Sample Category Title

EUR/CHF Weekly Outlook

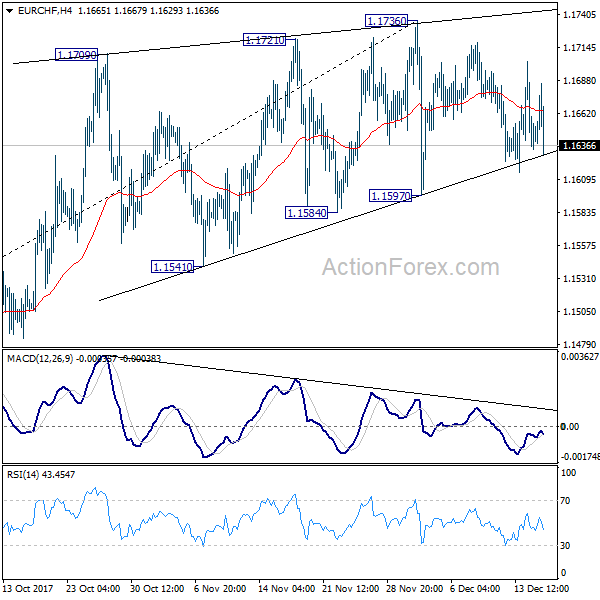

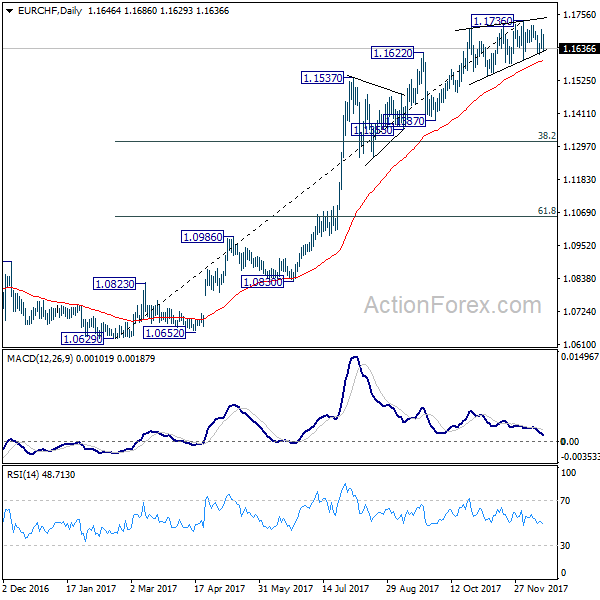

EUR/CHF engaged in range trading below 1.1736 last week and outlook is unchanged Initial bias stays neutral this week first. Again, we believe that the cross is close to topping, if not formed. This is under persistent bearish divergence condition in 4 hour MACD, and rising wedge like structure since 1.1709. On the downside, decisive break of 1.1597 support will a strong sign of trend reversal and should turn outlook bearish for 38.2% retracement of 1.0629 to 1.1736 at 1.1313.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

Dollar Could Be Ready for Rally as Tax Bill Obstacles Cleared

After some roller-coaster rides during the week, Dollar staged a broad based come back before the weekly close. The Republicans' tax plan is now back on track for being signed off by US President Donald Trump, by the end of the year, probably even before Christmas. There were various factors sank the greenback. Tamer than expected core CPI reading was one. An additional dissenter in Fed's rate hike was another. But looking back, the uncertainty on whether Senate could get the bill passed was probably the biggest weight on Dollar. It's still early to tell but focus will now be on whether Dollar could stage a sustainable turnaround before year end.

Staying in the currency markets, Sterling ended as the weakest one as traders cashed in on news that EU formally approved of the sufficient progress on Brexit negotiations. UK and EU team will enter into trade talks next year. BoE kept bank rate unchanged at 0.50% as widely expected, and revealed nothing new in its communications. (more in BOE Stands on Sideline after November Hike, Attributing Inflation Overshoot to Weak Currency). Euro was the second weakest one. ECB left monetary policies unchanged as widely expected too. GDP forecast for 2018, 2019 were raised. Headline inflation forecast for 2018 was also raised. But core inflation forecast for 2018 was revised lower. Also, ECB is not expecting inflation to hit target even in 2020. (More in ECB Upbeat On Economic Outlook, While Maintaining 'Dovish Tapering' Tone).

On the other hand, New Zealand and Australian Dollars were the star performers. Kiwi was boosted by the appointment of a former RBNZ Deputy Governor and chief economist Adrian Orr as next RBNZ governor. Orr will oversee the reform at RBNZ and it's generally believed he will take a practical and realistic approach. Australian Dollar was boosted by stunning employment data.

Tax bill en route to Trump's desk by year end

The Republicans have finally finalized the reconciliation of the tax plans. The final legislation was released late Friday, with the agreement. There are over 1000 pages in these two documents. Here is a summary of the Tax Cuts and Jobs Act policy highlights. The most significant development on Friday was there Sens. Marco Rubio of Florida and Bob Corker of Tennessee both changed their minds and expressed the support for the bill. Both House and Senate are now expected to vote on the bill by mid-week. And as House Majority Leader Kevin McCarthy of California said, the bill will be delivered to Trump's desk "just in time for Christmas".

FOMC announcement was not dovish at all

With corporate tax cut to 21% next year, it's getting more likely that Fed will raise interest rate three times in 2018 as policymakers projected. The FOMC announcement during the week wasn't a dovish one. Fed lifted federal funds rate by 25bps to 1.25-1.50% as widely expected. GDP growth was revised higher to 2.5% in 2017, 2.5% in 2018 and 2.1% in 2019, from 2.4%, 2.1% and 2% respectively. Unemployment rate was revised lower to 4.1% in 2017, 3.9% in 2018 and 2019, and 4% in 2020, from 4.3%, 4.1% and 4.2%, respectively. PCE inflation projection stayed unchanged all over the Fed's forecast horizon, at 1.9%, 2%, 2% and 2% in 2018, 2019, 2020. The only dovish part was that Chicago Fed President Charles Evans joined Minneapolis Fed President Neel Kashkari in dissenting the hike. But Evans is a known doves and he has already hinted in his recent comments that he'd vote "no". So that shouldn't be a surprise to anyone who followed closely.

Dollar index to take on 94.16 again

Dollar index once looked rejected by 94.16 resistance last week. But subsequent pull back was relatively shallow, contained at 93.28. Friday's rebound now put 94.16 back into focus for this week. Decisive break there will confirm that fall from 95.15 has completed at 92.49. And in that case, a retest of 95.15 should be seen next. In that case, there would be prospect of hitting 38.2% retracement of 103.82 to 91.01 at 95.90 around the turn of the year. But again, break of 92.49 will put 91.01 low back into focus.

Technically in the currency markets, the break of 94.16 in dollar index has to be accompanied by firm break of 1.1712 key support in EUR/USD. In addition, we'd also prefer to see firm break of 113.74 in USD/JPY, 0.9977 in USD/CHF and 1.2916 in USD/CAD to confirm Dollar's strength. Otherwise, we'll stay skeptical.

Trading strategy

Our order to buy USD/CAD on break of 1.2916 was not filled. USD/CAD dipped sharply after comments from BoC Governor Stephen Poloz raised the chance of a Q1 rate hike. But the pull back was contained by 55 day EMA as the pair quickly rebounded. We'd maintain our technical view on USD/CAD. Firstly, rebound from 1.2061 is still in progress. Consolidation from 1.2916 is about to finish. Secondly, the long term correction from 1.4689 (2016 high) should have completed at 1.2061. Rise from there should extend to 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and possibly above. Hence, we'll try to buy USD/CAD on break of 1.2916 again this week.

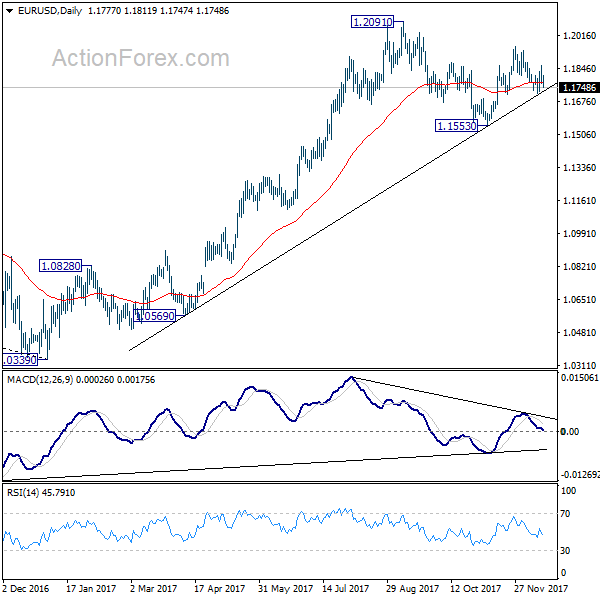

EUR/USD Weekly Outlook

EUR/USD rebounded to as high as 1.1862 last week but reversed from there. Initial bias is neutral this week first with focus on 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708) again. Decisive break there should confirm completion of rebound from 1.1553 to 1.1960. This would also be supported by a head and shoulder pattern (ls: 1.1860; h: 1.1960; rs: 1.1862). And in that case, deeper fall should be seen through 1.1553 to extend the medium term decline from 1.2091. Meanwhile, above 1.1862 will revive near term bullishness and target 1.1960 and above.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1435) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

In the long term picture, 1.0339 is seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action form 1.0339 is developing into a corrective or impulsive pattern. On the upside, strong resistance could be seen from 38.2% retracement of 1.6039 to 1.0339 at 1.2516. On the downside, we're not anticipating a break of 1.0339 in medium term.

Eco Data 12/22/17

[php_everywhere] [/php_everywhere]

Eco Data 12/21/17

[php_everywhere] [/php_everywhere]

Eco Data 12/20/17

[php_everywhere] [/php_everywhere]

Eco Data 12/19/17

[php_everywhere] [/php_everywhere]

Eco Data 12/18/17

[php_everywhere] [/php_everywhere]

Summary 12/18 – 12/22

Monday, Dec 18, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Dec 19, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Dec 20, 2017

[php_everywhere] [/php_everywhere]

Thursday, Dec 21, 2017

[php_everywhere] [/php_everywhere]

Friday, Dec 22, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Retail Sales Sing Into the Holidays

U.S. Review

Retail Sales Sing Into the Holidays

- As was widely expected, the Federal Open Market Committee (FOMC) hiked rates this week. The top range of the fed funds rate now stands at 1.50 percent.

- Inflation measures started to show signs of emerging price pressures for producers and consumers.

- Retail sales for November showed that the holiday shopping season was off to a strong start. Overall sales rose 0.8 percent for the month.

- Industrial output rose 0.2 percent in November with manufacturing output also climbing 0.2 percent.

Retail Sales Sing Into the Holidays

Economic data this week continued to signal moderate economic growth and inflation started to show signs of picking up. Following November's performance, consumer prices are now up 2.2 percent on a year-over-year basis, while producer prices are now up 3.1 percent. The more recent inflation data combined with the rate hike out of the FOMC this week showed that monetary policy normalization remains on track. With the release of our Annual Economic Outlook, we added a third rate hike into our forecast for 2018 while we kept two fed funds rate hikes in 2019. Retail sales data showed a surge in consumer spending in November to start the holiday shopping season. Industrial output also continued to rise for the month with manufacturing output posting its third consecutive month of improvement.

The FOMC hiked interest rates for the last time with Janet Yellen leading the FOMC. The committee continued to signal that evidence of inflation turning around combined with improvement in labor market conditions reinforced its view for continued normalization of monetary policy through further rate hikes and balance-sheet normalization in the year ahead.

Inflation data this week reinforced the idea that the downshift in inflation is likely behind us. The headline Consumer Price Index rose 0.4 percent in November, while core inflation climbed 0.1 percent. Energy prices helped boost the headline CPI reading while softer lodging, airfare and apparel prices held back the gains in the core CPI. Looking at producer prices, the PPI for final demand rose 0.4 percent, while the core PPI measure climbed 0.3 percent. Import prices also accelerated for the month, climbing 0.7 percent following October's 0.2 percent increase. Even with a slightly softer core CPI reading we still see the FOMC on track to hike rates three times in 2018 as other measures of inflation continued to edge higher.

Retail sales data were one of the biggest economic data surprises of the week, climbing an impressive 0.8 percent in November. The strong start to the holiday shopping season was partially due to greater spending in electronic stores and non-store retailers, which captures online retailers. Gasoline station sales also rose 2.8 percent on the month with at least some of those gains reflecting higher prices in the nominally reported number. The retail sales control group, which feeds into the calculation of GDP, was revised higher for October and climbed an additional 0.8 percent in November. Our forecast for Q4 real consumer spending stands at 3.0 percent. If our forecasted real PCE growth materializes in Q4, consumer spending should end 2017 at 2.7 percent year over year, matching last year's growth rate.

Industrial output climbed 0.2 percent in November with manufacturing output also climbing 0.2 percent for the month. We estimate that there will be continued growth in industrial production in 2018 with a rise of 2.7 percent on a year-over-year basis compared to this year's expected 1.9 percent growth rate.

U.S. Outlook

Housing Starts • Tuesday

The rebound in housing starts in October was solid following the hurricane-induced construction stumble in September. Starts rose 13.7 percent to a 1.29 million-unit pace in October which is among the strongest months of the current cycle. This marks a strong start for residential investment in Q4 GDP, which is slated to be positive after being a drag the past two quarters.

The ramp up in construction was broad-based as only the West saw building slow, and single-family and multifamily posted solid gains. That the pace of building came back so much stronger in October than before the storms hit is an encouraging sign. The increase in permits issued combined with continued strength in builder confidence also bodes well for residential investment in coming months. Still, we are calling for the pace of starts to slow down a bit in November after October's outsized ramp up.

Previous: 1.290M Wells Fargo: 1.237M Consensus: 1.250M

Existing Home Sales • Wednesday

Existing home sales showed a strong rebound in closings in October as weather disruptions disappeared. Contract closings rose 2 percent to a 5.48 million unit pace. October's existing sales report suggested a good start for a Q4 rebound in residential investment in GDP. November's resales pace likely also accelerated. We expect residential investment to be a positive contributor to Q4 economic growth after two quarters of decline.

Inventory of homes for sale continued to decline in October, which is restraining sales and pushing up selling prices. Looking through the temporary weather disruptions, the greater issue in the existing home sales market is the general lack of available inventory. This is likely to keep a significant pickup in sales activity in 2018 more difficult, although we still expect next year to be stronger than 2017.

Previous: 5.48M Wells Fargo: 5.61M Consensus: 5.53M

Personal Income • Friday

Personal income was up a solid 0.4 percent in October, while spending rose 0.3 percent. Real disposable income growth has perked up recently, which is a refreshing development following a relatively long spell of softness. Stronger income growth also came in just in time for holiday shopping, which was already slated to be strong as consumer confidence is at a multiyear high. Personal spending softened in October from a large hurricane-induced bump in September.

Inflation took a bite out of consumers' purchasing power, as real spending rose 0.1 percent. Higher prices persisted in November, which is welcome news to the FOMC, even though it was mostly driven by energy costs. Even adjusted for inflation, we still expect that personal spending is slated for a solid increase based on the consumer confidence in recent months, October's welcome income bump, and the strong showing for retail sales in November.

Previous: 0.4 % Wells Fargo: 0.4% Consensus: 0.4 % (Month-over-Month)

Global Review

Global Central Bank Meetings

- It was a big week for central banks as the Federal Reserve, the Bank of England and the European Central Bank all met.

- After a period in which the Fed was somewhat by itself in terms of raising rates, there is now a widening front along which other major central banks are either also raising rates or, in the case of the ECB, at least guiding monetary policy in a somewhat less expansionary direction.

Eminence Front: It's No Put-On

The Federal Reserve was not the only major global central bank gathering this week. The European Central Bank (ECB) and the Bank of England (BoE) conducted policy meetings as well. The word 'eminence' can be used to describe a recognized superiority within a sphere or profession as well as a piece of rising ground. This week it can be accurately used in both senses to describe central bank activity. Some of the world's most influential central banks met this week and, to varying degrees, nudged the global economy toward higher ground in terms of interest rates or at least less-accommodative monetary policy.

Bank of England

The meeting of the BoE followed news earlier in the week that CPI inflation came in a bit hotter than expected with a 0.3 percent pickup in November that lifted the year-over-year rate of CPI inflation above the top end of the BoE's 1 to 3 percent target range. The breach obliges BoE Governor Carney to draft a note explain the reasons behind this event to the Chancellor of the Exchequer.

Even amid this firming inflation, the growth outlook is less than certain. The year-over-year rate has been trending steadily, if only slightly, lower over the past two years. Worries about the eventual effects of Brexit have been cause for caution as well; our own forecast looks for full-year GDP growth of just 1.7 percent in 2018. The challenge for the BoE is to rein-in inflation without squeezing economic growth at a time when the outlook is uncertain.

The BoE decided at its prior policy meeting on November 2 to raise its main policy rate 25 bps, but based on language this week, the BoE's Monetary Policy Committee (MPC) does not seem to be in a hurry to tighten further, stating that any future rate hikes "would be expected to be at a gradual pace and to a limited extent." Furthermore, the statement highlighted the downside risks to the economic outlook posed by the uncertainty of the Brexit process.

European Central Bank

As for the ECB, if raising rates is the anticipated "main event," then the "opening act" is a dialing back of its program of asset purchases. The ECB had already offered forward guidance on that front. Specifically, the ECB will purchase only €30 billion worth of bonds beginning in January 2018, and it intends to keep this monthly purchase rate unchanged through at least next September.

At its meeting this week, the ECB essentially offered no change in this guidance despite indications of firming in the Eurozone economy like the PMIs, which have climbed to multi-year highs for the services and manufacturing sectors.

If the overall rate of inflation in the Eurozone trends slowly higher in the months ahead as our analysis suggests, then we think the conditions will be in place for the ECB to end its bond purchases in late 2018.

Global Outlook

Russian Real Retail Sales • Monday

Data for Russian real retail sales, real wages and industrial output all print next week. Real retail sales have climbed higher this year as the Russian economy has recovered from a deep recession that occurred over the 2015-2016 period. At its peak in early 2015, consumer price inflation in Russia was up nearly 17 percent year over year, eroding consumer purchasing power and leading to a jump in interest rates. Inflation has since receded to 2.7 percent versus a year ago.

The Russian economy has clearly improved from its recent trough, and next week's data will likely show some continued modest progress. That said, the headwinds on the Russian economy are multi-faceted and difficult to address quickly; oil prices remain relatively low, international sanctions are in place and an aging population presents demographic challenges. As a result, although we expect some continued near-term improvement, a return to the run-rate of the early years of the past decade does not look likely.

Previous: 3.0% Consensus: 3.3% (Year-over-Year)

Bank of Japan Meeting • Thursday

Unlike many of the developed world's central banks, the Bank of Japan (BoJ) has shown few signs of taking its foot off of the accelerator. This continued stimulus comes at a time when the Japanese economy is doing reasonably well. We expect the Japanese economy will end up growing 1.5 percent for full-year 2017. If realized, that would mark the fastest rate of GDP growth since 2013.

We do not currently envision the BoJ tightening policy in a meaningful way at any point through the end of our current forecast horizon (2019). Unlike many of the world's other major developed economies, Japan has faced more severe deflationary episodes in its recent history in addition to struggling with severe structural challenges related to demography and other factors. Thus, we believe monetary policymakers in Japan are likely to wait until deflation and razor thin margins between expansion and contraction are banished before reversing course.

Previous: -0.1% (Policy Balance Rate) Wells Fargo: -0.1%

Canadian CPI • Thursday

The Canadian economy has had a strong run in 2017 as fixed investment spending rebounded after a swoon alongside oil prices. The Canadian consumer has also proved resilient despite high household debt levels. Year-over-year economic growth picked up to a 3.0 percent pace through Q3. Against this backdrop, the Bank of Canada hiked rates 25 bps twice in 2017.

The Bank of Canada targets core inflation between 1 and 3 percent. At present, core inflation is toward the lower end of this band (see chart at right). The tame inflation, coupled with high household debt levels, have led the Bank of Canada to temper monetary policy tightening expectations relative to what the growth numbers alone might suggest. We expect two more rate hikes from the BoC next year, although we believe there is some upside to this forecast. Inflation moving closer to the midpoint of the BoC's target band would be a big factor in turning this upside risk into reality.

Previous: 1.6% (Core-Common YoY) Wells Fargo: 2.0%

Point of View

Interest Rate Watch

Inflation, Models and Belief

In recent years the upswing for inflation has been consistently below the pace anticipated by the Phillips curve model approach. Policymakers believe in this model and therefore project, represented by their dot-plot, an upswing in the benchmark fed funds rate in the year ahead. For us, we expect the FOMC to raise the fed funds rate three times in 2018 but that the pace of increases in the short-end of the Treasury curve will outpace that of the long-end, thereby prompting discussions about an inverted yield curve and its implications for a recession.

Just the Facts: Inflation

Our expectation for the path of the PCE inflation benchmark is an upward trajectory (top graph). We expect an unwinding of what we believe were largely one-off disinflationary forces in 2017 (caused by declines in wireless phone services and physician services). In addition, higher labor costs and higher energy prices as global oil demand has improved and producers remain fairly disciplined should also generate a lift to inflation. Finally a weaker dollar should generate higher import prices, all else equal.

Introduce a Model

From the FOMC's point of view, a lower unemployment rate will lead to a higher inflation rate over time. The middle figure shows the fairly loose relationship.

Belief

Given the FOMC's inflation model, the dotplot illustrates the path of the fed funds rate going forward (bottom graph). Our outlook is now for three fed funds rate increases in 2018. The market, however, has priced in a little less than two hikes.

Moreover, at the long-end of the Treasury curve we have an increase in rates below the pace at the short-end of the curve. The 10-two year spread declines from 69 bps to 55 bps over the first two quarters of 2018. Our 10-year to three-month yield spread declines from 114 bps to 85 bps. This imbalance in rate changes could potentially lead to an inverted yield curve – whispers surrounding the probability of a recession will likely follow.

Credit Market Insights

Borrowing Remains Healthy

Consumer credit rose $20.5 billion in October, marking the largest monthly gain since November 2016. Up 6.5 percent at a seasonally adjusted annual rate, consumer borrowing in October continues to build off of the 6.1 percent gain seen in September.

Total consumer credit was supported by solid growth in revolving and nonrevolving credit. Revolving credit, up 9.9 percent at an annual rate, led the surge mainly due to increased credit card balances. Revolving credit in October also registered its largest monthly gain ($8.3 billion) since November 2016, which in part could be attributable to increased spending to start the holiday season. Nonrevolving credit, however, jumped $12.2 billion, and was up at an annual rate of 5.3 percent. The rise in nonrevolving credit was likely aided by rebound effects in auto-sales due to damage from the recent hurricanes.

Despite healthy borrowing conditions, charge-off rates at commercial banks remain on a slight upward trend. The rise in charge-off rates is in line with a rising interest rate environment, and this relationship is expected to persist as the Fed continues to tighten policy in 2018. We expect borrowing to remain healthy into the new year, as elevated levels of consumer confidence coupled with modest wage improvements continue to cause consumers to utilize credit to fund their consumption habits.

Topic of the Week

2018 Annual Economic Outlook

A Cautious Tale for an Optimistic Outlook

If we count the months since the economy emerged from recession in July 2009, this January marks the 103rd month of the current expansion. The longest expansion on record is 120 months, which was the expansion of the 1990s. Our forecast of roughly 2.5 percent quarterly GDP growth on an uninterrupted basis for 2018 and 2019 means that we are implicitly stating that this cycle will break the record for the longest expansion in U.S. history (top chart). However, with the average annual real GDP growth rate since mid-2009 at a rather tepid 2.3 percent, the current expansion will also hold the record of the weakest of the post-war era.

The unusually slow pace of this economic recovery has left the economy in pretty good shape, as there are few visible excesses present today. Similarly, for the first time in a long time just about every corner of the global economy is expanding at the same time. We are not bracing for a recession in Europe as we were in 2010- 2012 after the sovereign debt crisis, nor are we expecting knock-on effects of another great moderation in China. Instead, we are seeking slow, steady global growth, warranting no minus signs in our GDP forecasts for any of the foreign economies that we follow (bottom chart).

As global growth begins to firm, central banks are entering a period of monetary policy "convergence," rather than one of divergence. As the Federal Reserve has led the charge, we expect the FOMC to continue to tighten policy with three hikes in the federal funds rate this coming year, based on continued growth in employment and modest improvements in inflation.

Our probit model suggests a relatively low 1.17 percent probability of recession in the next six months, as it is difficult to point to a sector that has over-extended itself so much that recession is right around the corner. However, despite our admittedly sanguine assessment of the current path of the global economy, in our 2018 Annual Economic Outlook we highlight the potential risks that could warrant caution in the future.

The Weekly Bottom Line: Taxmas is Coming and the Debt is Getting Fat

U.S. Highlights

- Economic policymakers in Washington squeezed a lot in this week before heading home for the holidays. As expected, the Fed raised rates a quarter point and upgraded their economic growth forecasts.

- Republican members of Congress rushed to wrap up a compromise tax plan to be voted on early next week. While the final details are not yet known, the plan is likely to provide a modest boost to growth over the next few years. But, it has several potentially negative consequences for government finances over the longer-term.

- Our Quarterly Economic Forecast also features an upgraded economic outlook, in part reflecting better momentum in the second half of the year, and fiscal stimulus.

Canadian Highlights

- November saw healthy gains in housing resale activity as markets continue to come off the lows of the summer. In contrast, October manufacturing data was weak on the back of since-resolved disruptions in the auto sector.

- Bank of Canada Governor Poloz gave a relatively hawkish speech, painting a positive picture in remarks meant to focus on his worries. He followed this with more cautious remarks to CBC, suggesting that markets should put less stock in his words, and more in the economic data.

- To that end, our latest forecast sees continued economic momentum heading into 2018. As this forecast gets realized, the stage will be set for further Bank of Canada tightening, albeit at a gradual pace.

U.S. - Taxmas is Coming and the Debt is Getting Fat

Economic policymakers have been squeezing a lot in before heading home for the holidays. The Fed raised interest rates this week, as Janet Yellen gave her last press conference as Chair. Congressional Republicans were busy wrapping up a compromise tax cut plan. They face a new sense of urgency, since they will face a diminished Senate majority in the New Year once the newly elected Democratic Senator from Alabama takes office. At time of writing, the full details of the tax cut are not yet known, but the House and Senate are expected to vote on it early next week.

Given the high likelihood of a fiscal boost, our latest Quarterly Economic Forecast, released this week, incorporates a modest boost to real GDP over the next few years (Chart 1). It's "Onward and Upward" for the U.S. economy over the next two years, with growth expected to accelerate from 2.3% in 2017 to 2.6% next year.

Even before a tax cut, the U.S. economy appears to be hitting a sweet spot. The unemployment rate is at a 17-year low, businesses are ramping up investment and inflation remains contained.

The consumer continues to be a stalwart of the economy. This was confirmed by a strong retail sales report for November. Consumer spending growth is on tracking for a healthy 2.8% annualized pace in the fourth quarter, which marks a rebound from a hurricane-dampened 2.3% pace in Q3.

The Fed also raised its economic growth forecast, but left its expectation for the number of rate hikes over the next year unchanged. The reason for the seeming inconsistency is unclear, but likely it is in part because of continued weakness in inflation would have necessitated a downgrade in the number of hikes, were it not for the offsetting growth upgrade.

All told, this is not a picture of an economy calling out for a fiscal boost. Moreover, deficit-financed tax cuts have several potentially negative consequences for the federal budget, and the economy as a whole. First, fiscal stimulus in an economy running full tilt is likely to stoke higher wages and inflation, and could result in a slightly faster pace of rate hikes by the Federal Reserve, ultimately dampening the support to growth. Second, since the personal tax cuts are temporary, a future Congress will need to deal with another fiscal cliff down the road. Third, higher deficits over the next few years (Chart 2)also make it more difficult for the government to respond to a potential economic downturn.

Finally, the plan is estimated to add about one trillion dollars to a debt burden that was already slated to grow due to rising expenditures from an aging population. This means interest costs will eat up more of the budget, leaving less room for other priorities. Larger government debt burdens also crowd out investment in the private sector, dampening productivity growth over the longer term. And, it raises the likelihood of a fiscal crisis – where interest rates on federal debt would rise suddenly and sharply as investors demand additional compensation to hold U.S. debt.

Canada - Decoding Poloz

The past week gave us further updates on economic progress heading into the close of 2017. Housing continued to recover, recording a fourth straight monthly increase in resale activity in November, helped by a recovering Ontario market (Chart 1). As discussed in our latest Forecast, changes to underwriting guidelines will impose a new headwind to the sector in 2018, with the fourth quarter likely to be benefitting from some pull-forward of activity ahead of this change. At the same time, manufacturing sales took a step back in October, but this was to be expected as retooling and labour disruptions affected two large auto manufacturing facilities. Importantly, both facilities have since returned to full production, and the forward-looking components of the report remained healthy, suggesting that October should be the last month of setbacks in a sector that has been plagued by disruption in recent months.

Undoubtedly, the key event of the week was a speech by Bank of Canada Governor Stephen Poloz on December 14th. Monetary policy may often be seen as a boring, technical field, but Governor Poloz did his best to make it interesting, and markets took notice, as reflected by moves in the loonie (Chart 2). To begin with, Poloz opened a speech meant to focus on his worries with an upbeat assessment of the economy. Areas of concern were followed with notes that progress is being made towards addressing issues such as high house prices and household debt and what he perceives to be weakness in labour markets. Also notable for a risk-oriented speech, NAFTA negotiations were not mentioned – the only reference to trade was a positive remark on exports.

The somewhat hawkish tone was further reinforced in the Q+A period. When asked about his use of the word 'caution', which markets seemed to read as indicating a hold, he referred to the dictionary definition, and provided the metaphor of driving home in a snow storm. In effect, that caution doesn't mean standing still, it means going slow. The net result was to send the loonie roughly a cent higher against the U.S. dollar as the overall tone of the Governor's remarks suggested rate rises may be coming sooner than markets were anticipating.

It was not to last however. Later in the day, in a pre-taped interview with the CBC, the Governor struck a much more dovish tone, noting that he wants the economy to "run hotter for a while" to absorb remaining labour market slack. When asked about the Federal Reserve's outlook for interest rates (with the overnight rate seen breaching 3% by 2020), Poloz stated that he sees the Canadian economic cycle being about a year or two behind the U.S. This was enough to pare back some of the earlier gains, leaving the loonie up just 0.3 cents on the day.

The key question is thus: what message was Poloz trying to convey? The answer may ultimately be none at all. Recent communication has emphasized data dependency and keeping options open, and with the shifting tone seen on the 14th, Poloz may be telling us not to hang on his every word. This goes back to the core notion of 'data dependency', as exemplified in September's hike. Ultimately, should fourth quarter economic growth come in as expected, another rate hike likely won't be far behind.

U.S.: Upcoming Key Economic Releases

U.S. Personal Income & Spending - November

Release Date: December 21, 2017

Previous Result: Income 0.4% m/m; Spending 0.3% m/m

TD Forecast: Income 0.5% m/m; Spending 0.5% m/m

Consensus: Income 0.4% m/m; Spending 0.4% m/m

Headline PCE inflation is expected to pick up to 1.8% in November, consistent with the rebound in the CPI on higher energy prices. Food prices are expected to be flat for the fourth month, though slightly higher on a y/y basis. Excluding food and energy, core PCE inflation is likely to firm marginally to 1.5% y/y on a relatively weak 0.1% m/m. Details should show several categories acting as a drag, notably apparel (as seen in the CPI report), while there is scope for healthcare services to disappoint its CPI counterpart (in line with continued weakness in PPI healthcare services categories). This still points to a 0.1% m/m rise in the core PCE, matching the increase in the core CPI.

Nominal PCE (personal spending) is expected to rise 0.5% in November, pointing to Q4 real consumer spending near a 2.5% pace. We expect gains to again be driven by nondurables and services, partially offset by a drag from vehicle sales which continued to contract in November. We also expect a firmer 0.5% increase in November personal income.

Canada: Upcoming Key Economic Releases

Canadian CPI - November

Release Date: December 21, 2017

Previous Result: 0.1% m/m

TD Forecast: 0.2% m/m

Consensus: N/A

We expect headline CPI inflation to jump to 1.9% y/y in November from 1.4% y/y, driven by a surge in gasoline prices. The sharp pickup will be short-lived as base effects are adverse over the coming months and gasoline prices are set for a partial reversal in December. This should lead headline inflation back down to 1.7% y/y in December before bottoming out at 1.4% y/y in January. That said, outside of energy, the inflation picture should be fairly constructive in November. After a series of declines, food prices have scope for a rebound helped by a weaker Canadian dollar, which by November returned to its pre-July hike levels. Other past sources of weakness also should show some recovery, such as vehicle prices. Excluding food and energy, prices should post an acceleration to 1.6% y/y, the highest read since March. The rapid absorption in labour market slack, which is now more apparent in wage growth, also points to stable to higher readings in the three new core metrics (CPI common, trimmed mean and median), which would be viewed favourably by the BoC.

Canadian Retail Sales - October

Release Date: December 21, 2017

Previous Result: 0.1% m/m, ex-auto: 0.3% m/m

TD Forecast: 0.6% m/m, ex-auto: 0.8% m/m

Consensus: N/A

TD expects headline retail sales to post a 0.6% advance in October, led by a solid pickup in core sales. Auto sales should remain largely unchanged which will exert a modest drag on the headline print and leave ex-auto sales up 0.8%, while gasoline station sales will face a headwind from lower prices at the pump. Core retail sales should benefit from continued gains in the labour market and the persistence of wealth effects, as demonstrated by the strong increase in Q3 consumer spending. On a volumes basis, retail sales should underperform the nominal print though we still expect a positive contribution to industry-level GDP.

Canadian Real GDP - October

Releases Date: December 22, 2017

Previous Result: 0.2% m/m

TD Forecast: 0.2% m/m

Consensus: N/A

TD looks for a 0.2% advance in industry-level GDP for October, with growth led by the services sector. Goods sector output will be constrained by production woes in the automotive industry, reflecting both retooling shutdowns and labour disputes. Utilities output should also be a source of downside as the late summer heat wave fades, though a surge in residential construction should provide an offset. Services should show a rebound in retail and wholesale trade in addition to a solid contribution from real estate as the Toronto housing market continues to stabilize. Our forecast is consistent with Q4 growth near a 3% pace, which provides further reason for the Bank of Canada to hike in Q1 2018 given their assertion that the economy is operating near full capacity.