Sample Category Title

Brexit Battle Is Switching To Tackle Inflation, Says BoE’s Carney

For the 24 hours to 23:00 GMT, the GBP rose 0.72% against the USD and closed at 1.4148, after the Bank of England's (BoE) Governor, Mark Carney, stated that the central bank can now focus increasingly on combating inflation and bringing it near to its target, as the drag from the historic Brexit vote on the broader economy and investment has started to recede, with signs of a pick-up in wage growth as the labour market strengthens.

On the data front, UK's number of mortgage approvals for house purchases fell to a nearly 3-year low level of 61.0K in December, highlighting that housing market took a further hit after the BoE raised the key interest rate for the first time in a decade in November. In the previous month, mortgage approvals had registered a revised reading of 64.7K, while investors had expected for a drop to a level of 63.5K. On the other hand, the nation's net consumer credit rose £1.5 billion in December, beating market estimates for a rise of £1.4 billion. In the previous month, net consumer credit had registered a revised similar rise.

In the Asian session, at GMT0400, the pair is trading at 1.4177, with the GBP trading 0.2% higher against the USD from yesterday's close.

Overnight data revealed that UK's GfK consumer confidence index unexpectedly climbed to a level of -9.0 in January, confounding market anticipations for the index to remain steady at a level of -13.0. Additionally, the nation's Lloyds business barometer rose to a level of 35.0 in January, compared to a reading of 28.0 in the prior month.

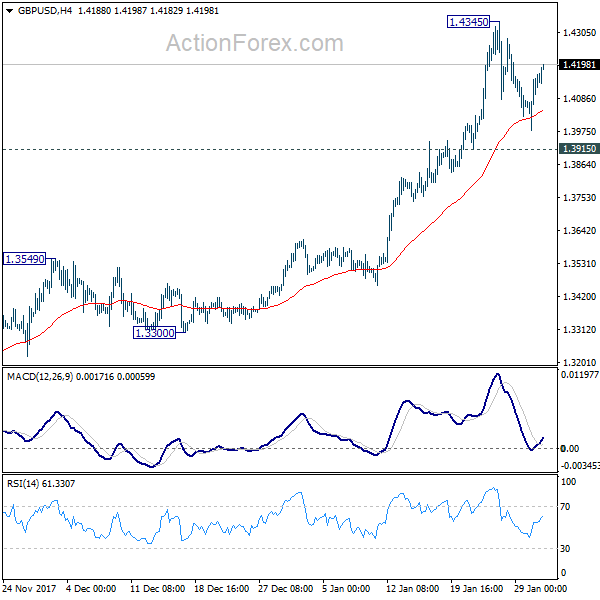

The pair is expected to find support at 1.4043, and a fall through could take it to the next support level of 1.3910. The pair is expected to find its first resistance at 1.4247, and a rise through could take it to the next resistance level of 1.4318.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Few Officials Call For Loosening Monetary Conditions In Future: BoJ Summary Of Opinions

For the 24 hours to 23:00 GMT, the USD declined 0.27% against the JPY and closed at 108.79.

In the Asian session, at GMT0400, the pair is trading at 108.89, with the USD trading 0.09% higher against the JPY from yesterday's close.

The Japanese Yen lost ground against the USD, after the Bank of Japan (BoJ) increased its buying of medium-term Japanese government bonds (JGBs).

Separately, according to the summary of opinions report from the BoJ's January monetary policy meeting, several policymakers shared the view that the central bank needs to consider hiking interest rates or scale-back purchases of risky assets, if Japan's economic fundamentals continue to recover. However, other board members believed that it was appropriate to stick to the central bank's current accommodative policy as inflation remains far from its 2.0% target.

On the economic front, Japan's preliminary industrial production advanced 2.7% on a monthly basis in December, compared to a gain of 0.5% in the prior month. Market anticipation was for industrial production to increase 1.5%.

The pair is expected to find support at 108.51, and a fall through could take it to the next support level of 108.13. The pair is expected to find its first resistance at 109.18, and a rise through could take it to the next resistance level of 109.47.

Moving ahead, Japan's final Nikkei manufacturing PMI for January, slated to release overnight, will be on investors' radar.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

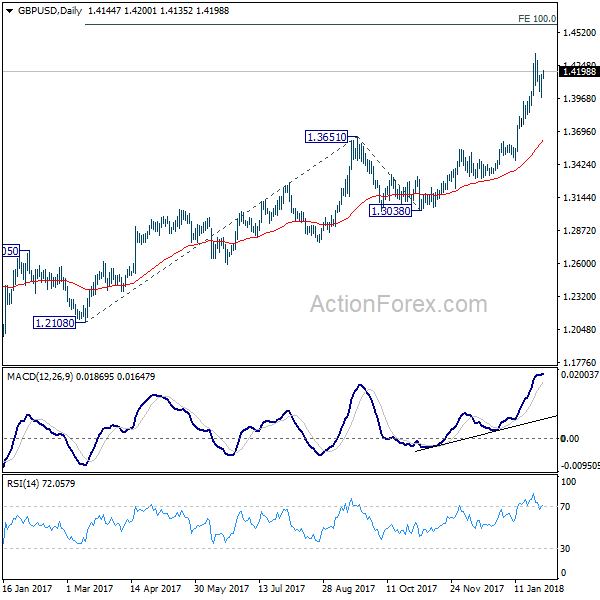

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4029; (P) 1.4098; (R1) 1.4216; More.....

GBP/USD is staying in consolidation below 1.4345 and intraday bias remains neutral first. More corrective trading could be seen. But downside should be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Swiss Trade Surplus Increased In December

For the 24 hours to 23:00 GMT, the USD declined 0.4% against the CHF and closed at 0.9347.

In economic news, trade surplus in Switzerland widened to CHF2.63 billion in December, after recording a revised trade surplus of CHF2.58 billion in the previous month.

On the contrary, the nation’s KOF leading indicator declined to a level of 106.9 in January, more than market expectations for a fall to a level of 110.8. The index had recorded a revised level of 111.4 in the prior month.

In the Asian session, at GMT0400, the pair is trading at 0.9338, with the USD trading 0.1% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9302, and a fall through could take it to the next support level of 0.9266. The pair is expected to find its first resistance at 0.9382, and a rise through could take it to the next resistance level of 0.9426.

Ahead in the day, traders would focus on Switzerland’s ZEW expectations index for January as well as the UBS consumption indicator for December.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Loonie Trading On A Stronger Footing, Ahead Of Canada’s GDP Data

For the 24 hours to 23:00 GMT, the USD declined 0.11% against the CAD and closed at 1.2337.

In the Asian session, at GMT0400, the pair is trading at 1.2318, with the USD trading 0.15% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2292, and a fall through could take it to the next support level of 1.2267. The pair is expected to find its first resistance at 1.2361, and a rise through could take it to the next resistance level of 1.2405.

Trading trend in the CAD today is expected to be determined by the release of Canada's GDP data for November, set to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

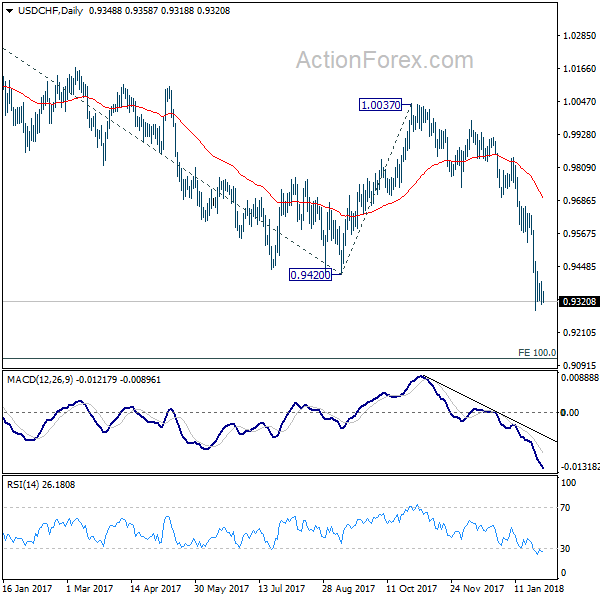

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9301; (P) 0.9347; (R1) 0.9384; More...

USD/CHF is staying in consolidation above 0.9288 temporary low. Intraday bias remains neutral first. But with 0.9536 resistance intact, outlook stays bearish and deeper fall is expected. Break of 0.9288 will resume the larger down trend and target next key fibonacci level at 0.9115.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 08545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.39; (P) 108.79; (R1) 109.18; More...

USD/JPY continues to stay in consolidation above 108.27 temporary low. Intraday bias remains neutral for the moment. As long as 110.18 resistance holds, deeper decline is expected. On the downside, break of 108.27 will extend recent fall through 107.31 support to next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Dollar Yawns Trump’s SoU Address, Decline Might be Resuming With FOMC Watched

The forex markets remain generally in consolidation mode today. US President Donald Trump's State of Union address provides little inspiration. Nonetheless, the soft tone of Dollar in Asian session suggests that it might be ready to resume recent decline, probably subject to FOMC statement. In other markets, DOW dropped -362 pts overnight to close at 26076.89. The index has likely started the long overdued near term correction and should head lower, possibly back to 25000 handle. 10 year yield extended recent rally to 2.726, up 0.030, but again, provides little support to Dollar.

BoJ Iwata: Some distance to 2% inflation

BoJ Deputy Governor Kikuo Iwata said today that the "powerful" monetary easing should be maintained. He noted "the economy is expanding moderately but prices remain weak." And, "there's some distance to 2 percent inflation." And he called for "government steps, as well as appropriate monetary policy, are necessary to achieve price stability with sustained economic growth." BoJ released summary of opinions from the January meeting. One member said that recent surge in market expectation of stimulus exit would be "undesirable".

Released from Japan, consumer confidence was unchanged at 44.7 in January. Housing starts dropped -2.1% yoy in December. Industrial production rose 2.7% mom in December.

Australia CPI picked up but missed expectations

Australia CPI accelerated to 1.9% yoy in Q4, up fro Q3's 1.8 yoy. However, this came in weaker than expectations of 2.0% yoy. On RBA's other inflation measures, the trimmed mean CPI stayed unchanged at 1.8%, missing consensus of 1.9%. The weighted median CPI rose to 2.0% from 1.9% in the third quarter. This exceeded expectations of 1.9%. The set of inflation data gives no pressure for RBA to hike any time soon. And indeed, recent rally in Aussie's exchange rate could give some downward pressure to inflation in near term ahead. And, there is still a lack of evidence of pick up in wage growth. Aussie weakens mildly after the release.

China manufacturing PMI slipped to 51.3

From China, official manufacturing PMI slipped -0.3 point to 51.3 in January, comparing to consensus of 51.5. Non-manufacturing PMI added 0.3 point to 55.3, beating expectations of 55. Note the government's PMI estimates cover large corporations while the one compiled by Caixin/ Markit covers medium to small firms. Traders should interpret China's economic data with caution as the accuracy is under question. HSBC complained about the country's lack of transparency and withdrew from being the partner of Markit in compilation of China's PMI data in 2015. Meanwhile, several provincial and local governments including Inner Mongolia and Tianjin have admitted exaggerating the economic data earlier this month.

GBP lifted mildly by hawkish

British pound resumed strength as BOE Governor Mark sent some hawkish messages. As he suggested, "as slack in the economy has been taken out, we've moved into a more conventional area for monetary policy where the focus is increasingly on returning inflation sustainably to target over an appropriate horizon".

Release from UK, Gfk consumer confidence rose to -9 in January. BRC shop price index dropped -0.5% yoy in January.

Looking ahead

FOMC rate decision is the main focus of the day. While it is widely expected that no change would be made in the monetary policy, the market focus is on the Fed's economic outlook and whether there are hints on the rate hike path. Notwithstanding the fact that inflation has remained soft, the robust employment market, with unemployment rate below the Fed's long-term target, should have anchored the Fed's confidence over the economic outlook. We do expect the Fed to address the issue recent USD weakness. On the monetary policy outlook, the market continued to price in over 70% of a rate hike in March.

In addition, Germany will release retail sales and unemployment. Eurozone will release CPI and unemployment. Swiss will release UBS consumption indicator.

Later in the day, US will release ADP employment, employment cost index, Chicago PMI and pending home sales. Canada will release GDP, IPPI and RMPI.

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.39; (P) 108.79; (R1) 109.18; More...

USD/JPY continues to stay in consolidation above 108.27 temporary low. Intraday bias remains neutral for the moment. As long as 110.18 resistance holds, deeper decline is expected. On the downside, break of 108.27 will extend recent fall through 107.31 support to next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Dec P | 2.70% | 1.50% | 0.50% | |

| 0:01 | GBP | GfK Consumer Confidence Jan | -9 | -13 | -13 | |

| 0:01 | GBP | BRC Shop Price Index Y/Y Jan | -0.50% | -0.40% | -0.60% | |

| 0:30 | AUD | CPI Q/Q Q4 | 0.60% | 0.70% | 0.60% | |

| 0:30 | AUD | CPI Y/Y Q4 | 1.90% | 2.00% | 1.80% | |

| 0:30 | AUD | CPI RBA Trimmed Mean Q/Q Q4 | 0.40% | 0.50% | 0.40% | |

| 0:30 | AUD | CPI RBA Trimmed Mean Y/Y Q4 | 1.80% | 1.90% | 1.80% | |

| 0:30 | AUD | CPI RBA Weighted Median Q/Q Q4 | 0.40% | 0.50% | 0.30% | |

| 0:30 | AUD | CPI RBA Weighted Median Y/Y Q4 | 2.00% | 1.90% | 1.90% | |

| 1:00 | CNY | Manufacturing PMI Jan | 51.3 | 51.5 | 51.6 | |

| 1:00 | CNY | Non-manufacturing PMI Jan | 55.3 | 55 | 55 | |

| 5:00 | JPY | Consumer Confidence Jan | 44.7 | 44.9 | 44.7 | |

| 5:00 | JPY | Housing Starts Y/Y Dec | -2.10% | 1.10% | -0.40% | |

| 7:00 | EUR | German Retail Sales M/M Dec | -0.40% | 2.30% | ||

| 7:00 | CHF | UBS Consumption Indicator Dec | 1.67 | |||

| 8:55 | EUR | German Unemployment Change Jan | -20K | -29K | ||

| 8:55 | EUR | German Unemployment Claims Rate Jan | 5.40% | 5.50% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 8.70% | 8.70% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan A | 1.00% | 0.90% | ||

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Jan | 1.30% | 1.40% | ||

| 13:15 | USD | ADP Employment Change Jan | 183K | 250K | ||

| 13:30 | USD | Employment Cost Index Q4 | 0.60% | 0.70% | ||

| 13:30 | CAD | GDP M/M Nov | 0.40% | 0.00% | ||

| 13:30 | CAD | Industrial Product Price M/M Dec | 0.00% | 1.40% | ||

| 13:30 | CAD | Raw Materials Price Index M/M Dec | -2.50% | 5.50% | ||

| 14:45 | USD | Chicago PMI Jan | 64 | 67.6 | ||

| 15:00 | USD | Pending Home Sales M/M Dec | 0.50% | 0.20% | ||

| 15:30 | USD | Crude Oil Inventories | -1.1M | |||

| 19:00 | USD | FOMC Rate Decision | 1.50% | 1.50% |

GBPUSD – Risk Turns Higher, Eyes 1.4285

GBPUSD - The pair closed higher after taking back all of its intra day losses on Tuesday. This has opened the door for more strength in the days ahead. Support lies at the 1.4100 level where a break will turn attention to the 1.4050 level. Further down, support lies at the 1.4000 level. Below here will set the stage for more weakness towards the 1.3950 level. Conversely, resistance stands at the 1.4200 levels with a turn above here allowing more strength to build up towards the 1.4250 level. Further out, resistance resides at the 1.4300 level followed by the 1.4350 level. On the whole, GBPUSD looks to move further higher with eyes on its key resistance.

Elliott Wave View: Dow Future In Correction

Dow Future Short Term Elliott Wave view suggests that the rally to 26690 ended Intermediate wave (3). Down from there, Intermediate wave (4) pullback is unfolding as a double three Elliott Wave structure where Minor wave W ended at 26121 and Minor wave X ended at 26314. Minor wave Y is in progress and while near term bounces stay below 26314, and more importantly below 26690, expect the Index to extend lower towards 25622 – 25754 area to end Intermediate wave (4) before Index resumes the rally or at least bounce in 3 waves. We don’t like selling the Index and expect buyers to appear from the above area for a 3 waves bounce at minimum.

YM_F Dow Future 1 Hour Elliott Wave Chart