Sample Category Title

Equity and Crypto Pain Persists

Tuesday February 6: five things the markets are talking about

The global equity rout extended overnight as Asian and European markets followed Wall Street and tumbled, sending equity indexes toward the biggest three-day slide in nearly three-years.

Volatility in stocks has pushed a number of investors to unwind equity bets and head to the 'mighty' dollar and the Japanese yen, another haven.

The dollar has also been benefiting from last Friday's robust U.S employment data. However, despite the greenbacks recent gains, the prospect of faster-than-expected monetary policy tightening abroad has left the buck atop of its lowest level outright in more than three-years.

Note: Yesterday, the VIX saw its biggest daily climb ever, both in percentage and absolute terms.

1. Stocks markets tumble again

Yesterday, U.S. stocks plunged the most in more than six years and volatility roared back into the market as the S&P 500 sank -4.1%.

In Japan, stocks suffered their biggest point drop in 18-months overnight on fears about rising U.S bond yields and a potential pick-up in inflation. The Nikkei share average ended down -4.73%, while the broader Topix fell -4.4%.

Down-under, Australia's S&P/ASX 200 traded at levels last seen in October as it slide -3%, while S. Korea's Kospi was the outperformer in dropping just -1.8%.

In Hong Kong, stocks joined the market rout intensified. The benchmark Hang Seng Index plummeted -5.1%, its biggest daily percentage drop since August 2015, while the China Enterprises index HSCE fell -5.9%.

Note: Hong Kong is particularly exposed to U.S rate moves because the HKD is pegged to the U.S dollar.

In China, Shanghai stocks post their worst day in two-years. The Shanghai Composite Index slumped -3.4%, its biggest single-day drop since February 2016, while the blue-chip CSI300 index ended down -2.9%.

In Europe, regional equities move well off its opening levels, but remain in negative territory as U.S futures stage a sharp turn around. Earnings continue to dominate corporate news.

U.S stocks are set to open in the black (+0.6%).

Indices: Stoxx600 -1.9% at 374.8, FTSE -2.0% at 7191, DAX -2.2% at 12409, CAC-40 -1.9% at 5192, IBEX-35 -1.9% at 9884, FTSE MIB -1.5% at 22494, SMI -1.9% at 8927, S&P 500 Futures +0.6%

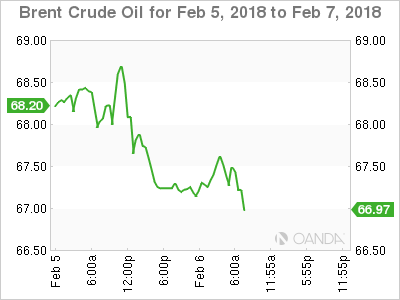

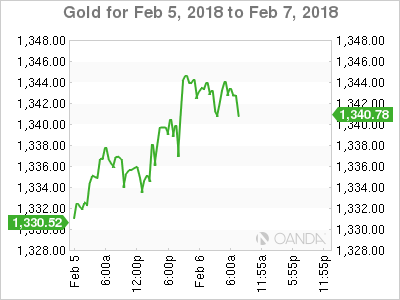

2. Oil prices ease, gold higher

Oil prices have fallen for a third consecutive session overnight, although the crude price remains in positive territory so far this year.

Oil is caught up in the markets general risk-off move and not helped by the strength of the U.S dollar in the past two trading sessions.

Brent crude futures are down -35c at +$67.27 a barrel, but still up +1% so far in 2018. U.S West Texas Intermediate (WTI) crude futures have eased by -25c to +$63.90.

Note: Since the S&P 500 hit a record high on Jan. 26, the index has lost -8%. Oil, in contrast, has lost -4.5%, while cryptocurrency bitcoin (BTC) has lost -50% of its value.

Adding to the pressure on oil, which hit its highest price in nearly three-years in January, has been evidence of rising U.S crude production, which could threaten OPES's efforts to support prices.

Data from the U.S government last week showed that output climbed above +10m bpd in November for the first time in nearly fifty-years, as shale drillers expanded operations.

Gold prices have rallied overnight as the global equity rout encouraged investors to seek shelter in safe havens, although expectations of more U.S rate hikes this year will weigh on the market. Spot gold is up +0.3% to +$1,342.95 per ounce, following yesterday's +0.5% gain.

3. Reserve Bank of Australia (RBA) on hold

The RBA overnight chose to stay out of the global shift among central banks toward higher interest rates, amid deep fears that domestic household debt burden would not stand up well to the pain of rising mortgage costs.

The RBA left its cash rate unchanged at a record low +1.5%, signalling no desire to follow the likes of the Fed, the BoE and the ECB in removing the policy accommodation.

Governor Philip Lowe said he remains hopeful that growth and inflation will trend higher this year, but stressed the big uncertainty is the outlook for consumers.

Elsewhere, investors have been dumping government debt, but for different reasons. In the U.S, investors see more inflation coming; while in the eurozone, they see stronger economic growth.

The yield on U.S 10-year Treasuries has increased +6 bps to +2.76%. In Germany, the 10-year Bund yield decreased -3 bps to +0.71%, while in the U.K, the 10-year Gilt yield has declined -3 bps to +1.53%, and the biggest drop in almost five weeks.

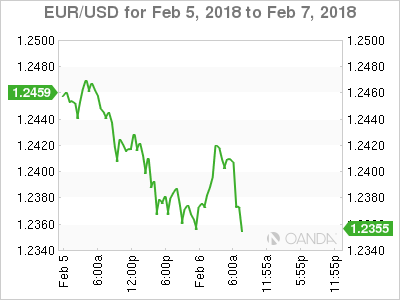

4. Dollar finds little traction

The USD remains on soft footing, unable to gather any safe-haven demand despite the pickup in global volatility.

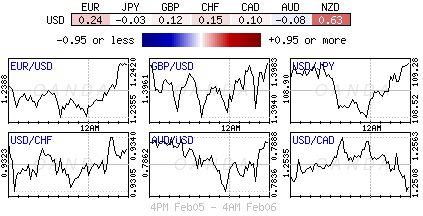

EUR/USD (€1.2400) continues to maintain within its recent consolidated range, €1.2350-1.25, supported by the market sentiment that the eurozone is expanding robustly with stronger growth rates than previously anticipated.

GBP/USD (£1.3935) remains on the defense, as U.K ministers seem to have a difference of opinion on the Brexit strategy.

USD/JPY 's strong correlation with U.S interest yields seems to have broken down as the pair tested ¥109 in the session overnight despite the BoJ's rhetoric that it would continue advocating an easy monetary policy.

Bitcoin (BTC) briefly traded below $6,000 overnight as weakness in digital tokens continued, with Ripple, Ether and Litecoin also tumbling at least -11%.

Note: The BIS said that central banks must be prepared to intervene to stem risks from digital currencies, as Bitcoin has become a "combination of a bubble, a Ponzi scheme and an environmental disaster."

5. German factory orders surge

Data this morning showed that German factory orders surged in December.

Orders, adjusted for seasonal swings and inflation, increased +3.8% after dropping a revised -0.1% in November. Demand was up +7.2% from the previous year.

The Bundesbank says the German economy will maintain its momentum. After growing +2.2% last year, GDP is forecast to increase +2.5% in 2018.

Note: Strong domestic spending and prosperous global trade is supporting Germany's economy. This has helped the country's largest union win a +4.3% pay increase over 27-months.

RBNZ Set To Maintain Neutral Tone, But Could Talk Down The NZD

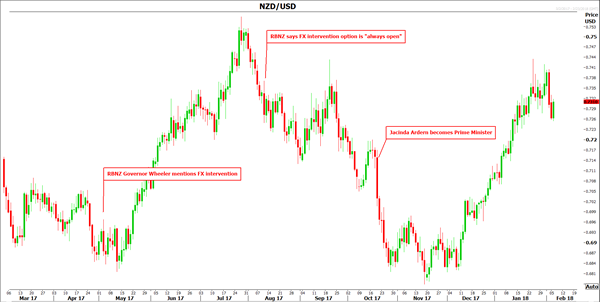

The Reserve Bank of New Zealand (RBNZ) will announce its rate decision on Wednesday at 2000 GMT, and the forecast is for no change in policy. Even though the Bank's cautiously optimistic bias is unlikely to change drastically amid mixed economic data, policymakers could still express their discomfort with the NZD's recent surge.

A lot has happened in New Zealand since the RBNZ's last policy meeting in November, and it will be very interesting to see how the Bank interprets recent developments. In late December, the nation's statistical service revised its GDP numbers for the previous years significantly higher, raising 2015 growth to 3.6% from 2.4% previously, and 2016 to 4.0%, from 3.0%. Hence, it appears that growth was much faster than what the Bank assumed in recent years. Does that mean the economy is closer to full capacity utilization (and thus higher inflation) than previously anticipated?

In terms of the latest releases, GDP growth was stronger than projected in the third quarter of 2017. However, business sentiment has collapsed recently according to most major surveys. In isolation, this presents a risk that the Bank could revise somewhat lower its near-term GDP forecasts. Turning to inflation, it surprisingly slowed in the fourth quarter, pouring cold water on expectations that the RBNZ could begin to signal rate hikes soon. The yearly CPI rate dropped to 1.6% from 1.9% previously; well below the Bank's own forecast of 1.8%.

As for the exchange rate, kiwi/dollar is 5.0% higher since the latest gathering. Importantly, it's now close to levels where the Bank previously threatened to intervene in the FX market to weaken the NZD, as a stronger currency may weigh on exports, growth and inflation. That said, policymakers may not go as far as warn of intervention this time. The broader surge in kiwi/dollar probably reflects more dollar weakness than kiwi strength, not to mention that the NZD has not appreciated nearly as much on a trade-weighted basis. Still, the RBNZ is unlikely to be happy with the whole situation, implying there is a decent probability that it could bring back the sentence it used in previous statements, that “a lower exchange rate is needed”.

All in all, the negatives seem to outweigh the positives, but not enough for the RBNZ to change its neutral policy language in a material manner. Nonetheless, it may well take the opportunity to jawbone the NZD a little. A statement that expresses discomfort with the exchange rate could weigh on kiwi/dollar, pushing it lower for a test of the 0.7230 support area. A clear break below that territory would open the way for the 0.7135 zone, marked by the lows of January 10.

On the other hand, should the Bank appear content about economic developments, or if it does not toughen its language around the exchange rate, then kiwi/dollar could surge. A decisive break above 0.7330 could set the stage for an extension of the upmove towards the round figure of 0.7400. After that, resistance may be found at 0.7435, marked by the peaks of January 24 and September 20.

Ahead of the RBNZ meeting, NZD-traders will also keep an eye out for New Zealand’s employment data for the fourth quarter, due out on Tuesday at 2145 GMT. Any potential surprise in these data – particularly on the wages front – could influence market expectations regarding the policy decision and thereby, impact kiwi/dollar ahead of the event.

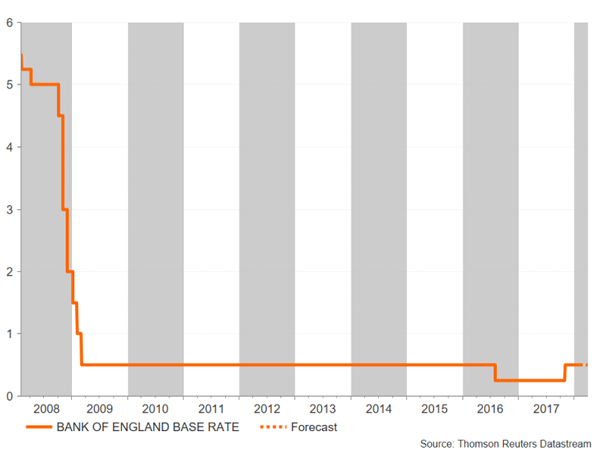

Bank Of England Could Flag Early Rate Hike But UK Political Risks Simmer

The Bank of England will hold a two-day monetary policy meeting this week – it’s first for 2018 – with the announcement expected on Thursday at 12:00 GMT. The Governor, Mark Carney, gave investors a peek as to what to expect from the Bank on ‘Super Thursday’ during a hearing before the House of Lords Economic Affairs Committee in Parliament last Tuesday. Expectations of a Spring rate rise have been rising since but growing unrest within the Conservative party, which has once more cast doubt about Theresa May’s future as prime minister, threatens to bring fresh chaos to the Brexit process.

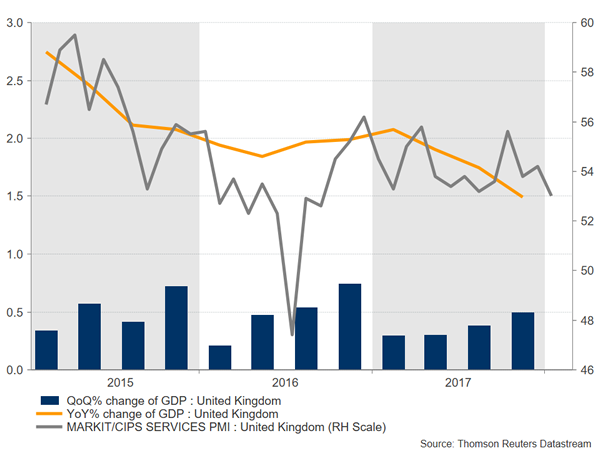

With no change in rates expected for the February meeting, all eyes will be on the Bank’s quarterly inflation report, which will contain revised forecasts on economic growth and inflation. Although the latest indications suggest the effects on prices from the pound’s depreciation after the Brexit referendum are diminishing, the Bank is concerned that inflation may not fall back towards the 2% target quick enough without any BoE action and that a tightening labour market could soon push up wage pressures.

Fourth quarter GDP figure, which came in above expectations at 0.5% quarter-on-quarter, and a surprisingly strong set of jobs data for the November period support the case for additional rate hikes by the BoE in the coming months. However, UK growth is still lagging most of its peers in the G7 and data released on Monday pointed to a weak start for the country’s dominant services sector. The IHS Markit services PMI fell far short of expectations in January, dropping from 54.2 to 53.0 – the slowest since September 2016.

The pound lost ground versus the dollar and the euro after the data, with cable moving away from last week’s high of 1.4277, when it rose on the back of expectations that the next increase in UK rates could come as early as May. However, renewed political risks added to sterling’s woes, pushing the currency to a two-week low of $1.3935 and to a three-week low of 0.8891 pounds per euro on Tuesday.

UK prime minister, Theresa May has come under heavy criticism from members of her own party over the past week for her ambiguous Brexit strategy and weak leadership, fuelling speculation of a possible vote of no confidence that would force her resignation. With time running out in the Brexit negotiations with the EU, and a looming March deadline for reaching an agreement on a transition deal, a leadership challenge couldn’t come at a worst time.

The question now is whether the Bank of England will stick to its increasingly hawkish rhetoric or return to a more cautious stance given the uncertainty still hanging over the UK’s economic outlook. In his remarks to Parliament last week, Carney sounded more confident about wages picking up in the next few years and said, “as slack in the economy has been taken out, we move into a more conventional area for monetary policy”. A stronger global economy and a weaker pound have improved the prospects for Britain’s economy, offsetting some of the impact from the slowdown in consumer spending and business investment.

However, the Bank may refrain from taking a too-hawkish tone in February in the event of a delay in reaching a Brexit transition deal in March, which would make a May rate hike difficult. Most economists still expect the BoE to wait until November before raising rates again but the shifting market expectations are generating volatility in sterling.

The strongest signal of a near-term rate increase that could emerge is if the Monetary Policy Committee (MPC) hawks, Ian McCafferty and Michael Saunders, vote for a rate hike on Thursday. This could drive the pound back above key resistance around $1.4120. But if the MPC vote unanimously to hold rates and the BoE’s latest economic projections are revised only modestly higher, sterling could struggle and fall below recent support at $1.3935, opening the way towards $1.3850.

DAX Slides As US Stock Markets See Red

The DAX index continues to lose ground this week. In the Tuesday session, the index is trading at 12,454.51, down 1.88% on the day. On the release front, German Factory Orders impressed with a gain of 3.8%, crushing the estimate of 0.6%. On Wednesday, Germany releases Industrial Production.

The DAX ended last week with losses, as a sharp decline in Deutsche Bank shares sent European stock markets lower on Friday. The DAX declined 4.2% last week, and the slide continues, as the index has shed another 2.4% this week. The Dow Jones posted its biggest loss in one day on Monday, losing 1,500 points at one stage. The index ended the day down 4.6%, and the downward trend has continued in the Asian and European markets on Tuesday. What happened? Some analysts are pointing to the changing of the guard at the Federal Reserve, with Jerome Powell replacing outgoing chair Janet Yellen on Saturday. However, Powell is not expected to change current monetary policy, so it’s unclear how Powell would have rubbed the markets the wrong way before uttering a word as head of the Fed.

More likely, the stock markets woes can be attributed to strong US nonfarm payrolls and wage growth reports, which were released on Friday. Investors fear that the sharp data could lead to higher inflation, which in turn would result in more rate hikes this year. Higher interest rates make the dollar more attractive for investors, at the expense of the stock markets. Adding to investors’ concerns, there are expectations that the ECB and possibly the Bank of Japan could raise rates late in 2018, which would push up the euro and yen and weigh on the stock markets.

The German economy continues to shine, despite the ongoing coalition negotiations, which have dragged on since September. A spokesman for the SPD party, which is negotiating with Angela Merkel’s conservative bloc, said on Tuesday that a deal is “90-95%” done. For her part, Merkel has said that she is willing to make painful concessions in order to form a government. Both parties have stated that they want to reach an agreement on Tuesday. If there is an announcement later in the day, the euro could move higher.

Euro Rebounds After Monday Losses, German Factory Orders Soar

The euro has posted gains on Tuesday, after starting the week with losses. Currently, the pair is trading at 1.2407, up 0.32% on the day. On the release front, German Factory Orders impressed with a gain of 3.8%, crushing the estimate of 0.6%. In the US, the key event of the day is JOLTS Job Openings, which is expected to climb to 5.95 million. On Wednesday, Germany releases Industrial Production.

The dollar kicked off the week with gains, after global stock markets posted sharp losses on Monday. The Dow Jones posted its biggest loss in one day, losing 1,500 points at one stage. The index ended the day down 4.6%. What happened? Some analysts are pointing to the changing of the guard at the Federal Reserve, although the new chair is not expected to veer off current monetary policy. More likely, strong US nonfarm payrolls and wage growth reports could lead to higher inflation, which in turn would result in more rate hikes this year. Higher interest rates make the dollar more attractive for investors, at the expense of the stock markets. As well, there are expectations that the ECB and possibly the Bank of Japan could raise rates late in 2018, which would push up the euro and yen and weigh on the stock markets.

In the US, January employment numbers were sharp, propelling the dollar to broad gains on Friday, as EUR/USD lost ground. Nonfarm payrolls, which is usually a market-mover, jumped to 200 thousand, beating the estimate of 181 thousand. Wage growth remained steady at 0.3%, edging above the estimate of 0.2%. The unemployment rate held steady at 4.1% for a fourth straight month. Will the strong numbers lead to additional interest rate hikes? Minneapolis Fed President Neel Kaskkari said on Friday that the Fed might need to be more aggressive if wages continued to move higher. The Fed is planning to raise rates three times in 2018, but some economists are forecasting four hikes. Either way, the Fed is expected to continue its monetary policy of incremental rates of 25 basis points, with the goal of not surprising the markets and preventing the robust US economy from overheating.

US Futures Pare Losses After Monday’s Plunge

- Markets Stabilise Ahead of the Open on Wall Street;

- Bitcoin Falls Below $6,000 For First Time Since November;

- No Room For Bitcoin When Traders Sought Safe Havens.

Markets Stabilise Ahead of the Open on Wall Street

US futures are gradually stabilising again ahead of the open on Wall Street on Tuesday, following an extremely volatile session at the start of the week and more of the same in overnight trade.

The sudden and sharp declines in equity markets over the last couple of sessions is still being attributed to higher interest rate expectations although the move appears to have been exacerbated by a combination of automated trading and panic selling. We've become so accustomed to dips being bought over the last couple of years that this appears to have caught people off-guard and that's generated some of the panic responses that we've seen.

Now that the dust appears to be settling, people seem to be reflecting on this as a reminder that market corrections are perfectly normal and not always a sign that something is about to go terribly wrong. The rally over the last couple of years has been very strong and without any corrections of note and it's possible that this has led to some complacency in the markets, with investors perhaps getting a little ahead of themselves.

Of course we'll have to wait and see over the next couple of days if the sell-off generates and further fear-driven selling but I'm not currently convinced it would be warranted. The economic fundamentals appear fine and the environment has been gradually improving over the last couple of years. This has led to higher interest rate expectations and it's possible that these have gone a little too far.

Bitcoin Falls Below $6,000 For First Time Since November

It's not just stock market investors that have been burned in recent days, cryptocurrency traders are also feeling the heat, as another plunge in bitcoin sees it trading back around $6,000, almost 70% off its December highs. Some other cryptocurrencies have fared even worse, with Ripple now more than 80% off its peak which was reached only a month ago. A constant flow of negative news flow hasn't helped the market for cryptocurrencies and neither, I would imagine, will the exit of speculators that helped inflation the bubble late last year.

Bitcoin has found some support again after dipping back below $6,000 earlier today for the first time since the middle of November. With cryptocurrencies being such a sentiment driven market, I wouldn't be surprised to see further losses even if prices do stabilise or even bounce in the near-term. Most cryptocurrencies are still up a considerable amount since the start of last year which some will point to as evidence that they have a lot further to fall and others as evidence of the belief that still exists in the space. Ultimately, we're seeing the market being flushed out which could prove handy in highlighting which players are serious and which simply piggybacked on the success of others.

No Room For Bitcoin When Traders Sought Safe Havens

Interestingly, despite the insistence of some that bitcoin could be the new Gold, we've seen little evidence of it benefiting from the recent panic. Gold on the other hand did see some safe haven flows late on Monday and is trading a little higher once again today. As is the yen, which is typically seen as a safe haven currency and is trading higher against the euro and pound today. It has pared its gains in the last few hours though as equity markets have pared losses.

EURUSD Analysis: Points To Slight Recovery After Fall

Contrary to expectations, the common European currency was dominated by bearish market on Monday. Following a minor period of consolidation between the 55– and 100-hour SMAs, the pair breached the latter together with the 200-hour SMA a few hours later.

This strong downside momentum resulted in the pair testing the weekly S1 and the bottom boundary of a two-month channel circa 1.2360 by Tuesday morning.

Converging technical indicators suggest that the pair should recover some losses in this session. Gains, however, are expected to be limited due to the combined resistance of the 200-, 100– and 55-hour SMAs and the weekly PP located near the 1.2440 mark. A reversal from the weekly S1 would likewise confirm a newly-formed ascending channel (dashed lines).

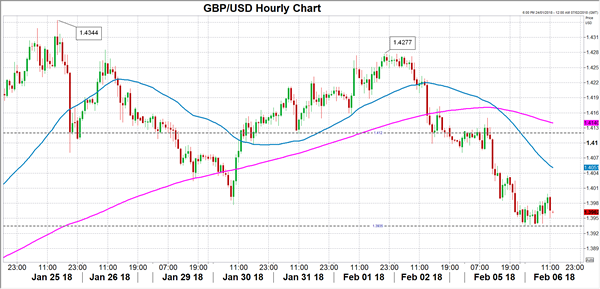

GBPUSD Analysis: Stops Near 38.20% Fibo

Bears have dominated GBP/USD for the second consecutive session. The slight recovery apparent on Monday morning was stopped by the 55-, 100– and 200-hour SMAs and the bottom boundary of a seven-week ascending channel circa 1.4150. As a result of this strong momentum south, the Sterling breached the monthly PP and was halted solely by the 38.20% Fibo near the 1.3950 mark.

Technical indicators are converging and are located in the strongly bearish territory, thus bulls might try to use this opportunity to push the rate higher. A possible upside target for today could be near 1.4150 where all the three moving averages are located.

In case bulls fail to move the rate above 1.40, a subsequent fall down to 1.3850 is likely.

USDJPY Analysis: Weak After Plunge

The US Dollar remained stable against the Yen on Monday until strong bearish momentum mid-session took over the market. As a result, the pair breached all three SMAs and the up-trend circa 109.00 and consequently plunged 1.04% throughout the day.

By Tuesday morning, the Greenback was showing some signs of recovery; however, it does face the previously breached support levels which have become strong resistance. Thus, it is likely that the pair remains tended southwards today.

The nearest support is set by the bottom line of a five-month descending channel located near the 108.00 mark. In terms of resistance, gains should be capped near 109.60.

XAUUSD Analysis: Stranded Between SMAs

After testing the bottom boundary of a two-month ascending channel late on Friday, Gold accelerated against the US Dollar, thus dashing through several important resistance areas, including the weekly PP and the 55– and 100-hour SMAs. On Tuesday morning, the rate was testing the upper boundary of a short term channel and the 200-hour SMA circa 1,345.10.

Technical indicators demonstrate that some upside potential still exists in the near term. In addition, the current positioning of the pair suggests that the junior channel should surrender under the bullish pressure, thus allowing the rate to breach the 200-hour SMA and the weekly R1 and approach its six-month high of 1,365.00. However, given the strength of the nearest resistance, the pair might consolidate for some time.