in early 2018 after failing to contribute to growth in the fourth quarter.

The New York Federal Reserve launched a benchmark US rate today to potentially replace Libor. Market participants hope it will prove more reliable after a long and complex switchover. The Secured Overnight Financing Rate (SOFR) set at 1.80%. SOFR is based on the overnight Treasury repurchase agreement market.

The Czech Republic has been sounding out the EU on winning an exemption from guaranteeing the old debt of EMU member states covered by EU financing mechanisms, as a way to encourage its people to back adopting the euro at some point, daily Hospodarske Noviny reported.

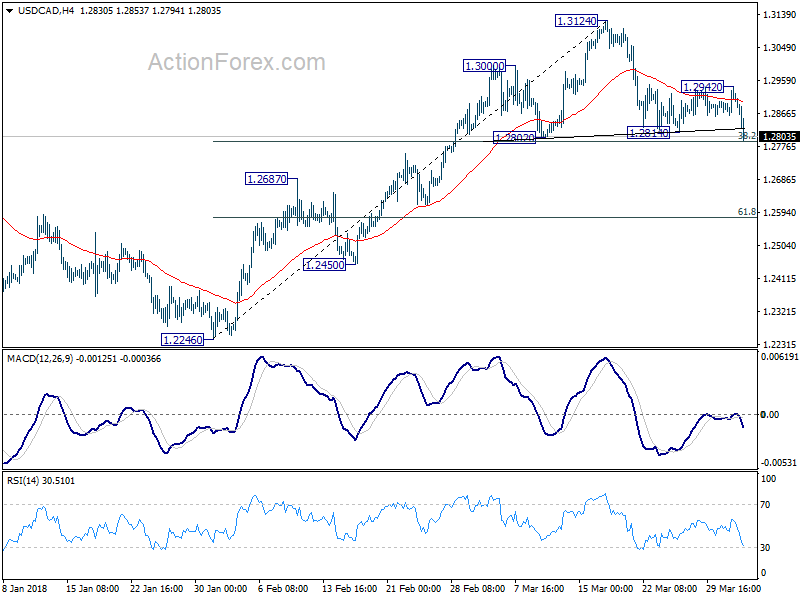

USDCAD head and shoulder top threatening bearish reversal

USD/CAD's selloff accelerates as the US session goes on, as supported by NAFTA news. The break of 1.2814 support now raise the chance of a head and shoulder top reversal pattern. (ls: 1.3000; h: 1.3124; rs: 1.2942). But for now, we'd prefer to see sustained break of 38.2% retracement of 1.2246 to 1.3124 at 1.2789 to confirm.

Also bare in mind that such near term reversal would also indicate rejection by 38.2% retracement of 1.4689 to 1.2061 at 1.3065. And in that case, the rebound from 1.2061 could have completed as a corrective three waves pattern to 1.3124 too. And in that case, 1.2061/2246 support zone will be back in sight.

For now, we'll wait and see if 1.2789 would be firmly taken out.

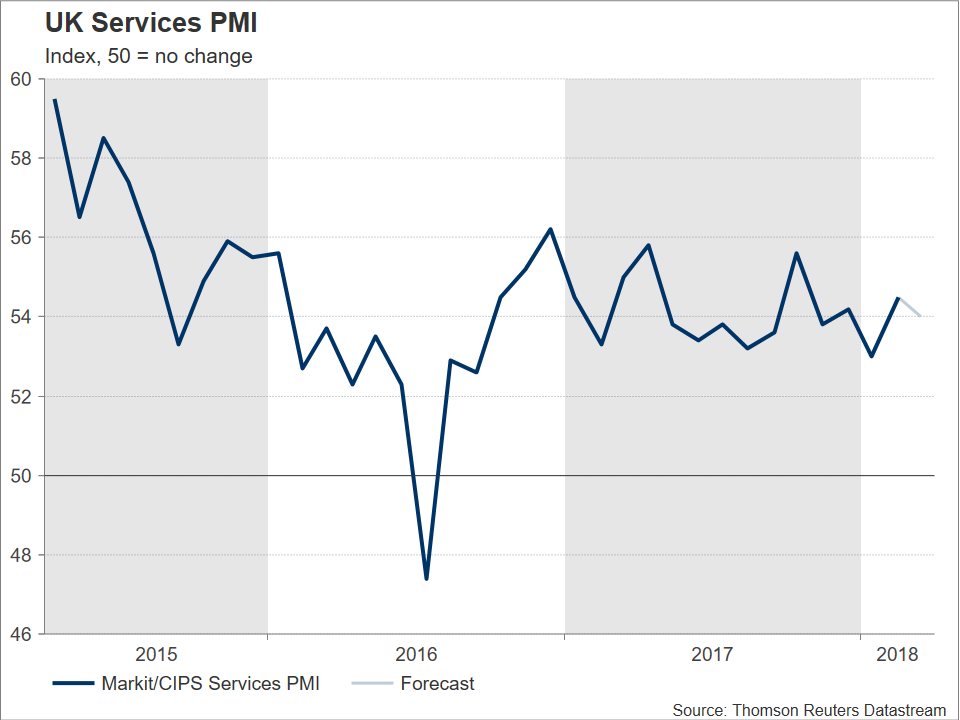

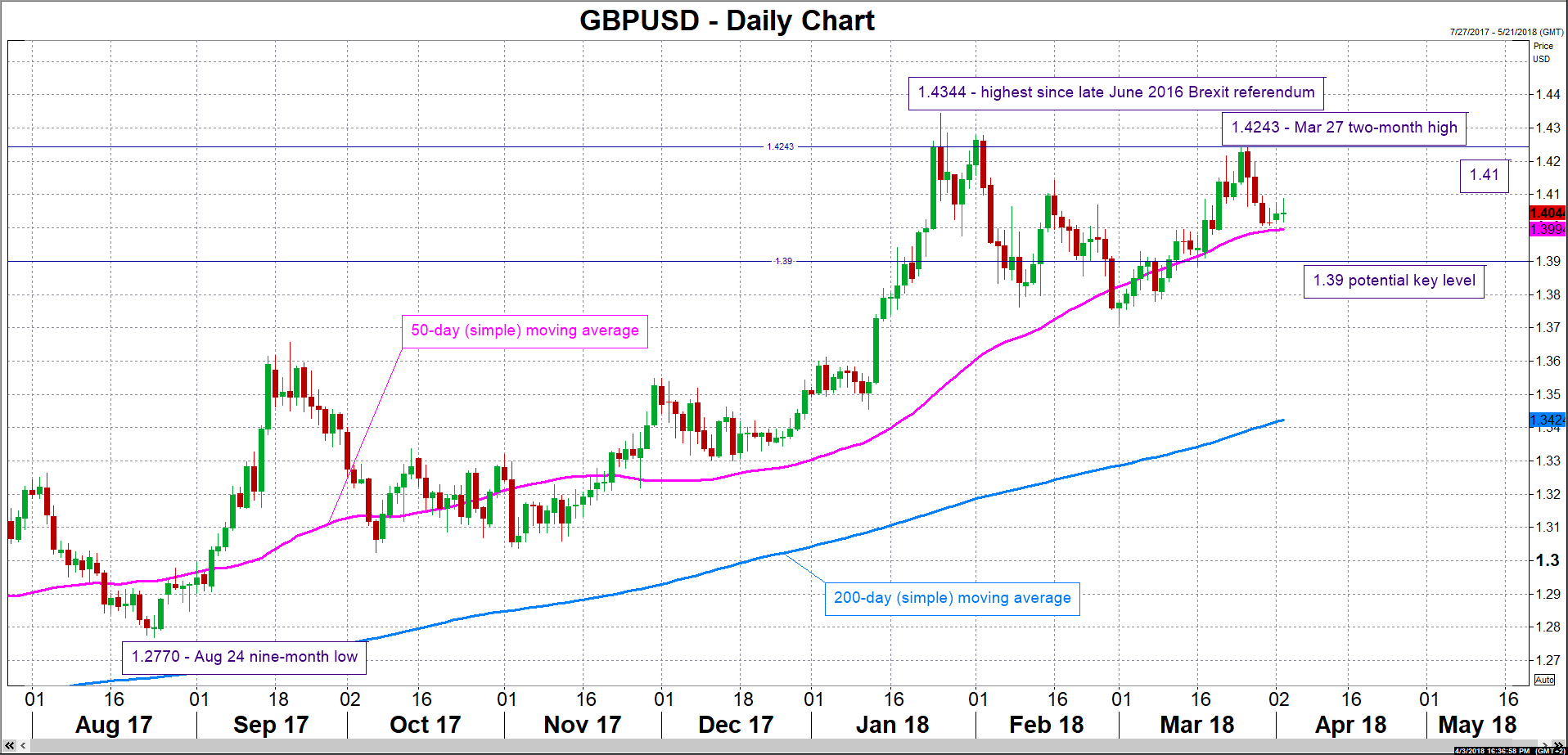

UK PMIs to Stoke May Hike Odds by the Bank of England?

The UK will see the release of March PMI figures for the construction and services sectors on Wednesday and Thursday respectively, both at 0830 GMT. The figures, especially the one for the dominant-for-the-UK-economy services sector, have the capacity to steer the probability of an interest rate hike by the Bank of England when it next meets in May, consequently leading to movements in sterling pairs.

The upcoming Markit/CIPS construction PMI reading is anticipated to stand at 50.8 and the one for the services sector is projected to come in at 54.0. Should both prints come as expected, they would reflect a reduction relative to February’s respective figures of 51.4 and 54.5. The 50-level separates expansion from contraction in the corresponding sector.

In terms of market reaction, that is likely to be more profound in the case of the services reading, given the sector’s prominence within the UK economy, contributing around 80% of GDP.

At the moment, the odds are in favor of a Bank of England interest rate increase by 25bps upon completion of its upcoming meeting on May 10, with markets having priced in such an outcome by 73% according to UK overnight index swaps. Strong PMI readings could give an additional lift to those projections, boosting the pound along the way.

At the moment, the odds are in favor of a Bank of England interest rate increase by 25bps upon completion of its upcoming meeting on May 10, with markets having priced in such an outcome by 73% according to UK overnight index swaps. Strong PMI readings could give an additional lift to those projections, boosting the pound along the way.

Focusing on pound/dollar, upbeat figures could see the pair advancing to meet resistance around the 1.41 round figure, before the attention starts to increasingly turn to last week’s two-month high of 1.4243. Conversely, a disappointment on the data front might see the pair heading lower. Immediate support could be taking place at the moment around the current level of the 50-day moving average at 1.3994, including the 1.40 handle that may be of psychological significance. A downside violation would shift the attention to the range around 1.39, which was relatively congested in the recent past, for additional support.

Earlier on Tuesday, manufacturing PMI numbers for the month of March were made public. Those surprised positively, coming in at 55.1 compared to the forecasted 54.7, suggesting that poor weather conditions affecting the nation did not have much of an impact on factories’ activity. Not everything was rosy though, with February’s print being revised downwards and new orders rising by the least in nine months. Moreover, manufacturing growth slid to a one-year low in Q1 2018, with Markit recognizing that UK “manufacturing has entered a softer growth phase.” For the record, manufacturing makes up around 10% of the UK economy.

Earlier on Tuesday, manufacturing PMI numbers for the month of March were made public. Those surprised positively, coming in at 55.1 compared to the forecasted 54.7, suggesting that poor weather conditions affecting the nation did not have much of an impact on factories’ activity. Not everything was rosy though, with February’s print being revised downwards and new orders rising by the least in nine months. Moreover, manufacturing growth slid to a one-year low in Q1 2018, with Markit recognizing that UK “manufacturing has entered a softer growth phase.” For the record, manufacturing makes up around 10% of the UK economy.

The reaction by market participants to manufacturing PMI data was muted within the first minutes of data release.

In the bigger picture, pound/dollar is up by 3.9% year-to-date, with sterling recording its best quarterly performance versus the greenback since 2015 in Q1 2018. The British currency was largely helped by Brexit-related developments – trading higher relative to the euro year-to-date as well – specifically the transition deal relating to its exit from the EU secured in March. Sterling is expected to remain sensitive to any updates on Brexit issues as the year unfolds.

Lastly, it is noteworthy that a seasonal trend tends to play out in April that is supportive of a stronger pound/dollar pair and is fueled by foreign companies making dividend payments to British shareholders. Within the context of the current week though, it should be kept in mind that numerous US releases can also spur movements in the pound/dollar pair. Most notable of those is Friday’s jobs report, while the world’s largest economy will see the release of its own services PMI out of the Institute for Supply Management on Wednesday. Adding to these, an escalation of trade tensions between the US and China is seen as a dollar-negative factor.

CAD and USD lifted by NAFTA news

Both CAD and USD seem to be lifted by news regarding NAFTA as American traders get up in the morning. Bloomberg reported, citing unnamed sources, that Trump is pushing for a preliminary NAFTA deal to be announced next week. That would likely happen at the Summit of the Americas in Peru on April 13.

For now the story is not verified by other media yet. But it's believed that Mexican Economy Minister Ildefonso Guajardo will meet with US Trade Representative Robert Lighthizer on Wednesday. Canadian Foreign Minister Chrystia Freeland will also meet Lighthizer on Thursday. White House trade advisor Peter Navarro also said on Monday that it's realistic to wrap up NAFTA in two weeks.

In any case, we'll likely have something more concrete in the coming days.

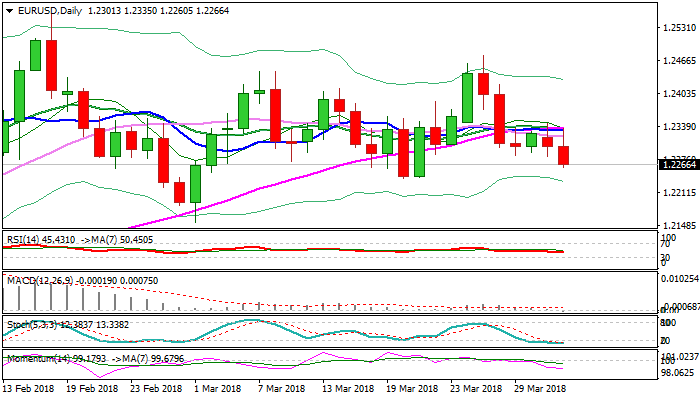

EURUSD Probes Below Range Floor, Pressured by Weak Data

The Euro enters the American session at the back foot and pressures the floor of four-day congestion at 1.2280 zone, after upside attempts in early European trading stalled on attempts through congestion tops, reinforced by converged 10/20/55SMA's at 1.2335. Weaker than expected German Manufacturing PMI data put the pair under fresh pressure for probe through 1.2280 pivot. Daily MA's and momentum are in bearish setup and maintain pressure, as eventual close below 1.2280 will signal an end of consolidative phase and extension of bear-leg from 1.2476 (27 Mar high). Fresh weakness eyes double-bottom at 1.2240, break of which would expose key short-term supports at 1.2172/46 (Fibo 38.2% of 1.1553/1.2555/daily cloud base). Only close above MA's cluster at 1.2335 would neutralize bearish threats and turn imme4diate focus higher.

Res: 1.2300; 1.2320; 1.2335; 1.2368

Sup: 1.2240; 1.2200; 1.2172; 1.2146