Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2857; (P) 1.2891; (R1) 1.2915; More...

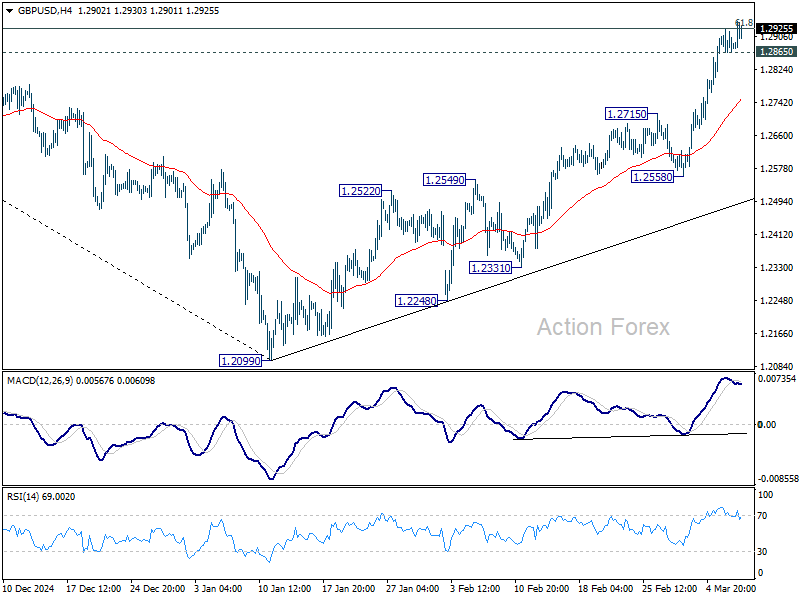

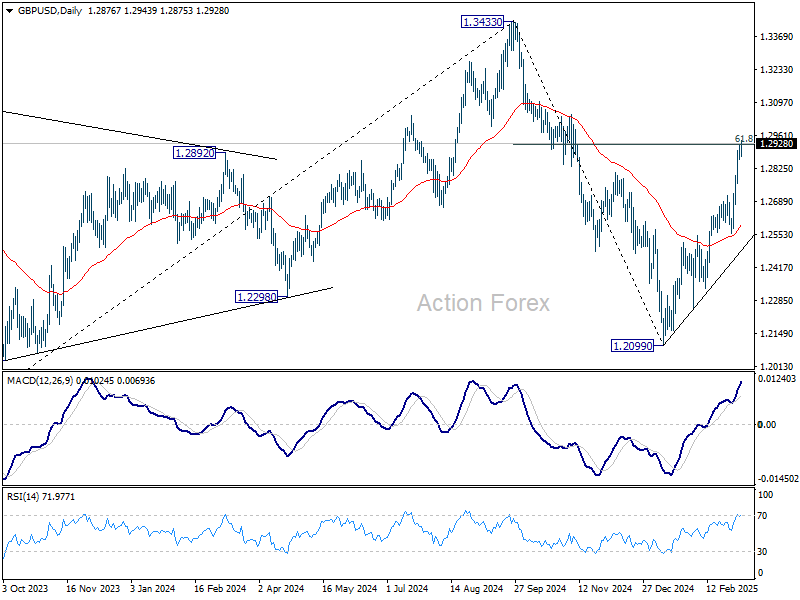

GBP/USD's rally resumed after brief retreat and intraday bias is back on the upside. Sustained break of 61.8% retracement of 1.3433 to 1.2099 at 1.2923 will pave the way back to 1.3433 high. On the downside, below 1.2865 minor support will turn intraday bias neutral again and bring consolidations.

In the bigger picture, fall from 1.3433 (2024 high) should have completed at 1.2099 as a corrective move. Up trend from 1.3051 (2022 low) is still in progress but it's too early to say that it's resuming. Corrective pattern from 1.3433 could extend with one more down leg. But after all, eventual upside breakout is expected at a later stage.

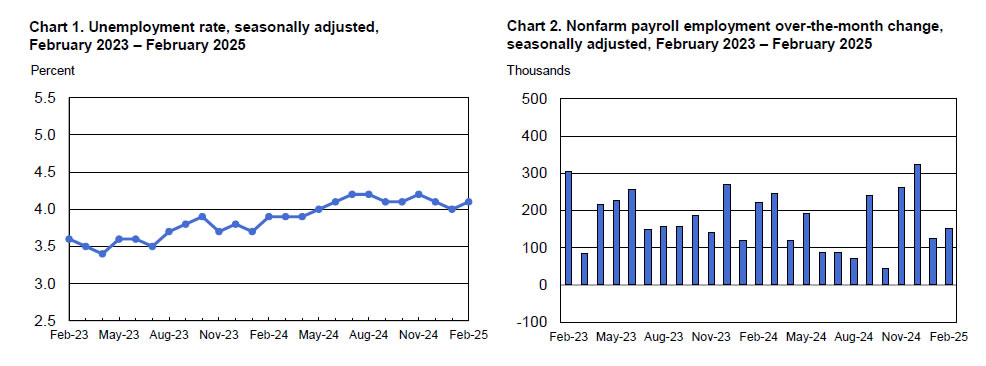

US: Payroll Growth Turns Higher in February, While Unemployment Rate Ticks Up to a Still Low 4.1%

The U.S. economy added 151k jobs in February, only a touch below the consensus forecast of 160k. Payroll figures for December 2024 were revised higher by 16k (to 323k), while January was revised lower by 18k (to 125k), resulting in a total net revision of -2k over the two prior months.

Private payrolls rose 140k – up from January's 81k – with the largest gains seen in private health care & social assistance (+63k), financial services (+21k), construction (+19k) and transportation & warehousing (+18k). Leisure & hospitality (-16k) and retail trade (-6k) both lost jobs on the month. Meanwhile, the public sector added a more modest 11k jobs in February – down from the 38k averaged over the prior twelve-months – but the gain was entirely due to a further uptick in state & local hiring. Employment at the federal level was lower by 10k.

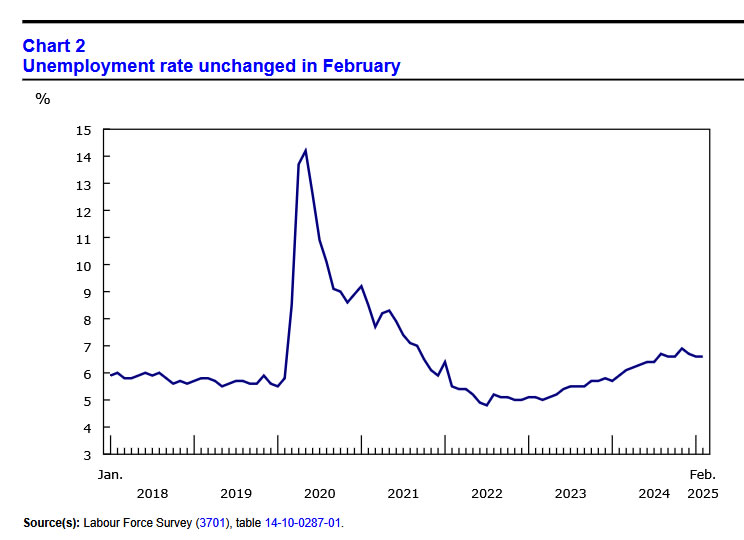

In the household survey, civilian employment (-588k) plunged by more than the labor force (-385k), pushing the unemployment rate up to a still low 4.1% (from 4.0% in January). The labor force participation rate dropped 0.2 percentage points to 62.4% or the lowest reading since January 2023.

Average hourly earnings (AHE) rose 0.3% month-on-month (m/m), a deceleration from January's downwardly revised gain of 0.4% m/m (previously 0.5% m/m). On a twelve-month basis, AHE held steady at 4.0%, while the three-month annualized pace dipped to 3.6% – signaling a further easing in wage pressures in the months ahead. Aggregate weekly hours rose 0.1% m/m, after having declined in each of the two prior months.

Key Implications

Payroll growth turned modestly higher in February, following a softer reading in January, which was likely hindered by inclement weather and the California wildfires. Over the last three months, hiring activity has remained solid – averaging 200k jobs per-month. However, job growth is likely to soften over the coming months, as federal layoffs related to DOGE continue to mount and ongoing trade policy uncertainty helps to weigh on near-term hiring intentions.

Financial markets have become increasingly concerned about slowing growth prospects in recent weeks, with fed futures now fully pricing for three 25bps rate cuts by year-end. However, the Fed is unlikely to be swayed by the recent market volatility, particularly amid a still healthy labor market and potential policy changes that could further add to still elevated inflationary pressures. More evidence of cooling inflation or a sudden U-turn in the labor market are likely a prerequisite for the next rate cut, something which Fed Chair Powell is likely to emphasize in his speech this afternoon at 12:30 PM ET.

Canada’s Jobs Market Gets Buried in Snow in February

The Canadian labour market came back down to earth in February, adding just 1.1k positions, compared to a gain of 76k in January. Full-time positions declined (-19.7k), offset by gains in part-time (+20.8k).

The unemployment rate held at 6.6%, as the labour force contracted for the first time in seven months. Easing population flows were the driver here, following the implementation of the federal government's new non-permanent resident policy.

Employment by sector diverged, with wholesale and retail trade (+51k) and finance/insurance/real estate (+16k) making gains. However, declines were seen in professional, scientific and technical services (-33k) and transportation and warehousing (-23k).

Lastly, total hours worked cratered by 1.3% month-on-month, as winter storms resulted in lost work for thousands of employees. Meanwhile wages were up 3.8% year-on-year (from 3.5% in January).

Key Implications

The job market couldn't keep up its feverish pace over the last few months. Winter storms were likely the culprit, but deteriorating hiring sentiment given heighten policy/trade uncertainty may have also started to bleed into the data. One month doesn't make a trend, but Canadians should be closely watching the labour market for signs of weakness in the months ahead. Luckily, the Canadian labour market came into the current tariff crisis on solid footing, which is important given the significant headwinds the economy is facing.

The Bank of Canada is set to meet next week, and markets are solidifying around a 25 bp cut. We have been arguing that it is prudent for the central bank to keep cutting as insurance against the downside risks brought on by tariffs. Our scenario analysis embeds significant risk of recession should President Trump keep holding tariffs over our heads. And even if delays keep happening, the uncertainty will weigh on business and consumer confidence, diminishing our previously rosy outlook for the economy.

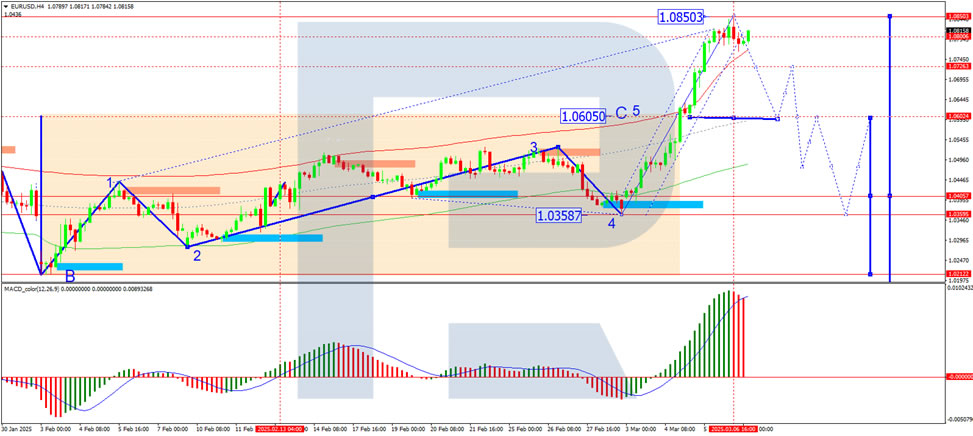

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0749; (P) 1.0801; (R1) 1.0837; More...

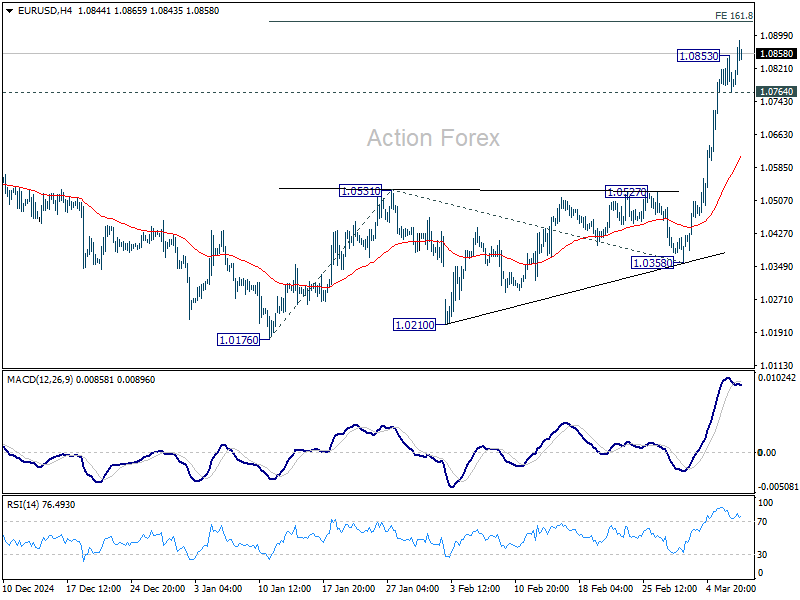

EUR/USD's rally from 1.0176 resumed after brief retreat, and intraday bias is back on the upside for 161.8% projection of 1.0176 to 1.0531 from 1.0358 at 1.0932 next. On the downside, below 1.0764 minor support will turn bias neutral and bring consolidations. But downside of retreat should be contained above 55 4H EMA (now at 1.0613) to bring another rally.

In the bigger picture, the strong break of 55 W EMA (now at 1.0668) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. That came after drawing support from 0.9534 (2022 low) to 1.1274 at 1.0199. Rise from 0.9534 is still intact, and might be ready to resume through 1.1274. This will now be the favored case as long as 1.0531 resistance turned support holds.

Muted Market Response to NFP, Euro Holds Strong While Loonie Struggles

The much-anticipated U.S. non-farm payrolls report came and went without much impact to the markets. With job growth largely in line with forecasts, the data signaled a stable labor market and the balanced outcome offers little guidance to Fed policymakers, who will continue weighing inflation trends, fiscal uncertainties, and global trade risks before committing to any policy shift. Investors, for their part, appear content to sit on the sidelines until more definitive signals emerge, resulting in subdued market reactions.

In contrast, Canadian dollar faltered after domestic employment data revealed a near standstill in job growth. Despite a short-lived uplift from fresh tariff exemptions, Loonie found itself on the back foot again, as stagnant employment reignited concerns over economic momentum. Whether the currency will face further downward pressure in the final trading hours of the week may depend heavily on broader risk sentiment, which has already pushed Australian and New Zealand Dollars lower.

Meanwhile, European majors are holding their ground, with Euro on track to end the week as the best performer. Sterling and Swiss Franc also remain well-supported, benefiting from the rally tied to Europe’s sweeping fiscal and defence initiatives.

In Europe, at the time of writing, FTSE is down -0.25%. DAX is down -1.79%. CAC is down -1.19%. UK 10-year yield is down -0.053 at 4.569. Germany 10-year yield is down -0.046 at 2.789. Earlier in Asia, Nikkei fell -2.17%. Hong Kong HSI fell -0.57%. China Shanghai SSE fell -0.25%. Singapore Strait Times fell -0.07%. Japan 10-year JGB yield rose 0.012 to 1.524.

US NFP rises 151k in Feb, slightly below expectations

US non-farm payroll employment increased by 151k in February, just slightly below expectations of 156k, and broadly in line with the 12-month average of 168k.

Unemployment rate edged up from 4.0% to 4.1%. Unemployment rate has remained in a narrow range of 4.0% to 4.2% since May 2024. Labor force participation rate slipped from 62.6% to 62.4%.

Average hourly earnings rose 0.3% mom, in line with forecasts, while the average workweek remained unchanged at 34.1 hours.

Canada's job growth stalls, unemployment rate steady at 6.6%

Canada's labor market was stagnant in February, with employment rising by just 1.1k, falling far short of the expected 17.8k increase.

Unemployment rate held steady at 6.6%, better than expectation of 6.7%, while the labor force participation rate dropped from 65.5% to 65.3%, marking its first decline since September 2024. A notable contraction was seen in total hours worked, which fell by -1.3% mom.

Despite the weak employment figures, wage growth accelerated, with average hourly wages rising 3.8% yoy, up from January's 3.5% gain.

China’s exports rise 2.3% yoy, imports fall -8.4% yoy

China’s exports rose just 2.3% yoy to USD 539.9B in the January–February period, coming in below forecasts of 5.0% yoy and down sharply from December’s 10.7% yoy.

Meanwhile, imports sank -8.4% yoy to USD 369.4B, missing expectations of 1.0% yoy growth and marking a noticeable drop from December’s 1.0% yoy.

As a result, trade balance resulted in USD 170.5B surplus exceeding projections of USD 147.5B.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0749; (P) 1.0801; (R1) 1.0837; More...

EUR/USD's rally from 1.0176 resumed after brief retreat, and intraday bias is back on the upside for 161.8% projection of 1.0176 to 1.0531 from 1.0358 at 1.0932 next. On the downside, below 1.0764 minor support will turn bias neutral and bring consolidations. But downside of retreat should be contained above 55 4H EMA (now at 1.0613) to bring another rally.

In the bigger picture, the strong break of 55 W EMA (now at 1.0668) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. That came after drawing support from 0.9534 (2022 low) to 1.1274 at 1.0199. Rise from 0.9534 is still intact, and might be ready to resume through 1.1274. This will now be the favored case as long as 1.0531 resistance turned support holds.

Canada’s job growth stalls, unemployment rate steady at 6.6%

Canada's labor market was stagnant in February, with employment rising by just 1.1k, falling far short of the expected 17.8k increase.

Unemployment rate held steady at 6.6%, better than expectation of 6.7%, while the labor force participation rate dropped from 65.5% to 65.3%, marking its first decline since September 2024. A notable contraction was seen in total hours worked, which fell by -1.3% mom.

Despite the weak employment figures, wage growth accelerated, with average hourly wages rising 3.8% yoy, up from January's 3.5% gain.

US NFP rises 151k in Feb, slightly below expectations

US non-farm payroll employment increased by 151k in February, just slightly below expectations of 156k, and broadly in line with the 12-month average of 168k.

Unemployment rate edged up from 4.0% to 4.1%. Unemployment rate has remained in a narrow range of 4.0% to 4.2% since May 2024. Labor force participation rate slipped from 62.6% to 62.4%.

Average hourly earnings rose 0.3% mom, in line with forecasts, while the average workweek remained unchanged at 34.1 hours.

Yen Extends Gains, Markets Eye US Nonfarm Payrolls

- Japanese yen extends rally for a third consecutive day

- BoJ’s Uchida says rate hikes still on the table despite tariff concerns

- US nonfarm payrolls expected to edge slightly

The Japanese yen has extended its gains on Friday. In the European session, USD/JPY is trading at 147.79, down 0.13% on the day.

It was a light calendar in Japan this week but that didn’t stop the yen from taking advantage of a broadly weaker US dollar. The yen has posted gains of 1.9% against the US dollar this week and strengthened as much as 147.19 to the dollar, its best level since Sep. 2024.

Will US tariffs target Japan?

Central bankers are watching nervously as US President Donald Trump has escalated trade tensions by imposing tariffs on China and a host of other countries. The US is yet to target Japan but Trump has complained about nations that have a trade surplus with the US, which include Japan. This means that Japan is at risk for US tariffs, which would hurt Japan’s economy and likely boost inflation.

This turbulent backdrop could complicate the Bank of Japan’s plans to continue raising interest rates. Deputy-Governor Shinichi Uchida appeared to dispel these concerns in a speech on Wednesday. Uchida sounded upbeat about the economy and said that rate hikes would continue if the economy and inflation evolved according to the BoJ’s projections.

US nonfarm payrolls expected to rise slightly

The market will be keeping a close eye on today’s US nonfarm payrolls. The labor market has been cooling down gradually, which is music to the ears of the Federal Reserve as it looks to guide the US economy to soft landing. The market estimate for February stands at 160 thousand, compared to 143 thousand in January. Wage growth is expected to rise 0.3% m/m in February, down from 0.5% in January. Annualized wage growth is expected to remain unchanged at 4.1%.

Only a few months ago, the market was expecting a series of rate cuts in 2025 from the Fed, but sticky inflation and solid economic growth have changed the rate outlook dramatically. The Fed is widely expected to hold rates at the March 19 meeting and there is a good chance that we won’t see any further rate cuts this year. The Fed’s rate path will largely depend on inflation and the strength of the labor market.

USD/JPY Technical

- 147.09 and 146.19 are providing support

- 148.21 and 149.11 are the next resistance lines

US, Canada Release Job Numbers – Will Canadian Dollar’s Rally Continue?

The Canadian dollar is on a three-day winning streak, gaining 1.2% during that time. USD/CAD is trading quietly at 1.4316 in the European session, up 0.14% on the day. We could see volatility from the pair later today, as both Canada and the US releases employment reports.

Canada’s job growth expected to drop sharply

Canada’s economy remains weak but the labor market has been surprisingly resilient. The economy added 76 thousand jobs in January and 90.9 thousand a month earlier. Those rosy numbers are unlikely to be repeated for February, with a market estimate of just 20 thousand. The unemployment rate has been creeping lower but is expected to edge up to 6.7% from 6.6%.

The escalation in trade tensions between Canada and the US is casting a dark cloud over the economic outlook. The US has imposed tariffs on all goods imported from Canada but announced a 30-day delay on all automobiles covered by the North American free trade agreement (USMCA). Canada has imposed retaliatory tariffs but can ill-afford a protracted trade war as 75% of Canadian exports head to the US. A trade war would also boost inflation and complicate the Bank of Canada’s plans to continue lowering interest rates.

US nonfarm payrolls expected to ease

All eyes will be on today’s US nonfarm payrolls. The US labor market has been cooling down but hasn’t shown signs of accelerated deterioation, which would mean further rate cuts from the Federal Reserve. The market estimate for February stands at 160 thousand, compared to 143 thousand in January. Wage growth is expected to rise 0.3% m/m in February, down from 0.5% in January. Annualized wage growth is expected to remain unchanged at 4.1%.

The Federal Reserve is watching carefully, as recent federal spending cuts and tariffs could weigh on the labor market. The Fed is widely expected to hold rates at the March 19 meeting and there is a good chance that we won’t see any futher rate cuts this year. The Fed’s rate path will depend on inflation and the strength of the labor market.

USD/CAD Technical

- USD/CAD is testing resistance at 1.4303. This is followed by resistance at 1.4468

- There is support at 1.4230 and 1.4165

EUR/USD Holds Firm as US Dollar Ends the Week With Losses

EUR/USD is trading near 1.0806 on Friday, maintaining its position despite failing to extend its gains further. Investors are focused on the upcoming US employment data for February, which will be released later today.

Key factors influencing EUR/USD

The US dollar briefly found support after President Donald Trump temporarily excluded some Canadian and Mexican goods from the 25% tariffs imposed earlier this week. This move raised hopes for further trade concessions, easing concerns slightly.

However, despite this development, the USD is on track to close the first week of March with a loss of over 3%. The escalating trade war has increased fears of negative economic consequences for the US, particularly given the heavy reliance of US companies on free trade.

Meanwhile, the euro gained support from expectations of increased government spending in Germany and other European nations, particularly in defence investments.

The European Central Bank (ECB) cut its interest rate as expected, reducing it to 2.65% per annum. This move was widely anticipated and did not create market surprises.

Technical analysis of EUR/USD

On the H4 chart, EUR/USD completed a growth wave to 1.0850 and is now forming a consolidation range around 1.0800. A downward breakout from this range is expected, potentially leading to a decline towards 1.0600. After reaching this level, a correction towards 1.0700 could follow. The MACD indicator supports this scenario, with its signal line above zero but turning downward, indicating potential weakness.

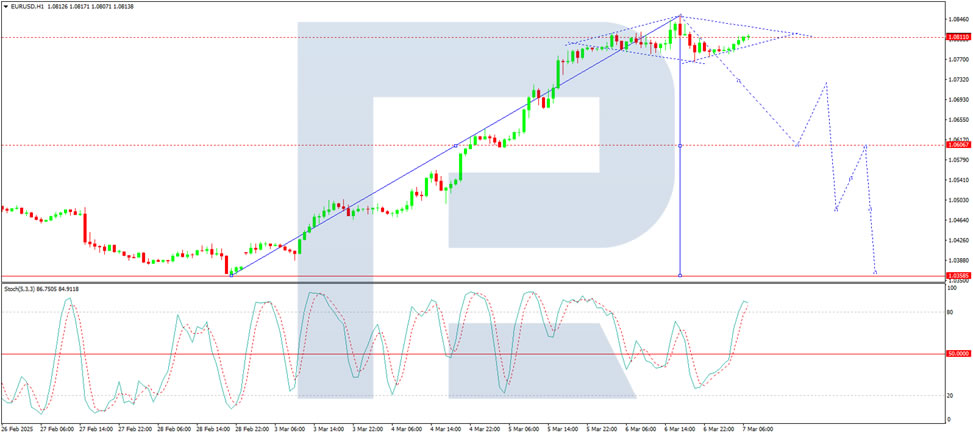

On the H1 chart, EUR/USD is consolidating around 1.0800. A move down to 1.0730 is expected, followed by a possible retest of 1.0800 from below before another decline towards 1.0600. If this trend continues, the next target could be 1.0400. The Stochastic oscillator confirms this outlook, with its signal line above 80 and preparing to decline towards 20, indicating a potential bearish shift.

Conclusion

EUR/USD remains elevated but faces increasing downside risks, particularly if US job data strengthens the dollar. While trade tensions and ECB policy support the euro, technical indicators suggest a potential decline towards 1.0600, with further downside possible. The US employment report will be a critical driver for the next major move in the pair.