Sample Category Title

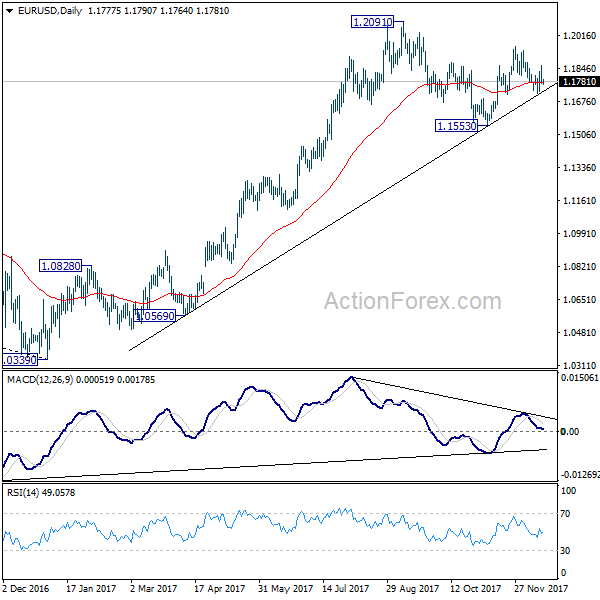

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1743; (P) 1.1803 (R1) 1.1835; More....

EUR/USD's rebound from 1.1717 was limited at 1.1862 and retreated deeply. Intraday bias is turned neutral first. Overall, near term outlook remains bullish with 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708) intact. Further rally is expected and above 1.1862 will target 1.1900 first. Break will target 1.2029 high next. However, decisive break there will indicate that rebound from 1.1553 has completed at 1.1960. In that case, deeper fall would be seen to 1.1553 and possibly below to extend the decline from 1.2091.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

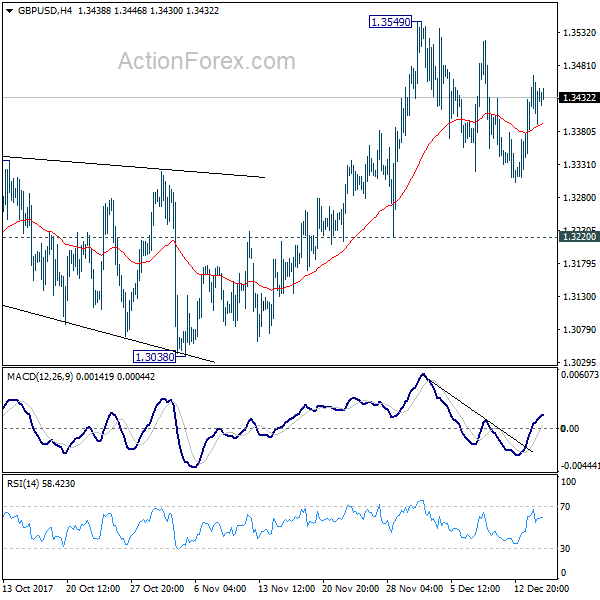

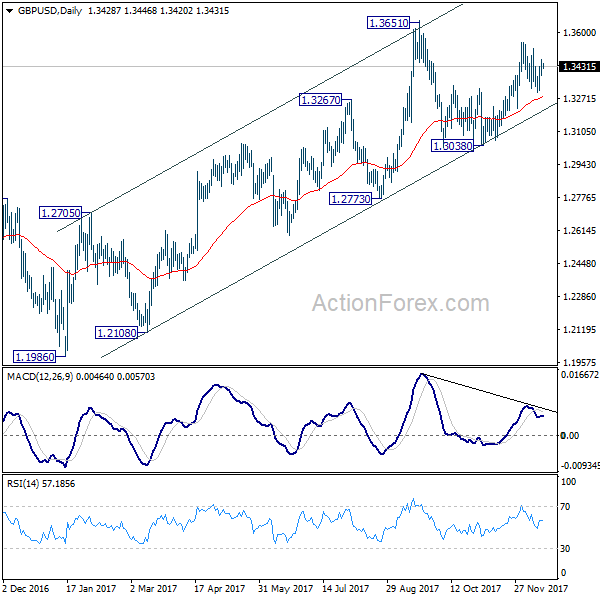

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3387; (P) 1.3425; (R1) 1.3467; More....

The corrective pattern from 1.3549 is still unfolding and intraday bias remains neutral. Another fall cannot be ruled out yet. But after all, as long as 1.3220 support holds, we'd continue to favor another rise. On the upside, break of 1.3549 will target 1.3651 high next. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

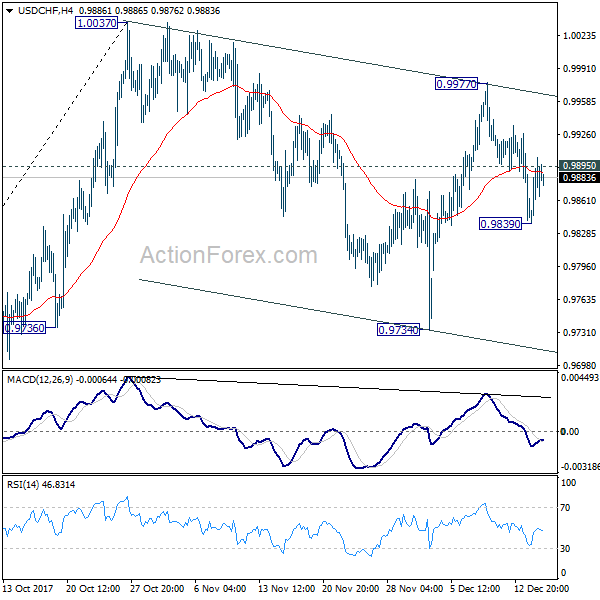

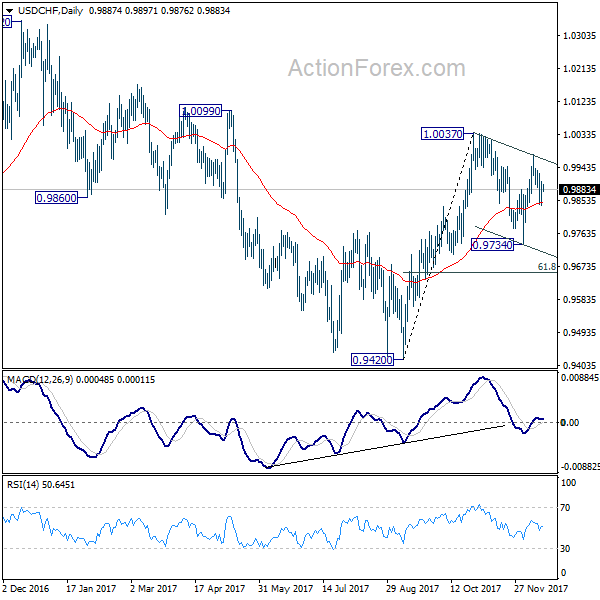

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9850; (P) 0.9877; (R1) 0.9915; More....

Breach of 0.9895 minor resistance argues that pull back from 0.9977 might be completed at 0.9839. But upside momentum is weak so far. Intraday bias is turned neutral first. On the downside, break of 0.9839 will extend the fall from 0.9977. Such decline is seen as part of the correction pattern from 1.0037. It could target 0.9734 support and below. But we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. On the upside, break of 0.9977 will revive near term bullishness and target 1.0037 and above.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Market Morning Briefing: Dollar-Index Reached A Low Of 93.28

STOCKS

Dow (24508.66, -0.31%) has weekly resistance near 24700 and if that holds, the index could enter into a sideways consolidation mode within 24700-24000 before again moving up towards 25000 in the longer term.

Dax (13068.08, -0.44%) came off sharply and could try to re-test lower levels of 12900 again before moving back towards 13100 or higher. For now, near term trade is likely to be stuck in the 13150-12900 region.

Nikkei (22494.76, -0.88%) has been pulled down by the US-Japan 10YR yield spread and Dollar Yen. While these look bearish for the near term, Nikkei could be headed towards 22250.

Shanghai (3275.53, -0.51%) is unable to move up$ sharply above 3270. Shanghai could either remain range-bound just now or try to move down towards 3250 again before it is pushed upwards. Near term likely to be sideways.

Nifty (10252.10, +0.58%) is fluctuating in the 10150-10300 region. It could well be ranged within the said region for some more time before it decides on further direction.

Sensex (33246.70, +0.59%) may bounce from levels near 32750. Overall sideways range-trade possible within 33500-32750 region.

COMMODITIES

Gold (1254.90) has paused a bit after making an intra-day high of 1260 as expected. While 1260 holds, the price may fall back towards 1240; else a break above 1260 if sustains could trigger a rally towards 1280 and higher.

Brent (63.33) and WTI (57.19) are both trading higher today. While support on Brent holds at 62, the price could eventually test 68 in the medium term while WTI is likely to re-test crucial levels of 59-60 resistance zone.

Copper (3.0755) has moved up a bit and could test important resistance near 3.10 which may push prices back towards 3.00-2.95 levels in the near to medium term.

FOREX

Dollar-Index (93.56) reached a low of 93.28 yesterday post the Fed rate hike but has been trading higher around 93.5-93.6 post the ECB announcement that they will be continuing their asset purchase programme till Sept next year, thereby indicating possible weakness in the Euro relative to the Dollar. However, the impact of this might be temporary in nature and we still expect to see the Index move towards support at 93 in a week or two.

Euro (1.1786) after seeing a high of 1.1863 yesterday has now dropped and is currently trading in the 1.177-1.179 range. The ECB’s plans to continue injecting liquidity in the medium term and its concerns about global factors (which could possibly affect European exports) point towards a possible interest in not letting Euro rise and harm exports. Although Euro is trading lower currently, we expect it to resume its upmove towards 1.19 by the end of this month and thereby test resistance on the weekly line charts.

Dollar-Yen (112.25) has dropped further as expected and might touch 112 by next week. A further decline towards 110 near support on weekly candles could happen by Jan if the US-Japan yield spread (2.313) finally drops towards 2.28 after having hovered near resistance (2.35-2.36) for couple of months.

Pound (1.3433) has been trading at similar levels as yesterday (near 1.342-1.345) and as mentioned yesterday, we might have to wait for a couple of sessions for more directional clarity (ie whether it will move back down on its downtrend towards support at 1.32-1.3225 on the daily, 3 day and weekly charts, or whether it will test resistance near 1.355-1.3575 on the weekly candles before dipping again.)

We were expecting Rupee (64.345) to drop to 64.15-64.20 in case Euro gained strength after the ECB meet. Inspite of Euro weakness after the meet, Rupee opened lower at 64.165. However, we could see markets factor in the Euro behavior and Dollar Rupee to rise back towards 64.30-64.40 today.

INTEREST RATES

The US yields have come down to test support levels and is likely to bounce back in the next few sessions. View is bullish for the early trades next week.

The US-Japan 10Yr (2.31%) is falling as expected. A further fall towards 2.28% or lower could bring down Dollar Yen also to lower levels.

The German-US 10YR (-2.04%) is stable at levels seen yesterday. The yield spread could test immediate resistance and could come off towards -2.08% or lower in the near term, indicating a fall in Euro too.

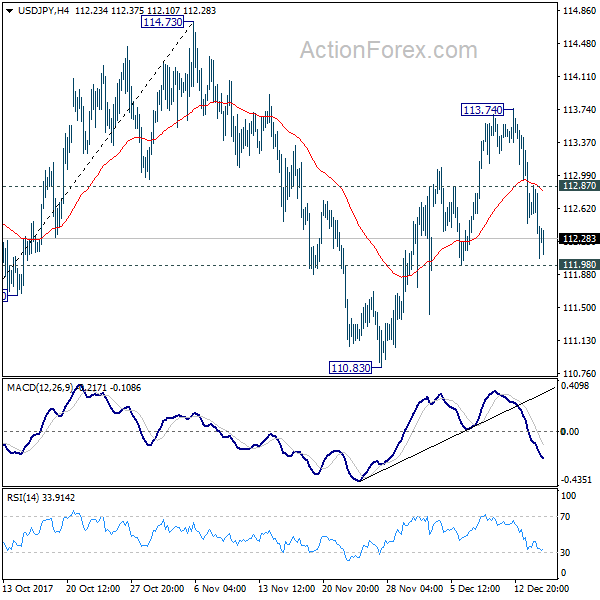

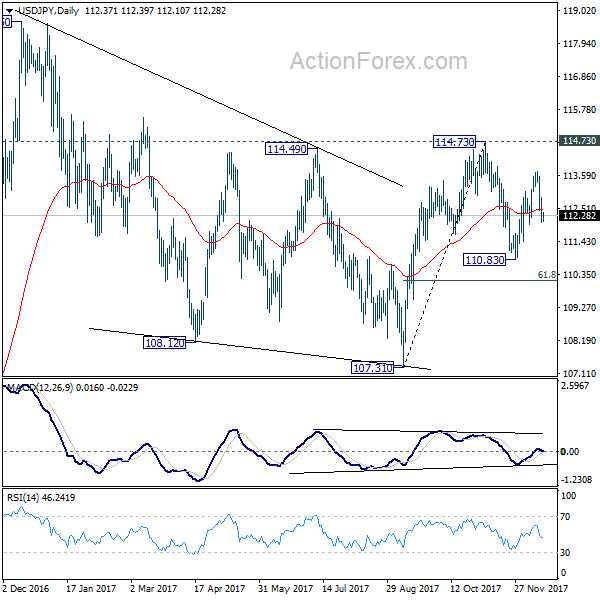

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.01; (P) 112.45; (R1) 112.83; More....

At this point, the fall from 113.74 is still seen as a correction. As long as 111.98 support holds, further rally is expected in USD/JPY. Above 112.87 minor resistance will turn bias to the upside for 113.74. Break will target 114.73 key resistance. However, break of 111.98 support will extend the decline from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

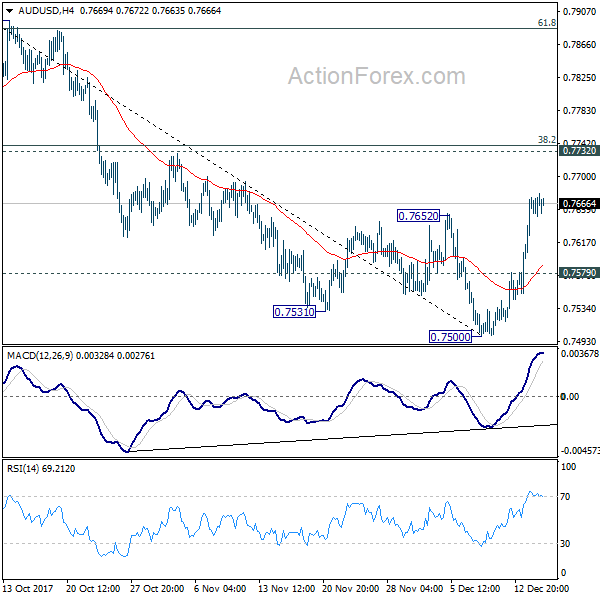

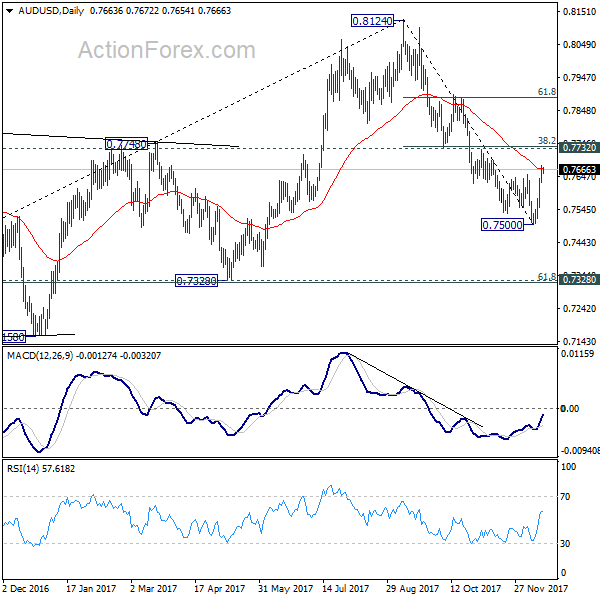

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7634; (P) 0.7656; (R1) 0.7687; More...

Intraday bias in AUD/USD remains mildly on the upside as rise from 0.7500 short term bottom is still in progress. Further rally could be seen. For now, we'd expect strong resistance from 0.7732 cluster resistance (38.2% retracement of 0.8124 to 0.7500 at 0.77385) to limit upside to bring fall resumption. Below 0.7579 minor support will turn bias to the downside for 0.7500 and below. However, sustained break of 0.7732 should invalidate our bearish view and bring stronger rise through 61.8% retracement at 0.7886.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8029). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7732 near term resistance holds.

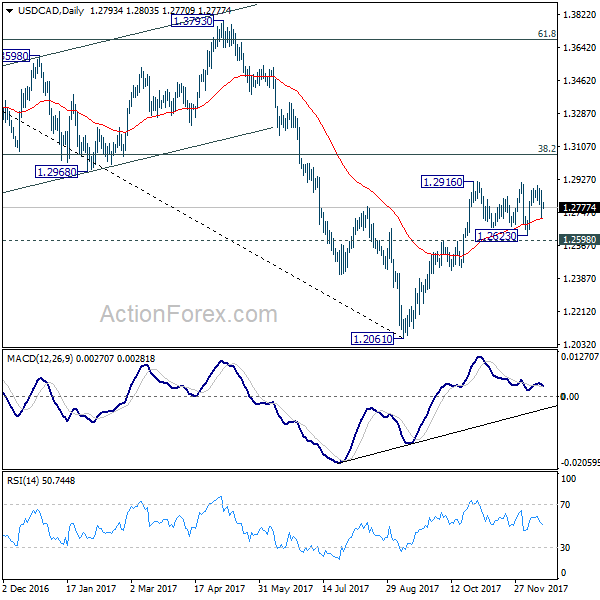

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2717; (P) 1.2791; (R1) 1.2869; More....

USD/CAD dropped sharply from 1.2891, but still it's staying in range below 1.2916. Consolidation from there is in progress and intraday bias remains neutral. Also, outlook remains bullish with 1.2598 resistance turned support intact. On the upside, firm break of 1.2916 will resume whole rally from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2888). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Dollar Back Under Pressure after Short Lived Recovery, Canadian Dollar Lifted by Upbeat BoC Poloz

Dollar's data inspired rally overnight was brief and weak. The greenback is still set to end as the weakest major currency for the week despite a Fed rate hike. It seems like markets are rather worried on passage of the reconciled tax bill in the Senate. Euro is indeed trading as the second weakest one for the week. Even though ECB raised both growth and inflation forecasts, it's still not going to meet 2% inflation target before 2020. Commodity currencies are trading broadly higher for the week. Canadian Dollar was given a boost by BoC Governor Stephen Poloz's upbeat comment. But it's overwhelmed by Aussie and Kiwi.

More on this week's central bank activities:

- ECB Review: Christmas Mood Leaves QE Exit Decisions for 2018

- BOE Stands on Sideline after November Hike, Attributing Inflation Overshoot to Weak Currency

- SNB Raised CPI Forecasts, Acknowledged Franc's Weakness But Pledged To Stay Cautious

- Bank of Canada Steals the Show Despite Not Making Rate Decision

- BoC: Poloz Worries, But Feels We're Still "Close to Home"

- Fed Raises Rates, Maintains Normalization Path

- FOMC Hikes Rate For Third Time, With Two Dissents

- The FOMC Takes Another Step Toward Normal

- Fed Delivers December Hike, With More Tightening in Store Next Year

- FOMC Review: Broadly Unchanged Fed Signal

- Federal Reserve Hikes Rates in December

Japan large manufacturing confidence hit 11 year high

Japan Tankan survey showed improvements in large manufacturing business confidence in Q4. The results support BoJ's upbeat assessment on the economy. And they will likely add to the central bank's confidence that inflation will eventually return to 2% target as economy improves. However, considering the slowdown in capex growth and slower improvement in other readings, there is still a long way to go for the BoJ. Large manufacturing index rose 3 pts to 25 in Q4, beating expectation of 24. That's also the highest level in 11 years since Q4 of 2006. Large manufacturing outlook was unchanged at 19, below expectation of 22. Large non0manufacturing index was unchanged at 23, below expectation of 24. Large non-manufacturing outlook rose to 20, but missed expectation of 21. All industry capex spending rose 7.4%, slowed from 7.7% and missed expectation of 7.5%.

BoC Poloz raised expectations of Q1 hike

Canadian Dollar was given a strong lift overnight by upbeat comments from BoC Governor Stephen Poloz. Poloz said that the economy made "tremendous" progress in 2017. And, It's now "close to reaching its full potential". He also said that policymakers are "growing increasingly confidence that the economy will need less monetary stimulus over time". Markets took that as confirmation that the next move is still a hike. More importantly, it wouldn't be too far away. His comments affirmed the expectation of another rate hike by BoC in Q1 next year.

UK PM May in Brussels EU summit

UK Prime Minster Theresa May arrived in Brussels yesterday for the highly anticipated EU summit. Brexit negotiation is widely expected to be given a go-ahead into trade talks. However, it's believe that the formal discussions on post Brexit trade relationship will not start until March. Also, according to a leaked European Council document, there will be "additional guidelines" for the negotiations onward, in particular regarding the "framework for the future relationship". Meanwhile, UK Parliament voted 309 to 305 on an amendment to the Brexit bill. And the Parliament must be given on vote on the final agreement with EU before withdrawal begins. That is seen as further weakening May's position.

Looking ahead

The economic calendar is much lighter today. Eurozone will release trade balance. Canada will release manufacturing sales. US Empire state manufacturing and industrial production will also be featured.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2717; (P) 1.2791; (R1) 1.2869; More....

USD/CAD dropped sharply from 1.2891, but still it's staying in range below 1.2916. Consolidation from there is in progress and intraday bias remains neutral. Also, outlook remains bullish with 1.2598 resistance turned support intact. On the upside, firm break of 1.2916 will resume whole rally from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2888). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Nov | 57.7 | 57.2 | 57.3 | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 25 | 24 | 22 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q4 | 19 | 22 | 19 | |

| 23:50 | JPY | Tankan Large Non-Manufacturing Index Q4 | 23 | 24 | 23 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q4 | 20 | 21 | 19 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 7.40% | 7.50% | 7.70% | |

| 23:50 | JPY | Tankan Small Manufacturing Index Q4 | 15 | 11 | 10 | |

| 23:50 | JPY | Tankan Small Manufacturing Outlook Q4 | 11 | 9 | 8 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Index Q4 | 9 | 9 | 8 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Outlook Q4 | 5 | 5 | 4 | |

| 10:00 | EUR | Eurozone Trade Balance Oct | 24.6B | 25.0B | ||

| 13:30 | CAD | Manufacturing Sales M/M Oct | 0.50% | |||

| 13:30 | USD | Empire State Manufacturing Index Dec | 18 | 19.4 | ||

| 14:15 | USD | Industrial Production M/M Nov | 0.30% | 0.90% | ||

| 14:15 | USD | Capacity Utilization Nov | 77.20% | 77.00% | ||

| 21:00 | USD | Net Long-term TIC Flows Oct | 80.9B |

ECB Review: Christmas Mood Leaves QE Exit Decisions for 2018

- Despite a stronger growth and inflation outlook, the ECB delivered a fairly balanced policy message, without further hints about a shift towards a more 'holistic' view on inflation and the economy. We expect discussions about QE exit and policy normalisation to gain prominence in the spring of 2018.

- ECB sees euro zone heading in 'the right direction' – we see EUR/USD headed firmly into 1.20s in 2018.

In line with our expectation, the ECB left its policy measures and forward guidance unchanged, keeping the QE programme open-ended. The ECB reiterated that policy rates would remain at current levels for an extended period and well past the horizon of asset purchases. The Q&A also brought little news as Draghi confirmed that both the new QE composition and a possible decoupling of the QE forward guidance from the inflation outlook were not discussed at the meeting.

Although Draghi stressed that the Governing Council is growing more confident in its ability to meet the inflation target eventually, not least because of the stronger growth outlook, today's meeting confirmed that the ECB is in a wait-and-see mode for now and any further discussions about QE exit and policy normalisation would probably only gain prominence in the spring of 2018. Related to this, we think it is important to watch out for growing support within the Governing Council for the idea of decoupling the forward guidance on QE from the requirement for a sustained rise in inflation and instead linking it to the overall monetary policy stance, as this would enable the ECB to end QE even if inflation continues to undershoot the target. Such a change in the forward guidance might come for example in the April or June meetings next year.

We still believe the ECB will end the QE programme in 2018 and taper purchases to zero in Q4 18, due to a combination of binding technical restrictions, the growing size and importance of QE reinvestments, fading deflationary risks with core inflation staying above 1.0% and a growing consensus within the Governing Council that the October QE extension was the last one. Given gradually rising underlying inflation pressures, we expect the ECB to deliver its first 10bp deposit rate hike in Q2 19, supported by a growing urge in the Governing Council to move ahead with monetary policy normalisation in order to regain room to manoeuvre for future crises and avoid falling behind the curve.

ECB projects core inflation at 1.8% in 2020

The ECB also released new economic forecasts at the meeting, which, as expected, painted a rosier picture for the eurozone growth and inflation outlook.

- The 'significant improvement in the growth outlook' gives the ECB greater confidence that inflation will converge to its aim. The GDP growth forecast for 2018 was lifted to 2.3% from 1.8%, reflecting the strong cyclical momentum, and which is even above our forecast of 2.0%. The projection for 2019 was also raised, by 0.2pp to 1.9%, while the ECB sees growth moderating to 1.7% in 2020. Risks to the growth outlook were judged to be broadly balanced.

- The inflation outlook was revised up, mainly reflecting higher oil and food prices, as we anticipated in Euro Area Research: ECB inflation gap persists in 2019. It was still judged that an ample degree of monetary accommodation was needed for underlying inflation pressures to continue to build up and Draghi stressed that the inflation outlook remains (too) dependent on the accommodative monetary policy stance. The ECB kept its 2017 and 2019 HICP inflation forecasts unchanged, but raised the 2018 forecast by 0.2pp to 1.4%. Interestingly, at the same time, the ECB lowered its core inflation forecast for 2018 by 0.2pp to 1.1%, which is now in line with our forecast. The new 2020 forecast projects core inflation close to the target at 1.8%, in line with the ECB's belief in increasing underlying inflation pressures in light of the continued strong economic momentum and an expected strong pick-up in wage growth to 2.7% in 2020.

FX: ECB sees euro zone headed in 'the right direction' – we see EUR/USD headed firmly into 1.20s

A fairly muted reaction in EUR/USD to the 'October replay message' from the ECB insofar as its stance on QE and forward guidance on rates were concerned. First, the sense Draghi tried to convey in terms of upward economic revisions, namely that things are moving in the right direction in the euro zone, helped to send EUR/USD higher at the start of the press conference. However, the fact that decoupling the inflation outlook from the QE decision had not been discussed helped to send the cross lower again (even as the inflation forecasts were lifted). We also note that the strong US retail sales figures, which came out this afternoon, and the ongoing tightening in USD liquidity (as evident in a stillwider basis) likely helped to send the cross back down again.

While there were no clear hints from Draghi today that the 'holistic' approach to the economic outlook and to the overall policy stance is gaining further traction yet, this is something for the FX market to watch out for when the minutes are published in a few weeks' time. Notably, Draghi did remind us of what we have dubbed the 'Sintra accord', i.e. the (seemingly coordinated) move by a range of central bankers back in late June to urge for policy 'normalisation' on the grounds that deflationary risks had evaporated. This suggests to us that the FX market should be able to keep the faith that the next level of ECB 'normalisation' is just around the corner. We think this will be a key theme in Q2 next year.

As we have stressed repeatedly - and notably in our recent Special Report - we see risks in EUR/USD tilted to the upside for 2018 as a whole. While relative rates could possibly weigh a bit in the near term, what the FX market would increasingly be focused on is the potential not least for debt flows to support the single currency in the ECB's 'exit' process that is only just getting started. We are long EUR/USD on a 12M horizon via options in our FX Top Trades 2018.

The Great Central Bank Yawn

Neither the ECB or the BOE offered up much of anything at yesterday's Central Bank events.

Not wanting to impede the nascent EU economic recovery via a stronger Euro, the ECB forward guidance remained dovish.

The BoE decision was equally dull as the central bank voted unanimously to keep rates in check while towing the usual G-4 Central Bank mantra to remain cautious.

The predictably cautious nature of the global central banks continues to drain volatility from currency markets. So get ready for more of the same old same old in early 2018 "that economic growth remains robust yet inflation remains dovish."

US shoppers are embracing the holiday season as retail sales surged. While it portends well for near-term consumption metrics, it does little to support the dollar as the shopping frenzy will likely cool in January.

Frankly, there are few if any conclusions to be made from overnight markets, so I suspect local traders are prepared to slide into the weekend on a quiet note.

Equities

With no news on Tax reform US stock markets were happy to take profits and trim positions ahead of the weekend which created an afternoon slide on the broader indices.

Oil

Oil prices are trading off overnight session lows as the Forties pipeline supply disruption, and a Texas refinery fire is helping to support gasoline prices, attracting some bottom feeders on WTI. It's been a long week for Oil Patch traders who will be looking to wind down for the weekend, so unless any surprises, trading should remain subdued.

Malaysian Ringgit

There were few if any fireworks from the global central banks who are more than content erring on the side of caution and steering a dovish tack. G-10 central bank dovishness bodes well for Asian currencies in the medium term and more so for the Malaysian Ringgit as BNM is expected tweak interest rates higher in January in response to surging economic growth and to thwart inflationary expectations.

My outlook for next week is for trading to remain subdued within the 4.0650-4.10 levels with US dollar rallies quickly faded. However, given that we are entering holiday season liquidity conditions so absent any surprises, we'll likely trade on a lighter note

The Japanese Yen

USDJPY has taken a bit of a beating after the FOMC's dovish rate hike put the final nail in the coffin on the long USDJPY trade into year end. Going forward, the weakness in the USD could pick up some speed into year end, but unless an unexpected downslide catalyst hits, traders are more apt to sit tight waiting to fade tax headline rallies than chase the dollar lower.