Sample Category Title

Weekly Market Outlook: Trigger Uncertainty, Nasdaq in Correction & US CPI Data Ahead

- Markets experienced turmoil this week, driven by investor concerns over the Trump administration’s tariff policies.

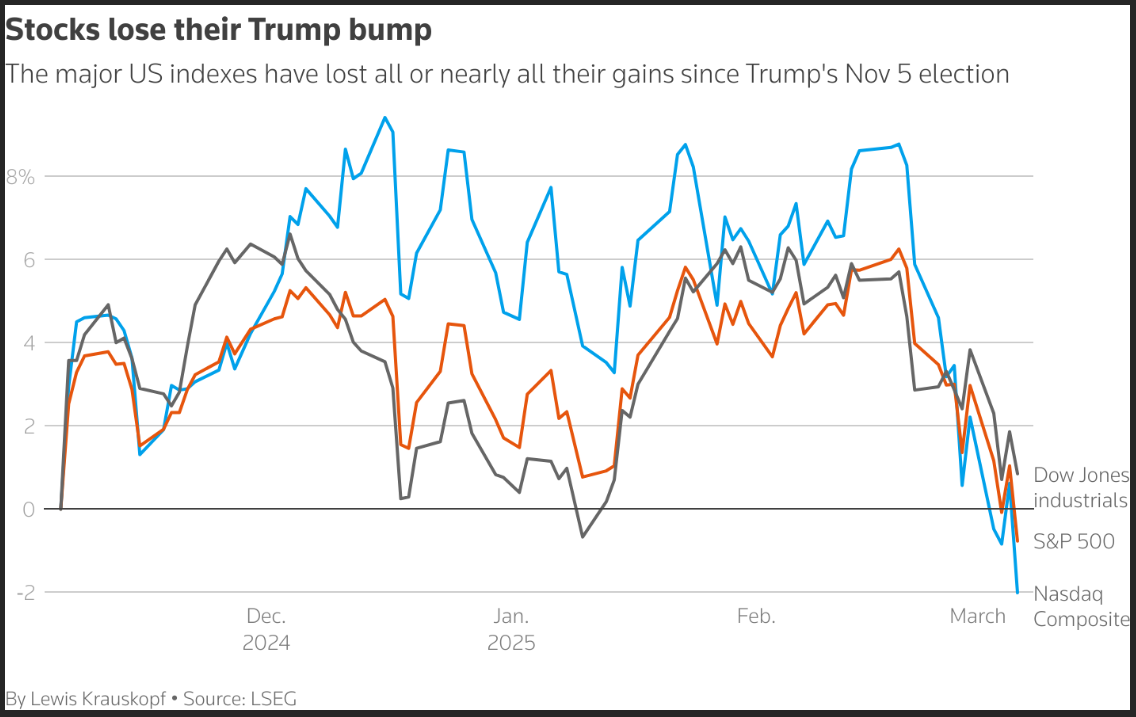

- The US dollar is on track for its worst week in over a year, Nasdaq entered a correction.

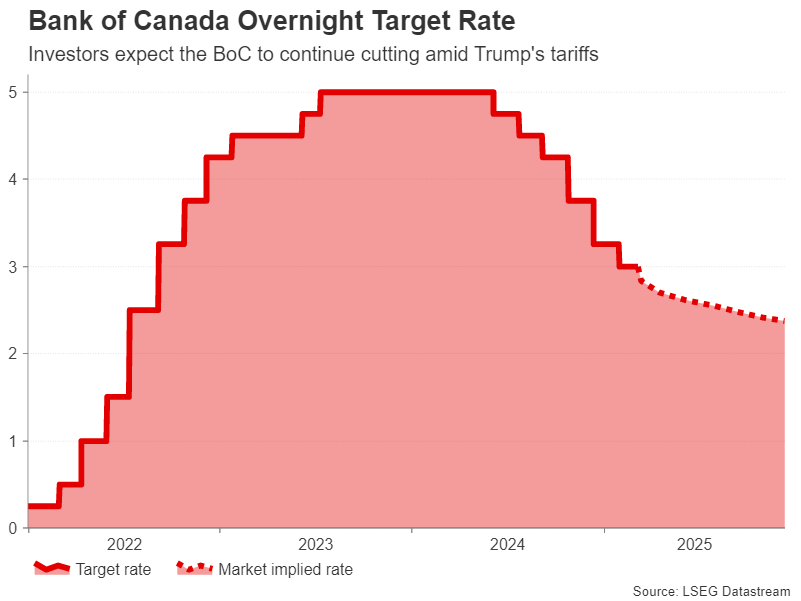

- The Bank of Canada may cut rates due to tariff impacts and economic concerns.

- US CPI is also due in the week ahead, will it rescue the ailing US Dollar?

Week in Review: Fear is Rising but US Labor Market Remains Steady for Now

Markets have struggled this week as fears are rising. Wall Street is on edge as investors say the Trump administration’s mixed signals on rolling back tariffs are creating confusion instead of easing concerns.

The S&P 500 has dropped 4.3% since President Trump took office on January 20, with tariffs being a major worry for investors. Many believe tariffs could hurt economic growth and lead to higher prices.

On Thursday, stocks faced a sharp selloff after Trump announced a one-month exemption for Canada and Mexico from the 25% tariffs he introduced earlier in the week. The Nasdaq fell 2.6% that day and has been in a correction since its record high on December 16.

This latest tariff move gave limited relief to stocks, as Wall Street remains unsure about how a tariff-driven trade policy might affect the economy.

The Nasdaq 100 has now officially entered corrective territory with losses of 10% from its all time high.

Trump believes tariffs can boost revenue, growth, and help in negotiations with other countries. However, investors are worried they may hurt consumer confidence and cause businesses to hold back on spending.

Sources: LSEG Datastream

A brief pause came on Friday with the US jobs data release. The U.S. added 151,000 jobs last month, according to the Labor Department, following a revised increase of 125,000 jobs in January. Economists had predicted a rise of 160,000 jobs, compared to the earlier reported January figure of 143,000.

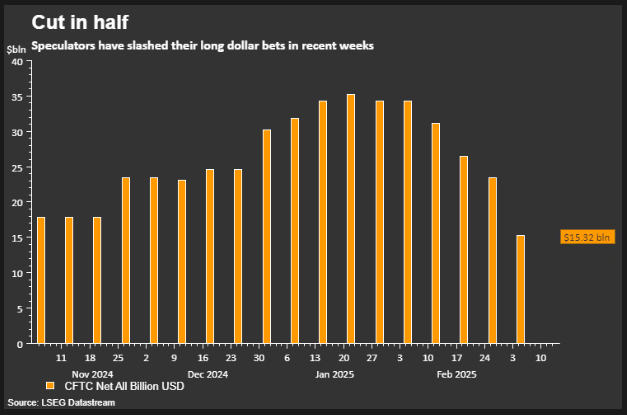

On the FX Front the dollar showed its vulnerabilities and is on course for its worst week in over a year. The dollar has dropped about 5% since President Trump took office in January and is now at a four-month low.

Concerns about U.S. growth, fueled by trade tariff news, have hurt the dollar. Meanwhile, Germany’s boost in spending has improved Europe’s economic outlook, leading investors to move their money to economies with stronger growth prospects.

The chart below shows how speculators have slashed their bets on a bullish US Dollar in recent weeks.

Source: LSEG

On the commodities front, Gold has rebounded this week to trade back above the $2900/oz mark, but continues to struggle to pierce through resistance at the $2924 handle. As we have discussed for weeks now, the geopolitical situation coupled with tariff uncertainty is likely to keep the precious metal supported.

Oil prices faltered this week thanks to the OPEC+ announcement and growth fears. For a full breakdown read Brent Oil Price Analysis: Six-Month Lows Amid OPEC Output, Tariffs & Russia-Ukraine Negotiations

The Week Ahead: Tariffs at the Forefront. Will Trump Follow Through?

Asia Pacific Markets

The main focus this week in the Asia Pacific region for me is China’s Two Sessions and inflation data.

China’s Two Sessions ends next Tuesday, with key policy updates expected on stimulus and reforms. February inflation data is due Sunday, and the Lunar New Year impact may push consumer inflation to -0.3% year-on-year, while producer inflation is also expected to stay negative. Credit data for February is expected next week, with markets predicting higher overall financing and new loans in RMB.

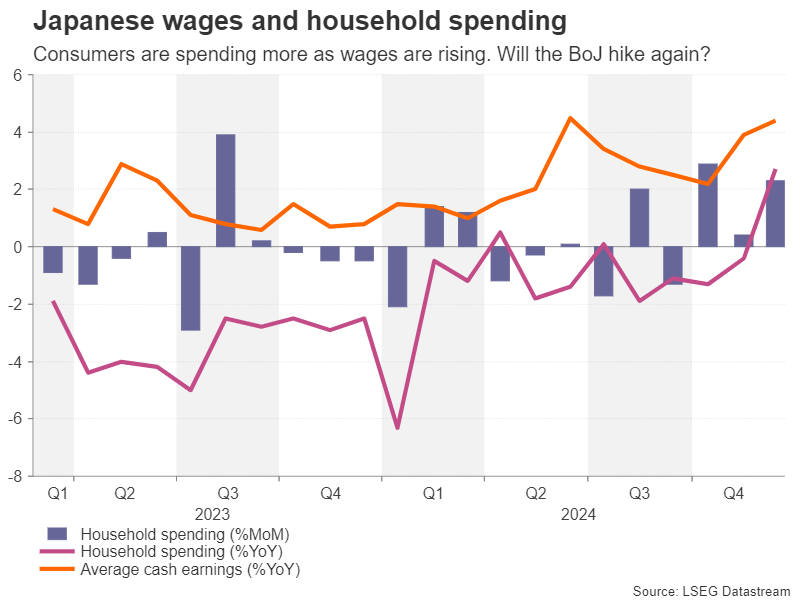

In Japan, I do expect growth in labor earnings to slow, mainly due to smaller bonus payments. January’s inflation spike will likely push real earnings into the negative. Fourth quarter GDP may be revised down from 0.7% to 0.5% because capital spending was weaker than expected.

Markets are still focused on Japan as further interest rate hikes from the Bank of Japan remain on the table.

Europe + UK + US

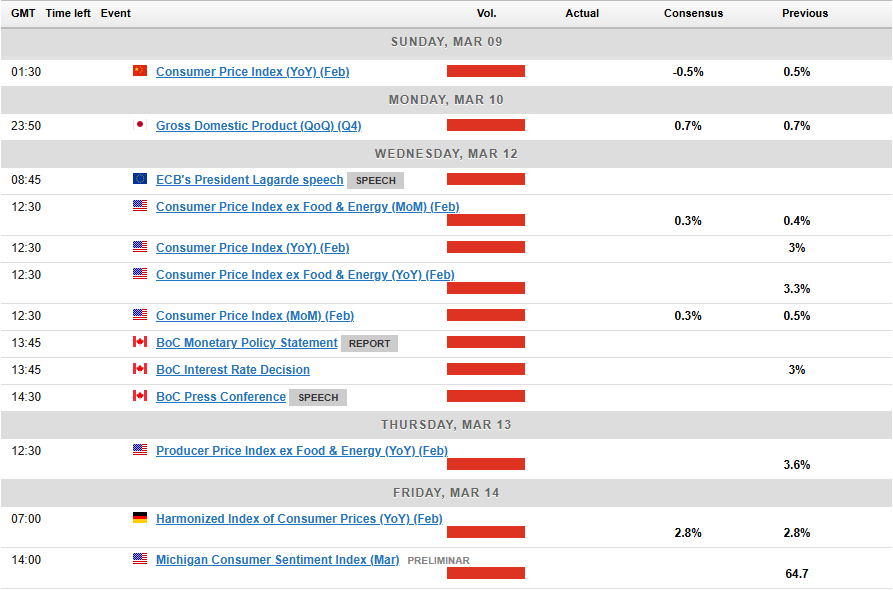

In developed markets, the US inflation is back in the limelight. The data however, might be overshadowed once more by the ongoing tit-for-tat tariff developments which are set to continue.

U.S. consumer price inflation is expected to remain high in the coming week, with a 0.3% month-on-month increase forecasted. Business surveys show some companies are raising prices ahead of potential tariffs. Food and energy costs are also pushing inflation higher, even though gasoline prices have recently dropped.

However, markets are currently more concerned about slowing growth, government spending cuts, and the risk of reduced purchasing power if tariffs lead to higher prices. Over the past three weeks, expectations have shifted from predicting one small rate cut this year to three. A 0.3% inflation figure is unlikely to change this outlook.

The EU and UK have a bit of breather on the data front next week with a speech by ECB President Christine Lagarde on Wednesday the highlight.

The Bank of Canada has already cut rates by 200 basis points due to weak growth and low inflation. U.S. tariffs on Canadian imports are adding fears of a recession. Governor Macklem warned that a long trade conflict could severely damage the economy, which their models show would shrink before recovering on a path 2.5% below earlier forecasts.

Since 76% of Canadian exports go to the U.S., equal to 20% of GDP, the risks are high. With 6.6% unemployment and 1.9% inflation, the BoC may cut rates by another 25 basis points on Wednesday.

Chart of the Week

This week’s focus is on the Nasdaq 100 chart as the index had fallen as much as 10% from its all time highs this past week.

Friday did however bring a significant recovery from the weekly low of 19733, with the index rising to trade at 20131 at the time of writing. That is a near 2% percent rise from the weekly low.

Is this a temporary pullback or are the bulls finally back?

Time will tell, but given the amount of uncertainty and concerns from companies, there is a real possibility that there may be more downside ahead.

Immediate resistance rests at the 20326 handle which also houses the 200-day MA and could prove a tough nut to crack. If the index is capable of recording a daily candle close above this level then a run toward 20484 and 20790 become a real possibility.

A break of the psychological 20000 handle though could be key and could lead to a longer term selloff down to the mid 18000’s.

Support may be found at 19750 and 19123.

Nasdaq 100 Daily Chart – March 7, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 20000

- 19733

- 19123

Resistance

- 20326

- 20484

- 20790

The Weekly Bottom Line: Trade Policy Rollercoaster Rattles Markets

Canadian Highlights

- Trump made good on his 25% tariffs threat against Canada and Mexico this week. In the end it only lasted 72 hours, but the rollercoaster gave markets a fright.

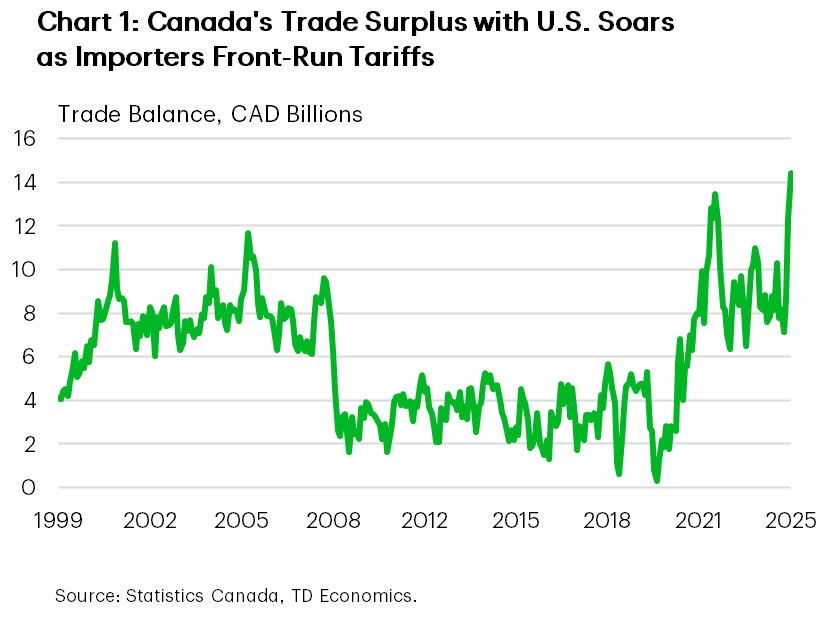

- Canada’s goods trade balance with the U.S. widened substantially in January, highlighting American companies are stockpiling supplies ahead of tariffs.

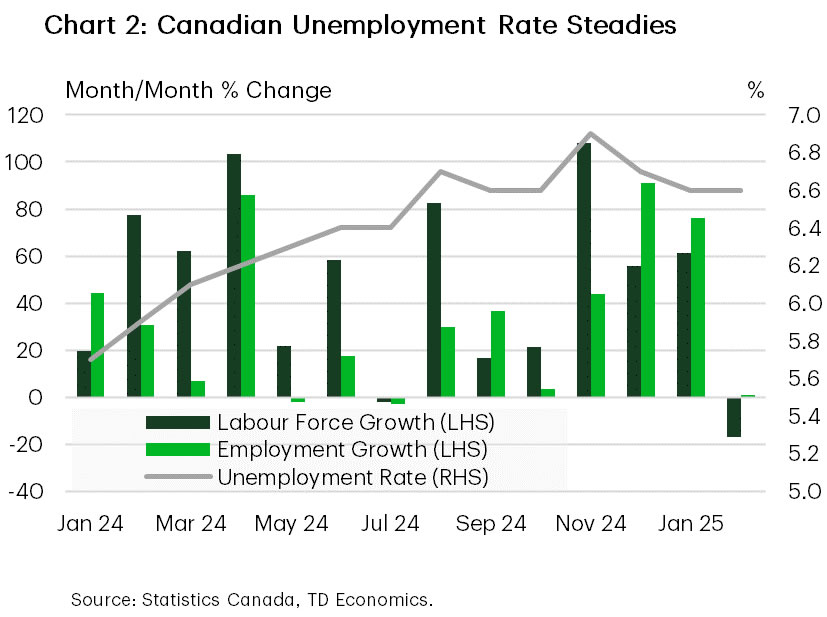

- Canada’s labour market got snowed-in in February. A labour force contraction balanced out the lack of job growth, keeping the unemployment rate steady.

U.S. Highlights

- On-again off-again trade policy continued this week as the U.S. implemented steep tariffs on imports from Canada and Mexico, but then backtracked, announcing carve-outs for USMCA-compliant imports until April 2nd.

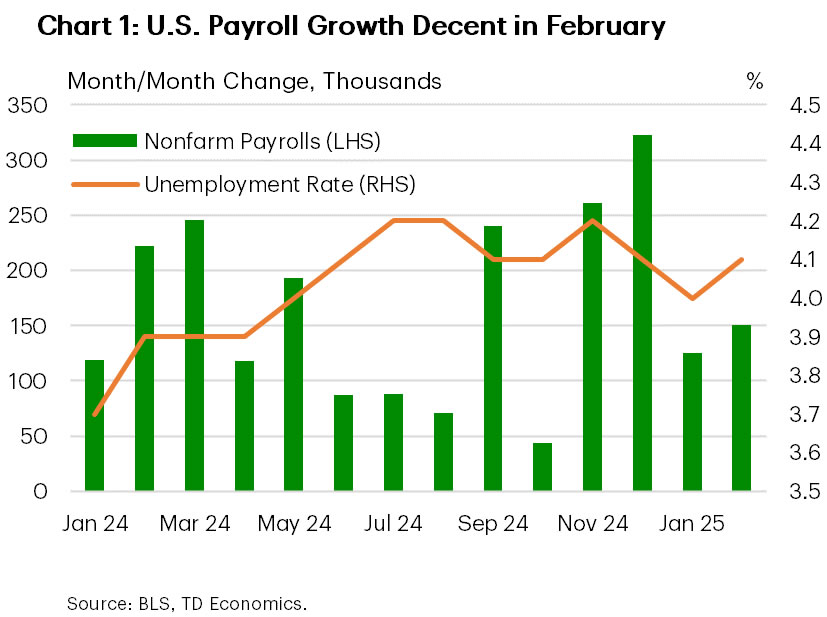

- U.S. hiring activity improved moderately in February, with the U.S. economy adding 151 thousand jobs last month. The unemployment rate ticked up from 4.0% to 4.1%.

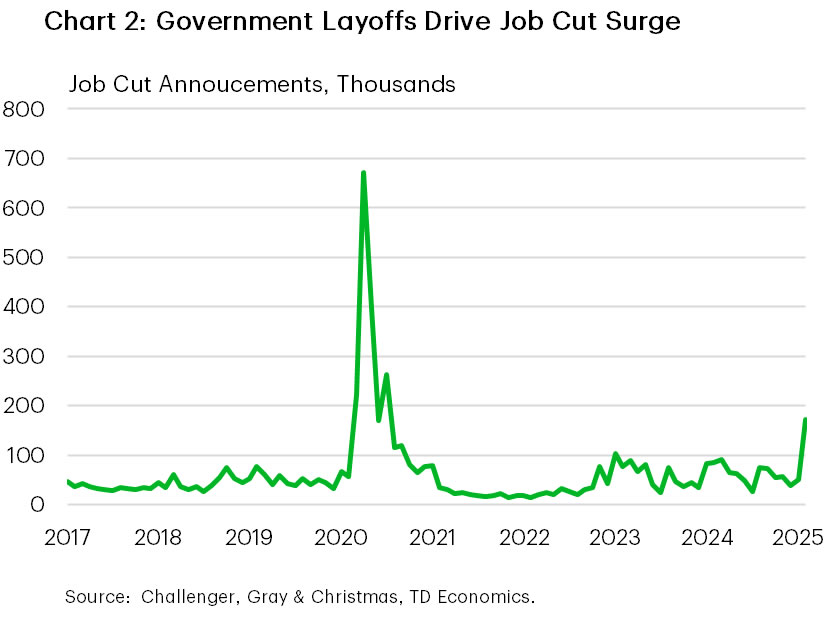

- One measurement of job cut announcements surged to 172 thousand in February, with government sector layoffs driving the surge.

Canada – Tariff-Induced Headaches

Canadians’ necks are likely sore from following the back and forth of this week’s tariff volleys. Beginning on March 4th, the previously unthinkable happened – the U.S. implemented 25% tariffs on Canadian and Mexican goods— with a 10% tariff on energy. Over the next 72 hours, Canada doubled-down on its retaliatory plan, the auto sector was granted a one-month carve out, and an executive order was signed pausing tariffs on Canadian and Mexican goods compliant with the United States-Mexico-Canada Free Trade Agreement (USMCA). And as it turns out, markets aren’t loving the uncertainty. Stocks continued to slide, with the S&P 500 and Canadian benchmark TSX dropping around 2% on the week. Canadian two and ten-year government bond yields rose modestly, helped by easing growth concerns, and the CAD nudged higher, finishing the week at 69.6 cents US.

Trade data confirmed that U.S. importers were proactive, and stockpiled Canadian goods to get ahead of tariffs. Canada’s monthly trade balance with the U.S. widened to over $14 billion in January, a new historical high (Chart 1). This was driven by a 7.5% month-on-month (m/m) surge in exports focused in the automotive sector, consumer goods, industrial machinery & equipment and energy products, which are key sectors impacted by tariffs. What’s more, since Trump won the election in November, nominal exports to the U.S. are up by a whopping 22%, the largest three-month gain on record, and by a considerable margin—excluding the frenetic export recovery in mid-2020. In the near-term, Canada’s economy will benefit from this tariff front-running, with early tracking showing a sizeable contribution from net trade to first quarter GDP growth. The expected broad-based weakness in the Canadian dollar could also buffer exports as trade flows constrict if and when tariffs set in.

Meanwhile, Canada’s labour market flatlined in February, with virtually no job created in the snowy month. Despite this, the unemployment rate held steady 6.6%, as the labour force contracted for the first time in seven months (Chart 2). On the margin, it was a weak report relative to expectations, but the readings were skewed by the intense snowstorms that occurred during the survey’s reference week. Almost half a million employees saw a reduction in hours worked because of the weather, pulling nation-wide total hours worked lower by 1.3%. This may have a negative impact on February’s industry-based GDP readings, but we’d expect a positive kick-back in March.

The Bank of Canada is set to make a highly anticipated interest rate announcement next Wednesday. For several weeks, we’ve expected the BoC to deliver a 25 basis point (bps) cut to take out insurance against a trade war escalation, despite the domestic economy running at a decent clip. Indeed, market pricing is aligned with our call, now predicting a 90% chance of a 25 basis (bps) rate cut, up from only 30% a couple weeks ago.

U.S. – Trade Policy Rollercoaster Rattles Markets

The first week of March proved to be a rollercoaster for financial markets. While plenty of important data reports were published, these generally played second fiddle to developments on the trade front. Early in the week, the U.S. imposed 25% tariffs on Canada and Mexico, and an additional 10% tariff on China. Canada and China retaliated, albeit in a more measured approach. As the trade conflict heated up, stock markets trended lower. But, slightly cooler heads seemed to prevail in the following days, with the U.S. first announcing a carve-out from tariffs for the auto sector, then announcing that all USMCA-compliant imports from Canada and Mexico would be exempt from the 25% tariff until April 2nd.

At a first glance, the latest backtracking on the tariff measures can be viewed as a positive development. However, the amount of trade that will ultimately be tariff exempt is still unclear, with at least some portion of imported goods from Canada and Mexico expected to face a higher tariff rate than they had until recently. The complicated nature of trade rules and processes is likely to cause delays and disruptions to supply chains.

Furthermore, the fact that this latest move provides only a partial reprieve from higher tariffs, with trade tensions likely to flare up once again in a month from now, does little to alleviate concerns. In fact, come April 2nd, tariff action is expected to involve many other countries. On that day, the U.S. is expected to impose reciprocal tariffs on all nations that place tariffs or tariff-like barriers on U.S. goods.

Tariff threats have already effected business decisions, as many firms ramped up shipments early in the year to get ahead of tariffs. Imports surged 10% in January, which widened the U.S. trade deficit to a record of $131 billion. This is likely to weigh on growth in the first quarter. The stop-start nature of policy moves also undermines consumer and business confidence, and is expected to weigh on investment decisions.

For the time being, the job market remains on solid footing, with the U.S. economy adding 151k jobs in February (Chart 1). However, job growth is likely to soften ahead. Apart from the potential for trade policy uncertainty to weigh on near-term hiring intentions, federal layoffs related to DOGE also continue to mount. Job cut announcements surged in February, with a steep increase in layoffs in the government sector being the largest contributor to the overall tally (Chart 2). The potential for a government shutdown, which could happen as early as next weekend, may pose additional downside risk over the near-term.

The Fed will have to carefully weigh the risks of a potential slowing in economic activity against the risk of a near-term boost in inflation. The price measures in both the Manufacturing and Services ISM surveys increased in February. For the time being, the Fed is expected to remain on hold, but come summer we could see chair Powell taking out the interest rate scissors.

Weekly Economic & Financial Commentary: Tariff Turmoil

Summary

United States: Tariff Turmoil

- The U.S. economy added 151K jobs in February accompanied by higher unemployment and lower labor force participation. Economic developments elsewhere reflected heightened uncertainty around trade policy, prompting a leap in imports, concerned industry comments and reports of higher input prices.

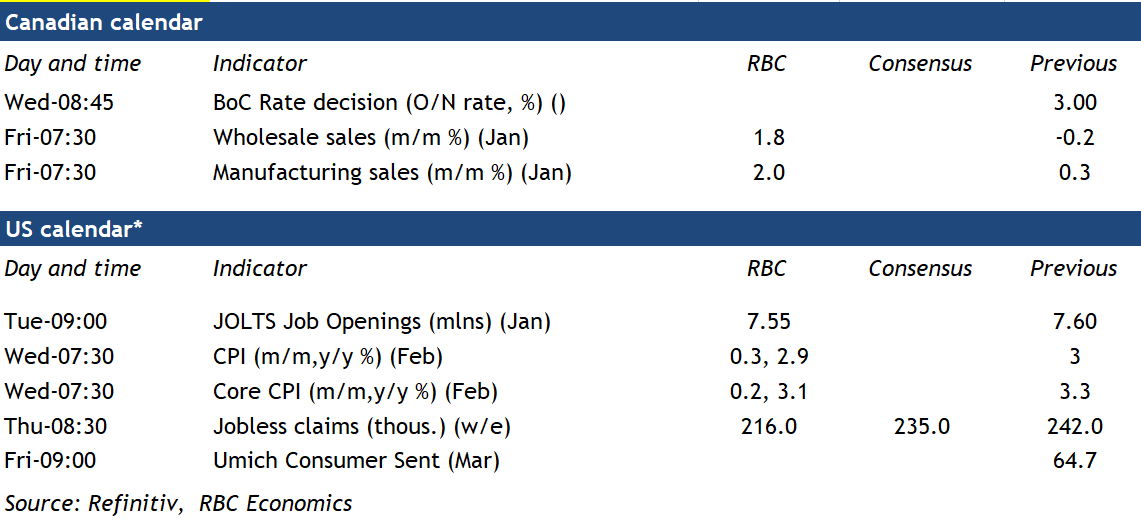

- Next week: JOLTS (Tue.), CPI (Wed.), Federal Budget (Wed.)

International: Simulating the Economic Impact of Tariffs

- In an effort to proactively assess the economic impact of changes to U.S. and international trade policy, we modeled two new tariff scenarios. The more aggressive and contentious simulation—defined by aggressive tariff hikes and matching retaliation—leads to global recession in 2026 and sharp economic downturns in Canada and Mexico.

- Next week: Tariff Talk (Mon.-Fri.), Bank of Canada Rate Decision (Wed.), Brazil Inflation (Wed.)

Interest Rate Watch: What to Make of the 10-Year Treasury Yield?

- The 10-year Treasury yield has fallen sharply to start the year. The yield on the 10-year note began 2025 around 4.6%, and it got as high as 4.8% in mid-January. But over the past couple of months, a more dour economic outlook amid an escalating trade war have pushed yields down to roughly 4.26% as we went to print. Have longer-term yields fallen too far too fast?

Topic of the Week: Don't Set Your Expectations Too High

- Tariffs pose upside risks to inflation, as the additional levies could be passed through to selling prices. Expectations for price growth in 2025 are recalibrating in response. Across several surveys and market-based measures, short-term inflation expectations have moved higher in recent months.

Bank of Canada’s Interest Rate Decision Will be a Tough Call

We expect the Bank of Canada interest rate decision on Wednesday will be a very close call as our base case forecast assumes it will forego a rate cut for the first time since April 2024, but U.S. trade risks could still easily tilt odds towards a seventh consecutive cut.

Outside of tariff risks, backward looking domestic demand in Canada is showing enough signs of recovering early in 2025 for the BoC to pause their cutting cycle. Inflation has remained around the central bank’s 2% target, but would be higher without the federal sales tax holiday that lowered prices for items like restaurant dining. Q4 GDP growth surprised substantially on the upside. There was some evidence of softening Canadian employment in trade sensitive sectors in February. But the unemployment rate is still below levels late last year, consistent with the view that the economy-wide production gap (the key driver of future inflation pressures in the BoC’s policy framework) had begun to narrow into 2025.

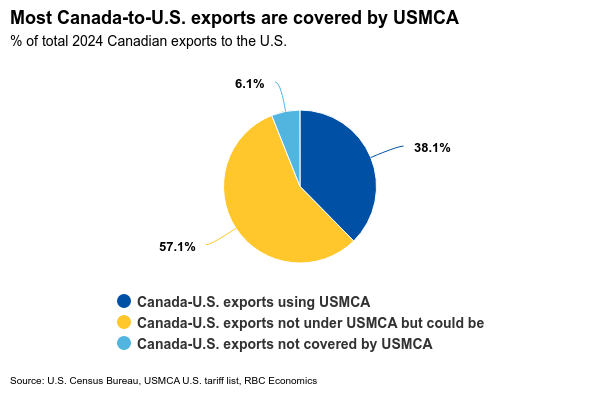

The latest round of 25% blanket tariffs on Canada and Mexico have already begun to be rolled back with reports that USMCA-compliant trade will be exempted. Only 38% of Canadian exports to the U.S. last year used CUSMA/USMCA but we expect the bulk of trade (potentially 90%+ based on our own early calculations) can be brought into compliance relatively quickly.

The reality is trade risks are not going away. Steel and aluminium tariffs are still set to be imposed in the coming week with broader reciprocal tariffs to be announced in April. What U.S. trade policy will look like week-by-week (or even hour-by-hour) is still highly uncertain. And that uncertainty itself is already threatening to choke off a recovery in Canadian business investment.

But as we have noted before , the BoC will also need to consider any potential fiscal policy response – which is better able to provided targeted, timely support than changes in interest rates that impact economic conditions more broadly and only with substantial lags. Interest rates are still relatively high. At 3%, the overnight rate remains near the top of the 2.25% to 3.25% range that the BoC views as having a neutral impact on the economy. But Governor Macklem has also explicitly highlighted the limits of monetary policy as a tool to offset tariff shocks, and the BoC still needs to strike balance between supporting the economy through uncertainty while guarding against adding unnecessarily to future inflation.

Summary 3/10 – 3/14

Monday, Mar 10, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | 3.20% | 4.80% |

| 23:50 | JPY | Bank Lending Y/Y Feb | 3.10% | 3% |

| 23:50 | JPY | Current Account (JPY) Jan | 1.99T | 2.73T |

| 05:00 | JPY | Leading Economic Index Jan P | 108.4 | |

| 05:00 | JPY | Eco Watchers Survey: Current Feb | 48.5 | 48.6 |

| 07:00 | EUR | Germany Industrial Production M/M Jan | 1.50% | -2.40% |

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | 21.2B | 20.7B |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | -10 | -12.7 |

| 21:45 | NZD | Manufacturing Sales Q4 | -1.20% | |

| 23:30 | AUD | Westpac Consumer Confidence Mar | 0.10% | |

| 23:30 | JPY | Overall Household Spending Y/Y Jan | 3.60% | 2.70% |

| 23:50 | JPY | GDP Q/Q Q4 F | 0.70% | 0.70% |

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | 2.80% | 2.80% |

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | 1.40% | 1.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | |

| Forecast: 3.20% | Previous: 4.80% | ||

| 23:50 | JPY | Bank Lending Y/Y Feb | |

| Forecast: 3.10% | Previous: 3% | ||

| 23:50 | JPY | Current Account (JPY) Jan | |

| Forecast: 1.99T | Previous: 2.73T | ||

| 05:00 | JPY | Leading Economic Index Jan P | |

| Forecast: | Previous: 108.4 | ||

| 05:00 | JPY | Eco Watchers Survey: Current Feb | |

| Forecast: 48.5 | Previous: 48.6 | ||

| 07:00 | EUR | Germany Industrial Production M/M Jan | |

| Forecast: 1.50% | Previous: -2.40% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Jan | |

| Forecast: 21.2B | Previous: 20.7B | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | |

| Forecast: -10 | Previous: -12.7 | ||

| 21:45 | NZD | Manufacturing Sales Q4 | |

| Forecast: | Previous: -1.20% | ||

| 23:30 | AUD | Westpac Consumer Confidence Mar | |

| Forecast: | Previous: 0.10% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Jan | |

| Forecast: 3.60% | Previous: 2.70% | ||

| 23:50 | JPY | GDP Q/Q Q4 F | |

| Forecast: 0.70% | Previous: 0.70% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | |

| Forecast: 1.40% | Previous: 1.30% | ||

Tuesday, Mar 11, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Feb | 4 | |

| 00:30 | AUD | NAB Business Conditions Feb | 3 | |

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | 4.70% | |

| 10:00 | USD | NFIB Business Optimism Index Feb | 101 | 102.8 |

| 23:50 | JPY | PPI Y/Y Feb | 4.00% | 4.20% |

| 23:50 | JPY | BSI Large Manufacturing Q1 | 6.5 | 6.3 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Feb | |

| Forecast: | Previous: 4 | ||

| 00:30 | AUD | NAB Business Conditions Feb | |

| Forecast: | Previous: 3 | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | |

| Forecast: | Previous: 4.70% | ||

| 10:00 | USD | NFIB Business Optimism Index Feb | |

| Forecast: 101 | Previous: 102.8 | ||

| 23:50 | JPY | PPI Y/Y Feb | |

| Forecast: 4.00% | Previous: 4.20% | ||

| 23:50 | JPY | BSI Large Manufacturing Q1 | |

| Forecast: 6.5 | Previous: 6.3 | ||

Wednesday, Mar 12, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 12:30 | USD | CPI M/M Feb | 0.30% | 0.50% |

| 12:30 | USD | CPI Y/Y Feb | 2.90% | 3.00% |

| 12:30 | USD | CPI Core M/M Feb | 0.30% | 0.40% |

| 12:30 | USD | CPI Core Y/Y Feb | 3.20% | 3.30% |

| 13:45 | CAD | BoC Interest Rate Decision | 2.75% | 3.00% |

| 14:30 | CAD | BoC Press Conference | ||

| 14:30 | USD | Crude Oil Inventories | 3.6M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 12:30 | USD | CPI M/M Feb | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 12:30 | USD | CPI Y/Y Feb | |

| Forecast: 2.90% | Previous: 3.00% | ||

| 12:30 | USD | CPI Core M/M Feb | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | CPI Core Y/Y Feb | |

| Forecast: 3.20% | Previous: 3.30% | ||

| 13:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 2.75% | Previous: 3.00% | ||

| 14:30 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 3.6M | ||

Thursday, Mar 13, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Mar | 4.60% | |

| 00:01 | GBP | RICS Housing Price Balance Feb | 20% | 22% |

| 07:30 | CHF | Producer and Import Prices M/M Feb | 0.20% | 0.10% |

| 07:30 | CHF | Producer and Import Prices Y/Y Feb | -0.30% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | 0.80% | -1.10% |

| 12:30 | USD | Initial Jobless Claims (Mar 7) | 224K | 221K |

| 12:30 | CAD | Building Permits M/M Jan | -4.80% | 11.00% |

| 12:30 | USD | PPI M/M Feb | 0.30% | 0.40% |

| 12:30 | USD | PPI Y/Y Feb | 3.50% | |

| 12:30 | USD | PPI Core M/M Feb | 0.30% | 0.30% |

| 12:30 | USD | PPI Core Y/Y Feb | 3.60% | |

| 14:30 | USD | Natural Gas Storage | -80B | |

| 21:30 | NZD | Business NZ PMI Feb | 51.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Mar | |

| Forecast: | Previous: 4.60% | ||

| 00:01 | GBP | RICS Housing Price Balance Feb | |

| Forecast: 20% | Previous: 22% | ||

| 07:30 | CHF | Producer and Import Prices M/M Feb | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Feb | |

| Forecast: | Previous: -0.30% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | |

| Forecast: 0.80% | Previous: -1.10% | ||

| 12:30 | USD | Initial Jobless Claims (Mar 7) | |

| Forecast: 224K | Previous: 221K | ||

| 12:30 | CAD | Building Permits M/M Jan | |

| Forecast: -4.80% | Previous: 11.00% | ||

| 12:30 | USD | PPI M/M Feb | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | PPI Y/Y Feb | |

| Forecast: | Previous: 3.50% | ||

| 12:30 | USD | PPI Core M/M Feb | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | PPI Core Y/Y Feb | |

| Forecast: | Previous: 3.60% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -80B | ||

| 21:30 | NZD | Business NZ PMI Feb | |

| Forecast: | Previous: 51.4 | ||

Friday, Mar 14, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany CPI M/M Feb F | 0.40% | 0.40% |

| 07:00 | EUR | Germany CPI Y/Y Feb F | 2.30% | 2.30% |

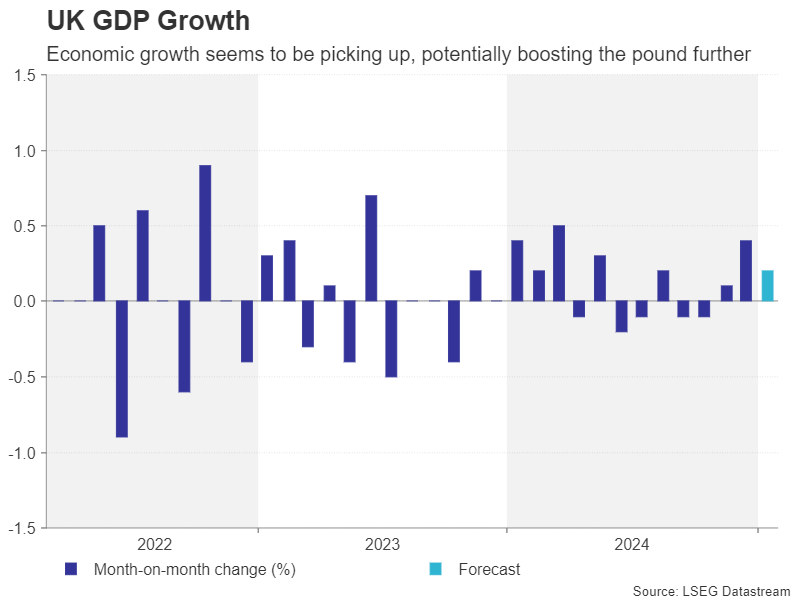

| 07:00 | GBP | GDP M/M Jan | 0.10% | 0.40% |

| 07:00 | GBP | Industrial Production M/M Jan | -0.10% | 0.50% |

| 07:00 | GBP | Industrial Production Y/Y Jan | -1.90% | |

| 07:00 | GBP | Manufacturing Production M/M Jan | 0.00% | 0.70% |

| 07:00 | GBP | Manufacturing Production Y/Y Jan | -1.40% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -17.1B | -17.4B |

| 12:30 | CAD | Manufacturing Sales M/M Jan | 2.00% | 0.30% |

| 12:30 | CAD | Wholesale Sales M/M Jan | 1.80% | -0.20% |

| 14:00 | USD | UoM Consumer Sentiment Mar P | 63.8 | 64.7 |

| 14:00 | USD | UoM Inflation Expectations Mar P | 3.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany CPI M/M Feb F | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 07:00 | EUR | Germany CPI Y/Y Feb F | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 07:00 | GBP | GDP M/M Jan | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 07:00 | GBP | Industrial Production M/M Jan | |

| Forecast: -0.10% | Previous: 0.50% | ||

| 07:00 | GBP | Industrial Production Y/Y Jan | |

| Forecast: | Previous: -1.90% | ||

| 07:00 | GBP | Manufacturing Production M/M Jan | |

| Forecast: 0.00% | Previous: 0.70% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Jan | |

| Forecast: | Previous: -1.40% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | |

| Forecast: -17.1B | Previous: -17.4B | ||

| 12:30 | CAD | Manufacturing Sales M/M Jan | |

| Forecast: 2.00% | Previous: 0.30% | ||

| 12:30 | CAD | Wholesale Sales M/M Jan | |

| Forecast: 1.80% | Previous: -0.20% | ||

| 14:00 | USD | UoM Consumer Sentiment Mar P | |

| Forecast: 63.8 | Previous: 64.7 | ||

| 14:00 | USD | UoM Inflation Expectations Mar P | |

| Forecast: | Previous: 3.50% | ||

Week ahead – US CPI Set to Ease, BoC to Probably Cut Again

- Dollar’s pain could worsen as US CPI expected to ease slightly.

- Bank of Canada faces rate cut dilemma amid US tariffs.

- UK and Japanese indicators also eyed.

Will US CPI report bring some inflation relief?

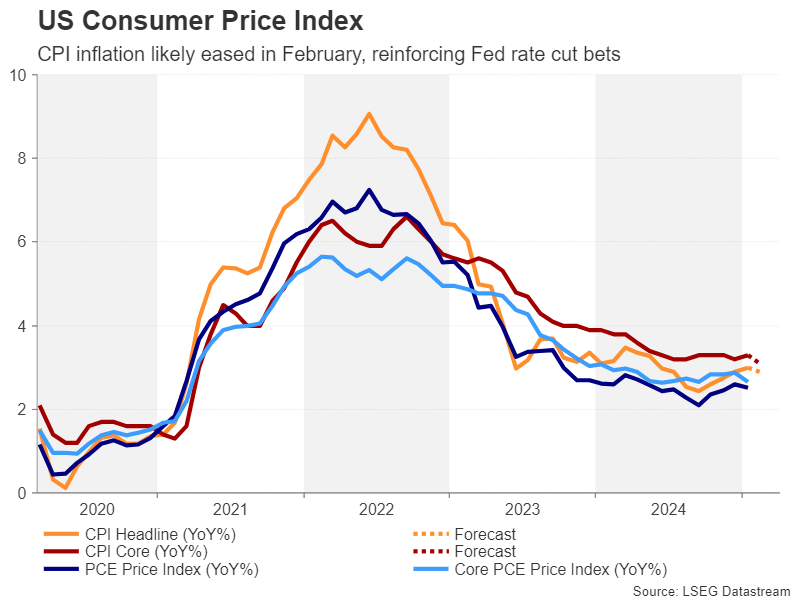

As investors attempt to keep up with the daily shift in President Trump’s tariff policies, the February CPI report out of the United States on Wednesday will likely come as a much-needed distraction. Specifically, the inflation data may signify the start of a new downward path for the CPI measure, following in the footsteps of the January PCE figures.

The Fed’s fight against high inflation hasn’t been easy. The recent uptick in price pressures must have been frustrating for policymakers to say the least. But US inflation appears to be turning a corner now and is expected to head lower over the next few months.

There is one problem – tariffs. Trump’s decision to go ahead with levies as high as 25% against Canada and Mexico and raise them by 20% for China, not to forget the sectoral and reciprocal tariffs that have yet to be finalized, could derail the Fed’s battle to steer inflation all the way down to 2.0%.

In January, the headline rate of CPI climbed to the highest since June 2024, reaching 3.0% y/y. Core CPI also edged up, rising to 3.3% y/y. But the February data will likely end months of worry that inflation is rearing its ugly head again, as headline CPI is projected to moderate to 2.9%, while core CPI is expected to decline to 3.1%. The month-on-month forecasts for both are 0.3%.

On Thursday, the producer price index for the same month will shed further light on underlying price pressures in the US economy, and on Friday, investors will turn their attention to the University of Michigan’s preliminary consumer sentiment survey for March. Last month’s survey sparked some concerns as it showed consumers’ inflation expectations creeping higher. In particular, five-year expectations rose to a 30-year high.

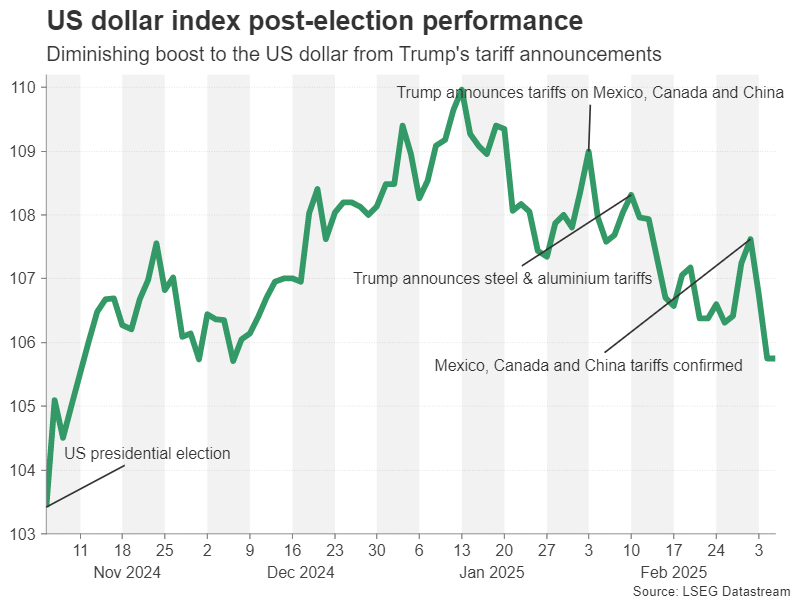

Can the Dollar recoup some lost ground?

A continuation of this uptrend would cast doubt on the notion that the inflation outlook is improving, arguing for ongoing caution at the Fed.

However, looking at Fed rate cut expectations, it seems that investors have already made up their minds that inflation no longer poses a threat, and that the bigger danger is economic growth grinding to a halt on the back of Trump’s protectionist trade policies.

Yet, with the US dollar having tumbled by more than 3% over the past week, any upside surprises in the incoming price indicators could spur a rebound.

BoC rate cut may hang in the balance

The Bank of Canada meets on Wednesday to set interest rates, keeping the spotlight on the country amid the trade spat with the United States. Unlike his Mexican counterpart, Prime Minister Justin Trudeau has not held back in announcing retaliatory tariffs on imports from Canada’s southern neighbour and by far its biggest trading partner.

Hence, this escalation is not only expected to deliver a severe blow to Canada’s economy, but it could also lead to higher prices on C$125 billion worth of goods imported from the US.

But it may not come to that, as Trump just signed new executive orders delaying the 25% tariffs on almost 40% of goods entering from Canada until April 2. In response, Trudeau has put on hold his latest counter levies.

For the Bank of Canada, however, this still poses a major policy dilemma. Following the Bank’s aggressive rate cuts last year, the Canadian economy is bouncing back, with employment surging, although consumer spending remains somewhat patchy. More importantly for policymakers, there are signs that inflation is bottoming out.

Having already slashed rates by a total of 200 basis points, it makes sense for the BoC to take to the sidelines. But the downside risks to growth from Trump’s tariffs will likely sway policymakers to cut again in March.

Investors have assigned a 66% probability of a 25-bps reduction in the target rate. The Canadian dollar therefore stands to see a strong reaction either way. Although in the scenario of a rate cut, the loonie might even appreciate against the US dollar if the BoC signals that a pause is on the horizon.

It’s possible of course that Trump may steal the BoC’s thunder if there are any further tariff developments over the next few days, keeping loonie traders on standby.

Will UK data spoil the Pound’s bullish streak?

The pound, along with the euro, have benefited the most from the dollar’s pullback. Sterling has set its sights on the $1.30 handle, recovering sharply from its January lows. However, it’s uncertain how sustainable this rally is as the UK economy is grappling with its own problems even in the absence of a direct tariff threat.

On Friday, investors will be keeping an eye on the latest monthly output figures on industrial, manufacturing and services production, as well as aggregate GDP.

There was a surprise rebound in GDP growth in December, providing some reprieve for the embattled Labour chancellor, Rachel Reeves. But if growth faltered again in January, the pressure on Reeves will increase ahead of the March 26 Spring Budget Statement to come up with stronger measures to support the economy.

Yen gets caught in Trump’s trade storm

The Japanese yen, on the other hand has been the laggard among the major FX pairs, despite the Bank of Japan maintaining its hawkish rhetoric. The underperformance could be related to the Trump’s remarks about Japan manipulating the yen to keep it weak, raising speculation that Tokyo could be next on the President’s tariff hit list.

In the meantime, there’s a flurry of releases out of Japan in the first half of the week. Wage growth and household spending data for January on Monday and Tuesday, respectively, will be important in gauging whether Japanese inflation is on a sustainable path of sticking near the BoJ’s 2% target. Revisions to Q4 GDP growth are also due on Tuesday, while on Wednesday, corporate goods prices for February will be watched.

Weekly Focus – Outperformance in European Assets Continues

The new European security order has become the main market driver. This week, European equities continued to outperform the US, driven by defence stocks. At the time of writing, the German 10y yield was up 20bp on the week, diverging from US rates developments. Euro was up more than 4% against the dollar. The optimism in European assets reflects expectations of a massive defence expenditure boost. This week, the European Council decided on creating a new European instrument, up to EUR 150bn in loans from the EU to member states. Additional flexibility within the Stability and Growth pact is expected to enable EUR 650bn in investments, while the EIB's expected mandate extension should improve access to private capital.

Danske Bank published its updated macroeconomic projections this week. Regardless of all the uncertainty, the cyclical story has not changed much, see Normalising economies despite the noise, 5 March. The disinflationary process is still on the way, rates are on decline, and labour markets are cooling. All Nordic economies are expected to recover this year but divergence in pace remains. The US economy, despite cooling down, is projected to grow by 2.3% this year, while growth in euro area is projected to remain slightly below 1%. Increased defence spending in euro area is an upside risk to growth, not least in Germany where the Parliament is expected to approve sizable fiscal packages next week, while also relaxing the debt brake. If implemented, these measures will boost the German economy, but the effects will be felt next year at the earliest. Read more on Euro Area Macro Monitor - Diverging signals as Germany proposes historic changes, 7 March.

The ECB cut its policy rates by 25bp this week, bringing the deposit rate to 2.5%. Importantly, the ECB adjusted its message saying that "monetary policy is becoming meaningfully restricted". As we read it, although this week's decision was still a consensus, it is likely that some Governing Council members would soon prefer at least a pause. The spillover from a broader rally in European assets prior to the ECB meeting had already led to markets pricing out one ECB cut for this year. Currently, markets price only two additional cuts for this year, and 19bp for April. As the disinflationary process is intact (Monday's February flash print confirmed that) and as the positive growth impact from additional fiscal spending in Europe will take time to materialise, we keep our call unchanged. We still see the ECB cutting deposit rate to 1.5% by September.

Tariffs also made headlines this week. The US tariffs on goods imported from Mexico and Canada were initially raised to 25% on Tuesday, but by the end of the week, Trump had signed orders that exempted most goods until early April. The additional 10% tariff on Chinese goods that entered into force this week remains in place, and China has retaliated with tariffs targeting US farmers. This week, China announced it will stick to its 5% growth target this year and will use stimulus to counterbalance the negative impact from US tariffs.

Next week will be quiet on the data front. The Chinese CPI data will be released early on Monday. On Wednesday, we will get the US February CPI data, and on Friday, the Michigan consumer survey for March will be released. In geopolitics, we will keep an eye on the US-Ukraine meeting in Saudi Arabia on Wednesday.

Sunset Market Commentary

Markets

US February payrolls and Chair Powell’s after-European-close speech wrap up a hectic week. The former showed US employment growing by 151k, more or less in line with the expected 160k. January was revised down a bit by 18k. The goods sector added 34k, services 106k, led by the health & social sector (63k) and finance (21k), offset by leisure & hospitality (-16k) and temporary help (-6k). DOGE’s work started showed up in the federal government sector, which has shed 10k jobs. It’s the biggest monthly decline since July 2022. The household survey brought a slightly different message, with employment actually dropping. This helps explain why the unemployment rate (calculated from this survey) unexpectedly picked up from 4% to 4.1% even as the labour force participation dropped as well (62.4%). Hourly wage growth rose the expected 0.3% m/m to come in at 4% on a yearly basis. January’s figures were slightly adjusted downwards. We’d label today’s report as decent and in any case close to expectations.

It makes the market reaction all the more telling. Markets took the soft view and with it reveal ongoing sensitivity for weaker economic data. We think the genie, set free by president Trump’s chaotic policy and DOGE-sparked fears, will be hard to put back in the bottle. US Treasury yields extended previous losses to change -4 to -7 bps on a daily basis at some point, before paring them again to pre-payrolls levels as US investors joined. The dollar is down for the day but the bulk of the declines happened before the payrolls release. DXY is near the November correction low (103.37) EUR/USD did try a first shy attempt for 1.09 shortly after the publication though, but it lacked strong enough momentum. It’s given another chance later today when Powell seizes the final opportunity to speech before the black-out period kicks in ahead of the Fed meeting March 19. Another rate status quo then is all but certain. But markets have dramatically shifted the timeline over the past couple of weeks: from a first new rate cut in September somewhere mid-February towards one fully priced in for June and already 50% for May today. Stressing the recent weaker than expected economic data and/or putting the spotlights on downside growth risks could prompt more aggressive bets. Next week brings some of the final input for that March FOMC meeting with JOLTS job openings on Tuesday, CPI figures on Wednesday and a closely watched consumer confidence indicator on Friday. On the tariff front, Wednesday is an important date with March 12 being the US deadline to impose 25% steel and aluminum tariffs on the EU. “The ECB and Its Watchers” conference kicks off the same day. Friday poses another US deadline. Lawmakers need to strike a spending deal in order to avoid a federal government shutdown.

News & Views

Czech nominal wage growth beat both market and Czech National Bank (7%) expectations yesterday, rising by 7.2% Y/Y in Q4. From the CNB's perspective, wage development is a reason for caution, especially given that wage growth in the private sector surprised on the upside (+8.3% vs. the CNB's staff forecast of 7.6%). In our view, this development increases the chances that the CNB will choose to pause again its cutting cycle at the March meeting, i.e. our baseline scenario, with a next cut in official interest rates to be delivered at the May meeting. The Czech koruna failed to take a new aim at EUR/CZK 25 with current euro momentum on the back of fiscal-driven growth prospects overturning such move.

Canadian employment was virtually unchanged in February with the economy adding 1.1k jobs. Consensus hoped on a stronger, 20k, net job creation. Details moreover showed gains in part-time employment (+20.8k) compensating for losses in full-time occupations (-19.7k). Employment increased in wholesale and retail trade (+51k) as well as finance, insurance, real estate, rental and leasing (+16k). There were declines in professional, scientific and technical services (-33k) and transportation and warehousing (-23k). Both employment (61.1%) and unemployment rate (6.6%) held steady. The latter occurred against a drop in the labour force participation rate from 65.5% to 65.3%. Average hourly wage growth accelerated from 3.5% Y/Y in January to 3.8%. The Loonie extends this week’s roller-coaster ride against the US dollar caused by the on-off tariff announcements by the US. The combination of good US payrolls and weaker Canadian ones, lifts USD/CAD from 1.4290 to 1.4360.

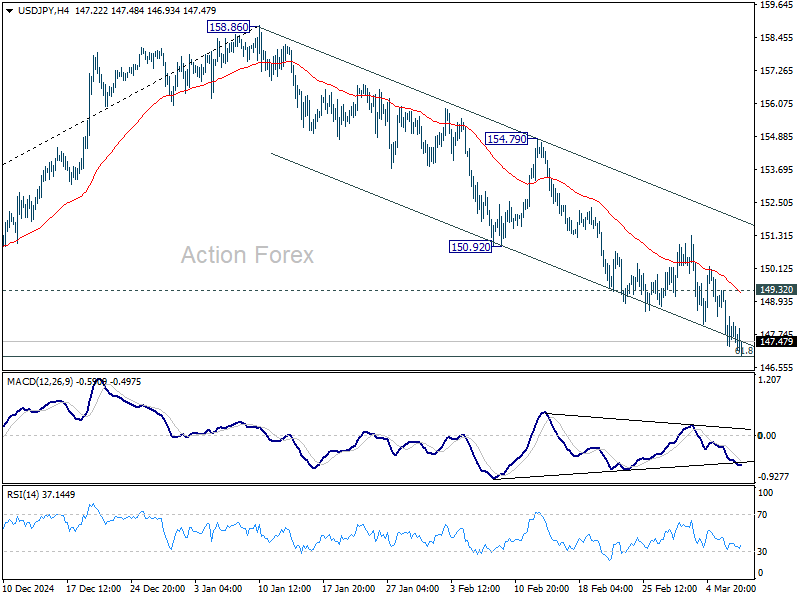

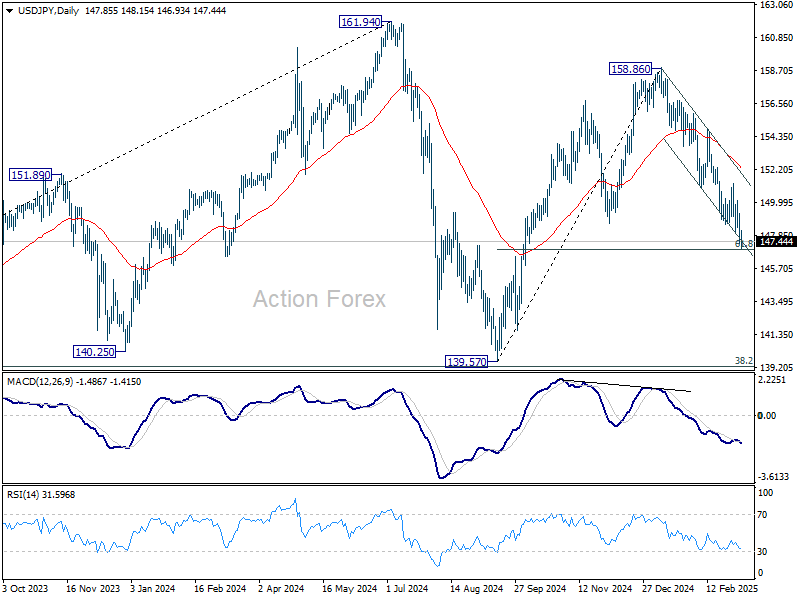

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.09; (P) 148.21; (R1) 149.11; More...

No change in USD/JPY's outlook and intraday bias stays on the downside. Fall from 158.86, as the third leg of the corrective pattern from 161.94 high, is in progress for 61.8% retracement of 139.57 to 158.86 at 146.32. Sustained break there will pave the way back to 139.57 low. On the upside, 149.32 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another fall.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

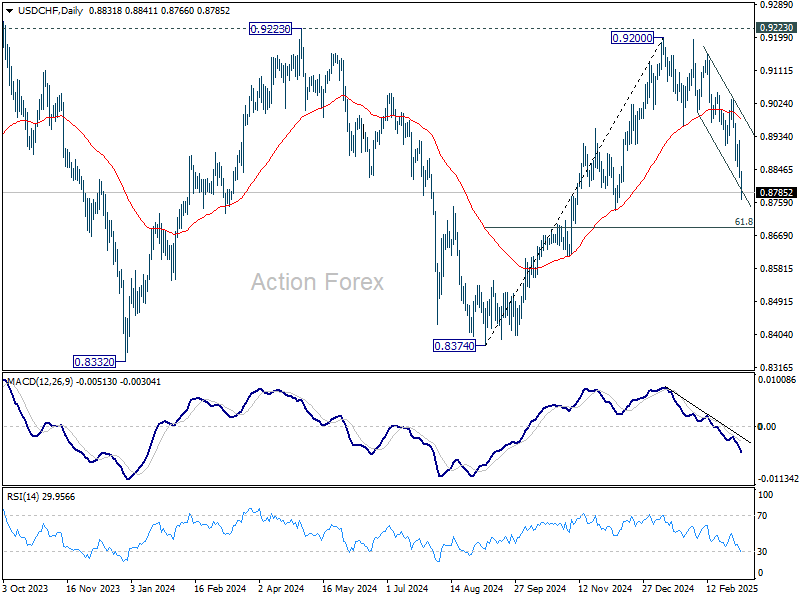

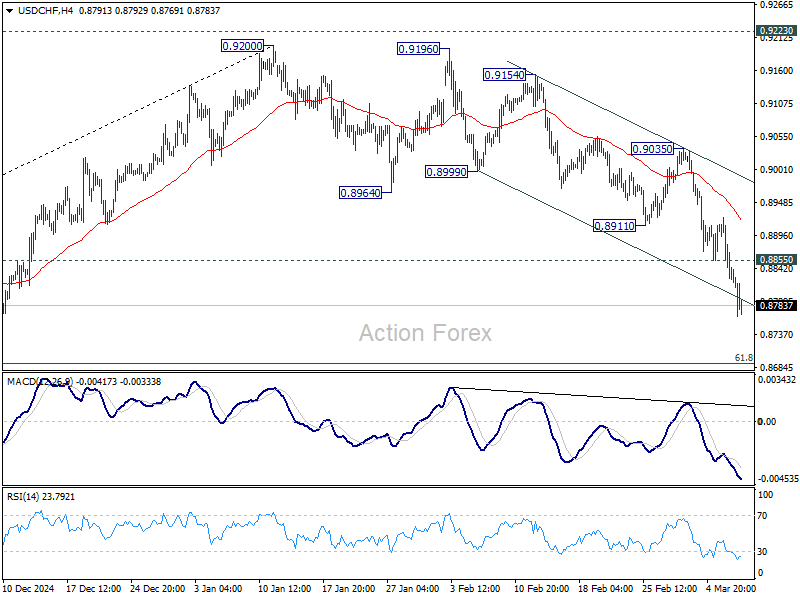

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8800; (P) 0.8863; (R1) 0.8900; More…

No change in USD/CHF's outlook and intraday bias stays on the downside. As noted before, rise from 0.8374 should have completed at 0.9222, after rejection by 0.9223 key resistance. Deeper fall should be seen to 61.8% retracement of 0.8374 to 0.9200 at 0.8690 next. On the upside, above 0.8855 minor resistance will turn intraday bias neutral first. But rise will stay on the downside as long as 0.9035 resistance holds, in case of recovery.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.