Sample Category Title

Bitcoin Tests $18,000 Again

Bitcoin price keeps on rising as market's interest for futures vanishes

Many market participants expected that the introduction of Bitcoin futures trading would trigger a sharp correction, as it would be finally possible to take short positions. In fact, the opposite happened, the price soared more than 20% and returned above the $17,000 threshold. Over the last 24 hours, the price has been moving sideways between $16,200 and $17,500.

When we look at the numbers, the market's interest for Bitcoin futures seems to be quite limited. The trading activity was quite limited at market opening on Monday. During the first hours, the average hourly volume was around 300 Bitcoin but it quickly declined as the future's price exploded, climbing as high as $18,850. After that, trading activity declined continuously with around 50 contracts traded hourly.

The figures suggest that investors are not keen to go short Bitcoin, which suggests that further gains are expected. Bitcoin is currently going through a period of accumulation at around $16,000-$17,000. Regarding the price outlook, we remain bullish Bitcoin and expect that the price will pick-up soon as money continue to flow into crypto-assets. It is reasonable to target the $20,000 level by year-end.

Japan: weak inflation to weigh on the yen

The USDJPY has been increasing since the last week of November and is now monitoring stronger levels below 114 yen for one single dollar note. The yen is getting weaker but remains way too strong for the Bank of Japan to start normalizing its monetary policy. The central bank is in all-in mode and the effect on the yen is still mixed. One very important thing needs to be said. It is that the day when the BoJ will even hint at a possible normalization of the monetary policy, the yen will likely spike disrupting all the strategy from the Japanese Central Bank.

We then believe that, the BoJ will remain in a “dovish mode” until inflation will have killed part of its debt. This can take years even decades. Hence, the BoJ is condemned to follow the path of the Fed or the ECB. Inflation is what BoJ officials are running for. Shinzo Habe recently declared that wages increase of 3% in order to boost consumer prices which in the end will have a positive impact on the debt. BoJ knows that inflation is now mandatory to kill the massive debt. It is still a long way to go. And the BoJ knows looks towards the US hoping for several Fed rate hike next years.

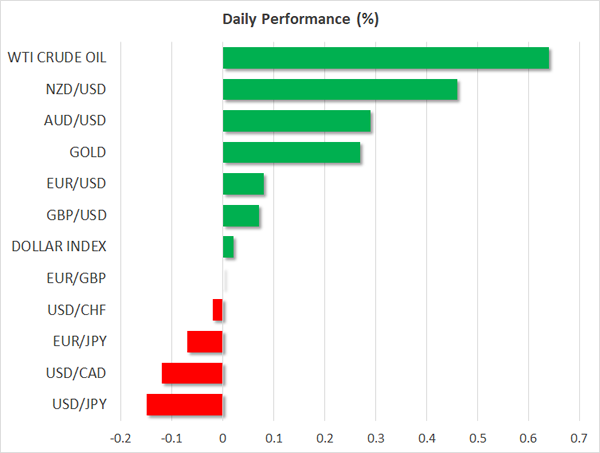

Dollar Steady Ahead Of UK And US Data, Kiwi Continues Rising

Here are the latest developments in global markets:

FOREX: The dollar was little changed against a basket of currencies ahead of a two-day meeting by the Federal Reserve that is to commence later in the day. The New Zealand dollar maintained positive momentum from yesterday, rising to its highest in a month relative to the greenback.

STOCKS: The Nikkei 225 finished 0.3% lower, but still remained close to its highest since early 1992; the Hang Seng was last 0.6% down following yesterday’s strong advance. Euro Stoxx 50 futures were 0.2% up at 0728 GMT. Dow, S&P 500 and Nasdaq 100 futures were not much changed.

COMMODITIES: Oil was edging higher as one of the most important pipelines in the world was closed and ahead of an API report on US crude stocks due later in the day (2130 GMT). WTI was 0.6% up at $58.36 a barrel and Brent traded 0.9% higher at $65.30. The latter also recorded a 2-1/2-year high earlier in the day while WTI was trading relatively close to similar high levels. Gold was 0.3% up, eyeing $1245 per ounce. The precious metal yesterday touched $1240.10, its lowest since late July.

Major movers: Dollar not much changed ahead of widely anticipated rate hike; kiwi continues gaining

The dollar index was marginally higher, trading close to the 94 level, as well as around its highest in three weeks recorded on Friday. The Fed meeting that is to be completed tomorrow is widely expected to result in a quarter percentage point increase in the fed funds rate. Dollar/yen was down, though not by much, trading not far below 113.50 and its highest since mid-November.

Euro/dollar and pound/dollar were both up by 0.1%, below the 1.18 handle and around 1.3350 respectively. The European Central Bank and the Bank of England will be holding policy meetings later this weeks as well (Thursday) with no change in their respective policies expected. Starting today with the release of November inflation figures, the UK will see the release of important data throughout the week.

The kiwi rallied yesterday, finishing the day 1.05% relative to the US dollar. Adrian Orr’s appointment to lead the Reserve Bank of New Zealand starting March continued to fuel long kiwi/dollar positions, pushing the pair to its highest since November 10. The pair was last trading 0.5% up, around 0.6940. Aussie/dollar rose in sympathy despite data on business confidence and home prices coming in weaker than forecasts. The pair last stood 0.3% higher at 0.7545.

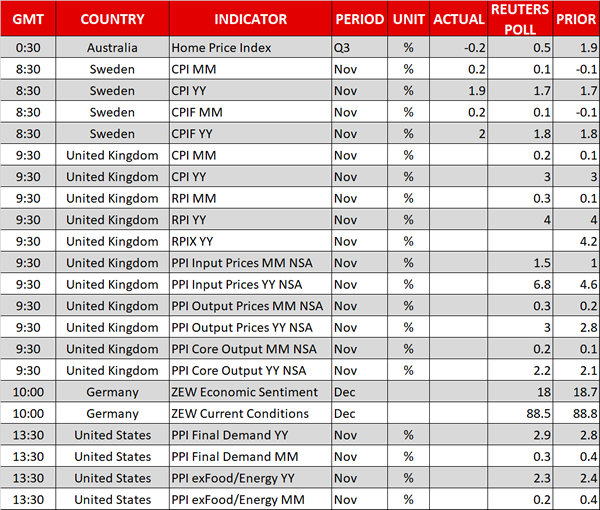

Day ahead: US & UK deliver PPI & CPI data; Fed policy meeting begins

At 0930 GMT the British Office for National Statistics will deliver data on consumer prices. Forecasts are for the headline CPI – the measure the BoE’s target of 2% is compared to – to stand flat at a more than five-year high of 3.0% y/y in November. The BoE governor, Mark Carney, recently stressed that further rate hikes might be needed the next few years to bring inflation back to the central bank’s target. It should be noted that if the indicator breaks above expectations, then Carney would have to write a letter to the Chancellor of the Exchequer Philip Hammond explaining the reasons behind the outcome. Month-on-month, CPI is expected to rise by 0.2%. Other inflationary measures, including producer and retail prices are expected to rise on a yearly basis in November.

Next, at 1000 GMT the ZEW institute will publish November’s readings on German economic sentiment, with analysts projecting the outlook for the next six months to deteriorate, driving the index down by 0.7 points to 18.0. However, this would still be among the highest readings recorded in two-years.

In the US, PPI figures for the month of November are expected to inch up by 0.1 percentage points to 2.9% y/y, picking up to a fresh two-year high, whereas the monthly PPI stats are anticipated to reflect a slowdown in the pace of growth, standing at 0.3% m/m growth.

Regarding central bank meetings, the FOMC members will gather to decide on interest rates later today, with the decision expected to be announced on Wednesday at 1900 GMT. Despite a third-rate hike being priced in by the markets, investors will scrutinize the monetary policy statement following the rate announcement and will keep a close eye on the Fed chair Janet Yellen’s news conference at 1930 GMT for clues on the path of future rate hikes.

In energy markets, the American Petroleum Institute will report inventory levels on US crude oil, gasoline and distillate stocks for the week ending December 8 at 2130 GMT.

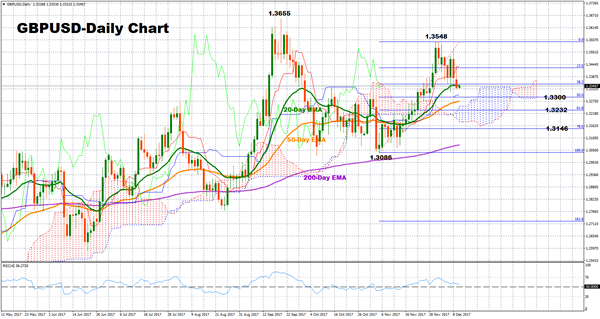

Technical Analysis: GBPUSD falls below two-month highs levels, looking neutral in short-term

GBPUSD retreated from two-month high levels last week. The market has not fully reversed the recent upleg from 1.3026 to 1.3548. The technical indicators suggest that the pair might enter a consolidation phase in the short-term given that the RSI is currently moving sideways above 50.

Today’s inflation data though, could shake the currency. Better than expected CPI readings could push the market back to the two-month high of 1.3548, while steeper increases would also target the 1-½ -year peak of 1.3655.

However, worse-than-anticipated figures could send the pair to re-test the 50% Fibonacci at 1.3300 of the upleg from 1.3086 to 1.3548, which recently acted as a strong resistance. Further down, additional support levels could be found at 1.3232 (61.8%) and at the swing-low of 1.3086.

WTI Oil Futures In Bullish Short-Term Phase After Strong Rebound From 57 Area

WTI oil futures are in a bullish phase and flowing back to the upside, having recouped almost all of the losses made from the decline of the early December high at 58.86 to the December 7 low of 55.79.

A clear break and daily close above 58.40 would open the way for a re-test of the more than two-year high of 59.02. The near-term bias is clearly on the upside and on the 4-hour chart, the market has crossed above the 20 and 50-period moving averages. However, while the RSI is in bullish territory, it is approaching overbought levels at 70. This suggests there could be some consolidation in prices or even a pullback.

The market is currently testing the 58.40 level. Failure to make a sustained move above it soon would lead to a loss in upside momentum and increase the odds of a reversal back to the downside. The key 57 level would be the next major support level, which has held firm in the past few days, despite several tests made. A break below 57 would bring about more bearish momentum to target 56.55 and then the low at 55.79.

In the bigger picture, WTI oil futures have been neutral since peaking at 59.02 on November 24. The medium-term neutral outlook is expected to remain in place with more sideways trading in a broad range between the 56-58 handles.

Technical Outlook: US CRUDE OIL – Bulls Eye Key Barrier At $59.02

Recovery rally off $55.81 trough extends into fourth straight day and broke above target at $58.14 (Fibo 76.4% of $58.86/$55.81) on Tuesday.

Bulls were boosted by North Sea pipeline shutdown and look for test of $58.63 resistance (bear-trendline connecting $59.02 / $58.86 tops) which marks the last obstacle en-route to key barriers at $58.86 (01 Dec) and $59.02 (24 Nov peak, the highest since late June 2015).

Bullish daily techs are supportive, however, oil price may show stronger hesitation before firm break above $59.02 pivot.

Corrective dips are expected to stay above daily Tenkan-sen ($57.34) to keep bullish structure intact.

Res: 58.63, 59.86, 59.02, 60.00

Sup: 58.14, 57.90, 57.34, 56.91

Technical Outlook: BRENT Rallies To New Over 2-Yr High

Brent oil surged to fresh high at $65.68 per barrel on Tuesday, extending rally from $61.15 higher base into four straight day and hitting the highest levels since mid-June 2015.

Brent price received additional support from reduced supply on shutdown of North Sea pipeline, which added on effects from major oil producers' output cut.

Bullish acceleration from $61.15 which formed a higher base and double-bottom on daily chart could extend towards psychological $70.00 barrier and key $70.31 resistance (06 May 2015 high). Meanwhile, bulls may take a breather as overbought slow stochastic on daily chart signals corrective easing.

Former recovery top at $64.63 (08 Nov high) marks initial support, ahead of $64.00 zone and extended dips to find ground above converged 10/20SMA's at $63.00 zone.

Res: 65.68, 66.27, 66.73, 67.48

Sup: 65.00, 64.63, 64.00, 63.00

Market Update – European Session: UK CPI Near 6-Year Highs, Oil And Natural Gas Move Higher In Session

Notes/Observations

European inflation data higher then expected (both UK and Sweden beat consensus)

UK Nov CPI hits highest level since March 2012; BOE Gov Carney to deliver inflation letter in Feb

Asia:

US , EU and Japan plan to step up trade pressure on China to address "severe excess capacity"

CNY currency (Yuan) might fluctuate between 6.4-6.8 in 2018 and had the potential appreciation in long term

Europe:

UK Trade Sec Fox: Would like a trading relationship with the European Union after it leaves the bloc that's "virtually identical" to the one it has now (**Note: EU's Barnier's warned that a Canada-style free-trade agreement was the best the U.K. can hope for)

Economic Data:

(FR) France Q3 Final Private Sector Payrolls Q/Q: 0.3% v 0.2% prelim; Total Payrolls: 0.2% v 0.3% prelim

(RO) Romania Nov CPI M/M: 0.7% v 0.6%e; Y/Y: 3.2% v 3.1%e

(SE) Sweden Nov CPI M/M: 0.2% v 0.1%e; Y/Y: 1.9% v 1.7%e

(SE) Sweden CPI CPIF M/M: 0.2% v 0.1%e; Y/Y: 2.0% v 1.8%e

(UK) Nov CPI M/M: 0.3% v 0.2%e; Y/Y: 3.1% v 3.0%e; CPI Core Y/Y: 2.7% v 2.7%e; CPIH Y/Y: 2.8% v 2.9%e

(UK) Nov RPI M/M: 0.2% v 0.3%e; Y/Y: 3.9% v 4.0%e, RPI-X (ex-mortgage interest payment) Y/Y: 4.0% v 4.1%e, Retail Price Index: 275.8 v 276.1e

(UK) Nov PPI Input M/M: 1.8% v 1.5%e; Y/Y: 7.3% v 6.7%e

(UK) Nov PPI Output M/M: 0.3% v 0.3%e; Y/Y: 3.0% v 3.0%e

(UK) Nov PPI Output Core M/M: 0.2% v 0.2%e; Y/Y: 2.2% v 2.2%e

(UK) Nov ONS House Price Index Y/Y: 4.5% v 5.2%e

(ZA) South Africa Q3 Non-Farm Payrolls Q/Q: -0.3% v -0.3% prior; Y/Y: -0.9% v 0.2% prior

(DE) Germany Dec ZEW Current Situation Survey: 89.3 v 88.7e; Expectations Survey: 17.4 v 18.0e

(EU) Euro Zone Dec ZEW Expectations Survey: 29.0 v 30.9 prior

Fixed Income Issuance:

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2032, 2040, 2044 and 2048 bonds

(ES) Spain Debt Agency (Tesoro) sold total €2.89B vs. €2.5-3,.5B indicated range in 3-month and 6-month Bills

(IT) Italy Debt Agency (Tesoro) sold €4.75B vs. €4.75B indicated in 12-month Bills; Avg yield: -0.407% v -0.395% prior; Bid-to-cover: 2.1x v 2.46x prior

(CH) Switzerland sold CHF559.2 in 3-month Bills; Avg Yield: -1.101% v -1.046% prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 0.2% at at 389.6, FTSE +0.2% at 7468, DAX +0.1% at 13141, CAC-40 +0.2% at 5399, IBEX-35 -0.2% at 10288, FTSE MIB flat at 22698, SMI -0.1% at 9305 , S&P 500 Futures flat]

Market Focal Points/Key Themes: European Indices trade mostly higher reversing earlier losses in relatively quiet trade. The FTSE outperforms once again on relative weakness in Cable despite a slightly stronger headline UK CPI figure. M&A activity denominated the news this morning with Unibail-Rodamco's mega acquisition of Westfield Group in Australia for $25B; Atos is to acquire Gemalto in a €4.3B deal, whilst Zurich Insurance acquired ANZ Australian life insurance business. Elsewhere Robert Walters trades sharply higher after lifting its outlook, and Carpetright trades sharply lower after a drop in profits.

Equities

Consumer Discretionary [Carpetright [CPR.UK] -8% (Earnings), Steinhoff [SNH.ZA] +32% (Looks to divest stakes in PSG and KAP), Ashtead [AHT.UK] +3% (Earnings), Robert Walters [RWA.UK] +10% (Raises outlook)]

Real Estate [Unibail-Rodamco [UL.FR] -2% (To acquires Westfield Group)]

Technology [Gemalto [GTO.NL] +32%, Atos [ATO.FR] +4.7% (Gemalto to be acquired by Atos for €46/shr)]

Financials [Unicredit [UCG.IT] +6% (Investor day)]

Materials [Glencore [GLEN.UK] -1.2% (Guidance, Investor day)]

Speakers

Germany Economic Ministry: 2017 GDP growth to show strong overall result. Domestic economy was on an upward trend at end of year

EU said to have hardened the language of a proposed Brexit resolution for this week's European Council summit

EU Chief Brexit Negotiator Barnier reiterated that EU will fully support Ireland throughout the Brexit talks

BOE: Gov Carney inflation letter to be published alongside the Feb CPI data (**Note: Inflation Letter comes out if Headline CPI is above 3%)

German ZEW Economists: Unclear outcome of govt formation did not influence expectations significantly

Turkey President Erdogan reiterated his view that inflation could not fall due to high interest rates. Pressures for rate hike were vain efforts

Brazil Central Bank Dec Minutes: Inflation at comfortable level but threatened by frustration of expectations over reforms

Currencies

Overall FX price action was muted ahead of the plethora of rate decision over the next 48 hours.

GBP/USD was softer just ahead of the NY morning despite the slightly higher Nov CPI data ahead of Thursday BOE rate decision.

SEK currency (Krona) was firmer after Sweden Nov CPI beat expectations and hovered near the Riksbank target.

Fixed Income

Bund futures trade 163.36 down 16 ticks, easing back marginally. Continued upside sees 163.63 then 164.25. A reversal targets 162.50 then 162.38.

Gilt futures trade at 125.71 down 17 ticks after stronger than expected UK inflation data. Continued upside eyeing 126.15 then 126.65. Downside targets include 125.24 then 124.75.

Wednesday's liquidity report showed Tuesday's use of the marginal lending facility rose to €283M from €135M prior.

Corporate issuance saw 3 issuers raise $2.8B in the primary market

Looking Ahead

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (CL) Chile Central Bank Economist Survey

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (BE) Belgium Debt Agency (BDA) to sell €2.1B in 3-Month and 12-Month Bills

05:30 (DE) Germany to sell €3.0B in 2019 Schaltz

06:00 (BR) Brazil CONAB Crop Report

06:00 (US) Nov NFIB Small Business Optimism: 104.0e v 103.8 prior

06:00 (IE) Ireland Oct Property Prices M/M: No est v 2.0% prior; Y/Y: No est v 12.8% prior

06:00 (ZA) South Africa Oct Manufacturing Production M/M: +1.0%e v -0.8% prior; Y/Y: +1.1%e v -1.6% prior

06:00 (TR) Turkey to sell 2019 and 2022 bonds - 06:45 (US) Daily Libor Fixing

07:00 (RU) Russia announces weekly OFZ bond auction .

07:00 (IN) India Nov CPI Y/Y: 4.3%e v 3.6% prior

07:00 (IN) India Oct Industrial Production Y/Y: 2.9%e v 3.8% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (PL) Poland Nov CPI Core M/M: 0.1%e v 0.3% prior; Y/Y: 0.9%e v 0.8% prior

09:00 (RU) Russia Oct Trade Balance: $9.5Be v $10.2B prior; Exports: $31.4Be v $30.6B prior; Imports: $21.1Be v $20.4B prior

08:05 (UK) Baltic Dry Bulk Index - 08:30 (US) Nov PPI Final Demand M/M: 0.3%e v 0.4% prior; Y/Y: 2.9%e v 2.8% prior

08:30 (US) Nov PPI Ex Food and Energy M/M: 0.2%e v 0.4% prior; Y/Y: 2.4%e v 2.4% prior

08:30 (US) Nov PPI Ex Food, Energy, Trade M/M: 0.2%e v 0.2% prior; Y/Y: No est v 2.3% prior

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves

09:00 (MX) Mexico Oct Industrial Production M/M: +0.7%e v -0.4% prior; Y/Y: +0.8%e v -1.2% prior, Manufacturing Production Y/Y: 3.8%e v 2.8% prior

09:00 (BR) Brazil to sell I/L 2022, 2026, 2035 and 2055 Bonds

11:30 (US) Treasuries to sell 4-Week Bills

12:00 DOE Short-Term Crude Outlook

12:00 (US) USDA World Agricultural Supply and Demand Estimate (WASDE) Crop Report

13:00 (US) Treasuries to sell 30-Year Bonds Reopening

14:00 (AR) Argentina Nov National CPI M/M: 1.4%e v 1.5% prior

14:00 (US) Nov Monthly Budget Statement: -$134.5Be v -$63.2B prior

14:00 (EU)ECB's Draghi

16:30 (US) Weekly API Oil Inventories

US Futures Trading Higher Ahead Of Key Economic Data

Making record highs have been the norm for the US equity market

An important week in terms of key central bank announcements

No Interest rate hike expected from BOE

US future are trading higher and picking up the momentum where they left off yesterday. Making record highs have been the norm for the US equity market throughout this year, thanks to the energy and tech sectors which have provided most of the tail wind. Speaking of the energy sector, both Brent and Crude are at their 30 month high today and investor are keeping are keeping a close eye on the upcoming inventory data. The oil leakage situation at the Forties oil field in the North sea is also having some positive impact on the price.

This is an important week in terms of key central bank announcements and currency traders are going to learn about their stance. The Fed will start their two day meeting tomorrow and it is widely expected that the Fed will be raising the interest rate by twenty five basis points. The US dollar index is rallying on the back of this, however, a lot of the momentum in the dollar index is also mainly due to the strong labour economic data which came out on last Friday.

The Bank of England will also be in the spot light on Thursday when it will occupy the stage. Theresa May, the UK prime minister has been able to shift gears in terms of Brexit negotiations after having a successful agreement with EU partners. The bank of England in its last meeting announced an interest rate hike and most of the market participants are of the mind frame that the bank was under tremendous pressure to adopt such a measure. No one in the market is expecting that the bank will announce another interest hike for some long period of time. The bank’s governor was somewhat lucky from not writing a letter to Chancellor of the Exchequer after the inflation data printed relatively a better number than the forecast.

The focus now turn towards the key economic data and it is evidently clear that the UK’s economy has been lacklustre as compared to other major four European economies.

Technical Outlook: USDCHF – Pullback Extends Into Daily Cloud, 55SMA Expected To Contain Correction

The pair holds in red for the third consecutive day and extends pullback from last Friday's peak at 0.9977, where strong upside rejection occurred. Failure ahead of parity level triggered fresh easing, with today's extension lower returning below the top of thick daily cloud (0.9904), which marked initial and strong support. Pullback is approaching next pivotal support at 0.9884 (Fibo 38.2% of 0.9734/0.9977 upleg) which lies above layers of supports provided by daily MA's within 0.9874/0.9858 zone. South-heading slow stochastic which reversed from overbought territory on daily chart, shows more room at the downside, with corrective dips expected to find ground at 0.9874/58 area (10/20SMA bull-cross/55SMA/50% retracement of 0.9734/0.9977) to keep bullish structure on daily chart in play. Conversely, sustained break here would signal lower top formation (0.9977) and risk extension towards 200SMA (0.9792).

Res: 0.9922, 0.9977, 1.0000, 1.0038

Sup: 0.9887, 0.9874, 0.9858, 0.9827

Has Bitcoin Battered Gold?

Gold crumples again overnight as Bitcoin futures start trading, setting the scene for lower levels.

I suspect it is no coincidence that the day that Bitcoin futures officially started trading, gold prices dropped in an otherwise sideways overnight session in most markets. The Commitment of Traders Report showed a substantial drop in speculative long positioning which should be no surprise once 1260.00 broke as spoken about ad nauseam in this column. There has been much talk of a rotation out of gold and into bitcoin (but no concrete evidence), and where there is smoke, there is fire. Even if that fire ends up being the “rotating” money eventually being burnt to ash.

Gold fell from 1247.80 to close at 1242.00 overnight, rallying and failing at resistance along the way. This morning it has eked out a small rally to 1244.50 on physical buying and profit taking, but the price action remains unconvincing.

Gold has resistance at 1252.50 which held yesterday’s recovery attempt. It is followed by the break-out at 1260.00. Support is at the overnight low at 1240.70 with the charts again opening up a chasm to the 1205.00 regions after that.

Hairline Fracture Sends Oil Higher

A pipeline fracture in the North Sea will be bringing smiles to OPEC today, increasing their production by 25.0% for the near future with no effort on their part.

It isn't often that a hairline fracture is regarded as good news, but in the case of Brent Crude, it was. Brent Crude raced higher by 2.0% overnight as news broke that the North Sea's Forties Pipeline system would have to be shut down for a “number of weeks” after a hairline crack was found in it. The pipeline carries 450,000 bpd or 40.0% of the U.K. North Sea's production and is a significant component underpinning of the Brent benchmark.

Brent Crude raced from 63.55 to close at 64.95 having touched 65.10 during the session. It has since climbed another 1.50% to 66.05. Far more significantly, it has taken out three formidable resistance zones at 64.00, 64.45 and 64.85 which all now become support. Initial resistance was at the overnight high after which the charts have nothing but clear sky until 69.50/70.00 region. The pipeline's closure is effectively adding 450,000 bpd to OPEC/Non-OPEC's 1.80 million bpd cut and thus it's significance to the global supply/demand situation should not be underestimated.

WTI also benefited, not least because the U.K will be scrambling to find alternative supplies with 80 North Sea platforms to all intents out of action. WTI spot was dragged 1.20% higher to touch 58.00 before settling just below at 57.95. It has climbed 0.45% in Asia to 58.35. The 58.00 level was also significant as it is also trend-line resistance, with a break opening up a challenge of the 58.90 triple top, the last rampart standing in the way of a test of 60.00.