Sample Category Title

BoC: Poloz Worries, But Feels We’re Still “Close to Home”

Bank of Canada Governor Stephen Poloz gave a speech today focused on the things keeping him awake at night.

Before getting to his concerns, Poloz laid out his view on the current state of play, noting that 2018 is "looking positive", with the export recovery to be "pulled along by rising foreign demand". Referencing prior speeches, he judged that "we find ourselves quite close to home, and getting closer".

The focus of the speech were the several key issues that concern the Governor: cyber threats, high home prices and household debt, and the tough job market for young people. He also commented on cryptocurrencies.

The latter risks are probably of most interest. On house prices and household debt, the 40% figure came up twice: this is both the share of housing backed loans that have a home-equity line of credit (HELOC) component, and the share of those HELOC borrowers that are not regularly paying down their principal. Poloz sees this as a risk, particularly if these lines of credit are being used to further speculate in housing markets. He was very supportive of the updated B20 mortgage stress test, advising borrowers that may choose to skirt the regulation by choosing an institution that doesn't impose the new test that ensuring you can handle rising rates is nevertheless a good idea.

Poloz noted that of the more than 350k full-time jobs created so far this year, only about 50k have gone to those aged 15-24. He also remarked that were the youth participation rate be brought back to pre-crisis levels, some 100k more young people would have jobs. This has the potential to create a long-term impact if these young people are not building the work experience that they otherwise would be. Encouragingly, the Governor noted that with the economy in a sweet spot right now, people are being more encouraged to enter or re-enter the workforce, as seen by rising wages and a tick-up in the participation rate among young people.

The Governor also took a moment to comment on cryptocurrencies, calling the term itself a misnomer as instruments like Bitcoin, in his view, are neither a store of value or act as a medium of exchange. Noting that he was not giving investment advice, he characterized the market as buying risk - calling it more like gambling than investing.

Key Implications

For Governor Poloz, what keeps him up at night isn't wondering whether Quentin Tarantino will actually make a Star Trek movie (though it might be), but ongoing issues in the Canadian economy. Specifically, it is cyber threats, housing markets and household debt, and the state of youth employment that generate restless nights for the Governor. However, in each case, Poloz made the point that progress is being made.

Indeed, despite the speech ostensibly being about the Governor's worries, it carried a somewhat hawkish bent. The three key areas of concern are seen as being addressed, at least on an ongoing basis. On top of this, while we were reminded that monetary policy is an exercise in risk management, ultimately Poloz sees the economy as being 'quite close to home' and has maintained a positive characterization of 2018 - something that suggests that we may be closer to the next hike than markets have been expecting of late.

Ultimately, while the decision may come down to the wire, today's speech confirms our view that the next hike will likely come sooner rather than later. As discussed in our latest Quarterly Economic Outlook, the Canadian economy is expected to run at an above-potential pace for a while longer. As such, although caution remains the watchword, we expect the incoming data to guide Poloz towards another rate hike in early-2018.

Canadian Dollar Higher After Poloz Hawkish Comments

The Canadian dollar appreciated on Thursday after Bank of Canada (BoC) Governor Stephen Poloz spoke at the Canadian Club in Toronto. His speech was titled "The Three Things Keeping Me Awake at Night". Poloz delivers a hawkish assessment of the economy confident that less stimulus will be needed going forward. The economy is in a sweet pot in the economic cycle running close to full output and inflation near the 2 percent target.

The USD/CAD was higher earlier in the session, but the loonie got support from Poloz's speech by keeping an interest rate hike on the table for the first quarter of 2018. The Bank of Canada (BoC) raised rates twice in 2017 to leave the benchmark rate at 1.00 percent, but as the economy cooled, so did the rhetoric. The words today from the BoC Governor suggest that current rates are still too low, but all monetary decisions will be based on the evolution of the economy.

After the U.S. Federal Reserve hiked the Fed funds rate on Wednesday by 25 basis points, the third lift by the central bank this year, the gap between the Canadian rate and the American rate was expected to grow as the BoC did not appear to be ready to raise. The statement from Mr Poloz makes it clear that the neutral rate for the Canadian central bank is higher, but also that it is no rush to get there and will do so only when the economy justifies it.

The USD/CAD lost 0.47 percent in the last 24 hours. The currency pair is trading at 1.2754 after the words from Bank of Canada (BoC) Governor Stephen Poloz pushed the loonie higher.

Mr Poloz focused on three things keeping him up at night: cyber threats, high house prices and household debt and the tough job market for young people. Housing related concerns are highly relevant given the new mortgage rules to try to keep prices grounded will come into effect on January 1st. Canadian borrowers are stretching themselves by combining mortgages with lines of home equity. Canadian banks have already suffered credit downgrades given their exposure to a fall in prices or higher rates that could make the payments unsustainable for these borrowers and the BoC is right to be monitoring the situation as it related to the path of interest rates in 2018.

NAFTA was a topic Poloz addressed several times during his speech and in the Q&A afterward. The Governor believes that the uncertainty of the trade deal is holding back investment in Canada. As negotiatiors meet in Washington without political interference this intercessional meeting is expected to bring tangible, albeit smaller results. Canada, Mexico and industries that would be affected by the sudden exit (6 months) if the Trump administration decides to terminate its involvement in the agreement, have started to lobby for a change in tactics. The defeat of Republican candidate Roy Moore in the special senate election will weigh on Republicans that side with the part line instead of the people.

Oil prices rose on Thursday. West Texas Intermediate is trading at $57.04 as the disruption in the North Sea pipeline continues to support higher prices. The outage of the Forties pipeline kept prices higher as crude inventories continue to shrink. The Organization of the Petroleum Exporting Countries (OPEC) trade agreement is partly responsible but of concern to traders is the rise in gasoline stocks signalling a lack of demand.

The Energy Information Administration (EIA) released its weekly US crude and gasoline stocks on Wednesday. Oil inventories shrank by 5.1 million barrels, but gasoline grew by 5.7 million barrels. Distillates proved to be the tie breaker as it also fell by 1.4 million barrels. Supply disruptions have kept lack of demand and rising US production in check versus the OPEC and other major producers efforts to reduce their output to stabilize prices.

Gold Yawns as Retail Sales Jump

Gold has ticked lower in the Thursday session. In North American trade, the spot price for an ounce of gold is $1254.27, down 0.11% on the day. On the release front, consumer spending indicators looked sharp, as Core Retail Sales and Retail Sales improved in November, with readings of 1.0% and 0.8%, respectively. Both indicators beat expectations. There was positive news on the employment front, as unemployment claims fell to 225 thousand, well below the forecast of 237 thousand. On Friday, the US releases the Empire State Manufacturing Index.

There were no surprises from the Federal Reserve, which raised rates on Wednesday, bringing the benchmark rate to a range between 1.25% and 1.50%. This marked the third rate hike in 2017, testimony to the strong performance of the US economy. The Fed statement was optimistic about the economy, noting that the labor market "remained strong". It also lowered its unemployment forecast in 2018 from 4.1% to 3.9%, and revised growth for 2018 from 2.1% to 2.5%. Despite this upbeat assessment, gold prices moved higher, as the US was broadly lower after the rate announcement. Why did investors give the dollar a thumbs-down despite a rate hike? One reason is the Achilles heel of the US economy – inflation. The Fed has not changed its September forecast for rate hikes next year, with the Fed dot plot indicating that three rate hikes are projected for 2018. This disappointed some investors who would like to see four increases next year. As well, the rate statement said that the Fed did not expect tax reform legislation to have any long-term effect on the economy, contradicting White House claims that the legislation would trigger substantial growth in the economy.

The Fed is pleased with the strength of the US economy, but remains puzzled why strong growth and a red-hot labor market has not led to higher inflation. The labor market continues to operate at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages. The Fed appears ready to continue to jack up rates, despite the lack of inflation. The markets are preparing for another quarter-point increase next month, with the odds of a rate hike standing at a remarkable 100%, according to the CME Group.

Pound Steady as BoE Stays on the Sidelines

The British pound is showing little movement in the Thursday session. In North American trade, GBP/USD is trading at 1.3429, up 0.10% on the day. On the release front, Retail Sales jumped 1.1%, crushing the estimate of 0.4%. As expected, the Bank of England maintained the benchmark rate at 0.50%. In the US, consumer spending climbed, as Core Retail Sales and Retail Sales improved in November, with readings of 1.0% and 0.8%, respectively. Both indicators beat expectations. There was positive news on the employment front, as unemployment claims fell to 225 thousand, well below the forecast of 237 thousand. On Friday, the US releases the Empire State Manufacturing Index.

Earlier on Thursday, the Bank of England maintained interest rates at 0.50%. Although this was not a surprise, the vote was significant in that there were no dissenters, as all 9 policymakers were in agreement for the first time since February. BoE Governor Mark Carney will certainly be pleased with the unanimous vote, but could be on the hot seat as inflation continues to creep higher. CPI climbed to 3.1% in November, edging above the forecast of 3.0%. Inflation is now running at its highest level since March 2012, and Carney will have to write an open letter to open letter to the British finance minister, explaining how the BoE plans to lower inflation closer to the Bank's target of 2.0%. Carney would rather not raise rates in the next few months, but that could be the most effective tool in bringing down inflation, which is at uncomfortably high levels.

There were no surprises from the Federal Reserve, which raised rates on Wednesday, bringing the benchmark rate to a range between 1.25% and 1.50%. This marked the third rate hike in 2017, testimony to the strong performance of the US economy. The Fed statement was optimistic about the economy, noting that the labor market "remained strong". It also lowered its unemployment forecast in 2018 from 4.1% to 3.9%, and revised growth for 2018 from 2.1% to 2.5%. Despite this rosy prognosis, the dollar was broadly down after the announcement. Why? One reason is the sore point in the economy – inflation. The Fed has not changed its September forecast for rate hikes next year, with the Fed dot plot indicating that three rate hikes are projected for 2018. This disappointed some investors who would like to see four increases next year. As well, the rate statement said that the Fed did not expect the tax reform legislation to have any long-term effect on the economy, contradicting White House claims that the legislation would trigger substantial growth in the economy.

BoJ Tankan Survey Attracting Interest; Yen in Focus

The Bank of Japan's fourth quarter tankan survey is due at 2350 GMT on Thursday. Big manufacturers' confidence in business conditions in Japan stood at a decade high in the third quarter, with fourth quarter projections indicating that positive momentum is to be maintained.

The Tankan big manufacturers index is expected to come in at 24 in Q4, reflecting its fifth consecutive quarterly rise and standing at its highest in 11 years. This compares to Q3's 22. Strong demand from foreign markets, in conjunction with corporate profitability exceeding expectations, are seen as boosting business confidence in the world's third largest economy. The Tankan big non-manufacturers index, a separate measure gauging sentiment in the services sector, is anticipated to remain at 23, its highest in two years.

It is not just overseas demand supporting sentiment though, but domestic as well. In the third quarter of the year the Japanese economy grew by 2.5% on an annualized basis, far exceeding forecasts of 1.5% and recording its seventh straight quarter of positive economic growth, the longest such stretch since the period between Q2 1999 and Q1 2001 during which the Japanese economy grew for eight straight quarters. The 2020 Tokyo Olympic Games are also promoting - and are expected to continue doing so - activity and sentiment in the nation.

Data on capital expenditure by big corporations are expected to show an increase in spending for the current fiscal year to March 2018 by 7.5% on an annualized basis, slightly below Q3's respective number of 7.7%.

Beyond the aforementioned releases, the respective data for small manufacturers and non- manufacturers will also be made public at 2350 GMT, with polls projecting an improvement in the numbers relative to the third quarter.

The tankan survey results may not be perceived as a typical market mover, but still more upbeat figures could lend some support to the yen. A strengthening Japanese currency relative to the US dollar - resulting in a weakening dollar/yen pair - could find support around the current level of the 200-day moving average at 111.63.

On the other hand, weaker-than-anticipated results could spur forex market participants to push dollar/yen higher. In such an event, the pair could meet resistance around 112.86, this being the current level of the 50-day moving average. Notice that price action is currently taking place close to this level. Stronger bullish movement might meet a barrier around December 12's one-month high of 113.74. Also, one should not disregard that beyond the release, US-related news definitely have the capacity to steer the pair in either direction.

December 17 (2350 GMT) will also see the release of Japanese trade data - exports, imports and trade balance - for the month of November. For the most part throughout 2017, year-on-year exports and imports grew by double digits in the months that preceded.

NZDUSD Shifts to Bullish after Surging to 8-Week High

NZDUSD surged more than 1% on Wednesday to hit its highest level since October 20 at 0.7027. The strong up-move happened after a break out of a consolidation phase and has shifted the bias to the upside, though today's down move is attempting to threaten the positive bias.

Short-term trend signals on the 4-hour chart (20 and 50-period moving averages) are bullishly aligned and NZDUSD is expected to find support on dips for now.

The market became overbought following the peak at 0.7027 as was indicated by the RSI crossing above 70 and there was a subsequent pullback for the pair towards 0.6985 today. This level is expected to act as a strong short-term support and corresponds to the 23.6% Fibonacci retracement of the rise from the December 11 low of 0.6827 to Wednesday's 0.7027 peak.

A deeper retracement will risk eliminating the bullish bias but as long as NZDUSD remains above 0.6900 there is room for a push towards the key 0.7100 area. A clear break above Wednesday's high would indicate the market has clearly moved into a bullish phase.

Yen Edges Higher, Investors Eye Tankan Indices

USD/JPY has posted slight gains in the Thursday session. In North American trade, USD/JPY is trading at 112.64, up 0.10% on the day. On the release front, Japanese indicators were positive. Flash Manufacturing PMI improved to 54.2, and Revised Industrial Production rebounded with a gain of 0.5%, matching the forecast. Later in the day, Japan releases the Tankan Manufacturing and Non-Manufacturing Indices, with both indicators expected to improve to 24 points.

There were no surprises from the Federal Reserve, which raised rates on Wednesday, bringing the benchmark rate to a range between 1.25% and 1.50%. This marked the third rate hike in 2017, testimony to the strong performance of the US economy. The Fed statement was optimistic about the economy, noting that the labor market "remained strong". It also lowered its unemployment forecast in 2018 from 4.1% to 3.9%, and revised growth for 2018 from 2.1% to 2.5%. Despite this rosy prognosis, the dollar was broadly down after the announcement. Why? One reason is the sore point in the economy – inflation. The Fed has not changed its September forecast for rate hikes next year, with the Fed dot plot indicating that three rate hikes are projected for 2018. This disappointed some investors who would like to see four increases next year. As well, the rate statement said that the Fed did not expect the tax reform legislation to have any long-term effect on the economy, contradicting White House claims that the legislation would trigger substantial growth in the economy.

When the Bank of Japan implemented its radical stimulus plan, one of the primary goals was to eliminate deflation and push prices higher. Years later, however, the BoJ's inflation target of 2 percent remains elusive. However, the program has led to a sharp depreciation in the yen. This has led to sharp denunciations from the US and other countries, and criticism that the Bank was manipulating the yen was especially sharp when the dollar rose to around 120 yen. A weak yen has been a boon for exports and helped revive the manufacturing sector. A chief economist at the NLI Research Institute went as far as saying that the low yen has been a major accomplishment for the BoJ. According to this view, the BoJ is reluctant to signal the possibility of a taper of stimulus, since that could trigger a sharp rise in the yen. Clearly, the BoJ is closely following yen fluctuations, and currency movement will continue to be an important factor for the BoJ.

EURUSD – Post-Fed Bulls Lost Traction after Upbeat US Data; Near-Term Focus Turns Lower

The Euro was sharply lower in the US session as the greenback received fresh boost from upbeat US retail sales which rose by 0.8% in November, strongly beating forecast for 0.3% increase.

US weekly jobless claims also surprised by falling to 225K vs forecasted rise to 239K, adding to fresh dollar's strength.

Fresh weakness commenced after extension of post-Fed rally stalled on approach to pivotal barrier at 1.1867 (Fibo 61.8% of 1.1961/1.1717 downleg) and accelerated after better than expected US data.

The latest move is generating negative signal after repeated failure to close above daily cloud top and subsequent weakness forming the right shoulder of H&S pattern on daily chart.

The H&S neckline lies at 1.1715 and break lower is needed to complete the pattern and signal further downside.

Daily studies are gaining negative tone as RSI turned south and probes below its 7-day MA and 14-day momentum is deeply in the negative territory.

Near-term bears are taking a breather above daily Kijun-sen (1.1773) where temporary footstep was found.

Prevailing bearish near-term tone could be expected while the price stays below 1.1800 (converging 10/100SMA's in attempt to form bear-cross.

Daily cloud top (1.1823) remains a key barrier and sustained break higher is needed to revive bulls.

Res: 1.1800; 1.1823; 1.1867; 1.1878

Sup: 1.1773; 1.1759; 1.1715; 1.1709

Diffuse News Flow Confines USD Trading to Tight Ranges

- European equity markets currently trade with small losses, recovering somewhat after the ECB meeting. US stock markets open with limited gains.

- Businesses across the euro zone are ending 2017 on a near seven-year high, with demand and price pressures picking up and forward-looking indicators pointing to a busy start to 2018. The EMU composite PMI climbed to 58.0 this month, its highest since February 2011 and beating the 57.2 forecast.

- Black Friday gave UK retailers a stronger-than-expected boost last month as discounts spurred Britons to snap up electrical appliances and other household products. The volume of goods sold in stores and online jumped 1.1% from October, the most in seven months. Sales excluding auto fuel rose 1.2%.

- US retail sales rose more than forecast in November (0.8% M/M from an upwardly revised 0.5% M/M). Core retail sales and the retail control group (which feeds into GDP) also rose by 0.8% M/M from upward revision to 0.4% M/M in October. US weekly jobless claims unexpectedly dropped to 225k, remaining near historically low levels.

- The ECB kept its policy rates unchanged as expected. The forward guidance on asset purchases and interest rates also remained the same. The central bank significantly raised the economic outlook in its new projections, citing greater confidence in the recovery. New inflation forecasts remain rather low though.

- Bank of England policy makers left interest rates unchanged, moving into a holding pattern after November saw their first hike in a decade. The MPC reiterated that "further modest increases" would probably be needed over the next few years if the economy performed as expected, without providing additional detail on the timing.

- The Norges Bank kept its policy rate unchanged at 0.5%. EUR/NOK declined from 9.85 to 9.75 as the central bank said in its monetary assessment report that "on the whole, the changes in the outlook and the balance of risks imply a somewhat earlier increase in the key policy rate." The central bank referred to "after autumn 2018".

- The Swiss National Bank expects inflation in Switzerland to exceed its target in three years -an indication of when it might exit its ultra-loose monetary policy. The SNB kept that policy in place, saying the Swiss franc weakened this year but remained"highly valued".

- Turkey's central bank raised the highest of the four interest rates it uses to set policy by a less-than-expected 50 bps, its first rate hike in eight months after inflation hit a 14-year peak last month. The Turkish lire tumbled with EUR/TRY rising from 4.5 to 4.6.

Rates

ECB lifts growth outlook, but hushes on inflation

Global core bonds lost ground today with US Treasuries underperforming German Bunds. Last night's sell-the-rumour, buy-the-fact reaction on the Fed's well-flagged rate hike proved to be short-lived. The central bank still intends to continue its tightening cycle in coming years, which is far from discounted in markets. EMU (December PMI survey) and US (November retail sales; weekly jobless claims) printed very strong. They added to bearish bond sentiment without having a direct impact. The ECB kept policy unchanged, but significantly upgraded its growth outlook, inflicting additional losses on the Bund. Dovishness on inflation limited the downside though. Overall, we think that losses could have been bigger given developments today and last night.

At the time of writing, changes on the US yield curve rise by 1.5 bps (30-yr) to 3.9 bps (5-yr). The German yield curve shifts 0.2 bps (30-yr) to 3 bps (5-yr) higher. On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrow up to 5 bps (Spain/Portugal) with Greece outperforming (-12 bps).

The ECB kept its policy rates unchanged as expected. The forward guidance on asset purchases and interest rates also remained the same. The Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases. There was no discussion on cutting this link. The GC confirmed that from January 2018 it intends to continue to make net asset purchases under the asset purchase programme (APP), at a monthly pace of €30 bn, until the end of September 2018, or beyond, if necessary, and in any case until the GC sees a sustained adjustment in the path of inflation consistent with its inflation aim.

The ECB significantly raised the economic outlook in its new projections, citing greater confidence in the recovery. The central bank forecasts above trend growth in 2017 (2.4% from 2.2%), 2018 (2.3% from 1.8%), 2019 (1.9% from 1.7%) and 2020 (1.7%). Risks for this scenario are broadly balanced. Downside risks are mainly related to global factors and developments in FX markets. The central bank expects that the output gap will close in the course of next year. There has been a "significant" reduction in economic slack, which is an upgrade from the October assessment of a "gradual" reduction.

The strong economic momentum signals that inflation will pick up, but the ECB judges that an ample degree of monetary stimulus is therefore still needed. Headline CPI is likely to moderate in coming months because of the evolution in energy prices before gaining upward momentum. Core inflation is expected to rise gradually over the medium term. New inflation forecasts remain rather low though despite the upbeat economic outlook and despite the ECB's increasing confidence that inflation will return to target. The new forecasts (especially for 2020) give Draghi enough room to manoeuver and defend the current easy monetary policy stance. The ECB expects inflation to average 1.5% in 2017 (from 1.5%), 1.4% in 2018 (from 1.2%), 1.5% in 2019 (from 1.5%) and 1.7% in 2020. Muted wage growth keeps the ECB cautious.

Currencies

Diffuse news flow confines USD trading to tight ranges

There was plenty of eco and central bank news to guide global FX trading today. However, no theme succeeded to dominate trading. Eco data were strong both in the US and in EMU. The ECB also failed to bring a straightforward story to give euro trading a clear direction. EUR/USD trades currently slightly north of 1.18 area. USD/JPY hovers in the 112.60.70 area.

Asian equities opened mixed overnight, but ceded gradually ground. Chinese data printed close to expectations. The PBOC raised the rate for some reverse-repurchases, confirming its intention to curb (excessive) leverage. The dollar stabilized after yesterday's setback. EUR/USD traded in the 1.1825 area. USD/JPY changed hands in the 112.60/70 going into the start of European trading.

European markets initially didn't know how to react to yesterday's developments in the US. European PMI's (both manufacturing and services) confirmed that the EU economy is firing on all cylinders, moving higher from already exceptional levels. Core bond yields drifted gradually back north after yesterday's correction in the US. Interest rate differentials between the US and Europe remained slightly tighter compared to the levels on the screens yesterday before the Fed/CPI data. However they didn't narrow any further. EUR/USD traded sideways in an extremely tight range, roughly between 1.1810/45 going into the ECB policy decision and the US retail sales data.

The ECB as expected left its policy unchanged. The ECB substantially raised the growth forecasts for 2017/2019, but the 2020 inflation forecast remained at a relatively soft 1.7%. The ECB president also said that the forward guidance was not discussed today, but it might become an issue in the coming months. At the same time of the start the ECB press conference, US retail sales printed much stronger than expected and US jobless claims declined to a very low 225 000. So, plenty of divergent information for EUR/USD traders. For now, the dollar wins on points. EUR/USD trades again in the low 1.18 area. However, the picture remains highly indecisive. USD/JPY tries to move away from the post-Fed overnight low, supported by strong EMU and US eco data. However, the move also fails to gain traction, probably as equities are struggling. The pair hovers in the 112.75 area. Conclusion: plenty of (mostly good) news, but no clear direction for the dollar.

BoE fails to guide sterling trading

As was the case for EUR/USD trading, there was also no unequivocal story to guide sterling trading. UK November retail sales beat the consensus by a wide margin, but had only a temporary positive impact on sterling. The BoE as expected left is policy unchanged. The Bank sees last week's Brexit deal as reducing the chances of disorderly UK departure. However, the BoE also sees tentative signs that the economy might be slowing into the yearend. There were no specific indications that the BoE considers a next rate hike in the near/foreseeable future. UK PM May attends the EU summit in Brussels and tries to convince the 27 EU leaders to approve the proposal to move to the next stage of the negotiations. The deal is likely to be approved tomorrow. However, even in that scenario, plenty of hurdles will have to be removed. The conclusion for EUR/GBP is quite similar than to EUR/USD: plenty of interesting news but no clear story for sterling trading. EUR/GBP hovers around the 0.88 pivot. Cable trades in the 1.34 area.

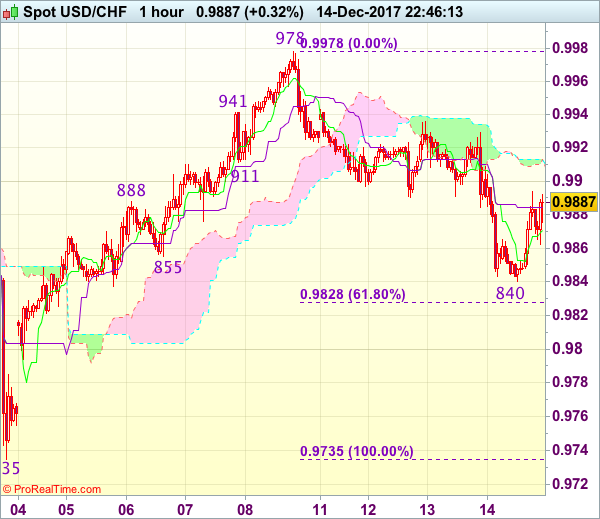

Trade Idea : USD/CHF – Buy at 0.9870

USD/CHF - 0.9902

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9875

Kijun-Sen level : 0.9875

Ichimoku cloud top : 0.9910

Ichimoku cloud bottom : 0.9908

Original strategy :

Exit long entered at 0.9860,

Position : - Long at 0.9860

Target : -

Stop : -

New strategy :

Buy at 0.9870, Target: 0.9970, Stop: 0.9835

Position : -

Target : -

Stop : -

Although the greenback fell marginally to 0.9840, renewed buying interest emerged there and dollar has staged another rebound, consolidation with upside bias is seen for further gain to 0.9935-40 but break there is needed to retain bullishness and signal low is formed, bring further gain towards resistance at 0.9978, however, only break there is confirm recent upmove has resumed and extend headway to psychological resistance at 1.0000.

In view of this, we are looking to buy dollar again on pullback as 0.9865-70 should limit downside. Below said support at 0.9840 would extend the fall from 0.9978 top for retracement of recent rise to 0.9820, then towards 0.9790-95, having said that, near term oversold condition should limit downside and price should stay above 0.9755-60, bring rebound later.