Sample Category Title

CAC Lower as ECB Maintains Rates at 0.00%

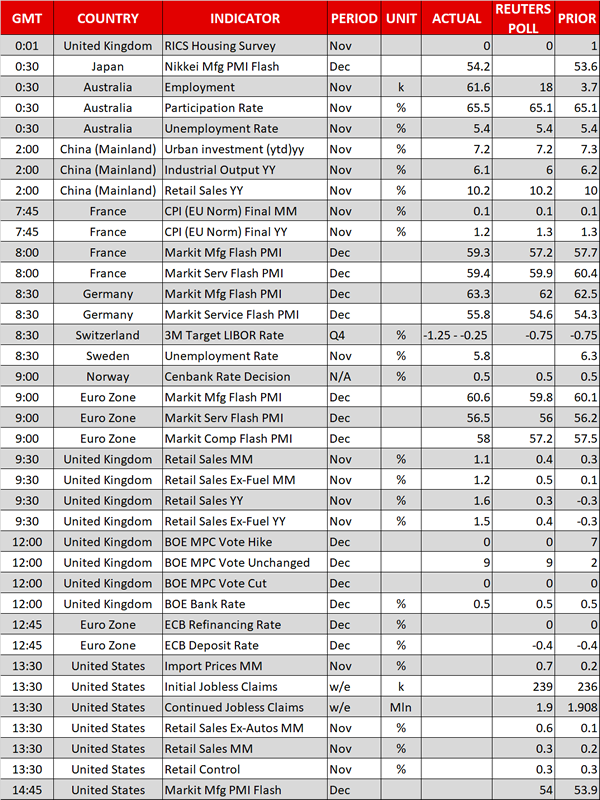

The CAC index has posted losses in the Thursday session. Currently, the index is at 5380.80, down 0.35% on the day. In France, Final CPI remained unchanged at 0.1%, matching the forecast. Manufacturing PMI accelerated for a seventh straight month, improving to 59.3 points. This easily beat the forecast of 57.2 points. The news was not as good from the services sector, as Services PMI dipped to 59.4, shy of the estimate of 59.8 points. Still, this is in indicative of strong expansion.

Thursday's French indicators are reflective of current economic conditions. The manufacturing and services sectors continue to point to expansion, with readings well above the 50-point level. However, inflation remains a sore point in France, reflective of low inflation levels across the eurozone. In the second half of 2017, French CPI has not cracked above 0.1%, with the exception of the August release. Still, the year is ending on an optimistic note in the eurozone's second largest economy. Growth has been steady, unemployment is lower, and investor and business confidence has been boosted by the election of pro-business Emmanuel Macron as president.

As expected, the Federal Reserve raised the benchmark interest rate on Wednesday, to a range between 1.25% and 1.50%. This marked the third rate hike in 2017, and is reflective of a strong performance of the US economy. The Fed statement was optimistic about the economy, noting that the labor market "remained strong". It also lowered its unemployment forecast in 2018 from 4.1% to 3.9%, and revised growth for 2018 from 2.1% to 2.5%. Despite this rosy prognosis, the US dollar was broadly down after the announcement. Why? One reason is the sore point in the economy – inflation. The Fed has not changed its September forecast for rate hikes next year, with the Fed dot plot indicating that three rate hikes are projected for 2018. This disappointed some investors who would like to see four increases next year. As well, the rate statement said that the Fed did not expect the tax reform legislation to have any long-term effect on the economy, contradicting White House claims that the legislation would trigger substantial economic growth.

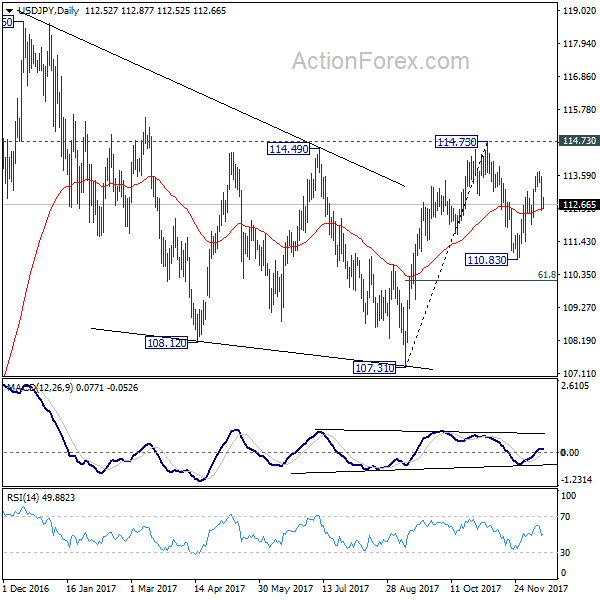

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.13; (P) 112.85; (R1) 113.25; More...

Intraday bias in USD/JPY remains neutral at this point. Decline from 113.74 is still seen as a correction. As noted before, as long as 111.98 support holds, further rally is expected in the pair. On the upside, above 113.68 will extend the rise from 110.83 to 114.73 resistance first. Decisive break there will resume whole rise from 107.31. More importantly, that will confirm completion of medium term correction from 118.65 at 107.31. In that case, retest of 118.65 should be seen next. However, break of 111.98 support will extend the correction from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

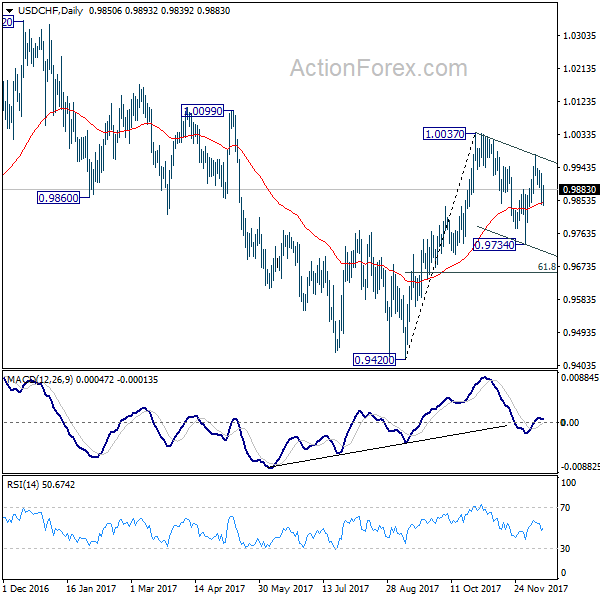

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9821; (P) 0.9874; (R1) 0.9908; More....

As long as 0.9895 minor resistance holds, intraday bias in USD/CHF remains on the downside for deeper fall. Decline from 0.9977 is part of the correction pattern from 1.0037. It could target 0.9734 support and below. But we'd We'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. On the upside, above 0.9895 minor resistance will turn bias back to the upside for 0.9977 instead.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

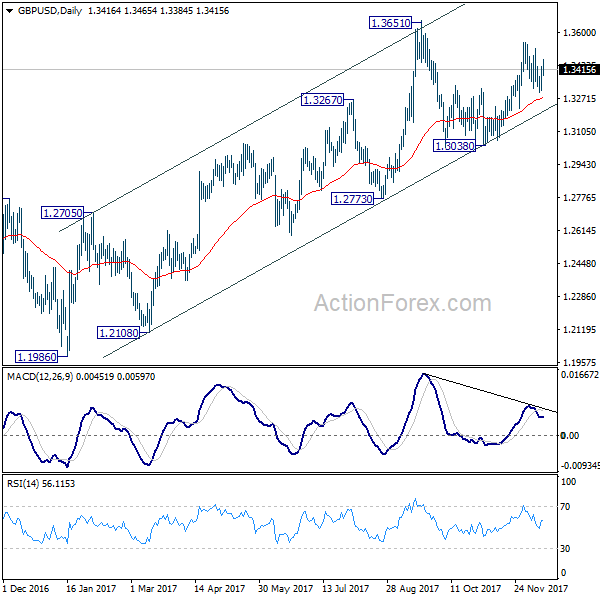

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3342; (P) 1.3384; (R1) 1.3458; More....

GBP/USD is still bounded in the corrective pattern from 1.3549 and intraday bias remains neutral. Another fall cannot be ruled out yet. But after all, as long as 1.3220 support holds, we'd continue to favor another rise. On the upside, break of 1.3549 will target 1.3651 high next. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

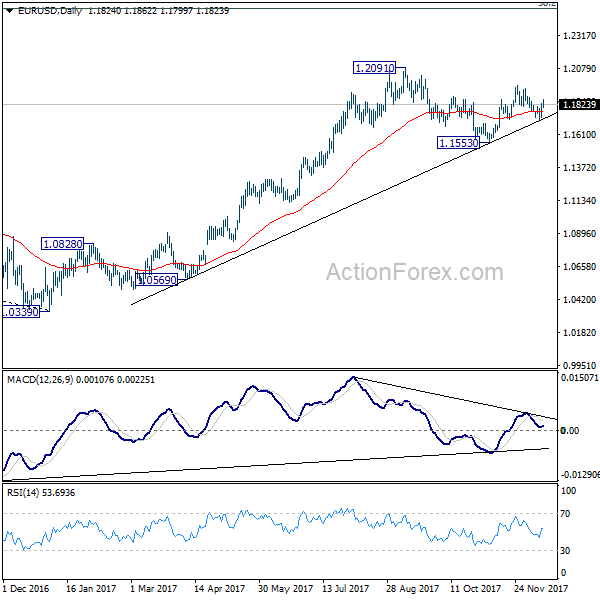

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1759; (P) 1.1795 (R1) 1.1861; More....

Intraday bias in EUR/USD remains on the upside for the moment. Corrective pull back from 1.1960 has completed at 1.1717 already. Also, as the pair defended 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708), near term bullish outlook is retained. Further rise should be seen to 1.1960 first. Break will target 1.2029 high next. And even in case of retreat, outlook will remain bullish as long as 1.1708/12 cluster support holds.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Dollar Borrows Support from Ultra-Low Jobless Claims and Strong Retail Sales, Euro Firm as ECB Upgraded Growth and Inflation...

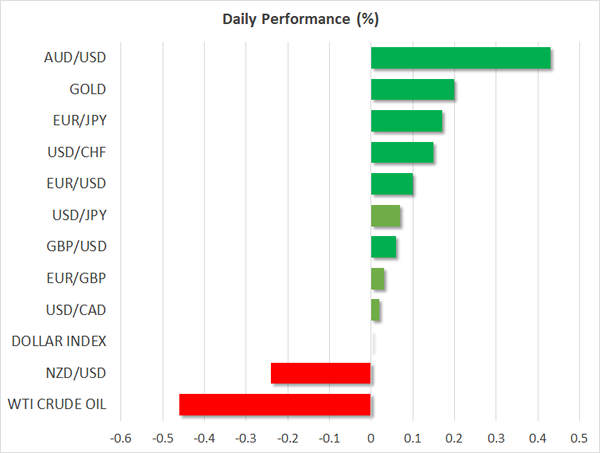

Dollar is trying to regain some ground in early US session after ultra-low jobless claims and strong retail sales. Indeed, at the time of writing, the greenback is trading up against all but Aussie for today. Nonetheless, after yesterday's post CPI and FOMC selloff, Dollar has to do more to convince the markets of its momentum. Meanwhile, Euro is actually trading as the strongest one today, trailing Dollar closely. The common currency is lifted by strong Eurozone PMIs. ECB also raised growth and 2019 inflation forecasts in the latest projections. Elsewhere, BoE and SNB stand pat as widely expected.

US jobless claims at 225k ultralow

US initial jobless claims dropped -11k to 225k in the week ended December 9, well below expectation of 239k. Four week moving average dropped 6.75k to to 234.75k. Continuing claims dropped to 1.89m in the week ended December 1. Headline retail sales rose 0.8% mom in November, well above expectation of 0.3% mom. Ex-auto sales grew 1.0% mom, also beat expectation of 0.7% mom. Import price index rose 0.7% mom in November. Also released in US session, Canada new housing price index rose 0.1% mom in October.

We'd maintain that yesterday's FOMC announcement was not dovish at all. Growth forecasts were revised higher, unemployment forecasts revised lower. Inflation forecasts and fed funds rate projections were unchanged. The only dovish part of the voting with Chicago Fed Evans joining Minneapolis Kashkari in dissenting. That's it. Dollar's selloff was largely due to a combination of factors. That includes Republican's defeat in deep red state of Alabama Senate Election, possibly dissatisfaction on the final corporate tax rate at 21%. But more importantly, the core CPI miss. More in FOMC Hikes Rate For Third Time, With Two Dissents

ECB stands pat, raised 2018 inflation forecast

ECB left the main refinancing rate unchanged at 0% as widely expected. The central bank also maintained the pledge to keep rates low for an extend period and be open to add stimulus if needed. ECB President Mario Draghi emphasized in the press conference that very favorable financial conditions are still needed in Eurozone. Also price pressure remained low and there was no sign of a pick up yet. Nonetheless, strong Eurozone growth momentum and improved growth outlook gave ECB confidence that inflation will climb back to 2% target.

In the updated economic forecasts, ECB project 2017 growth to be at 2.4%, revised up from 2.2%. For 2019, growth is seen at 1.9%, revised from from 1.7%. 2020 growth forecast was left unchanged at 1.7%. Inflation is projected to be at 1.5% in 2017, unchanged. 2018 inflation is estimated to be at 1.4%, notably revised up from 1.2%. 2019 inflation is projected to be at 1.5%, unchanged. 2020 inflation is projected to be at 1.7%. That is, within the projection horizon, ECB is still short of its 2% inflation target.

Solid Eurozone PMIs suggests strong Q4, and firm Q1.

PMIs from Eurozone generally strengthened in December, painting a brighter outlook for early next 2018. Eurozone PMI manufacturing rose to 60.6 in December, up from 60.1 and beat expectation of 59.7. That's also the highest level on record. Eurozone PMI services rose to 56.5, up from 56.2 and beat expectation of 56.0. Germany PMI manufacturing rose to 63.3, up from 62.5, above expectation of 62.0. Germany PMI services rose to 55.8, up from 54.3, above expectation of 54.6. France PMI manufacturing rose to 59.3, up from 57.7, above expectation of 57.2. France PMI services, however, dropped to 59.4, down from 60.4, missing expectation of 59.4.

Markit chief business economist Chris Williamson noted that "the eurozone economy is picking up further momentum as the year comes to a close, ending its best quarter since the start of 2011. The PMI is signalling an impressive 0.8% GDP increase in the fourth quarter, with accelerating growth seen in both Germany and France, where fourth quarter growth rates of 1.0% and 0.7-0.8% are indicated respectively."

Also, he added that "The eurozone upturn is being led by a booming manufacturing sector, with a record PMI seen in December, but stronger domestic demand is also helping drive faster service sector growth. Demand in the region's home markets is being buoyed by the improved labour market, with new jobs being created at a pace not seen for 17 years over the past two months."

BoE blames inflation overshoot on exchange rate

The BOE voted unanimously to leave the Bank rate unchanged at 0.5% today, following a historic rate hike in the prior month. Policymakers also decided to leave the asset purchase program unchanged at 435B pound. Overshooting of inflation remains a key concern with the central bank putting its blame on British pound's weakness. Policymakers noted that recent macroeconomic data have been "mixed" and raised the concern that GDP growth might slow in 4Q17. The central bank also acknowledged the progress of Brexit negotiations, suggesting that it has helped support the pound. We expect the BOE would keep its powder dry at least for the first half of next year, unless abrupt changes in the growth and inflation developments. More in BOE Stands on Sideline after November Hike, Attributing Inflation Overshoot to Weak Currency

SNB turned upbeat after standing pat

While leaving the policy rates unchanged for another month and pledged to continue FX market intervention when needed, the SNB has turned less dovish in today's announcement. It has turned more upbeat over the economic recovery outlook and acknowledged the depreciation of Swiss franc and the euro and US dollar. the central bank revised modestly higher the inflation forecasts for this year and 2018, while leaving that for 2019 unchanged. More in SNB Raised CPI Forecasts, Acknowledged Franc's Weakness But Pledged To Stay Cautious

Also from Swiss, PPI rose 0.6% mom, 1.8% yoy in November.

Aussie surges on stunning job data

Australian Dollar remains the strongest one for today as supported by strong job data. The employment market grew 61.6k in November, more than triple of expectation of 19.2k. Full time jobs grew 41.9k while part time jobs grew 19.7k. Unemployment rate was unchanged at 5.4% as participation rate jumped from 65.2% to 65.5%. Nonetheless, there is no change in the general view that RBA will stand pat throughout 2018, unless there is a pickup in wage growth. Also from Australia consumer inflation expectation rose 3.7% in December.

Release from China, retail sales rose 10.2% yoy in November, below expectation of 10.3% yoy. Fixed assets investments rose 7.2% yoy, in line with consensus, industrial production rose 6.1% yoy, below expectation of 6.2% yoy. From Japan, industrial production was finalized at 0.50% mom in October.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1759; (P) 1.1795 (R1) 1.1861; More....

Intraday bias in EUR/USD remains on the upside for the moment. Corrective pull back from 1.1960 has completed at 1.1717 already. Also, as the pair defended 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708), near term bullish outlook is retained. Further rise should be seen to 1.1960 first. Break will target 1.2029 high next. And even in case of retreat, outlook will remain bullish as long as 1.1708/12 cluster support holds.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectation Dec | 3.70% | 3.70% | ||

| 00:01 | GBP | RICS House Price Balance Nov | 0% | 0% | 1% | |

| 00:30 | AUD | Employment Change Nov | 61.6K | 19.2K | 3.7K | 7.8K |

| 00:30 | AUD | Unemployment Rate Nov | 5.40% | 5.40% | 5.40% | |

| 02:00 | CNY | Retail Sales Y/Y Nov | 10.20% | 10.30% | 10.00% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Nov | 7.20% | 7.20% | 7.30% | |

| 02:00 | CNY | Industrial Production Y/Y Nov | 6.10% | 6.20% | 6.20% | |

| 04:30 | JPY | Industrial Production M/M Oct F | 0.50% | 0.50% | 0.50% | |

| 08:00 | EUR | France Manufacturing PMI Dec P | 59.3 | 57.2 | 57.7 | |

| 08:00 | EUR | France Services PMI Dec P | 59.4 | 59.9 | 60.4 | |

| 08:15 | CHF | Producer & Import Prices M/M Nov | 0.60% | 0.30% | 0.50% | |

| 08:15 | CHF | Producer & Import Prices Y/Y Nov | 1.80% | 1.20% | ||

| 08:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | -0.75% | |

| 08:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | -0.25% | |

| 08:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | -1.25% | |

| 08:30 | EUR | Germany Manufacturing PMI Dec P | 63.3 | 62 | 62.5 | |

| 08:30 | EUR | Germany Services PMI Dec P | 55.8 | 54.6 | 54.3 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | 60.6 | 59.7 | 60.1 | |

| 09:00 | EUR | Eurozone Services PMI Dec P | 56.5 | 56 | 56.2 | |

| 09:30 | GBP | Retail Sales M/M Nov | 1.10% | 0.40% | 0.30% | |

| 12:00 | GBP | BoE Bank Rate | 0.50% | 0.50% | 0.50% | |

| 12:00 | GBP | BOE Asset Purchase Target Dec | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--0--9 | 0--0--9 | 7--0--2 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | 0--0--9 | |

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | CAD | New Housing Price Index M/M Oct | 0.10% | 0.20% | 0.20% | |

| 13:30 | USD | Initial Jobless Claims (DEC 09) | 225K | 239K | 236K | |

| 13:30 | USD | Retail Sales Advance M/M Nov | 0.80% | 0.30% | 0.20% | 0.50% |

| 13:30 | USD | Retail Sales Ex Auto M/M Nov | 1.00% | 0.70% | 0.10% | 0.40% |

| 13:30 | USD | Import Price Index M/M Nov | 0.70% | 0.80% | 0.20% | |

| 14:45 | USD | US Manufacturing PMI Dec P | 54.2 | 53.9 | ||

| 14:45 | USD | US Services PMI Dec P | 54.6 | 54.5 | ||

| 15:00 | USD | Business Inventories Oct | -0.10% | 0.00% | ||

| 15:30 | USD | Natural Gas Storage | 2B |

BoE Keeps Rates Unchanged, Draghi in Focus

Sterling offered a fairly muted response during Thursday's trading session after Bank of England policy makers unanimously voted to leave interest rates unchanged at 0.5% in December.

Although inflation in the United Kingdom has jumped to its highest level in almost six years, it seems that the growing uncertainty over Brexit is likely to encourage the central bank to adopt a wait and see approach moving forward. While the Monetary Policy Committee maintained the view that "further modest increases" in the key rate may be needed in the coming years, Sterling's muted price action suggests this has fallen on deaf ears.

The GBPUSD appreciated during Thursday's trading session on the back of a vulnerable US Dollar. With political risk in the United Kingdom and Brexit uncertainty still weighing on the Pound, the current upside may be limited. Technical traders will continue to observe how prices react below the 1.3520 region. Weakness under 1.3380 could encourage a decline back towards 1.3300.

ECB's Mario Draghi enters the scene

The Euro edged higher on Thursday after the European Central Bank kept rates on hold in December.

With the central bank halving its monthly asset purchases back in October to €30 billion from €60 billion, it was widely expected that monetary policy would remain unchanged today. Much attention will be directed towards Mario Draghi's press conference which could heavily impact the Euro. Although Europe's steadily improving macro fundamentals could continue stimulating buying sentiment towards the Euro, a cautious sounding Draghi today, has the ability to punish the currency.

Dollar dips on dovish hike

It is interesting how the Dollar sharply depreciated against a basket of major currencies during late trading on Wednesday, despite the Federal Reserve raising US interest rates by 25 basis points.

Although the central bank expressed optimism over the US economy by projecting GDP to grow 2.5% in 2018 from the 2.1% forecast in September, this simply failed to offer any support to the Dollar. With policymakers expressing concerns over stubbornly low levels of inflation, investors are likely to deeply ponder how this could impact the central bank's ability to raise US interest rates three times in 2018.

Taking a look at the technical picture, the Dollar Index was under extreme selling pressure on the daily charts following December's dovish rate hike. Sustained weakness below 93.50 may encourage a further decline lower towards 93.20 and 90.00, respectively.

Commodity spotlight - Gold

Gold sprinted to a weekly high above $1258 during Thursday's trading session on the back of a vulnerable US Dollar.

Although the Federal Reserve raised US interest rates on Wednesday as widely expected, concerns over low inflation in the US stole the show ultimately punishing the Greenback. With markets questioning the central bank's ability to raise rates three times next year amid inflation fears, Gold which is zero-yielding may receive further support.

From a technical standpoint, the yellow metal still remains somewhat pressured on the daily charts despite Wednesday's impressive resurgence. A technical bounce is in the process with the next level of interest at $1267. Alternatively, a failure of prices to keep above $1250 may trigger a decline back towards $1230.

Is Bitcoin gearing up for another record?

This has been one of those rare trading weeks where Bitcoin bulls have taken the back seat with the cryptocurrency currently ranging below the $17000 region as of writing.

With the market chatter over Bitcoin intensifying by the day and investors still rushing from all directions to acquire a piece of the crypto pie, bulls have much ammunition to attack again next week. Technical traders will continue to closely observe how prices behave with the current range with a weekly close above $17000 opening the gates to further upside.

2017 has been an incredibly bullish and phenomenal trading year for Bitcoin which has appreciated roughly 1500% YTD which is mouth-watering to any investor. $20000 is already in sight and it will be interesting to see if Bitcoin is able to maintain the upside momentum next year.

BOE Stands on Sideline after November Hike, Attributing Inflation Overshoot to Weak Currency

The BOE voted unanimously to leave the Bank rate unchanged at 0.5% in December, following a historic rate hike in the prior month. Policymakers also decided to leave the asset purchase program unchanged at 435B pound. Overshooting of inflation remains a key concern with the central bank putting its blame on British pound's weakness. Policymakers noted that recent macroeconomic data have been "mixed" and raised the concern that GDP growth might slow in 4Q17. The central bank also acknowledged the progress of Brexit negotiations, suggesting that it has helped support the pound. We expect the BOE would keep its powder dry at least for the first half of next year, unless abrupt changes in the growth and inflation developments.

Weak Sterling Pushes Inflation Higher:

UK's inflation continues to surprise to the upside in November. Headline CPI rose to +3.1% y/y in November, compared expectations of and October's +3%. Core CPI steadied at +2.7%. Policymakers attributed the overshooting of inflation above the +2% target to the weak sterling. As noted in the statement, "it remains the case that inflation has been pushed above the target by the boost to import prices that resulted from the past depreciation of sterling". In the medium term, policymakers believed that inflation would "decline towards the 2% target", as it is approaching the peak now.

Policymakers noted that "the recent news in the macroeconomic data has been mixed and relatively limited". While global growth has remained strong, the economy at home might be easing. The central bank noted that GDP growth in the fourth quarter might be slightly softer than the third quarter. They, however, indicated that "the measures announced in the Autumn Budget will lessen the drag on aggregate demand stemming from fiscal consolidation, relative to previous plans".

Brexit Progress

BOE also acknowledged the progress of the Brexit negotiations, suggesting the latest developments have reduced the chance of a "disorderly exit". They are also likely "to support household and corporate confidence". What the BOE did not mention was the defeat of Theresa May's government in the House of Commons as MPs supported an amendment to her Brexit bill with a 309-305 vote, curbing the powers of the government in the bill. On the EU side, the European Parliament has voted 556-62 to determine that "sufficient progress" has been made on the first phase of Brexit talks and to support a move to the next phase.

Pound Slips After BOE Meeting, Stocks Weaker, ECB Rate Decision Ahead

Here are the latest developments in global markets:

FOREX: The pound hit a one-month high at $1.3463 in the wake of better than expected retail sales in November. However, it soon slipped back to 1.3420 after the BOE held rates steady but signaled that GDP growth in Q4 “might be slightly softer than in Q3”. The euro rebounded to $1.1830 finding support from upbeat preliminary manufacturing PMI readings for the month of December, while versus the pound it inched up to 0.8812. The dollar continued ranging near yesterday’s lows against its major peers, while it reached intra-day highs versus the swissie at 0.9892 (+0.23%) after the SNB maintained its loose monetary policy to mitigate risks arising from an appreciated currency. The aussie consolidated gains from upbeat employment data above 0.76 key level (+0.37%) and the kiwi stretched lower to (-0.34%).

STOCKS: European stocks were in the red with tech shares being the worst performers, while bank stocks also retreated after yesterday’s not-so-hawkish comments by the Fed Chair. The benchmark STOXX 600 was down by 0.35% at 1100 GMT, the German DAX 30 fell by 0.40% and the French CAC 40 declined by 0.47%. The British FTSE 100 slipped by 0.25%.

COMMODITIES: Oil prices tumbled after the International Energy Agency raised its US output growth forecasts for 2018, fueling concerns from rising US supply. WTI crude declined by 0.25% to $56.40 per barrel and Brent fell by 0.43% to $62.17. Gold was flat near one-week highs at $1,255.70 per ounce.

Day ahead: ECB policy decision pending; US data in focus

Looking forward, the European Central Bank is anticipated to keep its main refinancing rate unchanged at 0.0% (1245 GMT) respectively. However, as this is widely expected, the focus will turn on future economic projections. ECB policymakers are expected to revise up growth forecasts and give the initial estimates for 2020. The outlook for inflation however, would be of greater importance to determine the path of future interest rates given that inflation in the Eurozone has stuck below the ECB’s goal.

Moreover, following the rates decision, ECB chief Mario Draghi will hold a press conference at 1330 GMT.

On the data front, US retail sales due at 1330 GMT are forecast to rise moderately by 0.1 percentage points to 0.3% m/m in November. Meanwhile, the US labour department is also expected to report a soft increase in initial jobless claims, with analysts projecting the number of people claiming unemployment benefits to rise by 3,000 to 239,000 in the week ending December 8.

Then at 1445 GMT, IHS Markit will publish its preliminary readings on the US manufacturing and services PMI for the month of December. Both indices are said to show some improvement.

Elsewhere, the Bank of Canada’s chief Stephen Poloz will give a speech at the Canadian Club of Toronto at 1740 GMT. A press conference will follow.

DAX Slips Despite Sharp German Mfg. Report, Investors Await ECB Decision

The DAX index has posted losses in the Thursday session. Currently, the DAX is at 13,057.00, down 0.57% on the day. On the release front, manufacturing indicators continue to climb, as German and Eurozone Manufacturing PMIs improved to 63.3 and 60.6 points, respectively. There was more good news from the services sector, as Germany and Eurozone Services PMI both beat their estimates. Later in the day, the ECB is expected to maintain interest rates at a flat 0.00%.

As expected, the Federal Reserve raised the benchmark interest rate on Wednesday, to a range between 1.25% and 1.50%. This marked the third rate hike in 2017, and is reflective of a strong performance of the US economy. The Fed statement was optimistic about the economy, noting that the labor market 'remained strong'. It also lowered its unemployment forecast in 2018 from 4.1% to 3.9%, and revised growth for 2018 from 2.1% to 2.5%. Despite this rosy prognosis, the dollar was broadly down after the announcement. Why? One reason is the sore point in the economy – inflation. The Fed has not changed its September forecast for rate hikes next year, with the Fed dot plot indicating that three rate hikes are projected for 2018. This disappointed some investors who would like to see four increases next year. As well, the rate statement said that the Fed did not expect the tax reform legislation to have any long-term effect on the economy, contradicting White House claims that the legislation would trigger substantial growth in the economy.

After the Fed raised rates, attention now shifts to the ECB, which will set interest rates later on Thursday. The ECB is widely expected to maintain current rates, so investors will be focusing on the follow-up press conference with ECB President Mario Draghi. If the ECB sends out an optimistic message about the economy, the euro rally could resume. Meanwhile, German indicators continue to sparkle. Manufacturing PMI hit a new record, climbing to 63.3 points. The PMI Composite Output Index, which measures business activity, improved to 58.7, its highest level since 2011. A robust German economy has been the locomotive for the eurozone, which has rebounded in 2017 with stronger growth and lower unemployment.