Sample Category Title

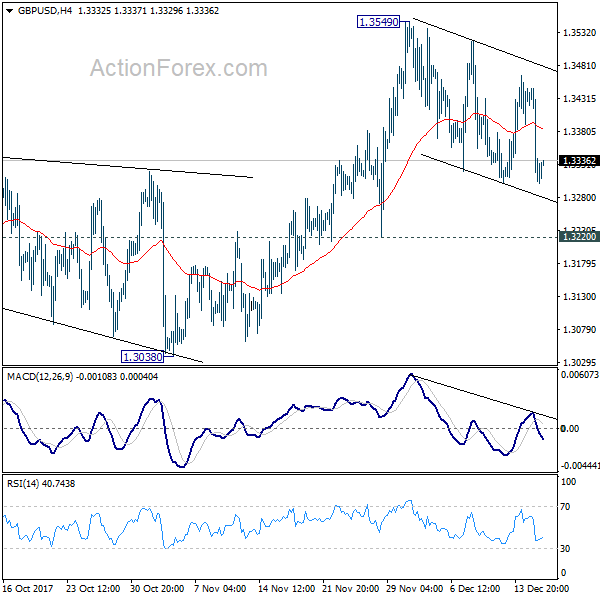

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3263; (P) 1.3354; (R1) 1.3410; More....

GBP/USD's correction from 1.3549 is still extending and intraday bias remains neutral at this point. As long as 1.3220 support holds, we'd favor another rise. Break of 1.3549 will target 1.3651 high next. Break there will resume medium term rally from 1.1946. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

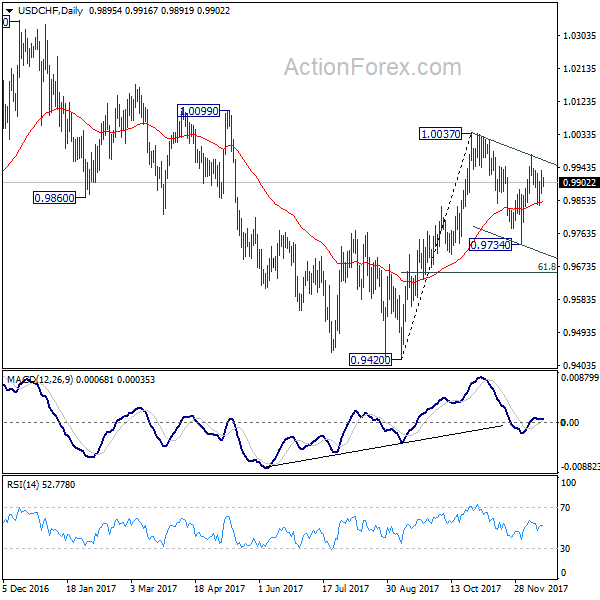

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9870; (P) 0.9902; (R1) 0.9931; More....

Intraday bias in USD/CHF remains neutral for the moment. On the upside, above 0.9977 will resume the rebound from 0.9734 for 1.0037 resistance. Break there will resume whole rally from 0.9420 and target 1..0342 key resistance next. On the downside, below 0.9839 will likely extend the correction from 1.0037 through 0.9734. But in that case, we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

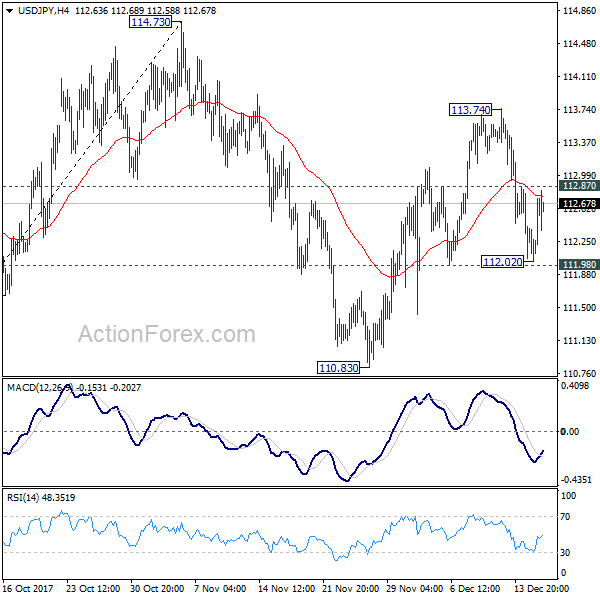

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.16; (P) 112.45; (R1) 112.87; More....

Intraday bias in USD/JPY remains neutral for the moment. With 111.98 intact, we'd favor another rise in the pair. Above 112.87 minor resistance will turn bias to the upside for 113.74. Break will target 114.73 key resistance. However, firm break of 111.98 support will extend the decline from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Market Morning Briefing: Dollar-Yen Has Also Moved Up On Back Of Perceived Dollar Strength

STOCKS

Dow (24651.74, +0.58%) could spend a few sessions sideways before trying to move up towards 24800 or higher. Near term looks bullish.

Dax (13103.56, +0.27%) has risen from 13000 levels but while below 13150, chances of a fall again towards 12900 remain on the cards. A sustained break above 13150 is needed to initiate further upmove towards 13300 or higher.

The falls from levels near 23000 on Nikkei (22820.81, +1.19%) have not been able to take the index below 22000. While Nikkei is trying to re-attempt a test of 23000 on the upside, it could again come off towards 22600 in the next few sessions. But note that continuous testing of 23000 may give way on the upside for the longer term, strengthening the bulls towards 23200-23400 on the very long term.

Shanghai (3263.75, -0.07%) is headed towards 3250 and is likely to move to lower levels in the coming sessions. 3250-3230 is the target for the near term.

Nifty (10333.25, +0.79%) made an intra-day high at levels above 10350 before closing slightly lower on Friday. With the Gujarat Election results on the cards, the Nifty is likely to move up further if the BJP wins. A test of 10400-10450 seems likely. Note immediate resistance is visible near 10500.

Sensex (33462.97, +0.65%) has immediate resistance near 33750, but may likely move up today towards 34000 levels.

COMMODITIES

Gold (1255.30) is stable just now and is likely to trade within 1265-1250 region for a couple of sessions. Near to medium term looks bullish.

Brent (63.32) and WTI (57.35) are almost stable at previous levels. WTI could slightly rise towards 58.0-58.5 before trying to break higher. The movement has been in a contraction phase and a break above 59 on the upside looks more likely just now. Else an initial test of 56-55 is possible before a bounce is seen. Brent looks bullish in the near to medium term and has enough scope on the upside towards 65-66 levels.

Copper (3.1205) has moved up to test immediate resistance just above current levels. While that holds, price could come off towards 3.05-3.00 levels in the near term.

FOREX

Dollar-Index (93.887) rose to a high of 94.02 (resistance on 3 day candles & daily line chart) on Friday as news of the US corporate tax bill moving closer to ratification started to come in. This is an important resistance which should hold in the near term; however a breach of the same could take the index towards resistance on daily candles around 94.4-94.5, followed by a corrective dip thereafter.

Euro (1.176) has come down further after the ECB meet and the US tax cut developments and is currently testing support around 1.175 on 3 day and weekly candles). This is seen as a strong support (in correspondence with support for Dollar Index at 94). A break of this support could take Euro to 1.17 (support on daily candles), from where a bounce should be seen.

Dollar-Yen (112.64) has also moved up on back of perceived dollar strength. If the dollar index retains its strength (around 94) for another week, we could see Dollar Yen move in the range of 112.5-113.5. In case of a test of 94.5 by the Dollar Index, Dollar-Yen could test 114 (acting as resistance on 3 day and weekly candles); post which there should be a corrective dip.

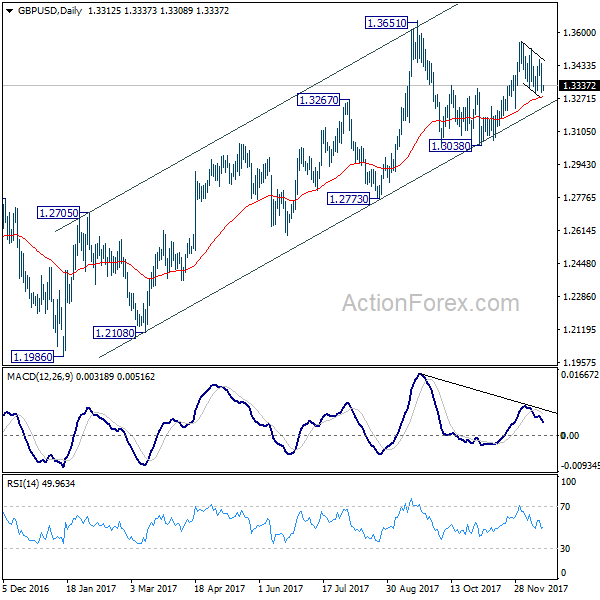

Pound (1.3333) also fell on Friday and is currently trading around 1.33 levels, which could imply a possible test of support near 1.326-1.328 on the daily candles and then a rise back towards resistance near 1.341-1.342. We might be seeing the formation of an ascending triangle on the daily candles for the Pound, which could imply few more rounds of rangewise oscillation between 1.325-1.35, followed by a break on the upside next month.

Rupee (64.045) seems to be oversold at this point and with a resurgence in Dollar strength over the weekend, might move up today to test immediate resistance around 64.13 or even go up to the next resistance level at 64.20-22.

INTEREST RATES

The US yields have moved down sharply and while the 30YR (2.70%) and the 10YR (2.37%) are testing supports at current levels, the 5YR (2.17%) seems to have moved up and may target higher levels of 2.20% in the near term. While the support holds on the 10Yr and the 30Yr, yields may move up in the coming sessions.

The UK-US 10Yr (-1.22%) and could be headed towards -1.33%. This could pull down Pound in the coming sessions.

The German-US 10YR (-2.06%) is down from channel resistance and could be headed towards -2.10% again in the near term.

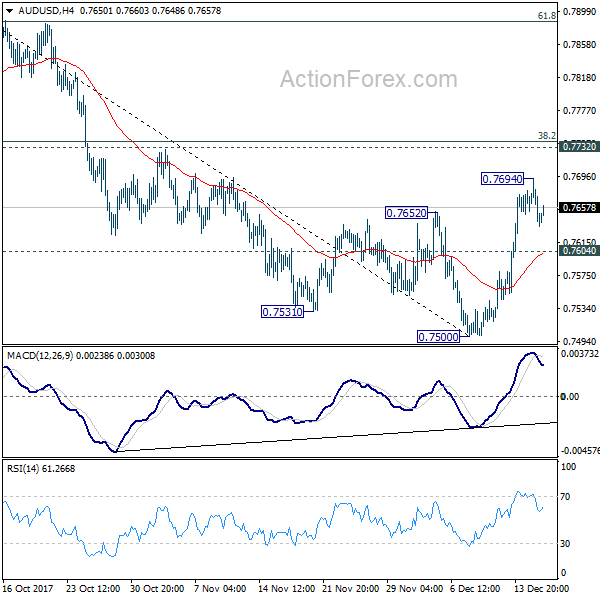

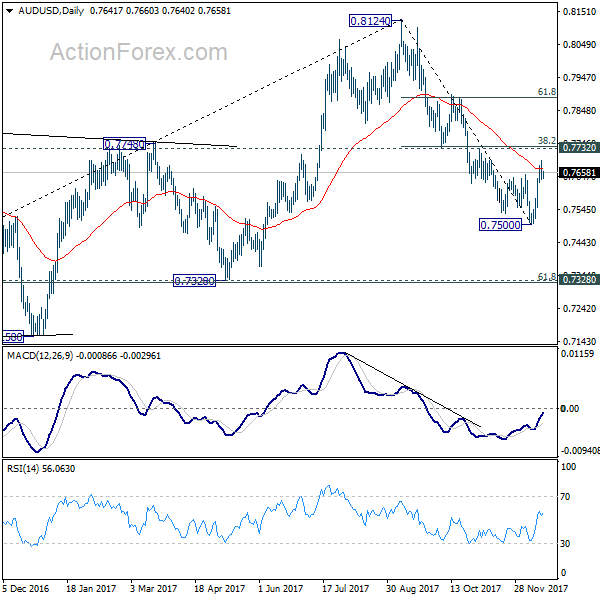

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7619; (P) 0.7657; (R1) 0.7676; More...

With a temporary top formed at 0.7694, intraday bias in AUD/USD is turned neutral first. Price actions from 0.7500 are viewed as a corrective pattern. Upside should be limited by 0.7732 cluster resistance (38.2% retracement of 0.8124 to 0.7500 at 0.7738). On the downside, below 0.7604 minor support will bring rest of 0.7500. Break will resume whole fall from 0.8124. However, sustained break of 0.7732 should invalidate our bearish view and bring stronger rise through 61.8% retracement at 0.7886.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8034). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7732 near term resistance holds.

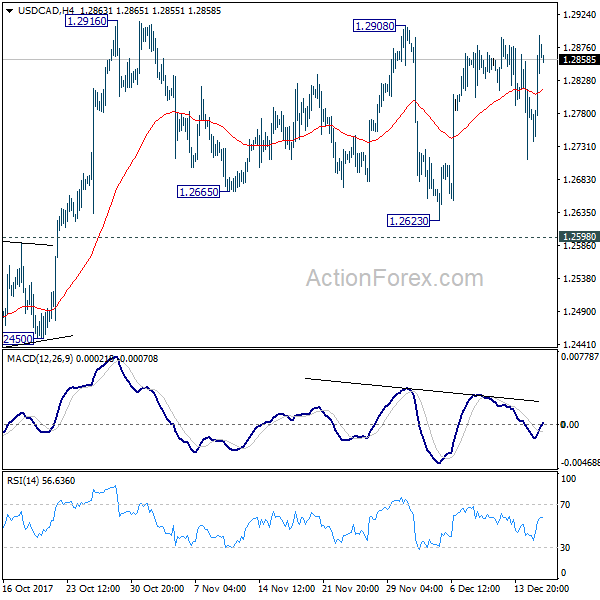

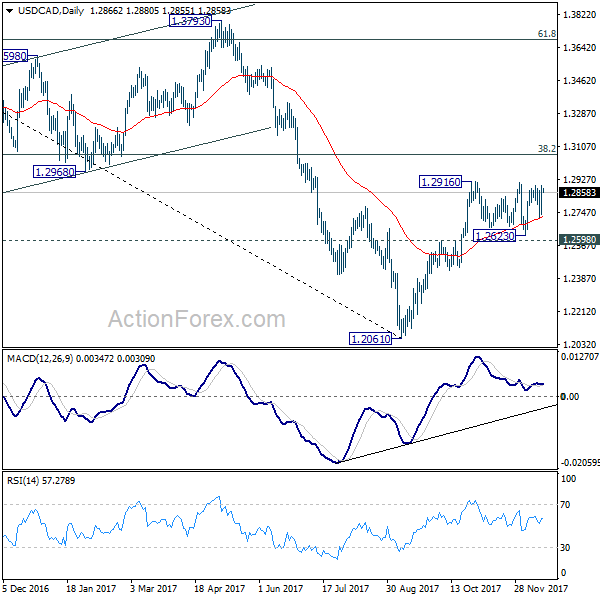

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2774; (P) 1.2834; (R1) 1.2929; More....

Intraday bias in USD/CAD remains neutral as sideway consolidation from 1.2916 might extend further. But after all, with 1.2598 resistance turned support intact, outlook remains bullish and further rally is expected. On the upside, break of 1.2916 will resume the rise from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2885). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Markets Quiet in Listless Session, Dollar Gets No Boost from Tax Bill

Markets are rather quiet as they start the pre-holiday week. Dollar attempts to rally on news of the tax bill, but there is little momentum seen. Yen trade broadly softer despite positive trade data. Weakness in Swiss Franc and Yen suggest that markets are in mild risk seeking mode. Aussie and Kiwi are generally firmer, followed by Euro. But overall, the forex markets are generally staying in Friday's range, without a clear direction.

House and Senate to vote on final tax bill this week

The Republicans have finally finalized the reconciliation of the tax plans last Friday. A summary could be found in the Tax Cuts and Jobs Act policy highlights. The most significant development was that Sens. Marco Rubio of Florida and Bob Corker of Tennessee both changed their minds and expressed the support for the bill. Even though John McCain could miss the vote due to health reason, its now looks like there will be enough vote in the Senate for passing the bill. Treasury Secretary Steven Mnuchin said on Sunday that he has "no doubt" that the bill will be passed this week. And President Donald Trump is expected to sign it next week.

Japan trade surplus widened

Japan adjusted trade surplus widened to JPY 364b in November, above expectation of JPY 270b. Exports rose 14.7% yoy while import rose 17.2% yoy. Increase in exports were broad based. Exports to China rose 25% yoy, to US rose 13% yoy, to EU also rose 13% yoy. The data adds to the case that the export-led Japanese economy is on track for gradual recovery.

Looking ahead

BoJ meeting will be a major focus of the week. With core CPI standing at 0.8%, there is little room for BoJ to talk about exiting stimulus. The central bank will maintain policies unchanged and pledge to drive inflation back to 2% target. RBA minutes for December meeting will likely reveal policymakers' concern over subdued wage growth. While trading would likely be subdued in pre-holiday week, some data might trigger volatility in the markets. German Ifo, New Zealand trade balance and GDP, Canada CPI, retail sales and GDP, US durable goods and PCE will be watched.

Here are some highlights for the week ahead

- Monday: Eurozone CPI final, UK CBI trends total orders; Canada foreign securities transactions; US NAHB housing index

- Tuesday: RBA minutes; German Ifo business climate: US housing starts and building permits, current account

- Wednesday: New Zealand trade balance; Japan all industry index; German PPI; Eurozone current account; UK CBI realized sales; Canada wholesale sales; US existing home sales

- Thursday: New Zealand GDP; BoJ rate decision; Swiss trade balance; UK public sector net borrowing; Canada CPI, retail sales; US Q3 GDP final, jobless claims, Philly Fed survey, house price index, leading indicator

- Friday: German Gfk consumer sentiment; Swiss KOF economic barometer; UK current account, Q3 GDP final; Canada GDP; US durable goods orders, personal income and spending, new home sales

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2774; (P) 1.2834; (R1) 1.2929; More....

Intraday bias in USD/CAD remains neutral as sideway consolidation from 1.2916 might extend further. But after all, with 1.2598 resistance turned support intact, outlook remains bullish and further rally is expected. On the upside, break of 1.2916 will resume the rise from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2885). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance Nov | 0.36T | 0.27T | 0.32T | 0.35T |

| 10:00 | EUR | Eurozone CPI M/M Nov | 0.10% | 0.10% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | 1.50% | 1.50% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov F | 0.90% | 0.90% | ||

| 11:00 | GBP | CBI Trends Total Orders Dec | 15 | 17 | ||

| 13:30 | CAD | International Securities Transactions (CAD) Oct | 16.81B | |||

| 15:00 | USD | NAHB Housing Market Index Dec | 70 | 70 |

EURUSD – Vulnerable, Sets Up To Weaken Further

EURUSD - The pair closed lower after reversing its earlier gains for the week. On the upside, resistance comes in at 1.1800 level with a cut through here opening the door for more upside towards the 1.1850 level. Further up, resistance lies at the 1.1900 level where a break will expose the 1.1950 level. Conversely, support lies at the 1.1700 level where a violation will aim at the 1.1650 level. A break of here will aim at the 1.1600 level. Below here will open the door for more weakness towards the 1.1550. All in all, EURUSD faces further downside weakness

GOLD – Vulnerable, Faces Pullback Risk

GOLD - The commodity caked off higher prices to close on a rejection candle on Friday. On the downside, support comes in at the 1,250.00 level where a break will turn attention to the 1,240.00 level. Further down, a cut through here will open the door for a move lower towards the 1,230.00 level. Below here if seen could trigger further downside pressure towards the 1,220.00 level. Conversely, resistance resides at the 1,260.00 level where a break will aim at the 1,270.00 level. A turn above there will expose the 1,280.00 level. Further out, resistance stands at the 1,290.00 level. All in all, GOLD looks to weaken further on correction.

Easing Into The Holiday Season, Not So Quick !

Easing into the holiday season, not so quick

USD regained some steam heading into the weekend as did US equity markets as Tax reform finality is in sight.

G10 dealers are expected to ease into Christmas and New Year break. So expect low liquidity, and year-end flows will begin to factor into the equation. So far there are few exacting signals, but typically passive portfolios sell the surplus dollars and buy other currencies and bring the overall fund back into balance. However, this year the funding scarcity is moving in the US direction as people seek dollars to cover them through the end of the year. Tighter USD funding conditions early Dec could imply 1) Short dollar position funding will be very scarce over the New Year turn or 2) because US funding is expensive, demand for treasuries and other US assets will be low the final two weeks.

But it’s no time to tap the breaks as the political calendar remains fraught with danger. As we near the finish line on US tax reform market jitters could accelerate and legislators in UK and EU continue to bluster about Brexit.

Bitcoin

After Bitcoin minor league debut on the CBOE, Cryptos are heading for the big leagues with today’s opener on the CME. Given the contract size difference 5 Bitcoin CME vs 1 Bitcoin CBOE, it will likely be a better gauge of institutional or pro trader buy-in. While firms like TD Ameritrade have announced they will agency client orders to the CME, the lack of buy-in from the traditional and significant market makers has many banks and brokers still sidelined.

Oil prices

Amongst all the confusing narratives and shifting signals, oil prices are getting a bounce this morning as the Nigerian oil union talks have hit an impasse and will begin strike action on Monday wich has triggered some weaker shorts to cover at today’s Futures open

G-10 FX

The Japanese Yen

Some early volatility on JPY this morning as the market digests headlines surrounding Abe cabinet approval rating and report that Japan prosecutors to inspect four companies on Maglev.Dollar-Yen fell from 112.74 to 112.50 bid If non-consequential headlines can trigger a gap this morning, think of what the impact could be on significant data releases which could trigger outsized moves in thin, year-end markets

But with the Feds leaning dovish and the USD continuing to wobble despite stronger data, it indeed suggests the path of least resistance remains lower even more so with Japans economy ending the year on a dominant note.

The US Dollar

The Fed dovish narrative is inescapable, despite a probable economic bump from Tax Reform, it’s viewed insignificant enough not to alter their Dot Plots. Given that most market pro’s trade the fundamentals this Fed view alone should erode any dollar positively heading into year-end.

I hate bringing out my crystal ball so soon but with the messy situation in Washington and the Presidents approval rating waning by the month, its difficult to envision the Republicans holding on the house or the Senate majority making it virtually impossible to get any Trump proposal passed. Without the infrastructure boost, the US dollar could be a dead duck in 2018.

Asia Fx

The Chinese Yuan

The RMB complex continues to be a sea of calm in the wake of domestic market upheaval due to reforms and deleveraging.Indeed, the dovish fed narrative weighs positively for the Yuan as we predictably moved towards the critical 6.60 level last week. Given the tepid inflation narrative in the US, the Fed dots remain very sticky and portends well for .the Yuan. The PBOC’s move Thursday to boost market interest rates demonstrates the Pboc’s boldness to continue with a deleveraging crusade which has sent domestic bond yields higher. By Pboc intention or not higher bond yields are probably attracting investor interest, even more so with the likely hood China bonds will be included on the Global Bond indexes.

The Malaysian Ringgit

The turnaround kid of the ASEAN currency block continues to perform well in the face of stable oil prices, healthy economic outlook and a more hawkish tilt from the BNM. Also, inflows into emerging markets should increase given the dovish Fed narrative and a strengthening current account surplus.Although momentum is waning as we enter year end, 2018 looks on the ups for the Ringgit with dealers now targeting 3.90 USDMYR level

This week’s key inflexion points

WTI

The Forties pipeline crack underpinned oil prices last week as Brent widened t to +7 USD premium per barrel over WTI. Mixed signals from the OIL patch giants are confusing the landscape. OPEC suggested production cuts will erode surplus while the IEA in Paris highlights a possible 2018 surplus. All this tells me the US inventory data will continue to provide the most action( Wednesday 10:30 AM EST) Besides Oil inventories the markets are digesting the surprising build in Gasoline stockpiles which has some suggesting a turning point for Crude oil futures ( lower) is on the cards.

USD

The upcoming PCE(Dec 22) release is the primary dollar event this week, but markets will be very tentative to add risk ahead of the Xmas and New Year break. Based on the weak CPI reading, PCE is expected to be another miss fire. But as discussed last week USD negative bets are relatively entrenched following the Fed dovish hike, Doug Jones victory and tepid CPI. The weaker inflation prints, however, will continue to cap dollar rallies. As for the big dollar trade this week this week, I suspect most of the US dollar bears are keeping powder dry to fade the dollar bump after the tax vote goes through

JPY

The BoJ will hold the last policy meeting on Dec 20-21, where the Bank is broadly expected to leave its policy unchanged. There will be no outlook forthcoming from this meeting which centres the risk on Gov Kuroda presser. In the wake of his Zurich meeting and YCC back on the airwaves, the press will likely hound him from additional policy clarity. All things being equal, this suggests a degree of downside risk for USDJPY post press conference

EUR

Eurozone final CPI for November ( December 18), German Ifo for December ( December 19), Catalonia regional election ( December 20). However, given the dovish tone of Draghi at last weeks, ECB presser and holiday thinned liquidity conditions we could see limited price action regardless. EUR has been a dead money the past few weeks, and that’s very unlikely to change

GBP

Brexit headline risk But we’re getting into the meat of the mater as on Tuesday traders will get there first look at how Cable will trade in this crucial phase of Brexit negotiation. Sterling may be vulnerable as U.K. Prime Minister Theresa May meets with her cabinet which could be a messy affair especially if the Brexit hardliners try to impose their views.

NZD

New Zealand trade balance,(Dec 20) and GDT this week’s risks. Given that political uncertainty continues to unwind more so after Adrian Orr was appointed the new Reserve Bank governor last week, the Kiwi should react more favourably from stronger domestic economic data.and firmer dairy prices.

XAU

Year-end premiums for physical delivery are kicking in as most gold refineries shut for holiday season, but the market looks stuck in the middle of no man’s land.It will trade inverse to USD in the absence of any critical drivers. Over the weekend Bloomberg markets are reporting that hedge funds are pulling out of gold bets in favour of equities and speculators are dumping gold at the fastest pace in 5 months.