Sample Category Title

GBP/JPY Weekly Outlook

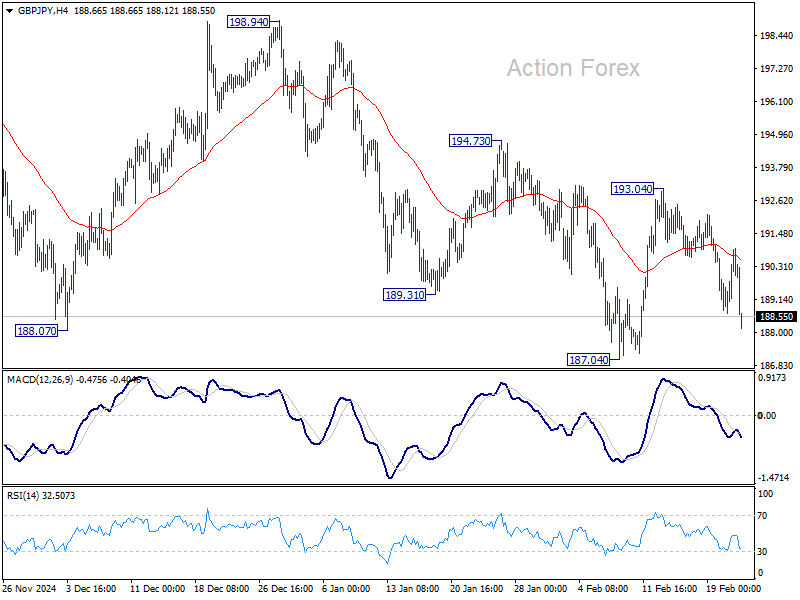

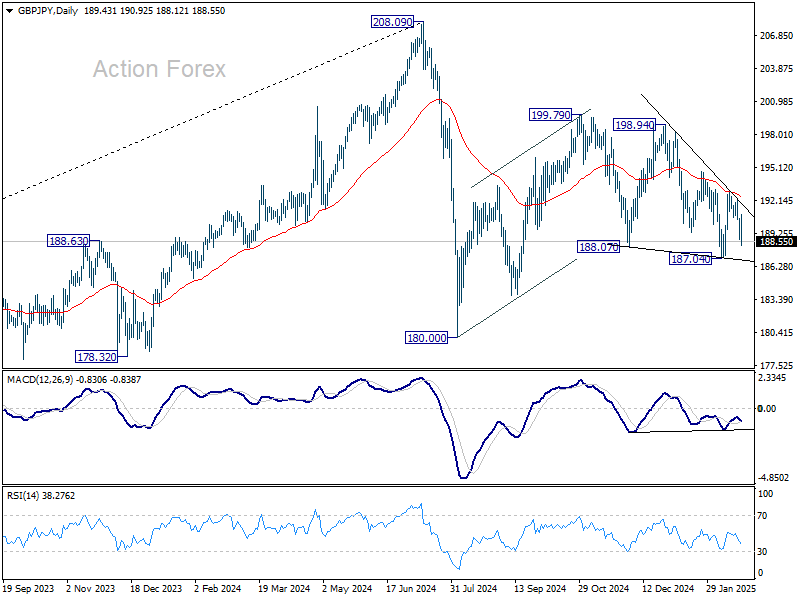

GBP/JPY's decline last week should confirm prior rejection by 55 D EMA (now at 192.44) which is a bearish sign. However, downside is still contained well above 187.04 support. Initial bias remains neutral this week first. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support.

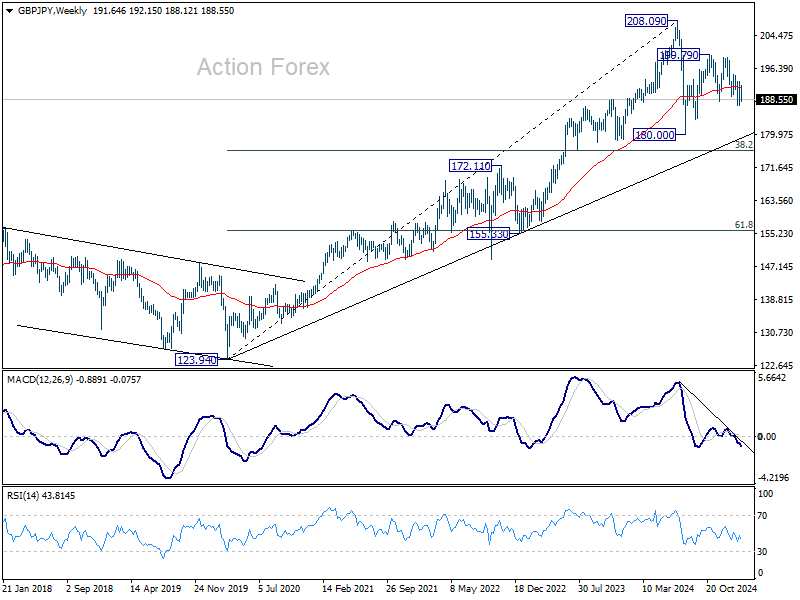

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

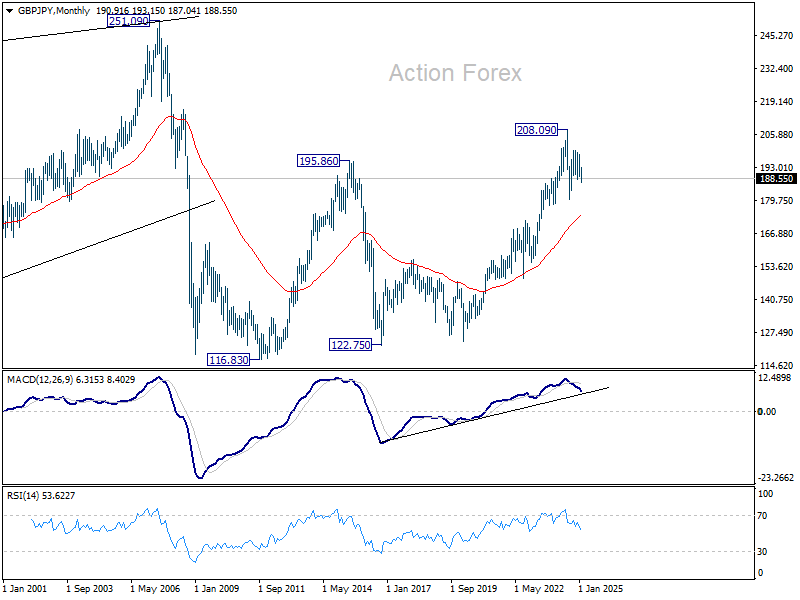

In the longer term picture, while a medium term top was formed at 208.09 (2024 high), it's still early to conclude that the up trend from 122.75 (2016 low) has completed. But GBP/JPY is at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 173.92).

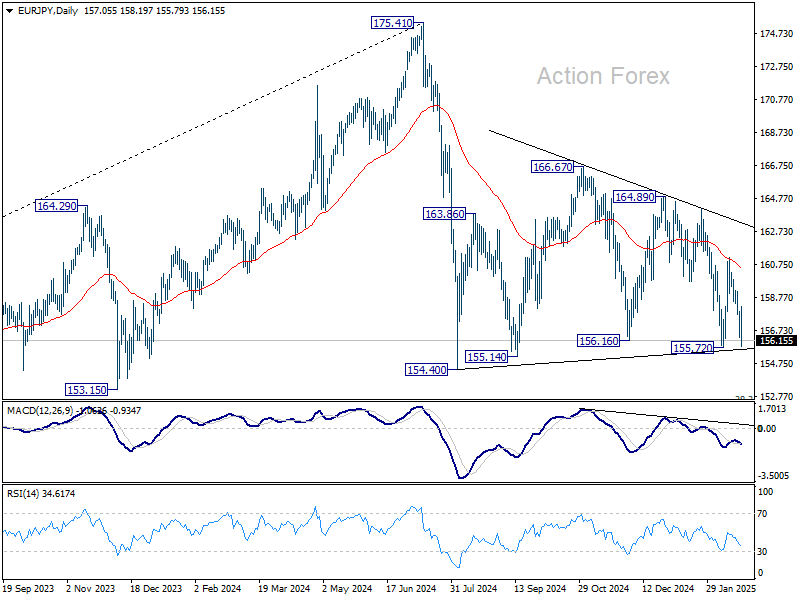

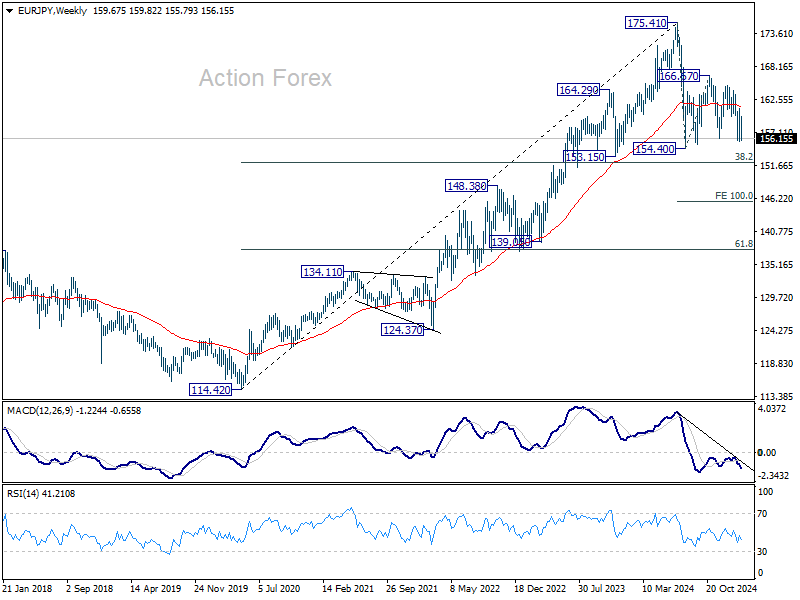

EUR/JPY Weekly Outlook

EUR/JPY's steep decline last week confirmed prior rejection by 55 D EMA (now at 160.47), which is a bearish sign. But downside is contained above 155.72 support so far. Initial bias is neutral this week first. On the downside, firm break of 155.72 will be a strong sign that whole fall from 175.41 is resuming. Retest of 154.40 support should be seen next and firm break there should confirm.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction. Next target will be 100% projection of 175.41 to 154.40 from 166.67 at 145.66.

In the long term picture, while 175.41 is at least a medium term top, it's still early to conclude that up trend from 94.11 (2012 low) has completed. A medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 148.45).

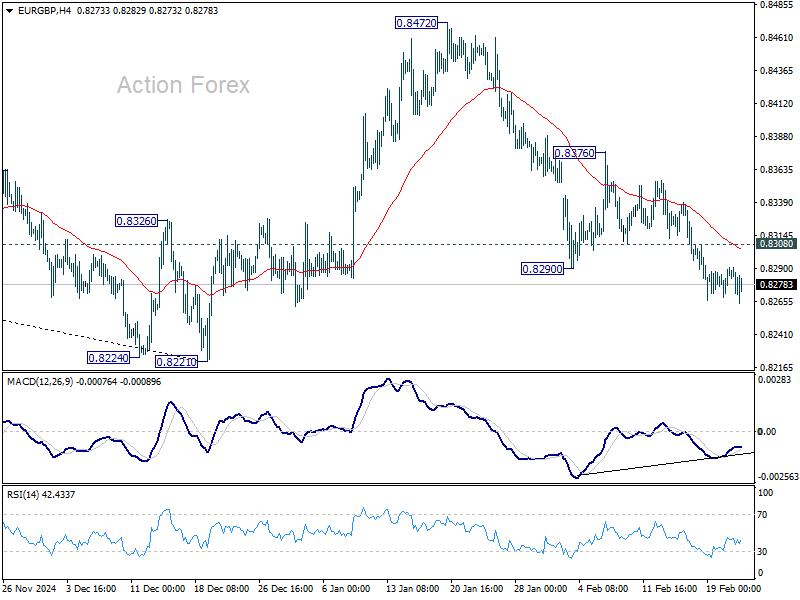

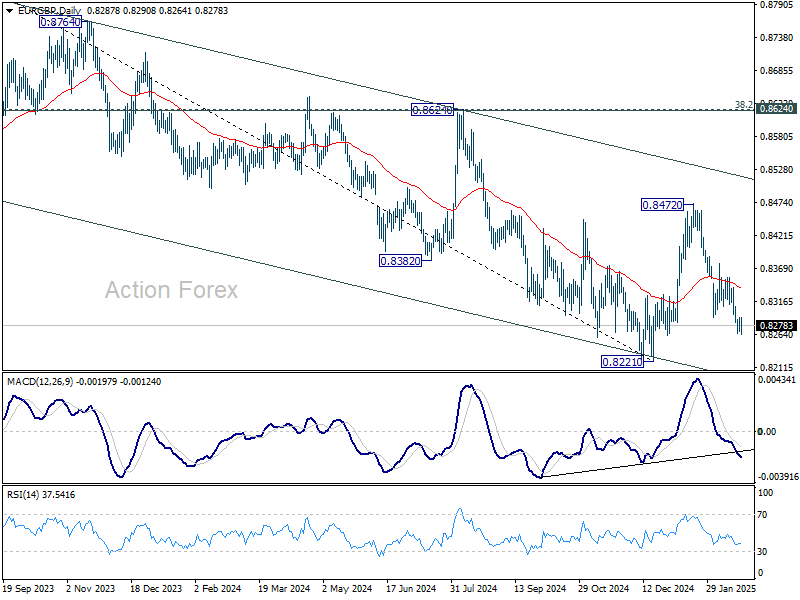

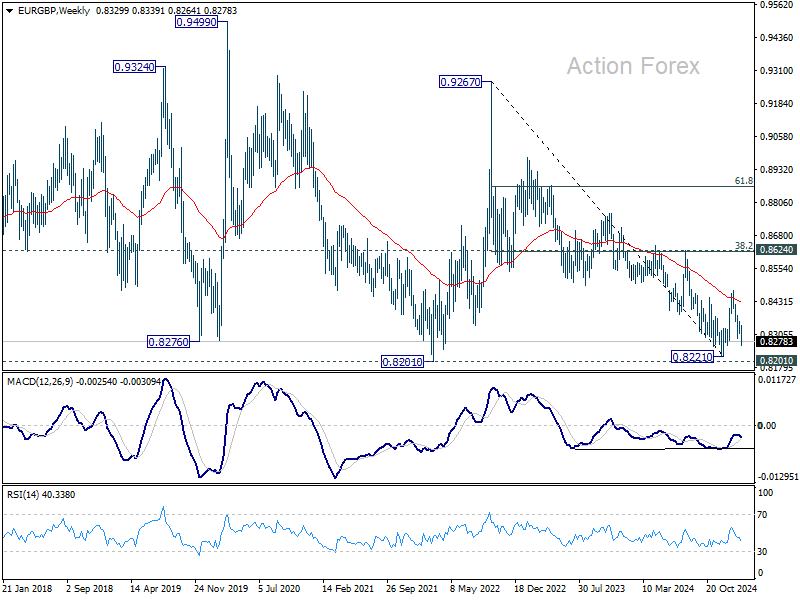

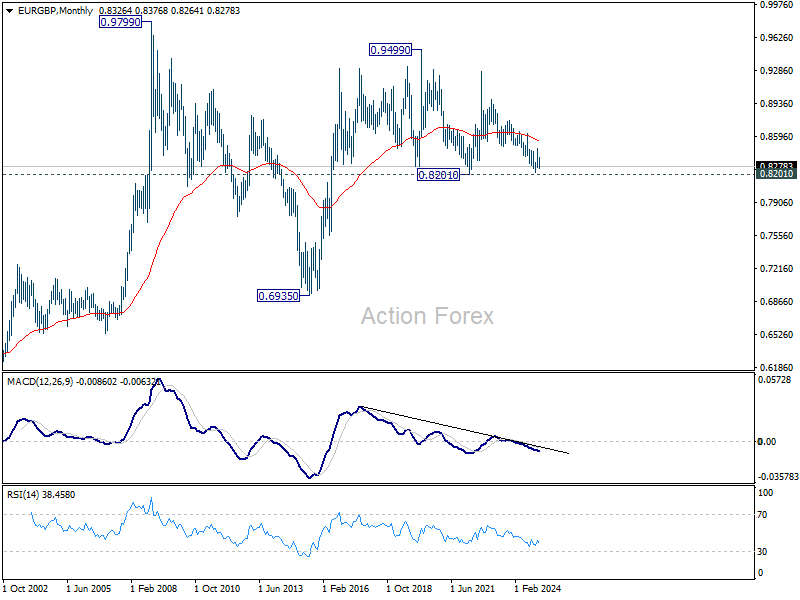

EUR/GBP Weekly Outlook

EUR/GBP's decline from 0.8472 resumed by breaking through 0.8290 support last week. Initial bias stays on the downside this week despite weak momentum. Further fall should be seen to retest 0.8221 low. Nevertheless, firm break of 0.8308 minor resistance will turn bias back to the upside for stronger rebound to 0.8376 resistance instead.

In the bigger picture, the medium term down trend remains intact with EUR/GBP staying well inside the falling channel. Prior rejection by 55 W EMA (now at 0.8431) also affirm bearishness. Decisive break of 0.8201/8221 support zone will resume whole down trend from 0.9449 (2020 high) and carry larger bearish implications.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

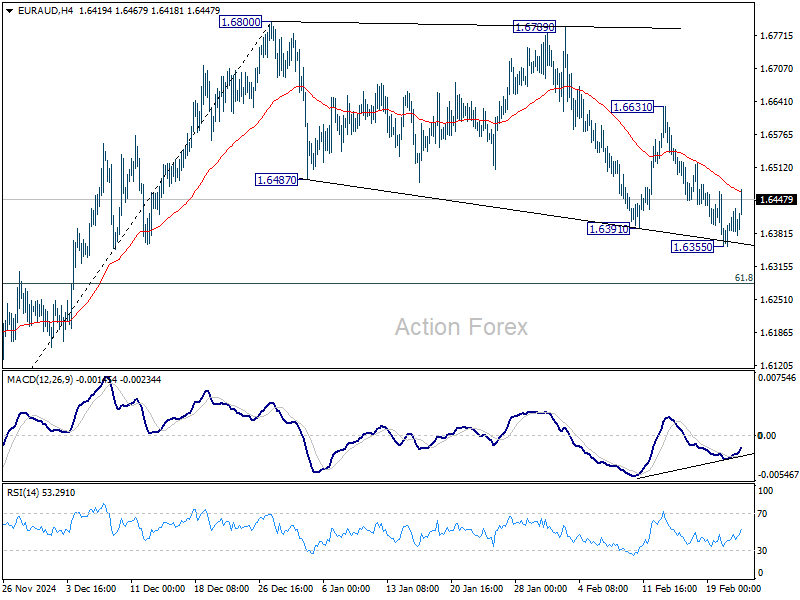

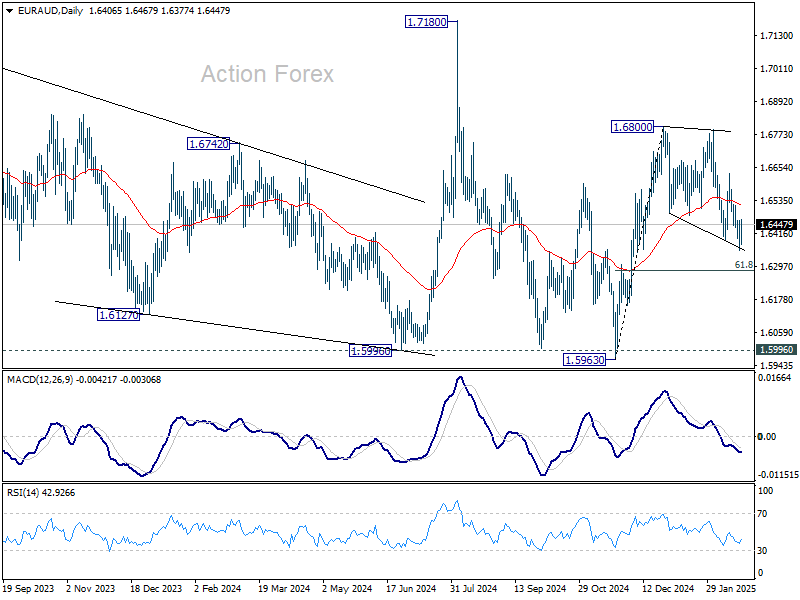

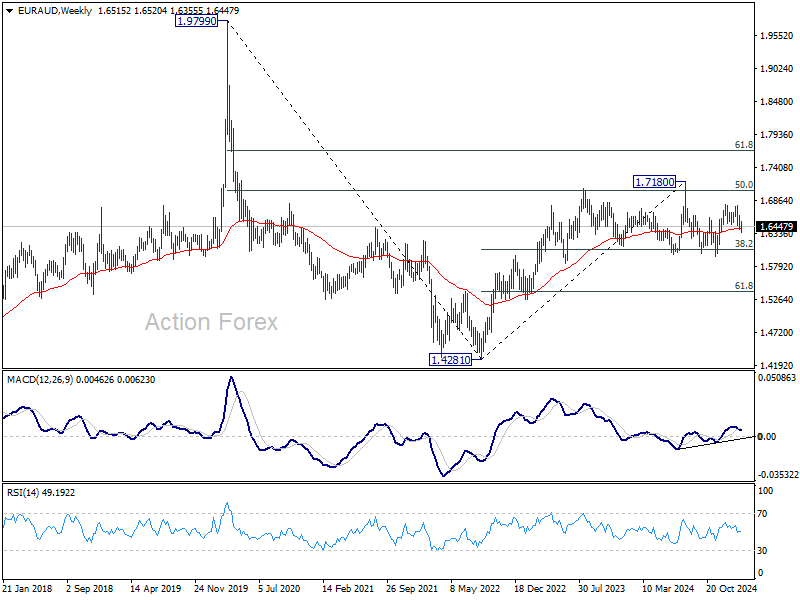

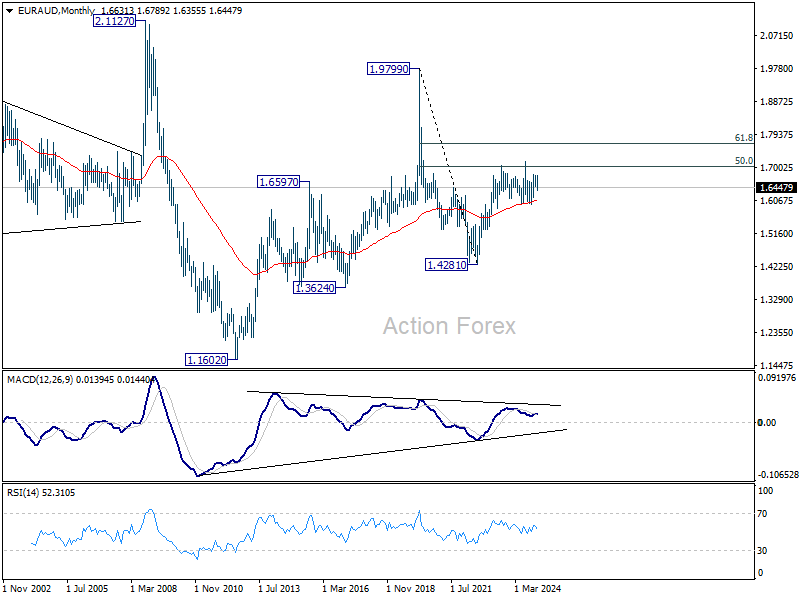

EUR/AUD Weekly Outlook

EUR/AUD's decline last week suggests that corrective pattern from 1.6800 is still extending. With a temporary low formed at 1.6355, initial bias is neutral this week first. On the downside, below 1.6355 will target 61.8% retracement of 1.5963 to 1.6800 at 1.6283. On the upside, firm break of 1.6631 resistance will suggest that the correction has likely completed, and rise from 1.5963 is finally ready to resume.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6090) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

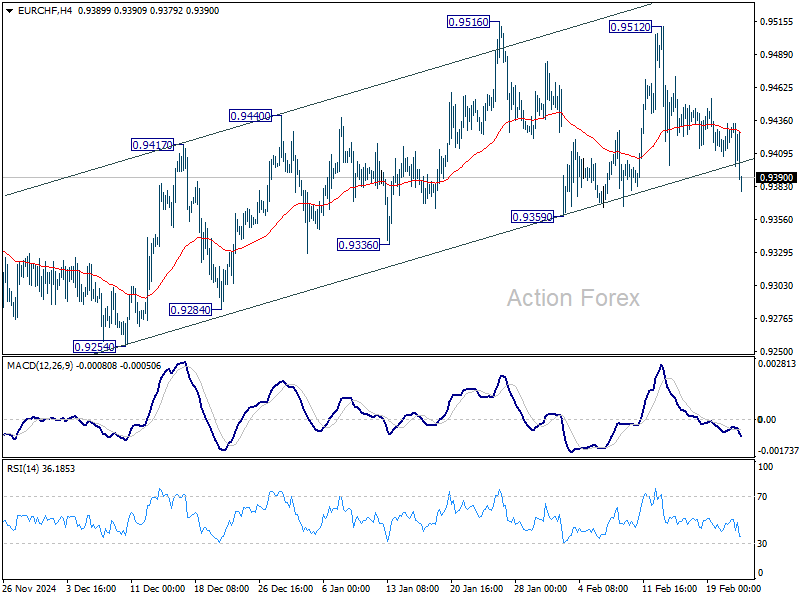

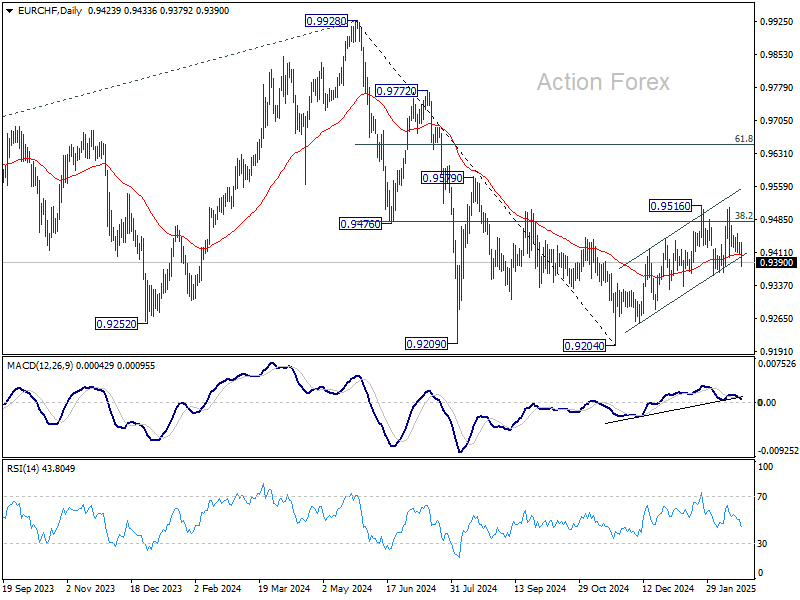

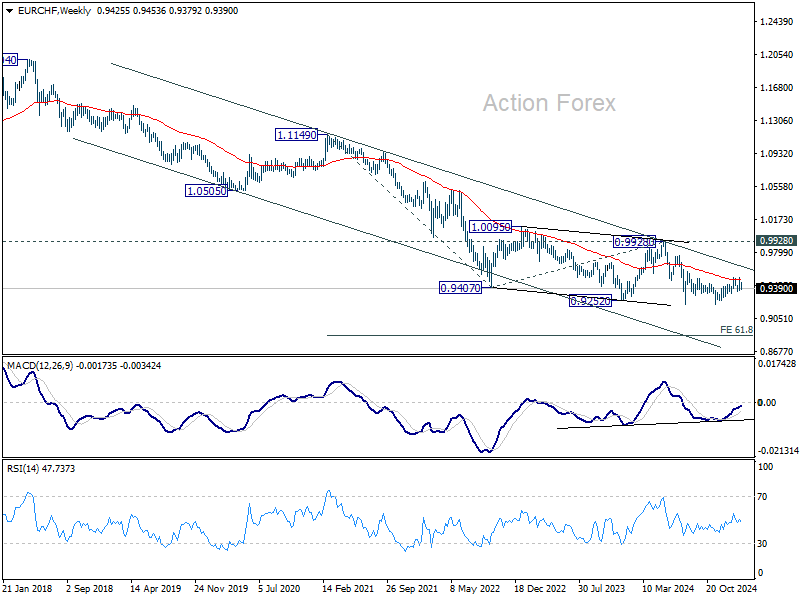

EUR/CHF Weekly Outlook

EUR/CHF dipped lower last week but stayed above 0.9359 support. Initial bias remains neutral this week first. On the downside, firm break of 0.9359 will revive the case that choppy rise from 0.9204 is merely a correction and has completed. Deeper fall should then be seen back to retest 0.9204 low. However, firm break of 0.9516 and sustained trading above 0.9481 fibonacci level will carry larger bullish implication and extend the rise from 0.9204.

In the bigger picture, sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204 at a later stage.

In the long term picture, as long as 0.9928 resistance holds, the multi-decade down trend remains intact, with decline from 1.2004 (2018 high) as another falling leg. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption to 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851.

Markets Weekly Outlook – US PCE, Japanese Inflation & Tariffs in Focus

- US equity markets experienced a slight downturn due to concerns about inflation impacting consumer spending, highlighted by Walmart’s cautious outlook.

- The upcoming US PCE data is crucial as the Fed’s preferred inflation measure.

- Japanese inflation data will also be key this week as markets eye the Bank of Japans next move.

- German elections take place over the weekend in what could be massive for Europe as a whole.

Week in Review: Tariff Chatter Continues to Drive Market Moves

Markets had another interesting week as US President Donald Trump pledged more tariffs ahead. A potential peace deal appears to be gaining traction between Russia and Ukraine but this did little to dent the appeal of Safe havens as Gold continues to hold the high ground.

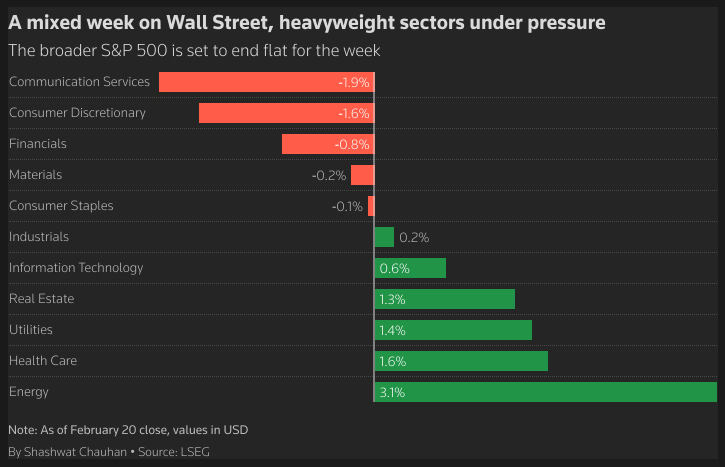

US Equity markets did take a slight hit toward the backend of the week largely driven by news from Walmart.

The $780 billion retailer reported strong holiday and January sales, thanks to wealthier customers looking for deals. However, it warned that inflation could hurt shoppers, causing its stock value to drop by 6%. This shows that the economic optimism seen after Donald Trump’s election may be starting to fade.

Walmart acknowledged “uncertain times,” which led to a cautious outlook and a $50 billion drop in its market value. Being a key indicator of U.S. spending habits, Walmart’s concerns matter. Even Donald Trump admitted that “inflation is back,” and research shows consumer confidence in business and jobs fell sharply in January.

Wall Street is also uneasy. David Kelly, a strategist at JPMorgan, warned about risks to economic growth from new policies, including tariffs and deportations. If Walmart is feeling nervous, it could signal a growing wave of fear in the economy.

This was compounded by weak US data as the S&P Global data showed that U.S. business activity barely grew in February as worries about import tariffs and major government spending cuts increased.

The S&P 500 and Nasdaq 100 both printed fresh highs before a selloff on Thursday and Friday, reflecting the market’s concerns about these developments.

Source: LSEG

On the commodities front, Gold continued its advance this week but did have a bit of a seesaw run. The one concern that bulls may have is that this week’s rally failed to print fresh all-time highs. Is this a sign that bullish pressure may be waning?

Oil prices had an interesting week with gains every day before a significant selloff on Friday left Brent crude trading flat for the week. Supply jitters continue to persist, but President Trump’s wish of lower energy and oil prices clearly is weighing on the minds of market participants. News filtered through today that the US is putting pressure on Iraq to restart the pipeline to Turkey which could explain the fall in Oil prices, or at least partially so.

On the FX front, the US Dollar struggled this week largely due to a massive selloff on Thursday. This was a surprise given that Wednesday FOMC minutes showed the Fed is concerned about the impact of tariffs on inflation. This has led to the idea that rate cuts may be pushed back later in the year than had been previously anticipated.

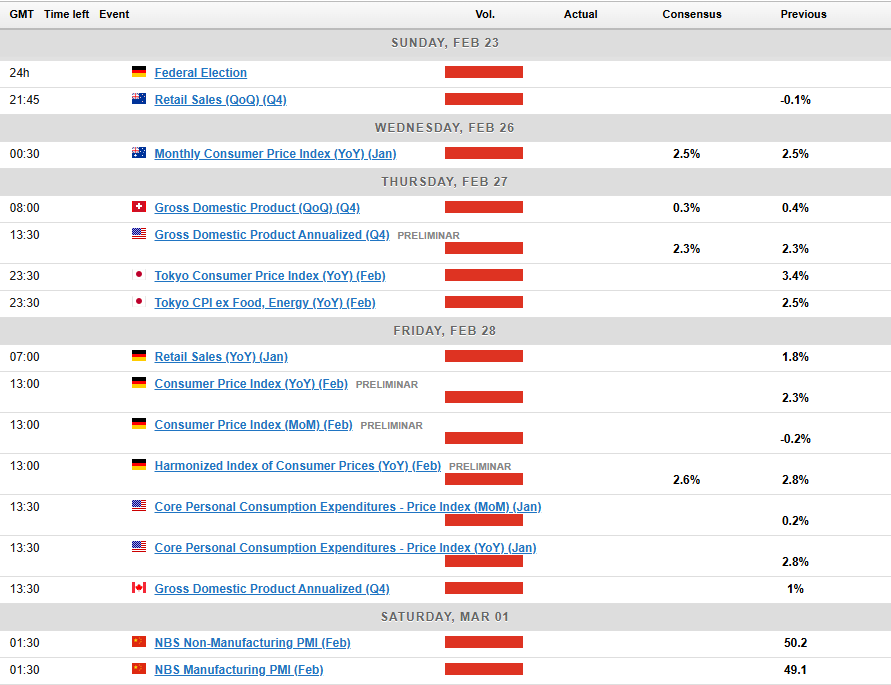

The Week Ahead: US CPE Will be Key After Hot US CPI data, German Elections are in Focus as Well

Asia Pacific Markets

The main focus this week in the Asia Pacific region for me will be inflation data from Japan while we also have some Chinese data to monitor.

The week’s key focus is Tokyo’s inflation data, expected to hold at 3.3% in February. Rising fresh food prices may drive costs up, but energy subsidies should balance this out. The BoJ will monitor if higher food costs, like rice, are affecting consumers. Economic data suggests a slow recovery, with industrial output improving due to exports and retail sales boosted by better wages and more tourists.

China’s schedule for economic data is light in the last week of February. On Tuesday, the People’s Bank of China is expected to decide on the medium-term lending facility (MLF) rate. Since the focus has shifted to the 7-day reverse repo rate as the main policy tool, no changes to the MLF rate are expected this month. Any surprise however could have a knock on effect on emerging markets.

Europe + UK + US

In developed markets, the US CPI release last week really stoked concerns about higher rates for longer. However, Fed Chair Powell was quick to stress how the Fed prefers the PCE data as their inflation gauge and cautioned against reading too much into the CPI release.

Next week’s PCE data includes the Fed’s preferred inflation measure, the core personal consumer expenditure (PCE) deflator. While the core CPI rose by a concerning 0.4% month-on-month, other data suggests that the core PCE deflator is likely to show a smaller increase of 0.3%. To reach the 2% yearly inflation target, monthly inflation needs to average 0.17%. Due to these factors, it’s unlikely we’ll see any rate cuts before the September FOMC meeting.

Europe’s most industrialized economy faces a big weekend as Germans head to the polls in what will be a key election for Europe as a whole. The German economy faces a host of challenges while the question of immigration has also been a key campaign point.

The elections could have an impact on both the Euro and German Bunds as well when the market opens on Sunday night.

Chart of the Week

This week’s focus is on the US Dollar Index (DXY) after Thursday’s selloff and a break of the key level of support at 107.00.

Moving into next week and with the PCE data on the horizon, will the DXY rebound? That is the big question for market participants.

Currently the DXY has found support at the 100-day MA resting at 106.47 with a bullish inside bar candle close on Friday.

This leaves me to believe that we could get some bullish strength on Monday and perhaps a retest of the 107.00 handle.

More tariff chatter could help propel the DXY above the support turned resistance at 107.00, however in the absence of tariff chatter the DXY may grind sideways until the release of the PCE Data.

US Dollar Index Daily Chart – February 21, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 106.47

- 106.13

- 105.63

Resistance

- 107.00

- 108.00

- 108.49

The Weekly Bottom Line: Data Dependent Decisions

Canadian Highlights

- Headline inflation for the month of January rose to 1.9% year-on-year, while price pressures built in core inflation measures.

- Canadian retail sales surged in December, registering its largest monthly gain in nearly three years. Spending fatigue likely set-in in January.

- Tariff-related uncertainties may be trickling into housing markets as existing home sales took a step back in January.

U.S. Highlights

- Fed Speakers this week emphasized the need for a data-dependent approach to policy decisions.

- As a result, next week’s inflation data in the Personal Income and Outlays Report for January will be closely watched.

- From our lens, the Fed is likely to remain on pause until the second quarter of this year, delivering two cuts by year end, as healthy economic activity supports the labor market and price growth.

Canada – Inflation and (Hockey) Elation

Canada, the spotlight is yours. Team Canada trumped the Americans in a hard-fought hockey game worthy of an applause for both teams. Hockey scores weren’t the only thing on the ticker as Canadian economic data was headlined by a warm inflation print and complimented by a very upbeat consumer spending report. Elsewhere, momentum in home sales halted in January, a relative weak spot amid the broader strength in other data. Taken together, markets have pared back the probability of a 25 basis point (bp) cut at the next Bank of Canada (BoC) rate announcement on March 12th to around 25%. That said, much will happen between now and then, including the outcome of President Trump’s plan to move forward with his threatened 25% tariffs (10% on energy) on Canadian imports.

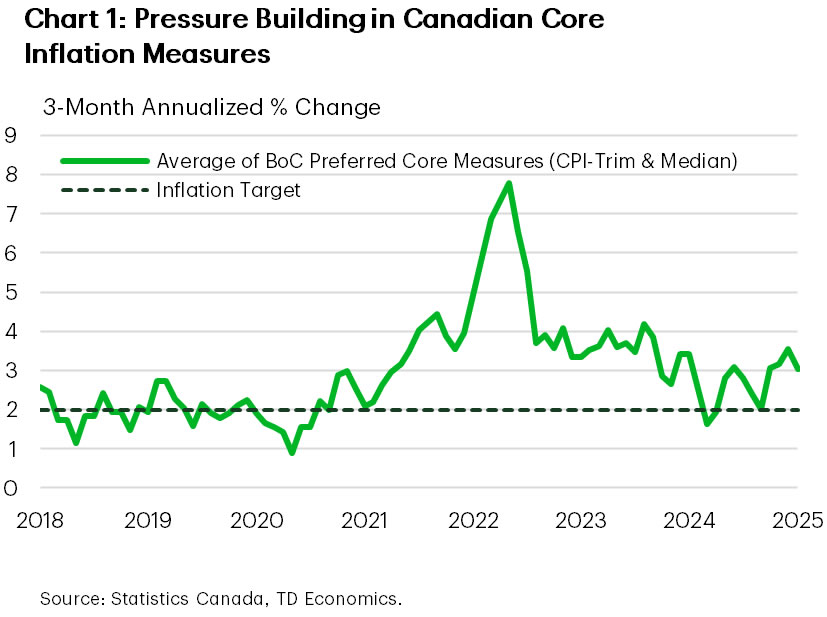

Inflation for the month of January edged up to 1.9% year-on-year (y/y), with rising energy prices making the biggest contribution to headline growth. Price growth was partially offset by the GST/HST holiday, while food price inflation found some respite, falling for the first time in nearly eight years. Headline inflation has stabilized around the Bank’s 2% target, though near-term risks are tilted to the upside as the end to the tax break will lead to higher inflation in coming months. The Bank’s preferred core inflation measure ticked up to 2.7% y/y and has hovered above 3% on a 3-month annualized basis for the past several months (Chart 1), something coming into greater focus as the BoC deliberates its next move.

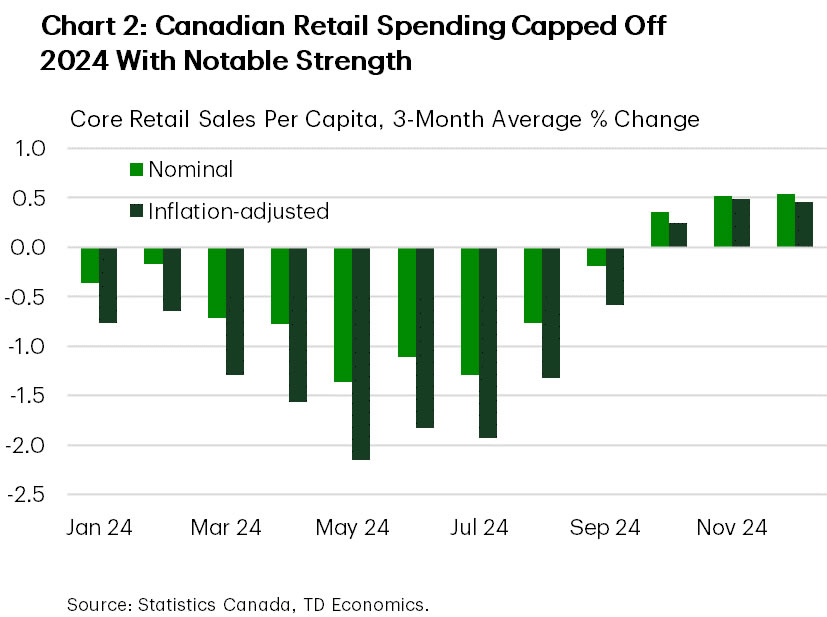

The cumulative 200 bps in interest rate easing since mid-2024, combined with the GST/HST tax break supported a 2.5% m/m surge in December retail spending, the largest increase in almost three years. Inflation-adjusted spending has strengthened over the past few months (Chart 2), supporting our call for an above-trend reading for Q4-2024 GDP growth. Even as spending momentum slows in the first quarter, the consumer is expected to be a pillar of strength for overall growth in 2025. That said, tariff uncertainty could stymie consumption progress to the extent that U.S. policy negatively affects Canada’s job market and wages.

Housing was the only dull point this week, as existing home sales slipped by 3% m/m in January. This was coupled with a surge in new listings that popped by the largest seasonally adjusted amount on record, pulling markets to the lower end of balanced market conditions. Tariff uncertainty may have weighed on buyer sentiment towards the end of January, but easing price pressures and further interest rate cuts should maintain a solid foundation for the housing market in coming quarters.

So where to from here? Our recently released Q&A discusses how the BoC may react to trade war scenarios. To take out insurance against escalating trade tensions, we think the BoC will prioritize the downside risk to growth and front-load interest rate cuts over the first half of the year, bringing the policy rate to 2.25%, the lower end of the Bank’s neutral range estimates.

U.S. – Data Dependent Decisions

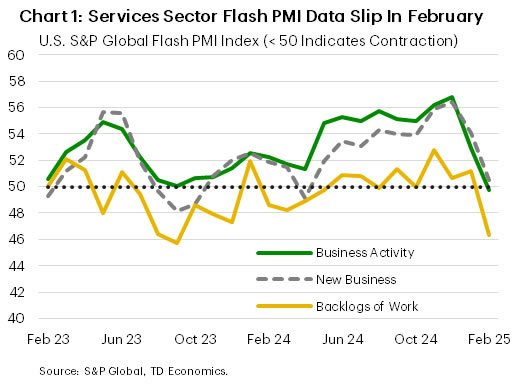

In the absence of major economic data, equities and Treasury yields were a smidge below where they started the week after reacting to a flash PMI release on Friday that suggested shrinking activity in the services sector in February (Chart 1). That said, the focus is on next week, when the second update of fourth quarter GDP and January’s Personal Income and Outlays report will give a fresh look at economic momentum and the first look at the Fed’s preferred inflation metric for 2025. Fed speakers provided some insights this week on why the data-dependent approach is key when looking to understand how inflation will evolve in a still-healthy economy.

At the start of the week Board member Christopher Waller gave a speech in Sydney with a title that left very little ambiguity, “Disinflation Progress Uneven but Still on Track. Rate Cuts on Track as Well.” The speech clearly outlined his views, including that monetary policy is restrictive and “putting downward pressure on inflation”, while economic momentum is holding up. Vice Chair Jefferson spoke later in the week, reaffirming the view that the economy and labor market are on solid footing, and the need to maintain a data dependent approach. Dr. Jefferson focused on the strength of household balance sheets and how they are supporting consumer spending. The key was that while they are generally in good position, households with lower- and middle-incomes “have less of a buffer of liquid assets than they did before the pandemic” and keeping an eye on balance sheet developments will help “inform forecasts of overall economic activity”.

One interesting concept to monitor was Dr. Waller’s acknowledgement that progress on cooling inflation in the early part of the year has been notably slow in past years. This could be attributable to “residual seasonality”– the idea that the price adjustments that usually come in the early part of the year are now bigger than they were typically and are showing up in the seasonally adjusted data that should have accounted for them. This is an interesting wrinkle, and Dr. Waller cited research that price pressures have tended to be greater in the first half of the year relative to the second in 16 of the past 22 years. The expectation then would be that even with stronger-than-expected inflation in the early part of the year, this effect should fade into the latter part of 2025, as it did in 2024.

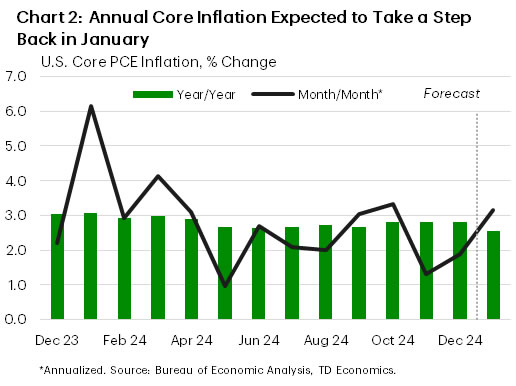

With speakers emphasizing the data-dependent approach, the focus will then be on the Personal Income and Outlays report on next Friday. The spending figures could be noisy, as cold weather and large fires in Los Angeles likely disrupted economic activity, so the focus will be on what happens with inflation. Current expectations are for the core PCE price index (the Fed’s preferred inflation gauge) to clock in at around 0.2%-0.3% month-on-month in January (2.6% year-on-year, Chart 2), but as Dr. Waller suggested even an upside surprise could be due to some residual seasonality. From our lens, the Fed is likely to remain on pause until the second quarter of this year, delivering two cuts by year-end, as healthy economic activity supports the labor market and price growth.

Weekly Economic & Financial Commentary: G10 Central Banks Ease Monetary Policy Further

Summary

United States: Housing Market Troubles to Continue

- Residential construction and existing home sales were muted in January, illustrating continued stress on the housing market amid elevated mortgage rates. Despite the pressure on interest-rate-sensitive sectors, underlying consumer demand is robust and has helped the labor market stand on firm footing.

- Next week: New Home Sales (Wed.), Durable Goods (Thurs.), Personal Income & Spending (Fri.)

International: G10 Central Banks Ease Monetary Policy Further

- The Reserve Bank of Australia began its easing cycle this week with a 25 bps rate cut. However, that appeared to be a tentative first easing step, given a still-tight labor market and as the central bank raised its medium-term inflation forecast. The Reserve Bank of New Zealand cut rates 50 bps this week but should slow the pace of rate cuts going forward, while elevated core inflation from Canada now means we expect the Bank of Canada to hold rates steady in March.

- Next week: India GDP (Fri.), Canada GDP (Fri.)

Credit Market Insights: Household Debt Balances Continue to Climb

- Total household debt increased by $93B in Q4 of last year to a new high of $18.04T. All categories of debt rose over the quarter, with credit card balances increasing the most, rising $45B to $1.21T. Though households continue to borrow, household debt has increased at a slower rate in recent quarters, suggesting consumers may be feeling the pinch of higher rates.

Topic of the Week: Republicans Approach a Budget Reconciliation Milestone

- Passing a budget reconciliation bill is critical to enacting Republicans' policy objectives for taxes and spending, and the next couple of weeks will mark an important first step in Congressional Republicans' efforts on this front. In this section, we discuss how the early innings of this process are shaping up.

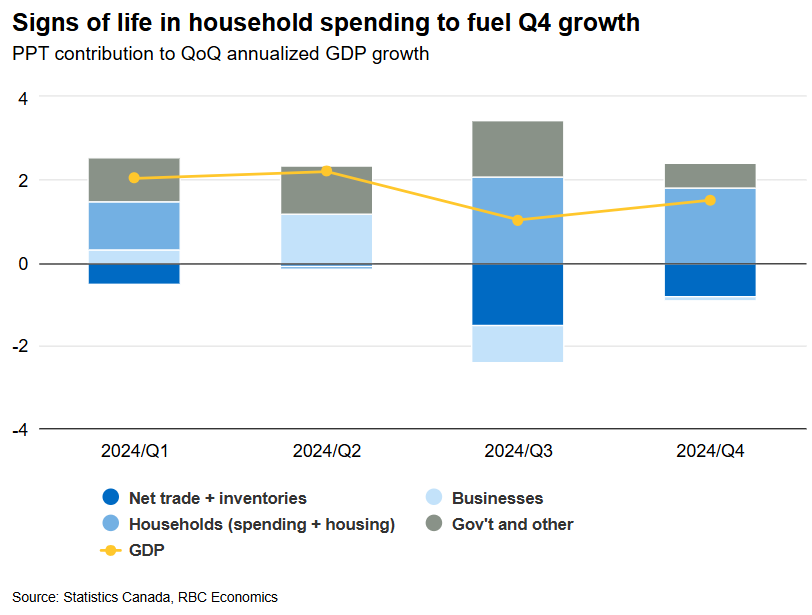

Focus on Canadian GDP Ahead of BoC’s March Interest Rate Decision

Canadian gross domestic product will be in focus after firmer labour market reports in December and January, and an upside headline inflation surprise increased the odds that the Bank of Canada will forego another rate cut in March.

Our expectation is for real GDP to rise 1.5% on an annualized quarter-over-quarter basis in Q4. Household spending has been showing signs of life in the wake of earlier interest rate cuts. We expect consumer spending rose 3% in Q4 on the largest retail sale volumes increase since Q3 2021. And, residential investment likely posted a second consecutive quarterly increase driven by higher building activity and surge in home resales. But, business spending has remained significantly softer—imports of machinery and equipment fell again in Q4, and an uncertain global trade backdrop will continue to weigh on business investment plans in 2025. Labour markets have firmed in recent months, but actual hours worked declined by 0.2% in Q4—the first quarterly drop in a year.

Growth momentum on a monthly basis appears to have faded later in the quarter. For December, we expect GDP edged up 0.1%, below Statistics Canada’s flash estimate a month ago of 0.2% growth and only partially retracing a 0.2% decline in November. Retail sales was robust in the December holiday shopping period—Canada’s tax holiday likely boosted a significant amount of goods consumption. But, accommodation and food services spending pulled back and December manufacturing sales came in substantially softer than preliminary estimates with details pointing to a contraction in output in the sector. Work stoppages in the transportation sector at ports and Canada Post in November and December will continue to distort the data, but Statistics Canada’s preliminary GDP estimate pointed on net to another decline in transportation and warehousing.

We expect the signs of life in the household sector and upside inflation surprises in recent months will be enough for the BoC to stand pat on interest rates in March for the first time since June 2024. The potential for significant tariff hikes remain a downside risk to economic growth and the interest rate outlook, but absent a trade shock, economic data is suggesting Canada’s economy may be faring better than initially feared.

Week ahead data watch

Next Thursday, job openings from SEPH will be watched closely for signs that labour market conditions are beginning to stabilize – job openings were still running 23% below year-ago levels at last count in November but postings reported separately from indeed.com rose in December.

U.S. Personal spending likely dipped by 0.1% in January, in line with the contractions in retail sales during that month. Personal spending is expected to grow by 0.6% in January, supported by higher transfer payments.

StatsCan will release the annual CAPEX intentions survey next Wednesday. The survey is an important annual gauge of business investment intentions but will likely not capture fully the impact that increased international trade uncertainty may be having on investment plans. The survey is typically conducted over the fall and early winter (September to January), which is before the period of significant tariff risks escalated.

Summary 2/24 – 2/28

Monday, Feb 24, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q4 | 0.60% | -0.10% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q4 | 0.30% | -0.80% |

| 09:00 | EUR | Germany IFO Business Climate Feb | 85.8 | 85.1 |

| 09:00 | EUR | Germany IFO Current Assessment Feb | 86.5 | 86.1 |

| 09:00 | EUR | Germany IFO Expectations Feb | 85.2 | 84.2 |

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 2.50% | 2.50% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 2.70% | 2.70% |

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | 2.90% | 2.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q4 | |

| Forecast: 0.60% | Previous: -0.10% | ||

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q4 | |

| Forecast: 0.30% | Previous: -0.80% | ||

| 09:00 | EUR | Germany IFO Business Climate Feb | |

| Forecast: 85.8 | Previous: 85.1 | ||

| 09:00 | EUR | Germany IFO Current Assessment Feb | |

| Forecast: 86.5 | Previous: 86.1 | ||

| 09:00 | EUR | Germany IFO Expectations Feb | |

| Forecast: 85.2 | Previous: 84.2 | ||

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | |

| Forecast: 2.70% | Previous: 2.70% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | |

| Forecast: 2.90% | Previous: 2.90% | ||

Tuesday, Feb 25, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany GDP Q/Q Q4 F | -0.20% | -0.20% |

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Dec | 4.30% | 4.30% |

| 14:00 | USD | Housing Price Index M/M Dec | 0.20% | 0.30% |

| 15:00 | USD | Consumer Confidence Feb | 103.3 | 104.1 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany GDP Q/Q Q4 F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Dec | |

| Forecast: 4.30% | Previous: 4.30% | ||

| 14:00 | USD | Housing Price Index M/M Dec | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 15:00 | USD | Consumer Confidence Feb | |

| Forecast: 103.3 | Previous: 104.1 | ||

Wednesday, Feb 26, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Jan | 2.50% | 2.50% |

| 00:30 | AUD | Construction Work Done Q4 | 0.80% | 1.60% |

| 07:00 | EUR | Germany GfK Consumer Sentiment Mar | -21.1 | -22.4 |

| 09:00 | CHF | UBS Economic Expectations Feb | 17.7 | |

| 15:00 | USD | New Home Sales Jan | 677K | 698K |

| 15:30 | USD | Crude Oil Inventories | 4.6M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Jan | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 00:30 | AUD | Construction Work Done Q4 | |

| Forecast: 0.80% | Previous: 1.60% | ||

| 07:00 | EUR | Germany GfK Consumer Sentiment Mar | |

| Forecast: -21.1 | Previous: -22.4 | ||

| 09:00 | CHF | UBS Economic Expectations Feb | |

| Forecast: | Previous: 17.7 | ||

| 15:00 | USD | New Home Sales Jan | |

| Forecast: 677K | Previous: 698K | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 4.6M | ||

Thursday, Feb 27, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Feb | 54.4 | |

| 00:30 | AUD | Private Capital Expenditure Q4 | 0.60% | 1.10% |

| 08:00 | CHF | GDP Q/Q Q4 | 0.20% | 0.40% |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 3.80% | 3.50% |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | -12.9 | |

| 10:00 | EUR | Eurozone Economic Sentiment Feb | 95.2 | |

| 10:00 | EUR | Eurozone Services Sentiment Feb | 6.6 | |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -13.6 | -13.6 |

| 12:30 | EUR | ECB Meeting Accounts | ||

| 13:30 | CAD | Current Account (CAD) Q4 | -3.2B | -3.2B |

| 13:30 | USD | Initial Jobless Claims (Feb 21) | 220K | 219K |

| 13:30 | USD | GDP Annualized Q4 P | 2.30% | 2.30% |

| 13:30 | USD | GDP Price Index Q4 P | 2.20% | 2.20% |

| 13:30 | USD | Durable Goods Orders Jan | 2.00% | -2.20% |

| 13:30 | USD | Durable Goods Orders ex Transport Jan | 0.40% | 0.30% |

| 15:00 | USD | Pending Home Sales M/M Jan | -1.30% | -5.50% |

| 15:30 | USD | Natural Gas Storage | -196B | |

| 23:30 | JPY | Tokyo CPI Y/Y Feb | 3.40% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Feb | 2.30% | 2.50% |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Feb | 2.50% | |

| 23:50 | JPY | Industrial Production M/M Jan P | -0.90% | -0.20% |

| 23:50 | JPY | Retail Trade Y/Y Jan | 4.00% | 3.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Feb | |

| Forecast: | Previous: 54.4 | ||

| 00:30 | AUD | Private Capital Expenditure Q4 | |

| Forecast: 0.60% | Previous: 1.10% | ||

| 08:00 | CHF | GDP Q/Q Q4 | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | |

| Forecast: 3.80% | Previous: 3.50% | ||

| 10:00 | EUR | Eurozone Industrial Confidence Feb | |

| Forecast: | Previous: -12.9 | ||

| 10:00 | EUR | Eurozone Economic Sentiment Feb | |

| Forecast: | Previous: 95.2 | ||

| 10:00 | EUR | Eurozone Services Sentiment Feb | |

| Forecast: | Previous: 6.6 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | |

| Forecast: -13.6 | Previous: -13.6 | ||

| 12:30 | EUR | ECB Meeting Accounts | |

| Forecast: | Previous: | ||

| 13:30 | CAD | Current Account (CAD) Q4 | |

| Forecast: -3.2B | Previous: -3.2B | ||

| 13:30 | USD | Initial Jobless Claims (Feb 21) | |

| Forecast: 220K | Previous: 219K | ||

| 13:30 | USD | GDP Annualized Q4 P | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 13:30 | USD | GDP Price Index Q4 P | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 13:30 | USD | Durable Goods Orders Jan | |

| Forecast: 2.00% | Previous: -2.20% | ||

| 13:30 | USD | Durable Goods Orders ex Transport Jan | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 15:00 | USD | Pending Home Sales M/M Jan | |

| Forecast: -1.30% | Previous: -5.50% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -196B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Feb | |

| Forecast: | Previous: 3.40% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Feb | |

| Forecast: 2.30% | Previous: 2.50% | ||

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Feb | |

| Forecast: | Previous: 2.50% | ||

| 23:50 | JPY | Industrial Production M/M Jan P | |

| Forecast: -0.90% | Previous: -0.20% | ||

| 23:50 | JPY | Retail Trade Y/Y Jan | |

| Forecast: 4.00% | Previous: 3.70% | ||

Friday, Feb 28, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Private Sector Credit M/M Jan | 0.60% | 0.60% |

| 05:00 | JPY | Housing Starts Y/Y Jan | -2.60% | -2.50% |

| 07:00 | EUR | Germany Import Price Index M/M Jan | 0.70% | 0.40% |

| 07:00 | EUR | Germany Retail Sales M/M Jan | 0.10% | -1.60% |

| 07:45 | EUR | France Consumer Spending M/M Jan | -0.80% | 0.70% |

| 07:45 | EUR | France GDP Q/Q Q4 | -0.10% | -0.10% |

| 08:00 | CHF | KOF Economic Barometer Feb | 102.1 | 101.6 |

| 08:55 | EUR | Germany Unemployment Change Jan | 15K | 11K |

| 08:55 | EUR | Germany Unemployment Rate Jan | 6.20% | 6.20% |

| 13:00 | EUR | Germany CPI M/M Feb P | 0.40% | -0.20% |

| 13:00 | EUR | Germany CPI Y/Y Feb P | 2.30% | |

| 13:30 | CAD | GDP M/M Dec | 0.30% | -0.20% |

| 13:30 | USD | Personal Income M/M Jan | 0.30% | 0.40% |

| 13:30 | USD | Personal Spending Jan | 0.20% | 0.70% |

| 13:30 | USD | PCE Price Index M/M Jan | 0.30% | |

| 13:30 | USD | PCE Price Index Y/Y Jan | 2.60% | |

| 13:30 | USD | Core PCE Price Index M/M Jan | 0.20% | |

| 13:30 | USD | Core PCE Price Index Y/Y Jan | 2.80% | |

| 13:30 | USD | Goods Trade Balance (USD) Jan P | -114.9B | -122.0B |

| 13:30 | USD | Wholesale Inventories Jan P | 0.10% | -0.50% |

| 14:45 | USD | Chicago PMI Feb | 40.3 | 39.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Private Sector Credit M/M Jan | |

| Forecast: 0.60% | Previous: 0.60% | ||

| 05:00 | JPY | Housing Starts Y/Y Jan | |

| Forecast: -2.60% | Previous: -2.50% | ||

| 07:00 | EUR | Germany Import Price Index M/M Jan | |

| Forecast: 0.70% | Previous: 0.40% | ||

| 07:00 | EUR | Germany Retail Sales M/M Jan | |

| Forecast: 0.10% | Previous: -1.60% | ||

| 07:45 | EUR | France Consumer Spending M/M Jan | |

| Forecast: -0.80% | Previous: 0.70% | ||

| 07:45 | EUR | France GDP Q/Q Q4 | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 08:00 | CHF | KOF Economic Barometer Feb | |

| Forecast: 102.1 | Previous: 101.6 | ||

| 08:55 | EUR | Germany Unemployment Change Jan | |

| Forecast: 15K | Previous: 11K | ||

| 08:55 | EUR | Germany Unemployment Rate Jan | |

| Forecast: 6.20% | Previous: 6.20% | ||

| 13:00 | EUR | Germany CPI M/M Feb P | |

| Forecast: 0.40% | Previous: -0.20% | ||

| 13:00 | EUR | Germany CPI Y/Y Feb P | |

| Forecast: | Previous: 2.30% | ||

| 13:30 | CAD | GDP M/M Dec | |

| Forecast: 0.30% | Previous: -0.20% | ||

| 13:30 | USD | Personal Income M/M Jan | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | USD | Personal Spending Jan | |

| Forecast: 0.20% | Previous: 0.70% | ||

| 13:30 | USD | PCE Price Index M/M Jan | |

| Forecast: | Previous: 0.30% | ||

| 13:30 | USD | PCE Price Index Y/Y Jan | |

| Forecast: | Previous: 2.60% | ||

| 13:30 | USD | Core PCE Price Index M/M Jan | |

| Forecast: | Previous: 0.20% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Jan | |

| Forecast: | Previous: 2.80% | ||

| 13:30 | USD | Goods Trade Balance (USD) Jan P | |

| Forecast: -114.9B | Previous: -122.0B | ||

| 13:30 | USD | Wholesale Inventories Jan P | |

| Forecast: 0.10% | Previous: -0.50% | ||

| 14:45 | USD | Chicago PMI Feb | |

| Forecast: 40.3 | Previous: 39.5 | ||