Sample Category Title

Trade Idea : GBP/USD – Buy at 1.3350

GBP/USD - 1.3433

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.3435

Kijun-Sen level : 1.3429

Ichimoku cloud top : 1.3400

Ichimoku cloud bottom : 1.3376

Original strategy :

Buy at 1.3350, Target: 1.3450, Stop: 1.3315

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3350, Target: 1.3450, Stop: 1.3315

Position : -

Target : -

Stop : -

As cable staged a strong rebound after finding good support at 1.3303 earlier this week, suggest low has been made there and consolidation with mild upside bias is seen for this rebound from 1.3303 to extend gain to 1.3475-80, then 1.3500, however, near term overbought condition would limit upside and price should falter below indicated resistance at 1.3432, bring another decline later.

In view of this, we are looking to buy cable on dips as 1.3345-50 should limit downside. Below 1.3320-25 would defer and suggest the rebound from 1.3303 has ended, bring retest of this level first, break there would extend the fall from 1.3550 top to 1.3280 and later 1.3250 but price should stay well above previous support at 1.3221.

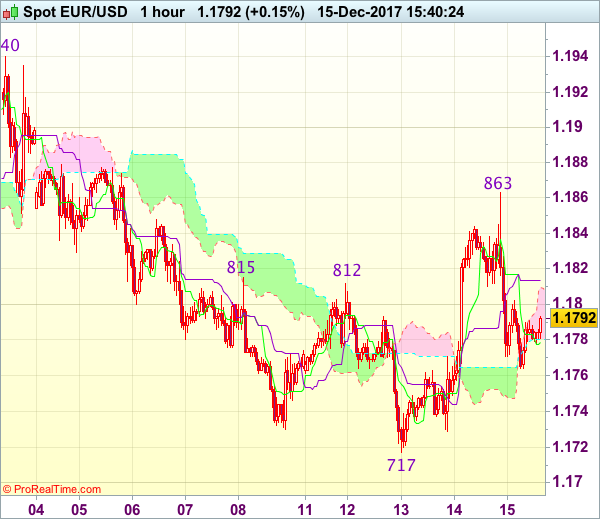

Trade Idea : EUR/USD – Stand aside

EUR/USD - 1.1793

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1781

Kijun-Sen level : 1.1814

Ichimoku cloud top : 1.1810

Ichimoku cloud bottom : 1.1781

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday brief bounce to 1.1863, lack of follow through buying and the subsequent sharp retreat suggest consolidation below this level would be seen and test of 1.1755-60 cannot be ruled out, however, reckon downside would be limited to 1.1730 and price should stay above this week’s low at 1.1717, bring another rebound later.

On the upside, whilst recovery to the Kijun-Sen (now at 1.1814) is likely, reckon upside would be limited to 1.1840 and said resistance at 1.1863 would hold. Only a break above this level would signal the rebound from 1.1717 is still in progress for further subsequent gain to 1.1880, then 1.1900 but price should falter well below resistance at 1.1940, bring retreat later. As near term outlook is mixed, would be prudent to stand aside for now.

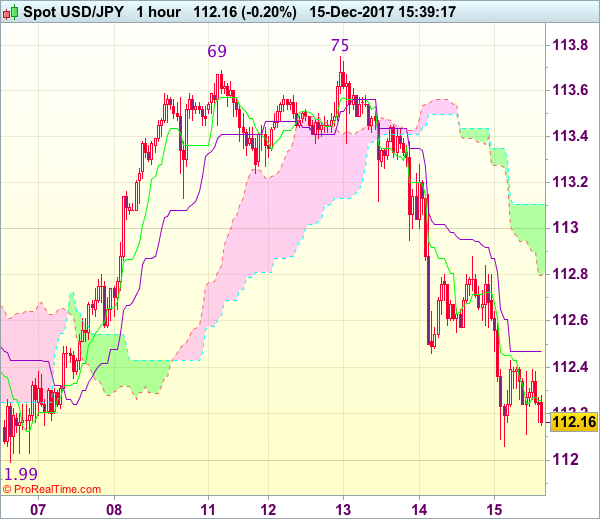

Trade Idea : USD/JPY – Stand aside

USD/JPY - 112.18

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.26

Kijun-Sen level : 112.47

Ichimoku cloud top : 113.11

Ichimoku cloud bottom : 112.80

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has slipped again after brief recovery and price has remained under pressure, suggesting a test of previous support at 111.99 would be seen, however, break there is needed to retain bearishness and signal the rebound from 110.84 low has ended at 113.75, then the fall from there may extend weakness to 111.65-70 but reckon previous support at 111.41 would hold from here.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above the Kijun-Sen (now at 112.47) would bring recovery to 112.85-90 but reckon the upper Kumo (now at 113.11) would limit upside and price should falter below 113.45-50, bring another decline later.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 150.45; (P) 151.12; (R1) 151.63; More...

Intraday bias in GBP/JPY remains neutral. As long as 149.74 support holds, outlook remains bullish in the cross. Break of 153.39 will resume the medium term up trend and target 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32. However, break of 149.74 will dampen our bullish view and turn bias back to the downside for 146.96 key support instead.

In the bigger picture, current development suggests that medium term rise from 122.36 is resuming. Sustained trading above 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 146.96 support will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

Forex: Central Banks Monetary Policy Unchanged

Thursday saw the latest Monetary Policy Committee (MPC) report from the Bank of England. The BoE stated that 'further modest increases' in interest rates are probable, as the Bank tries to bring inflation in line with its 2% target in the coming years. The MPC appeared to be unconcerned with inflation rising to 3.1% last month and voted unanimously at their December meeting to leave interest rates at current levels. The MPC is waiting to see where inflation will be in early 2018, along with the progress of Brexit negotiations, which will form a major part of their February Inflation Report.

The European Central Bank kept its ultra-easy monetary policy unchanged on Thursday, keeping interest rates low for an extended period and pledging to provide additional stimulus if required. At a press conference, ECB President Draghi commented 'The difference in the monetary policy decisions and therefore interest rate decisions (with the US) reflects the different position in the economic recovery, which incidentally is stronger now in Europe. However, it is more advanced in the US. We haven’t seen (any negative effect on the euro zone economy from the divergence in policy).' Going on to say, 'The incoming information, including our staff projections – our new staff projections – indicates a strong pace of economic expansion and a significant improvement in the growth outlook.'

The Swiss National Bank (SNB) kept its current monetary policy in place on Thursday, although the SNB does expect Swiss inflation to exceed its target in 3 years, a possible insight as to when it might end its ultra-loose monetary policy. SNB Chair Jordan stated that they were in 'no rush at all' to start normalizing policy, whilst other central banks have started to hike rates. Jordan commented that the CHF remained 'highly valued', despite the currency losing approximately 7% in value over the last 6 months.

With inflation a somewhat 'hot-topic', the US Commerce Department on Thursday released data showing US retail sales rose more than forecast in November and the previous month was revised higher, indicating a broad strengthening of consumer demand as the holiday shopping season got underway. November retail sales rose 0.8% with a revision of Octobers data up to 0.5% from the previously released 0.2%. In the UK, the Office for National Statistics released Retail Sales data for November that showed sales volumes were up 1.1% in the month, exceeding the 0.4% forecast by the market.

EURUSD is little changed overnight, trading around 1.1783.

USDJPY is unchanged in early session trading at around 112.35.

GBPUSD is trading around 1.3436.

Gold is 0.15% higher in early Friday trading at around $1,255.

WTI is 0.1% higher, trading around $57.20.

Major data releases for today:

At 10:00 GMT: Eurostat will release Trade Balance data for the Eurozone for October.

At 13:15 GMT: Bank of England Chief Economist, Andrew Haldane, is scheduled to speak at the 26th International Rome Money Banking and Finance Conference in Italy.

At 14:15 GMT: The Board of Governors of the Federal Reserve will release US Industrial Production (MoM) for November. Forecasts suggest a release of 0.3%, which is significantly lower than the previous release of 0.9%. The markets could experience USD volatility if the release is dramatically different from forecast.

At 14:15 GMT: US Capacity Utilization for November will be released by the Federal Reserve Board. Forecasts suggest a modest improvement to 77.2% from Octobers’ 77.0%.

At 18:00 GMT: The Baker Hughes US Oil Rig Count will be released. The number of active US Oil Rigs has grown throughout 2017, with the last release showing a count of 751. As more active rigs come online production increases which can dampen crude prices.

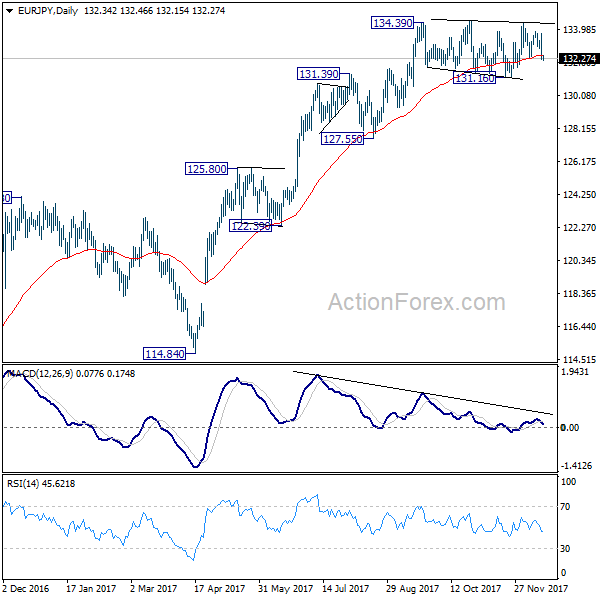

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.81; (P) 132.78; (R1) 133.32; More....

EUR/JPY is still bounded in range of 131.16/134.48 and intraday bias remains neutral. Further rise is expected as long as 131.16 support holds. Decisive break of 134.48 will resume medium term rise from 114.84 and target 141.04 resistance next. However, sustained break of 131.16 support will now indicate near term trend reversal and turn outlook bearish for 127.55 key support.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). Sustained break of 61.8% retracement of 149.76 to 109.03 at 134.20 will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will suggest medium term topping and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

Daily Wave Analysis: EUR/USD Completes Wave 5 And Reverses At Fibonacci Resistance

Currency pair EUR/USD

The EUR/USD respected the resistance zone which was indicated by the wave C (blue) of wave X (purple). Price is now in between support (blue) and resistance (red) trend lines. A bearish break would make the current wave pattern likely and could see price challenge the Fibs of wave 2 (pink).

The EUR/USD completed its 4 and 5th wave (green) yesterday as expected. Price made a reversal and is now challenging a support trend line (blue). An immediate bearish breakout could see price fall lower whereas a bullish bounce could be part of wave B (blue).

Currency pair GBP/USD

The GBP/USD is in a bullish channel (green lines) but price is close to a key resistance trend line (red).

A bullish breakout above resistance (orange/red) could see price move higher towards the Fibonacci targets of waves 5.

Currency pair USD/JPY

The USD/JPY continued lower within wave A (purple). A bullish bounce is probably part of a wave B (purple) correction within a larger wave 2/B (light purple).

The USD/JPYcould be building a wave 5 (blue) of waveA (purple). A break above resistance trend line (red) could start wave B (purple).

EU Backing For May After Loss Of Brexit Vote

Market movers today

Following the 'Central Bank Super Thursday' yesterday, we have a relatively light data calendar today.

Focus remains also on the EU summit in Brussels, where the Brexit discussions are scheduled to take place today. Following Wednesday's defeat about a parliamentary vote on the final Brexit deal, PM Theresa May's posit ion has weakened in t he negotiations.

In the US, industrial product ion for November and Empire manufacturing index for December are due to be released today.

In Russia, we expect the central bank to cut its policy rate to 8.0% from 8.25%.

In Denmark, Finance Denmark's housing market statistics for Q3 are due out .

Selected market news

The ECB left policy measures and forward guidance unchanged, while lifting its growth forecasts. As expected, the ECB reiterated that policy rates would remain at current or lower levels for an extended period and well beyond the horizon of asset purchases. Meanwhile, however, the forecast were lifted, particularly for 2018 (lifted to 2.3% from 1.8% in September). The inflation forecast was also lifted from 1.2% to 1.4% in 2018. Reflecting the stronger out look, Mario Draghi stressed that the ECB is growing more confident in its ability to meet the inflation target eventually. We expect the ECB to taper APP purchases to zero in Q4 18 and deliver the first deposit rate hike in Q2 19. See ECB review - Christmas mood leaves QE exit decisions for 2018, 14 December, for more details.

EU backing for May after loss of Brexit vote . Yesterday, several EU leaders expressed support for the UK Prime Minister after she had lost a vote on Wednesday meaning that the UK parliament will have a vote on the final Brexit deal. However, at the EU summit , there were warnings to UK MPs that the EU would not have the time nor will to renegotiate a Brexit deal.

In terms of economic data, the strong US retail sales took focus yesterday. Sales were up by 0.8% in November, well above expectations for a 0.3% rise. Also, October retail sales were revised higher to 0.5% from 0.2%, while the core retail sales rose 0.8% in November. The dollar index rose 0.1% as a result , while 10Y US Treasury yields were 2bp higher, closing at 2.35%.

Yesterday, Turkey's central bank left its benchmark repo rate unchanged at 8.00% as expected. Yet , the late liquidity rate was raised by 50bp to 12.75%, as inflation has accelerated to a multi-year highest and t he T RY's volatility has surged recently.

Market Update – Asian Session: Asian Equities Generally Track Weakness In US Session

Australia/New Zealand

ASX 200 opened -0.2%; closed -0.2%; REIT index -1%, Financials -0.5% Qantas -1%

(AU) RBA Harper (Dove): Excess capacity in labor market likely bigger than thought; Rates meed to stay supportive of the economy; 5% likely not tipping point for wage growth

(NZ) New Zealand Nov Business Manufacturing PMI: 57.7 v 57.3 prior

(NZ) NZ Fin Min Robertson: Comfortable with general trend of Kiwi (NZ$)

(NZ) New Zealand sells NZ$200M in April 2025 bonds, avg yield 2.5601%, implied bid to cover 3.86x

China/Hong Kong

Hang Seng opened -0.6%, Shanghai Composite -0.2%

Hang Seng Energy Index -1.5%, Property/Construction -1.2%, Financials -1%, Information Technology -0.9%

Property company Sunac China -9% (capital raise)

Li & Fung +5% (announced $1.1B asset sale, special dividend)

(CN) PBoC releases pledged financing business management rules; to accept more kinds of bonds for pledged financing; To accept local government bonds as collateral in certain cases; Says seeks to prevent payment and clearing risks.

(CN) PBoC OMO: CNY150B in 7 and 28-day reverse repos v CNY50B injected in 7 and 28 day reverse repos prior; Net injected CNY150B v CNY190B drain prior (leaves yields unchanged vs prior session)

(CN) PBoC sets yuan reference rate at 6.6113 v 6.6033 prior

(CN) China MOF sells 30-year bonds: Avg yield 4.3555% v 4.35%e, bid to cover 2.09x

(CN) China MOF sells 3-month bills: Avg yield 3.9275%

(HK) Hong Kong may seek to limit the voting power of dual-class shares – HK Press

Korea

Kospi opened +0.8%

Kumho Tire +30% (M&A speculation)

Moody’s raises South Korea Banking System Outlook to Stable from Negative; raises South Korea 2017 GDP growth forecast to 3.0% (2.5% prior), 2018 to 2.8% (2.0% prior)

South Korea Blockchain Association: To improve proof of identity for users of cryptocurrency trading on exchanges; new measures take effect on Jan 1, 2018

Thursday’s late session weakness in the Kospi linked to program trading – Analyst

South Korea Nov Trade Balance: $7.6B v $7.8Be

(KR) US North Korea Envoy Yun: US is open to dialogue with North Korea; has not met with North Korea officials in Thailand

(CN) PBoC Gov Zhou said to meet South Korea Vice Premier in relation to financial cooperation

Japan

Nikkei 225 opened -0.3%; closed: -0.6%

Large financials again track declines in the US: Mitsubishi UFJ -1.4%, Sumitomo Mitsui -0.8%

Rakuten’s planned entry into mobile network operator business continues to weigh on telecoms: Rakuten -5.4%, KDDI -5.5%, Softbank -2.4%

Automakers track US declines: Toyota -1.4%; TOPIX Iron & Steel index -1.4% (US Steel ended -3.4%)

Nikkei heavy component Fast Retailing +1%

Q4 Tankan Large Manufacturer sentiment hits 11-year high; Overall Tankan survey mixed

(JP) JAPAN Q4 TANKAN LARGE ALL INDUSTRY MFG INDEX: 25 V 24E (11-year high); LARGE MFG OUTLOOK 19 V 22E; LARGE ALL INDUSTRY CAPEX 7.4% V 7.5%E

Japan auto union said to again seek ¥3K base wage increase – Japanese press

Japan Auto Manufacturers Group (JAMA): Japan auto industry suffers from labor shortage

(JP) BoJ said to ‘tweak’ message as dissenter calls for more easing – US financial press; The BoJ is due to hold its Dec two-day policy meeting on Dec 20-21st (Wed and Thursday)

Japan Chief Cabinet Sec Suga: To implement additional sanctions on North Korea; To freeze assets of 19 groups

Other Asia

(ID) Indonesia Nov Trade Balance: $130M v $844Me; Imports Y/Y: 19.6% v 13.0%e

North America

US equities ended lower amid comments from Republican Senator Rubio: Dow -0.3%, S&P500 -0.4%, Nasdaq -0.3%, Russell 2000 -1.2%

S&P500 Materials Sector -1.1%, Health Care -1%

Oracle: -6.5% afterhours (guided Q3 earnings below ests)

Costco: +2.3% afterhours (Q1 results above ests)

CSX: Announces Medical Leave of CEO E. Hunter Harrison; Names COO James Foote as acting CEO

NPD: US Nov Total Video Game Sales $2.69B, +30% y/y

(US) Senator Rubio said to vote no on tax bill unless working poor tax credit is expanded - Washington Post

(US) Speaker of House Ryan (R-WI) considering retiring from Congress after 2018 – Politico

Europe

(UK) UK PM May said expected to ‘back down’ on Brexit date plan – UK Press

(UK) Germany Chancellor Merkel: EU leaders could move to Brexit Phase 2 on Friday

(ES) Survey shows Catalan separatists have lost their lead ahead of new elections - Spain press

(FR) Bank of France: Sees 2017 GDP +1.8% (v prior forecast 1.3%), sees 2018 GDP +1.7% (v prior forecast 1.5%)

(EU) ECB's Vasiliauskas (Lithuania): Does not see need for additional QE in 2018; measures implemented are showing results

(RU) EU's Tusk: The EU is united on the rollover of continuing economic sanctions on Russia

Levels as of 01:00ET

- Hang Seng -0.8%; Shanghai Composite -0.6%%; Kospi +0.5%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.2%; FTSE100 flat

EUR 1.1765-1.1791 ; JPY 112.12-112.41; AUD 0.7655-0.7675 ;NZD 0.6979-0.7023

Dec Gold flat at $1,256/oz; Jan Crude Oil +0.3% at $57.20/brl; Dec Copper +0.2% at $3.079/lb

Aussie Dollar Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.37% against the USD and closed at 0.766.

LME Copper prices rose 0.6% or $38.0/MT to $6723.0/MT. Aluminium prices rose 1.0% or $20.0/MT to $2017.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7668, with the AUD trading 0.1% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7653, and a fall through could take it to the next support level of 0.7637. The pair is expected to find its first resistance at 0.7682, and a rise through could take it to the next resistance level of 0.7695.

Next week, investors would keep a close watch on the Reserve Bank of Australia’s (RBA) December monetary policy meeting.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.