Sample Category Title

Market Update – European Session: European National Central Bank Raise Growth Outlook

Notes/Observations

Various European central banks raise their growth outlook (France, Germany, Austria) in the aftermath followed ECB staff projections (Spain cut citing Catalonia crisis)

Asia:

Japan Q4 Tankan All Industry Manufacturing Index 25 v 24e (11-year high); Large Manufacturing Index: 23e v 24e; Large Manufacturers Outlook: 19 v 22e

BoJ said to ‘tweak’ message as dissenter calls for more easing. BoJ to adjust its communication to flag risks of additional easing after some investors wrong interpreted BOJ Kuroda’s recent remarks on reversal rate theory as a hint about an early policy exit

Europe:

Minority of ECB officials sought to signal guidance may change if inflation keeps accelerating

ECB's Weidmann (Germany): Loose EU monetary policy contributed to deceptive calm; it's a fallacy to believe the euro area was prepared for all cases

UK PM May said expected to ‘back down’ on Brexit date plan to avoid a 2nd Commons defeat next week

Germany Chancellor Merkel: EU leaders could move to Brexit Phase 2. EU leaders have made clear that UK PM May has made good offers which might make it possible for the EU27 to see sufficient progress and agree to move on to phase 2 discussions. There still remain many questions to be solved; time was running out

Bank of France raised GDP growth forecasts for 2017 thru 2019 (in-line with ECB staff projections). Raised 2017 GDP growth forecast from 1.3% to 1.8% and 2018 GDP from 1.5% to 1.7%

Americas:

Senator Rubio said to vote no on tax bill unless working poor tax credit is expanded

Speaker of House Ryan (R-WI) said ti be considering retiring from Congress after 2018

Bank of Canada (BOC) Gov Poloz: To continue to be cautious on rates; growing increasingly confident that the economy would need less monetary stimulus over time

Mexico Central Bank (Banxico) raised Overnight Rate by 25bps to 7.25% (as expected)

Economic Data:

(NL) Netherlands Oct Retail Sales Y/Y: 0.2% v 6.5% prior

(DK) Denmark Nov PPI M/M: 0.9 v 0.5% prior; Y/Y: 1.2% v 1.9% prior

(NO) Norway Nov Trade Balance (NOK): -4.2B v 15.1B prior

(TR) Turkey Sept Unemployment Rate: 10.6% v 10.7%e

(CN) Weekly Shanghai copper inventories (SHFE): 142.1K v 158.1K tons prior

(FR) France Q3 Final Wages Q/Q: 0.3% v 0.3%e

(IT) Italy Oct General Government Debt: €2.290T v €2.284T prior

(EU) Euro Zone Oct Trade Balance (Seasonally Adj): €19.0B v €24.3Be; Trade Balance NSA (unadj): €B v €26.4B prior

Fixed Income Issuance:

(ZA) South Africa sold total ZAR900M vs. ZAR900M indicated in I/L 2029, 2033 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at at 387.9, FTSE -0.1% at 7444, DAX -0.4% at 13020, CAC-40 -0.2% at 5345, IBEX-35 +0.1% at 10189, FTSE MIB -0.4% at 22110, SMI flat at 9382 , S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

European Indices trade largely lower across the board following the lead from Asia and US markets overnight. Markets have drifted slightly lower digesting the plethroa of rate dcesions yesterday with the BoE and ECB keeping rates unchanged.

On the corporate front Swedish retail giant trades sharply lower after big miss on Q4 Rev, citing lower footfall at their physical stores. Elsewhere SDL trades sharply lower in the UK after warning on profits, while SQS Quality software trades over 50% higher on a potential takeover; Tele2 trades higher after merging its Dutch operation with Deutsche Telekom.

Equities

Consumer Discretionary [H&M [HMB.SE] -15.5% (Q4 Rev), Steinhoff [SNH.ZA] -7% (Chairman steps down)]

Telecoms [Telit Comms [TCM.UK] +3.0% (Trading update), Tele2 [TELE2A.SE] +1.8% (Merges dutch ops with Deutsche Telekom)]

Technology [SQS Quality Software [SQS] +54% (Potential takeover), SDL [SDL.UK] -26% (Profit warning)]

Speakers

ECB's Vasiliauskas (Lithuania) stated that did not see need for additional QE in 2018; measures implemented were showing results

ECB's Nowotny (Austria) stated that ECB should look through oil-price impact on inflation

EU's Juncker: stated ahead of the EU Leader Summit that UK PM May had made a big effort and this should be recognized

Italy PM Gentiloni stated that 2nd phase of Brexit would not be easier than the 1st

German Bundesbank raised its GDP growth forecasts for 2017 thru 2019 citing export-driven boom. Raised 2017 GDP from 1.9% to 2.6%; 2018 GDP from 1.7% to 2.5% and 2019 GDP from 1.6% to 1.7%. It did noted that the domestic economy was reaching an increasingly mature state. Export growth to weaken further out, particularly due to capacity constraints and labor shortages

Bank of Italy (BOI) Quarterly Economic Bulletin: Raised GDP growth forecasts for 2017 thru 2019. It raised 2017 GDP growth from 1.4% to 1.6%; 2018 GDP growth from 1.3% to 1.4% and 2019 GDP growth from 1.2% to 1.3%

Bank of Spain (BOS) updated its economic forecasts: Reduces growth outlook citing Catalonia crisis but see economy maintaining growth in the coming 2-3 years

Austria Central Bank updated its economic forecasts which raised the GDP growth forecast for the 2017 thru 2019 period. It also bumped up its inflation view for both 2017 and 2018

Japan government expected to cut JGB sales to market in FY18/19 by about ¥7T from this FY to around ¥134T

Currencies

EUR/USD stayed below the 1.18 level as dealers assessed the implication of still subdued inflation in the euro zone in 2020. The session saw various national central banks follow the ECB lead in upgrading its growth forecast. However, despite the activity exceeding expectations it suspected not to generate further price pressures.

Fixed Income

Bund futures trade 163.53 up 1 tick, following a record high in German manufacturing PMI. Continued upside sees 163.63 then 164.25. A reversal targets 162.50 then 162.38.

Gilt futures trade at 126.29 down 1 tick near the highs for the week. Continued upside eyeing 126.15 then 126.65. Downside targets include 125.24 then 124.75.

Friday’s liquidity report showed Thursday's use of the marginal lending facility fell to €203M from €633M prior.

Corporate issuance saw four issuers raise $2.2B in primary market. Primary expected to close for the year after this week.

Looking Ahead

(BR) Brazil Dec CNI Industrial Confidence: No est v 56.5 prior

05:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to cut 1-Week Auction Rate by 25bps to 8.00%

06:00 (IE) Ireland Q3 GDP Q/Q: 1.6%e v 1.4% prior; Y/Y: No est v 5.8% prior

06:00 (IE) Ireland Q3 Current Account Balance: No est v -€0.9B prior

06:00 (IE) Ireland Oct Trade Balance: No est v €3.6B prior

06:00 (BR) Brazil Oct IBGE Services Sector Volume Y/Y: -0.8%e v -3.2% prior

06:00 (UK) DMO to sell combined £5.0B in 1-month, 3-month and 6-month Bills (£2.0B, £1.0B and £2.0B respectively)

06:30 (IN) India Weekly Forex Reserves

06:45 (US) Daily Libor Fixing

07:00 (IS) Iceland Nov Unemployment Rate: No est v 1.9% prior

07:00 (IL) Israel Nov CPI M/M: -0.2%e v +0.3% prior; Y/Y: 0.4%e v 0.2% prior

07:00 (UK) BOE Quarterly Bulletin:

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Dec Empire Manufacturing: 18.8e v 19.4 prior

08:30 (CA) Canada Oct Manufacturing Sales M/M: 0.9%e v 0.5% prior

09:00 (BE) Belgium Oct Trade Balance: No est v €1.4B prior

09:15 (US) Nov Industrial Production M/M: 0.3%e v 0.9% prior; Capacity Utilization: 77.2%e v 77.0% prior, Manufacturing Production: 0.3%e v 1.3% prior

10:00 (CO) Colombia Oct Industrial Production Y/Y: +0.8%e v -1.9% prior, Retail Sales Y/Y: 1.2%e v 1.4% prior

10:00 (MX) Mexico Central Bank (Banxico) Economist Survey

11:00 (EU) Potential sovereign ratings after EU close

(PT) Portugal Sovereign Debt to be rated by Fitch

(IE) Ireland Sovereign Debt to be rated by Fitch

(UK) United Kingdom Sovereign Debt to be rated by DBRS

13:00 (US) Weekly Baker Hughes Rig Count data

16:00 (US) Oct Total Net TIC Flows: No est v $51.3B prior; Net Long-Term Tic Flows: No est v $80.9B prior

Weekend events:

(DE) Bavaria's Ruling CSU Party Holds Convention

(ZA) South Africa ruling African National Congress (ANC) leadership election

(BR) Brazil Oct Economic Activity Index (monthly GDP) M/M: No est v 0.4% prior; Y/Y: No est v 1.3% prior

EUR/CHF 4H Chart: In Triangle

The previously described and mysterious support line on the EUR/CHF currency pair chart has done its work. However, another important trend line has been noticed.

The currency rate faces a resistance line, which is of similar scale than the previously described trend line. This trend line together with the previously described support are creating a medium scale triangle pattern.

However, to which side the pair will break out is quite unclear, as for that the larger scale situation should be looked at. Meanwhile, look up how to actually trade triangle patterns.

USD/RUB 4H Chart: Reconfirms Dominant Support

Due to notable developments on the USD/RUB currency pair’s chart a review of the situation is done by Dukascopy analytics department.

In general the pair has broken the previously mapped channel up pattern to the downside due to fundamental events in the United States. However, the currency pair has not moved out of the larger scale trend. Instead it has provided an opportunity to adjust the trend lines of the dominant pattern.

Meanwhile, in regards what all the readers want to know, the short term is quite tricky, as the pair is set to face various resistance levels at the 59.00 mark. Until they are broken, the pair might trade sideways.

CRUDE OIL Ready For Another Leg Higher

Crude oil is has failed to break resistance given at 59.05 (24/12/2017 high). Support is given at 55.82 (07/12/2017 low). Expected to bounce back higher.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

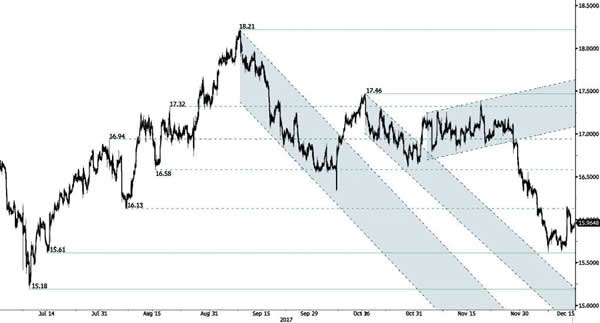

SILVER Lack Of Follow-Through

Silver has been bouncing on hourly support at 15.61 (14/07/2017 low). Hourly resistance is given at 16.15 (13/12/2017 high). Expected to show renewed bearish pressures.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

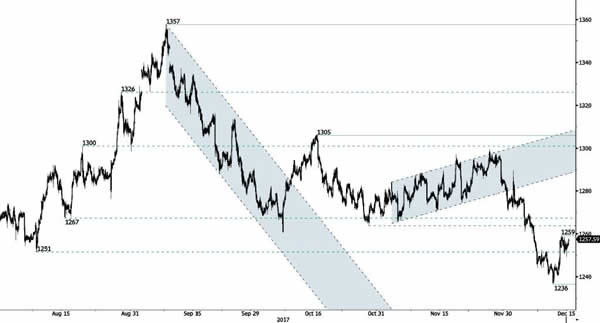

GOLD Short-Squeeze

Gold is consolidating after the strong collapse even though traders are taking some profit. . Hourly support is given at 1236 (12/12/2017 low) . Resistance is located at 1259 (14/12/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Ready For A Bullish Breakout

Bitcoin's bullish momentum is far fom over. The technical structure has shown a tremendous positive short-term momentum. Hourly support is located below 14k (08/12/2017 low). Strong support stands very far at 2975 (22/08/2017 low). In the short-term, the digital currency should continue rising at levels unseen so far.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $40'000 in 2018.

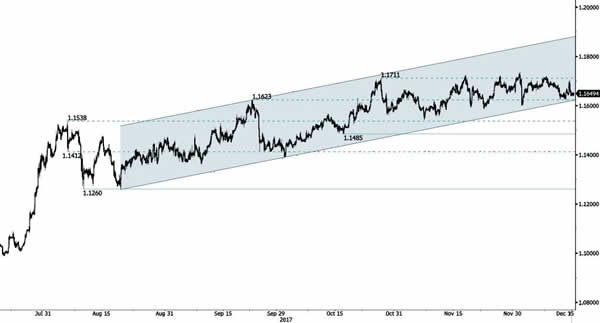

EUR/CHF Stalling Below 1.1700

EUR/CHF continues to push towards resistance area above 1.17 and support given at 1.1610 (27/10/2017 low). Expected to show continued increase.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Edging Lower

EUR/GBP is trading slightly lower. The pair is trading between support at 0.8689 (08/12/2017 low). Resistance is located at 0.8867 (05/12/2017 high). Expected to show further sideways trading.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Bullish Move

AUD/USD's downside pressures have vanished. Hourly resistance is given at a distance at 0.7730 (02/11/2017 high). Support stands at 0.7502 (08/12/2017 low). Expected to push even higher.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.