Sample Category Title

EUR/AUD Regular Bullish Divergence at D L3 Camarilla Support

The EUR/AUD has formed a regular bullish divergence exactly at D L3 support.. The double top could break to the upside and 1.5370-80 could be a breakout zone which could spike the price up to 1.5410, 1.5440 and 1.5485. The pair has already break below W L5 and while its capped above 1.5340 we could see a retest. For intraday targets 1.5439 and 1.5457 is the zone should the price proceed above the breakout point.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Canada: Manufacturing Sales Take a Step Back in October

Following two months of gains, Canadian manufacturing sales slid 0.4% in October. In real terms, the picture was worse, as sales volumes were down 1.5% during the month.

The bulk of the decline stemmed from the motor vehicle industry (-6.7%), which saw volumes fall 7.6% thanks to assembly plant shutdowns during the month. Several industries provided some offset, including petroleum and coal products (+2.2%), fabricated metal products (+2.6%), computer electronic products (+3.9%) and wood products (+3.4%).

Regionally, sales were down in six provinces. Ontario recorded a 2.2% drop due in large part to the auto industry. On the flipside, sales in Alberta (+4.2%) and B.C. (+2.1%) were up during the month.

The inventory-to-sales ratio increased to 1.40 in October (previously 1.37) thanks to a 1.6% increase in inventories.

Forward looking indicators were encouraging, with unfilled orders up 2.4% and new orders rising 5.3%.

Key Implications

Manufacturing volumes were held back in October by disruptions in the auto sector, which have since been resolved. As such, auto manufacturing should bounce back strongly over the remainder of 2018, helping to lift overall output in the sector.

Outside the auto sector, forward looking indicators point to a better performance in the coming months. Moreover, with economic activity in the U.S. expected to pick up, demand for Canadian-made goods should follow suit, supporting factory production in Canada.

As such, manufacturing should contribute to another strong performance from the Canadian economy in the fourth quarter - which we expect to come in around 3.0% (annualized) - and over the next year. This momentum will not be lost on the Bank of Canada which is in data dependent mode. As such, higher interest rates are on the way, with a hike likely in early-2018.

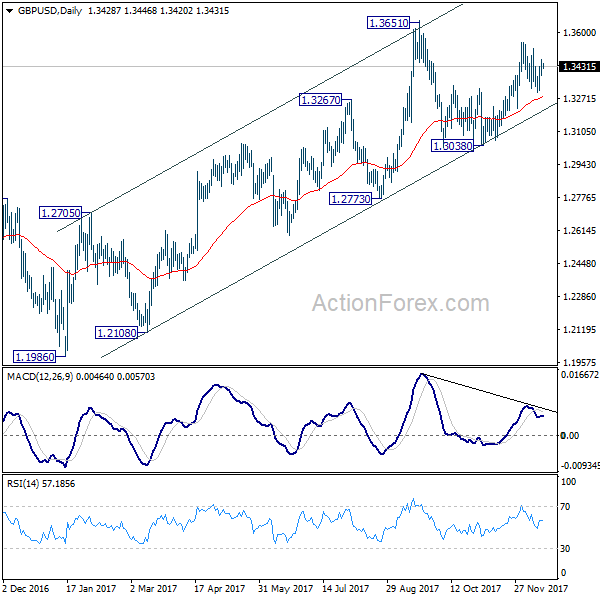

GBPUSD – Near-Term Bias Turns Negative and Favors Attack at Key 1.3302 Support

Cable came under pressure in early hours of European session and broke below pivotal supports at 1.3401 (10 SMA) and 1.3374 (20SMA), weakening near-term structure.

Fresh bearish acceleration at the beginning of American session approached key support at 1.3303 (12 Dec low/30SMA/daily Kijun-sen) and shifted near-term bias lower.

Fresh bears are on track to fully retrace 1.3302/1.3464 recovery phase and signal continuation of bear-leg from 1.3549 (01 Dec high).

Firm break below 1.3302 handle is expected to undermine larger bulls from 1.3038 and generate stronger bearish signal for extension towards 1.3253 (55SMA/daily cloud top) and 1.3233 (Fibo 61.8% of 1.3038/1.3549 ascend). Broken 20/10 SMA's now act as resistances and should keep the upside protected.

The pair is also on track for the second straight bearish weekly close which supports negative scenario.

Res: 1.3374; 1.3415; 1.3447; 1.3464

Sup: 1.3303; 1.3253; 1.3233; 1.3196

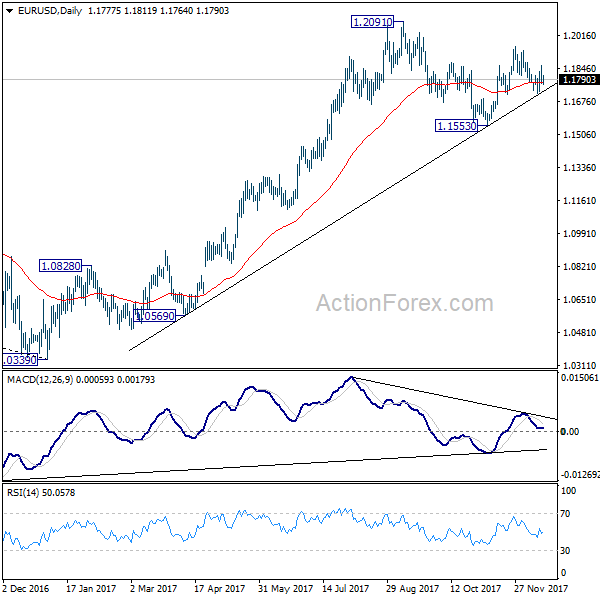

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1743; (P) 1.1803 (R1) 1.1835; More....

Intraday bias in EUR/USD remains neutral at this point. Overall, near term outlook remains bullish with 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708) intact. Further rally is expected and above 1.1862 will target 1.1900 first. Break will target 1.2029 high next. However, decisive break there will indicate that rebound from 1.1553 has completed at 1.1960. In that case, deeper fall would be seen to 1.1553 and possibly below to extend the decline from 1.2091.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

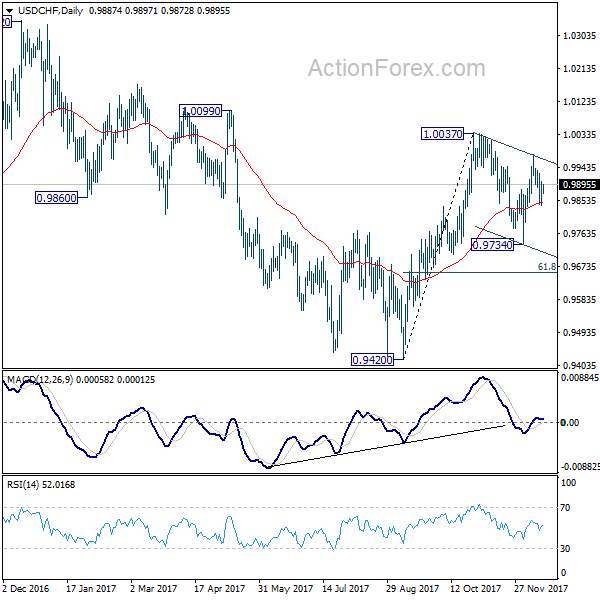

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9850; (P) 0.9877; (R1) 0.9915; More....

Intraday bias in USD/CHF remains neutral for the moment. On the downside, break of 0.9839 will extend the fall from 0.9977. Such decline is seen as part of the correction pattern from 1.0037. It could target 0.9734 support and below. But we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. On the upside, break of 0.9977 will revive near term bullishness and target 1.0037 and above.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

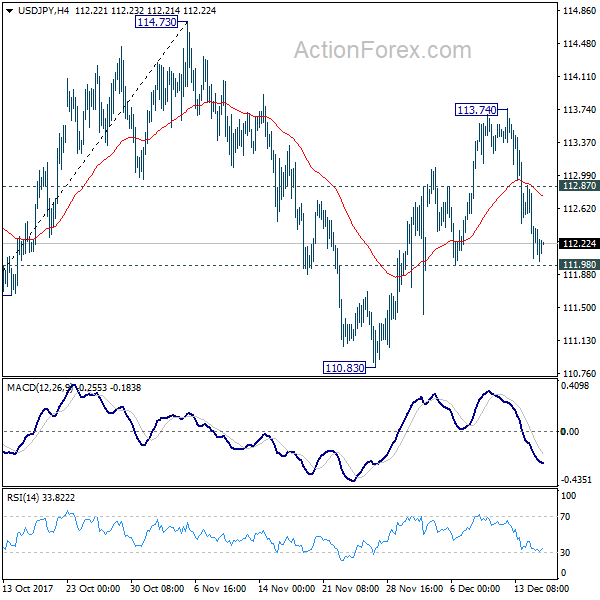

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.01; (P) 112.45; (R1) 112.83; More....

Intraday bias in USD/JPY remains neutral as it's staying above 111.98 support. Another rise is still mildly in favor. Above 112.87 minor resistance will turn bias to the upside for 113.74. Break will target 114.73 key resistance. However, firm break of 111.98 support will extend the decline from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

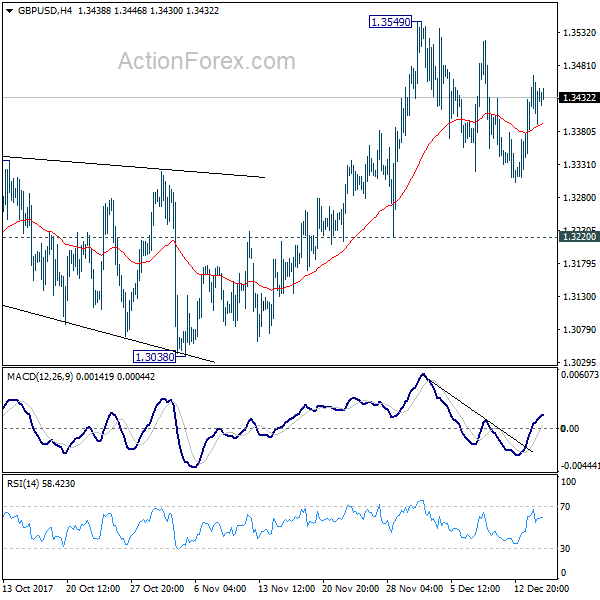

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3387; (P) 1.3425; (R1) 1.3467; More....

GBP/USD drops sharply today as correction from 1.3549 is extending. Intraday bias remains neutral for the moment. Overall, we'd maintain that as long as 1.3220 support holds, further rise is in favor. On the upside, break of 1.3549 will target 1.3651 high next. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Dollar Weak on Tax Plan Jitters, Sterling Even Worse

Dollar stays broadly weak today as Republicans' tax plan is entering the final stage with some political jitters. Nonetheless, the Pound is overtaking Dollar is the weakest one. News that Brexit negotiation is formally entering the next phase provides little support to Sterling. Euro recovers today on news that German SPD is willing to formally start coalition talk with Angela Merkel's CDU/CSU. But the common currency will still likely end as the third weakest as markets took ECB announce negatively. Commodity currencies are set to end the week as the strongest ones.

Actual tax bill texts expected soon, but Senate vote uncertain

Regarding the tax plan, members of the conference committee, the panel of House and Senate lawmakers would likely sign the report early today. Details about what were agreed would be included in the report, as well as the language of the final legislation. The report, and possibly the actual tax bill texts too, will probably released before the weekend.

The chambers are expected to vote on the bill next week but it's unsure whether House of Senate will go first. Situation in the Senate has worsened this week with Marco Rubio of Florida threatened to vote against the bill. Bob Corker of Tennessee could also maintain his "no" vote. It's well known that Republicans only have a slim 52 majority there. Vice President Mike Pence said he's postponed a trip to the Middle East to preside over the Senate vote. His vote may be needed in case of of 50-50 tie.

Released from US, Empire state manufacturing index dropped to 18 in December, down from 19. Canada manufacturing sales dropped -0.4% mom in October.

EU formally agreed to start 2nd phase of Brexit talks

As European Council President Donald Tusk tweeted, "EU leaders agree to move on to the second phase of Brexit talks". It came in as widely expected as it's already declared last week that sufficient progress were made on the negotiations. UK Prime Minister Theresa May told EU leaders during the summit in Brussels that the UK "makes no secret of wanting to move on to the next phase and to approaching it with ambition and creativity". And, she emphasized that "a particular priority should be agreement on the implementation period so that we can bring greater certainty to businesses in the UK and across the 27."

Bundesbank: German economy will grow robustly

Bundesbank raised growth projection for 2018 to 2.5%, up from 1.7%. For 2019, growth is projected to be 1.7%, up from prior 1.6%. For 2020, growth is expected to slow further to 1.5%. Headline inflation projection for 2018 was revised up to 1.6% (from 1.4%), but revised down to 1.7% (from 1.8%) in 2019. Nonetheless, the path is still up from 1.6% to 1.7% and then 1.9% in 2020.

Bundesbank President Jens Weidmann said in a statement that "we will see a persistently high underlying pace of economic growth not only in the final quarter of 2017 and the first quarter of 2018, but also over the remainder of 2018, during which time the German economy will grow robustly."

However, "the further growth opportunities are being constrained, above all, by strong capacity utilization and, in particular, labor shortages."

Japan large manufacturing confidence hit 11 year high

Japan Tankan survey showed improvements in large manufacturing business confidence in Q4. The results support BoJ's upbeat assessment on the economy. And they will likely add to the central bank's confidence that inflation will eventually return to 2% target as economy improves. However, considering the slowdown in capex growth and slower improvement in other readings, there is still a long way to go for the BoJ.

Large manufacturing index rose 3 pts to 25 in Q4, beating expectation of 24. That's also the highest level in 11 years since Q4 of 2006. Large manufacturing outlook was unchanged at 19, below expectation of 22. Large non0manufacturing index was unchanged at 23, below expectation of 24. Large non-manufacturing outlook rose to 20, but missed expectation of 21. All industry capex spending rose 7.4%, slowed from 7.7% and missed expectation of 7.5%.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3387; (P) 1.3425; (R1) 1.3467; More....

GBP/USD drops sharply today as correction from 1.3549 is extending. Intraday bias remains neutral for the moment. Overall, we'd maintain that as long as 1.3220 support holds, further rise is in favor. On the upside, break of 1.3549 will target 1.3651 high next. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Nov | 57.7 | 57.2 | 57.3 | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 25 | 24 | 22 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q4 | 19 | 22 | 19 | |

| 23:50 | JPY | Tankan Large Non-Manufacturing Index Q4 | 23 | 24 | 23 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q4 | 20 | 21 | 19 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 7.40% | 7.50% | 7.70% | |

| 23:50 | JPY | Tankan Small Manufacturing Index Q4 | 15 | 11 | 10 | |

| 23:50 | JPY | Tankan Small Manufacturing Outlook Q4 | 11 | 9 | 8 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Index Q4 | 9 | 9 | 8 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Outlook Q4 | 5 | 5 | 4 | |

| 10:00 | EUR | Eurozone Trade Balance Oct | 19.0B | 24.6B | 25.0B | 24.5B |

| 13:30 | CAD | Manufacturing Sales M/M Oct | -0.40% | 0.90% | 0.50% | 0.40% |

| 13:30 | USD | Empire State Manufacturing Index Dec | 18 | 18 | 19.4 | |

| 14:15 | USD | Industrial Production M/M Nov | 0.30% | 0.90% | ||

| 14:15 | USD | Capacity Utilization Nov | 77.20% | 77.00% | ||

| 21:00 | USD | Net Long-term TIC Flows Oct | 80.9B |

Canadian Dollar Edges Higher, Manufacturing Sales Ahead

The Canadian dollar has posted modest gains this week against the greenback, and continues to move higher in the Friday session. Currently, USD/CAD is trading at 1.2772, down 0.21% on the day. On the release front, it's a quiet end to the week. Canada will release Manufacturing Sales, which is expected to post a strong gain of 0.9%. In the US, the key event is the Empire State Manufacturing Index, with the markets predicting the indicator will soften to 18.8 points.

The Canadian dollar jumped on the currency bandwagon on Wednesday, as the US dollar was broadly lower after the Federal Reserve raised rates by a quarter-point. This marked the third rate hike in 2017, testimony to the strong performance of the US economy. The Fed statement was optimistic about the economy, noting that the labor market "remained strong". It also lowered its unemployment forecast in 2018 from 4.1% to 3.9%, and revised growth for 2018 from 2.1% to 2.5%. Despite this rosy prognosis, the US dollar was broadly down after the announcement. Why? One reason is the sore point in the economy – inflation. The Fed has not changed its September forecast for rate hikes next year, with the Fed dot plot indicating that three rate hikes are projected for 2018. This disappointed some investors who would like to see four increases next year. As well, the rate statement said that the Fed did not expect the tax reform legislation to have any long-term effect on the economy, contradicting White House claims that the legislation would trigger substantial growth in the economy.

The Canadian currency also received a boost from BoC Governor Stephen Poloz, who spoke at an event in Toronto on Wednesday. Poloz presented an upbeat assessment of the Canadian economy, and indicated that there is more room for rate hikes next year. With the Fed raising rates this week, and almost certain to do so again at the January meeting, the BoC will be under pressure to increase rates early in 2018, or the Canadian dollar could take a tumble.

Will President Trump get his tax reform bill on the books before Christmas? The House and Senate are currently working on a reconciliation bill, which would Trump hopes to sign before Christmas. With the Republicans losing a precious Senate seat in Alabama this week, their majority in the Senate has shriveled to just two seats (51-49), so every vote is crucial. Republican senator Mario Rubio has indicated that he might not vote for the tax bill unless child credits are raised, and this has stoked concerns on global markets that the bill might get stalled, which would be a disaster for Trump and could send stock markets sharply lower. The countdown in Washington continues, as a final bill could be unveiled on Friday, with a final vote next week.

Global Stocks Dip on Tax Reform Jitters, Gold Shines

A sense of caution was felt across financial markets during Thursday's trading session as concerns surrounding the progress of U.S. tax reforms resurfaced.

Asian stocks were mostly lower early trading on Friday thanks to this growing uncertainty, while the lack of risk appetite exposed European shares to further losses. With Asian and European markets gripped by U.S. tax reform jitters, Wall Street could come under pressure this afternoon as investors scatter away from riskier assets to safe-haven investments.

Dollar slips on tax reform uncertainty

It has certainly been a rough trading week for the Dollar, which was thoroughly punished by low inflation concerns and growing uncertainty over the fate of U.S. tax reforms.

The impact of Wednesday's dovish U.S. rate hike can still be reflected in the Dollar's price action, with growing concerns about the progress of U.S. tax reform fueling the downside. Taking a look at the technical picture, the Dollar Index still remains under pressure on the daily charts. Repeated weakness below the 93.50 level may open a path lower towards 93.20 and 90.00 respectively.

Currency spotlight - EURUSD

The Euro sharply depreciated against the Dollar during Thursday's trading session after the European Central Bank left rates unchanged in December.

Although the central bank raised growth forecasts, inflation was still predicted to remain below the golden 2% target into 2020. With the ECB reiterating its pledge to provide stimulus as long as needed, bears were offered a fresh opportunity to attack the Euro currency. While the EURUSD has ventured higher during Friday's trading session, there is a suspicion that this could be based on Dollar weakness.

Taking a closer look at the technical picture, the EURUSD is still under some noticeable pressure on the daily charts with 1.1850 acting as a resistance. Sustained weakness below this level may encourage a further decline back towards 1.1730 and 1.1680, respectively. Alternatively, a breakout above 1.1850 could open a path higher to 1.1920.

Commodity spotlight - Gold

Gold prices appreciated during Friday's trading session as the Dollar slipped, driven by investor concerns about the progress of U.S. tax reforms.

The upside was complimented by fears over low inflation in the United States, which clouded the prospects of higher interest rates beyond 2017. With the Dollar vulnerable to further losses, thanks to uncertainty over tax reforms and investors questioning the Federal Reserve's ability to raise rates three times in 2018, Gold (which is zero-yielding) could remain buoyant.

From a technical standpoint, the yellow metal is in the process of a technical bounce on the daily charts, with the next level of interest at $1267. Alternatively, a failure for prices to keep above $1250 has the ability to open a path back towards $1236 and $1230, respectively.