Sample Category Title

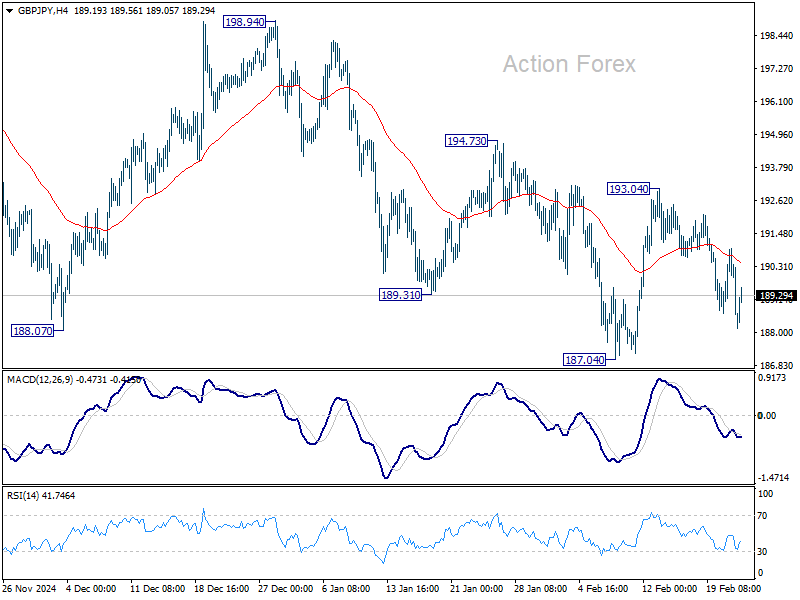

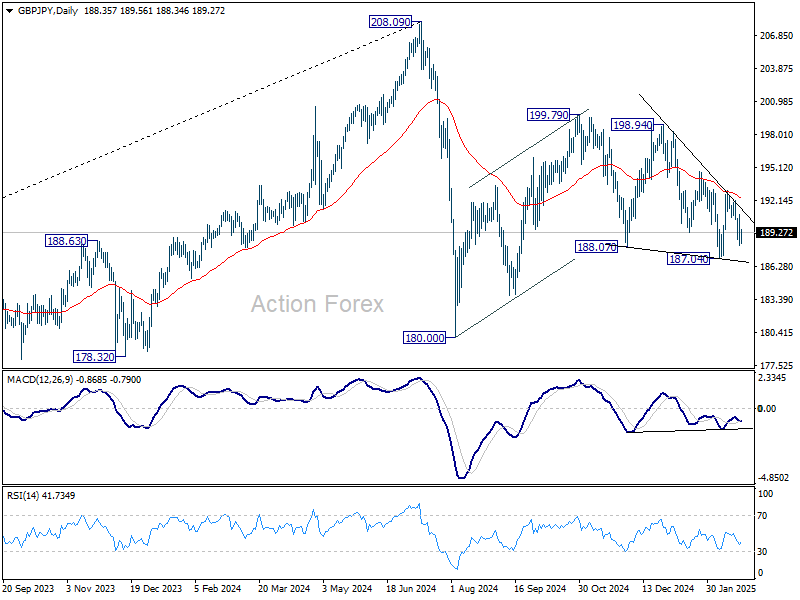

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.51; (P) 189.22; (R1) 190.30; More...

Intraday bias in GBP/JPY remains neutral for the moment. Risk will be mildly on the downside as long as 193.04 resistance holds. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

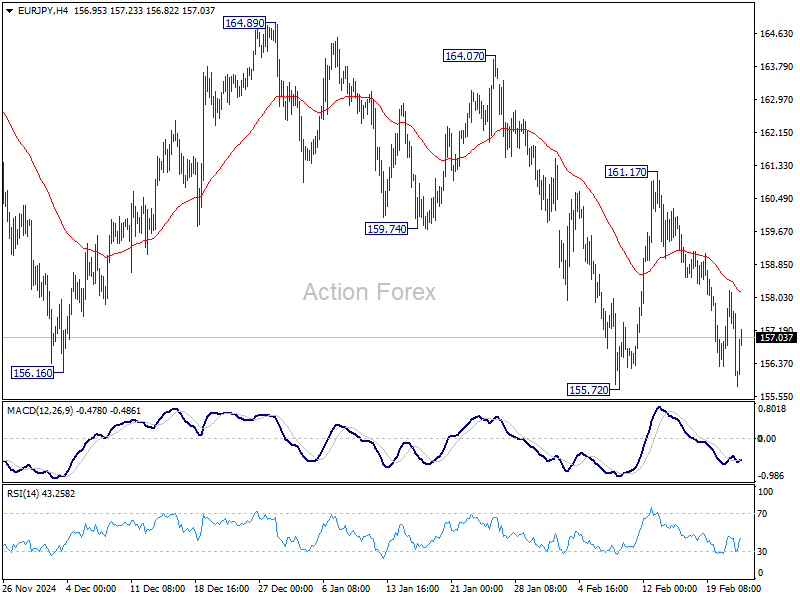

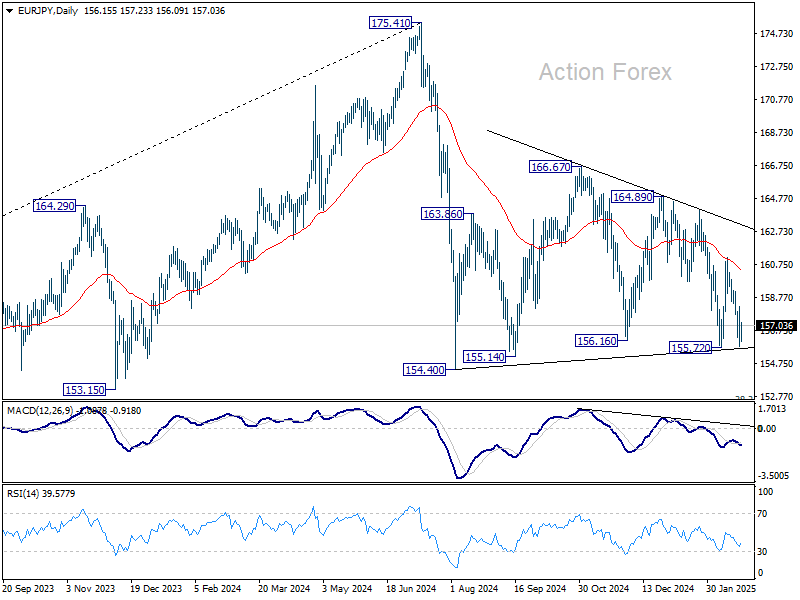

EUR/JPY Daily Outlook

Daily Pivots: (S1) 155.27; (P) 156.74; (R1) 157.67; More...

Intraday bias in EUR/JPY remains neutral for the moment. On the downside, firm break of 155.72 will be a strong sign that whole fall from 175.41 is resuming. Retest of 154.40 support should be seen next and firm break there should confirm.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction. Next target will be 100% projection of 175.41 to 154.40 from 166.67 at 145.66.

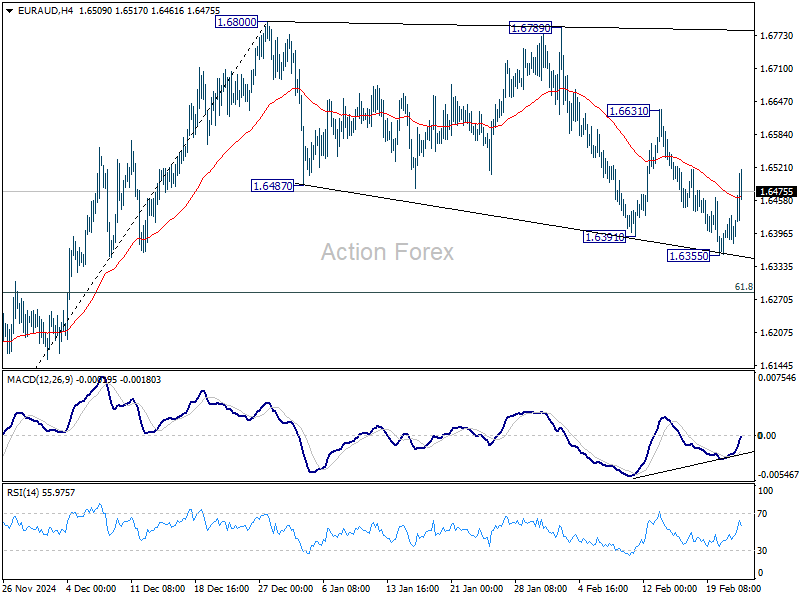

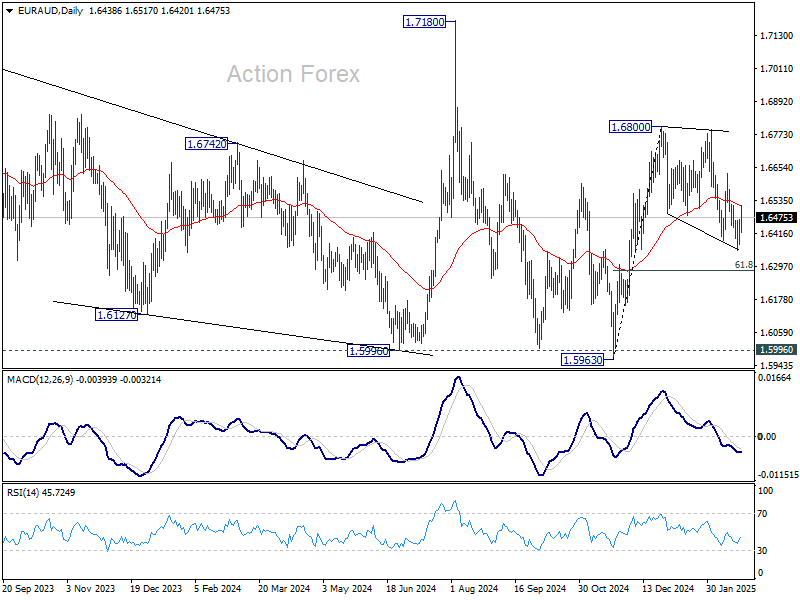

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6402; (P) 1.6436; (R1) 1.6492; More...

Intraday bias in EUR/AUD remains neutral for the moment. Corrective pattern from 1.6800 could still extend and break of 1.6355 will target 61.8% retracement of 1.5963 to 1.6800 at 1.6283. On the upside, firm break of 1.6631 resistance will suggest that the correction has likely completed, and rise from 1.5963 is finally ready to resume.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

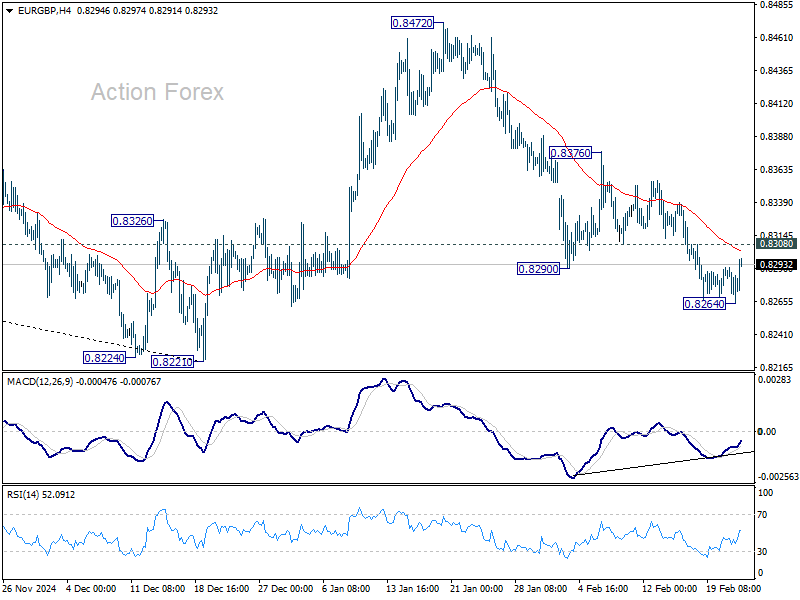

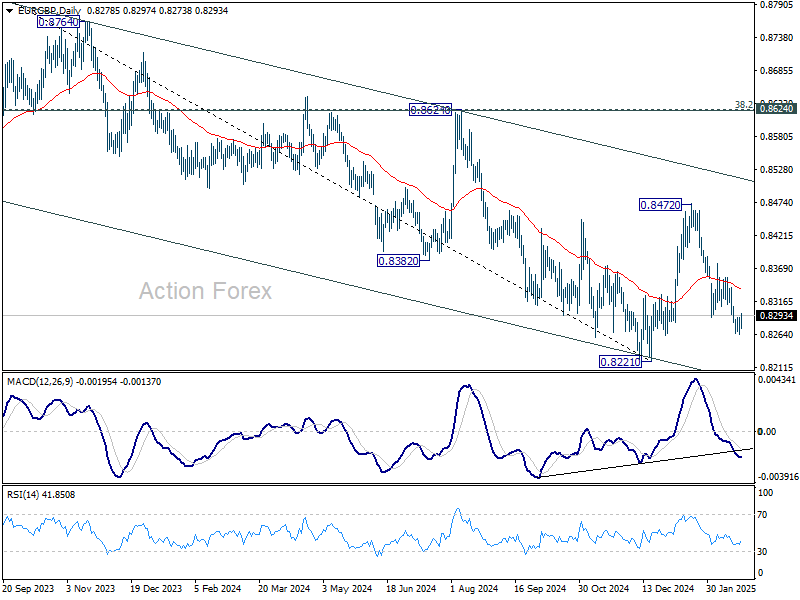

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8266; (P) 0.8279; (R1) 0.8293; More...

Intraday bias in EUR/GBP is turned neutral first with current recovery. Another fall is expected as long as 0.8308 minor resistance holds. Below 0.8264 will resume the whole decline from 0.8472 to retest 0.8221 low. Nevertheless, firm break of 0.8308 minor resistance will turn bias back to the upside for stronger rebound to 0.8376 resistance instead.

In the bigger picture, the medium term down trend remains intact with EUR/GBP staying well inside the falling channel. Prior rejection by 55 W EMA (now at 0.8431) also affirm bearishness. Decisive break of 0.8201/8221 support zone will resume whole down trend from 0.9449 (2020 high) and carry larger bearish implications.

Euro Gains Modestly After German Election, But Coalition Uncertainty Keeps Rally in Check

Euro opened the week slightly higher against all major currencies, as traders reacted positively to the German election results. Conservatives CDU/CSU secured victory, setting Friedrich Merz up as the next chancellor. However, Euro's gains remain limited, as uncertainty over coalition talks persists, with negotiations potentially dragging on until Easter.

While Merz’s CDU/CSU emerged as the largest party, winning 28.5% of the vote, it was far from a decisive mandate, leaving him in a weakened position for coalition negotiations.

The far-right AfD secured second place, marking its best-ever result. However, Merz has ruled out coalition talks with AfD, meaning a broader, more traditional coalition will be needed.

It remains unclear whether Merz will require one or two partners to form a government. Given the complexity of the negotiations, analysts expect haggling could last until Easter, prolonging political uncertainty in Europe's largest economy.

For now, Euro is the best-performing currency of the day so far, followed by Aussie and Sterling. On the other hand, Dollar is the weakest performer, followed by Yen and Swiss Franc, indicating a mild risk-on market sentiment. Kiwi and Loonie are trading in the middle of the pack.

Looking ahead, market focus will shift back to economic data, particularly Tuesday's US Conference Board consumer confidence report. While markets still weighing tariff concerns and geopolitics, the US consumer outlook could be more important for setting the near-term tone for forex markets and broader risk sentiment.

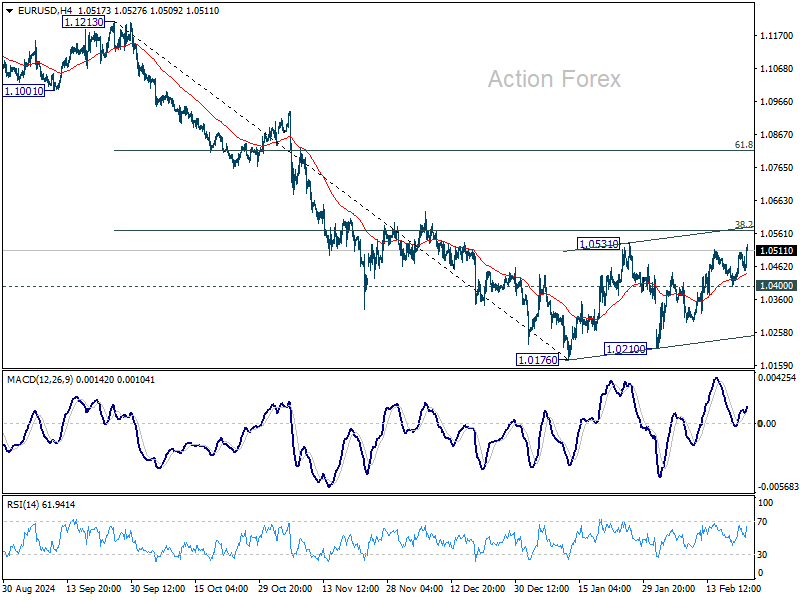

Technically, EUR/USD's outlook is unchanged with today's mild bounce. Price actions from 1.0176 are seen as a corrective pattern only. Fall from 1.1213 is expected to continue as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. Break of 1.0400 support will suggest that the correction has completed and bring retest of 1.0176 low.

In Asia, at the time of writing, Hong Kong HSI is down -0.55%. China Shanghai SSE is down -0.11%. Singapore Strait Times is up 0.31%. Japan is on holiday.

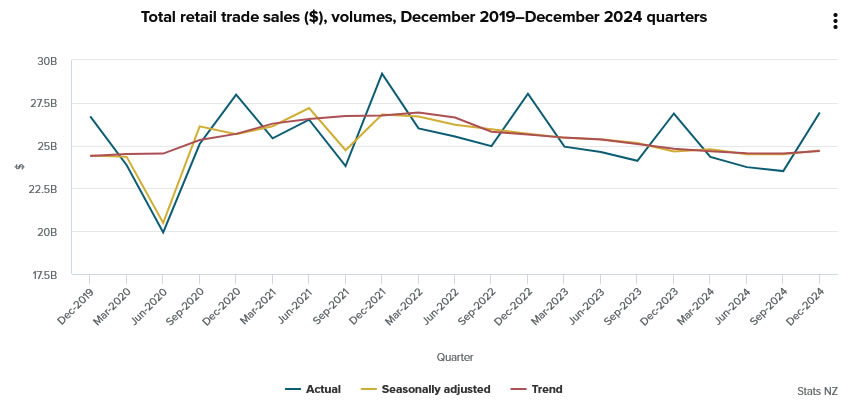

New Zealand retail sales rises 0.9% qoq in Q4, ex-auto sales jumps 1.4% qoq

New Zealand's Q4 retail sales volume rose 0.9% qoq to NZD 25B, surpassing expectations of 0.6% qoq. Excluding autos, sales jumped 1.4% qoq, well above the 0.3% qoq forecast.

Sales volume growth was broad-based, with 10 of 15 industries posting gains. The largest increases came from electrical and electronic goods (+5.1%), department stores (+4.2%), and accommodation (+7.6%). Meanwhile, food and beverage services rose 2.3%, but pharmaceutical and other retailing declined -3.4%.

Retail sales value climbed 1.4% qoq to NZD 30B, with 11 of 15 sectors reporting gains. Price effects were evident, particularly in accommodation (+11%), food and beverage services (+3.3%), and department stores (+2.9%).

ECB’s Escriva advises caution; Villeroy sees rate at 2% by summer

Spanish ECB Governing Council member Jose Luis Escriva stressed caution in an interview published Sunday, highlighting uncertainty in the economic outlook. He stated that it is "very difficult to gauge the impact of events that are unfolding", emphasizing the need to "wait for doubts around certain issues to be cleared" before making monetary policy adjustments.

Escriva reinforced ECB’s meeting-by-meeting approach, stating there “isn’t a pre-established future path for interest rates.” He also noted that Eurozone demand remains weak, with "notable differences among countries."

Separately, French ECB Governing Council member Francois Villeroy de Galhau offered a more direct outlook on interest rate, stating that “seen from where we are today, we could be at 2% by the coming summer.”

US consumer confidence, ECB accounts, and inflation reads

US consumers came into sharp focus last week, with deteriorating U of Michigan sentiment triggering a late selloff in stock markets. This week, the Conference Board’s consumer confidence report will be a key data point, as investors will be watching for any further signs of consumer strain.

Additionally, the personal income and outlays report, including PCE inflation data, will be closely watched—particularly the core inflation trend, which is Fed’s preferred gauge of price pressures. While Fed is unlikely to cut rates at its next two meetings barring a major shock, traders remain divided between June and July for the first rate cut, making incoming data critical in shaping expectations.

In Europe, ECB’s meeting accounts will be a major focus, though they are unlikely to change the bank’s current message of gradual easing. German Ifo business climate index and Gfk consumer sentiment survey will also provide insights into economic conditions in Europe’s largest economy. However, these releases will likely take a backseat to the outcome of Germany’s weekend elections, as coalition government negotiations could have a more immediate impact on market sentiment.

Beyond the US and Europe, a range of regional economic data will also be in focus, including Australia’s monthly CPI, Japan’s Tokyo CPI, and Swiss GDP.

While Australian monthly CPI release lacks the depth of the quarterly inflation report that the RBA relies on for policy decisions, it will still offer important clues on inflation trends and could influence rate-cut expectations.

Similarly, Japan’s Tokyo CPI serves as a leading indicator for the broader national inflation trend. However, it remains insufficient to shift BoJ policy stance, as the central bank is expected to wait for the results of the Shunto wage negotiations before considering its next move.

Here are some highlights for the week:

- Monday: New Zealand retail sales; Germany Ifo business climate; Eurozone CPI final.

- Tuesday: Japan corporate service price index; Germany GDP final; US house price index, consumer confidence.

- Wednesday: Australia monthly CPI; Germany Gfk consumer sentiment; US new home sales.

- Thursday: New Zealand ANZ business confidence; Swiss GDP; Eurozone M3 monthly supply; ECB meeting accounts; US GDP revision, jobless claims, durable goods orders, pending home sales.

- Friday: Japan Tokyo CPI, industrial production, retail sales; Germany import prices, retail sales, unemployment, CPI flash; Swiss retail sales, KOF economic barometer; Canada GDP; US personal income and spending, PCE inflation, goods trade balance.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8266; (P) 0.8279; (R1) 0.8293; More...

Intraday bias in EUR/GBP is turned neutral first with current recovery. Another fall is expected as long as 0.8308 minor resistance holds. Below 0.8264 will resume the whole decline from 0.8472 to retest 0.8221 low. Nevertheless, firm break of 0.8308 minor resistance will turn bias back to the upside for stronger rebound to 0.8376 resistance instead.

In the bigger picture, the medium term down trend remains intact with EUR/GBP staying well inside the falling channel. Prior rejection by 55 W EMA (now at 0.8431) also affirm bearishness. Decisive break of 0.8201/8221 support zone will resume whole down trend from 0.9449 (2020 high) and carry larger bearish implications.

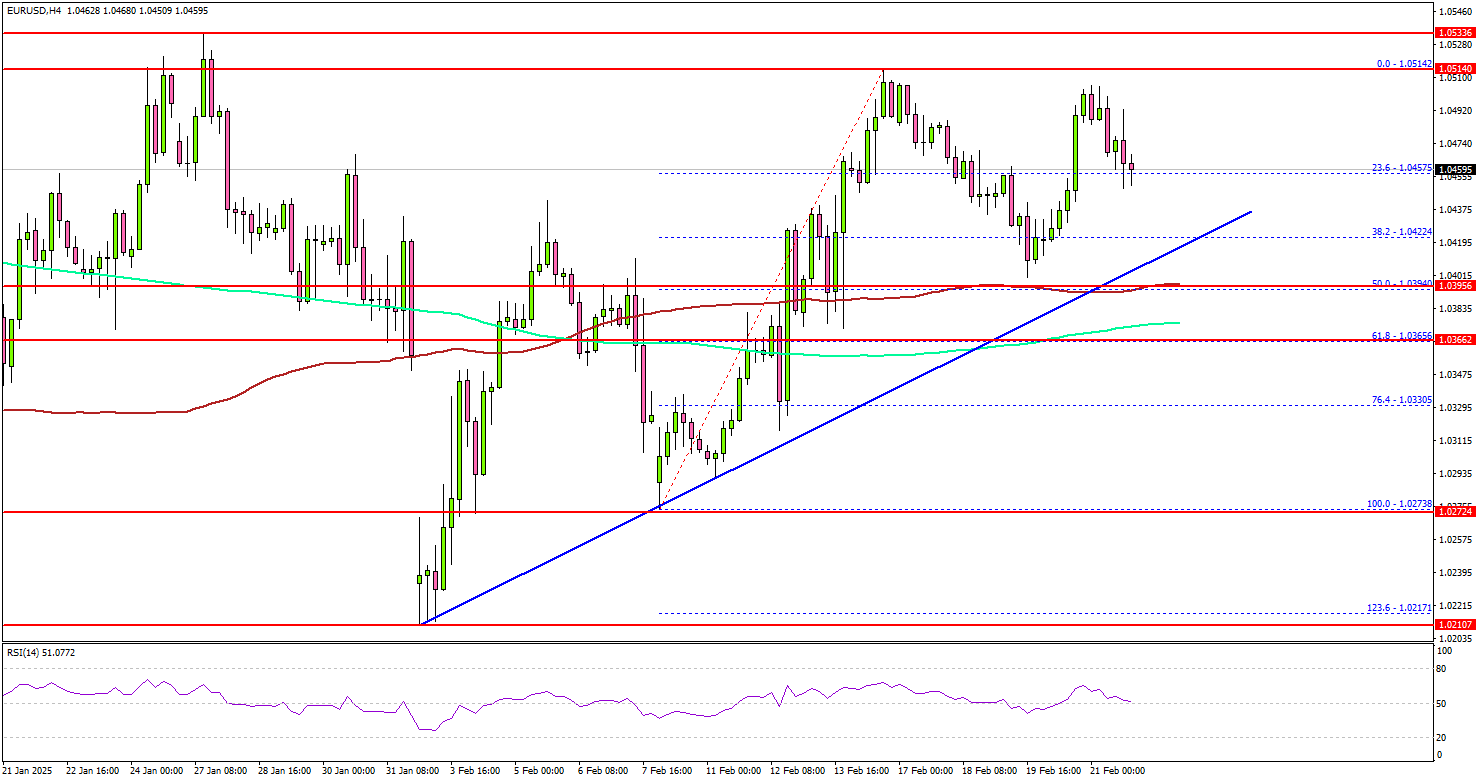

EUR/USD Finds Support—Are More Gains Coming?

Key Highlights

- EUR/USD started a consolidation phase from the 1.0515 resistance.

- A key bullish trend line is forming with support at 1.0420 on the 4-hour chart.

- GBP/USD is showing positive signs above the 1.2560 support.

- Crude oil prices declined below the $71.50 and $70.50 support levels.

EUR/USD Technical Analysis

The Euro started a decent increase above 1.0400 against the US Dollar. EUR/USD tested the 1.0515 resistance before the bears appeared.

Looking at the 4-hour chart, the pair settled above the 1.0420 support, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair started a consolidation phase and corrected some gains below 1.0480.

On the downside, immediate support sits near the 1.0420 level. There is also a key bullish trend line forming with support at 1.0420 on the same chart.

The next key support sits near the 1.0395 level and the 100 simple moving average (red, 4-hour). The main support could be 1.0365. Any more losses could send the pair toward the 1.0300 level.

On the upside, the pair seems to be facing hurdles near the 1.0515 level. The next major resistance is near the 1.0530 level. The main resistance is now forming near the 1.0550 zone. A close above the 1.0550 level could set the tone for another increase. In the stated case, the pair could even clear the 1.0620 resistance.

Looking at GBP/USD, the pair remained stable above 1.2560 and might aim for more gains above the 1.2650 resistance.

Upcoming Economic Events:

- Euro Zone CPI for Jan 2025 (YoY) - Forecast +2.5%, versus +2.5% previous.

- Euro Zone CPI for Jan 2025 (MoM) - Forecast -0.3%, versus -0.3% previous.

ECB’s Escriva advises caution; Villeroy sees rate at 2% by summer

Spanish ECB Governing Council member Jose Luis Escriva stressed caution in an interview published Sunday, highlighting uncertainty in the economic outlook. He stated that it is "very difficult to gauge the impact of events that are unfolding", emphasizing the need to "wait for doubts around certain issues to be cleared" before making monetary policy adjustments.

Escriva reinforced ECB’s meeting-by-meeting approach, stating there “isn’t a pre-established future path for interest rates.” He also noted that Eurozone demand remains weak, with "notable differences among countries."

Separately, French ECB Governing Council member Francois Villeroy de Galhau offered a more direct outlook on interest rate, stating that “seen from where we are today, we could be at 2% by the coming summer.”

New Zealand retail sales rises 0.9% qoq in Q4, ex-auto sales jumps 1.4% qoq

New Zealand's Q4 retail sales volume rose 0.9% qoq to NZD 25B, surpassing expectations of 0.6% qoq. Excluding autos, sales jumped 1.4% qoq, well above the 0.3% qoq forecast.

Sales volume growth was broad-based, with 10 of 15 industries posting gains. The largest increases came from electrical and electronic goods (+5.1%), department stores (+4.2%), and accommodation (+7.6%). Meanwhile, food and beverage services rose 2.3%, but pharmaceutical and other retailing declined -3.4%.

Retail sales value climbed 1.4% qoq to NZD 30B, with 11 of 15 sectors reporting gains. Price effects were evident, particularly in accommodation (+11%), food and beverage services (+3.3%), and department stores (+2.9%).

First Impressions: NZ Retail Trade, December Quarter 2024

Retail spending levels rose 0.9% in the December quarter. That was slightly ahead of forecast. The details of today’s report point to a firming in discretionary spending appetites.

December quarter retail sales (volume of goods sold): +0.9% (Prev: flat)

- Westpac f/c: +0.7%, Market: +0.5%

December quarter nominal retail sales: +1.4% (Prev: -0.5%)

New Zealanders dusted off their credit cards and hit the malls over the holidays.

Retail spending rose a solid 0.9% over the December quarter. That was slightly ahead of our forecast for a 0.7% rise.

The December quarter increase follows soft spending earlier in the year, leaving spending around the same levels as they were this time last year.

The rise in spending over the past few months was due to increased spending in discretionary areas. That includes a lift in spending on household durables, like electronics (up 5%) and furnishings (up 4%). We also saw increased spending in department stores (up 4%) and on clothing (up 2%), as well as a solid rise in spending in the hospitality sector.

The widespread increase in spending in discretionary areas points to a firming in households’ spending appetites. That’s consistent with the reduced pressure on households’ finances as inflation and interest rates have fallen, as well as the rise in consumer confidence in recent months.

We did see spending on groceries dropping back, but in part that will reflect that people have chosen to spend more on dining out.

What’s the outlook for the year ahead?

We expect spending levels will continue trending higher over the coming year. Interest rates have continued to drop. Importantly, the full impact of those declines is yet to be felt, as many mortgages are still on the relatively high interest rates from recent years. However, over the next six months, around half of all mortgages will come up for re-fixing, and many borrowers will have the opportunity to re-fix at lower rates. That will give spending a boost, especially through the second half of the year.

While the trend in spending over 2025 is likely to be to the upside, a couple of factors will limit the rise. First, unemployment is likely to rise from 5.1% currently to around 5.4%. In addition, inflation is likely to pick up over the coming year, with the NZ dollar likely to push up the price of some imported goods.

Even with the above headwinds, spending is likely to be firmer over 2025. That will be welcome news for many retailers and hospitality businesses who have faced tough trading conditions over the past couple of years.

Implications for GDP growth

We’re forecasting a 0.3% rise in GDP over the December quarter. Today’s result was a little ahead of our expectations. However, we’ll take a closer look at how our forecast for GDP growth is shaping up over the next couple of weeks as additional data on December quarter activity is released.

EURJPY Market Analysis: ECB, BOJ, and Technical Outlook

ECB Rate Decision: Inflation, Tariffs, and Market Sentiment Impact on EURJPY

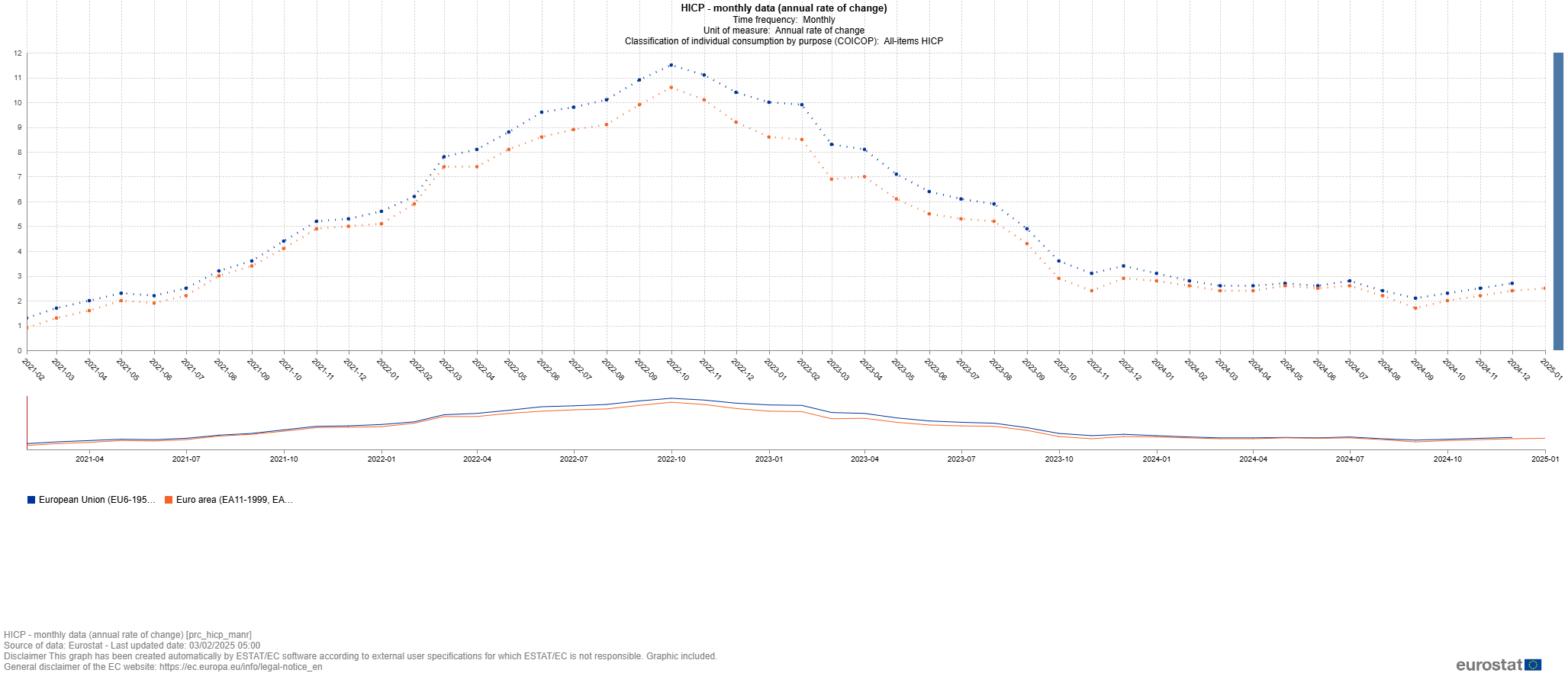

The European Central Bank (ECB) is scheduled to announce its interest rates and monetary policy statement on March 6th, 2025, followed by its standard press conference. The meeting occurs during a period of heightened market uncertainty due to trade wars and tariff implications. The Eurozone inflation indicator, the Harmonized Index of Consumer Prices (HICP), rose from its low of 1.7% in September 2024 (a 5-year low) to 2.5% in December 2024. This increase in HICP was mainly due to rising costs in housing, energy, and transportation. The Core HICP remained steady at 2.7% during the same period.

EZ HICP – Source: https://ec.europa.eu/eurostat/en/

The increase in inflation, along with concerns about the impact of US tariffs on Eurozone inflation, may affect market sentiment. According to Bloomberg analyst surveys, 97.5% of participants expect the ECB to cut rates by 25 basis points at its March 6th, 2025, meeting. This is down from 135.0% on January 30th, 2025, when markets anticipated a possible 50 basis point cut.

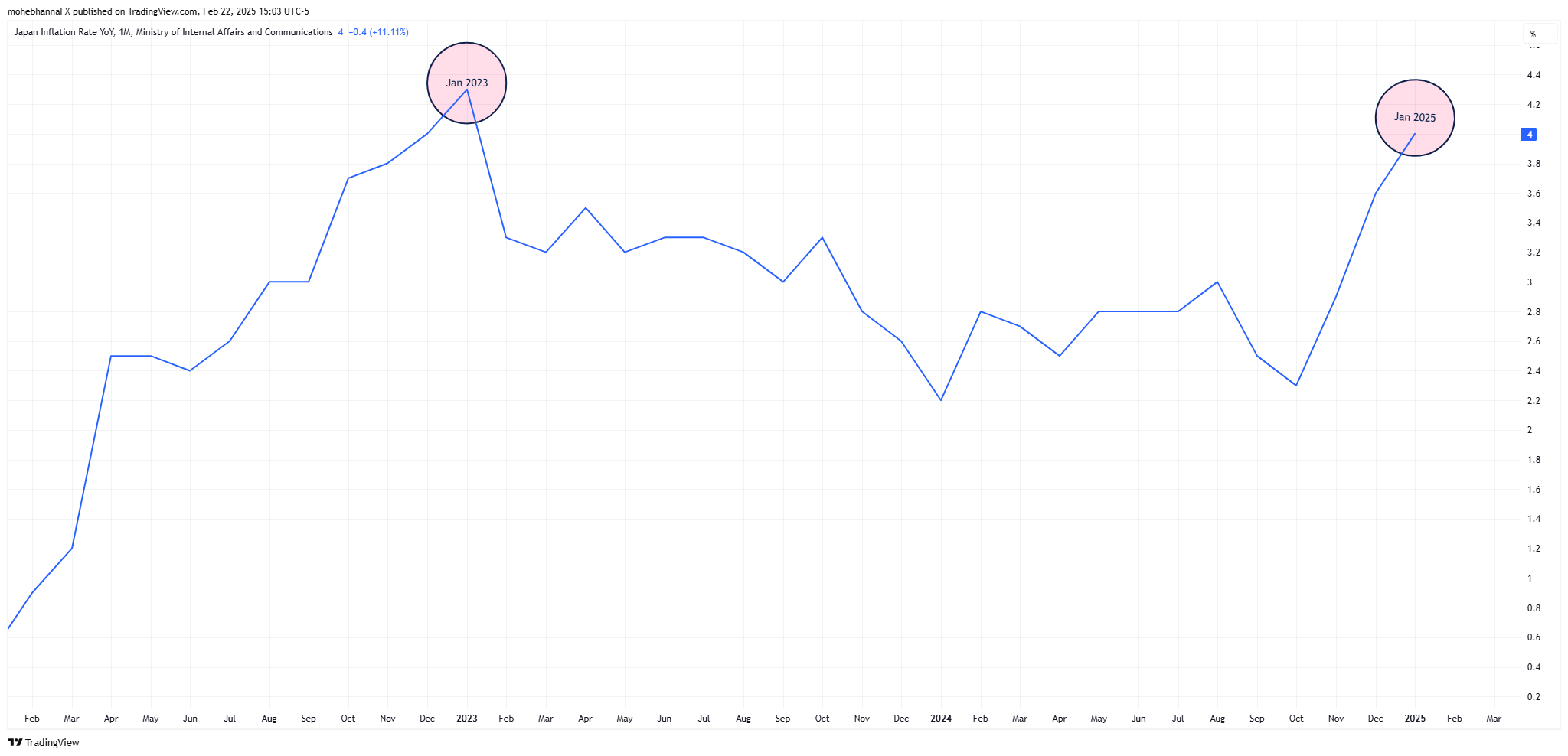

Japanese Yen (JPY) Strength: Inflation, Interest Rates, and BOJ Policy Impact on USDJPY

The Japanese Yen has gained some strength against the US dollar in early 2025, rising approximately 6% as of early January 2025. While 6% is a significant move in currency trading, it is small compared to the Yen’s 35% weakness against the US dollar, which began in early 2021 and ended in July 2024.

Source: https://www.tradingview.com/chart/5SnueDXH/

The recent upward move was supported by a slower-than-anticipated interest rate cut path by the Federal Reserve and an increase in Japan’s inflation to a 2-year high of 4%, suggesting that BOJ’s rate hikes could be on the horizon. The Bank of Japan (BOJ) Policy rate decision is scheduled for March 18th, 2025, a day before the FOMC statement and the federal funds rate announcement. Last week, Bank of Japan Governor Kazuo Ueda stated in parliament that the “BOJ would buy bonds nimbly if yields rise sharply.” According to Bloomberg analyst surveys, expectations for a 25 basis point interest rate hike at the BOJ’s March 18th, 2025, meeting stand at only 1.8%, down from 38.7% in December 2024.

EURJPY Technical Analysis: Ascending Channel Breakout, Head and Shoulders Pattern, and Flag Formation

Source: https://www.tradingview.com/chart/PxTXLbsa/

EURJPY Weekly Japanese Candlestick Chart

- EURJPY has been trading within an ascending channel since mid-2020. Price action broke and closed below the channel, followed by two pullbacks (PB1 and PB2). Both attempts met resistance along the channel border extension. Two more pullbacks followed (PB3 and PB4), but a shortfall occurred as the price was unable to reach the channel border. The four pullbacks together completed a complex head and shoulders pattern, which had already broken below its neckline and reached its technical target.

- The overall price action following the breakout below the ascending channel completed a flag formation, a continuation chart pattern. (The flag chart pattern is highlighted in yellow.)

- A potential exhaustion downward gap formation took the price down to the head and shoulders technical target at the market open on February 3rd, 2025, following President Trump’s tariff announcement regarding Canada and Mexico.

- Currently, price action is at a confluence of support represented by the lower side of the flag formation and support level S1 of 157.07, where it previously found support in September 2024. (Purple arrows)

- Price is trading below its moving averages (EMA9, SMA9, and SMA20). The three moving averages intersect with the gap formation near the monthly pivot point of 161.88, forming a confluence of resistance above the price action.

- The default RSI 14 is at level 40 and approaching oversold territory, and the MACD line remains below its signal line.

Considering the confluence of technical factors, including the ascending channel breakout, head and shoulders pattern, and flag formation, along with the fundamental factors of ECB and BOJ policy decisions and inflation rates, EURJPY presents a complex trading landscape. Traders should closely monitor key support and resistance levels, moving averages, and momentum indicators like RSI and MACD. Robust risk management strategies are essential to navigate the potential volatility and capitalize on opportunities while mitigating downside risk.