Sample Category Title

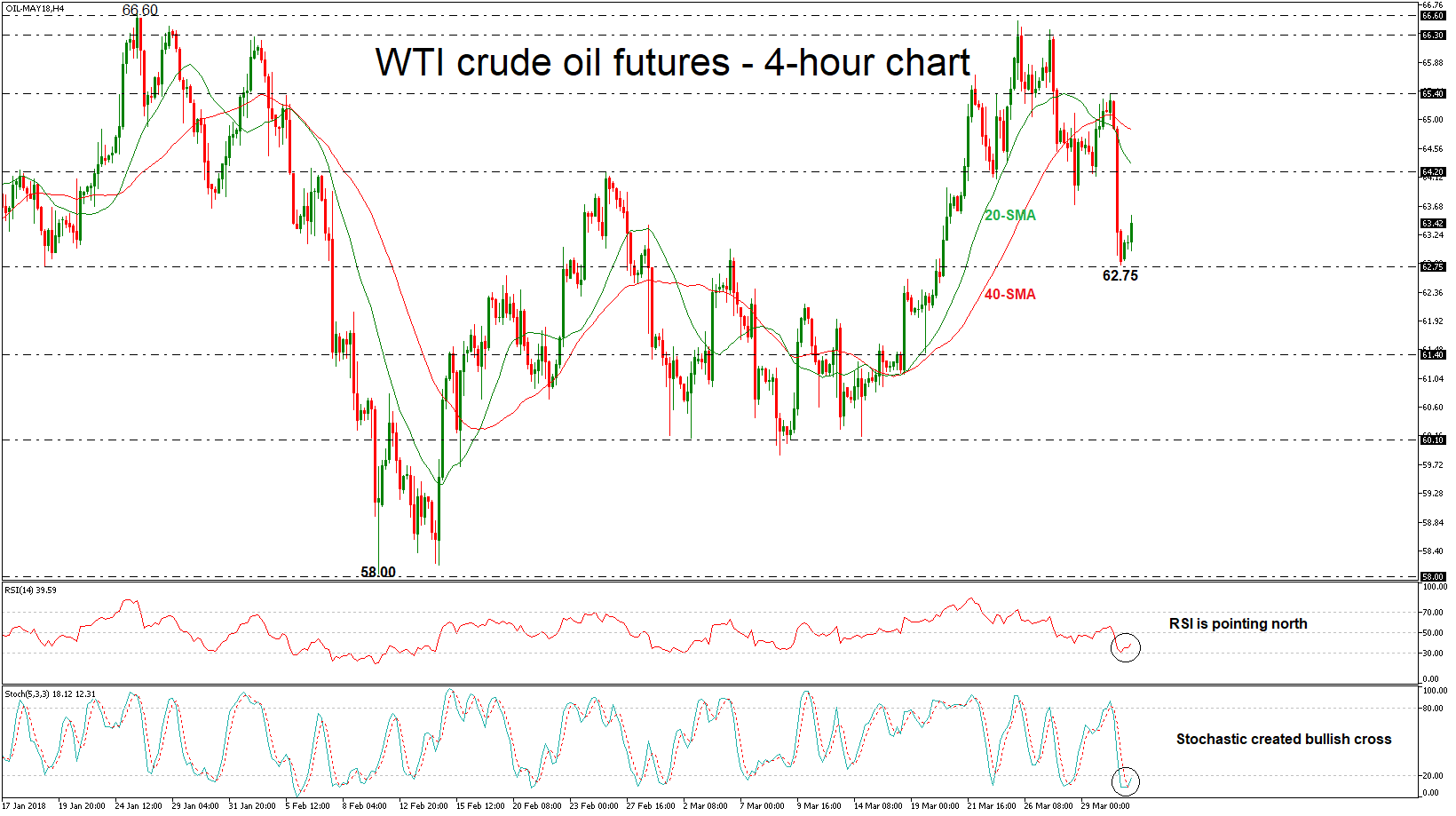

WTI Crude Oil Futures Hover Above Two-Week Low Of 62.75

WTI has reversed back down again and plummeted aggressively after finding resistance at the 65.40 level during yesterday’s session. The price recorded a new two-week low of 62.75, which holds near the 20-day simple moving average (SMA) and currently, is paring some losses.

After their deep fall, in the 4-hour chart, the momentum indicators are moving higher after hitting the oversold areas. The Relative Strength Index (RSI) is hovering below the 50-neutral level in the past few days but is sloping to the upside. The %K line of the stochastic oscillator has jumped above the %D line and attempted a bullish crossover, suggesting upside correction.

If prices continue to head higher, after the sharp sell-off, resistance could come at the 64.20 resistance barrier, which is standing slightly below the 20-SMA in the short-term. A jump above the aforementioned level and a move higher towards the 40-SMA would reinforce the near-term bullish view, that will open the way towards the 65.40 key level.

However, should a downside reversal take form again, immediate support will likely come from the two-week low. If this area is breached, it could increase downside pressure until the 61.40 obstacle, taken from the low on March 19

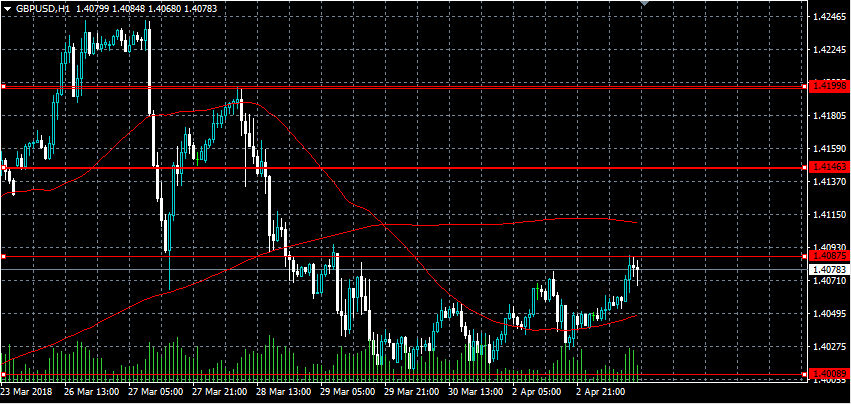

GBPUSD Challenging Key 1.4087 Resistance Level

The British pound has moved higher against the greenback during the European trading session, following a better than expected March Manufacturing PMI reading from the United Kingdom. The GBPUSD pair has so far tested the key 1.4087 level resistance level, and been rejected, although price-action currently remains close to this pivotal resistance level, at 1.4078. Sterling traders now look to the U.S session open, with the intraday bullish bias firmly intact while the pair trades above the 1.4048 level.

The GBPUSD pair is intraday bullish whilst trading above the 1.4048 level, key resistance is now located at the 1.4087 and 1.4146 levels.

If the GBPUSD pair declines below the 1.4048 level for a sustained period, sellers will likely test towards the 1.4008 and 1.3960 support levels.

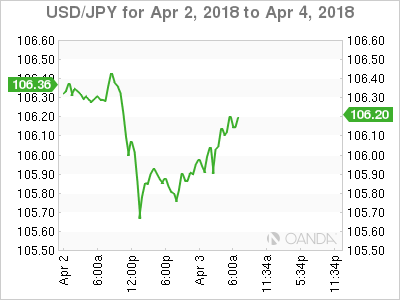

USDJPY Testing Demand Above 106.00 Level

The greenback has recovered above the 106.00 handle against the Japanese yen during the European trading session, reaching 106.20, as the U.S dollar index rebounds across the board. Despite risk-off trading sentiment spreading through financial markets on Tuesday, the USDJPY pair has remained well supported by dip buying demand. Moving into the U.S session, the direction of U.S equity markets and the U.S dollar index are likely to influence the pairs next intraday movement.

The USDJPY pair is bullish whilst holding above the 106.00 level, an intraday correction towards the 106.45 and 107.00 resistance levels remains possible.

Should price-action move back the key 106.00 level, USDJPY sellers will likely test towards the 105.64 and 105.50 support levels.

Euro Steady As German, Eurozone Manufacturing PMIs Within Expectations

EUR/USD continues to trade sideways this week. Currently, the pair is trading at 1.2310 up 0.07% on the day. After a quiet start to the week, there are a host of Eurozone indicators. German Retail Sales was unexpectedly soft, with a decline of 0.7%. This reading was well off the estimate of +0.7% and marked the fourth decline in five months. On the manufacturing front, German and eurozone manufacturing PMIs softened in March, although both indicators were within expectations and continued to point to expansion. There are no major US events on the schedule. On Wednesday, the eurozone releases CPI reports and the unemployment rate. The US will publish ADP payrolls and the ISM Non-Manufacturing PMI.

Britain and EU negotiators were all smiles in March, with the announcement that the two sides had reached a transition agreement on Brexit. The agreement will take effect at the end of March 2019, when Britain leaves the European Union. The transition phase will last until December 2020, and is meant to serve as a 'cushion' to allow businesses to adjust to Britain’s departure. Broadly speaking, EU rules will still apply to the UK, but Britain will no longer have a seat at the table with regards to EU decision-making. However, according to a report in the Times newspaper on Tuesday, EU regulators have warned UK banks operating on the Continent not to rely on the transition deal, and to prepare for a 'hard Brexit', in which the UK would simply depart the EU without any agreement. This position is in stark contrast to that of the Bank of England, which has embraced the transition agreement. The status of financial services in the post-Brexit era remains a key sticking point between the sides, and the stakes are very high, as Paris and Frankfurt are hoping to lure thousands of financial jobs away from the City of London.

The tariff battles have continued this week, with China firing the latest shot. On Monday, China responded to recent US tariffs, imposing its own duties on a range of US goods, including frozen pork and wines. This move is bound to escalate tensions between the two economic giants and has raised fears that a new global trade war could be underway. If the tit-for-tat measures continue, both the US and Chinese economies could suffer, which could lead to a global slowdown. Gold is sensitive to geopolitical crisis, as investors tend to snap up safe-haven assets such as gold during times of uncertainty. If tensions worsen between China and the US, gold prices could continue to move upwards.

Global Stocks Crumble On Risk Aversion, Pound Higher

Investors have entered the second trading quarter of 2018 on a mission to avoid riskier assets amid the escalating trade tensions between the U.S and China.

After global equities experienced their worst three months in more than two years, retaliatory tariffs announced by China resulted in stocks suffering their worst start to April since the great depression. Asian shares were depressed during early trade, as jitters about a U.S-China trade war weighed heavily on sentiment. In Europe, stocks moved lower thanks to the market caution and ongoing concerns about technology firms. With Wall Street experiencing losses so severe on Monday, that the S&P 500 closed below the 200-Day Moving Average, further losses could be on the cards this afternoon.

Now that China has fought back by imposing tariffs on 128 U.S imports worth $3 billion, investors are clearly on edge with markets questioning “what next”? The mounting sense of unease over the ongoing trade drama between the U.S and China is likely to promote risk aversion consequently punishing global stocks.

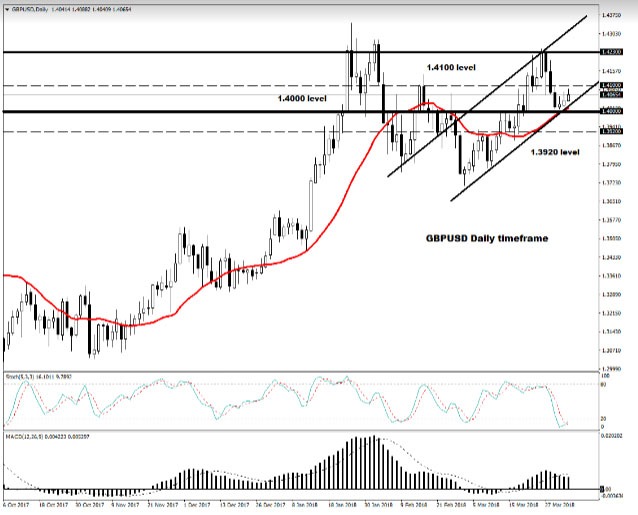

Sterling buoyed by UK manufacturing data

Sterling edged higher against the Dollar after UK manufacturing survey data for March exceeded market expectations.

The UK’s manufacturing sector activity reading rose to 55.1 in March, beating expectations of 54.7 and slightly higher than the 55.0 in February. Sterling is likely to remain somewhat supported by market expectations of the Bank of England, raising UK interest rates in May and potential Dollar weakness.

Taking a look at the technical picture, the GBPUSD has scope to venture higher, as long as bulls can defend the 1.4000 level. Prices are trading above the daily 20 SMA, while the MACD has crossed to the upside. A technical breakout above 1.4100 could encourage an inline higher towards 1.4140 and 1.4230, respectively. If bulls are unable to defend 1.4100, the GBPUSD is at risk of sinking back towards 1.3920.

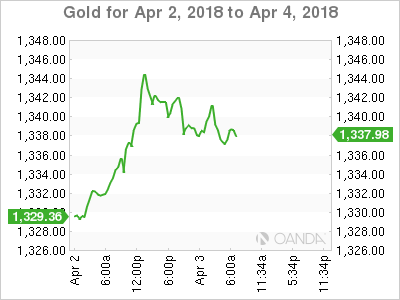

Commodity spotlight – Gold

Gold inched lower on Tuesday, as some investors locked in profits after the metal punched above the $1340 resistance level.

With escalating trade tensions between the U.S and China sparking risk aversion, punishing global equity markets and weakening the Dollar, Gold could remain heavily supported moving forward. Investors will be paying very close attention to the NFP report on Friday, which will play a leading role in where the yellow metal concludes this week. Prior to the NFP report, market uncertainty and overall caution is likely to inspire bulls to push the yellow metal higher. Taking a look at the technical picture, Gold has scope to venture higher towards $1360 if bulls are able to secure control above $1340. Alternatively, sustained weakness below $1340 could result in a decline back to $1324.

China’s First Renminbi Crude Oil Futures Unlikely Accelerates Currency Internationalization

On March 26, China launched its, and also the world’s, first renminbi-denominated crude oil futures. The debut appeared successful with 20M barrels of oil changed hands on average in each of the first two trading days. This represents 3% of combined WTI and Brent volumes on these days. The futures attracted both international commodity traders as well as China’s state-owned oil companies. While we agree that further liberalization of China’s financial markets would promote the use of its currency – renminbi, the lack of transparency of the currency’s pricing mechanism and the unpredictable government policies suggest that the road to renminibi internationalization remains a protracted one.

Response to Rising Hedging Needs

As the world’s largest oil importers, Chinese oil companies find it increasingly necessary to better manage their price exposure. As such, an instrument is needed for hedging against risks of oil price volatility. Chinese crude oil imports mainly concentrated on medium and heavy sour crudes, while the existing benchmarks, WTI (39.6 API gravity; 0.24% sulfur) and Brent (38.06 API gravity; 0.37% sulfur), are based on light and sweet crude oils. The mismatch has raised the need for a new instrument which is based on a basket of medium and heavy crudes. The newly launched contract, focusing on oil with higher sulfur content, is based on 7 deliverable crude grades (30-33 API gravity; 1.6-2.8% sulfur) from the Middle East (Dubai, Upper Zakum, Oman, Qatar Marine, Masila and Basra Light) and China(Shengli)

Moreover, the renminbi-denominated nature allows Chinese firm to manage their risks more effectively.

Provision of More Trading Vehicles to Domestic Investors

As Shanghai Futures Exchange seeks to increase variety of trading vehicles, the new crude futures should be appealing. Domestic investors have until now lacked opportunity to trade oil. Renminibi is neither freely convertible nor freely float. Meanwhile, the government has imposed various capital control measures so as to prevent excessive selloff of its currency. Such monetary policy environment has deprived domestic investors’ overseas investment opportunities. Let alone other costs and only consider the current trading price and lot size, the minimum investment for WTI and Brent crude futures is US$ 64 000 and US$ 68 000, respectively. Chinese investors would find it impossible to enter the markets as they are only allowed to transfer US$50 000 a year per person. The huge pool of domestic speculators is definitely lured to the first crude derivative in China.

Opening up its commodity markets, the government allows foreign investors to trade the futures directly from offshore, using US dollar or offshore renminbi (CNH) as collateral. Income taxes for foreign investor are also waived for the first three years. By allowing foreign investors to tap China’s commodity market for the first time, the government is encouraging the use of its currency. However, we do not agree with those who have regarded the move as a further step to renminbi liberation and for the currency to challenge US dollar’s status as the world’s reserve currency,

Despite the launch of the new futures, foreign access to Chinese financial assets remained limited. Moreover, Collateral made by foreign investors is kept in designated accounts, which, together with any capital gain, would be transferred back to foreign accounts. Another problem is renminbi. Although the government has implemented a number of reforms, currency is still neither freely convertible nor free-float. The pricing of the currency has lacked transparency as government policies are erratic and unpredictable. For instance, the mysterious “counter-cyclical factor” introduced in May 2017 for renminbi fixing was abruptly suspended on January 2018. Investors find it very difficult to gauge the movement of the currency. Despite China’s status as the world’s largest exporter and second largest importer, we doubt if any country would prefer currency of this nature to dominate its foreign exchange reserve.

References:

http://www.shfe.com.cn/content/2018-yyQH-en/index.html

https://www.theice.com/products/219/Brent-Crude-Futures

http://www.cmegroup.com/trading/energy/crude-oil/light-sweet-crude_contract_specifications.html

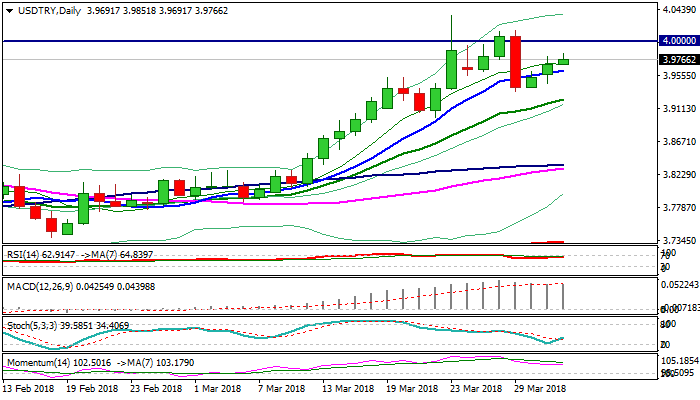

USDTRY Extends Recovery But Lower Inflation In Turkey Could Slow Bulls

The USDTRY holds in a steady recovery from 3.9338 (29 Mar low, posted after sharp fall) which extends into third straight day and retraced so far 61.8% of 4.0150/3.9338 dip.

Recovery rally returned above rising 10SMA (currently at 3.9622 and marking initial support) which was bullish signal, however, weakening momentum warns of possible recovery stall.

Inflation in Turkey surprisingly fell in March, report released today showed.

Annualized inflation was 10.23% in March, slightly below 10.26% previous month, marking the lowest level since July 2017, but still holding double-digit figure.

Marginally lower inflation could be limiting factor for fresh bulls which attempt at psychological 4.00 barrier and eye new all-time high at 4.0359, posted on 23 Mar.

The price may remain within initial range between 4.0150 and 3.9338, before establishing in fresh direction.

Focus turns towards Turkey’s current account data, due on 11 Apr and CBRT policy meeting on 25 Apr, which could provide stronger direction signals.

Res: 3.9851, 4.0000, 4.0150, 4.0359

Sup: 3.9691, 3.9622, 3.9449, 3.9390

Dollar At A Crossroads On Trade Worries

Regional euro bourses have reopened after the long weekend under pressure, but the declines, thus far, are muted when compared to yesterday’s U.S equity selloff, while in Asia, stocks were able to pare some of their initial drop. The U.S dollar is again under pressure vs. its G10 counterparts, while Treasury prices edge lower.

The key concerns among investors are trade conflicts between the U.S and other countries and higher interest rates in the U.S. Q1 has been the worst three-months for global equities in more than 24-months and Q2 has started on the back foot in risk off mode as the market prepares for earnings season. Consensus anticipates a strong showing, but the market will be watchful for any more signs of a slowdown in the global expansion.

1. Stocks mixed results

On Monday, major U.S indices fell -2%, with early pressure likely exacerbated by the holiday trading schedule and heightened by further trade war worries, though markets ended well off the day’s lows.

The S&P 500 closed below its 200-day moving average for first time since mid-2016 amid pressure on tech names. The VIX rose above 25 for the first time in 10-days.

Overnight in Japan, stocks fell, led by tech firms and makers of electronic components. The Nikkei ended -0.5% lower, while the broader Topix dropped -0.3%.

Down-under, Aussie shares ended slightly lower on Tuesday, as gains in material stocks and a surge in energy names countered losses in financial and industrial stocks. The S&P/ASX 200 index closed down -0.13%, marking its third consecutive day of losses. In S. Korea, the Kospi index skidded about -1%, pressured mostly by Samsung Electronics being down more than -1%.

In Hong Kong, stocks reversed earlier losses to edge higher overnight, led by gains in consumer goods makers, although caution prevailed amid escalating trade tensions after Beijing unveiled retaliatory trade measures against the U.S. At close of trade, the Hang Seng index was up +0.3%, while the Hang Seng China Enterprises index closed up +1.2%.

In China, stocks ended lower on Tuesday, amid resurgent trade war fears after Beijing unveiled retaliatory trade measures against the U.S. At the close, the Shanghai Composite index was down -0.8%, while the blue-chip CSI300 index declined -0.6%.

In Europe, regional bourses trade lower across the board following closures for Easter Holidays, after a sharp sell off stateside yesterday. No surprise to see technology names are under pressure in the region, mirroring what happened on Wall St.

U.S stocks are set to open in the black (+0.4%).

Indices: Stoxx600 -1.0% at 367.3, FTSE -0.8% at 7002, DAX -1.4% at 11925, CAC-40 -0.9% at 5122, IBEX-35 -0.9% at 9510, FTSE MIB -0.7% at 22254, SMI -1.3% at 8627, S&P 500 Futures +0.4%

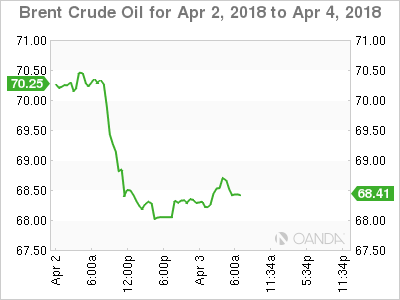

2. Oil inches up, but rising Russian output still weighs, gold higher

Oil prices have inched higher overnight as rising Russian output and expectations of a reduction in Saudi Arabian crude prices were offset by a potential slowdown in U.S production.

Brent crude futures are at +$67.84 per barrel, up +20c, or +0.3%, after it fell more than -2% on Monday. U.S WTI crude futures are at +$63.2 a barrel, up +18c, or +0.3% from yesterday’s close.

For ‘long’ crude positions, they are worried that top exporter Saudi Arabia will cut prices for all crude grades it sells to Asia in May and are also concerned about Russia’s production numbers – Russia pumped +10.97m bpd of crude in March, up from +10.95m bpd in February – an 11-month high.

However, supporting the crude ‘bulls’ is last week’s Baker Hughes data which showed that U.S drillers cut -7 oilrigs in the week to March 29, bringing the total down to +797, the first decline in three-weeks.

The market will take its cues from this weeks inventory reports. Weekly official EIA data, which includes production figures, is due to be published on Wednesday.

Ahead of the U.S open, gold prices rose slightly overnight after a more than +1% gain in the previous session, as mounting global trade tensions fuelled demand for the safe-haven metal. Spot gold is up +0.1% at +$1,341.68 per ounce.

Note: The ‘yellow’ metal climbed +1.3% on Easter Monday, its biggest one-day percentage rise in a week.

3. Sovereign yields trade atop of two-week lows

As widely expected, the Reserve Bank of Australia (RBA) ended yesterday’s April policy meeting with the benchmark rate unchanged at +1.5%, where it has been for the last 20-months.

Governor Lowe expects inflation to 'remain low for some time,' reflecting 'low growth in labor costs and strong competition in retailing.' 'Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual.'

The Governor has repeatedly emphasized that the central bank sees no strong case for a near term hike in rates, exhibiting policy patience.

In Europe, sovereign bonds trade barely changed early in the first trading day of Q2. The 10-year Bund yield is trading flat at +0.49%, while 10-year Spanish, Italian and Portuguese bond yields are trading about +1 bps higher. There is no supply scheduled in the eurozone today, with the week’s first bond auction due tomorrow when Germany taps five-year debt, followed by Spain and France on Thursday.

Note: Consensus expects the eurozone bond markets may run into some profit taking from short-term investors after their strong performance in the last 10-days.

Elsewhere, the yield on 10-year U.S Treasuries has gained +1 bps to +2.74%, the biggest advance in more than a week, while in the U.K, the 10-year Gilt yield has decreased -1 bps to +1.35%, reaching the lowest in more than 10-weeks on its seventh straight decline.

4. Dollar at a crossroads

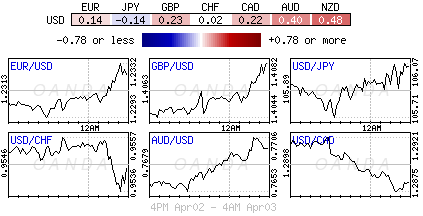

As we officially start Q2, the market begins to debate the U.S dollars direction. Will it trend or continue to move sideways in the quarter? The April-May period historical is one of 'extending price moves for forex.' The techies would very much welcome a change and are expecting a new fresh trend to materialize over the coming weeks.

The EUR/USD (€1.2311) has been locked in a +350 pip range for most of Q1. Momentum is expected to build whenever there is a real break of either €1.2100 or €1.2500. Until then, the majority will play the four-handle range.

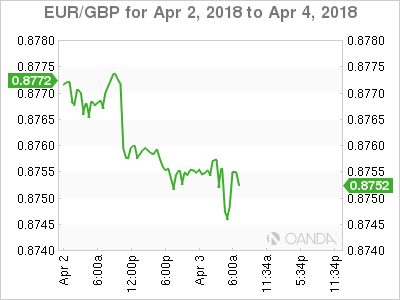

The pound (£1.4069) did not react much to this morning’s U.K manufacturing PMI for March (see below), which came in at 55.1, compared with 55.0 in February, above forecasts for 54.4. GBP/USD last traded up +0.1% on the day at £1.4069, little changed from before the release. EUR/GBP is also little changed at €0.8753, down -0.1% on the day. The pound has also been unfazed by reports that the ECB is said to have told U.K banks to prepare for a scenario where there was 'no deal' leading to a hard Brexit with no transition.

Finally, USD/JPY (¥106.18) briefly dipped below the psychological ¥106 level as BoJ’s Governor Kuroda testified in parliament that the BoJ was internally discussing an exit, and the way forward to depend on prices, economy and markets.

5. U.K manufacturing PMI muted

Data this morning showed that the U.K manufacturing sector maintained a steady pace of expansion during March. Output growth picked up, although this was offset by slower increases in both new orders and employment.

The seasonally adjusted IHS Markit/CIPS Purchasing Managers’ Index posted 55.1 in March, little-changed from 55.0 in February.

Note: The average reading over Q1 (55.1) was the weakest in a year, suggesting that the underlying pace of expansion has been generally slower since the start 2018.

Digging deeper, on the price front, rates of inflation in input costs and output charges remained elevated despite easing slightly since February.

Manufacturing production rose for the twentieth successive month in March. The rate of expansion accelerated to the sharpest in the year-so-far, despite a moderation in growth of incoming new orders.

PMI Data Continues To Move Off From Cycle Highs

Notes/Observations

- Major European PMI Manufacturing continue to move off recent cycle highs (Beats: UK, France, Poland, Hungary; Misses: Germany, Italy, Netherlands, Norway, Czech; in-line: Euro Zone)

- All eyes on the US March labor market report due on Friday, with wages in focus

Asia:

- RBA left its Cash Rate Target unchanged at 1.50% (as expected). Reiterated view that low level of interest rates was supporting the domestic economy. Inflation remained low. Reiterated that Australian dollar remained within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

Europe:

- EU warned UK banks not to rely on Brexit transition deal and urged to implement their 'hard' Brexit contingency plans. ECB said to have told banks to prepare for a scenario where there was no deal, leading to a hard Brexit with no transition

Americas:

- Mexico Economy Min Guajardo saw the possibility to send positive signals on NAFTA among heads of governments at upcoming Americas summit in Peru

- President Trump said to be pushing for a preliminary NAFTA deal at a summit in Peru next month. Trump to host cabinet ministers in Washington to try and get a breakthrough

- White House Trade Advisor Navarro: Did not believe US and China will go into an 'action-response' escalation of trade differences; China needed to think about its response. Needed to be hopeful about NAFTA negotiations; wanted to get it done before Mexico election (July 1st)

Economic Data:

- (IE) Ireland Mar Manufacturing PMI: 54.1 v 56.2 prior (58th month of expansion)

- (IN) India Mar Manufacturing PMI: 51.0 v 52.1 prior (8th month of expansion but lowest since March 2017)

- (DE) Germany Feb Retail Sales M/M: -0.7% v +0.7%e; Y/Y: 1.3% v 2.4%e

- (AU) Australia Mar Commodity Index (AUD): 113.2 v 112.1 prior; Commodity Index SDR Y/Y -2.1% v -2.8% prior

- (SE) Sweden Mar Manufacturing PMI: 55.9 v 59.9 prior

- (CZ) Czech Q4 Final GDP Q/Q: 0.8% v 0.5%e; Y/Y: 5.5% v 5.2%e

- (ES) Spain Mar Net Unemployment M/M: -47.7K v -47.5Ke

- (NL) Netherlands Mar Manufacturing PMI: 61.5 v 62.2e (55th month of expansion)

- (NO) Norway Mar Manufacturing PMI: 55.0 v 56.6e

- (PL) Poland Mar Manufacturing PMI: 53.7 v 53.0e (40th month of expansion)

- (HU) Hungary Mar Manufacturing PMI: 57.0 v 57.2 prior (28th month of expansion)

- (TR) Turkey Mar CPI M/M: 1.0% v 0.9%e; Y/Y: 10.2% v 10.0%e, CPI Core Index Y/Y: 11.4% v 11.9% prior

- (TR) Turkey Mar PPI M/M: 1.5% v 2.7% prior; Y/Y: 14.3% v 13.7% prior

- (ES) Spain Mar Manufacturing PMI: 54.8 v 54.7e (53rd month of expansion)

- (CH) Swiss Feb Real Retail Sales Y/Y: -0.2% v -0.4% prior

- (CH) Swiss Mar Manufacturing PMI: 60.3 v 65.5 prior

- (CZ) Czech Mar Manufacturing PMI: 57.3 v 57.6e (20th month of expansion)

- (IT) Italy Mar Manufacturing PMI: 55.1 v 55.5e (19th month of expansion)

- (FR) France Mar Final Manufacturing PMI: 53.7 v 53.6e (confirmed its 18th month of expansion but lowest since March 2017)

- (DE) Germany Mar Final Manufacturing PMI: 58.2 v 58.4e (confirmed its 39th month of expansion but lowest since July)

- (EU) Euro Zone Mar Final Manufacturing PMI: 56.6 v 56.6e (confirmed its 56th month of expansion)

- (CH) SNB Total Sight Deposits for Week Ended Mar 30th (CHF): 575.4B v 576.0B prior

- (BR) Brazil Mar FIPE CPI (Sao Paulo): 0.0% v 0.0%e

- (UK) Mar Manufacturing PMI: 55.1 v 54.7e (20th month of expansion)

- (HK) Hong Kong Feb Retail Sales Value Y/Y: 29.8% v 7.5%e; Retail Sales Volume Y/Y: 28.2% v 5.0%e

- (ZA) South Africa Mar Manufacturing PMI: 46.9 v 50.8 prior

- (DK) Denmark Mar PMI Survey: 62.9 v 70.0 prior

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro) sold total €4.5B vs. €4.0-5.0B indicated range in 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -1.0% at 367.3, FTSE -0.8% at 7002, DAX -1.4% at 11925, CAC-40 -0.9% at 5122, IBEX-35 -0.9% at 9510, FTSE MIB -0.7% at 22254, SMI -1.3% at 8627, S&P 500 Futures +0.4%]

Market Focal Points/Key Themes:

- European Indices trade lower across the board following closures for Easter Holidays, after a sharp sell off in Wallstreet overnight. Following weakness in the Nasdaq, Tech names are under pressure in Europe with Dialog Semi, Infineon and STM Micro among the names trading lower. On the earnings front Bossard outperforms after upbeat Q1 comments, while Groupe Gorge trades lower after final FY results and outlook. Elsewhere Air Partner trades over 15% lower after a year end update, warning on uncollected receivables with Flybe trading higher after a Q4 update. Looking ahead notable earners include International Speedway and Beyond Spring.

Movers

- Consumer Discretionary [- Air Partner [AIR.UK] -17% (Year end update), Hornby [HRN.UK] -6% (Trading update), Flybe [FLYB.UK] +2.6% (Trading update) ]

- Industrials [Bossard [BOSN.CH] +5.7% (Q1 update), Groupe Gorge [GOE.FR] -4.3% (Earnings) ]

- Healthcare [Astrazeneca [AZN.UK] -0.9% (Reports anonymously paying to promote drugs),

- Technology [Dialog Semi [DLG.DE] -1%, ST Micro [STM.FR] -2.9%, Infineon [IFX.DE] -2.4% (Tech sector selloff) ]

Equities

Speakers

- Greece PM Tsipras: To hold elections in autumn 2019

- Spain Budget Ministry plans 2018 gross debt issuance of €215.3B and net issuance at €40B

- BoJ Gov Kuroda testified in Parliament that the BOJ was internally discussing an exit with the manner to depend on prices, economy and markets. BOJ communicate well with market when needed. He stressed that it was too early to discuss exit strategy as remained quite distant from inflation target. Politics would not prevent BOJ from taking needed policy.

- UAE Oil Min Mazrouei: Global economy is benefiting from OPEC/Non-Opec production cut agreement. Not concerned about a trade war affecting oil

- Qatar Oil Min Al Sada (OPEC President): Russia has been a great partner on production cuts

Currencies

- The start of Q2 brought the same trading range for the USD. Dealers debated whether the greenback will trend or continue moving sideways in the quarter. The April-May period historical is one of extending price moves in FX. All the moving parts on the global trade front seems encouraging that a fresh trend will emerge in coming weeks. The EUR/USD has been locked in a 400 pip range for the bulk of 2018 thus far. Momentum likely to be fired up on the break of either 1.21 or 1.25

- The GBP currency was unfazed by reports the ECB said to have told banks to prepare for a scenario where there was no deal leading to a hard Brexit with no transition. GBP/USD was higher by 0.2% at 1.4080 area. Slightly better UK PMI data helping cable hold onto session gains

- USD/JPY briefly dipped below the 106 level as BOJ Gov Kuroda testified in Parliament that the BOJ was internally discussing an exit and the way forward to depend on prices, economy and markets (**Note he began his testimony that it was too early to discuss exit strategy as was still distant from inflation target). The pair recovered as the session progressed

Fixed Income

- Bund Futures trade 23 ticks lower at 159.14 as major European manufacturing pmi data comes in mixed. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 122.86 down 4 ticks tentatively respecting the 123 handle. Support continues stands at 121.25 then 120.85, with upside resistance at 123.35 then 123.85.

- Tuesday's liquidity report showed Thursday's excess liquidity fell to €1.758T from €1.789T prior. Use of the marginal lending facility increased from €131M to €189M.

- Corporate issuance saw 1 issuer raise $0.5B in the primary market

Looking Ahead

- (BE) Belgium Dec Unemployment Rate: No est v 6.8% prior

- (US) Mar Wards Total & Domestic Vehicle Sales

- (IT) Italy Mar Budget Balance: No est v -€6.3B prior

- (AR) Argentina Mar Government Tax Revenue (ARS): No est v 235.6B prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (EU) ECB allotment in 7-day Main Financing Tender (prior €2.4B with 33 bids recd)

- 05:30 (BE) Belgium Debt Agency (BDA) to sell 3-month Bills

- 05:30 (NL) Netherlands Debt Agency (DSTA) to sell €1.0-2.0B in 6-month bills

- 05:30 (ZA) South Africa to sell total ZAR2.3B in 2032, 2035 and 2041 bonds

- 06:30 (EU) ESM to sell €2.0B in 3-month Bills - 06:45 (US) Daily Libor Fixing

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (CZ) Czech Mar Budget Balance (CZK): No est v 25.8B prior

- 08:00 (BR) Brazil Feb Industrial Production M/M: +0.6%e v -2.4% prior; Y/Y: 3.9%e v 5.7% prior

- 08:00 (CL) Chile Feb Retail Sales Y/Y: 5.3%e v 3.8% prior, Commercial Activity Y/Y: No est v 7.3% prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:55 (US) Weekly Redbook Sales

- 08:55 (FR) France Debt Agency (AFT) to sell combined €4.6-5.8B in 3-month, 6-month and 12-month BTF Bills

- 09:30 (NZ) Fonterra Global Dairy Trade Auction: Dairy Trade price index: No est v -1.2% prior

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 10:00 (DK) Denmark Mar Foreign Reserves (DKK): No est v 467B prior

- 11:00 (CO) Colombia Feb Exports: $3.1Be v $3.2B prior

- 11:30 (US) Treasury to sell 4-Week Bills

- 12:00 (IT) Italy Mar New Car Registrations Y/Y: No est v -1.4% prior

- 16:30 (US) Weekly API Oil Inventories

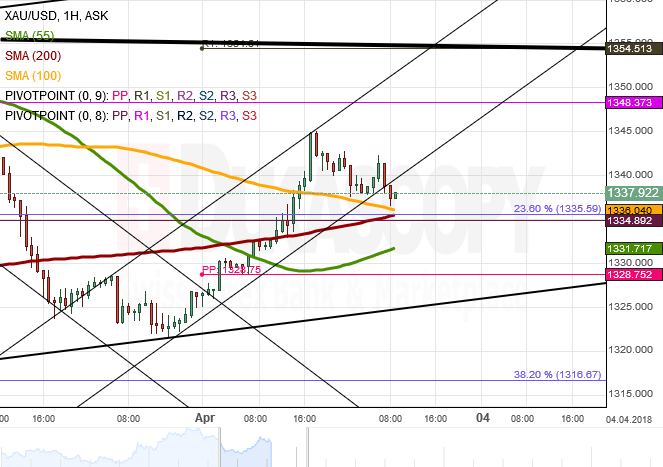

XAU/USD Analysis: Reaches1,345.00

Strong upside risks have dominated the given pair since late Thursday.

It reversed from the 1,322.15 area, thus providing another confirmation of the bottom boundary of a four-week channel, and began its movement towards the 1.345.00 mark. As apparent on the chart, Gold dashed through several significant resistance levels, including the 100– and 200-hour SMAs and the 23.60% Fibo at 1,335.00.

The base scenario favours the pair continuing to trade in line with the medium-term pattern and re-testing its March high of 1,355.00 where the senior channel and the monthly R1 are located.

Meanwhile, it is unlikely that the strong support at 1,335.00 is breached today, especially when the US Dollar is weakened by global trade tensions.