Sample Category Title

ECB Kept Interest Rates At Record Low, Lifted Euro-Zone’s Growth Forecasts

For the 24 hours to 23:00 GMT, the EUR declined 0.47% against the USD and closed at 1.1767, after the European Central Bank (ECB) boosted the Euro-zone's 2018 economic growth and inflation forecasts, but stuck with its pledge to maintain its ultra-loose monetary policy as long as needed.

The ECB, as widely expected, maintained the key interest rate unchanged at 0.00% at its recent monetary policy meeting, and signalled that it would keep its aggressive monetary stimulus in place despite strong economic recovery in the Euro-bloc, in order to “sustain inflation” towards the ECB's target. Further, the central bank boosted the Euro-zone's growth forecast to 2.4% for 2017, up 0.2% and to 2.3% for 2018, from 1.8% predicted earlier. Inflation is expected to rise 1.4% next year, revised up from 1.2% estimated in September.

Macroeconomic data revealed that the flash Markit manufacturing PMI in the common currency region unexpectedly climbed to a record high level of 60.6 in December, confounding market expectations for a drop to a level of 59.7, thus highlighting that an upturn in the manufacturing sector continued to surge forward. The PMI had recorded a reading of 60.1 in the prior month. Moreover, the region's preliminary Markit services PMI unexpectedly rose to a level of 56.5 in December, notching its highest level in 80 months. Markets were expecting the PMI to ease to a level of 56.0, after recording a reading of 56.2 in the prior month.

Separately, growth in Germany's manufacturing sector surprisingly advanced to an all-time high level of 63.3 in December, against market expectations for a fall to a level of 62.0. In the prior month, the PMI had registered a reading of 62.5. Furthermore, the nation's services sector expanded at its fastest pace in 24 months, after it jumped to a level of 55.8 in December, beating market expectations for an advance to a level of 54.6. The PMI had registered a level of 54.3 in the prior month.

The greenback declined against its major peers, as upbeat US manufacturing sector data was offset by poor report on the services sector.

The flash Markit services PMI in the US registered an unexpected drop to a level of 52.4 in December, hitting its lowest level in over a year. In the previous month, the PMI had registered a level of 54.5, while investors had envisaged for an increase to a level of 54.7. On the other hand, the nation's preliminary Markit manufacturing PMI surprised to the upside, jumping to an 11-month high level of 55.0 in December, after recording a level of 53.9 in the prior month and defying market consensus for the index to record a steady reading.

Another set of data revealed that advance retail sales in the US grew 0.8% MoM in November, topping market expectations for a gain of 0.3%. Retail sales had risen by a revised 0.5% in the previous month. Also, the number of American filing for fresh jobless claims unexpectedly eased to a level of 225.0K in the week ended 09 December, declining to its lowest level since mid-October. Market participants had anticipated the initial jobless claims to remain steady at a reading of 236.0K recorded in the prior week.

In the Asian session, at GMT0400, the pair is trading at 1.1781, with the EUR trading 0.12% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1743, and a fall through could take it to the next support level of 1.1705. The pair is expected to find its first resistance at 1.1841, and a rise through could take it to the next resistance level of 1.1901.

Looking ahead, traders would focus on the Euro-zone's trade balance numbers for October, due to release in a few hours. Additionally, the US industrial and manufacturing production data for November, due to release later in the day, will garner a lot of market attention.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

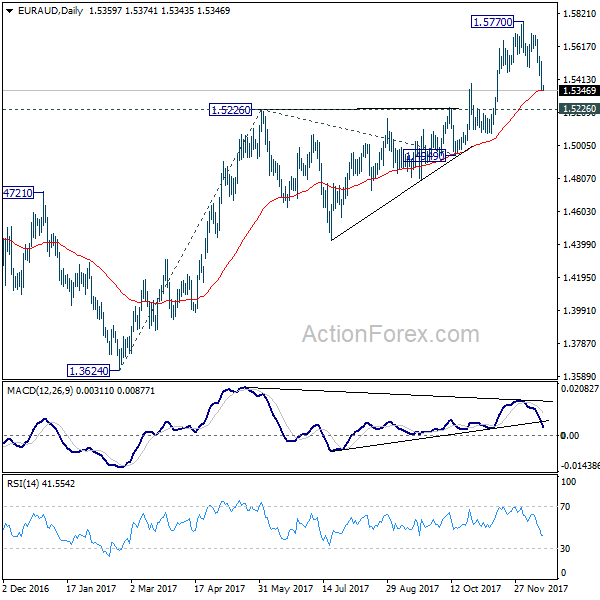

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5298; (P) 1.5409; (R1) 1.5473; More....

EUR/AUD drops further to as low as 1.5343 as correction from 1.5770 extends. At this point, we'd still expect downside to be contained above 1.5226 key support to bring rally resumption. Above 1.5482 minor resistance will turn bias to the upside for 1.5770. Break there will resume the medium term rise and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, sustained break of 1.5226 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

BoE Held Interest Rate Steady At 0.50%, Stuck To Its Outlook For Modest Tightening

For the 24 hours to 23:00 GMT, the GBP rose 0.09% against the USD and closed at 1.3424, following better-than-expected retail sales data in the UK.

However, gains in the Pound were limited, after the Bank of England (BoE), at its latest monetary policy meeting, vowed that interest rates were likely to rise only gradually.

The BoE unanimously voted to keep its benchmark interest rate steady at 0.50% and its asset purchase facility at £435.0 billion, as widely expected. In the minutes accompanying the decision, policymakers stated that growth in the fourth quarter of this year “might be slightly softer” than in the previous quarter, while judging that inflation is likely to be close to its peak and will decline towards the 2.0% target in the medium term. The central bank also held the view that “further modest increases” in interest rates would be warranted over the next few years to help bring inflation to its target of 2.0%. On Brexit negotiations, the central bank stated that the latest developments reduce the chance of a disorderly exit from the EU.

On the macro front, Britain’s retail sales climbed more-than-expected by 1.1% on a monthly basis in November, allaying concerns of a slowdown in consumer spending. Retail sales had posted a revised gain of 0.5% in the prior month, while markets were expecting for an increase of 0.4%.

In the Asian session, at GMT0400, the pair is trading at 1.3433, with the GBP trading 0.07% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3395, and a fall through could take it to the next support level of 1.3358. The pair is expected to find its first resistance at 1.3468, and a rise through could take it to the next resistance level of 1.3504.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japan’s Tankan Big Manufacturers’ Mood Improved To An 11-Year High Level In The Fourth Quarter Of 2017

For the 24 hours to 23:00 GMT, the USD declined 0.28% against the JPY and closed at 112.38.

In the Asian session, at GMT0400, the pair is trading at 112.27, with the USD trading 0.1% lower against the JPY from yesterday's close.

Overnight data revealed that Japan's Tankan large manufacturing index rose more-than-expected to a level of 25.0 in 4Q 2017, surging to an 11-year high level. Market participants had anticipated for a rise to a level of 24.0, compared to a reading of 22.0 in the preceding month. Meanwhile, the nation's Tankan non-manufacturing index remained steady at a level of 23.0 in 4Q 2017, while investors had envisaged for an increase to a level of 24.0.

Moreover, the nation's Tankan large manufacturing outlook index unexpectedly remained steady at 19.0 in 4Q 2017, while the non-manufacturing outlook index climbed less-than-anticipated to a level of 20.0 in 4Q 2017, after recording a reading of 19.0 in the previous month.

The pair is expected to find support at 111.93, and a fall through could take it to the next support level of 111.60. The pair is expected to find its first resistance at 112.74, and a rise through could take it to the next resistance level of 113.22.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

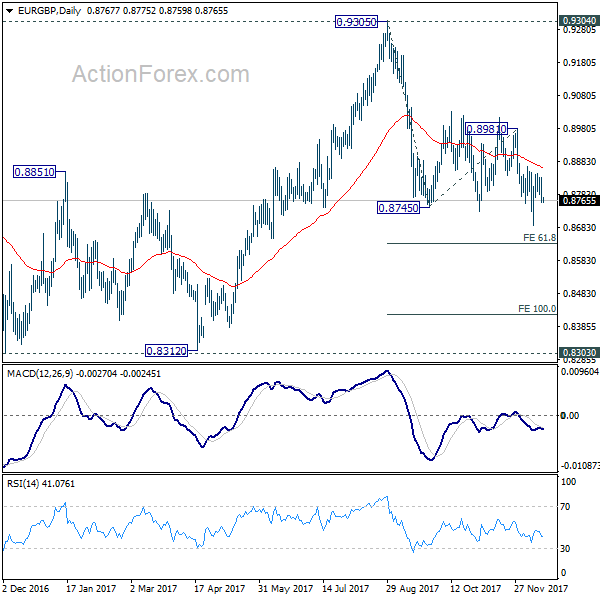

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8740; (P) 0.8787; (R1) 0.8813; More...

Intraday bias in EUR/GBP stays neutral at this point. With 0.8866 resistance intact, near term outlook remains mildly bearish and deeper fall is expected. Break of 0.8688 will extend the fall from 0.9305 and target 61.8% projection of 0.9305 to 0.8745 from 0.8981 at 0.8468 first and then 100% projection at 0.8151 next. However, break of 0.8866 resistance will indicate near term reversal and turn bias back to the upside for 0.8981 resistance instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

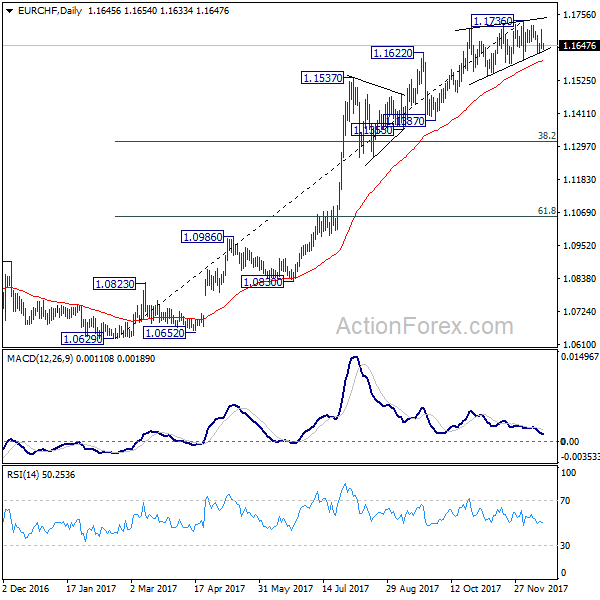

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1619; (P) 1.1662; (R1) 1.1687; More...

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. It's close to topping, if not formed. This is supported by persistent bearish divergence condition in 4 hour MACD, and rising wedge like structure. On the downside, break of 1.1597 support will will be a strong sign of trend reversal and should turn outlook bearish for 38.2% retracement of 1.0629 to 1.1736 at 1.1313.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

SNB Left Interest Rate On Hold At -0.75%, Lifted Its Inflation Forecast

.

For the 24 hours to 23:00 GMT, the USD rose 0.34% against the CHF and closed at 0.9896.

Yesterday, the Swiss National Bank (SNB) retained the benchmark interest rate at -0.75% and projected that inflation in Switzerland would exceed its target in three years. However, the central bank reiterated its commitment to “intervene in the foreign exchange market as necessary”. The central bank upgraded its inflation forecast to 0.5% for 2017, up from 0.4% predicted earlier and to 0.7% for next year, from 0.4%. The central bank also predicted the Swiss economy to expand around 2.0% in 2018, after advancing by 1.0% in 2017.

In the Asian session, at GMT0400, the pair is trading at 0.9885, with the USD trading 0.11% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9848, and a fall through could take it to the next support level of 0.9812. The pair is expected to find its first resistance at 0.9913, and a rise through could take it to the next resistance level of 0.9942.

Moving ahead, market participants would eye Switzerland’s trade balance and the KOF leading indicator, both due to release next week.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Canada’s New Housing Price Index Climbed In October

For the 24 hours to 23:00 GMT, the USD declined 0.14% against the CAD and closed at 1.2803.

On the data front, Canada's new housing price index advanced 0.1% MoM in October, compared to a rise of 0.2% in the prior month, while markets had anticipated for a gain of 0.2%.

In the Asian session, at GMT0400, the pair is trading at 1.2780, with the USD trading 0.18% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2707, and a fall through could take it to the next support level of 1.2635. The pair is expected to find its first resistance at 1.2859, and a rise through could take it to the next resistance level of 1.2939.

Ahead in the day, Canada's existing home sales data for November, will be on investor's radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

ECB: Confident About Economy, But Cautious About Policy

- Draghi more upbeat on growth, but policy outlook unchanged

- Markets unmoved by expected commitment to continuing easy policy

- ECB makes substantial upward revisions to growth outlook…

- …But inflation to remain subdued

- Clear message that easy policy will continue but can it last throughout 2018?

There was little or no excitement expected by markets from the ECB's governing council meeting and the ECB lived down to these expectations. ECB president Mario Draghi's press conference and new ECB economic projections both spelled out the same two related messages. The ECB is pleasantly surprised by the strength of the recovery in activity in the Euro area and it is determined to avoid any unpleasant surprises in financial markets that might threaten that recovery any time soon.

As a result, the strong signal from the ECB was that any adjustment in its monetary policy is still a long way away even if Mr Draghi seemed to create a very small element of wriggle room in this regard. Indeed, on several occasions during the press conference Mr Draghi sought to underline policy continuity by indicating that there had been no discussion of future policy options. A slight easing in the exchange rate of the Euro and unchanged market interest rates in the immediate aftermath of the ECB's pronouncements suggested that the message of no change now or any time soon was received and understood by markets.

While acknowledging the current momentum in the Euro area economy, Mr Draghi avoided any worrisome implications for ECB policy by emphasising the lack of any notable follow through from stronger growth to higher inflation. The new ECB projections which show growth remaining well above potential but inflation remaining below target out to 2020 provide further re-assurance of a decoupling of growth and inflation that could allow 'An ample degree of monetary stimulus ' remain in place for some considerable time.

New ECB projections entail material upward revisions to the outlook for economic growth for each year from 2017 to 2019 (2.4% v2.2%, 2.3% v 1.8% and 1.9% v 1.7%). Although growth moderates to 1.7% in the ECB's initial projection for 2020, this remains well above most estimates of the Euro area's potential growth rate.

As the graph illustrates, the new ECB staff projections envisage the four year period between 2017 and 2020 delivering the strongest sustained period of growth in activity and employment since the mid 2000's. However, unlike that period which saw inflation persistently above 2%, the new ECB projections see only a modest pick-up in consumer prices that means inflation remains below the ECB's target rate out to 2020 (when questioned, Mr Draghi carefully avoided repeating last December's assertion that an inflation outturn of 1.7% is 'not really' in line with the ECB's target).

Indeed, ECB projections imply that, although increases in GDP are set to remain well above the Euro area's potential growth rate and the output gap is now moving into positive territory, current policy settings can deliver a notable break from history by helping growth and inflation to remain on smooth glide paths towards desired outcomes.

It may be that global economic slack and reforms in some parts of the Euro area will mean that, as in the US, inflation falls substantially short of the trend in activity but this would mark a dramatic change in the performance of the Euro area economy.

We would note one small pointer that hints albeit slightly towards an inflation trend that might warrant a somewhat less accommodative future monetary policy stance. The initial headline inflation forecast of 1.7% for 2020 is restrained marginally by oil prices and underlying inflation at 1.8% is probably broadly in line with the stated ECB target of a rate 'below, but close to, 2%'.

We would also highlight that Mr Draghi was careful to avoid suggesting that reaching any particular inflation rate would trigger consideration of policy tightening. Instead, he repeatedly said that what matters in terms of policy is evidence of a pick-up in inflation that is 'sustainable and self- sustaining'. He also said that it remains 'quite early' both in terms of the measures the ECB announced in October and, more generally, in terms of current activity and inflation developments to even begin to contemplate future policy measures.

While we think that a clear pick-up in inflation accompanied by signs of faster increases in wages may prompt notably different messaging from the ECB, that is not an issue for today. A more relevant near term policy signal is the continuing reference today to 'domestic price pressures (that) remain muted overall and have yet to show convincing signs of a sustained upward trend. An ample degree of monetary stimulus therefore remains necessary for underlying inflation pressures to continue to build up and support headline inflation developments over the medium term.'

Mr Draghi did note that the Governing council is now more confident than it was six weeks ago that in time improving economic conditions will translate into higher inflation.

But again he sought to distance the point between stronger growth and any inflation outcome that might require tighter policy. For now, he suggested healthier growth meant that the risk of deflation had disappeared and the possibility of very low inflation had become much more remote. The clear message is that growth and inflation have some way to go before they trigger any significant policy discussion. To further emphasise this point, he noted that a strong majority on the Governing council favour keeping the Asset Purchase Programme open-ended rather than preannouncing a specific end date.

Our sense is that while there is a strong consensus around the ECB's governing council table on the outlook for Euro area activity, views on the likely consequences for inflation may be more diverse and judgements as to the implications for policy may be becoming more fractured. There is little doubt that dovish thinking remains dominant at least for now. However, the persistence of above trend growth and even tentative signs of emerging price pressures could tilt the balance notably as 2018 progresses.

For now, the ECB's current message and the near term policy outlook are crystal clear. The key question is whether markets are pricing in at least the possibility of a more forceful change in ECB policy even if that possibility remains a year or more away.

USD/JPY Signaling Bearish Continuation Below 112.30

Key Highlights

- The US Dollar faced bearish pressure after the fed rate decision and declined below 113.00 against the Japanese Yen.

- USD/JPY also broke a crucial support area near 112.30 and a bullish trend line on the 4-hours chart.

- Japan's Tankan Large Manufacturing Index in Q4 2017 posted an increase from 22 to 25.

- Today's Industrial production report in the US could be important since the production is forecasted to increase by 0.3% (MoM).

USDJPY Technical Analysis

After a steady rise, the US Dollar faced offers near 113.75 against the Japanese Yen. The USD/JPY pair declined and moved below the 113.00 support area to break 112.50.

The fed interest rate decision and yesterday's CPI release were the main drivers of the recent downside move from 113.75. At the outset, the 4-hours chart of USD/JPY suggests that the recent break below the 112.30-40 support area holds a lot of importance.

There was a bullish trend line positioned at 112.50 on the same chart. More importantly, the 100 simple moving average (red, 4-hour) was at 112.30. Sellers also succeeded in pushing the pair below the 50% fib retracement level of the last wave from the 110.84 low to 113.75 high.

Therefore, a close below the 112.30 support means there could be more declines in USD/JPY toward 112.00 and 111.60. An intermediate support on the downside is around the 61.8% fib retracement level of the last wave from the 110.84 low to 113.75 high.

On the upside, the broken support at 112.30 and 112.50 are likely to act as a resistance. However, the most important resistance on the upside is around the 200 simple moving average (green, 4-hou) at 112.85.

Looking at the 4-hour RSI for USD/JPY, there is a declining pattern below the neutral level. Therefore, buyers will most likely struggle to retain bullish traction in the near term.

The current market sentiment is mixed for the US dollar since EUR/USD failed to remain above the 1.1820 level. On the other hand, GBP/USD was able to settle above the 1.3400 support. Therefore, it would be interesting to see how this week ends for the greenback and especially USD/JPY.