Sample Category Title

Elliott Wave View: DXY Extended Correction As Triple Three

DXY Short Term Elliott Wave view suggests that the decline to 88.44 ended Intermediate wave (3). Up from there, correction in Intermediate wave (4) is in progress as a triple three Elliott Wave structure. Rally to 89.64 ended Minor wave W, decline to 88.55 ended Minor wave X, Minor wave Y ended at 90.03 and Minor second wave X ended at 89.48. Near term, while pullbacks stay above 89.48, Index has scope to extend higher to 90.67 – 90.95 area to end wave Z of (4) before the decline resumes. We don’t like buying the Index and expect sellers to appear from the above area for a 3 waves pullback at least

DXY 1 Hour Elliott Wave Chart

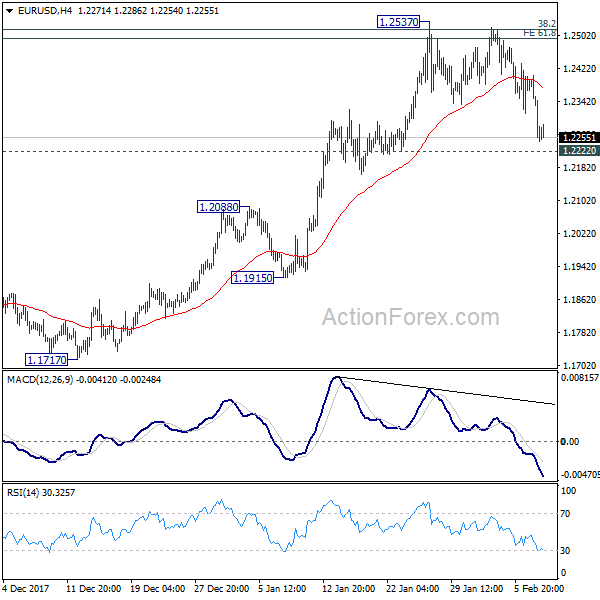

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2204; (P) 1.2305 (R1) 1.2364; More....

EUR/USD drops to as low as 1.2245 so far. Downside acceleration as seen in 4 hour MACD is raising the chance of trend reversal. But we'd prefer to see decisive break of 1.2222 support to confirm. Sustained break of 1.2222 will indicate rejection from 1.2494/2516 key fibonacci level, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 1.2091 resistance turned support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

New Zealand Dollar Tumbles on Neutral RBNZ, Dollar Picking Up Momentum

The global markets turned into consolidative mode, digesting recent losses. DOW attempted to rebound to 25293.96 but closed down -0.08% at 24893.35. Nikkei is trading up 0.35% at the time of writing but lacks follow through momentum. An important development to watch is that 10 year yield closed sharply higher by 0.076 at 2.845. Monday's high at 2.862 is now back in radar. And a strong break there will release recent up trend in yields, and could prompt another round of selloff in stocks. In the currency markets, Yen remains the strongest major currency for the week and is back pressing this week's low against Europeans. Dollar follow as the second strongest and has picked up from momentum overnight. New Zealand Dollar trades broadly lower after RBNZ stands pat and maintained a neutral stance. The Kiwi is so far the weakest one for the week.

RBNZ stands pat and maintained neutral stance

RBNZ left the Official Cash Rate unchanged at 1.75% today as widely expected. Kiwi tumbled as the central bank maintained a dovish stance. The accompanying statement noted that "monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly." RBNZ Governor Grant Spencer tried to talk down the recent global stock market crash.. He said in the press conference that "the bond market didn't really react, it's more of an equity market phenomenon. And now it's settled down, so that's not really going to have a long term effect." However, Spencer also warned that "it's been a warning sign because that volatility shows how nervous the market is about...the normalization of interest rates."

Separately, RBNZ Assistant Governor John McDermott said in a Reuters interview that "Core inflation is sitting a little bit below the midpoint... it still needs a little shove to get it towards the midpoint. That strategy hasn't changed." He reiterated RBNZ's "neutral stance". And he added that "there is a significant probability that the next rate move could be an increase sometime in the future, and there's also a substantial probability that the next move could actually be a cut."

Following up on NZD/USD, the decline from 0.7435 short term top extends to as low as 0.7181 so far today. It's on track to 55 day EMA (now at 0.7170). Sustained break there will confirm completion of the rebound from 0.6779 and pave the way to retest this low. Overall, medium term range trading is expected to continue inside 0.6779/7557 for a while.

Fed Williams: Economy can clearly handle gradual hikes

San Francisco Fed President John Williams said yesterday that "the economy clearly can handle gradually rising interest rates." And, he's "not really worried about the downside risks of the economy slowing too much." Also, regarding recent market crash, Williams said " I don't see any of the movements in asset prices of late to fundamentally change my view of the economy." He reiterated his expectation for three or four interest rate hikes this year. Chicago Fed President Charles Evans said that rising wages and inflation expectations suggested that inflation might be on the up. And, "if we get to that point and have more confidence that inflation is moving up sustainably, then further rate increases would be warranted,"

German grand coalition reformed

German Chancellor Angela Merkel formally announced the reformation of grand coalition yesterday, after marathon negotiation with SPD. Merkel said in a press conference that the agreement would create "the good and stable government that our country needs and that many in the world expect from us". Martin Schulz will step down as SPD leader and enter the government as Foreign Minister. Schulz is known for his pro-EU stance and his push for turning EU into a "United States of Europe". Another SPD member Olaf Scholz will likely take up the job of Finance Minister. But some analysts noted that Scholz is in the liberal wing of SPD and he's not too different from Wolfgang Schaeuble.

BoE Super Thursday: Voting and forecasts to watch

BoE rate decision and Inflation Report will be the biggest focus of today. There are rising speculations that BoE could pull ahead the next rate hike, to as soon as May. Traders will be very eager to get any hints on that. The vote split will be the first thing to watch. Markets generally expect an unanimous vote to keep interest rate unchanged at 0.50%. Any dissent and push for hike will show some impatience in the MPC. And, if someone would dissent, known hawks Ian McCafferty and Michael Saunders will be the likely candidate.

The Inflation Report will also bear much significance. Back in November, BoE projected 2018 GDP growth to be at 1.7%, CPI to slow to 2.4% and Bank Rate to be at 0.7% by the end of the year. There could be an upgrade in growth forecast as Brexit negotiation has finally entered into the second phase. But the key will be on whether BoE still expect CPI to slow from current 3.0% to 2.4%. And just a slight change in rate forecast could prompt much volatility in the Pound.

On the data front

Japan current account surplus narrowed to JPY 1.48T in December. China trade surplus narrowed sharply to CNY 136b, or USD 20.3b in January. Australia NAB business confidence dropped to 6 in Q4. German will release trade balance in European session while ECB will release monthly bulletin. Later in the day, Canada will release housing starts and new housing price index. US will release jobless claims on a Thursday as usual.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2204; (P) 1.2305 (R1) 1.2364; More....

EUR/USD drops to as low as 1.2245 so far. Downside acceleration as seen in 4 hour MACD is raising the chance of trend reversal. But we'd prefer to see decisive break of 1.2222 support to confirm. Sustained break of 1.2222 will indicate rejection from 1.2494/2516 key fibonacci level, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 1.2091 resistance turned support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:50 | JPY | Current Account (JPY) Dec | 1.48T | 1.66T | 1.70T | |

| 0:01 | GBP | RICS House Price Balance Jan | 8.00% | 5.00% | 8.00% | |

| 0:30 | AUD | NAB Business Confidence Q4 | 6 | 7 | 8 | |

| 2:00 | CNY | Trade Balance (CNY) Jan | 136B | 325B | 362B | |

| 3:45 | CNY | Trade Balance (USD) Jan | 20.3B | 54.9B | 54.7B | |

| 5:00 | JPY | Eco Watchers Survey Current Jan | 53.6 | 53.9 | ||

| 7:00 | EUR | German Trade Balance Dec | 21.0b | 23.7b | ||

| 9:00 | EUR | ECB Economic Bulletin | ||||

| 12:00 | GBP | BoE Rate Decision | 0.50% | 0.50% | ||

| 12:00 | GBP | BoE Asset Purchase Target Feb | 435B | 435B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--0--9 | 0--0--9 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | ||

| 12:00 | GBP | BoE Inflation Report | ||||

| 13:15 | CAD | Housing Starts Jan | 211K | 218K | ||

| 13:30 | CAD | New Housing Price Index M/M Dec | 0.20% | 0.10% | ||

| 13:30 | USD | Initial Jobless Claims (3 FEB) | 236K | 230K | ||

| 15:30 | USD | Natural Gas Storage | -99B |

USD/CAD Poised To Gain Bullish Momentum

Key Highlights

- The US Dollar traded higher this week and moved above 1.2400 against the Canadian Dollar.

- There was a break above a major declining channel with resistance at 1.2380 on the 4-hours chart of USD/CAD.

- The Building Permits in Canada in Dec 2017 increased 4.2%, more than the forecast of +2.0%.

- A lot of high risk events are lined up today, including German Trade Balance, BoE interest rate decision, Canadian Housing Starts and US Initial Jobless Claims.

USDCAD Technical Analysis

There were solid gains in the US Dollar from the 1.2250 swing low against the Canadian Dollar. The USD/CAD pair is back in a bullish trend with a close above 1.2400.

Looking at the 4-hours chart of USD/CAD, the pair formed a major support near 1.2250 and started an upside move. It gained a lot of momentum and broke a major declining channel with resistance at 1.2380.

There was also a close above the 1.2400 resistance and the 100 simple moving average (red, 4-hours). The upside move was strong and the pair traded as high as 1.2567. Later, a downside correction was initiated and the pair tested the 23.6% Fib retracement level of the last wave from the 1.2248 low to 1.2567 high.

It seems like the pair is back in a bullish trend and dips towards 1.2460 and 1.2400 remain supported. On the upside, a break above the 1.2560-70 zone could trigger a push above the 1.2600 level.

On the downside, an immediate support sits at 1.2480, followed by 1.2460 and 1.2400.

Canada's Building Permits

Recently, the Canadian Building Permits report for Dec 2017 was released by Statistics Canada. The forecast was slated for an increase of 2.0% in Dec 2017 compared with the previous month.

The actual result was much better as there was an increase of 4.8%, but there no major downside reaction in USD/CAD. Overall, the greenback is gaining bullish momentum.

EUR/USD broke a major support at 1.2400 and GBP/USD declined below the 1.4000 pivot level. However, the US Dollar is still struggling to move higher versus the Japanese Yen, as USD/JPY is trading below the 110.00 level.

There are many important and high risk events lined up during the European and NY session, including German Trade Balance, BoE interest rate decision, Canadian Housing Starts and US Initial Jobless Claims. Therefore, there could be swing moves in pairs such as EUR/USD, GBP/USD, USD/CAD and EUR/GBP.

Market Morning Briefing: Euro Has Seen A Test Of Support Near 1.2275

STOCKS

Dow (24893.35, -0.08%) moved up to test almost levels near 25500. Near term is likely to see some ranged-trade in the 25500-24000 region. A break above 25500 if seen over today and tomorrow could take the index higher towards 26000.

Dax (12590.43, +1.60%) moved up from 12200 but a rise above 12700 is needed to take the index to higher levels in the near term. While below immediate resistance near 12700, there could be another chance of a fall back towards 12400-12300.

Nikkei (21700.94, +0.26%) may move up towards 22600 while important support near 21000 holds in the coming sessions. Near term looks ranged to bullish while above 21000.

Shanghai (3282.74, -0.80%) broke below the channel support seen on the 3-day candles. If the index comes back above 3300, then it could move up towards 3450 in the near term; else a fall towards 3250 or lower looks likely while below 3300.

Nifty (10476.70, -0.21%) and Sensex (34082.71, -0.33%) came off in the second half of the session yesterday to close at lower levels. Weakness in the indices may not have ended yet but while it remains in a pause mode just now, we may look for a re-test of 10380 and 33750 levels again. Watch price action near mentioned support levels.

COMMODITIES

Brent (65.36) and WTI (61.62) are down sharply. Brent has broken below immediate support level while WTI is testing one just at current level. A bounce if not seen immediately could lead to further fall in the crude prices to 64 and 60 respectively.

Gold (1313.64) has come off below 1320 and may now be headed towards 1300 in the next couple of sessions. 1280-1300 is an important near term support region which is likely to hold and produce a bounce back in the medium term. View is bearish for the coming sessions.

Copper (3.1180) broke sharply on the downside indicating more of upcoming bearishness in the price. The fall is likely to continue and price could move down towards important long term support near 3.05. That if holds could thereafter produce a bounce back to higher levels in the longer run.

FOREX

As per expectation, Dollar Index (90.244) has moved past 90 and has been trading in the 90.2-90.4 range. There should be some resistance just below 91 as seen on the daily candles and weekly line charts. A test of 91 could however be postponed to next week.

Euro (1.2278) has seen a test of support near 1.2275 (on the weekly candles) earlier than expected. It is however still to be seen if this acts as a decent support or not. There is lower support near 1.22 on the 3 day line chart and near 1.215-1.22 on the daily candles, which could prove to be strong support levels leading to a bounce.

Dollar-Yen (109.34) seems to be struggling to move up beyond 109.5 as 21-day and 13-day moving average lines on the daily line chart continue providing some resistance. On the weekly line chart, it might again come down to test support near 108.5, which is an important level. Near term for Dollar Yen looks bearish for now and further directional clarity might come about in the next few days.

Euro Yen (134.25) dropped to levels near 133.87 but is again trading above 134, indicating that support near 134 on the daily, 3 day and weekly candles might hold for some more time. However, if Euro goes down towards 1.22 without Dollar Yen breaking below 108.5, Euro Yen could break this support at 134.

Pound (1.3894) has been on a downtrend for the last 5 days and as mentioned yesterday, could test support near 1.36-1.37 on the daily candles in a week’s time.

Dollar Rupee (64.28) is likely to remain ranged within 64.30-64.00 region this week. Only on a break above 64.30, we may consider a re-test of 64.40/45 on the upside.

INTEREST RATES

US 10 Year Yield (2.7865), US 30 year Yield (3.0592), US 5 year yield (2.5227), US 2 year yield (2.0930) have again moved up after the dramatic fall yesterday. However we might see all of them stay below 2.85, 3.15, 2.6 and 2.2 respectively as there are long term resistances near those levels. The global equity selloff in favour of safer debt is still underway and we might have to wait and watch till we are certain of a narrower range in which US yields could move for the next few days. The volatility phase might just be ending for now. The next rate hike is supposed to be in March when the volatility could again return.

Japan 10 year yield (0.081) continues its oscillation between the broad 0.07 and 0.088 level which might continue for now.

Canadian Dollar Risks Mount

USD/CAD is in the midst of a second week of gains and with two important events before the weekend, the highs of the year are within reach. The yen was the top performer on Wednesday while the New Zealand dollar lagged. The RNBZ left rates unchanged in early Asia-Pacific trade. The EURUSD trade was allosed to be stopped out. A new short in a key equity index has just been posted to susbcribers. Dow futures are currently -260 pts. S&P500 futures -26 pts.

The market remained jittery on Wednesday and that's likely to continue for some time. After spending most of the day in positive territory, the S&P 500 closed 0.5% lower and full further after hours. Recoveries are rarely V-shaped unless central banks or governments take dramatic action.

What's increasingly clear is that the FX market has been shaken out of its recent paradigm and the dollar is a beneficiary. We need only to look to the bond market to see why. Yesterday we highlighted the quick rebound in yields after the VIX-termination. More evidence came in a soft Treasury auction Wednesday and another 3.4 bps rise in yields. It's difficult to envision a scenario when 10s aren't trading at 3% soon.

One spot where the dollar is having success is against commodity currencies. Oil slid Wednesday after a 300K jump in US production to above 10mbpd for the first time since the 1970s. The US is now producing more oil than Saudi Arabia – something that's sure to irk OPEC, and something that threatens the recent oil climb.

That makes the Canadian dollar particularly vulnerable. What adds to that vulnerability is the uncertainty of the path of the BOC. Some clarity might come on Thursday in a speech from Wilkins that will be watched very closely. The market is pricing in a 22% chance of a March hike and a 56% chance in April.

Two critical factors determining BoC hikes are NAFTA discussions late this month and and Friday's Canadian jobs report. The prior two reports were sensational but a minimum wage hike and some mean revisions are downside risks to the +10K consensus.

A near-term level to watch in USD/CAD is 1.2620, which is the confluence of the 55 and 100 DMAs.

Another commodity currency to watch is NZD. The RBNZ left rates at 1.75% and added a note to the statement saying inflation is projected to remain subdued through the forecast period. Spencer also said he expected the kiwi to weaken.

Market Jitters Remain

Market Jitters Remain

US stocks toppled again on Wednesday in choppy and messy fashion after a dispirited US Treasury auction revived concerns about a hawkish Fed, unnerving investors already spooked after the rapid climb in US Treasuries apparently ignited a jump in the Cboe Volatility index.

A deplorable auction with meek demand pushed yields on 10-year US Treasuries to 2.84 percent, up four basis points, with traders now eyeing Monday’s a four-year high of 2.88 percent.

The market is now hedging against the Fed potentially leaning more hawkish which is explaining the uptick in USD and US yields.

There was a glimmer of hope earlier in the NY session that equities markets were finding a happy medium, but the equilibrium shattered as optimism gave way to more selling when Federal Reserve Doves see the inflationary lightbulb flicker.

Fed Evans, who dissented along with Kashkari on the December rate hike, has also embraced Kashkari’s new hawkish tone post-Friday’s earnings data. While his baseline remains a hold in rates until mid-year but with on crucial commonition: “In contrast, suppose inflation picks up more assuredly, as many expect. Then, we still could easily raise rates another three or even four times in 2018 if that were necessary. And I would support such a faster pace if the data point convincingly in this direction.”

Of course, this hawkish Fed discourse has elevated market chatter this morning centring on how the Trump Administration could react if the USD parades higher on a more hawkish Fed. It certainly makes for exciting international intrigue to the debate in the wake of comments from ECB member Nowotny who charged that the US Treasury is deliberately putting pressure on the USD

Oil Prices

Oil prices have been getting battered by forces beyond the nodding donkey of late. The weaker narrative has been underpinning prices, but with the market shifting to a more hawkish fed description the US dollar slide has come to a blunt halt is now weighing negatively on oil prices. Notwithstanding the unforeseen disorder in the broader financial system has seeped into the oil markets.

With Oil prices ones WTI fell abruptly after the U.S. government reported crude stockpiles rose by 1.9 million barrels. But its the deluge US production that remains the most significant menace to OPEC production cuts. The bottom line is the US crude production should keep hitting new highs throughout 2018 after reaching an all-time higher of 10.25 m barrels per day. 11’s are not that far away.

Gold Prices

Stronger US dollar and higher US Treasury yields have depressed demand for Gold overnight. And with equities souring and with prices continuing to melt away, gold markets could be susceptible to a stock market rebound.

The shifting Fed narrative that is gathering hawkish following could be the most significant thorn in the Gold Bulls side.

Currency Markets

Japanese Yen

The Yen will be traded like a puppet whose strings are manipulated by equities and fixed income price movements.

Australian Dollar

The risk-off moves from Monday’s equity plunge were enough to liquidate short USD and with continued broad de-risking assignments still being played out. I suspect the Aussie bulls with remain in time out corner until we get back above .7850 and a fraction of risk appetite returns. When you view every possible trade scenario as an ambush, probably best to tread cautiously.

The Malaysian Ringgit

The re-emergence of the Federal Reserve Board Hawks and Oil prices looking very susceptible to ramped up US shale oil production continues to weigh negatively on the MYR.

But indeed, the uptick in market volatility has tamed investors appetite, so bullish signals are far and few between

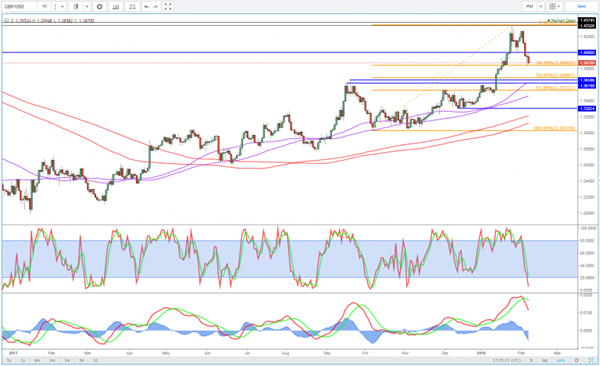

Are BoE Interest Rate Expectations Too Bullish?

BoE to Release New Economic Forecasts Alongside Rate Decision

The Bank of England holds its first monetary policy meeting of the year this week, after which it will release the quarterly inflation report alongside its monetary policy decision and hold a press conference with Governor Mark Carney.

The event - which is often referred to as 'Super Thursday' - is one of the most hotly anticipated of the UK calendar as it offers significant insight into the thoughts of the Monetary Policy Committee, something that's become increasingly sought after since it started raising interest rates in November.

BoE policy makers took the decision to raise interest rates after inflation surpassed 3% in November, a level deemed by many to be too high despite being driven by one-off currency moves in the aftermath of Brexit. This is led many economists to forecast another hike this year and two more over the three forecasting period, but have they and others been misled by the central bank?

In many ways, the dilemma facing the BoE is no different than that facing other central banks - the economy is growing, unemployment is very low, labour market slack appears low and yet inflation is stubbornly low - but one very important difference exists, Brexit.

The sheer amount of uncertainty that exists because of Brexit has resulted in low growth compared to its peers and its pre-referendum levels, businesses are reluctant to invest and the consumer squeeze is taking its toll. The economy may well have shown more resilience than many feared prior to the referendum but is this really the kind of environment that the central bank should be raising rates in? If not, why did they raise by 25 basis points in November?

The central bank will naturally point to the above target inflation as warranting a hike which would be fair, assuming they believed it would remain at those levels of exceed it, which is debatable. This would also indicate a willingness to raise more if inflation remains well above target. While it's likely to have peaked, it's not expected to fall very far for a while which is why people may be anticipating further hikes.

Another possibility could be that they wanted to reverse the emergency post-Brexit rate cut which many Brexiteers criticized at the time and some others have questioned the need for since. Especially when you consider that the central bank was reluctant to move below 0.5% throughout the aftermath of the global financial crisis and eurozone debt crisis. If lower rates were seen as risky or unnecessary then, can they possibly be warranted now? If not and this was behind November's decision, are the markets wrong in anticipating another hike this year and more after?

This could become a lot clearer in the coming meetings and Thursday should offer some early insight, particularly as the inflation report includes growth and inflation forecasts. Any indication that policy makers are in no rush to raise again could see markets pare back expectations resulting in lower yields on UK debt which could in turn weigh on the pound. We may not get this on Thursday though, assuming we do at all, as they may opt to gradually soften their stance over a number of meetings, particularly if Brexit negotiations aren't progressing as planned. Ultimately, these will have a major bearing on how interest rates move over the three year forecast period.

The FTSE 100 may also be sensitive to the BoE event on Thursday, given its inverse relationship with the pound. A stronger pound has typically weighed on the index due to the external exposure of the companies that make up the index, while a weaker pound has been positive for it, as seen in the aftermath of the referendum. It's been a rough couple of weeks for the FTSE, the last couple of days in particular as volatility has returned in force and equities have been sent into a tailspin lower. A strengthening pound - should the BoE release bullish forecasts and adopt a hawkish tone - may not help matters.

Gold Slides To 4-Week Low As Stock Markets Settles Down

Gold has posted losses in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1318.19, down 0.47% on the day. On the release front, there are no major US events on the schedule.

It's been a volatile week for stock markets across the world, and this has triggered strong movement in gold prices. A massive sell-off on Monday sent spooked investors looking for safe assets, boosting gold prices. A key factor in the stock market slide was strong employment numbers on Friday, as nonfarm payrolls and wage growth reports beat their estimates. Investors shied away from the stock markets, concerned that the sharp data could lead to higher inflation. This in turn would result in more rate hikes this year, making the dollar more attractive at the expense of gold and other currencies. However, US markets quickly recovered, posting gains on Tuesday and Wednesday. With risk appetite returning, gold has become less attractive, and is trading at its lowest level since January 11.

Jerome Powell was probably hoping for a quiet start at his new job as chair of the Federal Reserve, but the stock markets had other plans. Powell, who took over on Saturday, was greeted by the largest one-day drop ever on the Dow Jones on Monday, as US stock markets nosedived. Some analysts went as far as attributing some of the losses on the changing of the guard at the Fed, but this appears unlikely, given that Powell is expected to follow Janet Yellen's policies. This sentiment was echoed by on Tuesday by St. Louis Federal Reserve President James Bullard, who said that he does not think that policy will change appreciably under Powell.

Pound Under Pressure, BoE Rate Decision Next

The British pound is lower on Wednesday, as the currency has been under pressure for most of the week. In the North American session, GBP/USD is trading at 1.3883, down 0.48% on the day. On the release front, British Halifax HPI declined 0.6%, below the estimate of +0.2%. This marked the first decline since June. There are no US releases on the schedule. On Thursday, the US releases unemployment claims.

It’s been a rough week for the pound, which started the week with losses and has shed 1.6%. The US dollar has posted gains against the pound and the other majors, after a massive sell-off on global stock markets on Monday. The sell-off was precipitated by strong US nonfarm payrolls and wage growth reports on Friday. This triggered concerns that higher inflation was on the way, which in turn would result in more rate hikes this year. Higher interest rates make the dollar more attractive for investors, at the expense of other currencies. Although global stock markets have settled down, concerns remain that inflation could move higher after years of being AWOL across industrialized countries, and could again spook the markets.

The spotlight will be on the Bank of England on Thursday, as the bank sets the benchmark rate and releases the Inflation Report. The markets will be also be keeping a close eye on the Inflation Letter, which Governor Mark Carney is required to write due to inflation being more than 1% off the target of 2.0% (CPI is currently running at a 3.1% clip). Carney will address what the Bank is doing to lower inflation, and higher interest rates is one remedy, but one that Carney will hope to avoid, given the economic uncertainty surrounding Brexit. The BoE is expected to hold current rates at 0.50%, and all nine members of the Monetary Policy Committee are expected to support this move. If some members vote in favor of a rate hike, the pound could respond with gains.