Sample Category Title

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3530; (P) 1.3558; (R1) 1.3593; More.....

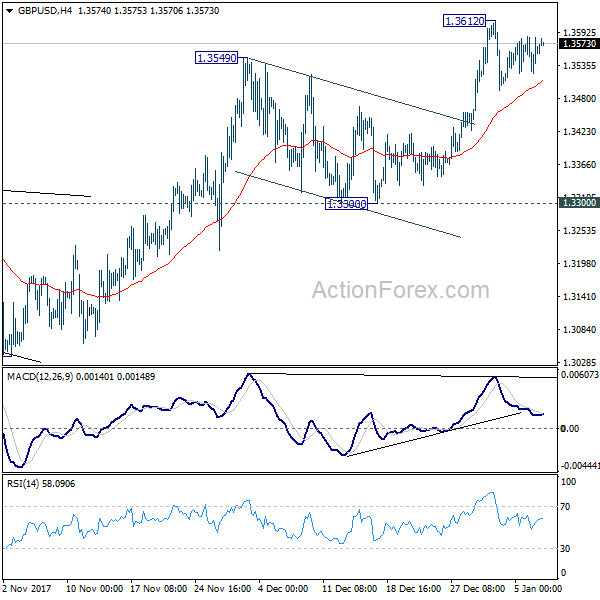

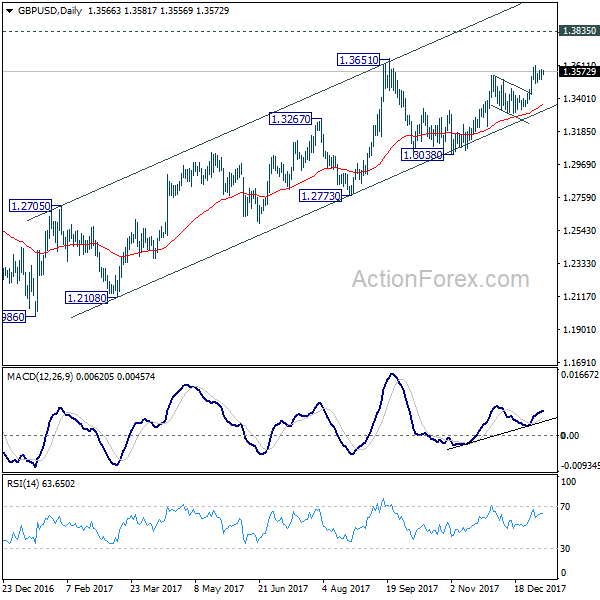

GBP/USD is staying in consolidation from 1.3612 temporary top. Intraday bias remains neutral first. As long as 4 hour 55 EMA (now at 1.3508) holds, further rally is expected. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, sustained break of 4 hour 55 EMA will turn focus back to 1.3300 support instead.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9745; (P) 0.9764; (R1) 0.9791; More....

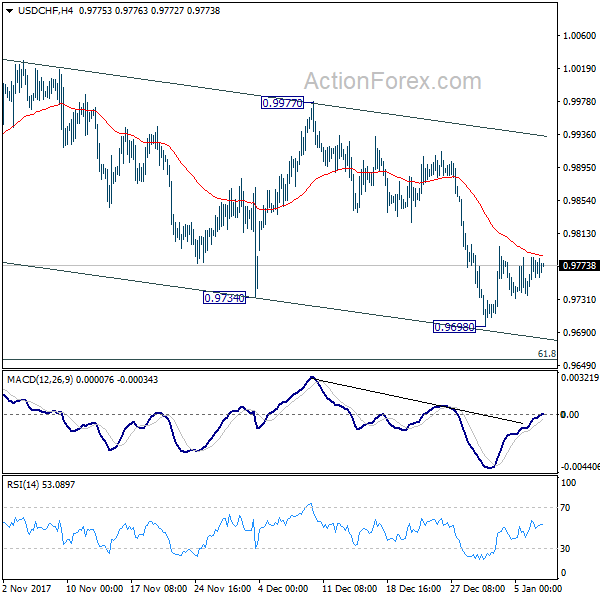

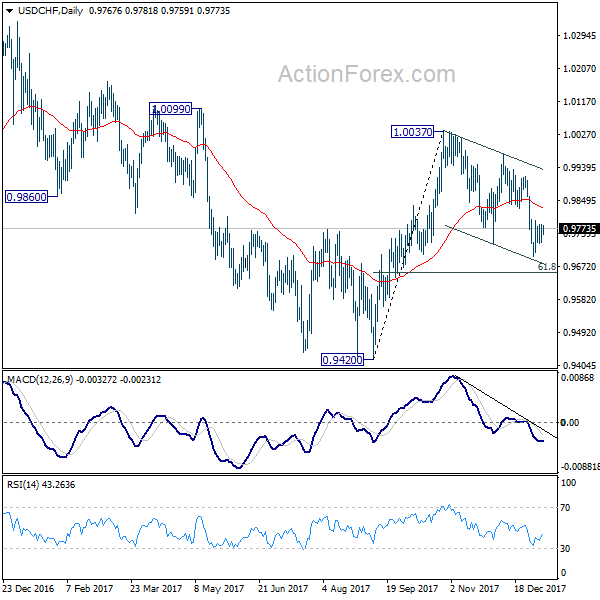

USD/CHF is still staying in corrective trading above 0.9689 temporary low. Intraday bias remains neutral at this point. As long as 4 hour 55 EMA (now at 0.9785) holds, deeper fall is mildly in favor. But we'd expect 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. Sustained break of 4 hour 55 EMA will argue that the correction from 1.0037 has completed and turn focus to 0.9977 resistance for confirmation.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

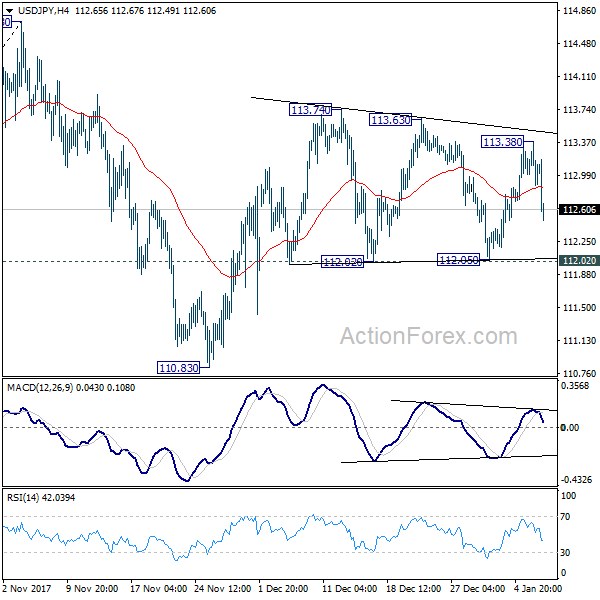

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.85; (P) 113.11; (R1) 113.35; More...

USD/JPY drops sharply after hitting 113.38. But after all, it's staying in range of 112.02/113.74. Intraday bias remains neutral at this point. Also, outlook remains cautiously bullish as long as 112.02 holds and further rise is in favor. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Yen Jumps as BoJ Lowers Long Dated JGB Purchase, Aussie Rebounds on Housing Data

Yen strengthens against all major currencies in Asian session on news that BoJ lowers its long-dated JGB purchases. Strength in Yen is followed by Aussie, which is lifted by strong housing data. On the other hand, Dollar and Euro are both trading weakly. Comments from Fed officials overnight gave no extra confidence to the markets that Fed would hike three more times this year, not to mention four. Meanwhile, Euro stays soft as recent rally lost steam.

BoJ cut 10-25 years JGB purchase by JPY 10b

Yen surges broadly today as data showed BoJ has cut its long-dated JGB purchases in market operations. That's seen as a sign by many of BoJ is finally moving towards stimulus exit. Today, BoJ offered to buy JPY 190b of JGBs with 10 to 25 years maturity. That's JPY 10b lower from the prior tender on December 28. Besides, BoJ also lower the offer on 25 to 40 years maturity JGBs by JPY 10b to JPY 90b. Nonetheless, it should be emphasized that it's far still early for BoJ to start stimulus exit as inflation remains way off target.

Also, it's still uncertain whether BoJ Governor Haruhiko Kuroda's term would be renewed this year. Prime Minister Shinzo Abe said during the weekend that "Gov. Kuroda has met my expectations with job availability at a 43-year high," and "I want him to keep up his efforts". But Abe also noted that "I haven't made up my mind" on who's going to lead BoJ after Kuroda's term expires in April.

Released from Japan, labor cash earnings rose 0.9% yoy in November, above expectation of 0.6% yoy.

Aussie rebounds on strong building approvals

Australian dollar rebounds notably today following strong housing data. Building approvals rose 11.7% mom in November, versus consensus of -1.0% mom fall. AUD/USD dipped briefly yesterday after the government forecasts iron ore price to drop 20% this year. While loss was very limited, it should be noted that upside momentum in AUD/USD has been diminishing for a while. Hence, we're not expecting a 0.7896 near term resistance on the next move. Aussie will look into retail sales and China data later in the week.

North and South Korea delegates meet in the "Peace House"

North and South Korea holds a rare high-level talks in the so-called Peace House in Panmunjom, a village in the Demilitarized Zone between the two countries. North Korea said that it would send athletes and a high-level delegation to the Winter Olympics in South Korea in February. The delegation will include athletes and supporters, amongst others. The North also expressed the willingness to resolve inter-Korea issues through dialogues. On the other hand, delegates from the South wants both nations to march together at the Games and proposed reunions of families during the upcoming Lunar New Year.

More bet on BoC hike this month

Hopes for a BOC rate hike, by 25 bps, at next week's meeting has surged to 85%, thanks to the Business Outlook and Senior Loan Office surveys for 4Q17 and the strong job market data which has already sent the loonie to a 3 months' higher last week. Canadian government bond prices generally weakened across the yield curve, sending 2-year yields lower 1.784% and 10-year yields down to 2.159%. The Business Outlook survey revealed that a net 56% of firms admitted "some" or "significant" difficulty in meeting additional demand. This marks the highest reading for a decade. Meanwhile, firms' capex and hiring intentions strengthened in 4Q17. However, inflation expectations remained subdued, a net 56% of respondents expecting inflation to stay at or below 2% over the next 2 years, compared with 59% in the previous survey.

Atlanta Fed Bostic: May not need three hikes per year

Atlanta Fed President Raphael Bostic said that he agrees to Fed's "slow removal" of monetary policy accommodations. But he emphasized "I would caution that that doesn't necessarily mean as many as three of four moves per year." He pointed to the surveys should that "individuals may not be completely convinced" on Fed's commitment or ability to reach the 2% inflation target. And "this possibility is one factor that might argue for being somewhat more patient in raising rates." Bedsides, he noted that the so called "neutral" rate could have dropped to "close to 2%". And Fed only needs to hike two or three more times before monetary policy is no longer considered "loose".

On the other hand, San Francisco Fed President John Williams said Fed should hike three times this year. He noted that "we're in a pretty good situation: the economy is doing great, everyone expects us to raise rates gradually ... and if the data change we can respond to that." He expressed that "I'm not worried about inflation suddenly taking off," and "something like three rate hikes makes sense to me".

Looking ahead

Swiss unemployment rate, foreign currency reserves and retail sales will be featured in European session. Eurozone will release unemployment rate, German industrial production and trade balance. Later in the data, Canada will release housing starts.

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.85; (P) 113.11; (R1) 113.35; More...

USD/JPY drops sharply after hitting 113.38. But after all, it's staying in range of 112.02/113.74. Intraday bias remains neutral at this point. Also, outlook remains cautiously bullish as long as 112.02 holds and further rise is in favor. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | JPY | Labor Cash Earnings Y/Y Nov | 0.90% | 0.60% | 0.60% | 0.20% |

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Dec | 0.60% | 0.30% | 0.60% | |

| 0:30 | AUD | Building Approvals M/M Nov | 11.70% | -1.00% | 0.90% | -0.10% |

| 5:00 | JPY | Consumer Confidence Index Dec | 45 | 44.9 | ||

| 6:45 | CHF | Unemployment Rate Dec | 3.00% | 3.00% | ||

| 7:00 | EUR | German Industrial Production M/M Nov | 1.80% | -1.40% | ||

| 7:00 | EUR | German Trade Balance Nov | 20.7B | 19.9B | ||

| 8:00 | CHF | Foreign Currency Reserves Dec | 738B | |||

| 8:15 | CHF | Retail Sales Real Y/Y Nov | -2.50% | -3.00% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 8.70% | 8.80% | ||

| 13:15 | CAD | Housing Starts Dec | 240K | 252K |

Market Morning Briefing: Dollar Index Has Moved Up

STOCKS

Dow (25283.00, -0.05%) was quiet yesterday with not much of movement. There is scope of further rise towards 25400-25600 before a corrective dip or sideways consolidation is seen. Overall the index looks bullish.

Dax (13367.78, +0.36%) closed just below resistance at 13400 and while that holds, the index could probably pause for sometime before attempting to move higher. Failure to pause just now could take it higher towards 13600-13800 in the next couple of weeks.

Nikkei (23843.70, +0.54%) saw a dip as the resistance near 113.50 produced a rejection on the Dollar Yen. Weekly resistance is visible near 24000 and that could be tested before a sharp correction sets in.

Shanghai (3412.37, +0.08%) is eventually moving up and could test 3450. Near term looks bullish.

Nifty (10623.60, +0.61%) could face rejection from levels near 10750-10800 which could push it back towards10400 while Sensex (34352.79, +0.58%) is likely to come off from 34500-34650 while above 34200 levels.

COMMODITIES

Gold (1319.11) is in a pause mode after rallying from levels near 1240 in Dec’17. A small pause is possible with a maximum extension towards 1300 on the downside before another leg of rally sets in. Medium term looks bullish.

Brent (68.22) and WTI (62.25) have both moved up quite a bit. As mentioned yesterday, Brent could test immediate resistance near 70 on the upside while WTI could test 63 in the next few sessions.

Copper (3.2330) has come off further and is likely to move down towards 3.20-3.15 in the coming sessions. Near term looks bearish.

FOREX

Dollar Index (92.267) has moved up and seems to be on course to test 92.5-92.75, seen as near term resistance on 3 day candles and 3 day line charts. Simultaneously, we saw Euro (1.1971) break below 1.20, which could now move down towards crucial support near 1.19-1.195 (seen on 3 day and weekly candles) as the Dollar Index moves towards 92.5-92.75.

Dollar-Yen (112.58) as per expectations has seen a dip from resistance level near 113-113.25 and might now test support at 112.50 on the daily candles. This could prove to be a crucial support, which would see a break if Dollar Index goes back to levels below 92.

The Pound (1.3579) is continuing its trade in the narrow range of 1.35-1.36 and we might have to wait for a couple of sessions to get further directional clarity.

Aussie (0.7858) is pausing in its uprise beyond the 200 day moving average on the weekly line charts and should be ranged between 0.78-0.786 for the next couple of sessions.

Dollar-Rupee (63.5050) rose yesterday on back of Dollar strength against the Euro and might see trade within 63.40-63.60 today, with 63.20 acting as a strong support.

INTEREST RATES

The US 10Yr (2.4836%), US 5 Yr (2.2886%) and US 30 Yr (2.8136%) haven’t seen much movement yet. We can expect minimal movement in US yields till the CPI data release on 12th Jan. In case, the data reflects higher inflation due to the recent rise in crude prices, we could see the 5 Yr move past resistance near 2.3 and the 30 Yr could move closer to resistance near 2.9%-3%.

The German-US 10 Yr Yield Spread (-2.0553%) has fallen since yesterday and instead of moving up towards -2%, it could first test support near -2.06%—2.07%.

Japanese 10 Yr Yield (0.068%) has been rising in the last few days, having broken resistance near 0.06% on the short term charts and is now around long term resistance near 0.07%. This has brought the US-Japan 10 Yr yield spread down to 2.4156% and we might see a test of support near 2.36%-2.37% in case the Japanese 10 Yr breaches long term resistance near 0.07%.

Top Weighs On Euro

EUR/USD is in danger of forming a double top after the failure at 1.21. The New Zealand dollar was the top performer while the euro lagged. Japan returns from holiday Tuesday. There are currently 7 Premium trades in progress, 4 of which are in profit, 2 in a loss and 1 unchanged.

EUR/USD slid 60 pips to 1.1960 on Monday in a soggy start to the week. The record net long in CFTC positioning was the talk of the trade and surely made a few longs nervous.

The technicals are another reason to worry as a potential double top coincides with the completed inverted Head-&-Shoulder formation along the September high of 1.2092. The weakness emerges despite upbeat eurozone retail sales and business confidence data.

In the US, there was also a dovish hint from Atlanta Fed President Bostic who said he thinks the FOMC should hike 2-3 times this year rather than 3-4 but his comments didn't have an effect on the market.

In terms of economic data, the main headlines emerged from the Bank of Canada's business outlook survey. It showed increasing optimism from businesses and a line from the central bank saying that excess capacity has been absorbed, except in the resource sector.

The report solidified calls for a BOC hike next week, with the probability up to 86%. See Ashraf's detailed piece on the loonie & CAD here. What's also more likely is a hawkish statement and a return to the 'sunny' Stephen Poloz from early in his term. If so, the loonie could continue back down to its 2017 lows.

The S&P 500 rallied for a fifth day to another record at 2747.

Looking ahead, Japan returns from holidays and that will put a renewed focus on the yen. The November report on Japanese labor cash earnings is due at 0000 GMT and forecast to show just a 0.6% y/y rise.

Dollar Bears Got Too Far Over Their Skis

Dollar bears got too far over their skis

The USD dollar has a spring in its step to start the week. But with little to no evidence that the broader US dollar downtrend has run its course, the short-term correction is little more than the recent buildup on EURUSD longs has left dollar bears too far over their skis and vulnerable to a position squeeze given the lack of near-term bullish Euro catalysts.

With no imminent threat from a more aggressive policy shift from US Federal Reserve. Most traders will feel comfortable selling USD dollar rallies but are likely waiting for a more pronounced correction or a stronger signal to re-engage dollar shorts. In the meantime, they’re equally content to take to the sidelines keeping the powder dry but most of all avoiding any early year losses. There is nothing worse than digging oneself out of a hole at the beginning of the year so best to have your ducks in a row before testing the waters.

Oil prices

Protest in Iran, and decreasing US crude inventories are providing a stable floor on WTI. And while the frigid temperatures in the US North East are pressuring heating oil, travel chaos sparked by heavy snows is keeping driver off the roads adding to higher inventories of gasoline which could temper price action. And while speculative positioning is stretched in record territory increasing the potential for a position squeeze, there’s no arguing the trend is your friend in this move. And with geopolitical risk extending from Tehran to Venezuela’s economic demise, the market remains on a bullish tack.

Gold

Gold prices edged a bit lower overnight after the US dollar took back some lost ground from the EUR.But as the USD mini-correction ran out of steam, gold prices quickly retraced earlier loses. Given the very tight current correlation between Gold and USD coupled with relatively sparse news flow, bullion dealers will be keying on Fed speak to provide a catalyst for the dollar ahead of Friday key US CPI, but so far the Fed rhetoric as contributed few sparks.

Equity Markets

With absolutely no threat from the US Federal Reserve who is guiding the market to a well-telegraphed three rate hikes this year and the ECB ambling into an equally well-telegraphed temperate monetary policy for 2018, equity investors continue to enjoy the relative calm exuded by centeral banks.

And with earning season brings renewed optimism, but in the absence of any significant news flow overnight investors sat idle, but none the less the S&P managed to eke out a small gain despite US 10-year Treasury yield sticky around the 2.48% level.

G-10

The Euro

The latest IMM data suggests speculators increased their largest EUR long position since October 2013. And with the Euro falling to take out 2017 highs after the weaker NFP there been a bit of a clear out of weaker longs this week. But market positioning is still substantial, and the dollar bears are playing more of a tactical game early in the week and not showing a competitive bias to accumulate EURO. Also, the Euro rate curve is taking a pause this week after the EONIA curve steepened last week when the market started repricing ECB risk more aggressively.

The Japanese Yen

There’s a disconnect between USDJPY and broader US dollar trend that’s likely a result of EURJPY steering the JPY ship these days. And with the Euro in consolidation mode, it looks like we’re stuck in the range bound malaise.

Looking for a medium-term trade on USDJPY is like sitting on a razor’s edge. We know JPY could weaken given the favourable global risk conditions and rising global yields. But the vast unknown remains the hawkish tail risks to the speed of the BoJ’s “stealth taper”, which in turn could accelerate repatriation into Japan.

Australian Dollar

The broader commodity space continues to look medium term bullish especially oil and hard commodities on the back of the stronger global growth narrative. This period of consolidation should not be confused with anything other than just that. However, commodity block traders are pilling their risk into the Canadain Dollar in the wake of last week stupendous employment data and a probable Bank of Canada rate hike later this month.The speculative rotation is taking a bit of focus away from the Antipodeans early this week.

Via Reuters AUSTRALIA’S MINING INDEX HITS NEAR 5-YR HIGH AS IRON ORE PRICES RISE –

The Chinese Yaun

Despite the mini-dollar correction yesterday the overtones from the mainland suggest regulators are determined to accelerate Yuan exchange rate reform after a two-year hiatus. Given the probable inclusion of CGB’s in Global Bond Indexes later in 2018, the Yuan is likely to keep strengthening through the first part of the year.

Asia FX

While there’s tangible evidence that trends tend to reverse in January on their volition, however unofficial jawboning from an unnamed Korean official was enough to upset the $ Asia apple cart yesterday

The Korean Won

After breaking the critical USDKRW 1060 level driven exporter and foreign fast money flow, vague rumours of intervention chatter started to circulate sending the quick money types into a tizzy posting the USDKRW 1% higher. If recent history tells us anything about verbal intervention is that it’s entirely ineffective in reversing or slowing down domestic currency appreciation

None the less, it spooked the $Asia complex on the assumption that other regional central banks will be just as vigilant against currency appreciation, when in fact nothing could be further from the truth.

With diplomacy between North Korea and South Korea on tap today, the easing of regional tensions could play favourably into the Won and regional currency sentiment today.

The Malaysia Ringgit

The Ringgit held its ground overnight as unlike the BOK the BNM has indicated that they welcome a stronger currency to fend off inflationary pressure . Mind you the Ringgit remains relatively undervalued on a trade-weighted basis.

However, the broader picture remains favourable for further Ringgit appreciation in the lead up to the BNM policy decision later in the month especially in the backdrop of a soft dollar trend and surging Oil prices.

The Philippines Peso

The Philippines Peso suffered a LIFO event after most of the regional currency sentiment wilted on the intervention chatter. The PHP was in the process of playing catch up to region peers ( Last In) but took the biggest hit ( First Out) on the regional currency wobble.

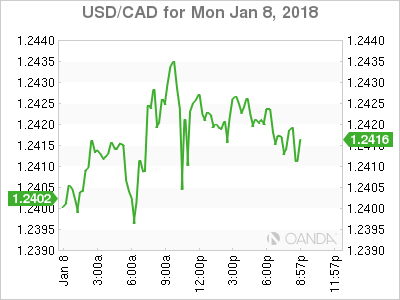

USD/CAD Canadian Dollar Flat As BoC Ponders January Rate Hike

The Canadian dollar was slightly lower agains the US dollar at the start of the week. The loonie is up 1.17 percent versus the greenback so far in 2018. The American currency has not had the best of starts this year. The tax reform and December interest rate hike by the Fed had already been priced in and investors are looking ahead to a highly political year for the USD. Canadian employment was a huge surprise to the upside with another massive job gain. The number of jobs added to the economy in December was 78,600 much higher than the forecasted 1,000. The monster gain has prompted Canadian financial institutions to update their forecasts for the January policy meeting of the BoC with the majority expecting a rate hike. The loonie continued rising after the slow start to the year of the US and the boost from higher oil prices.

The fate of NAFTA remains a possible threat to the CAD, but today’s release of the Bank of Canada (BoC) Business survey shows that companies are not suffering extra anxiety in their outlook. The BoC hiked twice in 2017 before a slowdown in the economy forced the central bank to adopt a more neutral tone. Governor Poloz ended the year with a speech focusing on the topics that kept him up at night but the solid December jobs report and the BoC Survey have all but convinced the market that a rate hike will be announced on the January 17 central bank meeting. Societe Generale is forecasting a price level of 1.2050 or lower if the Bank of Canada (BoC) goes ahead with life of the interest rate to 1.25 percent next week.

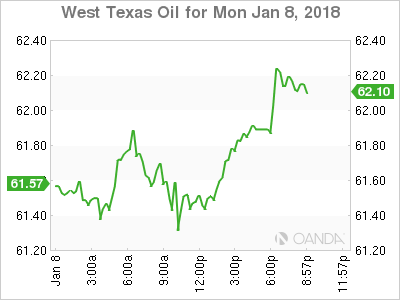

Oil is still near 2015 highs but as supply disruptions or geopolitical risks remain investors are looking at higher production from US producers starting to ramp up. The Organization of the Petroleum Exporting Countries (OPEC) deal to cut production enlisted major producers, but those not included could be the biggest winners if prices remain in current levels.

The USD/CAD rose 0.09 percent on Monday. The currency pair is trading at 1.2422 as the USD seeks to regain traction after a disappointing U.S. non farm payrolls (NFP) report on Friday, January 5 and a monster number of jobs gain in Canada on the same day. The near 80,000 added jobs convinced major institutions to change their forecast for the January 17 central bank meeting. A 25 basis points has been forecasted by most major banks with Royal Bank of Canada being one of the outliers who does expect higher rates, but later in the year. The BoC is expected to lift rates 2 or 3 times this year, the same as the U.S. Federal Reserve. The Canadian central bank has been aware of the high level of household debt but improving economic indicators could hasten the monetary policy decision.

West Texas Intermediate is trading at 61.87. The price of crude remains high as political tension in Iran and the North Sea pipeline maintenance work continues. Drilling has not been particularly strong in the US but that is expected to change soon as weather improves and shale operations could ramp up at a higher rate explaining the lack of new oil rigs.

Geopolitical risk in the oil market has been high as various members of the Organization of the Petroleum Exporting Countries (OPEC) are facing political headwinds. The big three: Saudi Arabia, Iraq and Iran have all experienced different forms of uncertainty as leadership has either changed or had to respond to different challenges. The relationship between them has also been frayed which could put into question how effective the OPEC’s production cut agreement will remain in place, or even the organization if there is a major disagreement between its biggest producers.

Market events to watch this week:

Wednesday, January 10

4:30am GBP Manufacturing Production m/m

10:30am USD Crude Oil Inventories

7:30pm AUD Retail Sales m/m

Thursday, January 11

8:30am USD PPI m/m

8:30am USD Unemployment Claims

Friday, January 12

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Gold Rally Takes Pause As Investors Look For Cues

After another week of gains, gold is trading quietly in the Monday session. In North American trade, the spot price for an ounce of gold is $1319.03, down 0.07% on the day. On the release front, it’s a quiet start to the trading week, with no major US releases.

On Friday, the US posted mixed employment numbers. Nonfarm Payrolls dropped to 148 thousand, down from 228 thousand in the previous release. This was well below the estimate of 190 thousand. There was better news from wage growth, which edged up to 0.3%, matching the forecast. This marked a 3-month high. The unemployment rate remained unchanged, at a sizzling 4.1%.

Gold prices continue to head higher, as the metal rolled off a fourth straight winning week. Gold has jumped an impressive 5.5% since December 11, despite a strong US economy and a December rate hike from the Federal Reserve. On Friday, gold touched a high of $1326, its highest level since mid-September. Risk appetite on the part of investors remains high, but for now, this has not dampened enthusiasm for gold. With the US dollar showing broad losses in recent days, gold could continue to rally.

Another Quarter of Solid Sentiment from Canadian Firms

Sentiment among Canadian firms remained positive during the final quarter of 2018, according the Bank of Canada's quarterly Business Outlook Survey (BOS).

The 'headline' indicator of the balance of firm opinion on future sales ticked down a notch (to 19% on balance, from 31% previously), but remained in positive territory. The broader-based indicator of future sales, which summarizes order books, advance bookings, sales inquiries and similar information, also ticked down slightly, but at 55% still marked its third highest reading on record (last quarter saw the second highest reading). Firms cited increased competition, notably in the retail sector as dampening the sales outlook.

On the investment and hiring front, it was a positive story. The balance of opinion on investment intentions rose to 29% as the share of firms planning to reduce investment fell. It is important to remember that these questions are relative to the past 12 months, which have seen a healthy recovery of investment activity, making today's figures more impressive. A similar improvement was seen in hiring plans, where the balance of intentions ticked up to +40%. Hiring intentions were reportedly driven by the service sector, and by firms located in Central Canada. Firms also reported anticipating more difficulty meeting an unexpected increase in demand, with labour shortages more widely reported than in the previous survey.

On the price front, firms are now expecting an increase in the pace of input cost growth, on balance, but expect competition to limit their ability to pass these costs on (the balance of opinion on output prices was 0%). Inflation expectations remain well within the control range, but the share of firms expecting inflation over the next two years to fall into the 2% to 3% range climbed 14 percentage points.

Senior Loan Officer Survey

Released alongside the BOS, the Senior Loan Officer Survey indicated that lending conditions eased slightly as spreads on lending to corporate borrowers narrowed. This ended a five quarter run of effectively unchanged lending conditions. It was also reported that both price and non-price conditions eased in the Prairies as activity in the resource sector continued to increase. On the other side of the coin, demand for credit reportedly rose after a flat reading in the prior survey.

Key Implications

This was a solid report. Headline sales expectations may have ticked down a hair, but overall sentiment remains robust. This is best captured by the Bank of Canada's summary measure (The "BOS indicator"), which rose to within a hair of its 2017Q2 reading (which presaged last year's back-to-back rate hikes).

Reinforcing the strength, while the spectre of a poor outcome from NAFTA renegotiations continues to hang over business leaders, healthy US demand and a supportive loonie were also reported as supporting the business outlook.

Particularly interesting in the current context, additional focus was given to wage pressures. Pressure is now seen as positive in all regions, and while minimum wage changes may be driving the gain in some areas, so too are healthy labour markets that are leading to reported challenges in recruiting and retaining staff.

When the wage outlook and its underlying drivers are taken together with the tick-up in investment intentions and the healthy outlook for hiring (even more impressive in light of the recent string of strong jobs numbers), the picture that emerges is one of economic strength. Today's report should thus provide Bank of Canada Governor Stephen Poloz with further confidence that emergency level interest rates are no longer needed, with the next policy interest rate increase to come next week (January 17th)